Flexible Paper Packaging Bags Market Size, Share & Trends Analysis Report by Product Type (Stand-up Pouches, Flat Pouches, Side Gusset Bags, and Others), Material Type, Closure Type, Capacity/Size, Printing Technology, Thickness, Distribution Channel, End-Use Industry, and Geography (North America, Europe, Asia Pacific, Middle East, Africa, and South America) – Global Industry Data, Trends, and Forecasts, 2025–2035

|

|

|

Segmental Data Insights |

|

|

Demand Trends |

|

|

Competitive Landscape |

|

|

Strategic Development |

|

|

Future Outlook & Opportunities |

|

Flexible Paper Packaging Bags Market Size, Share, and Growth

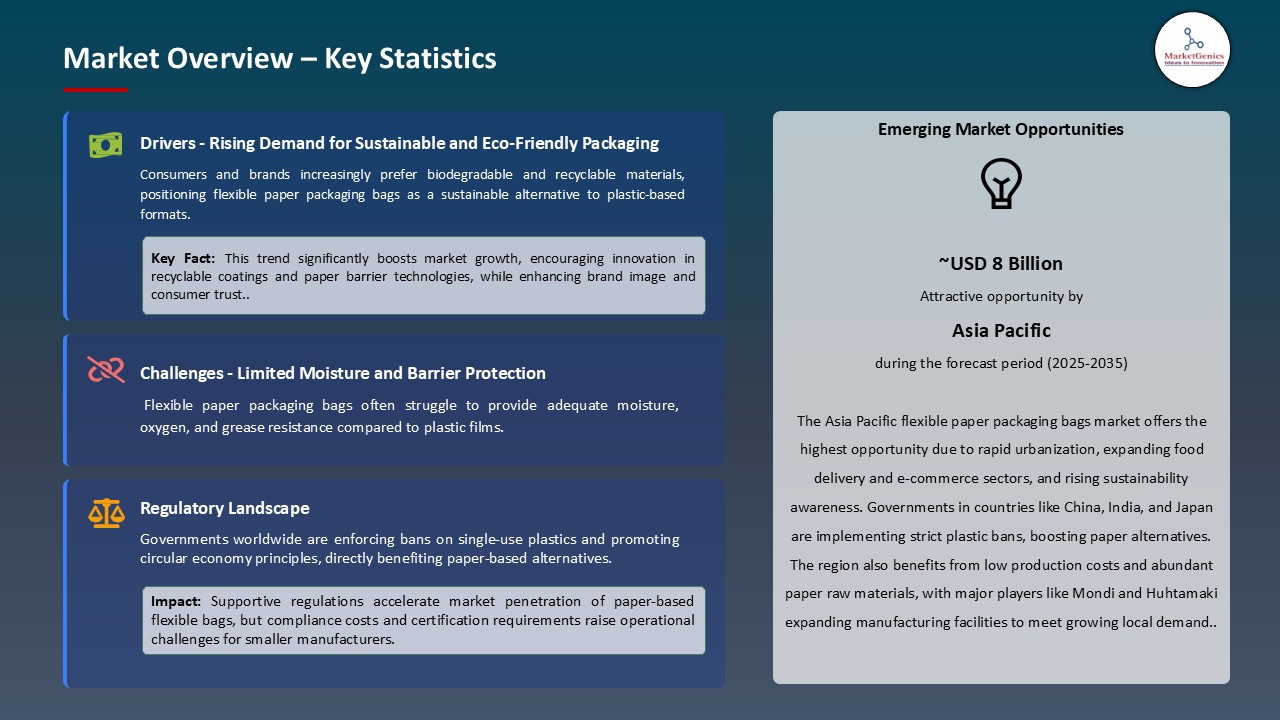

The global flexible paper packaging bags market is experiencing robust growth, with its estimated value of USD 25.8 billion in the year 2025 and USD 46.6 billion by the period 2035, registering a CAGR of 6.1%, during the forecast period. The flexible paper packaging bags market is growing due to increasing consumer preference for sustainable and eco-friendly materials, a desire for convenience and portability in packaging, and the growing need for functional features like barrier protection, reseal ability, and grease resistance.

Florian Ullrich, Sales Director Paper Bags Germany, Mondi said,

“Valve bags are designed for high-speed filling and with sensitive contents such as these specialty chemical powders, high quality material and secure closing options are also paramount. Being able to deliver and indeed improve on these elements, while reducing the carbon footprint of the packaging, was a challenge we were delighted to answer alongside Evonik.”

The global flexible paper packaging bags market is because of rising sustainability regulations and consumer demand for recyclable packaging are propelling the shift from plastic laminates to paper-based flexible bags across food and beverage sectors. For instance, in March 2025, Amcor has announced the launch of its new AmFiber Performance Paper stand-up pouch, a paper-based refill pack for instant coffee and dry beverage products. This innovation strengthens Amcor’s position in sustainable flexibles and validates the commercial readiness of fibre-based alternatives in premium dry goods packaging.

Moreover, growing emphasis on renewable materials, plastic reduction targets, and brand-driven circular economy commitments is accelerating the transition toward flexible paper packaging bags. For instance, in November 2024, Smurfit Westrock announced of its latest pioneering innovation, the EasySplit Bag-in-Box design which was specifically developed to meet the upcoming requirements of the Packaging and Packaging Waste Regulation (PPWR).

The regulatory framework across various countries is fostering the growth of the flexible paper packaging bags market by encouraging sustainability, recyclability, and material efficiency across food, retail, and industrial applications. For instance, in 2024, India’s Plastic Waste Management (Amendment) Rules imposed higher Extended Producer Responsibility (EPR) targets, incentivizing industries to adopt paper-based alternatives. Strengthening government mandates on sustainability and material circularity are accelerating the transition toward renewable, recyclable paper-based flexible packaging solutions across key regions.

The key market opportunities of the global flexible paper packaging bags market are in paper-based pouches, biodegradable coatings, fiber-based barrier films, compostable adhesives, and digital printing for sustainable packaging. These emerging areas enable performance enhancement, customization, and recyclability, expanding eco-friendly solutions across industries.

Flexible Paper Packaging Bags Market Dynamics and Trends

Driver: Expansion of Circular Economy Regulations Encouraging Fiber-Based Packaging Adoption

- Global momentum toward circular economy policies is propelling the demand for flexible paper packaging bags. Governments and multinational retailers are setting strict guidelines for recyclable, renewable, and compostable packaging to minimize landfill waste. Manufacturers are transitioning from plastic laminates to paper-based solutions that align with extended producer responsibility (EPR) targets. For instance, In 2025, International Paper enhanced its paper bag portfolio following the EU’s updated circular economy framework, introducing lightweight fiber-based industrial sacks that reduce carbon footprint and support closed-loop recycling systems

- Additionally, strengthened global circular economy policies are accelerating large-scale investment in recyclable, fiber-based flexible packaging formats across end-use sectors. For instance, in August 2025, Mondi announced €16 million investment in state-of-the-art technology at its plant in Solec (Poland) Mondi is ramping up production of this high-performance barrier paper which offers exceptional protection against oxygen, water vapour and grease, with an oxygen transmission rate (OTR) below 0.5 cm3/m2d and water vapor transmission rate (WVTR) below 0.5 g/m2d.

Restraint: Performance Limitations in Moisture and Grease Barrier Applications

- Despite strong sustainability advantages, flexible paper packaging bags market face challenges in moisture, oxygen, and grease resistance compared to multi-layer plastic laminates. This limits their application in high-barrier food and chemical packaging segments. Manufacturers continue to explore alternative coatings and hybrid paper composites to bridge this performance gap. For instance, in 2025, Huhtamaki Group announced R&D advancements in water-based dispersion barrier technology, aimed at improving the shelf life of dry and greasy foods without compromising recyclability.

- However, large-scale commercial adoption remains limited due to cost and machinery adaptation requirements. These constraints may slow penetration in certain high-performance packaging niches such as dairy or frozen foods.

Opportunity: Rapid Expansion of E-commerce Driving Demand for Durable Paper Mailers

- The global surge in online retail is creating substantial opportunities for flexible paper packaging bags optimized for shipping, returns, and sustainable branding. E-commerce players are seeking recyclable and lightweight packaging alternatives to reduce plastic dependency while enhancing customer perception. For instance, in 2022 Smurfit Kappa Group expanded its Better Planet Packaging line to include customized paper mailers that combine strength and print adaptability for direct-to-consumer fulfillment. These developments reflect growing retailer alignment with sustainability mandates and consumer eco-consciousness in digital commerce.

- Furthermore, packaging businesses are investing in long-lasting, recyclable paper-mailer designs designed for direct-to-consumer fulfillment as e-commerce volumes continue to rise globally. For instance, in September 2025, PAC Worldwide revealed at PACK EXPO a new wicketed paper mailer with a fixed-release liner and post-consumer recycled content aimed at high-volume e-commerce operations. These innovations underscore PAC’s commitment to delivering more sustainable, high-performance solutions for e-commerce and retail markets.

- The shift to fiber-based mailers for e-commerce logistics is unlocking new growth pathways for flexible paper packaging and accelerating uptake across D2C and fulfilment channels.

Key Trend: Integration of Digital Printing and Smart Labeling in Paper Packaging

- Digital printing technology is enabling converters of fiber-based flexible packaging to offer rapid turnaround, variable artwork, and short-run customization meeting the dual demands of direct-to-consumer e-commerce and brand differentiation while maintaining recyclable paper structures. For instance, in September 2025, Polyart Group announced at Labelexpo Europe 2025 a new range of sustainable substrates for digital printing and labelling (r-Polyart, r-Fluolux, r-JetPrint Aquaskin) designed for label and flexible packaging markets with high compatibility for digital workflows.

- Furthermore, smart labeling such as QR codes, NFC tags and other intelligent print-linked features is gaining traction in paper-based flexible packaging, enabling brands to engage consumers, provide authentication and support recycling instructions, all on a sustainably printed paper bag. For instance, in January 2024, Toppan Inc. developed paper-based packaging with embedded NFC tags where the NFC circuit is built into the paper substrate rather than plastic film enabling authentication and consumer tap-access in a recyclable fibre format.

- In addition, the integration of advanced digital printing and smart labeling technologies is revolutionizing the flexible paper packaging landscape by combining sustainability with functionality. These innovations enable personalization, traceability, and consumer engagement while maintaining recyclability, positioning fibre-based packaging as a high-value, and tech-enabled alternative to conventional plastic-based formats in global markets.

Flexible Paper Packaging Bags Market Analysis and Segmental Data

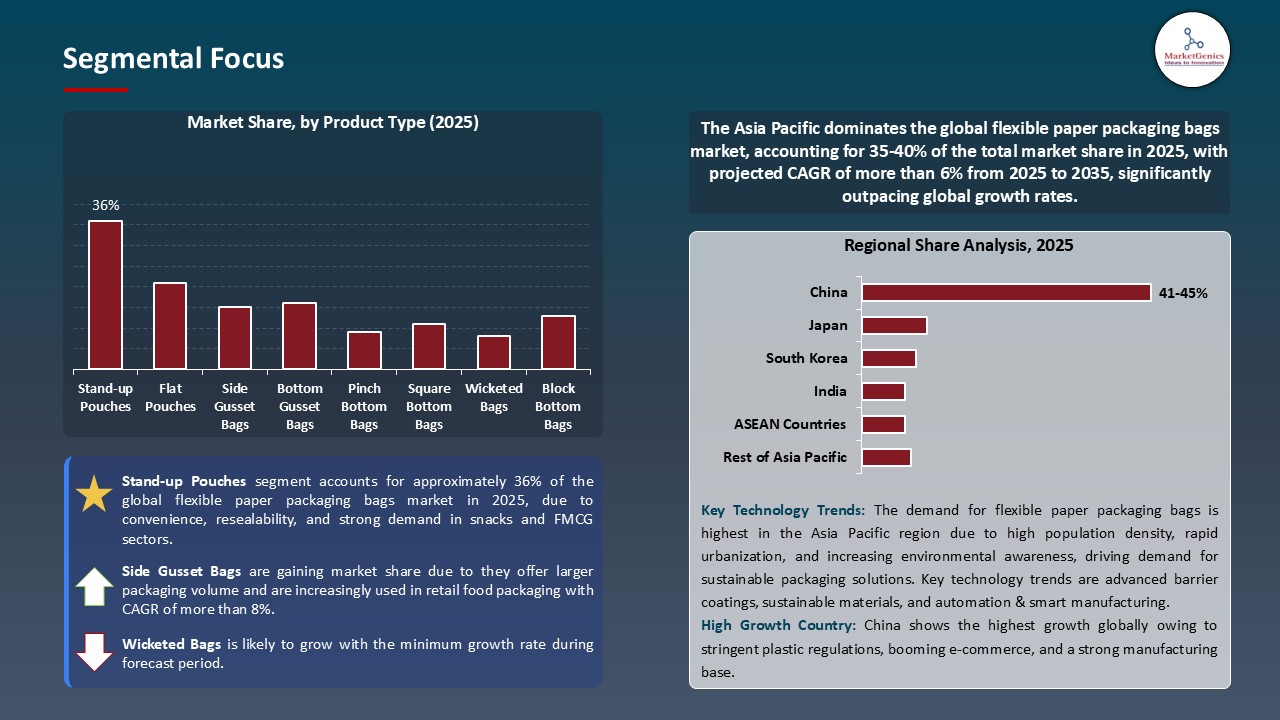

Stand-up Pouches Dominate Global Flexible Paper Packaging Bags Market

- Stand-up pouches the global flexible paper packaging bags market owing to stand-up pouches are especially appealing for the food, beverage, home care, and personal care sectors because to their upright, gusseted shape, which offers shelf-ready display and consumer convenience. For instance, in February 2025, Mondi collaborated with Proquimia to launch paper-based stand-up pouches for dishwashing tabs in Spain and Portugal made with them re/cycle FunctionalBarrier Paper 95/5, achieving over 85 % paper content and meeting local recyclability standards.

- Furthermore, the as brands and regulators mandate higher paper content and recyclability in flexible formats, manufacturers are accelerating launches of stand-up pouches using fibre-rich barrier papers. For instance, in March 2025, Amcor has announced the launch of its new AmFiber Performance Paper stand-up pouch, a paper-based refill pack for instant coffee and dry beverage products. The growing adoption of fibre-rich, recyclable stand-up pouches is reshaping the flexible packaging landscape, driving a rapid shift from plastic laminates to sustainable paper-based formats while enhancing brand compliance with global circular economy and recyclability regulations.

Asia Pacific Leads Global Flexible Paper Packaging Bags Market Demand

- The Asia Pacific's dominance in the global flexible paper packaging bags market is propelled by the major packaging players are establishing regional production hubs and strategic manufacturing collaborations in the Asia Pacific to reduce lead times, respond to local regulations, and serve high-growth FMCG and e-commerce markets. For instance, in February 2025, UFlex Limited announced over Rs 750 cr investment in India and Mexico to expand flexible packaging capabilities and strengthen its foothold in fast-growing domestic markets.

- Furthermore, production and supply-chain localisation in Asia Pacific is accelerating adoption of flexible paper packaging bags by enabling faster market responsiveness and compliance with regional circular economy mandates. For instance, in August 2025, Windmöller & Hölscher Asia Pacific signed multiple distribution agreements to support converting equipment for paper-bag and pouch production in markets such as Vietnam, Malaysia, Thailand and Indonesia.

Flexible Paper Packaging Bags Market Ecosystem

The global flexible paper packaging bags market is moderately fragmented, with high concentration among key players such as Amcor plc, Mondi Group, Smurfit Kappa Group, International Paper Company, and Huhtamaki Group, who dominate through technological innovation, product diversification, and strategic sustainability initiatives. These companies continuously invest in advanced paper barrier technologies, lightweight recyclable substrates, and eco-efficient production systems to meet evolving environmental regulations and consumer preferences. For instance, in July 2025, Amcor announced that its AmFiber Performance Paper has been proven recyclable in Brazil's mixed-paper recycling stream, marking a significant step forward in more sustainable packaging innovation.

Recent Development and Strategic Overview:

- In April 2025, Mondi delivered a new paper valve bag for Evonik that removed a prior plastic-coated layer, reducing packaging weight by ~30% while preserving protection for chemical powders. The new paper bag also has a lower carbon footprint which was assessed in Mondi’s in-house life cycle-based PIA (Product Impact Assessment) tool.

- In November 2024, Smurfit Westrock announced the launch of its latest pioneering innovation, the EasySplit Bag-in-Box design which was specifically developed to meet the upcoming requirements of the Packaging and Packaging Waste Regulation (PPWR).

Report Scope

|

Detail |

|

|

Market Size in 2025 |

USD 25.8 Bn |

|

Market Forecast Value in 20255 |

USD 46.6 Bn |

|

Growth Rate (CAGR) |

6.1% |

|

Forecast Period |

2025 – 20255 |

|

Historical Data Available for |

2021 – 2024 |

|

Market Size Units |

US$ Billion for Value MMT for Volume |

|

Report Format |

Electronic (PDF) + Excel |

|

North America |

Europe |

Asia Pacific |

Middle East |

Africa |

South America |

|

|

|

|

|

|

|

Companies Covered |

|||||

|

|

|

|

|

|

Flexible Paper Packaging Bags Market Segmentation and Highlights

|

Segment |

Sub-segment |

|

Flexible Paper Packaging Bags Market By Product Type |

|

|

Flexible Paper Packaging Bags Market By Material Type

|

|

|

Flexible Paper Packaging Bags Market By Closure Type

|

|

|

Flexible Paper Packaging Bags Market By Capacity/Size |

|

|

Flexible Paper Packaging Bags Market By Printing Technology

|

|

|

Flexible Paper Packaging Bags Market By Thickness

|

|

|

Flexible Paper Packaging Bags Market By Distribution Channel |

|

|

Flexible Paper Packaging Bags Market By End-Use Industry |

|

Frequently Asked Questions

Table of Contents

- 1. Research Methodology and Assumptions

- 1.1. Definitions

- 1.2. Research Design and Approach

- 1.3. Data Collection Methods

- 1.4. Base Estimates and Calculations

- 1.5. Forecasting Models

- 1.5.1. Key Forecast Factors & Impact Analysis

- 1.6. Secondary Research

- 1.6.1. Open Sources

- 1.6.2. Paid Databases

- 1.6.3. Associations

- 1.7. Primary Research

- 1.7.1. Primary Sources

- 1.7.2. Primary Interviews with Stakeholders across Ecosystem

- 2. Executive Summary

- 2.1. Global Flexible Paper Packaging Bags Market Outlook

- 2.1.1. Flexible Paper Packaging Bags Market Size (Volume-MMT and Value - US$ Bn), and Forecasts, 2021-2035

- 2.1.2. Compounded Annual Growth Rate Analysis

- 2.1.3. Growth Opportunity Analysis

- 2.1.4. Segmental Share Analysis

- 2.1.5. Geographical Share Analysis

- 2.2. Market Analysis and Facts

- 2.3. Supply-Demand Analysis

- 2.4. Competitive Benchmarking

- 2.5. Go-to- Market Strategy

- 2.5.1. Customer/ End-use Industry Assessment

- 2.5.2. Growth Opportunity Data, 2025-2035

- 2.5.2.1. Regional Data

- 2.5.2.2. Country Data

- 2.5.2.3. Segmental Data

- 2.5.3. Identification of Potential Market Spaces

- 2.5.4. GAP Analysis

- 2.5.5. Potential Attractive Price Points

- 2.5.6. Prevailing Market Risks & Challenges

- 2.5.7. Preferred Sales & Marketing Strategies

- 2.5.8. Key Recommendations and Analysis

- 2.5.9. A Way Forward

- 2.1. Global Flexible Paper Packaging Bags Market Outlook

- 3. Industry Data and Premium Insights

- 3.1. Global Flexible Paper Packaging Bags Industry Overview, 2025

- 3.1.1. PackagingIndustry Ecosystem Analysis

- 3.1.2. Key Trends for Packaging Industry

- 3.1.3. Regional Distribution for Packaging Industry

- 3.2. Supplier Customer Data

- 3.3. Technology Roadmap and Developments

- 3.4. Trade Analysis

- 3.4.1. Import & Export Analysis, 2025

- 3.4.2. Top Importing Countries

- 3.4.3. Top Exporting Countries

- 3.5. Trump Tariff Impact Analysis

- 3.5.1. Manufacturer

- 3.5.1.1. Based on the component & Raw material

- 3.5.2. Supply Chain

- 3.5.3. End Consumer

- 3.5.1. Manufacturer

- 3.6. Raw Material Analysis

- 3.1. Global Flexible Paper Packaging Bags Industry Overview, 2025

- 4. Market Overview

- 4.1. Market Dynamics

- 4.1.1. Drivers

- 4.1.1.1. Rising consumer and regulatory demand for sustainable/eco-friendly packaging.

- 4.1.1.2. Growth of e-commerce and retail packaged goods increasing demand for lightweight, customizable bags.

- 4.1.1.3. Technological advances in barrier coatings, printing and laminations expanding food-grade applications.

- 4.1.2. Restraints

- 4.1.2.1. Inferior barrier/protection vs some plastics, limiting use for moisture/oxygen-sensitive products.

- 4.1.2.2. Raw material price volatility and limited recycling/collection infrastructure for coated paper.

- 4.1.1. Drivers

- 4.2. Key Trend Analysis

- 4.3. Regulatory Framework

- 4.3.1. Key Regulations, Norms, and Subsidies, by Key Countries

- 4.3.2. Tariffs and Standards

- 4.3.3. Impact Analysis of Regulations on the Market

- 4.4. Value Chain Analysis

- 4.4.1. Raw Material Suppliers

- 4.4.2. Flexible Paper Packaging Bags Manufacturers

- 4.4.3. Distributors/ Suppliers

- 4.4.4. End-users/ Customers

- 4.5. Porter’s Five Forces Analysis

- 4.6. PESTEL Analysis

- 4.7. Global Flexible Paper Packaging Bags Market Demand

- 4.7.1. Historical Market Size - in (Volume-MMT and Value - US$ Bn), 2020-2024

- 4.7.2. Current and Future Market Size - in (Volume-MMT and Value - US$ Bn), 2025–2035

- 4.7.2.1. Y-o-Y Growth Trends

- 4.7.2.2. Absolute $ Opportunity Assessment

- 4.1. Market Dynamics

- 5. Competition Landscape

- 5.1. Competition structure

- 5.1.1. Fragmented v/s consolidated

- 5.2. Company Share Analysis, 2025

- 5.2.1. Global Company Market Share

- 5.2.2. By Region

- 5.2.2.1. North America

- 5.2.2.2. Europe

- 5.2.2.3. Asia Pacific

- 5.2.2.4. Middle East

- 5.2.2.5. Africa

- 5.2.2.6. South America

- 5.3. Product Comparison Matrix

- 5.3.1. Specifications

- 5.3.2. Market Positioning

- 5.3.3. Pricing

- 5.1. Competition structure

- 6. Global Flexible Paper Packaging Bags Market Analysis, by Product Type

- 6.1. Key Segment Analysis

- 6.2. Flexible Paper Packaging Bags Market Size (Volume-MMT and Value - US$ Bn), Analysis, and Forecasts, by Product Type, 2021-2035

- 6.2.1. Stand-up Pouches

- 6.2.1.1. With Zipper

- 6.2.1.2. Without Zipper

- 6.2.2. Flat Pouches

- 6.2.3. Side Gusset Bags

- 6.2.4. Bottom Gusset Bags

- 6.2.5. Pinch Bottom Bags

- 6.2.6. Square Bottom Bags

- 6.2.7. Wicketed Bags

- 6.2.8. Block Bottom Bags

- 6.2.1. Stand-up Pouches

- 7. Global Flexible Paper Packaging Bags Market Analysis, by Material Type

- 7.1. Key Segment Analysis

- 7.2. Flexible Paper Packaging Bags Market Size (Volume-MMT and Value - US$ Bn), Analysis, and Forecasts, by Material Type, 2021-2035

- 7.2.1. Kraft Paper

- 7.2.1.1. Virgin Kraft Paper

- 7.2.1.2. Recycled Kraft Paper

- 7.2.2. Coated Paper

- 7.2.2.1. PE Coated

- 7.2.2.2. Wax Coated

- 7.2.2.3. PLA Coated

- 7.2.3. Greaseproof Paper

- 7.2.4. Parchment Paper

- 7.2.5. Multilayer Paper Laminates

- 7.2.1. Kraft Paper

- 8. Global Flexible Paper Packaging Bags Market Analysis and Forecasts, by Closure Type

- 8.1. Key Findings

- 8.2. Flexible Paper Packaging Bags Market Size (Volume-MMT and Value - US$ Bn), Analysis, and Forecasts, by Closure Type, 2021-2035

- 8.2.1. Zipper Closure

- 8.2.1.1. Slider Zipper

- 8.2.1.2. Press-to-Close Zipper

- 8.2.2. Tin Tie Closure

- 8.2.3. Heat Seal Closure

- 8.2.4. Adhesive Closure

- 8.2.5. Fold-over Closure

- 8.2.6. Valve Closure

- 8.2.7. Others

- 8.2.1. Zipper Closure

- 9. Global Flexible Paper Packaging Bags Market Analysis and Forecasts, by Capacity/Size

- 9.1. Key Findings

- 9.2. Flexible Paper Packaging Bags Market Size (Volume-MMT and Value - US$ Bn), Analysis, and Forecasts, by Capacity/Size, 2021-2035

- 9.2.1. Small (Up to 500g)

- 9.2.2. Medium (500g - 2kg)

- 9.2.3. Large (2kg - 5kg)

- 9.2.4. Extra Large (Above 5kg)

- 10. Global Flexible Paper Packaging Bags Market Analysis and Forecasts, by Printing Technology

- 10.1. Key Findings

- 10.2. Flexible Paper Packaging Bags Market Size (Volume-MMT and Value - US$ Bn), Analysis, and Forecasts, by Printing Technology, 2021-2035

- 10.2.1. Flexographic Printing

- 10.2.2. Rotogravure Printing

- 10.2.3. Digital Printing

- 10.2.4. Offset Printing

- 10.2.5. Unprinted/Plain

- 10.2.6. Others

- 11. Global Flexible Paper Packaging Bags Market Analysis and Forecasts, by Thickness

- 11.1. Key Findings

- 11.2. Flexible Paper Packaging Bags Market Size (Volume-MMT and Value - US$ Bn), Analysis, and Forecasts, by Thickness, 2021-2035

- 11.2.1. Below 40 GSM

- 11.2.2. 40-60 GSM

- 11.2.3. 60-80 GSM

- 11.2.4. 80-100 GSM

- 11.2.5. Above 100 GSM

- 12. Global Flexible Paper Packaging Bags Market Analysis and Forecasts, by Distribution Channel

- 12.1. Key Findings

- 12.2. Flexible Paper Packaging Bags Market Size (Volume-MMT and Value - US$ Bn), Analysis, and Forecasts, by Distribution Channel, 2021-2035

- 12.2.1. Direct Sales/B2B

- 12.2.2. Distributors & Wholesalers

- 12.2.3. Online/E-commerce

- 12.2.4. Retail Outlets

- 13. Global Flexible Paper Packaging Bags Market Analysis and Forecasts, by End-Use Industry

- 13.1. Key Findings

- 13.2. Flexible Paper Packaging Bags Market Size (Volume-MMT and Value - US$ Bn), Analysis, and Forecasts, by Thickness, 2021-2035

- 13.2.1. Food & Beverage Industry

- 13.2.1.1. Bakery & Confectionery

- 13.2.1.2. Bread Packaging

- 13.2.1.3. Cookies & Biscuits

- 13.2.1.4. Cakes & Pastries

- 13.2.1.5. Candies & Chocolates

- 13.2.1.6. Others

- 13.2.2. Coffee & Tea

- 13.2.2.1. Ground Coffee

- 13.2.2.2. Coffee Beans

- 13.2.2.3. Tea Leaves

- 13.2.2.4. Instant Beverages

- 13.2.2.5. Others

- 13.2.3. Snacks & Savory

- 13.2.3.1. Chips & Crisps

- 13.2.3.2. Nuts & Seeds

- 13.2.3.3. Popcorn

- 13.2.3.4. Dried Fruits

- 13.2.3.5. Others

- 13.2.4. Flour & Grains

- 13.2.4.1. Wheat Flour

- 13.2.4.2. Rice

- 13.2.4.3. Pulses

- 13.2.4.4. Cereals

- 13.2.4.5. Others

- 13.2.5. Pet Food

- 13.2.5.1. Dry Pet Food

- 13.2.5.2. Pet Treats

- 13.2.5.3. Pet Supplements

- 13.2.5.4. Others

- 13.2.6. Fresh Produce

- 13.2.6.1. Fruits

- 13.2.6.2. Vegetables

- 13.2.6.3. Mushrooms

- 13.2.6.4. Others

- 13.2.7. Frozen Foods

- 13.2.7.1. Frozen Vegetables

- 13.2.7.2. Frozen Snacks

- 13.2.7.3. Others

- 13.2.8. Personal Care & Cosmetics

- 13.2.9. Bath & Body

- 13.2.9.1. Bath Salts

- 13.2.9.2. Soap Packaging

- 13.2.9.3. Body Scrubs

- 13.2.9.4. Others

- 13.2.10. Hair Care

- 13.2.10.1. Hair Masks

- 13.2.10.2. Dry Shampoo

- 13.2.10.3. Others

- 13.2.11. Skincare Samples

- 13.2.12. Others

- 13.2.13. Pharmaceuticals & Nutraceuticals

- 13.2.14. Chemical & Industrial

- 13.2.15. Retail & E-commerce

- 13.2.16. Home Care & Household

- 13.2.17. Textile & Apparel

- 13.2.18. Stationery & Office Supplies

- 13.2.19. Other End-use Industries

- 13.2.1. Food & Beverage Industry

- 14. Global Flexible Paper Packaging Bags Market Analysis and Forecasts, by Region

- 14.1. Key Findings

- 14.2. Flexible Paper Packaging Bags Market Size (Volume-MMT and Value - US$ Bn), Analysis, and Forecasts, by Region, 2021-2035

- 14.2.1. North America

- 14.2.2. Europe

- 14.2.3. Asia Pacific

- 14.2.4. Middle East

- 14.2.5. Africa

- 14.2.6. South America

- 15. North America Flexible Paper Packaging Bags Market Analysis

- 15.1. Key Segment Analysis

- 15.2. Regional Snapshot

- 15.3. North America Flexible Paper Packaging Bags Market Size (Volume-MMT and Value - US$ Bn), Analysis, and Forecasts, 2021-2035

- 15.3.1. Product Type

- 15.3.2. Material Type

- 15.3.3. Closure Type

- 15.3.4. Capacity/Size

- 15.3.5. Printing Technology

- 15.3.6. Thickness

- 15.3.7. Distribution Channel

- 15.3.8. End-Use Industry

- 15.3.9. Country

- 15.3.9.1. USA

- 15.3.9.2. Canada

- 15.3.9.3. Mexico

- 15.4. USA Flexible Paper Packaging Bags Market

- 15.4.1. Country Segmental Analysis

- 15.4.2. Product Type

- 15.4.3. Material Type

- 15.4.4. Closure Type

- 15.4.5. Capacity/Size

- 15.4.6. Printing Technology

- 15.4.7. Thickness

- 15.4.8. Distribution Channel

- 15.4.9. End-Use Industry

- 15.5. Canada Flexible Paper Packaging Bags Market

- 15.5.1. Country Segmental Analysis

- 15.5.2. Product Type

- 15.5.3. Material Type

- 15.5.4. Closure Type

- 15.5.5. Capacity/Size

- 15.5.6. Printing Technology

- 15.5.7. Thickness

- 15.5.8. Distribution Channel

- 15.5.9. End-Use Industry

- 15.6. Mexico Flexible Paper Packaging Bags Market

- 15.6.1. Country Segmental Analysis

- 15.6.2. Product Type

- 15.6.3. Material Type

- 15.6.4. Closure Type

- 15.6.5. Capacity/Size

- 15.6.6. Printing Technology

- 15.6.7. Thickness

- 15.6.8. Distribution Channel

- 15.6.9. End-Use Industry

- 16. Europe Flexible Paper Packaging Bags Market Analysis

- 16.1. Key Segment Analysis

- 16.2. Regional Snapshot

- 16.3. Europe Flexible Paper Packaging Bags Market Size (Volume-MMT and Value - US$ Bn), Analysis, and Forecasts, 2021-2035

- 16.3.1. Product Type

- 16.3.2. Material Type

- 16.3.3. Closure Type

- 16.3.4. Capacity/Size

- 16.3.5. Printing Technology

- 16.3.6. Thickness

- 16.3.7. Distribution Channel

- 16.3.8. End-Use Industry

- 16.3.9. Country

- 16.3.9.1. Germany

- 16.3.9.2. United Kingdom

- 16.3.9.3. France

- 16.3.9.4. Italy

- 16.3.9.5. Spain

- 16.3.9.6. Netherlands

- 16.3.9.7. Nordic Countries

- 16.3.9.8. Poland

- 16.3.9.9. Russia & CIS

- 16.3.9.10. Rest of Europe

- 16.4. Germany Flexible Paper Packaging Bags Market

- 16.4.1. Country Segmental Analysis

- 16.4.2. Product Type

- 16.4.3. Material Type

- 16.4.4. Closure Type

- 16.4.5. Capacity/Size

- 16.4.6. Printing Technology

- 16.4.7. Thickness

- 16.4.8. Distribution Channel

- 16.4.9. End-Use Industry

- 16.5. United Kingdom Flexible Paper Packaging Bags Market

- 16.5.1. Country Segmental Analysis

- 16.5.2. Product Type

- 16.5.3. Material Type

- 16.5.4. Closure Type

- 16.5.5. Capacity/Size

- 16.5.6. Printing Technology

- 16.5.7. Thickness

- 16.5.8. Distribution Channel

- 16.5.9. End-Use Industry

- 16.6. France Flexible Paper Packaging Bags Market

- 16.6.1. Country Segmental Analysis

- 16.6.2. Product Type

- 16.6.3. Material Type

- 16.6.4. Closure Type

- 16.6.5. Capacity/Size

- 16.6.6. Printing Technology

- 16.6.7. Thickness

- 16.6.8. Distribution Channel

- 16.6.9. End-Use Industry

- 16.7. Italy Flexible Paper Packaging Bags Market

- 16.7.1. Country Segmental Analysis

- 16.7.2. Product Type

- 16.7.3. Material Type

- 16.7.4. Closure Type

- 16.7.5. Capacity/Size

- 16.7.6. Printing Technology

- 16.7.7. Thickness

- 16.7.8. Distribution Channel

- 16.7.9. End-Use Industry

- 16.8. Spain Flexible Paper Packaging Bags Market

- 16.8.1. Country Segmental Analysis

- 16.8.2. Product Type

- 16.8.3. Material Type

- 16.8.4. Closure Type

- 16.8.5. Capacity/Size

- 16.8.6. Printing Technology

- 16.8.7. Thickness

- 16.8.8. Distribution Channel

- 16.8.9. End-Use Industry

- 16.9. Netherlands Flexible Paper Packaging Bags Market

- 16.9.1. Country Segmental Analysis

- 16.9.2. Product Type

- 16.9.3. Material Type

- 16.9.4. Closure Type

- 16.9.5. Capacity/Size

- 16.9.6. Printing Technology

- 16.9.7. Thickness

- 16.9.8. Distribution Channel

- 16.9.9. End-Use Industry

- 16.10. Nordic Countries Flexible Paper Packaging Bags Market

- 16.10.1. Country Segmental Analysis

- 16.10.2. Product Type

- 16.10.3. Material Type

- 16.10.4. Closure Type

- 16.10.5. Capacity/Size

- 16.10.6. Printing Technology

- 16.10.7. Thickness

- 16.10.8. Distribution Channel

- 16.10.9. End-Use Industry

- 16.11. Poland Flexible Paper Packaging Bags Market

- 16.11.1. Country Segmental Analysis

- 16.11.2. Product Type

- 16.11.3. Material Type

- 16.11.4. Closure Type

- 16.11.5. Capacity/Size

- 16.11.6. Printing Technology

- 16.11.7. Thickness

- 16.11.8. Distribution Channel

- 16.11.9. End-Use Industry

- 16.12. Russia & CIS Flexible Paper Packaging Bags Market

- 16.12.1. Country Segmental Analysis

- 16.12.2. Product Type

- 16.12.3. Material Type

- 16.12.4. Closure Type

- 16.12.5. Capacity/Size

- 16.12.6. Printing Technology

- 16.12.7. Thickness

- 16.12.8. Distribution Channel

- 16.12.9. End-Use Industry

- 16.13. Rest of Europe Flexible Paper Packaging Bags Market

- 16.13.1. Country Segmental Analysis

- 16.13.2. Product Type

- 16.13.3. Material Type

- 16.13.4. Closure Type

- 16.13.5. Capacity/Size

- 16.13.6. Printing Technology

- 16.13.7. Thickness

- 16.13.8. Distribution Channel

- 16.13.9. End-Use Industry

- 17. Asia Pacific Flexible Paper Packaging Bags Market Analysis

- 17.1. Key Segment Analysis

- 17.2. Regional Snapshot

- 17.3. East Asia Flexible Paper Packaging Bags Market Size (Volume-MMT and Value - US$ Bn), Analysis, and Forecasts, 2021-2035

- 17.3.1. Product Type

- 17.3.2. Material Type

- 17.3.3. Closure Type

- 17.3.4. Capacity/Size

- 17.3.5. Printing Technology

- 17.3.6. Thickness

- 17.3.7. Distribution Channel

- 17.3.8. End-Use Industry

- 17.3.9. Country

- 17.3.9.1. China

- 17.3.9.2. India

- 17.3.9.3. Japan

- 17.3.9.4. South Korea

- 17.3.9.5. Australia and New Zealand

- 17.3.9.6. Indonesia

- 17.3.9.7. Malaysia

- 17.3.9.8. Thailand

- 17.3.9.9. Vietnam

- 17.3.9.10. Rest of Asia Pacific

- 17.4. China Flexible Paper Packaging Bags Market

- 17.4.1. Country Segmental Analysis

- 17.4.2. Product Type

- 17.4.3. Material Type

- 17.4.4. Closure Type

- 17.4.5. Capacity/Size

- 17.4.6. Printing Technology

- 17.4.7. Thickness

- 17.4.8. Distribution Channel

- 17.4.9. End-Use Industry

- 17.5. India Flexible Paper Packaging Bags Market

- 17.5.1. Country Segmental Analysis

- 17.5.2. Product Type

- 17.5.3. Material Type

- 17.5.4. Closure Type

- 17.5.5. Capacity/Size

- 17.5.6. Printing Technology

- 17.5.7. Thickness

- 17.5.8. Distribution Channel

- 17.5.9. End-Use Industry

- 17.6. Japan Flexible Paper Packaging Bags Market

- 17.6.1. Country Segmental Analysis

- 17.6.2. Product Type

- 17.6.3. Material Type

- 17.6.4. Closure Type

- 17.6.5. Capacity/Size

- 17.6.6. Printing Technology

- 17.6.7. Thickness

- 17.6.8. Distribution Channel

- 17.6.9. End-Use Industry

- 17.7. South Korea Flexible Paper Packaging Bags Market

- 17.7.1. Country Segmental Analysis

- 17.7.2. Product Type

- 17.7.3. Material Type

- 17.7.4. Closure Type

- 17.7.5. Capacity/Size

- 17.7.6. Printing Technology

- 17.7.7. Thickness

- 17.7.8. Distribution Channel

- 17.7.9. End-Use Industry

- 17.8. Australia and New Zealand Flexible Paper Packaging Bags Market

- 17.8.1. Country Segmental Analysis

- 17.8.2. Product Type

- 17.8.3. Material Type

- 17.8.4. Closure Type

- 17.8.5. Capacity/Size

- 17.8.6. Printing Technology

- 17.8.7. Thickness

- 17.8.8. Distribution Channel

- 17.8.9. End-Use Industry

- 17.9. Indonesia Flexible Paper Packaging Bags Market

- 17.9.1. Country Segmental Analysis

- 17.9.2. Product Type

- 17.9.3. Material Type

- 17.9.4. Closure Type

- 17.9.5. Capacity/Size

- 17.9.6. Printing Technology

- 17.9.7. Thickness

- 17.9.8. Distribution Channel

- 17.9.9. End-Use Industry

- 17.10. Malaysia Flexible Paper Packaging Bags Market

- 17.10.1. Country Segmental Analysis

- 17.10.2. Product Type

- 17.10.3. Material Type

- 17.10.4. Closure Type

- 17.10.5. Capacity/Size

- 17.10.6. Printing Technology

- 17.10.7. Thickness

- 17.10.8. Distribution Channel

- 17.10.9. End-Use Industry

- 17.11. Thailand Flexible Paper Packaging Bags Market

- 17.11.1. Country Segmental Analysis

- 17.11.2. Product Type

- 17.11.3. Material Type

- 17.11.4. Closure Type

- 17.11.5. Capacity/Size

- 17.11.6. Printing Technology

- 17.11.7. Thickness

- 17.11.8. Distribution Channel

- 17.11.9. End-Use Industry

- 17.12. Vietnam Flexible Paper Packaging Bags Market

- 17.12.1. Country Segmental Analysis

- 17.12.2. Product Type

- 17.12.3. Material Type

- 17.12.4. Closure Type

- 17.12.5. Capacity/Size

- 17.12.6. Printing Technology

- 17.12.7. Thickness

- 17.12.8. Distribution Channel

- 17.12.9. End-Use Industry

- 17.13. Rest of Asia Pacific Flexible Paper Packaging Bags Market

- 17.13.1. Country Segmental Analysis

- 17.13.2. Product Type

- 17.13.3. Material Type

- 17.13.4. Closure Type

- 17.13.5. Capacity/Size

- 17.13.6. Printing Technology

- 17.13.7. Thickness

- 17.13.8. Distribution Channel

- 17.13.9. End-Use Industry

- 18. Middle East Flexible Paper Packaging Bags Market Analysis

- 18.1. Key Segment Analysis

- 18.2. Regional Snapshot

- 18.3. Middle East Flexible Paper Packaging Bags Market Size (Volume-MMT and Value - US$ Bn), Analysis, and Forecasts, 2021-2035

- 18.3.1. Product Type

- 18.3.2. Material Type

- 18.3.3. Closure Type

- 18.3.4. Capacity/Size

- 18.3.5. Printing Technology

- 18.3.6. Thickness

- 18.3.7. Distribution Channel

- 18.3.8. End-Use Industry

- 18.3.9. Country

- 18.3.9.1. Turkey

- 18.3.9.2. UAE

- 18.3.9.3. Saudi Arabia

- 18.3.9.4. Israel

- 18.3.9.5. Rest of Middle East

- 18.4. Turkey Flexible Paper Packaging Bags Market

- 18.4.1. Country Segmental Analysis

- 18.4.2. Product Type

- 18.4.3. Material Type

- 18.4.4. Closure Type

- 18.4.5. Capacity/Size

- 18.4.6. Printing Technology

- 18.4.7. Thickness

- 18.4.8. Distribution Channel

- 18.4.9. End-Use Industry

- 18.5. UAE Flexible Paper Packaging Bags Market

- 18.5.1. Product Type

- 18.5.2. Material Type

- 18.5.3. Closure Type

- 18.5.4. Capacity/Size

- 18.5.5. Printing Technology

- 18.5.6. Thickness

- 18.5.7. Distribution Channel

- 18.5.8. End-Use Industry

- 18.6. Saudi Arabia Flexible Paper Packaging Bags Market

- 18.6.1. Country Segmental Analysis

- 18.6.2. Product Type

- 18.6.3. Material Type

- 18.6.4. Closure Type

- 18.6.5. Capacity/Size

- 18.6.6. Printing Technology

- 18.6.7. Thickness

- 18.6.8. Distribution Channel

- 18.6.9. End-Use Industry

- 18.7. Israel Flexible Paper Packaging Bags Market

- 18.7.1. Country Segmental Analysis

- 18.7.2. Product Type

- 18.7.3. Material Type

- 18.7.4. Closure Type

- 18.7.5. Capacity/Size

- 18.7.6. Printing Technology

- 18.7.7. Thickness

- 18.7.8. Distribution Channel

- 18.7.9. End-Use Industry

- 18.8. Rest of Middle East Flexible Paper Packaging Bags Market

- 18.8.1. Country Segmental Analysis

- 18.8.2. Product Type

- 18.8.3. Material Type

- 18.8.4. Closure Type

- 18.8.5. Capacity/Size

- 18.8.6. Printing Technology

- 18.8.7. Thickness

- 18.8.8. Distribution Channel

- 18.8.9. End-Use Industry

- 19. Africa Flexible Paper Packaging Bags Market Analysis

- 19.1. Key Segment Analysis

- 19.2. Regional Snapshot

- 19.3. Africa Flexible Paper Packaging Bags Market Size (Volume-MMT and Value - US$ Bn), Analysis, and Forecasts, 2021-2035

- 19.3.1. Product Type

- 19.3.2. Material Type

- 19.3.3. Closure Type

- 19.3.4. Capacity/Size

- 19.3.5. Printing Technology

- 19.3.6. Thickness

- 19.3.7. Distribution Channel

- 19.3.8. End-Use Industry

- 19.3.9. Country

- 19.3.9.1. South Africa

- 19.3.9.2. Egypt

- 19.3.9.3. Nigeria

- 19.3.9.4. Algeria

- 19.3.9.5. Rest of Africa

- 19.4. South Africa Flexible Paper Packaging Bags Market

- 19.4.1. Country Segmental Analysis

- 19.4.2. Product Type

- 19.4.3. Material Type

- 19.4.4. Closure Type

- 19.4.5. Capacity/Size

- 19.4.6. Printing Technology

- 19.4.7. Thickness

- 19.4.8. Distribution Channel

- 19.4.9. End-Use Industry

- 19.5. Egypt Flexible Paper Packaging Bags Market

- 19.5.1. Country Segmental Analysis

- 19.5.2. Product Type

- 19.5.3. Material Type

- 19.5.4. Closure Type

- 19.5.5. Capacity/Size

- 19.5.6. Printing Technology

- 19.5.7. Thickness

- 19.5.8. Distribution Channel

- 19.5.9. End-Use Industry

- 19.6. Nigeria Flexible Paper Packaging Bags Market

- 19.6.1. Country Segmental Analysis

- 19.6.2. Product Type

- 19.6.3. Material Type

- 19.6.4. Closure Type

- 19.6.5. Capacity/Size

- 19.6.6. Printing Technology

- 19.6.7. Thickness

- 19.6.8. Distribution Channel

- 19.6.9. End-Use Industry

- 19.7. Algeria Flexible Paper Packaging Bags Market

- 19.7.1. Country Segmental Analysis

- 19.7.2. Product Type

- 19.7.3. Material Type

- 19.7.4. Closure Type

- 19.7.5. Capacity/Size

- 19.7.6. Printing Technology

- 19.7.7. Thickness

- 19.7.8. Distribution Channel

- 19.7.9. End-Use Industry

- 19.8. Rest of Africa Flexible Paper Packaging Bags Market

- 19.8.1. Country Segmental Analysis

- 19.8.2. Product Type

- 19.8.3. Material Type

- 19.8.4. Closure Type

- 19.8.5. Capacity/Size

- 19.8.6. Printing Technology

- 19.8.7. Thickness

- 19.8.8. Distribution Channel

- 19.8.9. End-Use Industry

- 20. South America Flexible Paper Packaging Bags Market Analysis

- 20.1. Key Segment Analysis

- 20.2. Regional Snapshot

- 20.3. Central and South Africa Flexible Paper Packaging Bags Market Size (Volume-MMT and Value - US$ Bn), Analysis, and Forecasts, 2021-2035

- 20.3.1. Product Type

- 20.3.2. Material Type

- 20.3.3. Closure Type

- 20.3.4. Capacity/Size

- 20.3.5. Printing Technology

- 20.3.6. Thickness

- 20.3.7. Distribution Channel

- 20.3.8. End-Use Industry

- 20.3.9. Country

- 20.3.9.1. Brazil

- 20.3.9.2. Argentina

- 20.3.9.3. Rest of South America

- 20.4. Brazil Flexible Paper Packaging Bags Market

- 20.4.1. Country Segmental Analysis

- 20.4.2. Product Type

- 20.4.3. Material Type

- 20.4.4. Closure Type

- 20.4.5. Capacity/Size

- 20.4.6. Printing Technology

- 20.4.7. Thickness

- 20.4.8. Distribution Channel

- 20.4.9. End-Use Industry

- 20.5. Argentina Flexible Paper Packaging Bags Market

- 20.5.1. Country Segmental Analysis

- 20.5.2. Product Type

- 20.5.3. Material Type

- 20.5.4. Closure Type

- 20.5.5. Capacity/Size

- 20.5.6. Printing Technology

- 20.5.7. Thickness

- 20.5.8. Distribution Channel

- 20.5.9. End-Use Industry

- 20.6. Rest of South America Flexible Paper Packaging Bags Market

- 20.6.1. Country Segmental Analysis

- 20.6.2. Product Type

- 20.6.3. Material Type

- 20.6.4. Closure Type

- 20.6.5. Capacity/Size

- 20.6.6. Printing Technology

- 20.6.7. Thickness

- 20.6.8. Distribution Channel

- 20.6.9. End-Use Industry

- 21. Key Players/ Company Profile

- 21.1. Amcor plc

- 21.1.1. Company Details/ Overview

- 21.1.2. Company Financials

- 21.1.3. Key Customers and Competitors

- 21.1.4. Business/ Industry Portfolio

- 21.1.5. Product Portfolio/ Specification Details

- 21.1.6. Pricing Data

- 21.1.7. Strategic Overview

- 21.1.8. Recent Developments

- 21.2. Berry Global Inc.

- 21.3. Capri Packages

- 21.4. Detmold Group

- 21.5. Essentra plc

- 21.6. Gascogne Group

- 21.7. Hood Packaging Corporation

- 21.8. Huhtamaki Group

- 21.9. International Paper Company

- 21.10. Klabin S.A.

- 21.11. Mondi Group

- 21.12. Novolex Holdings

- 21.13. Packaging Corporation of America

- 21.14. ProAmpac LLC

- 21.15. Rengo Co. Ltd.

- 21.16. Schur Flexibles Group

- 21.17. Sealed Air Corporation

- 21.18. Smurfit Kappa Group

- 21.19. Sonoco Products Company

- 21.20. United Bags Inc.

- 21.21. Welton Bibby & Baron

- 21.22. WestRock Company

- 21.23. Other Key Players

- 21.1. Amcor plc

Note* - This is just tentative list of players. While providing the report, we will cover more number of players based on their revenue and share for each geography

Research Design

Our research design integrates both demand-side and supply-side analysis through a balanced combination of primary and secondary research methodologies. By utilizing both bottom-up and top-down approaches alongside rigorous data triangulation methods, we deliver robust market intelligence that supports strategic decision-making.

MarketGenics' comprehensive research design framework ensures the delivery of accurate, reliable, and actionable market intelligence. Through the integration of multiple research approaches, rigorous validation processes, and expert analysis, we provide our clients with the insights needed to make informed strategic decisions and capitalize on market opportunities.

MarketGenics leverages a dedicated industry panel of experts and a comprehensive suite of paid databases to effectively collect, consolidate, and analyze market intelligence.

Our approach has consistently proven to be reliable and effective in generating accurate market insights, identifying key industry trends, and uncovering emerging business opportunities.

Through both primary and secondary research, we capture and analyze critical company-level data such as manufacturing footprints, including technical centers, R&D facilities, sales offices, and headquarters.

Our expert panel further enhances our ability to estimate market size for specific brands based on validated field-level intelligence.

Our data mining techniques incorporate both parametric and non-parametric methods, allowing for structured data collection, sorting, processing, and cleaning.

Demand projections are derived from large-scale data sets analyzed through proprietary algorithms, culminating in robust and reliable market sizing.

Research Approach

The bottom-up approach builds market estimates by starting with the smallest addressable market units and systematically aggregating them to create comprehensive market size projections.

This method begins with specific, granular data points and builds upward to create the complete market landscape.

Customer Analysis → Segmental Analysis → Geographical Analysis

The top-down approach starts with the broadest possible market data and systematically narrows it down through a series of filters and assumptions to arrive at specific market segments or opportunities.

This method begins with the big picture and works downward to increasingly specific market slices.

TAM → SAM → SOM

Research Methods

Desk / Secondary Research

While analysing the market, we extensively study secondary sources, directories, and databases to identify and collect information useful for this technical, market-oriented, and commercial report. Secondary sources that we utilize are not only the public sources, but it is a combination of Open Source, Associations, Paid Databases, MG Repository & Knowledgebase, and others.

- Company websites, annual reports, financial reports, broker reports, and investor presentations

- National government documents, statistical databases and reports

- News articles, press releases and web-casts specific to the companies operating in the market, Magazines, reports, and others

- We gather information from commercial data sources for deriving company specific data such as segmental revenue, share for geography, product revenue, and others

- Internal and external proprietary databases (industry-specific), relevant patent, and regulatory databases

- Governing Bodies, Government Organizations

- Relevant Authorities, Country-specific Associations for Industries

We also employ the model mapping approach to estimate the product level market data through the players' product portfolio

Primary Research

Primary research/ interviews is vital in analyzing the market. Most of the cases involves paid primary interviews. Primary sources include primary interviews through e-mail interactions, telephonic interviews, surveys as well as face-to-face interviews with the different stakeholders across the value chain including several industry experts.

| Type of Respondents | Number of Primaries |

|---|---|

| Tier 2/3 Suppliers | ~20 |

| Tier 1 Suppliers | ~25 |

| End-users | ~25 |

| Industry Expert/ Panel/ Consultant | ~30 |

| Total | ~100 |

MG Knowledgebase

• Repository of industry blog, newsletter and case studies

• Online platform covering detailed market reports, and company profiles

Forecasting Factors and Models

Forecasting Factors

- Historical Trends – Past market patterns, cycles, and major events that shaped how markets behave over time. Understanding past trends helps predict future behavior.

- Industry Factors – Specific characteristics of the industry like structure, regulations, and innovation cycles that affect market dynamics.

- Macroeconomic Factors – Economic conditions like GDP growth, inflation, and employment rates that affect how much money people have to spend.

- Demographic Factors – Population characteristics like age, income, and location that determine who can buy your product.

- Technology Factors – How quickly people adopt new technology and how much technology infrastructure exists.

- Regulatory Factors – Government rules, laws, and policies that can help or restrict market growth.

- Competitive Factors – Analyzing competition structure such as degree of competition and bargaining power of buyers and suppliers.

Forecasting Models / Techniques

Multiple Regression Analysis

- Identify and quantify factors that drive market changes

- Statistical modeling to establish relationships between market drivers and outcomes

Time Series Analysis – Seasonal Patterns

- Understand regular cyclical patterns in market demand

- Advanced statistical techniques to separate trend, seasonal, and irregular components

Time Series Analysis – Trend Analysis

- Identify underlying market growth patterns and momentum

- Statistical analysis of historical data to project future trends

Expert Opinion – Expert Interviews

- Gather deep industry insights and contextual understanding

- In-depth interviews with key industry stakeholders

Multi-Scenario Development

- Prepare for uncertainty by modeling different possible futures

- Creating optimistic, pessimistic, and most likely scenarios

Time Series Analysis – Moving Averages

- Sophisticated forecasting for complex time series data

- Auto-regressive integrated moving average models with seasonal components

Econometric Models

- Apply economic theory to market forecasting

- Sophisticated economic models that account for market interactions

Expert Opinion – Delphi Method

- Harness collective wisdom of industry experts

- Structured, multi-round expert consultation process

Monte Carlo Simulation

- Quantify uncertainty and probability distributions

- Thousands of simulations with varying input parameters

Research Analysis

Our research framework is built upon the fundamental principle of validating market intelligence from both demand and supply perspectives. This dual-sided approach ensures comprehensive market understanding and reduces the risk of single-source bias.

Demand-Side Analysis: We understand end-user/application behavior, preferences, and market needs along with the penetration of the product for specific application.

Supply-Side Analysis: We estimate overall market revenue, analyze the segmental share along with industry capacity, competitive landscape, and market structure.

Validation & Evaluation

Data triangulation is a validation technique that uses multiple methods, sources, or perspectives to examine the same research question, thereby increasing the credibility and reliability of research findings. In market research, triangulation serves as a quality assurance mechanism that helps identify and minimize bias, validate assumptions, and ensure accuracy in market estimates.

- Data Source Triangulation – Using multiple data sources to examine the same phenomenon

- Methodological Triangulation – Using multiple research methods to study the same research question

- Investigator Triangulation – Using multiple researchers or analysts to examine the same data

- Theoretical Triangulation – Using multiple theoretical perspectives to interpret the same data

Custom Market Research Services

We will customise the research for you, in case the report listed above does not meet your requirements.

Get 10% Free Customisation