Automated Material Handling Equipment Market Size, Share & Trends Analysis Report by Equipment Type (Automated Storage & Retrieval Systems (AS/RS), Automated Guided Vehicles (AGV), Autonomous Mobile Robots (AMR), Conveyor Systems, Robotic Systems, Palletizers & Depalletizers, Sortation Systems, Cranes & Hoists, Other Equipment Type), Technology, Load Capacity, Operation Mode, Function, Ownership Model, Integration Level, Installation Type, End-Use Industry and Geography (North America, Europe, Asia Pacific, Middle East, Africa, and South America) – Global Industry Data, Trends, and Forecasts, 2026–2035

|

|

|

Segmental Data Insights |

|

|

Demand Trends |

|

|

Competitive Landscape |

|

|

Strategic Development |

|

|

Future Outlook & Opportunities |

|

Automated Material Handling Equipment Market Size, Share, and Growth

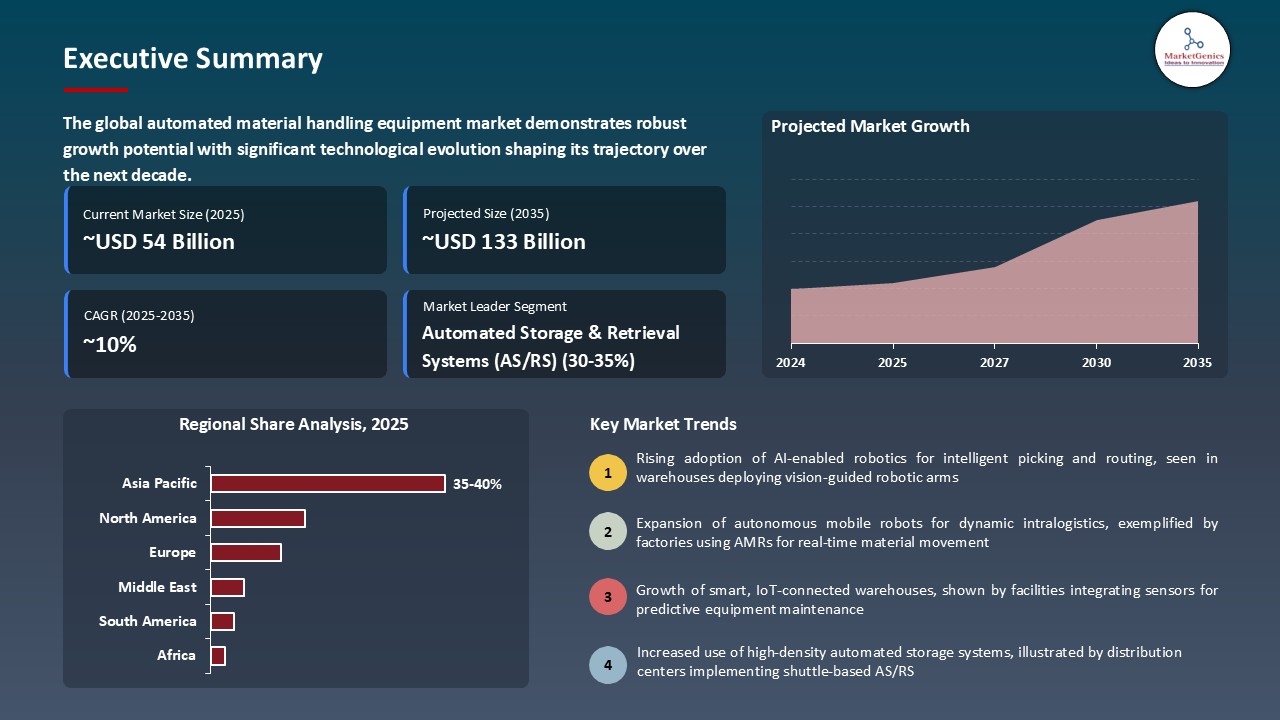

The global automated material handling equipment market is witnessing strong growth, valued at USD 53.7 billion in 2025 and projected to reach USD 133.1 billion by 2035, expanding at a CAGR of 9.5% during the forecast period. The US is the fastest-growing region in the automated material handling equipment market due to rapid warehouse automation, large-scale e-commerce expansion, and strong investments in robotics and smart logistics.

Sandy Stephens, chief strategy officer at Hy-Tek Intralogistics, said, “At Hy-Tek, we build our solutions around what creates the greatest long-term value for our customers, Adding Locus Robotics to our automation portfolio ensures we can deliver scalable, flexible robotics solutions that integrate seamlessly with broader warehouse orchestration strategies. Together, we’re equipping customers to grow with confidence while driving faster ROI”

The adoption of automated material handling equipment is promoted by Industry 4.0 and smart manufacturing projects in which manufacturing companies put automated systems, IoT, and data analytics to improve productivity, intratractability of inventory, and supply chain responsiveness. As an example, in January 2025, KION Group collaborated with NVIDIA and Accenture to build a smart warehouse with AI-controlled autonomous robots and digital twins. The system used NVIDIA Omniverse to optimize operations and simulate them, which allowed planning routes in real-time, automation of tasks, and enhances inventory trackability.

The partnerships between technology developers, manufacturers and logistics firms lead to innovation, product improvement, and market expansion, accelerating automated material handling equipment (AMHE) market growth. An example is the case of Hy-Tek Intralogistics collaborating with Locus Robotics to offer scalable autonomous mobile robots (AMR) warehouse solutions in 2025. Its cooperation provides the possibility to deploy it flexibly, coordinate the fleet in real-time, and deploy AI-based navigation to allow the businesses to achieve a higher level of fulfilling orders, adapt to changing demand, and optimize the work at the warehouse without significant initial investment.

The rising focus on sustainability is providing robust opportunities to energy-efficient AMHE solutions, with companies turning more to low-power robotics, regenerative AS/RS and environmentally friendly automation to lower operational costs and achieve environmental ambitions. A 2025 eBook by OPEX has noted that modern AS/RS systems are adopting regenerative-braking robots, which recapture energy, and that wireless power-management and dense vertical storage to reduce power consumption in the warehouse by a great deal, some systems have gone as far as 50 % less power use than traditional systems.

Automated Material Handling Equipment Market Dynamics and Trends

Driver: E-Commerce Expansion and Omnichannel Fulfillment Requirements

- The automated material handling equipment market is driven by the rapid growth of e-commerce and the emergence of omnichannel retailing. As the consumers become more demanding of shorter delivery times, the warehouses and fulfillment centers are pressured to improve the efficiency, accuracy, and throughput.

- Automated solutions, including conveyor systems, automated storage and retrieval systems (AS/RS), and robotic picking systems, can help businesses to receive orders in large volumes with minimum mistakes and save labor expenses. Moreover, the omnichannel filler strategies are also associated with the process of seamless integration of inventory in several sales channels, which enhances the dependence on sophisticated material handling systems.

- In 2025, Amazon achieved a significant milestone in implementing its one millionth industrial robot into the global fulfillment network that currently has more than 300 plants worldwide. Accompanied by this deployment, Amazon launched a new generative AI foundation model, DeepFleet, which is meant to maximize the movement and coordination of its robotic fleet.

- The AI technology enhances efficiency in the process of travelling by 10%, lowering congestion, quickening the processing of orders, and boosting the delivery speed at minimal operation expenses. Combining AI with automation, Amazon optimizes the productivity of the warehouse, facilitates the functioning of the omnichannel, and provides the ability to manage the growing number of orders in e-commerce, which is an effective example of how advanced material handling technologies can be implemented in practice.

- Developments include the changing nature of the automated material handling equipment market by AI-driven automation providing quicker, more efficient and scalable e-commerce and omnichannel fulfillment.

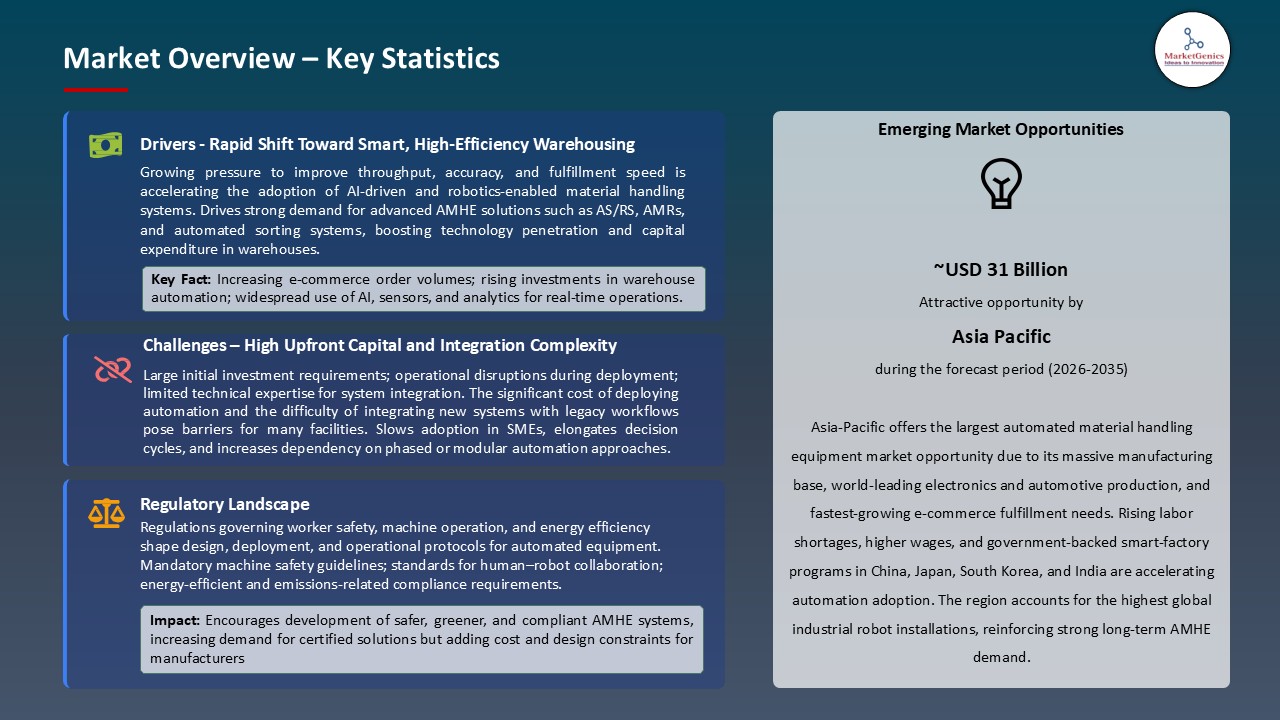

Restraint: High Initial Capital Investment and Integration Complexity

- The automated material handling equipment market is highly held by high initial expenses of sophisticated systems such as conveyors, automated storage and retrieval systems (AS/RS), and robotic picking systems. Small and medium-sized enterprises are usually unable to provide enough budgets to make large-scale automation.

- In addition to the cost, integration complexity is also an issue, where AMHE implementation needs to be compatible with the current warehouse management systems, IT infrastructure, and operational processes without issues. The installation can be used to include customization, training, and temporary down time which adds cost and operational risks.

- Technical skills, especially in high-level AI or robots, are also required, which is sometimes scarce in some areas. These technical and financial obstacles can delay the adoption rates especially by smaller players, limiting the overall adoption of automated material handling solutions even as it brings huge benefits in terms of efficiency, accuracy and scalability to the current warehousing and fulfillment centres.

Opportunity: Automation-as-a-Service and Flexible Deployment Models

- Automated material handling equipment market has a tremendous potential because of the emergence of Automation-as-a-Service (AaaS) and flexible deployment models. These are solutions that lower the initial capital investments and, in the equation, all business parties are able to take advantage of the advanced automation technologies without incurring huge startup costs.

- Flexible deployment allows scaling operations quickly with demand fluctuations to accommodate seasonal changes and e-commerce development. Also, AaaS models provide constantly updated, maintained, and optimized services, by means of which companies can enhance their efficiency in operations and minimize downtime. These models can reduce financial and technical barriers and thus promote the use of automated material handling systems and enable more productive warehouses and support more companies to satisfy the needs of the omnichannel fulfillment.

- As a service enterprise Locus Robotics launched the Robots-as-a-Service (RaaS) model, an autonomous robot’s subscription service, in 2025, allowing warehouses to use autonomous mobile robots without spending a lot of money on their acquisition and deployment. The hardware, software, integration, and support are all part of this flexible solution that allows businesses to scale automation effectively, enhance the productivity of their operations, and adjust quickly to the fluctuating order volumes.

- The automated material handling is becoming easier, more scalable, and efficient with AaaS and flexible deployment models.

Key Trend: Artificial Intelligence and Autonomous Navigation Enhancement

- The adoption of artificial intelligence (AI) and autonomous navigation technologies is one of the primary trends that make the automated material handling equipment market. AI allows robots and automated systems to perform real-time analysis, plan routes, and make smart decisions and enhance the performance of warehouses in terms of efficiency and mistakes.

- Autonomous systems of navigation, such as the LiDAR, computer vision, and machine learning algorithms, enable mobile robots and automated guided vehicles (AGVs) to move safely in dynamic environments, avoiding disturbances and cooperating harmoniously with human employees.

- Brightpick introduced Autopicker 2.0 with in-motion picking and improved AI to make autonomous decisions. The improved system helps in resolving the need to fulfill orders faster and more precisely because the robots can pick objects on the move thereby maximizing warehouse performance, minimizing downtime and enhancing the overall productivity of the operations.

- Developments emphasize that automated material handling equipment market is being changed by AI and autonomous-guided navigation that allows the use of smarter, faster, and more efficient warehouse logistics, fewer errors, and scaling, high-throughput order fulfillment in complex and dynamic environments.

Automated-Material-Handling-Equipment-Market Analysis and Segmental Data

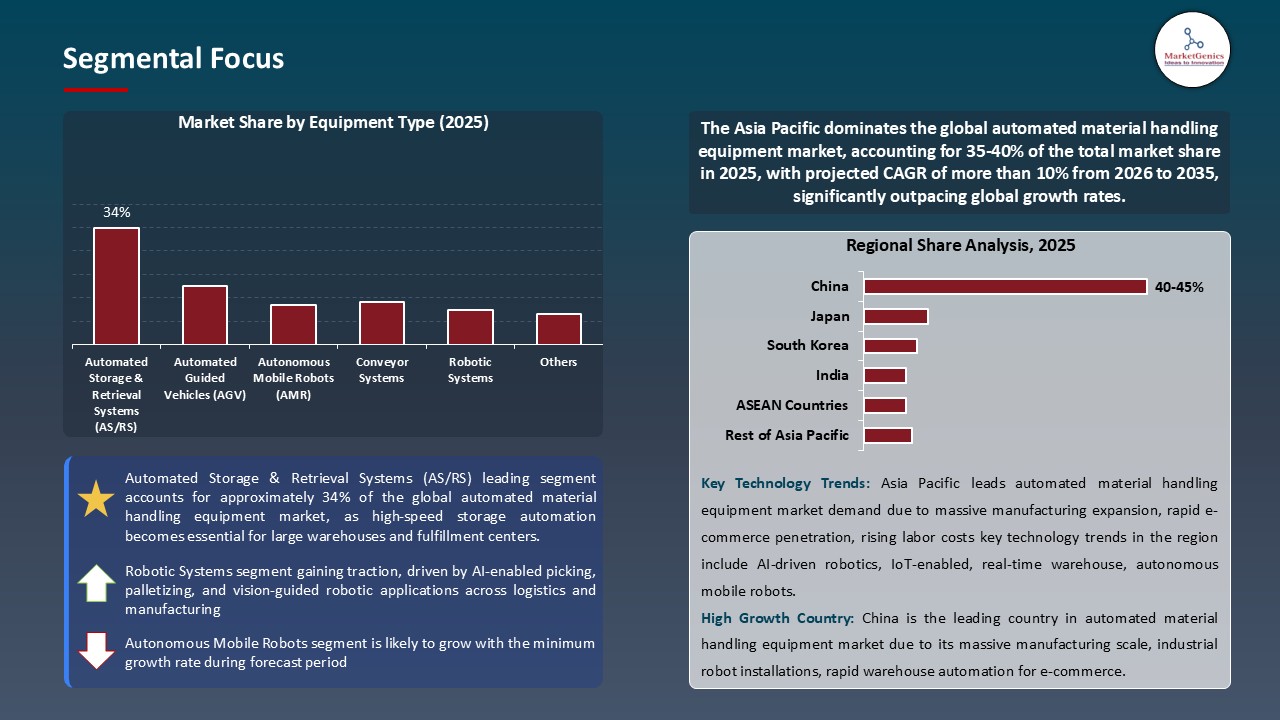

Automated Storage & Retrieval Systems (AS/RS) Dominate Global Automated Material Handling Equipment Market

- Automated Storage and Retrieval Systems (AS/RS) constitute the largest portion of the automated material handling equipment market globally because they are capable of boosting warehouse performance, lowering labour expenses, and maximising storage capacity. These systems provide fast, precise and reliable material processing within the business, and thus they allow companies to cope with increasing demands in e-commerce, manufacturing and retailing industries.

- The growing use of robotics, IoT, and AI technologies in AS/RS enhances the operation visibility, inventory control, and automation of workflows. Also, the fact that AS/RS is flexible to manage product type and volume, makes it a desirable option among the warehouses and distribution centers that expect to operate at higher throughput and costs effectively, which cement its superiority in the AMHE market.

- The first AI-based robotic piece picking solution AutoStore announced in 2025 under Berkshire Grey collaboration was CarouselAI. The system is labor-intensive and is automated, 24/7, and high SKU coverage, which makes the system incredibly efficient in fulfillment. The technology is also available to be embraced by existing users of AutoStore through a retrofit kit without significant infrastructure modifications, with Kardex demonstrations providing live demonstrations of the technology combined with FulfillX warehouse execution system showing a seamless AI-driven automation of the warehouse.

- Innovations underline the fact that AS/RS, which are run by AI and robotics, remain efficient, scalable and innovative in the global automated material handling equipment market.

Asia Pacific Leads Global Automated Material Handling Equipment Market Demand

- Asia Pacific is the most promising market of automated material handling equipment worldwide, due to the blistering industrialization, huge production volumes, and violent implementation of intelligent factory technologies. China, Japan, South Korea, and India are rapidly investing in robotics, IoT-based automation, and high-density warehousing to handle the increasing labor expenses, increase their production efficiency, and satisfy the rising e-commerce fulfilment demands.

- Government support through powerful digital manufacturing initiatives, like the Society 5.0 in Japan, the Made in China 2025 in China, and the Make in India in India, contribute to even faster AMHE deployment. The massive concentration of automotive, electronics, and semiconductor manufacturers in the region is now heavily dependent on the AS/RS systems, AGVs/AMRs and automated conveyors in order to streamline the operations and this makes Asia Pacific the foremost automotive material handling equipment in the world market.

- In April 2025, Daifuku Intralogistics India Pvt. Ltd. opened a new state of the art manufacturing facility in Hyderabad to manufacture the AS/RS systems, pallet sorters, and conveyors locally in India and targeting the Indian market.

- The technological progress, governmental subsidies, and the high volume of industrial usages of automated material handling devices used in Asia Pacific are factors that guarantee its further dominance in the worldwide market of automated material handling equipment.

Automated-Material-Handling-Equipment-Market Ecosystem

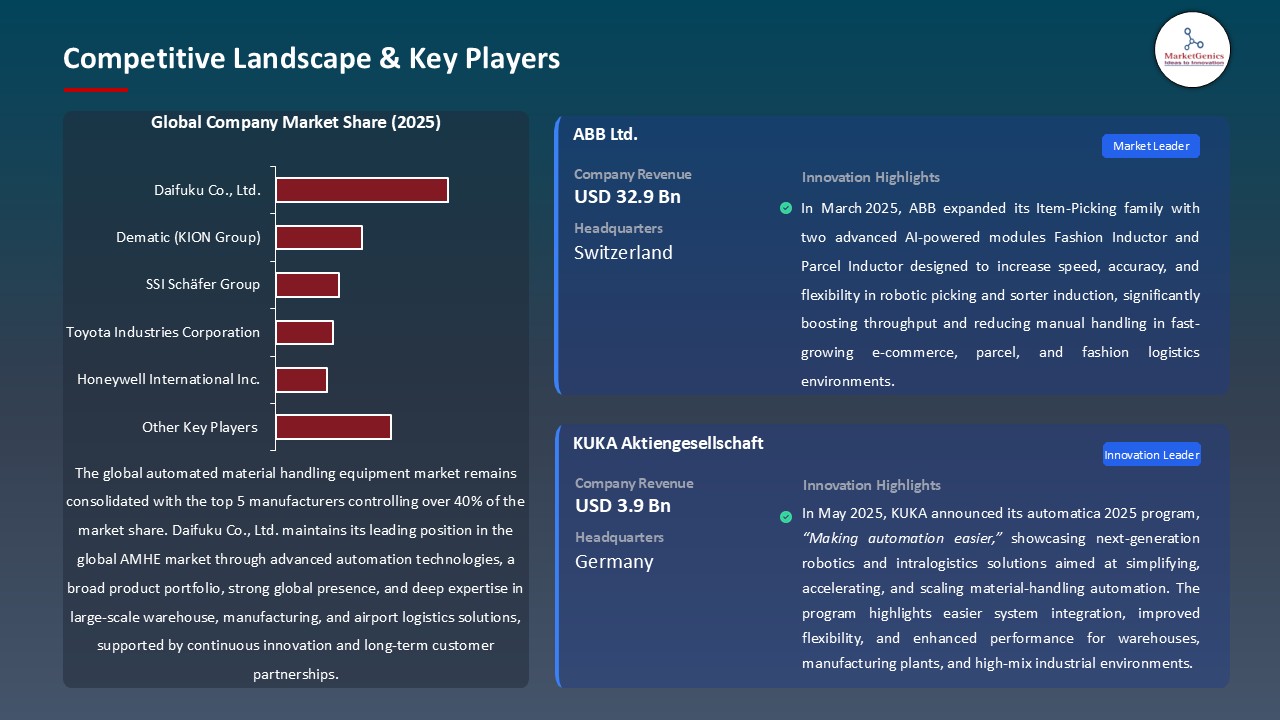

The automated material handling equipment market is centralized globally with Daifuku Co., Ltd., Dematic (KION Group), SSI Schaefer Group, Toyota industries Corporation and Honeywell International Inc. holding approximately 40% of the market. These are the major players in the industry that employ sophisticated automation technology systems, efficient storage and retrieval systems, intelligent robotics systems that streamline the operations of the warehouse, enhance throughput and cut labor expenses. Their capability of powerful research and development as well as their large intellectual property rights and the fact that they have well established global distribution channels make new entrants difficult.

Moreover, it is possible to use strategic collaborations with the logistics companies, e-commerce businesses, and manufacturing corporations that ease the implementation of new AMHE solutions, system integration, and adherence to the industry requirements. These partnerships contribute to faster implementation of automation technologies, increased operational effectiveness, and strengthening the leadership of these large players, which leads to the general development of the market.

Recent Development and Strategic Overview:

- In October 2025, AutoStore, in partnership with Kardex, deployed a fully operational AS/RS system at Balluff’s facility in just six months, installing 20,100 bins, seven Red Line robots, a ConveyorPort, and three CarouselPorts, without major infrastructure modifications, leading to a 177 percent increase in throughput and uninterrupted integration with the SAP system at Balluff.

- In July 2025, Hunkemoller implemented the Shelf-to-Person robots of Geekplus at its Almere distribution center, where 150+ mobile robots will improve the accuracy, speed, and efficiency of picking and storage. The AI-powered system assists with scalable and fast and precise omnichannel order fulfillment in 750 plus stores and e-commerce activities.

Report Scope

|

Detail |

|

|

Market Size in 2025 |

USD 53.7 Bn |

|

Market Forecast Value in 2035 |

USD 133.1 Bn |

|

Growth Rate (CAGR) |

9.5% |

|

Forecast Period |

2026 – 2035 |

|

Historical Data Available for |

2021 – 2024 |

|

Market Size Units |

US$ Billion for Value Thousand Units for Volume |

|

Report Format |

Electronic (PDF) + Excel |

|

North America |

Europe |

Asia Pacific |

Middle East |

Africa |

South America |

|

|

|

|

|

|

|

Companies Covered |

|||||

|

|

|

|

|

|

Automated-Material-Handling-Equipment-Market Segmentation and Highlights

|

Segment |

Sub-segment |

|

Automated Material Handling Equipment Market, By Equipment Type |

|

|

Automated Material Handling Equipment Market, By Technology |

|

|

Automated Material Handling Equipment Market, By Load Capacity |

|

|

Automated Material Handling Equipment Market, By Operation Mode |

|

|

Automated Material Handling Equipment Market, By Function |

|

|

Automated Material Handling Equipment Market, By Ownership Model |

|

|

Automated Material Handling Equipment Market, By Integration Level |

|

|

Automated Material Handling Equipment Market, By Installation Type |

|

|

Automated Material Handling Equipment Market, By End-Use Industry |

|

Frequently Asked Questions

Table of Contents

- 1. Research Methodology and Assumptions

- 1.1. Definitions

- 1.2. Research Design and Approach

- 1.3. Data Collection Methods

- 1.4. Base Estimates and Calculations

- 1.5. Forecasting Models

- 1.5.1. Key Forecast Factors & Impact Analysis

- 1.6. Secondary Research

- 1.6.1. Open Sources

- 1.6.2. Paid Databases

- 1.6.3. Associations

- 1.7. Primary Research

- 1.7.1. Primary Sources

- 1.7.2. Primary Interviews with Stakeholders across Ecosystem

- 2. Executive Summary

- 2.1. Global Automated Material Handling Equipment Market Outlook

- 2.1.1. Automated Material Handling Equipment Market Size (Volume - Thousand Units and Value - US$ Bn), and Forecasts, 2021-2035

- 2.1.2. Compounded Annual Growth Rate Analysis

- 2.1.3. Growth Opportunity Analysis

- 2.1.4. Segmental Share Analysis

- 2.1.5. Geographical Share Analysis

- 2.2. Market Analysis and Facts

- 2.3. Supply-Demand Analysis

- 2.4. Competitive Benchmarking

- 2.5. Go-to- Market Strategy

- 2.5.1. Customer/ End-use Industry Assessment

- 2.5.2. Growth Opportunity Data, 2026-2035

- 2.5.2.1. Regional Data

- 2.5.2.2. Country Data

- 2.5.2.3. Segmental Data

- 2.5.3. Identification of Potential Market Spaces

- 2.5.4. GAP Analysis

- 2.5.5. Potential Attractive Price Points

- 2.5.6. Prevailing Market Risks & Challenges

- 2.5.7. Preferred Sales & Marketing Strategies

- 2.5.8. Key Recommendations and Analysis

- 2.5.9. A Way Forward

- 2.1. Global Automated Material Handling Equipment Market Outlook

- 3. Industry Data and Premium Insights

- 3.1. Global Automation & Process Control Industry Overview, 2025

- 3.1.1. Automation & Process Control Industry Ecosystem Analysis

- 3.1.2. Key Trends for Automation & Process Control Industry

- 3.1.3. Regional Distribution for Automation & Process Control Industry

- 3.2. Supplier Customer Data

- 3.3. Technology Roadmap and Developments

- 3.4. Trade Analysis

- 3.4.1. Import & Export Analysis, 2025

- 3.4.2. Top Importing Countries

- 3.4.3. Top Exporting Countries

- 3.5. Trump Tariff Impact Analysis

- 3.5.1. Manufacturer

- 3.5.1.1. Based on the component & Raw material

- 3.5.2. Supply Chain

- 3.5.3. End Consumer

- 3.5.1. Manufacturer

- 3.6. Raw Material Analysis

- 3.1. Global Automation & Process Control Industry Overview, 2025

- 4. Market Overview

- 4.1. Market Dynamics

- 4.1.1. Drivers

- 4.1.1.1. Growing e-commerce and high-volume warehouse operations

- 4.1.1.2. Rising labor shortages and need for operational efficiency

- 4.1.1.3. Increasing adoption of AI, IoT, and robotics in logistics

- 4.1.2. Restraints

- 4.1.2.1. High initial investment and maintenance costs

- 4.1.2.2. Integration complexity with legacy systems

- 4.1.1. Drivers

- 4.2. Key Trend Analysis

- 4.3. Regulatory Framework

- 4.3.1. Key Regulations, Norms, and Subsidies, by Key Countries

- 4.3.2. Tariffs and Standards

- 4.3.3. Impact Analysis of Regulations on the Market

- 4.4. Value Chain Analysis

- 4.4.1. Component Suppliers

- 4.4.2. Equipment Manufacturers

- 4.4.3. System Integrators

- 4.4.4. Dealers/ Distributors

- 4.4.5. End Users/ Customers

- 4.5. Porter’s Five Forces Analysis

- 4.6. PESTEL Analysis

- 4.7. Global Automated Material Handling Equipment Market Demand

- 4.7.1. Historical Market Size – Volume (Thousand Units) and Value (US$ Bn), 2020-2024

- 4.7.2. Current and Future Market Size – Volume (Thousand Units) and Value (US$ Bn), 2026–2035

- 4.7.2.1. Y-o-Y Growth Trends

- 4.7.2.2. Absolute $ Opportunity Assessment

- 4.1. Market Dynamics

- 5. Competition Landscape

- 5.1. Competition structure

- 5.1.1. Fragmented v/s consolidated

- 5.2. Company Share Analysis, 2025

- 5.2.1. Global Company Market Share

- 5.2.2. By Region

- 5.2.2.1. North America

- 5.2.2.2. Europe

- 5.2.2.3. Asia Pacific

- 5.2.2.4. Middle East

- 5.2.2.5. Africa

- 5.2.2.6. South America

- 5.3. Product Comparison Matrix

- 5.3.1. Specifications

- 5.3.2. Market Positioning

- 5.3.3. Pricing

- 5.1. Competition structure

- 6. Global Automated Material Handling Equipment Market Analysis, By Equipment Type

- 6.1. Key Segment Analysis

- 6.2. Automated Material Handling Equipment Market Size (Volume - Thousand Units and Value - US$ Bn), Analysis, and Forecasts, By Equipment Type, 2021-2035

- 6.2.1. Automated Storage & Retrieval Systems (AS/RS)

- 6.2.1.1. Unit Load AS/RS

- 6.2.1.2. Mini Load AS/RS

- 6.2.1.3. Vertical Lift Modules (VLM)

- 6.2.1.4. Horizontal Carousels

- 6.2.1.5. Vertical Carousels

- 6.2.1.6. Others

- 6.2.2. Automated Guided Vehicles (AGV)

- 6.2.2.1. Tow Vehicles

- 6.2.2.2. Unit Load Carriers

- 6.2.2.3. Pallet Trucks

- 6.2.2.4. Assembly Line Vehicles

- 6.2.2.5. Forklift AGVs

- 6.2.2.6. Others

- 6.2.3. Autonomous Mobile Robots (AMR)

- 6.2.3.1. Goods-to-Person AMRs

- 6.2.3.2. Collaborative AMRs

- 6.2.3.3. Heavy Load AMRs

- 6.2.3.4. Others

- 6.2.4. Conveyor Systems

- 6.2.4.1. Belt Conveyors

- 6.2.4.2. Roller Conveyors

- 6.2.4.3. Overhead Conveyors

- 6.2.4.4. Pallet Conveyors

- 6.2.4.5. Chain Conveyors

- 6.2.4.6. Others

- 6.2.5. Robotic Systems

- 6.2.5.1. Articulated Robots

- 6.2.5.2. SCARA Robots

- 6.2.5.3. Cartesian Robots

- 6.2.5.4. Collaborative Robots (Cobots)

- 6.2.5.5. Delta Robots

- 6.2.5.6. Others

- 6.2.6. Palletizers & Depalletizers

- 6.2.6.1. Conventional Palletizers

- 6.2.6.2. Robotic Palletizers

- 6.2.6.3. Layer Palletizers

- 6.2.6.4. Others

- 6.2.7. Sortation Systems

- 6.2.7.1. Cross-Belt Sorters

- 6.2.7.2. Tilt-Tray Sorters

- 6.2.7.3. Sliding Shoe Sorters

- 6.2.7.4. Bomb-Bay Sorters

- 6.2.7.5. Others

- 6.2.8. Cranes & Hoists

- 6.2.8.1. Overhead Cranes

- 6.2.8.2. Gantry Cranes

- 6.2.8.3. Jib Cranes

- 6.2.8.4. Monorail Cranes

- 6.2.8.5. Others

- 6.2.9. Other Equipment Type

- 6.2.1. Automated Storage & Retrieval Systems (AS/RS)

- 7. Global Automated Material Handling Equipment Market Analysis, By Technology

- 7.1. Key Segment Analysis

- 7.2. Automated Material Handling Equipment Market Size (Volume - Thousand Units and Value - US$ Bn), Analysis, and Forecasts, By Technology, 2021-2035

- 7.2.1. Navigation Technology

- 7.2.1.1. Laser Guided

- 7.2.1.2. Magnetic Guided

- 7.2.1.3. Vision Guided

- 7.2.1.4. Inductive Guided

- 7.2.1.5. Natural Navigation

- 7.2.1.6. Others

- 7.2.2. Control Systems

- 7.2.2.1. Warehouse Management Systems (WMS)

- 7.2.2.2. Warehouse Control Systems (WCS)

- 7.2.2.3. Transportation Management Systems (TMS)

- 7.2.2.4. Enterprise Resource Planning (ERP) Integration

- 7.2.2.5. Others

- 7.2.3. Power Source

- 7.2.3.1. Battery Powered (Lithium-ion)

- 7.2.3.2. Battery Powered (Lead-acid)

- 7.2.3.3. Fuel Cell Powered

- 7.2.3.4. Hybrid Systems

- 7.2.3.5. Others

- 7.2.4. Connectivity

- 7.2.4.1. IoT Enabled

- 7.2.4.2. 5G Connected

- 7.2.4.3. Cloud-Based Systems

- 7.2.4.4. Edge Computing

- 7.2.4.5. Others

- 7.2.5. Emerging Technologies

- 7.2.1. Navigation Technology

- 8. Global Automated Material Handling Equipment Market Analysis,By Load Capacity

- 8.1. Key Segment Analysis

- 8.2. Automated Material Handling Equipment Market Size (Volume - Thousand Units and Value - US$ Bn), Analysis, and Forecasts, By Load Capacity, 2021-2035

- 8.2.1. Up to 500 kg

- 8.2.2. 500 kg - 2,000 kg

- 8.2.3. 2,000 kg - 10,000 kg

- 8.2.4. Above 10,000 kg

- 9. Global Automated Material Handling Equipment Market Analysis, By Operation Mode

- 9.1. Key Segment Analysis

- 9.2. Automated Material Handling Equipment Market Size (Volume - Thousand Units and Value - US$ Bn), Analysis, and Forecasts, By Operation Mode, 2021-2035

- 9.2.1. Fully Automated

- 9.2.2. Semi-Automated

- 9.2.3. Manual with Automation Assistance

- 10. Global Automated Material Handling Equipment Market Analysis, By Function

- 10.1. Key Segment Analysis

- 10.2. Automated Material Handling Equipment Market Size (Volume - Thousand Units and Value - US$ Bn), Analysis, and Forecasts, By Function, 2021-2035

- 10.2.1. Storage

- 10.2.2. Transportation

- 10.2.3. Assembly

- 10.2.4. Packaging

- 10.2.5. Picking & Placing

- 10.2.6. Sorting & Distribution

- 10.2.7. Loading & Unloading

- 11. Global Automated Material Handling Equipment Market Analysis, By Ownership Model

- 11.1. Key Segment Analysis

- 11.2. Automated Material Handling Equipment Market Size (Volume - Thousand Units and Value - US$ Bn), Analysis, and Forecasts, By Ownership Model, 2021-2035

- 11.2.1. Purchase/Capital Investment

- 11.2.2. Rental/Lease

- 11.2.3. Robotics-as-a-Service (RaaS)

- 12. Global Automated Material Handling Equipment Market Analysis, By Integration Level

- 12.1. Key Segment Analysis

- 12.2. Automated Material Handling Equipment Market Size (Volume - Thousand Units and Value - US$ Bn), Analysis, and Forecasts, By Integration Level, 2021-2035

- 12.2.1. Standalone Systems

- 12.2.2. Partially Integrated Systems

- 12.2.3. Fully Integrated Systems

- 13. Global Automated Material Handling Equipment Market Analysis, By Installation Type

- 13.1. Key Segment Analysis

- 13.2. Automated Material Handling Equipment Market Size (Volume - Thousand Units and Value - US$ Bn), Analysis, and Forecasts, By Installation Type, 2021-2035

- 13.2.1. New Installation

- 13.2.2. Retrofit/Upgrade

- 14. Global Automated Material Handling Equipment Market Analysis, By End-Use Industry

- 14.1. Key Segment Analysis

- 14.2. Automated Material Handling Equipment Market Size (Volume - Thousand Units and Value - US$ Bn), Analysis, and Forecasts, By End-Use Industry, 2021-2035

- 14.2.1. Manufacturing Industry

- 14.2.1.1. Raw Material Handling

- 14.2.1.2. Work-in-Process Movement

- 14.2.1.3. Finished Goods Storage

- 14.2.1.4. Assembly Line Feeding

- 14.2.1.5. Quality Control Transportation

- 14.2.1.6. Packaging Operations

- 14.2.1.7. Others

- 14.2.2. E-commerce & Retail

- 14.2.2.1. Order Fulfillment

- 14.2.2.2. Warehouse Storage

- 14.2.2.3. Product Sorting

- 14.2.2.4. Returns Processing

- 14.2.2.5. Cross-Docking Operations

- 14.2.2.6. Last-Mile Distribution Center Operations

- 14.2.2.7. Others

- 14.2.3. Logistics & Warehousing

- 14.2.3.1. Inbound Receiving

- 14.2.3.2. Put-Away Operations

- 14.2.3.3. Order Picking

- 14.2.3.4. Packing & Shipping

- 14.2.3.5. Inventory Management

- 14.2.3.6. Cross-Docking

- 14.2.3.7. Others

- 14.2.4. Automotive

- 14.2.4.1. Parts Storage & Retrieval

- 14.2.4.2. Assembly Line Material Supply

- 14.2.4.3. Finished Vehicle Storage

- 14.2.4.4. Component Sequencing

- 14.2.4.5. Paint Shop Material Handling

- 14.2.4.6. Tire & Wheel Handling

- 14.2.4.7. Others

- 14.2.5. Food & Beverage

- 14.2.5.1. Cold Storage Operations

- 14.2.5.2. Ingredient Handling

- 14.2.5.3. Finished Product Distribution

- 14.2.5.4. Palletizing & Depalletizing

- 14.2.5.5. Order Picking for Distribution

- 14.2.5.6. Temperature-Controlled Transportation

- 14.2.5.7. Others

- 14.2.6. Pharmaceutical & Healthcare

- 14.2.6.1. Drug Storage & Retrieval

- 14.2.6.2. Cold Chain Management

- 14.2.6.3. Order Fulfillment

- 14.2.6.4. Cleanroom Material Handling

- 14.2.6.5. Medical Device Assembly

- 14.2.6.6. Hospital Logistics

- 14.2.6.7. Others

- 14.2.7. Aviation

- 14.2.7.1. Baggage Handling

- 14.2.7.2. Cargo Sorting

- 14.2.7.3. Aircraft Component Storage

- 14.2.7.4. Ground Support Equipment Movement

- 14.2.7.5. Maintenance Part Distribution

- 14.2.7.6. Others

- 14.2.8. Chemicals

- 14.2.8.1. Raw Material Handling

- 14.2.8.2. Hazardous Material Storage

- 14.2.8.3. Finished Product Distribution

- 14.2.8.4. Drum & Container Handling

- 14.2.8.5. Mixing & Blending Support

- 14.2.8.6. Others

- 14.2.9. Electronics & Semiconductors

- 14.2.9.1. Cleanroom Material Transport

- 14.2.9.2. Component Storage

- 14.2.9.3. Assembly Line Supply

- 14.2.9.4. Testing Equipment Handling

- 14.2.9.5. Finished Product Distribution

- 14.2.9.6. Others

- 14.2.10. Textile & Apparel

- 14.2.10.1. Fabric Roll Handling

- 14.2.10.2. Garment Sorting

- 14.2.10.3. Order Fulfillment

- 14.2.10.4. Warehouse Storage

- 14.2.10.5. Distribution Center Operations

- 14.2.10.6. Others

- 14.2.11. Metals & Heavy Machinery

- 14.2.11.1. Metal Sheet Handling

- 14.2.11.2. Coil Storage & Retrieval

- 14.2.11.3. Heavy Component Movement

- 14.2.11.4. Warehouse Operations

- 14.2.11.5. Scrap Material Handling

- 14.2.11.6. Others

- 14.2.12. Third-Party Logistics (3PL)

- 14.2.12.1. Multi-Client Warehousing

- 14.2.12.2. Cross-Docking Operations

- 14.2.12.3. Order Fulfillment Services

- 14.2.12.4. Reverse Logistics

- 14.2.12.5. Value-Added Services

- 14.2.12.6. Others

- 14.2.13. Other Industries

- 14.2.1. Manufacturing Industry

- 15. Global Automated Material Handling Equipment Market Analysis and Forecasts, by Region

- 15.1. Key Findings

- 15.2. Automated Material Handling Equipment Market Size (Volume - Thousand Units and Value - US$ Bn), Analysis, and Forecasts, by Region, 2021-2035

- 15.2.1. North America

- 15.2.2. Europe

- 15.2.3. Asia Pacific

- 15.2.4. Middle East

- 15.2.5. Africa

- 15.2.6. South America

- 16. North America Automated Material Handling Equipment Market Analysis

- 16.1. Key Segment Analysis

- 16.2. Regional Snapshot

- 16.3. North America Automated Material Handling Equipment Market Size (Volume - Thousand Units and Value - US$ Bn), Analysis, and Forecasts, 2021-2035

- 16.3.1. Equipment Type

- 16.3.2. Technology

- 16.3.3. Load Capacity

- 16.3.4. Operation Mode

- 16.3.5. Function

- 16.3.6. Ownership Model

- 16.3.7. Integration Level

- 16.3.8. Installation Type

- 16.3.9. End-Use Industry

- 16.3.10. Country

- 16.3.10.1. USA

- 16.3.10.2. Canada

- 16.3.10.3. Mexico

- 16.4. USA Automated Material Handling Equipment Market

- 16.4.1. Country Segmental Analysis

- 16.4.2. Equipment Type

- 16.4.3. Technology

- 16.4.4. Load Capacity

- 16.4.5. Operation Mode

- 16.4.6. Function

- 16.4.7. Ownership Model

- 16.4.8. Integration Level

- 16.4.9. Installation Type

- 16.4.10. End-Use Industry

- 16.5. Canada Automated Material Handling Equipment Market

- 16.5.1. Country Segmental Analysis

- 16.5.2. Equipment Type

- 16.5.3. Technology

- 16.5.4. Load Capacity

- 16.5.5. Operation Mode

- 16.5.6. Function

- 16.5.7. Ownership Model

- 16.5.8. Integration Level

- 16.5.9. Installation Type

- 16.5.10. End-Use Industry

- 16.6. Mexico Automated Material Handling Equipment Market

- 16.6.1. Country Segmental Analysis

- 16.6.2. Equipment Type

- 16.6.3. Technology

- 16.6.4. Load Capacity

- 16.6.5. Operation Mode

- 16.6.6. Function

- 16.6.7. Ownership Model

- 16.6.8. Integration Level

- 16.6.9. Installation Type

- 16.6.10. End-Use Industry

- 17. Europe Automated Material Handling Equipment Market Analysis

- 17.1. Key Segment Analysis

- 17.2. Regional Snapshot

- 17.3. Europe Automated Material Handling Equipment Market Size (Volume - Thousand Units and Value - US$ Bn), Analysis, and Forecasts, 2021-2035

- 17.3.1. Equipment Type

- 17.3.2. Technology

- 17.3.3. Load Capacity

- 17.3.4. Operation Mode

- 17.3.5. Function

- 17.3.6. Ownership Model

- 17.3.7. Integration Level

- 17.3.8. Installation Type

- 17.3.9. End-Use Industry

- 17.3.10. Country

- 17.3.10.1. Germany

- 17.3.10.2. United Kingdom

- 17.3.10.3. France

- 17.3.10.4. Italy

- 17.3.10.5. Spain

- 17.3.10.6. Netherlands

- 17.3.10.7. Nordic Countries

- 17.3.10.8. Poland

- 17.3.10.9. Russia & CIS

- 17.3.10.10. Rest of Europe

- 17.4. Germany Automated Material Handling Equipment Market

- 17.4.1. Country Segmental Analysis

- 17.4.2. Equipment Type

- 17.4.3. Technology

- 17.4.4. Load Capacity

- 17.4.5. Operation Mode

- 17.4.6. Function

- 17.4.7. Ownership Model

- 17.4.8. Integration Level

- 17.4.9. Installation Type

- 17.4.10. End-Use Industry

- 17.5. United Kingdom Automated Material Handling Equipment Market

- 17.5.1. Country Segmental Analysis

- 17.5.2. Equipment Type

- 17.5.3. Technology

- 17.5.4. Load Capacity

- 17.5.5. Operation Mode

- 17.5.6. Function

- 17.5.7. Ownership Model

- 17.5.8. Integration Level

- 17.5.9. Installation Type

- 17.5.10. End-Use Industry

- 17.6. France Automated Material Handling Equipment Market

- 17.6.1. Country Segmental Analysis

- 17.6.2. Equipment Type

- 17.6.3. Technology

- 17.6.4. Load Capacity

- 17.6.5. Operation Mode

- 17.6.6. Function

- 17.6.7. Ownership Model

- 17.6.8. Integration Level

- 17.6.9. Installation Type

- 17.6.10. End-Use Industry

- 17.7. Italy Automated Material Handling Equipment Market

- 17.7.1. Country Segmental Analysis

- 17.7.2. Equipment Type

- 17.7.3. Technology

- 17.7.4. Load Capacity

- 17.7.5. Operation Mode

- 17.7.6. Function

- 17.7.7. Ownership Model

- 17.7.8. Integration Level

- 17.7.9. Installation Type

- 17.7.10. End-Use Industry

- 17.8. Spain Automated Material Handling Equipment Market

- 17.8.1. Country Segmental Analysis

- 17.8.2. Equipment Type

- 17.8.3. Technology

- 17.8.4. Load Capacity

- 17.8.5. Operation Mode

- 17.8.6. Function

- 17.8.7. Ownership Model

- 17.8.8. Integration Level

- 17.8.9. Installation Type

- 17.8.10. End-Use Industry

- 17.9. Netherlands Automated Material Handling Equipment Market

- 17.9.1. Country Segmental Analysis

- 17.9.2. Equipment Type

- 17.9.3. Technology

- 17.9.4. Load Capacity

- 17.9.5. Operation Mode

- 17.9.6. Function

- 17.9.7. Ownership Model

- 17.9.8. Integration Level

- 17.9.9. Installation Type

- 17.9.10. End-Use Industry

- 17.10. Nordic Countries Automated Material Handling Equipment Market

- 17.10.1. Country Segmental Analysis

- 17.10.2. Equipment Type

- 17.10.3. Technology

- 17.10.4. Load Capacity

- 17.10.5. Operation Mode

- 17.10.6. Function

- 17.10.7. Ownership Model

- 17.10.8. Integration Level

- 17.10.9. Installation Type

- 17.10.10. End-Use Industry

- 17.11. Poland Automated Material Handling Equipment Market

- 17.11.1. Country Segmental Analysis

- 17.11.2. Equipment Type

- 17.11.3. Technology

- 17.11.4. Load Capacity

- 17.11.5. Operation Mode

- 17.11.6. Function

- 17.11.7. Ownership Model

- 17.11.8. Integration Level

- 17.11.9. Installation Type

- 17.11.10. End-Use Industry

- 17.12. Russia & CIS Automated Material Handling Equipment Market

- 17.12.1. Country Segmental Analysis

- 17.12.2. Equipment Type

- 17.12.3. Technology

- 17.12.4. Load Capacity

- 17.12.5. Operation Mode

- 17.12.6. Function

- 17.12.7. Ownership Model

- 17.12.8. Integration Level

- 17.12.9. Installation Type

- 17.12.10. End-Use Industry

- 17.13. Rest of Europe Automated Material Handling Equipment Market

- 17.13.1. Country Segmental Analysis

- 17.13.2. Equipment Type

- 17.13.3. Technology

- 17.13.4. Load Capacity

- 17.13.5. Operation Mode

- 17.13.6. Function

- 17.13.7. Ownership Model

- 17.13.8. Integration Level

- 17.13.9. Installation Type

- 17.13.10. End-Use Industry

- 18. Asia Pacific Automated Material Handling Equipment Market Analysis

- 18.1. Key Segment Analysis

- 18.2. Regional Snapshot

- 18.3. Asia Pacific Automated Material Handling Equipment Market Size (Volume - Thousand Units and Value - US$ Bn), Analysis, and Forecasts, 2021-2035

- 18.3.1. Equipment Type

- 18.3.2. Technology

- 18.3.3. Load Capacity

- 18.3.4. Operation Mode

- 18.3.5. Function

- 18.3.6. Ownership Model

- 18.3.7. Integration Level

- 18.3.8. Installation Type

- 18.3.9. End-Use Industry

- 18.3.10. Country

- 18.3.10.1. China

- 18.3.10.2. India

- 18.3.10.3. Japan

- 18.3.10.4. South Korea

- 18.3.10.5. Australia and New Zealand

- 18.3.10.6. Indonesia

- 18.3.10.7. Malaysia

- 18.3.10.8. Thailand

- 18.3.10.9. Vietnam

- 18.3.10.10. Rest of Asia Pacific

- 18.4. China Automated Material Handling Equipment Market

- 18.4.1. Country Segmental Analysis

- 18.4.2. Equipment Type

- 18.4.3. Technology

- 18.4.4. Load Capacity

- 18.4.5. Operation Mode

- 18.4.6. Function

- 18.4.7. Ownership Model

- 18.4.8. Integration Level

- 18.4.9. Installation Type

- 18.4.10. End-Use Industry

- 18.5. India Automated Material Handling Equipment Market

- 18.5.1. Country Segmental Analysis

- 18.5.2. Equipment Type

- 18.5.3. Technology

- 18.5.4. Load Capacity

- 18.5.5. Operation Mode

- 18.5.6. Function

- 18.5.7. Ownership Model

- 18.5.8. Integration Level

- 18.5.9. Installation Type

- 18.5.10. End-Use Industry

- 18.6. Japan Automated Material Handling Equipment Market

- 18.6.1. Country Segmental Analysis

- 18.6.2. Equipment Type

- 18.6.3. Technology

- 18.6.4. Load Capacity

- 18.6.5. Operation Mode

- 18.6.6. Function

- 18.6.7. Ownership Model

- 18.6.8. Integration Level

- 18.6.9. Installation Type

- 18.6.10. End-Use Industry

- 18.7. South Korea Automated Material Handling Equipment Market

- 18.7.1. Country Segmental Analysis

- 18.7.2. Equipment Type

- 18.7.3. Technology

- 18.7.4. Load Capacity

- 18.7.5. Operation Mode

- 18.7.6. Function

- 18.7.7. Ownership Model

- 18.7.8. Integration Level

- 18.7.9. Installation Type

- 18.7.10. End-Use Industry

- 18.8. Australia and New Zealand Automated Material Handling Equipment Market

- 18.8.1. Country Segmental Analysis

- 18.8.2. Equipment Type

- 18.8.3. Technology

- 18.8.4. Load Capacity

- 18.8.5. Operation Mode

- 18.8.6. Function

- 18.8.7. Ownership Model

- 18.8.8. Integration Level

- 18.8.9. Installation Type

- 18.8.10. End-Use Industry

- 18.9. Indonesia Automated Material Handling Equipment Market

- 18.9.1. Country Segmental Analysis

- 18.9.2. Equipment Type

- 18.9.3. Technology

- 18.9.4. Load Capacity

- 18.9.5. Operation Mode

- 18.9.6. Function

- 18.9.7. Ownership Model

- 18.9.8. Integration Level

- 18.9.9. Installation Type

- 18.9.10. End-Use Industry

- 18.10. Malaysia Automated Material Handling Equipment Market

- 18.10.1. Country Segmental Analysis

- 18.10.2. Equipment Type

- 18.10.3. Technology

- 18.10.4. Load Capacity

- 18.10.5. Operation Mode

- 18.10.6. Function

- 18.10.7. Ownership Model

- 18.10.8. Integration Level

- 18.10.9. Installation Type

- 18.10.10. End-Use Industry

- 18.11. Thailand Automated Material Handling Equipment Market

- 18.11.1. Country Segmental Analysis

- 18.11.2. Equipment Type

- 18.11.3. Technology

- 18.11.4. Load Capacity

- 18.11.5. Operation Mode

- 18.11.6. Function

- 18.11.7. Ownership Model

- 18.11.8. Integration Level

- 18.11.9. Installation Type

- 18.11.10. End-Use Industry

- 18.12. Vietnam Automated Material Handling Equipment Market

- 18.12.1. Country Segmental Analysis

- 18.12.2. Equipment Type

- 18.12.3. Technology

- 18.12.4. Load Capacity

- 18.12.5. Operation Mode

- 18.12.6. Function

- 18.12.7. Ownership Model

- 18.12.8. Integration Level

- 18.12.9. Installation Type

- 18.12.10. End-Use Industry

- 18.13. Rest of Asia Pacific Automated Material Handling Equipment Market

- 18.13.1. Country Segmental Analysis

- 18.13.2. Equipment Type

- 18.13.3. Technology

- 18.13.4. Load Capacity

- 18.13.5. Operation Mode

- 18.13.6. Function

- 18.13.7. Ownership Model

- 18.13.8. Integration Level

- 18.13.9. Installation Type

- 18.13.10. End-Use Industry

- 19. Middle East Automated Material Handling Equipment Market Analysis

- 19.1. Key Segment Analysis

- 19.2. Regional Snapshot

- 19.3. Middle East Automated Material Handling Equipment Market Size (Volume - Thousand Units and Value - US$ Bn), Analysis, and Forecasts, 2021-2035

- 19.3.1. Equipment Type

- 19.3.2. Technology

- 19.3.3. Load Capacity

- 19.3.4. Operation Mode

- 19.3.5. Function

- 19.3.6. Ownership Model

- 19.3.7. Integration Level

- 19.3.8. Installation Type

- 19.3.9. End-Use Industry

- 19.3.10. Country

- 19.3.10.1. Turkey

- 19.3.10.2. UAE

- 19.3.10.3. Saudi Arabia

- 19.3.10.4. Israel

- 19.3.10.5. Rest of Middle East

- 19.4. Turkey Automated Material Handling Equipment Market

- 19.4.1. Country Segmental Analysis

- 19.4.2. Equipment Type

- 19.4.3. Technology

- 19.4.4. Load Capacity

- 19.4.5. Operation Mode

- 19.4.6. Function

- 19.4.7. Ownership Model

- 19.4.8. Integration Level

- 19.4.9. Installation Type

- 19.4.10. End-Use Industry

- 19.5. UAE Automated Material Handling Equipment Market

- 19.5.1. Country Segmental Analysis

- 19.5.2. Equipment Type

- 19.5.3. Technology

- 19.5.4. Load Capacity

- 19.5.5. Operation Mode

- 19.5.6. Function

- 19.5.7. Ownership Model

- 19.5.8. Integration Level

- 19.5.9. Installation Type

- 19.5.10. End-Use Industry

- 19.6. Saudi Arabia Automated Material Handling Equipment Market

- 19.6.1. Country Segmental Analysis

- 19.6.2. Equipment Type

- 19.6.3. Technology

- 19.6.4. Load Capacity

- 19.6.5. Operation Mode

- 19.6.6. Function

- 19.6.7. Ownership Model

- 19.6.8. Integration Level

- 19.6.9. Installation Type

- 19.6.10. End-Use Industry

- 19.7. Israel Automated Material Handling Equipment Market

- 19.7.1. Country Segmental Analysis

- 19.7.2. Equipment Type

- 19.7.3. Technology

- 19.7.4. Load Capacity

- 19.7.5. Operation Mode

- 19.7.6. Function

- 19.7.7. Ownership Model

- 19.7.8. Integration Level

- 19.7.9. Installation Type

- 19.7.10. End-Use Industry

- 19.8. Rest of Middle East Automated Material Handling Equipment Market

- 19.8.1. Country Segmental Analysis

- 19.8.2. Equipment Type

- 19.8.3. Technology

- 19.8.4. Load Capacity

- 19.8.5. Operation Mode

- 19.8.6. Function

- 19.8.7. Ownership Model

- 19.8.8. Integration Level

- 19.8.9. Installation Type

- 19.8.10. End-Use Industry

- 20. Africa Automated Material Handling Equipment Market Analysis

- 20.1. Key Segment Analysis

- 20.2. Regional Snapshot

- 20.3. Africa Automated Material Handling Equipment Market Size (Volume - Thousand Units and Value - US$ Bn), Analysis, and Forecasts, 2021-2035

- 20.3.1. Equipment Type

- 20.3.2. Technology

- 20.3.3. Load Capacity

- 20.3.4. Operation Mode

- 20.3.5. Function

- 20.3.6. Ownership Model

- 20.3.7. Integration Level

- 20.3.8. Installation Type

- 20.3.9. End-Use Industry

- 20.3.10. Country

- 20.3.10.1. South Africa

- 20.3.10.2. Egypt

- 20.3.10.3. Nigeria

- 20.3.10.4. Algeria

- 20.3.10.5. Rest of Africa

- 20.4. South Africa Automated Material Handling Equipment Market

- 20.4.1. Country Segmental Analysis

- 20.4.2. Equipment Type

- 20.4.3. Technology

- 20.4.4. Load Capacity

- 20.4.5. Operation Mode

- 20.4.6. Function

- 20.4.7. Ownership Model

- 20.4.8. Integration Level

- 20.4.9. Installation Type

- 20.4.10. End-Use Industry

- 20.5. Egypt Automated Material Handling Equipment Market

- 20.5.1. Country Segmental Analysis

- 20.5.2. Equipment Type

- 20.5.3. Technology

- 20.5.4. Load Capacity

- 20.5.5. Operation Mode

- 20.5.6. Function

- 20.5.7. Ownership Model

- 20.5.8. Integration Level

- 20.5.9. Installation Type

- 20.5.10. End-Use Industry

- 20.6. Nigeria Automated Material Handling Equipment Market

- 20.6.1. Country Segmental Analysis

- 20.6.2. Equipment Type

- 20.6.3. Technology

- 20.6.4. Load Capacity

- 20.6.5. Operation Mode

- 20.6.6. Function

- 20.6.7. Ownership Model

- 20.6.8. Integration Level

- 20.6.9. Installation Type

- 20.6.10. End-Use Industry

- 20.7. Algeria Automated Material Handling Equipment Market

- 20.7.1. Country Segmental Analysis

- 20.7.2. Equipment Type

- 20.7.3. Technology

- 20.7.4. Load Capacity

- 20.7.5. Operation Mode

- 20.7.6. Function

- 20.7.7. Ownership Model

- 20.7.8. Integration Level

- 20.7.9. Installation Type

- 20.7.10. End-Use Industry

- 20.8. Rest of Africa Automated Material Handling Equipment Market

- 20.8.1. Country Segmental Analysis

- 20.8.2. Equipment Type

- 20.8.3. Technology

- 20.8.4. Load Capacity

- 20.8.5. Operation Mode

- 20.8.6. Function

- 20.8.7. Ownership Model

- 20.8.8. Integration Level

- 20.8.9. Installation Type

- 20.8.10. End-Use Industry

- 21. South America Automated Material Handling Equipment Market Analysis

- 21.1. Key Segment Analysis

- 21.2. Regional Snapshot

- 21.3. South America Automated Material Handling Equipment Market Size (Volume - Thousand Units and Value - US$ Bn), Analysis, and Forecasts, 2021-2035

- 21.3.1. Equipment Type

- 21.3.2. Technology

- 21.3.3. Load Capacity

- 21.3.4. Operation Mode

- 21.3.5. Function

- 21.3.6. Ownership Model

- 21.3.7. Integration Level

- 21.3.8. Installation Type

- 21.3.9. End-Use Industry

- 21.3.10. Country

- 21.3.10.1. Brazil

- 21.3.10.2. Argentina

- 21.3.10.3. Rest of South America

- 21.4. Brazil Automated Material Handling Equipment Market

- 21.4.1. Country Segmental Analysis

- 21.4.2. Equipment Type

- 21.4.3. Technology

- 21.4.4. Load Capacity

- 21.4.5. Operation Mode

- 21.4.6. Function

- 21.4.7. Ownership Model

- 21.4.8. Integration Level

- 21.4.9. Installation Type

- 21.4.10. End-Use Industry

- 21.5. Argentina Automated Material Handling Equipment Market

- 21.5.1. Country Segmental Analysis

- 21.5.2. Equipment Type

- 21.5.3. Technology

- 21.5.4. Load Capacity

- 21.5.5. Operation Mode

- 21.5.6. Function

- 21.5.7. Ownership Model

- 21.5.8. Integration Level

- 21.5.9. Installation Type

- 21.5.10. End-Use Industry

- 21.6. Rest of South America Automated Material Handling Equipment Market

- 21.6.1. Country Segmental Analysis

- 21.6.2. Equipment Type

- 21.6.3. Technology

- 21.6.4. Load Capacity

- 21.6.5. Operation Mode

- 21.6.6. Function

- 21.6.7. Ownership Model

- 21.6.8. Integration Level

- 21.6.9. Installation Type

- 21.6.10. End-Use Industry

- 22. Key Players/ Company Profile

- 22.1. ABB Ltd.

- 22.1.1. Company Details/ Overview

- 22.1.2. Company Financials

- 22.1.3. Key Customers and Competitors

- 22.1.4. Business/ Industry Portfolio

- 22.1.5. Product Portfolio/ Specification Details

- 22.1.6. Pricing Data

- 22.1.7. Strategic Overview

- 22.1.8. Recent Developments

- 22.2. AutoStore

- 22.3. Bastian Solutions

- 22.4. Berkshire Grey

- 22.5. Beumer Group

- 22.6. Daifuku Co., Ltd.

- 22.7. Dematic (KION Group)

- 22.8. Fanuc Corporation

- 22.9. Fives Group

- 22.10. Geek+

- 22.11. Honeywell Intelligrated

- 22.12. IAM Robotics

- 22.13. Jungheinrich AG

- 22.14. Kardex Group

- 22.15. Knapp AG

- 22.16. Körber AG

- 22.17. KUKA AG

- 22.18. Locus Robotics

- 22.19. Mecalux S.A.

- 22.20. Murata Machinery, Ltd.

- 22.21. Omron Corporation

- 22.22. SSI Schäfer Group

- 22.23. Swisslog (KUKA Group)

- 22.24. TGW Logistics Group

- 22.25. Toyota Industries Corporation

- 22.26. Vanderlande Industries

- 22.27. WITRON Logistik + Informatik GmbH

- 22.28. YASKAWA Electric Corporation

- 22.29. Other Key Players

- 22.1. ABB Ltd.

Note* - This is just tentative list of players. While providing the report, we will cover more number of players based on their revenue and share for each geography

Research Design

Our research design integrates both demand-side and supply-side analysis through a balanced combination of primary and secondary research methodologies. By utilizing both bottom-up and top-down approaches alongside rigorous data triangulation methods, we deliver robust market intelligence that supports strategic decision-making.

MarketGenics' comprehensive research design framework ensures the delivery of accurate, reliable, and actionable market intelligence. Through the integration of multiple research approaches, rigorous validation processes, and expert analysis, we provide our clients with the insights needed to make informed strategic decisions and capitalize on market opportunities.

MarketGenics leverages a dedicated industry panel of experts and a comprehensive suite of paid databases to effectively collect, consolidate, and analyze market intelligence.

Our approach has consistently proven to be reliable and effective in generating accurate market insights, identifying key industry trends, and uncovering emerging business opportunities.

Through both primary and secondary research, we capture and analyze critical company-level data such as manufacturing footprints, including technical centers, R&D facilities, sales offices, and headquarters.

Our expert panel further enhances our ability to estimate market size for specific brands based on validated field-level intelligence.

Our data mining techniques incorporate both parametric and non-parametric methods, allowing for structured data collection, sorting, processing, and cleaning.

Demand projections are derived from large-scale data sets analyzed through proprietary algorithms, culminating in robust and reliable market sizing.

Research Approach

The bottom-up approach builds market estimates by starting with the smallest addressable market units and systematically aggregating them to create comprehensive market size projections.

This method begins with specific, granular data points and builds upward to create the complete market landscape.

Customer Analysis → Segmental Analysis → Geographical Analysis

The top-down approach starts with the broadest possible market data and systematically narrows it down through a series of filters and assumptions to arrive at specific market segments or opportunities.

This method begins with the big picture and works downward to increasingly specific market slices.

TAM → SAM → SOM

Research Methods

Desk / Secondary Research

While analysing the market, we extensively study secondary sources, directories, and databases to identify and collect information useful for this technical, market-oriented, and commercial report. Secondary sources that we utilize are not only the public sources, but it is a combination of Open Source, Associations, Paid Databases, MG Repository & Knowledgebase, and others.

- Company websites, annual reports, financial reports, broker reports, and investor presentations

- National government documents, statistical databases and reports

- News articles, press releases and web-casts specific to the companies operating in the market, Magazines, reports, and others

- We gather information from commercial data sources for deriving company specific data such as segmental revenue, share for geography, product revenue, and others

- Internal and external proprietary databases (industry-specific), relevant patent, and regulatory databases

- Governing Bodies, Government Organizations

- Relevant Authorities, Country-specific Associations for Industries

We also employ the model mapping approach to estimate the product level market data through the players' product portfolio

Primary Research

Primary research/ interviews is vital in analyzing the market. Most of the cases involves paid primary interviews. Primary sources include primary interviews through e-mail interactions, telephonic interviews, surveys as well as face-to-face interviews with the different stakeholders across the value chain including several industry experts.

| Type of Respondents | Number of Primaries |

|---|---|

| Tier 2/3 Suppliers | ~20 |

| Tier 1 Suppliers | ~25 |

| End-users | ~25 |

| Industry Expert/ Panel/ Consultant | ~30 |

| Total | ~100 |

MG Knowledgebase

• Repository of industry blog, newsletter and case studies

• Online platform covering detailed market reports, and company profiles

Forecasting Factors and Models

Forecasting Factors

- Historical Trends – Past market patterns, cycles, and major events that shaped how markets behave over time. Understanding past trends helps predict future behavior.

- Industry Factors – Specific characteristics of the industry like structure, regulations, and innovation cycles that affect market dynamics.

- Macroeconomic Factors – Economic conditions like GDP growth, inflation, and employment rates that affect how much money people have to spend.

- Demographic Factors – Population characteristics like age, income, and location that determine who can buy your product.

- Technology Factors – How quickly people adopt new technology and how much technology infrastructure exists.

- Regulatory Factors – Government rules, laws, and policies that can help or restrict market growth.

- Competitive Factors – Analyzing competition structure such as degree of competition and bargaining power of buyers and suppliers.

Forecasting Models / Techniques

Multiple Regression Analysis

- Identify and quantify factors that drive market changes

- Statistical modeling to establish relationships between market drivers and outcomes

Time Series Analysis – Seasonal Patterns

- Understand regular cyclical patterns in market demand

- Advanced statistical techniques to separate trend, seasonal, and irregular components

Time Series Analysis – Trend Analysis

- Identify underlying market growth patterns and momentum

- Statistical analysis of historical data to project future trends

Expert Opinion – Expert Interviews

- Gather deep industry insights and contextual understanding

- In-depth interviews with key industry stakeholders

Multi-Scenario Development

- Prepare for uncertainty by modeling different possible futures

- Creating optimistic, pessimistic, and most likely scenarios

Time Series Analysis – Moving Averages

- Sophisticated forecasting for complex time series data

- Auto-regressive integrated moving average models with seasonal components

Econometric Models

- Apply economic theory to market forecasting

- Sophisticated economic models that account for market interactions

Expert Opinion – Delphi Method

- Harness collective wisdom of industry experts

- Structured, multi-round expert consultation process

Monte Carlo Simulation

- Quantify uncertainty and probability distributions

- Thousands of simulations with varying input parameters

Research Analysis

Our research framework is built upon the fundamental principle of validating market intelligence from both demand and supply perspectives. This dual-sided approach ensures comprehensive market understanding and reduces the risk of single-source bias.

Demand-Side Analysis: We understand end-user/application behavior, preferences, and market needs along with the penetration of the product for specific application.

Supply-Side Analysis: We estimate overall market revenue, analyze the segmental share along with industry capacity, competitive landscape, and market structure.

Validation & Evaluation

Data triangulation is a validation technique that uses multiple methods, sources, or perspectives to examine the same research question, thereby increasing the credibility and reliability of research findings. In market research, triangulation serves as a quality assurance mechanism that helps identify and minimize bias, validate assumptions, and ensure accuracy in market estimates.

- Data Source Triangulation – Using multiple data sources to examine the same phenomenon

- Methodological Triangulation – Using multiple research methods to study the same research question

- Investigator Triangulation – Using multiple researchers or analysts to examine the same data

- Theoretical Triangulation – Using multiple theoretical perspectives to interpret the same data

Custom Market Research Services

We will customise the research for you, in case the report listed above does not meet your requirements.

Get 10% Free Customisation