Peptide-based Cancer Therapeutics Market Size, Share & Trends Analysis Report by Peptide Type (Antimicrobial Peptides, Cell-Penetrating Peptides, Modified Peptides, Peptide Conjugates, Peptide Vaccines, Others), Mechanism of Action, Cancer Type, Route of Administration, Therapeutic Approach, End-Use, and Geography (North America, Europe, Asia Pacific, Middle East, Africa, and South America) – Global Industry Data, Trends, and Forecasts, 2026–2035

|

|

|

Segmental Data Insights |

|

|

Demand Trends |

|

|

Competitive Landscape |

|

|

Strategic Development |

|

|

Future Outlook & Opportunities |

|

Peptide-based Cancer Therapeutics Market Size, Share, and Growth

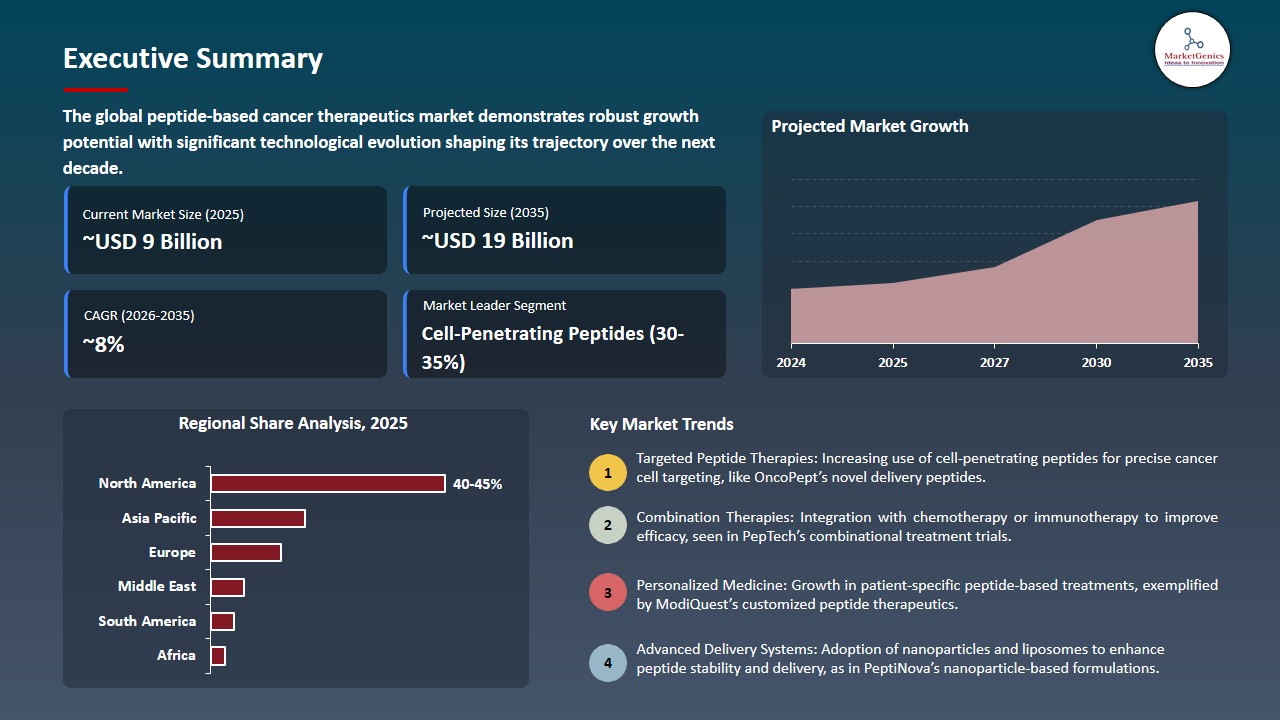

The global peptide-based cancer therapeutics market is witnessing strong growth, valued at USD 8.5 billion in 2025 and projected to reach USD 18.7 billion by 2035, expanding at a CAGR of 8.2% during the forecast period. Asia Pacific is the fastest-growing peptide-based cancer therapeutics market due to increasing cancer prevalence, rising healthcare investments, growing adoption of advanced biologics, and expanding access to specialized oncology treatments across emerging economies.

Vishwas Paralkar, Ph.D., Chief Scientific Officer of Cybrexa Therapeutics, said, “These data reinforce the potential of the alphalex platform to overcome the challenges of antigen-based therapies, while providing a powerful, tumor-selective approach to delivering cytotoxic agents, In bypassing the limitations of antibody-drug conjugates, we are opening new therapeutic possibilities for patients with hard-to-treat solid tumors”.

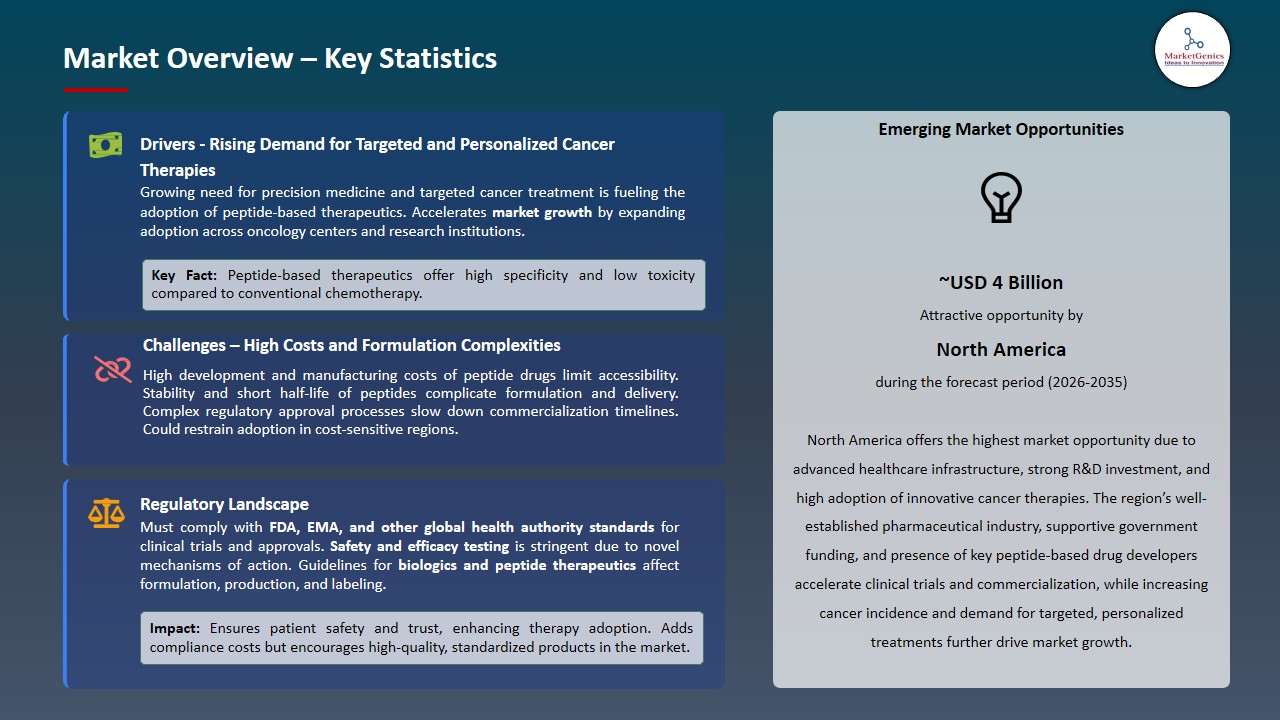

The most crucial factor driving the peptide-based cancer therapeutics market is the rising global incidence of cancer, which has created an imminent prerequisite for innovative and effective treatments. The growing incidence of several types of cancer, along with the growing awareness of the field of precision medicine, are driving the need to find specialized treatment. Therapeutics are characterized by peptide-based therapeutics; it is specific, less toxic and can be used in combination with other treatments, which is why peptide-based therapeutics are gaining popularity among clinicians and patients all over the world.

The concept of peptides and personalized medicine combined with precision oncology is a promising opportunity to the market. Individual tumor profile of patients can be targeted with peptide-based therapeutics leading to increased efficacy, reduction of side effects, and tailoring the therapy to patient needs. With the growing popularity of genomic profiling and biomarker-based treatment approaches and the development of peptides therapeutics is rapidly becoming a complementary approach to precision oncology, providing personalized and next-generation cancer therapies with better clinical outcomes and patient quality of life.

Key adjacent opportunities for the peptide-based cancer therapeutics market include peptide-drug conjugates, immuno-oncology combination therapies, advanced delivery systems (nanoparticles, liposomes), and RNA/peptide hybrid therapeutics. These areas enable innovation, improve treatment specificity, and expand therapeutic applications, collectively strengthening market growth and enhancing overall patient outcomes.

Peptide-based Cancer Therapeutics Market Dynamics and Trends

Driver: Advancements in AI‑Designed Peptide Therapeutics Accelerate Innovation

-

An artificial intelligence (AI) approach to peptide-based cancer therapy is resulting in a huge market expansion, by allowing the speedy design and optimization of new peptides with increased specificity, stability, and therapeutic capability. AI platforms can compute the large molecular data, make predictions on peptide-target interactions, and simplify the process of identifying candidates to enter preclinical testing, lessening time and cost taken by conventional drug discovery.

- These AI-based technologies can improve the efficacy of various treatments, reduce side effects, and provide more accurate navigation of tumor cells. The integration of AI is making the process of drug discovery more efficient and therapeutic performance effective, making peptide therapeutics in oncology a groundbreaking solution.

- ProteinQure Inc. raised $11 million in Series A financing in May 2025 to bring PQ203, the first AI-designed peptide-drug conjugate, to Phase 1 clinical trials in triple-negative breast cancer. The investment will help it by clinically validating its AI-driven platform, which increases the ability to quickly design the next generation of peptide therapeutics with increased specificity and efficacy.

- AI-based design fosters innovation and increases the creation of targeted and effective cancer treatments.

Restraint: Complex Clinical Validation and Regulatory Requirements Delay Market Uptake

-

The limitations of clinical validation and rigorous regulatory factors are major constraints to market growth and challenge the development of peptide-based cancer therapeutics. The enhancement of peptide drugs needs long-term preclinical research, such as pharmacokinetics, toxicity, and efficacy tests to guarantee safety and stability. The preclinical testing to clinical trials is usually lengthy and expensive as several stages of human testing are necessary to exhibit the therapeutic value in various types of cancers.

- There are stringent rules that are set by regulatory bodies in the peptide-based therapy, especially when it comes to consistency of manufacturing, quality control, and safety monitoring. Also, new modalities like peptide-drug conjugates or AI-programmed peptides can undergo further critique owing to their novel mechanism of action. Such demands add to development times, increment costs and can delay product approvals posing challenges to small biotech companies and slow uptake on the market.

- Regulatory and clinical entanglements delay the commercialization of peptide-based therapeutics, inhibiting short-term market expansion and uptake.

Opportunity: Expansion of Tumor‑Selective Peptide‑Drug Conjugates as Next‑Gen Therapies

-

The invention and growth of tumor-targeted peptide-drug conjugates (PDCs) is a significant opportunity within the peptide-based cancer therapeutics market. PDCs are able to combine the specificity of peptides with the efficacy of cytotoxic drugs, and therefore, can be delivered selectively to cancer cells with minimal effects on normal tissue. The strategy improves the response of therapies, minimizes systemic toxicity, and solves the shortcomings of traditional chemotherapy.

- The engineering of peptides, linker technology, and payload optimization are leading to production of next-generation PDCs that are more stable, bioavailability, and tumor penetrating. As more clinical pipelines target a wide range of types of cancers, including difficult-to-treat solid tumors, PDCs would become a transformational treatment modality. The innovation increases the range of treatment and makes peptide therapeutics one of the most promising pillars of precision oncology.

- Cybrexa Therapeutics has shown preclinical results of its alphalex tumor-selective peptide-drug conjugates in March 2025 at the ESMO Targeted Anticancer Therapies Congress, showing specific tumor targeting, effective anti-tumor activity and improved immune response.

- Selective PDCs against tumors increase the specificity and efficacy of treatment and hasten its implementation in advanced cancer treatment.

Key Trend: Pre‑Insulated Panels & Hybrid Insulation Solutions

-

The major trends observed in the market of peptide-based cancer therapeutics include the rising number of clinical trials and the emergence of multi-functional peptide platforms. Peptides are undergoing design not just as a therapeutic modality, but also as a diagnostic and imaging modality, thus allowing theranostics integrating therapeutic and real-time imaging. This twofold capability is able to provide personalized treatment plans, enable a better stratification of patients and therapeutic results.

- Ongoing clinical trials are investigating new peptide modalities, such as peptide-drug conjugates, cell-penetrating peptides and immune-modulating peptides in an extensive list of cancer types. The trend was indicative of a rising level of confidence in peptide-based methods, improvements in delivery technology, as well as a combination with precision medicine, which broadens the range and uptake of peptide-based therapeutics.

- In 2025, Avacta Therapeutics advanced its pre|CISION peptide-drug conjugate platform, demonstrating tumor-targeted delivery, FAP-mediated activation, and potent anti-tumor activity of candidates such as AVA6000 and AVA6103, highlighting the expansion of multifunctional peptide therapeutics and the growing clinical development of next-generation cancer treatments.

- Increased clinical activity and multifunctional platforms strengthen peptide therapeutics’ role in personalized and targeted cancer care.

Peptide-based-Cancer-Therapeutics-Market Analysis and Segmental Data

Cell-Penetrating Peptides Dominate Global Peptide-based Cancer Therapeutics Market

-

The cell-penetrating peptides segment holds a leading position in the peptide-based cancer therapeutics market due to their ability to efficiently transport therapeutic molecules, including small drugs, peptides, and nucleic acids, directly into cancer cells. CPPs enhance intracellular delivery, improving the efficacy of anticancer agents while minimizing systemic toxicity. Their versatility allows integration with peptide-drug conjugates, immune-modulating therapies, and targeted delivery platforms, enabling precision oncology approaches.

- Ongoing studies are aiming against improving cell-penetrating peptides sequences to become more specific, stable and have fewer off-target effects which continue to push adoptions. The strong showing in the preclinical and clinical studies, the increasing need in the intracellular-targeted therapies have supported its leadership in the global peptides therapeutics market.

- PEP-Therapy entered into Phase 1b clinical trials with its first-in-class PEP-010, a cell-penetrating peptide that reinstates apoptosis in cancer cells, in platinum-resistant ovarian cancer and pancreatic ductal adenocarcinoma.

- Cell-penetrating peptides are the most popular segment of the peptide-based oncology therapies due to their high cellular uptake and therapeutic versatility.

North America Leads Global Peptide-based Cancer Therapeutics Market Demand

-

North America holds a leading position in the global peptide-based cancer therapeutics market due to a combination of advanced healthcare infrastructure, robust oncology research programs, and strong pharmaceutical and biotechnology ecosystems. The region benefits from substantial investment in cancer research, well-established clinical trial networks, and favorable regulatory frameworks that support the rapid development and approval of innovative peptide-based therapies.

- The availability of state-of-the-art research institutions, cancer focused centers and academia and industry partnerships hasten the discovery, clinical testing and commercialization of new peptide therapeutics. Moreover, the growing awareness of the existence of the so-called precision medicine, and the growing cancer prevalence, as well as the early adoption of the next-generation therapeutics are all factors that add to the high demand in the market.

- Favourable reimbursement policies and high access to novel treatments by the patient also favour the market setting, which supports the adoption of peptide-based treatment. All these factors only strengthen the position of the region in the world market and promote further research and development of specific peptide therapy.

- North America has a dominant market in peptide-based cancer therapeutics due to advanced infrastructure and an early embrace of innovation.

Peptide-based-Cancer-Therapeutics-Market Ecosystem

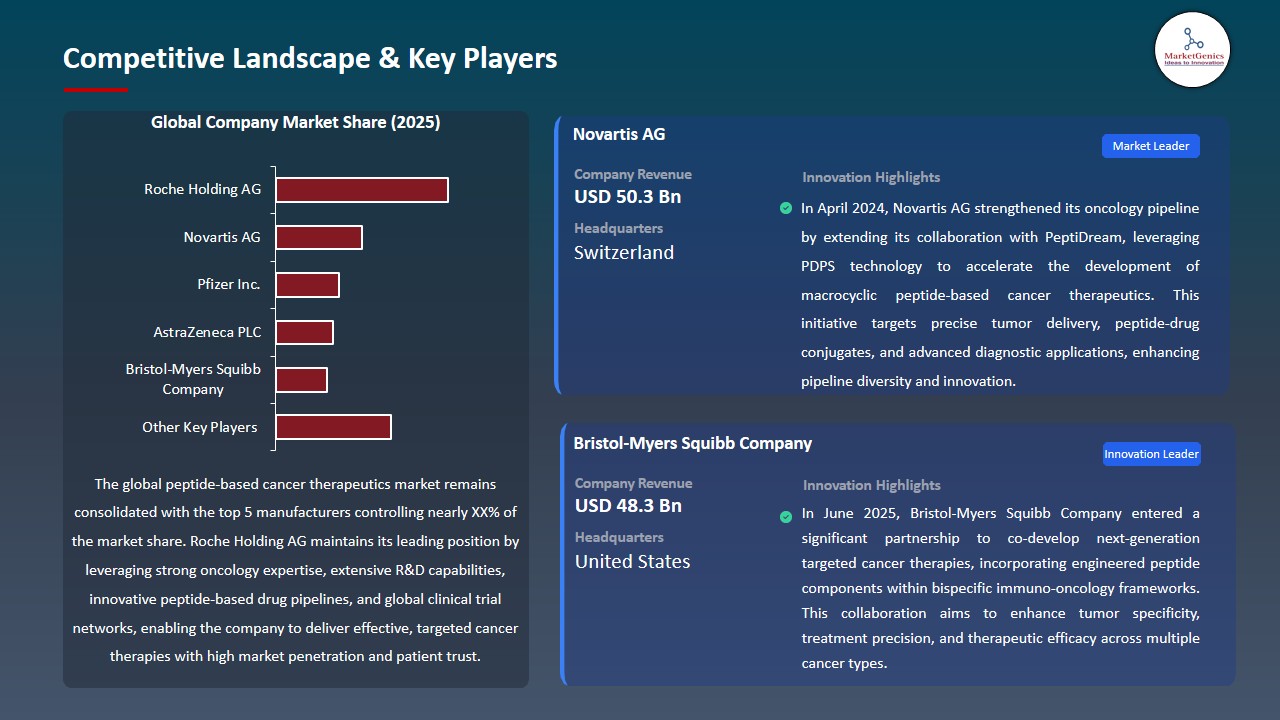

The global peptide-based cancer therapeutics market is consolidated, with leading players including Roche Holding AG, Novartis AG, Pfizer Inc., AstraZeneca PLC, and Bristol-Myers Squibb Company. These companies maintain strong competitive positions through extensive research and development capabilities, diverse oncology-focused peptide portfolios, strategic collaborations with biotech firms, and the ability to meet stringent regulatory and safety standards. Their strengths are further reinforced by global clinical trial networks, robust commercialization strategies, and established relationships with hospitals, research institutions, and healthcare providers.

The market value chain encompasses peptide discovery, preclinical and clinical development, regulatory approvals, manufacturing of high-purity therapeutics, distribution through healthcare channels, and post-marketing surveillance. These stages ensure consistent product quality, efficacy, and compliance with global regulatory frameworks.

High entry barriers exist due to extensive R&D investment, complex clinical validation requirements, regulatory compliance, and the need for specialized expertise in peptide design and manufacturing. Continuous innovation, including targeted peptide-drug conjugates, multifunctional peptides, and advanced delivery systems, drives differentiation, improves therapeutic outcomes, and sustains market growth globally.

Recent Development and Strategic Overview:

-

In April 2024, Novartis received FDA approval for Lutathera as the first radioligand therapy specifically indicated for pediatric patients (ages 12–17) with somatostatin receptor-positive gastroenteropancreatic neuroendocrine tumors (GEP-NETs). The approval, based on the NETTER-P trial, confirmed a safety profile consistent with adults and positions Lutathera as a pioneering peptide-based targeted therapy in pediatric oncology.

- In November 2025, Verrica Pharmaceuticals reported new Phase 2 data for VP‑315 (ruxotemitide), a first-in-class oncolytic peptide, showing strong tumor microenvironment modulation, increased cytotoxic T‑cell infiltration, and a 97% objective response rate in basal cell carcinoma. The findings reinforce VP‑315’s potential as a non-surgical immunotherapeutic option.

Report Scope

|

Detail |

|

|

Market Size in 2025 |

USD 8.5 Bn |

|

Market Forecast Value in 2035 |

USD 18.7 Bn |

|

Growth Rate (CAGR) |

8.2% |

|

Forecast Period |

2026 – 2035 |

|

Historical Data Available for |

2021 – 2024 |

|

Market Size Units |

US$ Billion for Value |

|

Report Format |

Electronic (PDF) + Excel |

|

North America |

Europe |

Asia Pacific |

Middle East |

Africa |

South America |

|

|

|

|

|

|

|

Companies Covered |

|||||

|

|

|

|

|

|

Peptide-based-Cancer-Therapeutics-Market Segmentation and Highlights

|

Segment |

Sub-segment |

|

Peptide-based Cancer Therapeutics Market, By Peptide Type |

|

|

Peptide-based Cancer Therapeutics Market, By Mechanism of Action |

|

|

Peptide-based Cancer Therapeutics Market, By Cancer Type |

|

|

Peptide-based Cancer Therapeutics Market, By Route of Administration |

|

|

Peptide-based Cancer Therapeutics Market, By Therapeutic Approach |

|

|

Peptide-based Cancer Therapeutics Market, By End-use |

|

Frequently Asked Questions

Table of Contents

- 1. Research Methodology and Assumptions

- 1.1. Definitions

- 1.2. Research Design and Approach

- 1.3. Data Collection Methods

- 1.4. Base Estimates and Calculations

- 1.5. Forecasting Models

- 1.5.1. Key Forecast Factors & Impact Analysis

- 1.6. Secondary Research

- 1.6.1. Open Sources

- 1.6.2. Paid Databases

- 1.6.3. Associations

- 1.7. Primary Research

- 1.7.1. Primary Sources

- 1.7.2. Primary Interviews with Stakeholders across Ecosystem

- 2. Executive Summary

- 2.1. Global Peptide-based Cancer Therapeutics Market Outlook

- 2.1.1. Peptide-based Cancer Therapeutics Market Size Value (US$ Bn), and Forecasts, 2021-2035

- 2.1.2. Compounded Annual Growth Rate Analysis

- 2.1.3. Growth Opportunity Analysis

- 2.1.4. Segmental Share Analysis

- 2.1.5. Geographical Share Analysis

- 2.2. Market Analysis and Facts

- 2.3. Supply-Demand Analysis

- 2.4. Competitive Benchmarking

- 2.5. Go-to- Market Strategy

- 2.5.1. Customer/ End-use Industry Assessment

- 2.5.2. Growth Opportunity Data, 2026-2035

- 2.5.2.1. Regional Data

- 2.5.2.2. Country Data

- 2.5.2.3. Segmental Data

- 2.5.3. Identification of Potential Market Spaces

- 2.5.4. GAP Analysis

- 2.5.5. Potential Attractive Price Points

- 2.5.6. Prevailing Market Risks & Challenges

- 2.5.7. Preferred Sales & Marketing Strategies

- 2.5.8. Key Recommendations and Analysis

- 2.5.9. A Way Forward

- 2.1. Global Peptide-based Cancer Therapeutics Market Outlook

- 3. Industry Data and Premium Insights

- 3.1. Global Healthcare & Pharmaceutical Industry Overview, 2025

- 3.1.1. Healthcare & Pharmaceutical Industry Ecosystem Analysis

- 3.1.2. Key Trends for Healthcare & Pharmaceutical Industry

- 3.1.3. Regional Distribution for Healthcare & Pharmaceutical Industry

- 3.2. Supplier Customer Data

- 3.3. Technology Roadmap and Developments

- 3.4. Trade Analysis

- 3.4.1. Import & Export Analysis, 2025

- 3.4.2. Top Importing Countries

- 3.4.3. Top Exporting Countries

- 3.5. Trump Tariff Impact Analysis

- 3.5.1. Manufacturer

- 3.5.1.1. Based on the component & Raw material

- 3.5.2. Supply Chain

- 3.5.3. End Consumer

- 3.5.1. Manufacturer

- 3.6. Raw Material Analysis

- 3.1. Global Healthcare & Pharmaceutical Industry Overview, 2025

- 4. Market Overview

- 4.1. Market Dynamics

- 4.1.1. Drivers

- 4.1.1.1. Rising global cancer burden increasing demand for targeted and personalized therapies.

- 4.1.1.2. Advances in peptide engineering and drug delivery enhancing efficacy and specificity.

- 4.1.1.3. Strong oncology R&D investments and expanding clinical pipelines for peptide therapeutics.

- 4.1.2. Restraints

- 4.1.2.1. High development and manufacturing costs associated with peptide synthesis and trials.

- 4.1.2.2. Stability, bioavailability, and delivery challenges limiting broader clinical adoption.

- 4.1.1. Drivers

- 4.2. Key Trend Analysis

- 4.3. Regulatory Framework

- 4.3.1. Key Regulations, Norms, and Subsidies, by Key Countries

- 4.3.2. Tariffs and Standards

- 4.3.3. Impact Analysis of Regulations on the Market

- 4.4. Ecosystem Analysis

- 4.5. Porter’s Five Forces Analysis

- 4.6. PESTEL Analysis

- 4.7. Global Peptide-based Cancer Therapeutics Market Demand

- 4.7.1. Historical Market Size – Value (US$ Bn), 2020-2024

- 4.7.2. Current and Future Market Size – Value (US$ Bn), 2026–2035

- 4.7.2.1. Y-o-Y Growth Trends

- 4.7.2.2. Absolute $ Opportunity Assessment

- 4.1. Market Dynamics

- 5. Competition Landscape

- 5.1. Competition structure

- 5.1.1. Fragmented v/s consolidated

- 5.2. Company Share Analysis, 2025

- 5.2.1. Global Company Market Share

- 5.2.2. By Region

- 5.2.2.1. North America

- 5.2.2.2. Europe

- 5.2.2.3. Asia Pacific

- 5.2.2.4. Middle East

- 5.2.2.5. Africa

- 5.2.2.6. South America

- 5.3. Product Comparison Matrix

- 5.3.1. Specifications

- 5.3.2. Market Positioning

- 5.3.3. Pricing

- 5.1. Competition structure

- 6. Global Peptide-based Cancer Therapeutics Market Analysis, by Peptide Type

- 6.1. Key Segment Analysis

- 6.2. Peptide-based Cancer Therapeutics Market Size Value (US$ Bn), Analysis, and Forecasts, by Peptide Type, 2021-2035

- 6.2.1. Antimicrobial Peptides

- 6.2.2. Cell-Penetrating Peptides

- 6.2.2.1. Therapeutic Peptides

- 6.2.2.2. Linear Peptides

- 6.2.2.3. Cyclic Peptides

- 6.2.3. Modified Peptides

- 6.2.4. Peptide Conjugates

- 6.2.5. Peptide Vaccines

- 6.2.6. Others

- 7. Global Peptide-based Cancer Therapeutics Market Analysis, by Mechanism of Action

- 7.1. Key Segment Analysis

- 7.2. Peptide-based Cancer Therapeutics Market Size Value (US$ Bn), Analysis, and Forecasts, by Mechanism of Action, 2021-2035

- 7.2.1. Apoptosis Induction

- 7.2.2. Angiogenesis Inhibition

- 7.2.3. Cell Cycle Arrest

- 7.2.4. Receptor Targeting

- 7.2.5. Immune System Modulation

- 7.2.6. Enzyme Inhibition

- 7.2.7. Signal Transduction Interference

- 7.2.8. Others

- 8. Global Peptide-based Cancer Therapeutics Market Analysis, by Cancer Type

- 8.1. Key Segment Analysis

- 8.2. Peptide-based Cancer Therapeutics Market Size Value (US$ Bn), Analysis, and Forecasts, by Cancer Type, 2021-2035

- 8.2.1. Breast Cancer

- 8.2.2. Lung Cancer

- 8.2.2.1. Non-Small Cell Lung Cancer

- 8.2.2.2. Small Cell Lung Cancer

- 8.2.3. Prostate Cancer

- 8.2.4. Colorectal Cancer

- 8.2.5. Pancreatic Cancer

- 8.2.6. Melanoma

- 8.2.7. Leukemia

- 8.2.8. Lymphoma

- 8.2.9. Ovarian Cancer

- 8.2.10. Gastric Cancer

- 8.2.11. Others

- 9. Global Peptide-based Cancer Therapeutics Market Analysis, by Route of Administration

- 9.1. Key Segment Analysis

- 9.2. Peptide-based Cancer Therapeutics Market Size Value (US$ Bn), Analysis, and Forecasts, by Route of Administration, 2021-2035

- 9.2.1. Intravenous

- 9.2.2. Subcutaneous

- 9.2.3. Intramuscular

- 9.2.4. Oral

- 9.2.5. Topical

- 9.2.6. Intratumoral

- 10. Global Peptide-based Cancer Therapeutics Market Analysis, by Therapeutic Approach

- 10.1. Key Segment Analysis

- 10.2. Peptide-based Cancer Therapeutics Market Size Value (US$ Bn), Analysis, and Forecasts, by Therapeutic Approach, 2021-2035

- 10.2.1. Monotherapy

- 10.2.2. Combination Therapy

- 10.2.2.1. With Chemotherapy

- 10.2.2.2. With Immunotherapy

- 10.2.2.3. With Targeted Therapy

- 10.2.2.4. With Radiation Therapy

- 11. Global Peptide-based Cancer Therapeutics Market Analysis, by End-Use

- 11.1. Key Segment Analysis

- 11.2. Peptide-based Cancer Therapeutics Market Size Value (US$ Bn), Analysis, and Forecasts, by End-Use, 2021-2035

- 11.2.1. Hospitals & Clinics

- 11.2.1.1. Oncology Departments

- 11.2.1.2. Solid Tumor Treatment

- 11.2.1.3. Hematological Malignancies Treatment

- 11.2.1.4. Palliative Care

- 11.2.1.5. Others

- 11.2.1.6. Surgical Oncology Units

- 11.2.1.7. Radiation Oncology Centers

- 11.2.1.8. Intensive Care Units

- 11.2.1.9. Others

- 11.2.2. Cancer Research Institutes

- 11.2.2.1. Drug Discovery & Development

- 11.2.2.2. Biomarker Research

- 11.2.2.3. Clinical Trial Conducting

- 11.2.2.4. Peptide Library Screening

- 11.2.2.5. Mechanism of Action Studies

- 11.2.2.6. Others

- 11.2.3. Pharmaceutical & Biotechnology Companies

- 11.2.3.1. Commercial Manufacturing

- 11.2.3.2. Drug Formulation Development

- 11.2.3.3. Quality Control & Testing

- 11.2.3.4. Scale-Up Production

- 11.2.3.5. Regulatory Compliance

- 11.2.3.6. Others

- 11.2.4. Contract Research Organizations (CROs)

- 11.2.5. Specialty Cancer Centers

- 11.2.6. Academic & Research Organizations

- 11.2.7. Others

- 11.2.1. Hospitals & Clinics

- 12. Global Peptide-based Cancer Therapeutics Market Analysis and Forecasts, by Region

- 12.1. Key Findings

- 12.2. Peptide-based Cancer Therapeutics Market Size Value (US$ Bn), Analysis, and Forecasts, by Region, 2021-2035

- 12.2.1. North America

- 12.2.2. Europe

- 12.2.3. Asia Pacific

- 12.2.4. Middle East

- 12.2.5. Africa

- 12.2.6. South America

- 13. North America Peptide-based Cancer Therapeutics Market Analysis

- 13.1. Key Segment Analysis

- 13.2. Regional Snapshot

- 13.3. North America Peptide-based Cancer Therapeutics Market Size Value (US$ Bn), Analysis, and Forecasts, 2021-2035

- 13.3.1. Peptide Type

- 13.3.2. Mechanism of Action

- 13.3.3. Cancer Type

- 13.3.4. Route of Administration

- 13.3.5. Therapeutic Approach

- 13.3.6. End-Use

- 13.3.7. Country

- 13.3.7.1. USA

- 13.3.7.2. Canada

- 13.3.7.3. Mexico

- 13.4. USA Peptide-based Cancer Therapeutics Market

- 13.4.1. Country Segmental Analysis

- 13.4.2. Peptide Type

- 13.4.3. Mechanism of Action

- 13.4.4. Cancer Type

- 13.4.5. Route of Administration

- 13.4.6. Therapeutic Approach

- 13.4.7. End-Use

- 13.5. Canada Peptide-based Cancer Therapeutics Market

- 13.5.1. Country Segmental Analysis

- 13.5.2. Peptide Type

- 13.5.3. Mechanism of Action

- 13.5.4. Cancer Type

- 13.5.5. Route of Administration

- 13.5.6. Therapeutic Approach

- 13.5.7. End-Use

- 13.6. Mexico Peptide-based Cancer Therapeutics Market

- 13.6.1. Country Segmental Analysis

- 13.6.2. Peptide Type

- 13.6.3. Mechanism of Action

- 13.6.4. Cancer Type

- 13.6.5. Route of Administration

- 13.6.6. Therapeutic Approach

- 13.6.7. End-Use

- 14. Europe Peptide-based Cancer Therapeutics Market Analysis

- 14.1. Key Segment Analysis

- 14.2. Regional Snapshot

- 14.3. Europe Peptide-based Cancer Therapeutics Market Size Value (US$ Bn), Analysis, and Forecasts, 2021-2035

- 14.3.1. Peptide Type

- 14.3.2. Mechanism of Action

- 14.3.3. Cancer Type

- 14.3.4. Route of Administration

- 14.3.5. Therapeutic Approach

- 14.3.6. End-Use

- 14.3.7. Country

- 14.3.7.1. Germany

- 14.3.7.2. United Kingdom

- 14.3.7.3. France

- 14.3.7.4. Italy

- 14.3.7.5. Spain

- 14.3.7.6. Netherlands

- 14.3.7.7. Nordic Countries

- 14.3.7.8. Poland

- 14.3.7.9. Russia & CIS

- 14.3.7.10. Rest of Europe

- 14.4. Germany Peptide-based Cancer Therapeutics Market

- 14.4.1. Country Segmental Analysis

- 14.4.2. Peptide Type

- 14.4.3. Mechanism of Action

- 14.4.4. Cancer Type

- 14.4.5. Route of Administration

- 14.4.6. Therapeutic Approach

- 14.4.7. End-Use

- 14.5. United Kingdom Peptide-based Cancer Therapeutics Market

- 14.5.1. Country Segmental Analysis

- 14.5.2. Peptide Type

- 14.5.3. Mechanism of Action

- 14.5.4. Cancer Type

- 14.5.5. Route of Administration

- 14.5.6. Therapeutic Approach

- 14.5.7. End-Use

- 14.6. France Peptide-based Cancer Therapeutics Market

- 14.6.1. Country Segmental Analysis

- 14.6.2. Peptide Type

- 14.6.3. Mechanism of Action

- 14.6.4. Cancer Type

- 14.6.5. Route of Administration

- 14.6.6. Therapeutic Approach

- 14.6.7. End-Use

- 14.7. Italy Peptide-based Cancer Therapeutics Market

- 14.7.1. Country Segmental Analysis

- 14.7.2. Peptide Type

- 14.7.3. Mechanism of Action

- 14.7.4. Cancer Type

- 14.7.5. Route of Administration

- 14.7.6. Therapeutic Approach

- 14.7.7. End-Use

- 14.8. Spain Peptide-based Cancer Therapeutics Market

- 14.8.1. Country Segmental Analysis

- 14.8.2. Peptide Type

- 14.8.3. Mechanism of Action

- 14.8.4. Cancer Type

- 14.8.5. Route of Administration

- 14.8.6. Therapeutic Approach

- 14.8.7. End-Use

- 14.9. Netherlands Peptide-based Cancer Therapeutics Market

- 14.9.1. Country Segmental Analysis

- 14.9.2. Peptide Type

- 14.9.3. Mechanism of Action

- 14.9.4. Cancer Type

- 14.9.5. Route of Administration

- 14.9.6. Therapeutic Approach

- 14.9.7. End-Use

- 14.10. Nordic Countries Peptide-based Cancer Therapeutics Market

- 14.10.1. Country Segmental Analysis

- 14.10.2. Peptide Type

- 14.10.3. Mechanism of Action

- 14.10.4. Cancer Type

- 14.10.5. Route of Administration

- 14.10.6. Therapeutic Approach

- 14.10.7. End-Use

- 14.11. Poland Peptide-based Cancer Therapeutics Market

- 14.11.1. Country Segmental Analysis

- 14.11.2. Peptide Type

- 14.11.3. Mechanism of Action

- 14.11.4. Cancer Type

- 14.11.5. Route of Administration

- 14.11.6. Therapeutic Approach

- 14.11.7. End-Use

- 14.12. Russia & CIS Peptide-based Cancer Therapeutics Market

- 14.12.1. Country Segmental Analysis

- 14.12.2. Peptide Type

- 14.12.3. Mechanism of Action

- 14.12.4. Cancer Type

- 14.12.5. Route of Administration

- 14.12.6. Therapeutic Approach

- 14.12.7. End-Use

- 14.13. Rest of Europe Peptide-based Cancer Therapeutics Market

- 14.13.1. Country Segmental Analysis

- 14.13.2. Peptide Type

- 14.13.3. Mechanism of Action

- 14.13.4. Cancer Type

- 14.13.5. Route of Administration

- 14.13.6. Therapeutic Approach

- 14.13.7. End-Use

- 15. Asia Pacific Peptide-based Cancer Therapeutics Market Analysis

- 15.1. Key Segment Analysis

- 15.2. Regional Snapshot

- 15.3. Asia Pacific Peptide-based Cancer Therapeutics Market Size Value (US$ Bn), Analysis, and Forecasts, 2021-2035

- 15.3.1. Peptide Type

- 15.3.2. Mechanism of Action

- 15.3.3. Cancer Type

- 15.3.4. Route of Administration

- 15.3.5. Therapeutic Approach

- 15.3.6. End-Use

- 15.3.7. Country

- 15.3.7.1. China

- 15.3.7.2. India

- 15.3.7.3. Japan

- 15.3.7.4. South Korea

- 15.3.7.5. Australia and New Zealand

- 15.3.7.6. Indonesia

- 15.3.7.7. Malaysia

- 15.3.7.8. Thailand

- 15.3.7.9. Vietnam

- 15.3.7.10. Rest of Asia Pacific

- 15.4. China Peptide-based Cancer Therapeutics Market

- 15.4.1. Country Segmental Analysis

- 15.4.2. Peptide Type

- 15.4.3. Mechanism of Action

- 15.4.4. Cancer Type

- 15.4.5. Route of Administration

- 15.4.6. Therapeutic Approach

- 15.4.7. End-Use

- 15.5. India Peptide-based Cancer Therapeutics Market

- 15.5.1. Country Segmental Analysis

- 15.5.2. Peptide Type

- 15.5.3. Mechanism of Action

- 15.5.4. Cancer Type

- 15.5.5. Route of Administration

- 15.5.6. Therapeutic Approach

- 15.5.7. End-Use

- 15.6. Japan Peptide-based Cancer Therapeutics Market

- 15.6.1. Country Segmental Analysis

- 15.6.2. Peptide Type

- 15.6.3. Mechanism of Action

- 15.6.4. Cancer Type

- 15.6.5. Route of Administration

- 15.6.6. Therapeutic Approach

- 15.6.7. End-Use

- 15.7. South Korea Peptide-based Cancer Therapeutics Market

- 15.7.1. Country Segmental Analysis

- 15.7.2. Peptide Type

- 15.7.3. Mechanism of Action

- 15.7.4. Cancer Type

- 15.7.5. Route of Administration

- 15.7.6. Therapeutic Approach

- 15.7.7. End-Use

- 15.8. Australia and New Zealand Peptide-based Cancer Therapeutics Market

- 15.8.1. Country Segmental Analysis

- 15.8.2. Peptide Type

- 15.8.3. Mechanism of Action

- 15.8.4. Cancer Type

- 15.8.5. Route of Administration

- 15.8.6. Therapeutic Approach

- 15.8.7. End-Use

- 15.9. Indonesia Peptide-based Cancer Therapeutics Market

- 15.9.1. Country Segmental Analysis

- 15.9.2. Peptide Type

- 15.9.3. Mechanism of Action

- 15.9.4. Cancer Type

- 15.9.5. Route of Administration

- 15.9.6. Therapeutic Approach

- 15.9.7. End-Use

- 15.10. Malaysia Peptide-based Cancer Therapeutics Market

- 15.10.1. Country Segmental Analysis

- 15.10.2. Peptide Type

- 15.10.3. Mechanism of Action

- 15.10.4. Cancer Type

- 15.10.5. Route of Administration

- 15.10.6. Therapeutic Approach

- 15.10.7. End-Use

- 15.11. Thailand Peptide-based Cancer Therapeutics Market

- 15.11.1. Country Segmental Analysis

- 15.11.2. Peptide Type

- 15.11.3. Mechanism of Action

- 15.11.4. Cancer Type

- 15.11.5. Route of Administration

- 15.11.6. Therapeutic Approach

- 15.11.7. End-Use

- 15.12. Vietnam Peptide-based Cancer Therapeutics Market

- 15.12.1. Country Segmental Analysis

- 15.12.2. Peptide Type

- 15.12.3. Mechanism of Action

- 15.12.4. Cancer Type

- 15.12.5. Route of Administration

- 15.12.6. Therapeutic Approach

- 15.12.7. End-Use

- 15.13. Rest of Asia Pacific Peptide-based Cancer Therapeutics Market

- 15.13.1. Country Segmental Analysis

- 15.13.2. Peptide Type

- 15.13.3. Mechanism of Action

- 15.13.4. Cancer Type

- 15.13.5. Route of Administration

- 15.13.6. Therapeutic Approach

- 15.13.7. End-Use

- 16. Middle East Peptide-based Cancer Therapeutics Market Analysis

- 16.1. Key Segment Analysis

- 16.2. Regional Snapshot

- 16.3. Middle East Peptide-based Cancer Therapeutics Market Size Value (US$ Bn), Analysis, and Forecasts, 2021-2035

- 16.3.1. Peptide Type

- 16.3.2. Mechanism of Action

- 16.3.3. Cancer Type

- 16.3.4. Route of Administration

- 16.3.5. Therapeutic Approach

- 16.3.6. End-Use

- 16.3.7. Country

- 16.3.7.1. Turkey

- 16.3.7.2. UAE

- 16.3.7.3. Saudi Arabia

- 16.3.7.4. Israel

- 16.3.7.5. Rest of Middle East

- 16.4. Turkey Peptide-based Cancer Therapeutics Market

- 16.4.1. Country Segmental Analysis

- 16.4.2. Peptide Type

- 16.4.3. Mechanism of Action

- 16.4.4. Cancer Type

- 16.4.5. Route of Administration

- 16.4.6. Therapeutic Approach

- 16.4.7. End-Use

- 16.5. UAE Peptide-based Cancer Therapeutics Market

- 16.5.1. Country Segmental Analysis

- 16.5.2. Peptide Type

- 16.5.3. Mechanism of Action

- 16.5.4. Cancer Type

- 16.5.5. Route of Administration

- 16.5.6. Therapeutic Approach

- 16.5.7. End-Use

- 16.6. Saudi Arabia Peptide-based Cancer Therapeutics Market

- 16.6.1. Country Segmental Analysis

- 16.6.2. Peptide Type

- 16.6.3. Mechanism of Action

- 16.6.4. Cancer Type

- 16.6.5. Route of Administration

- 16.6.6. Therapeutic Approach

- 16.6.7. End-Use

- 16.7. Israel Peptide-based Cancer Therapeutics Market

- 16.7.1. Country Segmental Analysis

- 16.7.2. Peptide Type

- 16.7.3. Mechanism of Action

- 16.7.4. Cancer Type

- 16.7.5. Route of Administration

- 16.7.6. Therapeutic Approach

- 16.7.7. End-Use

- 16.8. Rest of Middle East Peptide-based Cancer Therapeutics Market

- 16.8.1. Country Segmental Analysis

- 16.8.2. Peptide Type

- 16.8.3. Mechanism of Action

- 16.8.4. Cancer Type

- 16.8.5. Route of Administration

- 16.8.6. Therapeutic Approach

- 16.8.7. End-Use

- 17. Africa Peptide-based Cancer Therapeutics Market Analysis

- 17.1. Key Segment Analysis

- 17.2. Regional Snapshot

- 17.3. Africa Peptide-based Cancer Therapeutics Market Size Value (US$ Bn), Analysis, and Forecasts, 2021-2035

- 17.3.1. Peptide Type

- 17.3.2. Mechanism of Action

- 17.3.3. Cancer Type

- 17.3.4. Route of Administration

- 17.3.5. Therapeutic Approach

- 17.3.6. End-Use

- 17.3.7. Country

- 17.3.7.1. South Africa

- 17.3.7.2. Egypt

- 17.3.7.3. Nigeria

- 17.3.7.4. Algeria

- 17.3.7.5. Rest of Africa

- 17.4. South Africa Peptide-based Cancer Therapeutics Market

- 17.4.1. Country Segmental Analysis

- 17.4.2. Peptide Type

- 17.4.3. Mechanism of Action

- 17.4.4. Cancer Type

- 17.4.5. Route of Administration

- 17.4.6. Therapeutic Approach

- 17.4.7. End-Use

- 17.5. Egypt Peptide-based Cancer Therapeutics Market

- 17.5.1. Country Segmental Analysis

- 17.5.2. Peptide Type

- 17.5.3. Mechanism of Action

- 17.5.4. Cancer Type

- 17.5.5. Route of Administration

- 17.5.6. Therapeutic Approach

- 17.5.7. End-Use

- 17.6. Nigeria Peptide-based Cancer Therapeutics Market

- 17.6.1. Country Segmental Analysis

- 17.6.2. Peptide Type

- 17.6.3. Mechanism of Action

- 17.6.4. Cancer Type

- 17.6.5. Route of Administration

- 17.6.6. Therapeutic Approach

- 17.6.7. End-Use

- 17.7. Algeria Peptide-based Cancer Therapeutics Market

- 17.7.1. Country Segmental Analysis

- 17.7.2. Peptide Type

- 17.7.3. Mechanism of Action

- 17.7.4. Cancer Type

- 17.7.5. Route of Administration

- 17.7.6. Therapeutic Approach

- 17.7.7. End-Use

- 17.8. Rest of Africa Peptide-based Cancer Therapeutics Market

- 17.8.1. Country Segmental Analysis

- 17.8.2. Peptide Type

- 17.8.3. Mechanism of Action

- 17.8.4. Cancer Type

- 17.8.5. Route of Administration

- 17.8.6. Therapeutic Approach

- 17.8.7. End-Use

- 18. South America Peptide-based Cancer Therapeutics Market Analysis

- 18.1. Key Segment Analysis

- 18.2. Regional Snapshot

- 18.3. South America Peptide-based Cancer Therapeutics Market Size Value (US$ Bn), Analysis, and Forecasts, 2021-2035

- 18.3.1. Peptide Type

- 18.3.2. Mechanism of Action

- 18.3.3. Cancer Type

- 18.3.4. Route of Administration

- 18.3.5. Therapeutic Approach

- 18.3.6. End-Use

- 18.3.7. Country

- 18.3.7.1. Brazil

- 18.3.7.2. Argentina

- 18.3.7.3. Rest of South America

- 18.4. Brazil Peptide-based Cancer Therapeutics Market

- 18.4.1. Country Segmental Analysis

- 18.4.2. Peptide Type

- 18.4.3. Mechanism of Action

- 18.4.4. Cancer Type

- 18.4.5. Route of Administration

- 18.4.6. Therapeutic Approach

- 18.4.7. End-Use

- 18.5. Argentina Peptide-based Cancer Therapeutics Market

- 18.5.1. Country Segmental Analysis

- 18.5.2. Peptide Type

- 18.5.3. Mechanism of Action

- 18.5.4. Cancer Type

- 18.5.5. Route of Administration

- 18.5.6. Therapeutic Approach

- 18.5.7. End-Use

- 18.6. Rest of South America Peptide-based Cancer Therapeutics Market

- 18.6.1. Country Segmental Analysis

- 18.6.2. Peptide Type

- 18.6.3. Mechanism of Action

- 18.6.4. Cancer Type

- 18.6.5. Route of Administration

- 18.6.6. Therapeutic Approach

- 18.6.7. End-Use

- 19. Key Players/ Company Profile

- 19.1. Aileron Therapeutics Inc.

- 19.1.1. Company Details/ Overview

- 19.1.2. Company Financials

- 19.1.3. Key Customers and Competitors

- 19.1.4. Business/ Industry Portfolio

- 19.1.5. Product Portfolio/ Specification Details

- 19.1.6. Pricing Data

- 19.1.7. Strategic Overview

- 19.1.8. Recent Developments

- 19.2. Amgen Inc.

- 19.3. AstraZeneca PLC

- 19.4. Bachem Holding AG

- 19.5. Bristol-Myers Squibb Company

- 19.6. Eli Lilly and Company

- 19.7. GlaxoSmithKline plc

- 19.8. Ipsen Pharma

- 19.9. Johnson & Johnson

- 19.10. Merck & Co. Inc.

- 19.11. Novartis AG

- 19.12. Pepticom Ltd.

- 19.13. Pfizer Inc.

- 19.14. PolyPeptide Group

- 19.15. Polyphor Ltd.

- 19.16. Roche Holding AG

- 19.17. Sanofi SA

- 19.18. Takeda Pharmaceutical Company Limited

- 19.19. Teva Pharmaceutical Industries Ltd.

- 19.20. Zealand Pharma A/S

- 19.21. Other Key Players

- 19.1. Aileron Therapeutics Inc.

Note* - This is just tentative list of players. While providing the report, we will cover more number of players based on their revenue and share for each geography

Research Design

Our research design integrates both demand-side and supply-side analysis through a balanced combination of primary and secondary research methodologies. By utilizing both bottom-up and top-down approaches alongside rigorous data triangulation methods, we deliver robust market intelligence that supports strategic decision-making.

MarketGenics' comprehensive research design framework ensures the delivery of accurate, reliable, and actionable market intelligence. Through the integration of multiple research approaches, rigorous validation processes, and expert analysis, we provide our clients with the insights needed to make informed strategic decisions and capitalize on market opportunities.

MarketGenics leverages a dedicated industry panel of experts and a comprehensive suite of paid databases to effectively collect, consolidate, and analyze market intelligence.

Our approach has consistently proven to be reliable and effective in generating accurate market insights, identifying key industry trends, and uncovering emerging business opportunities.

Through both primary and secondary research, we capture and analyze critical company-level data such as manufacturing footprints, including technical centers, R&D facilities, sales offices, and headquarters.

Our expert panel further enhances our ability to estimate market size for specific brands based on validated field-level intelligence.

Our data mining techniques incorporate both parametric and non-parametric methods, allowing for structured data collection, sorting, processing, and cleaning.

Demand projections are derived from large-scale data sets analyzed through proprietary algorithms, culminating in robust and reliable market sizing.

Research Approach

The bottom-up approach builds market estimates by starting with the smallest addressable market units and systematically aggregating them to create comprehensive market size projections.

This method begins with specific, granular data points and builds upward to create the complete market landscape.

Customer Analysis → Segmental Analysis → Geographical Analysis

The top-down approach starts with the broadest possible market data and systematically narrows it down through a series of filters and assumptions to arrive at specific market segments or opportunities.

This method begins with the big picture and works downward to increasingly specific market slices.

TAM → SAM → SOM

Research Methods

Desk / Secondary Research

While analysing the market, we extensively study secondary sources, directories, and databases to identify and collect information useful for this technical, market-oriented, and commercial report. Secondary sources that we utilize are not only the public sources, but it is a combination of Open Source, Associations, Paid Databases, MG Repository & Knowledgebase, and others.

- Company websites, annual reports, financial reports, broker reports, and investor presentations

- National government documents, statistical databases and reports

- News articles, press releases and web-casts specific to the companies operating in the market, Magazines, reports, and others

- We gather information from commercial data sources for deriving company specific data such as segmental revenue, share for geography, product revenue, and others

- Internal and external proprietary databases (industry-specific), relevant patent, and regulatory databases

- Governing Bodies, Government Organizations

- Relevant Authorities, Country-specific Associations for Industries

We also employ the model mapping approach to estimate the product level market data through the players' product portfolio

Primary Research

Primary research/ interviews is vital in analyzing the market. Most of the cases involves paid primary interviews. Primary sources include primary interviews through e-mail interactions, telephonic interviews, surveys as well as face-to-face interviews with the different stakeholders across the value chain including several industry experts.

| Type of Respondents | Number of Primaries |

|---|---|

| Tier 2/3 Suppliers | ~20 |

| Tier 1 Suppliers | ~25 |

| End-users | ~25 |

| Industry Expert/ Panel/ Consultant | ~30 |

| Total | ~100 |

MG Knowledgebase

• Repository of industry blog, newsletter and case studies

• Online platform covering detailed market reports, and company profiles

Forecasting Factors and Models

Forecasting Factors

- Historical Trends – Past market patterns, cycles, and major events that shaped how markets behave over time. Understanding past trends helps predict future behavior.

- Industry Factors – Specific characteristics of the industry like structure, regulations, and innovation cycles that affect market dynamics.

- Macroeconomic Factors – Economic conditions like GDP growth, inflation, and employment rates that affect how much money people have to spend.

- Demographic Factors – Population characteristics like age, income, and location that determine who can buy your product.

- Technology Factors – How quickly people adopt new technology and how much technology infrastructure exists.

- Regulatory Factors – Government rules, laws, and policies that can help or restrict market growth.

- Competitive Factors – Analyzing competition structure such as degree of competition and bargaining power of buyers and suppliers.

Forecasting Models / Techniques

Multiple Regression Analysis

- Identify and quantify factors that drive market changes

- Statistical modeling to establish relationships between market drivers and outcomes

Time Series Analysis – Seasonal Patterns

- Understand regular cyclical patterns in market demand

- Advanced statistical techniques to separate trend, seasonal, and irregular components

Time Series Analysis – Trend Analysis

- Identify underlying market growth patterns and momentum

- Statistical analysis of historical data to project future trends

Expert Opinion – Expert Interviews

- Gather deep industry insights and contextual understanding

- In-depth interviews with key industry stakeholders

Multi-Scenario Development

- Prepare for uncertainty by modeling different possible futures

- Creating optimistic, pessimistic, and most likely scenarios

Time Series Analysis – Moving Averages

- Sophisticated forecasting for complex time series data

- Auto-regressive integrated moving average models with seasonal components

Econometric Models

- Apply economic theory to market forecasting

- Sophisticated economic models that account for market interactions

Expert Opinion – Delphi Method

- Harness collective wisdom of industry experts

- Structured, multi-round expert consultation process

Monte Carlo Simulation

- Quantify uncertainty and probability distributions

- Thousands of simulations with varying input parameters

Research Analysis

Our research framework is built upon the fundamental principle of validating market intelligence from both demand and supply perspectives. This dual-sided approach ensures comprehensive market understanding and reduces the risk of single-source bias.

Demand-Side Analysis: We understand end-user/application behavior, preferences, and market needs along with the penetration of the product for specific application.

Supply-Side Analysis: We estimate overall market revenue, analyze the segmental share along with industry capacity, competitive landscape, and market structure.

Validation & Evaluation

Data triangulation is a validation technique that uses multiple methods, sources, or perspectives to examine the same research question, thereby increasing the credibility and reliability of research findings. In market research, triangulation serves as a quality assurance mechanism that helps identify and minimize bias, validate assumptions, and ensure accuracy in market estimates.

- Data Source Triangulation – Using multiple data sources to examine the same phenomenon

- Methodological Triangulation – Using multiple research methods to study the same research question

- Investigator Triangulation – Using multiple researchers or analysts to examine the same data

- Theoretical Triangulation – Using multiple theoretical perspectives to interpret the same data

Custom Market Research Services

We will customise the research for you, in case the report listed above does not meet your requirements.

Get 10% Free Customisation