Advanced Semiconductor Packaging Technologies Market Size, Share & Trends Analysis Report by Technology Type (2.5 / 3D Packaging, Fan-Out Wafer Level Packaging (FOWLP), Fan-In Wafer Level Packaging (FIWLP), Flip Chip Packaging, Embedded Die Packaging, Chiplet-Based Packaging, System-in-Package (SiP), Other Technologies), Package Type, Material Type, Interconnect Technology, Node Size/Process Technology, Power Rating, I/O Density, Die Count, End-Use Industry , and Geography (North America, Europe, Asia Pacific, Middle East, Africa, and South America) – Global Industry Data, Trends, and Forecasts, 2026 – 2035

|

Market Structure & Evolution |

|

|

Segmental Data Insights |

|

|

Demand Trends |

|

|

Competitive Landscape |

|

|

Strategic Development |

|

|

Future Outlook & Opportunities |

|

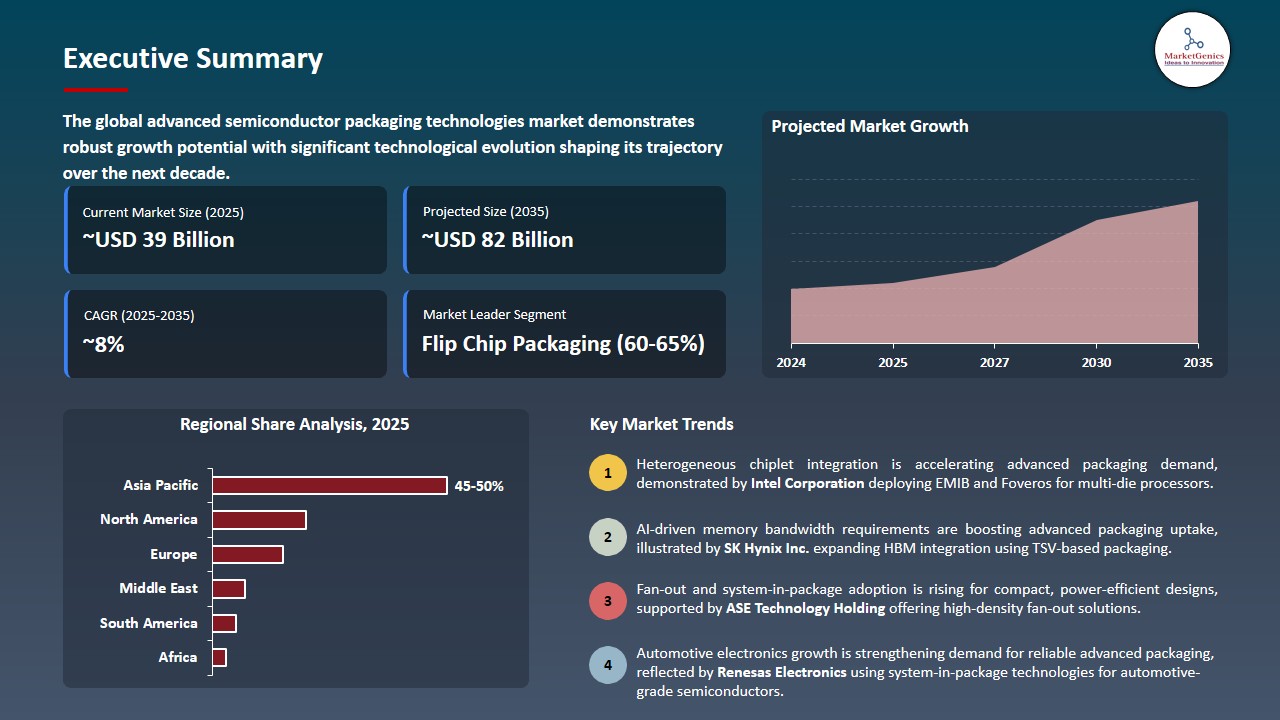

Advanced Semiconductor Packaging Technologies Market Size, Share, and Growth

The global advanced semiconductor packaging technologies market is experiencing robust growth, with its estimated value of USD 38.9 billion in the year 2025 and USD 81.7 billion by the period 2035, registering a CAGR of 7.7% during the forecast period.

“As the world's leading OSAT, ASE continues to innovate relentlessly for its customers. The evolution from automated IDE 1.0 to intelligent IDE 2.0 demonstrates the power of AI in advancing ASE's integrated design ecosystem. As packaging architectures grow more complex, IDE 2.0 enables significant gains in efficiency, quality, and design effectiveness while moving us closer to realizing the Digital Twins vision, stated by Yin Chang, Executive Vice President, ASE.”

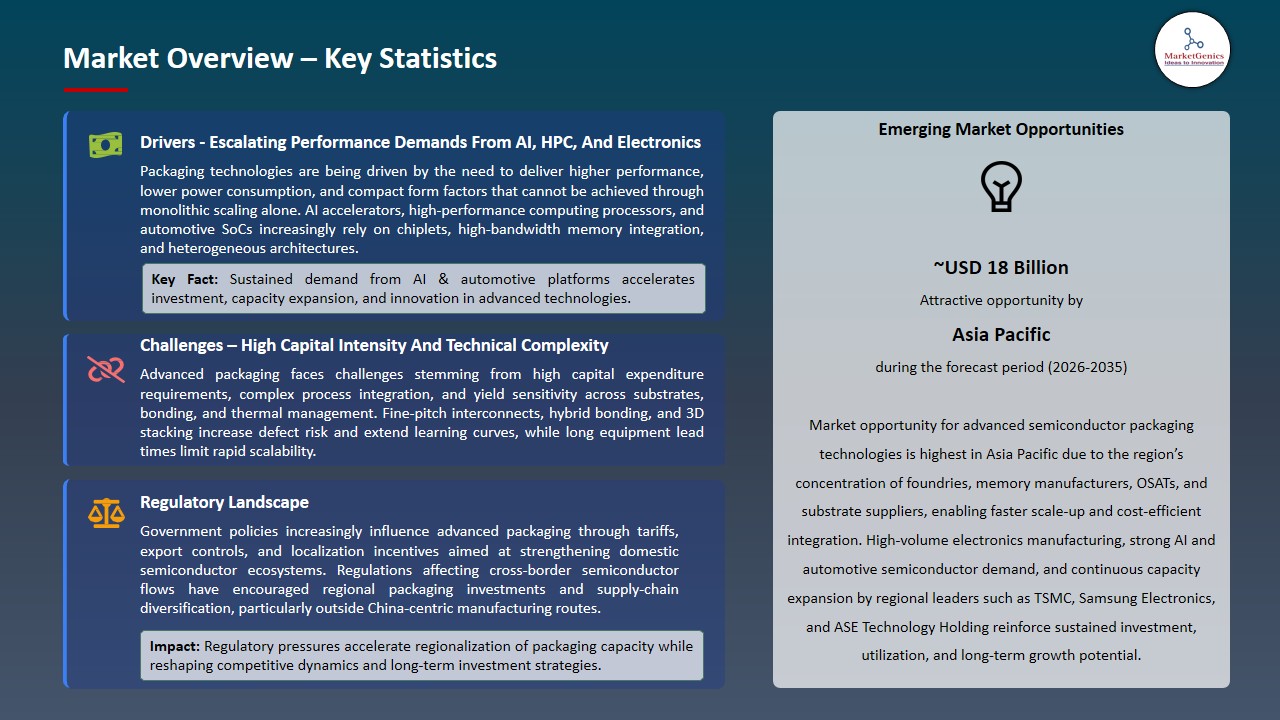

Advanced semiconductor packaging technologies are driven by explosive AI, high-performance computing, and automotive electronics adoption, which require heterogeneous integration, higher bandwidth, thermal efficiency, and cost optimization beyond traditional node scaling. The rising cost of wafer fabrication, declining the benefits of the Moore Law, and geopolitical re-alignment of supply chains compel the manufactures to deliver performance, yield and reliability improvements through advanced substrates, chiplets, fan-out and 3D stacking.

For instance, in January 2026, TSMC stated a growth of its high-capacity CoWoS and SoIC packaging in Arizona and Taiwan to accommodate the soaring demand of AI accelerator and HBM integration. Similarly, in May 2025, ASE Technology Holding presented its FOCoS-Bridge with improvements in TSV, reducing power loss and increasing the interconnect density of next-generation AI and HPC processor cores.

Meanwhile, in October 2025, Amkor Technology started building a large advanced packaging and test plant in Arizona, in accordance with long-term supply obligations with major fabless and IDM clients. The semiconductor value chains are redefined by accelerated advanced packaging investment towards integration leadership.

Adjacent opportunities include advanced substrate manufacturing for high-density interposers, HBM and advanced memory integration services, semiconductor packaging materials such as dielectrics and underfills, thermal management solutions including liquid and embedded cooling, and AI-driven electronic design automation tools enabling chiplet co-design and heterogeneous integration at scale. The expanded adjacencies increase the sophisticated packaging ecosystem, enhancing diversification of revenue and resilience to the market in the long run.

Advanced Semiconductor Packaging Technologies Market Dynamics and Trends

Driver: AI Memory Bandwidth Explosion Forces Packaging Innovation Across Global Supply Chains

-

Generative AI training and inference workloads are rapidly increasing high-bandwidth memory demands that are fueling the rapid development of advanced semiconductor packaging technologies. Logic scaling is simply not adequate any longer to meet throughput goals, changing architectural focus to tightly coupled logic-memory systems, which depend on the performance efficiency of advanced packaging.

- In January 2026, SK hynix declared an investment of USD 12.9 billion in a new AI-oriented advanced packaging plant in Cheongju, South Korea, to be committed to next-generation HBM stacking and integration. The announcement is an indication of the vertical integration of memory suppliers into packaging to achieve competitiveness at the system level and provide continuity in supply.

- Sophisticated packaging is now inseparable to memory roadmaps, especially to accelerators of artificial intelligence, which offers sustained demand on future platform refresh cycles. Memory-based AI designs make advanced packaging a growth engine which is structurally pivotal.

Restraint: Extreme Process Complexity and Yield Sensitivity Limit Rapid Industry-Wide Adoption

-

The pressures of increasing process complexity and yield sensitivity are being held in line in advanced semiconductor packaging, especially in the case of heterogeneous and multi-die assemblies. Advanced interposers, hybrid bonding and fine-pitch redistribution layers add compounded defect risk which adds to the cost per packaged device.

- In February 2025, Applied Materials announced that advanced packaging clients were lengthening cycle times in qualification as a result of narrower process margins across substrates, bonding and metrology at high interconnect densities. These limits reduce volume ramps and limit access by the smaller fabless companies who do not have long-term supply agreements.

- Despite the continued high demand, technical yield stabilization still acts as a gateway factor in the value chain. The complexity in the processes to be followed moderates the short-term scalability and maintains the barriers of entry.

Opportunity: Regional OSAT Expansion in Emerging Manufacturing Hubs Creates New Growth Avenues

-

The opportunity presented by geographic expansion through emerging manufacturing centers in search of localized semiconductor ecosystems is being opened by advanced semiconductor packaging technologies. Packaging is also being considered as a less time consuming and achievable entry mode as compared to wafer fabrication.

- In February 2025 ASE Technology Holding opened its fifth advanced packaging facility in Penang, Malaysia with a substantially larger floor space to help it serve next-generation AI and high-performance computing applications. This growth shows that the OSAT providers are aligning capacity development and regional talent supply and industry incentives allowing the customers to diversify the supply-chain risk without losing sophisticated integration capacity.

- Investments in regional OSAT speed up the capacity growth and enhance the resilience of supply-chain.

Key Trend: Domestic Packaging Ecosystems Gain Strategic Importance Amid Sovereignty Priorities

-

The trends in advanced semiconductor packaging are more and more characterized by national and domestic attempts to build end-to-end domestic semiconductor ecosystems. Packaging is becoming a key sovereignty layer that supplements the front-end manufacturing and design capacity.

- Tata Electronics joined a strategic partnership with Intel in December 2025 to produce and assemble semiconductors in India, with a distinct emphasis on advanced packaging at future OSAT plants. This transformation indicates that packaging is being staged as a part of national industrial policies and not a downstream practice.

- Domestic packaging proposals supported by policies ensure long-term market growth and strategic appropriateness.

Advanced-Semiconductor-Packaging-Technologies-Market Analysis and Segmental Data

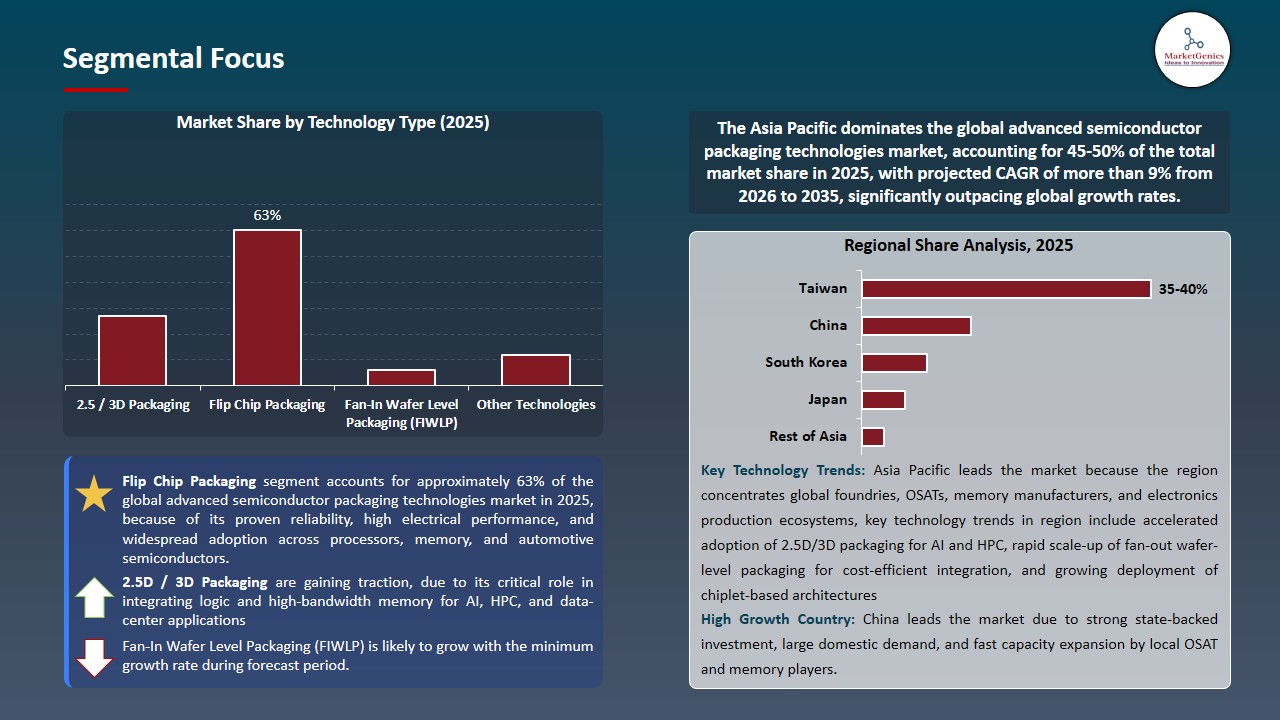

Flip Chip Packaging Anchors Performance Scaling in Heterogeneous Semiconductor Architectures

-

Demand for flip chip packaging is highest because it enables short interconnect lengths, superior electrical performance, and effective heat dissipation required by high-frequency AI, networking, and automotive processors. The technology has better I/O density and power integrity than wire bonding and is structurally compatible with advanced-node logic and chiplet-based system designs.

- Samsung Electro-Mechanics declared plans to scale up its superior chip packaging in January 2026, with the progression of AI hardware necessities, highlighting the long-term clientele in the selection of flip chip division in performance-focused equipment. The company intends to operate its flip-chip ball grid array (FC-BGA) assembly lines on full capacity in H2 2026, to accommodate high-end application processors and automotive SoCs.

- The market domination of flip chip packaging plays into its success as the early technology in advanced semiconductor packaging expansion.

Asia Pacific Concentrates Advanced Packaging Demand Through Manufacturing Depth and System Integration

-

Asia Pacific offers the highest demand advanced semiconductor packaging technologies due to the highest concentration of semiconductor back-end manufacturing in the region, which is backed by well-developed substrate, material, equipment, and engineering talent supply chains.

- Consumer devices, data centers, and automotive system high-volume electronics production are strongly co-located with packaging and testing processes to allow a design-to-production cycle to be aggressive and yield optimization to be faster. For instance, in March 2025, CDIL Semiconductors and Infineon Technologies Asia Pacific collaborated to package semiconductors to domestic customers. Infineon will provide its high-performance bare die wafers to CDIL which subsequently will package the same to discrete and module semiconductor products.

- Moreover, local governments in the region focus on semiconductor back-end capacity as a strategic industry and are speeding up permitting, infrastructure preparation, and worker training. This structural congruency allows regional producers to scale advanced packaging at a quicker rate and with reduced systemic riskiness than through different regions.

- In October 2025, Silicon Box declared that it had shipped 100-million-units of its high-end panel-level packaging (PLP) in its flagship factory in Tampines Wafer Park in Singapore. This proprietary technology can support chiplet integration is in capable of tackling issues in performance, scalability and costs in wafer-level and conventional packaging designs.

- With its ecosystem leadership, the Asia Pacific region has become the foremost provider of advanced packaging technologies.

Advanced-Semiconductor-Packaging-Technologies-Market Ecosystem

The advanced semiconductor packaging technologies market is highly consolidated, with global leadership held by ASE Technology Holding, Amkor Technology, JCET Group, Taiwan Semiconductor Manufacturing Company (TSMC) and Intel Corporation. These companies dominate the market through scale, proprietary integration platforms, and continuous advancements in 2.5D, 3D, fan-out, and heterogeneous packaging technologies that address rising performance, power efficiency, and form-factor requirements across AI, automotive, and high-performance computing applications.

Key players increasingly differentiate themselves through specialized solutions such as TSMC’s CoWoS and SoIC platforms for advanced logic-memory integration, Intel’s EMIB and Foveros technologies for chiplet-based architectures, and ASE’s high-density fan-out solutions designed for AI accelerators and networking processors. OSAT providers such as SPIL, JCET Group, and PTI focus on niche capabilities including advanced test integration, automotive-grade reliability, and system-in-package solutions, supporting faster time-to-market for fabless and IDM customers.

Government bodies and research institutions play a critical role in advancing packaging innovation. In September 2025, imec announced the expansion of its advanced packaging pilot line in Belgium, focusing on hybrid bonding and 3D interconnect technologies to improve energy efficiency and yield for sub-2-nanometer systems.

Market participants are also emphasizing portfolio diversification and integrated offerings that combine packaging, testing, and co-design services to enhance productivity and sustainability. In August 2025, Intel reported successful deployment of AI-driven process optimization across its advanced packaging lines, achieving measurable yield improvements and cycle-time reduction, reinforcing how digital technologies are accelerating operational efficiency across the advanced packaging value chain.

Recent Development and Strategic Overview:

-

In February 2025, Advanced Semiconductor Engineering, Inc. officially launched its fifth plant in Penang, expanding the floor space of ASE’s Malaysia facility from its current area of 1 million square feet to approximately 3.4 million square feet. The new plant harnesses the power of Artificial Intelligence of Things (AIoT) to enhance productivity and efficiency on the factory floor.

- In January 2025, Micron Technology, Inc. unveiled new High-Bandwidth Memory (HBM) advanced packaging facility adjacent to the company’s current facilities in Singapore. The launch of this facility will further strengthen Singapore’s local semiconductor ecosystem and innovation, operations are scheduled to begin in 2026.

Report Scope

|

Attribute |

Detail |

|

Market Size in 2025 |

USD 38.9 Bn |

|

Market Forecast Value in 2035 |

USD 81.7 Bn |

|

Growth Rate (CAGR) |

7.7% |

|

Forecast Period |

2026 – 2035 |

|

Historical Data Available for |

2021 – 2024 |

|

Market Size Units |

US$ Billion for Value |

|

Report Format |

Electronic (PDF) + Excel |

|

Regions and Countries Covered |

|||||

|

North America |

Europe |

Asia Pacific |

Middle East |

Africa |

South America |

|

|

|

|

|

|

|

Companies Covered |

|||||

|

|

|

|

|

|

Advanced-Semiconductor-Packaging-Technologies-Market Segmentation and Highlights

|

Segment |

Sub-segment |

|

Advanced Semiconductor Packaging Technologies Market, By Technology Type |

|

|

Advanced Semiconductor Packaging Technologies Market, By Material Type |

|

|

Advanced Semiconductor Packaging Technologies Market, By Interconnect Technology |

|

|

Advanced Semiconductor Packaging Technologies Market, By Node Size/Process Technology |

|

|

Advanced Semiconductor Packaging Technologies Market, By Power Rating |

|

|

Advanced Semiconductor Packaging Technologies Market, By I/O Density |

|

|

Advanced Semiconductor Packaging Technologies Market, By Die Count |

|

|

Advanced Semiconductor Packaging Technologies Market, By End-Use Industry |

|

Frequently Asked Questions

Table of Contents

- 1. Research Methodology and Assumptions

- 1.1. Definitions

- 1.2. Research Design and Approach

- 1.3. Data Collection Methods

- 1.4. Base Estimates and Calculations

- 1.5. Forecasting Models

- 1.5.1. Key Forecast Factors & Impact Analysis

- 1.6. Secondary Research

- 1.6.1. Open Sources

- 1.6.2. Paid Databases

- 1.6.3. Associations

- 1.7. Primary Research

- 1.7.1. Primary Sources

- 1.7.2. Primary Interviews with Stakeholders across Ecosystem

- 2. Executive Summary

- 2.1. Global Advanced Semiconductor Packaging Technologies Market Outlook

- 2.1.1. Advanced Semiconductor Packaging Technologies Market Size (Value - US$ Bn), and Forecasts, 2021-2035

- 2.1.2. Compounded Annual Growth Rate Analysis

- 2.1.3. Growth Opportunity Analysis

- 2.1.4. Segmental Share Analysis

- 2.1.5. Geographical Share Analysis

- 2.2. Market Analysis and Facts

- 2.3. Supply-Demand Analysis

- 2.4. Competitive Benchmarking

- 2.5. Go-to- Market Strategy

- 2.5.1. Customer/ End-use Industry Assessment

- 2.5.2. Growth Opportunity Data, 2026-2035

- 2.5.2.1. Regional Data

- 2.5.2.2. Country Data

- 2.5.2.3. Segmental Data

- 2.5.3. Identification of Potential Market Spaces

- 2.5.4. GAP Analysis

- 2.5.5. Potential Attractive Price Points

- 2.5.6. Prevailing Market Risks & Challenges

- 2.5.7. Preferred Sales & Marketing Strategies

- 2.5.8. Key Recommendations and Analysis

- 2.5.9. A Way Forward

- 2.1. Global Advanced Semiconductor Packaging Technologies Market Outlook

- 3. Industry Data and Premium Insights

- 3.1. Global Advanced Semiconductor Packaging Technologies Industry Overview, 2025

- 3.1.1. Semiconductors & Electronics Industry Ecosystem Analysis

- 3.1.2. Key Trends for Semiconductors & Electronics Industry

- 3.1.3. Regional Distribution for Semiconductors & Electronics Industry

- 3.2. Supplier Customer Data

- 3.3. Technology Roadmap and Developments

- 3.4. Trade Analysis

- 3.4.1. Import & Export Analysis, 2025

- 3.4.2. Top Importing Countries

- 3.4.3. Top Exporting Countries

- 3.5. Trump Tariff Impact Analysis

- 3.5.1. Manufacturer

- 3.5.1.1. Based on the component & Raw material

- 3.5.2. Supply Chain

- 3.5.3. End Consumer

- 3.5.1. Manufacturer

- 3.6. Raw Material Analysis

- 3.1. Global Advanced Semiconductor Packaging Technologies Industry Overview, 2025

- 4. Market Overview

- 4.1. Market Dynamics

- 4.1.1. Drivers

- 4.1.1.1. Rising adoption of AI and high-performance computing workloads requiring high-bandwidth, low-latency logic–memory integration.

- 4.1.1.2. Increasing shift toward chiplet architectures and heterogeneous integration to optimize performance, cost, and scalability.

- 4.1.1.3. Growing demand from automotive electrification and advanced driver-assistance systems requiring compact, reliable packaging solutions.

- 4.1.2. Restraints

- 4.1.2.1. High capital intensity and long ramp-up cycles for advanced packaging facilities and equipment.

- 4.1.2.2. Limited availability and long qualification timelines of advanced substrates and materials.

- 4.1.1. Drivers

- 4.2. Key Trend Analysis

- 4.3. Regulatory Framework

- 4.3.1. Key Regulations, Norms, and Subsidies, by Key Countries

- 4.3.2. Tariffs and Standards

- 4.3.3. Impact Analysis of Regulations on the Market

- 4.4. Value Chain Analysis

- 4.4.1. Raw Material Suppliers

- 4.4.2. Semiconductor Packaging Companies

- 4.4.3. Dealers/ Distributors

- 4.4.4. End-users/ Customers

- 4.5. Porter’s Five Forces Analysis

- 4.6. PESTEL Analysis

- 4.7. Global Advanced Semiconductor Packaging Technologies Market Demand

- 4.7.1. Historical Market Size – in Value (US$ Bn), 2020-2024

- 4.7.2. Current and Future Market Size – in Value (US$ Bn), 2026–2035

- 4.7.2.1. Y-o-Y Growth Trends

- 4.7.2.2. Absolute $ Opportunity Assessment

- 4.1. Market Dynamics

- 5. Competition Landscape

- 5.1. Competition structure

- 5.1.1. Fragmented v/s consolidated

- 5.2. Company Share Analysis, 2025

- 5.2.1. Global Company Market Share

- 5.2.2. By Region

- 5.2.2.1. North America

- 5.2.2.2. Europe

- 5.2.2.3. Asia Pacific

- 5.2.2.4. Middle East

- 5.2.2.5. Africa

- 5.2.2.6. South America

- 5.3. Product Comparison Matrix

- 5.3.1. Specifications

- 5.3.2. Market Positioning

- 5.3.3. Pricing

- 5.1. Competition structure

- 6. Global Advanced Semiconductor Packaging Technologies Market Analysis, by Technology Type

- 6.1. Key Segment Analysis

- 6.2. Advanced Semiconductor Packaging Technologies Market Size (Value - US$ Bn), Analysis, and Forecasts, Technology Type, 2021-2035

- 6.2.1. 5 / 3D Packaging

- 6.2.1.1. 5D Packaging

- 6.2.1.1.1. Silicon Interposer

- 6.2.1.1.2. Organic Interposer

- 6.2.1.2. 3D Packaging

- 6.2.1.2.1. Through-Silicon Via (TSV)

- 6.2.1.2.2. Monolithic 3D

- 6.2.1.2.3. Stacked Die

- 6.2.1.1. 5D Packaging

- 6.2.2. Fan-Out Wafer Level Packaging (FOWLP)

- 6.2.2.1. eWLB (Embedded Wafer Level Ball Grid Array)

- 6.2.2.2. InFO (Integrated Fan-Out)

- 6.2.2.3. FOPLP (Fan-Out Panel Level Packaging)

- 6.2.3. Fan-In Wafer Level Packaging (FIWLP)

- 6.2.4. Flip Chip Packaging

- 6.2.4.1. Flip Chip Ball Grid Array (FCBGA)

- 6.2.4.2. Flip Chip Chip-Scale Package (FCCSP)

- 6.2.4.3. Flip Chip on Board (FCOB)

- 6.2.4.4. Others

- 6.2.5. Embedded Die Packaging

- 6.2.6. Chiplet-Based Packaging

- 6.2.7. System-in-Package (SiP)

- 6.2.8. Other Technologies

- 6.2.1. 5 / 3D Packaging

- 7. Global Advanced Semiconductor Packaging Technologies Market Analysis, by Package Type

- 7.1. Key Segment Analysis

- 7.2. Advanced Semiconductor Packaging Technologies Market Size (Value - US$ Bn), Analysis, and Forecasts, by Package Type, 2021-2035

- 7.2.1. Ball Grid Array (BGA)

- 7.2.2. Chip Scale Package (CSP)

- 7.2.3. Quad Flat No-Lead (QFN)

- 7.2.4. Land Grid Array (LGA)

- 7.2.5. Wafer Level Chip Scale Package (WLCSP)

- 7.2.6. Multi-Chip Module (MCM)

- 8. Global Advanced Semiconductor Packaging Technologies Market Analysis, by Material Type

- 8.1. Key Segment Analysis

- 8.2. Advanced Semiconductor Packaging Technologies Market Size (Value - US$ Bn), Analysis, and Forecasts, by Material Type, 2021-2035

- 8.2.1. Organic Substrates

- 8.2.1.1. Ajinomoto Build-up Film (ABF)

- 8.2.1.2. Standard Build-up

- 8.2.2. Silicon Substrates

- 8.2.3. Glass Substrates

- 8.2.4. Ceramic Substrates

- 8.2.5. Redistribution Layer (RDL) Materials

- 8.2.5.1. Polymer-based RDL

- 8.2.5.2. Glass-based RDL

- 8.2.6. Underfill Materials

- 8.2.7. Thermal Interface Materials (TIM)

- 8.2.8. Solder Bump Materials

- 8.2.9. Others

- 8.2.1. Organic Substrates

- 9. Global Advanced Semiconductor Packaging Technologies Market Analysis, by Interconnect Technology

- 9.1. Key Segment Analysis

- 9.2. Advanced Semiconductor Packaging Technologies Market Size (Value - US$ Bn), Analysis, and Forecasts, by Interconnect Technology, 2021-2035

- 9.2.1. Wire Bonding

- 9.2.2. Flip Chip Bonding

- 9.2.3. Through-Silicon Via (TSV)

- 9.2.4. Micro-Bumping

- 9.2.5. Hybrid Bonding

- 9.2.5.1. Copper-to-Copper Hybrid Bonding

- 9.2.5.2. Oxide-to-Oxide Hybrid Bonding

- 9.2.6. Copper Pillar

- 10. Global Advanced Semiconductor Packaging Technologies Market Analysis, by Node Size/Process Technology

- 10.1. Key Segment Analysis

- 10.2. Advanced Semiconductor Packaging Technologies Market Size (Value - US$ Bn), Analysis, and Forecasts, by Node Size/Process Technology, 2021-2035

- 10.2.1. Below 7nm

- 10.2.2. 7nm - 10nm

- 10.2.3. 10nm - 14nm

- 10.2.4. 16nm - 22nm

- 10.2.5. 28nm - 45nm

- 10.2.6. Above 45nm

- 11. Global Advanced Semiconductor Packaging Technologies Market Analysis, by Power Rating

- 11.1. Key Segment Analysis

- 11.2. Advanced Semiconductor Packaging Technologies Market Size (Value - US$ Bn), Analysis, and Forecasts, by Power Rating, 2021-2035

- 11.2.1. Below 5W

- 11.2.2. 5W - 50W

- 11.2.3. 50W - 150W

- 11.2.4. Above 150W

- 12. Global Advanced Semiconductor Packaging Technologies Market Analysis, by I/O Density

- 12.1. Key Segment Analysis

- 12.2. Advanced Semiconductor Packaging Technologies Market Size (Value - US$ Bn), Analysis, and Forecasts, by I/O Density, 2021-2035

- 12.2.1. Below 500 I/Os

- 12.2.2. 500 - 2000 I/Os

- 12.2.3. 2000 - 5000 I/Os

- 12.2.4. Above 5000 I/Os

- 13. Global Advanced Semiconductor Packaging Technologies Market Analysis, by Die Count

- 13.1. Key Segment Analysis

- 13.2. Advanced Semiconductor Packaging Technologies Market Size (Value - US$ Bn), Analysis, and Forecasts, by Die Count, 2021-2035

- 13.2.1. Single Die

- 13.2.2. Dual Die

- 13.2.3. Multiple Die (3-8 Dies)

- 13.2.4. High-Density Multi-Die (Above 8 Dies)

- 14. Global Advanced Semiconductor Packaging Technologies Market Analysis, by End-Use Industry

- 14.1. Key Segment Analysis

- 14.2. Advanced Semiconductor Packaging Technologies Market Size (Value - US$ Bn), Analysis, and Forecasts, by End-Use Industry, 2021-2035

- 14.2.1. Consumer Electronics

- 14.2.2. Automotive

- 14.2.3. Telecommunications & Networking

- 14.2.4. Data Centers & Cloud Computing

- 14.2.5. Artificial Intelligence & Machine Learning

- 14.2.6. Industrial & IoT

- 14.2.7. Aerospace & Defense

- 14.2.8. Medical & Healthcare

- 14.2.9. Computing & Graphics

- 14.2.10. Other Industries

- 15. Global Advanced Semiconductor Packaging Technologies Market Analysis, by Region

- 15.1. Key Findings

- 15.2. Advanced Semiconductor Packaging Technologies Market Size (Value - US$ Mn), Analysis, and Forecasts, by Region, 2021-2035

- 15.2.1. North America

- 15.2.2. Europe

- 15.2.3. Asia Pacific

- 15.2.4. Middle East

- 15.2.5. Africa

- 15.2.6. South America

- 16. North America Advanced Semiconductor Packaging Technologies Market Analysis

- 16.1. Key Segment Analysis

- 16.2. Regional Snapshot

- 16.3. North America Advanced Semiconductor Packaging Technologies Market Size Value - US$ Bn), Analysis, and Forecasts, 2021-2035

- 16.3.1. Technology Type

- 16.3.2. Package Type

- 16.3.3. Material Type

- 16.3.4. Interconnect Technology

- 16.3.5. Node Size/Process Technology

- 16.3.6. Power Rating

- 16.3.7. I/O Density

- 16.3.8. Die Count

- 16.3.9. End-Use Industry

- 16.3.10. Country

- 16.3.10.1. USA

- 16.3.10.2. Canada

- 16.3.10.3. Mexico

- 16.4. USA Advanced Semiconductor Packaging Technologies Market

- 16.4.1. Country Segmental Analysis

- 16.4.2. Technology Type

- 16.4.3. Package Type

- 16.4.4. Material Type

- 16.4.5. Interconnect Technology

- 16.4.6. Node Size/Process Technology

- 16.4.7. Power Rating

- 16.4.8. I/O Density

- 16.4.9. Die Count

- 16.4.10. End-Use Industry

- 16.5. Canada Advanced Semiconductor Packaging Technologies Market

- 16.5.1. Country Segmental Analysis

- 16.5.2. Technology Type

- 16.5.3. Package Type

- 16.5.4. Material Type

- 16.5.5. Interconnect Technology

- 16.5.6. Node Size/Process Technology

- 16.5.7. Power Rating

- 16.5.8. I/O Density

- 16.5.9. Die Count

- 16.5.10. End-Use Industry

- 16.6. Mexico Advanced Semiconductor Packaging Technologies Market

- 16.6.1. Country Segmental Analysis

- 16.6.2. Technology Type

- 16.6.3. Package Type

- 16.6.4. Material Type

- 16.6.5. Interconnect Technology

- 16.6.6. Node Size/Process Technology

- 16.6.7. Power Rating

- 16.6.8. I/O Density

- 16.6.9. Die Count

- 16.6.10. End-Use Industry

- 17. Europe Advanced Semiconductor Packaging Technologies Market Analysis

- 17.1. Key Segment Analysis

- 17.2. Regional Snapshot

- 17.3. Europe Advanced Semiconductor Packaging Technologies Market Size (Value - US$ Bn), Analysis, and Forecasts, 2021-2035

- 17.3.1. Technology Type

- 17.3.2. Package Type

- 17.3.3. Material Type

- 17.3.4. Interconnect Technology

- 17.3.5. Node Size/Process Technology

- 17.3.6. Power Rating

- 17.3.7. I/O Density

- 17.3.8. Die Count

- 17.3.9. End-Use Industry

- 17.3.10. Country

- 17.3.10.1. Germany

- 17.3.10.2. United Kingdom

- 17.3.10.3. France

- 17.3.10.4. Italy

- 17.3.10.5. Spain

- 17.3.10.6. Netherlands

- 17.3.10.7. Nordic Countries

- 17.3.10.8. Poland

- 17.3.10.9. Russia & CIS

- 17.3.10.10. Rest of Europe

- 17.4. Germany Advanced Semiconductor Packaging Technologies Market

- 17.4.1. Country Segmental Analysis

- 17.4.2. Technology Type

- 17.4.3. Package Type

- 17.4.4. Material Type

- 17.4.5. Interconnect Technology

- 17.4.6. Node Size/Process Technology

- 17.4.7. Power Rating

- 17.4.8. I/O Density

- 17.4.9. Die Count

- 17.4.10. End-Use Industry

- 17.5. United Kingdom Advanced Semiconductor Packaging Technologies Market

- 17.5.1. Country Segmental Analysis

- 17.5.2. Technology Type

- 17.5.3. Package Type

- 17.5.4. Material Type

- 17.5.5. Interconnect Technology

- 17.5.6. Node Size/Process Technology

- 17.5.7. Power Rating

- 17.5.8. I/O Density

- 17.5.9. Die Count

- 17.5.10. End-Use Industry

- 17.6. France Advanced Semiconductor Packaging Technologies Market

- 17.6.1. Country Segmental Analysis

- 17.6.2. Technology Type

- 17.6.3. Package Type

- 17.6.4. Material Type

- 17.6.5. Interconnect Technology

- 17.6.6. Node Size/Process Technology

- 17.6.7. Power Rating

- 17.6.8. I/O Density

- 17.6.9. Die Count

- 17.6.10. End-Use Industry

- 17.7. Italy Advanced Semiconductor Packaging Technologies Market

- 17.7.1. Country Segmental Analysis

- 17.7.2. Technology Type

- 17.7.3. Package Type

- 17.7.4. Material Type

- 17.7.5. Interconnect Technology

- 17.7.6. Node Size/Process Technology

- 17.7.7. Power Rating

- 17.7.8. I/O Density

- 17.7.9. Die Count

- 17.7.10. End-Use Industry

- 17.8. Spain Advanced Semiconductor Packaging Technologies Market

- 17.8.1. Country Segmental Analysis

- 17.8.2. Technology Type

- 17.8.3. Package Type

- 17.8.4. Material Type

- 17.8.5. Interconnect Technology

- 17.8.6. Node Size/Process Technology

- 17.8.7. Power Rating

- 17.8.8. I/O Density

- 17.8.9. Die Count

- 17.8.10. End-Use Industry

- 17.9. Netherlands Advanced Semiconductor Packaging Technologies Market

- 17.9.1. Country Segmental Analysis

- 17.9.2. Technology Type

- 17.9.3. Package Type

- 17.9.4. Material Type

- 17.9.5. Interconnect Technology

- 17.9.6. Node Size/Process Technology

- 17.9.7. Power Rating

- 17.9.8. I/O Density

- 17.9.9. Die Count

- 17.9.10. End-Use Industry

- 17.10. Nordic Countries Advanced Semiconductor Packaging Technologies Market

- 17.10.1. Country Segmental Analysis

- 17.10.2. Technology Type

- 17.10.3. Package Type

- 17.10.4. Material Type

- 17.10.5. Interconnect Technology

- 17.10.6. Node Size/Process Technology

- 17.10.7. Power Rating

- 17.10.8. I/O Density

- 17.10.9. Die Count

- 17.10.10. End-Use Industry

- 17.11. Poland Advanced Semiconductor Packaging Technologies Market

- 17.11.1. Country Segmental Analysis

- 17.11.2. Technology Type

- 17.11.3. Package Type

- 17.11.4. Material Type

- 17.11.5. Interconnect Technology

- 17.11.6. Node Size/Process Technology

- 17.11.7. Power Rating

- 17.11.8. I/O Density

- 17.11.9. Die Count

- 17.11.10. End-Use Industry

- 17.12. Russia & CIS Advanced Semiconductor Packaging Technologies Market

- 17.12.1. Country Segmental Analysis

- 17.12.2. Technology Type

- 17.12.3. Package Type

- 17.12.4. Material Type

- 17.12.5. Interconnect Technology

- 17.12.6. Node Size/Process Technology

- 17.12.7. Power Rating

- 17.12.8. I/O Density

- 17.12.9. Die Count

- 17.12.10. End-Use Industry

- 17.13. Rest of Europe Advanced Semiconductor Packaging Technologies Market

- 17.13.1. Country Segmental Analysis

- 17.13.2. Technology Type

- 17.13.3. Package Type

- 17.13.4. Material Type

- 17.13.5. Interconnect Technology

- 17.13.6. Node Size/Process Technology

- 17.13.7. Power Rating

- 17.13.8. I/O Density

- 17.13.9. Die Count

- 17.13.10. End-Use Industry

- 18. Asia Pacific Advanced Semiconductor Packaging Technologies Market Analysis

- 18.1. Key Segment Analysis

- 18.2. Regional Snapshot

- 18.3. Asia Pacific Advanced Semiconductor Packaging Technologies Market Size (Value - US$ Bn), Analysis, and Forecasts, 2021-2035

- 18.3.1. Technology Type

- 18.3.2. Package Type

- 18.3.3. Material Type

- 18.3.4. Interconnect Technology

- 18.3.5. Node Size/Process Technology

- 18.3.6. Power Rating

- 18.3.7. I/O Density

- 18.3.8. Die Count

- 18.3.9. End-Use Industry

- 18.3.10. Country

- 18.3.10.1. China

- 18.3.10.2. India

- 18.3.10.3. Japan

- 18.3.10.4. South Korea

- 18.3.10.5. Australia and New Zealand

- 18.3.10.6. Indonesia

- 18.3.10.7. Malaysia

- 18.3.10.8. Thailand

- 18.3.10.9. Vietnam

- 18.3.10.10. Rest of Asia Pacific

- 18.4. China Advanced Semiconductor Packaging Technologies Market

- 18.4.1. Country Segmental Analysis

- 18.4.2. Technology Type

- 18.4.3. Package Type

- 18.4.4. Material Type

- 18.4.5. Interconnect Technology

- 18.4.6. Node Size/Process Technology

- 18.4.7. Power Rating

- 18.4.8. I/O Density

- 18.4.9. Die Count

- 18.4.10. End-Use Industry

- 18.5. India Advanced Semiconductor Packaging Technologies Market

- 18.5.1. Country Segmental Analysis

- 18.5.2. Technology Type

- 18.5.3. Package Type

- 18.5.4. Material Type

- 18.5.5. Interconnect Technology

- 18.5.6. Node Size/Process Technology

- 18.5.7. Power Rating

- 18.5.8. I/O Density

- 18.5.9. Die Count

- 18.5.10. End-Use Industry

- 18.6. Japan Advanced Semiconductor Packaging Technologies Market

- 18.6.1. Country Segmental Analysis

- 18.6.2. Technology Type

- 18.6.3. Package Type

- 18.6.4. Material Type

- 18.6.5. Interconnect Technology

- 18.6.6. Node Size/Process Technology

- 18.6.7. Power Rating

- 18.6.8. I/O Density

- 18.6.9. Die Count

- 18.6.10. End-Use Industry

- 18.7. South Korea Advanced Semiconductor Packaging Technologies Market

- 18.7.1. Country Segmental Analysis

- 18.7.2. Technology Type

- 18.7.3. Package Type

- 18.7.4. Material Type

- 18.7.5. Interconnect Technology

- 18.7.6. Node Size/Process Technology

- 18.7.7. Power Rating

- 18.7.8. I/O Density

- 18.7.9. Die Count

- 18.7.10. End-Use Industry

- 18.8. Australia and New Zealand Advanced Semiconductor Packaging Technologies Market

- 18.8.1. Country Segmental Analysis

- 18.8.2. Technology Type

- 18.8.3. Package Type

- 18.8.4. Material Type

- 18.8.5. Interconnect Technology

- 18.8.6. Node Size/Process Technology

- 18.8.7. Power Rating

- 18.8.8. I/O Density

- 18.8.9. Die Count

- 18.8.10. End-Use Industry

- 18.9. Indonesia Advanced Semiconductor Packaging Technologies Market

- 18.9.1. Country Segmental Analysis

- 18.9.2. Technology Type

- 18.9.3. Package Type

- 18.9.4. Material Type

- 18.9.5. Interconnect Technology

- 18.9.6. Node Size/Process Technology

- 18.9.7. Power Rating

- 18.9.8. I/O Density

- 18.9.9. Die Count

- 18.9.10. End-Use Industry

- 18.10. Malaysia Advanced Semiconductor Packaging Technologies Market

- 18.10.1. Country Segmental Analysis

- 18.10.2. Technology Type

- 18.10.3. Package Type

- 18.10.4. Material Type

- 18.10.5. Interconnect Technology

- 18.10.6. Node Size/Process Technology

- 18.10.7. Power Rating

- 18.10.8. I/O Density

- 18.10.9. Die Count

- 18.10.10. End-Use Industry

- 18.11. Thailand Advanced Semiconductor Packaging Technologies Market

- 18.11.1. Country Segmental Analysis

- 18.11.2. Technology Type

- 18.11.3. Package Type

- 18.11.4. Material Type

- 18.11.5. Interconnect Technology

- 18.11.6. Node Size/Process Technology

- 18.11.7. Power Rating

- 18.11.8. I/O Density

- 18.11.9. Die Count

- 18.11.10. End-Use Industry

- 18.12. Vietnam Advanced Semiconductor Packaging Technologies Market

- 18.12.1. Country Segmental Analysis

- 18.12.2. Technology Type

- 18.12.3. Package Type

- 18.12.4. Material Type

- 18.12.5. Interconnect Technology

- 18.12.6. Node Size/Process Technology

- 18.12.7. Power Rating

- 18.12.8. I/O Density

- 18.12.9. Die Count

- 18.12.10. End-Use Industry

- 18.13. Rest of Asia Pacific Advanced Semiconductor Packaging Technologies Market

- 18.13.1. Country Segmental Analysis

- 18.13.2. Technology Type

- 18.13.3. Package Type

- 18.13.4. Material Type

- 18.13.5. Interconnect Technology

- 18.13.6. Node Size/Process Technology

- 18.13.7. Power Rating

- 18.13.8. I/O Density

- 18.13.9. Die Count

- 18.13.10. End-Use Industry

- 19. Middle East Advanced Semiconductor Packaging Technologies Market Analysis

- 19.1. Key Segment Analysis

- 19.2. Regional Snapshot

- 19.3. Middle East Advanced Semiconductor Packaging Technologies Market Size (Value - US$ Bn), Analysis, and Forecasts, 2021-2035

- 19.3.1. Technology Type

- 19.3.2. Package Type

- 19.3.3. Material Type

- 19.3.4. Interconnect Technology

- 19.3.5. Node Size/Process Technology

- 19.3.6. Power Rating

- 19.3.7. I/O Density

- 19.3.8. Die Count

- 19.3.9. End-Use Industry

- 19.3.10. Country

- 19.3.10.1. Turkey

- 19.3.10.2. UAE

- 19.3.10.3. Saudi Arabia

- 19.3.10.4. Israel

- 19.3.10.5. Rest of Middle East

- 19.4. Turkey Advanced Semiconductor Packaging Technologies Market

- 19.4.1. Country Segmental Analysis

- 19.4.2. Technology Type

- 19.4.3. Package Type

- 19.4.4. Material Type

- 19.4.5. Interconnect Technology

- 19.4.6. Node Size/Process Technology

- 19.4.7. Power Rating

- 19.4.8. I/O Density

- 19.4.9. Die Count

- 19.4.10. End-Use Industry

- 19.5. UAE Advanced Semiconductor Packaging Technologies Market

- 19.5.1. Country Segmental Analysis

- 19.5.2. Technology Type

- 19.5.3. Package Type

- 19.5.4. Material Type

- 19.5.5. Interconnect Technology

- 19.5.6. Node Size/Process Technology

- 19.5.7. Power Rating

- 19.5.8. I/O Density

- 19.5.9. Die Count

- 19.5.10. End-Use Industry

- 19.6. Saudi Arabia Advanced Semiconductor Packaging Technologies Market

- 19.6.1. Country Segmental Analysis

- 19.6.2. Technology Type

- 19.6.3. Package Type

- 19.6.4. Material Type

- 19.6.5. Interconnect Technology

- 19.6.6. Node Size/Process Technology

- 19.6.7. Power Rating

- 19.6.8. I/O Density

- 19.6.9. Die Count

- 19.6.10. End-Use Industry

- 19.7. Israel Advanced Semiconductor Packaging Technologies Market

- 19.7.1. Country Segmental Analysis

- 19.7.2. Technology Type

- 19.7.3. Package Type

- 19.7.4. Material Type

- 19.7.5. Interconnect Technology

- 19.7.6. Node Size/Process Technology

- 19.7.7. Power Rating

- 19.7.8. I/O Density

- 19.7.9. Die Count

- 19.7.10. End-Use Industry

- 19.8. Rest of Middle East Advanced Semiconductor Packaging Technologies Market

- 19.8.1. Country Segmental Analysis

- 19.8.2. Technology Type

- 19.8.3. Package Type

- 19.8.4. Material Type

- 19.8.5. Interconnect Technology

- 19.8.6. Node Size/Process Technology

- 19.8.7. Power Rating

- 19.8.8. I/O Density

- 19.8.9. Die Count

- 19.8.10. End-Use Industry

- 20. Africa Advanced Semiconductor Packaging Technologies Market Analysis

- 20.1. Key Segment Analysis

- 20.2. Regional Snapshot

- 20.3. Africa Advanced Semiconductor Packaging Technologies Market Size (Value - US$ Bn), Analysis, and Forecasts, 2021-2035

- 20.3.1. Technology Type

- 20.3.2. Package Type

- 20.3.3. Material Type

- 20.3.4. Interconnect Technology

- 20.3.5. Node Size/Process Technology

- 20.3.6. Power Rating

- 20.3.7. I/O Density

- 20.3.8. Die Count

- 20.3.9. End-Use Industry

- 20.3.10. Country

- 20.3.10.1. South Africa

- 20.3.10.2. Egypt

- 20.3.10.3. Nigeria

- 20.3.10.4. Algeria

- 20.3.10.5. Rest of Africa

- 20.4. South Africa Advanced Semiconductor Packaging Technologies Market

- 20.4.1. Country Segmental Analysis

- 20.4.2. Technology Type

- 20.4.3. Package Type

- 20.4.4. Material Type

- 20.4.5. Interconnect Technology

- 20.4.6. Node Size/Process Technology

- 20.4.7. Power Rating

- 20.4.8. I/O Density

- 20.4.9. Die Count

- 20.4.10. End-Use Industry

- 20.5. Egypt Advanced Semiconductor Packaging Technologies Market

- 20.5.1. Country Segmental Analysis

- 20.5.2. Technology Type

- 20.5.3. Package Type

- 20.5.4. Material Type

- 20.5.5. Interconnect Technology

- 20.5.6. Node Size/Process Technology

- 20.5.7. Power Rating

- 20.5.8. I/O Density

- 20.5.9. Die Count

- 20.5.10. End-Use Industry

- 20.6. Nigeria Advanced Semiconductor Packaging Technologies Market

- 20.6.1. Country Segmental Analysis

- 20.6.2. Technology Type

- 20.6.3. Package Type

- 20.6.4. Material Type

- 20.6.5. Interconnect Technology

- 20.6.6. Node Size/Process Technology

- 20.6.7. Power Rating

- 20.6.8. I/O Density

- 20.6.9. Die Count

- 20.6.10. End-Use Industry

- 20.7. Algeria Advanced Semiconductor Packaging Technologies Market

- 20.7.1. Country Segmental Analysis

- 20.7.2. Technology Type

- 20.7.3. Package Type

- 20.7.4. Material Type

- 20.7.5. Interconnect Technology

- 20.7.6. Node Size/Process Technology

- 20.7.7. Power Rating

- 20.7.8. I/O Density

- 20.7.9. Die Count

- 20.7.10. End-Use Industry

- 20.8. Rest of Africa Advanced Semiconductor Packaging Technologies Market

- 20.8.1. Country Segmental Analysis

- 20.8.2. Technology Type

- 20.8.3. Package Type

- 20.8.4. Material Type

- 20.8.5. Interconnect Technology

- 20.8.6. Node Size/Process Technology

- 20.8.7. Power Rating

- 20.8.8. I/O Density

- 20.8.9. Die Count

- 20.8.10. End-Use Industry

- 21. South America Advanced Semiconductor Packaging Technologies Market Analysis

- 21.1. Key Segment Analysis

- 21.2. Regional Snapshot

- 21.3. South America Advanced Semiconductor Packaging Technologies Market Size (Value - US$ Bn), Analysis, and Forecasts, 2021-2035

- 21.3.1. Technology Type

- 21.3.2. Package Type

- 21.3.3. Material Type

- 21.3.4. Interconnect Technology

- 21.3.5. Node Size/Process Technology

- 21.3.6. Power Rating

- 21.3.7. I/O Density

- 21.3.8. Die Count

- 21.3.9. End-Use Industry

- 21.3.10. Country

- 21.3.10.1. Brazil

- 21.3.10.2. Argentina

- 21.3.10.3. Rest of South America

- 21.4. Brazil Advanced Semiconductor Packaging Technologies Market

- 21.4.1. Country Segmental Analysis

- 21.4.2. Technology Type

- 21.4.3. Package Type

- 21.4.4. Material Type

- 21.4.5. Interconnect Technology

- 21.4.6. Node Size/Process Technology

- 21.4.7. Power Rating

- 21.4.8. I/O Density

- 21.4.9. Die Count

- 21.4.10. End-Use Industry

- 21.5. Argentina Advanced Semiconductor Packaging Technologies Market

- 21.5.1. Country Segmental Analysis

- 21.5.2. Technology Type

- 21.5.3. Package Type

- 21.5.4. Material Type

- 21.5.5. Interconnect Technology

- 21.5.6. Node Size/Process Technology

- 21.5.7. Power Rating

- 21.5.8. I/O Density

- 21.5.9. Die Count

- 21.5.10. End-Use Industry

- 21.6. Rest of South America Advanced Semiconductor Packaging Technologies Market

- 21.6.1. Country Segmental Analysis

- 21.6.2. Technology Type

- 21.6.3. Package Type

- 21.6.4. Material Type

- 21.6.5. Interconnect Technology

- 21.6.6. Node Size/Process Technology

- 21.6.7. Power Rating

- 21.6.8. I/O Density

- 21.6.9. Die Count

- 21.6.10. End-Use Industry

- 22. Key Players/ Company Profile

- 22.1. Advanced Micro Devices (AMD)

- 22.1.1. Company Details/ Overview

- 22.1.2. Company Financials

- 22.1.3. Key Customers and Competitors

- 22.1.4. Business/ Industry Portfolio

- 22.1.5. Product Portfolio/ Specification Details

- 22.1.6. Pricing Data

- 22.1.7. Strategic Overview

- 22.1.8. Recent Developments

- 22.2. Amkor Technology

- 22.3. ASE Technology Holding

- 22.4. ChipMOS Technologies

- 22.5. GlobalFoundries

- 22.6. Intel Corporation

- 22.7. JCET Group

- 22.8. Microchip Technology

- 22.9. Micron Technology

- 22.10. ON Semiconductor

- 22.11. Powertech Technology Inc. (PTI)

- 22.12. Qualcomm Technologies

- 22.13. Renesas Electronics

- 22.14. Samsung Electronics

- 22.15. Siliconware Precision Industries (SPIL)

- 22.16. SK Hynix Inc.

- 22.17. STATS ChipPAC Management Pte. Ltd.

- 22.18. Taiwan Semiconductor Manufacturing Company (TSMC)

- 22.19. Tongfu Microelectronics

- 22.20. United Microelectronics Corporation (UMC)

- 22.21. Other Key Players

- 22.1. Advanced Micro Devices (AMD)

Note* - This is just tentative list of players. While providing the report, we will cover more number of players based on their revenue and share for each geography

Research Design

Our research design integrates both demand-side and supply-side analysis through a balanced combination of primary and secondary research methodologies. By utilizing both bottom-up and top-down approaches alongside rigorous data triangulation methods, we deliver robust market intelligence that supports strategic decision-making.

MarketGenics' comprehensive research design framework ensures the delivery of accurate, reliable, and actionable market intelligence. Through the integration of multiple research approaches, rigorous validation processes, and expert analysis, we provide our clients with the insights needed to make informed strategic decisions and capitalize on market opportunities.

MarketGenics leverages a dedicated industry panel of experts and a comprehensive suite of paid databases to effectively collect, consolidate, and analyze market intelligence.

Our approach has consistently proven to be reliable and effective in generating accurate market insights, identifying key industry trends, and uncovering emerging business opportunities.

Through both primary and secondary research, we capture and analyze critical company-level data such as manufacturing footprints, including technical centers, R&D facilities, sales offices, and headquarters.

Our expert panel further enhances our ability to estimate market size for specific brands based on validated field-level intelligence.

Our data mining techniques incorporate both parametric and non-parametric methods, allowing for structured data collection, sorting, processing, and cleaning.

Demand projections are derived from large-scale data sets analyzed through proprietary algorithms, culminating in robust and reliable market sizing.

Research Approach

The bottom-up approach builds market estimates by starting with the smallest addressable market units and systematically aggregating them to create comprehensive market size projections.

This method begins with specific, granular data points and builds upward to create the complete market landscape.

Customer Analysis → Segmental Analysis → Geographical Analysis

The top-down approach starts with the broadest possible market data and systematically narrows it down through a series of filters and assumptions to arrive at specific market segments or opportunities.

This method begins with the big picture and works downward to increasingly specific market slices.

TAM → SAM → SOM

Research Methods

Desk / Secondary Research

While analysing the market, we extensively study secondary sources, directories, and databases to identify and collect information useful for this technical, market-oriented, and commercial report. Secondary sources that we utilize are not only the public sources, but it is a combination of Open Source, Associations, Paid Databases, MG Repository & Knowledgebase, and others.

- Company websites, annual reports, financial reports, broker reports, and investor presentations

- National government documents, statistical databases and reports

- News articles, press releases and web-casts specific to the companies operating in the market, Magazines, reports, and others

- We gather information from commercial data sources for deriving company specific data such as segmental revenue, share for geography, product revenue, and others

- Internal and external proprietary databases (industry-specific), relevant patent, and regulatory databases

- Governing Bodies, Government Organizations

- Relevant Authorities, Country-specific Associations for Industries

We also employ the model mapping approach to estimate the product level market data through the players' product portfolio

Primary Research

Primary research/ interviews is vital in analyzing the market. Most of the cases involves paid primary interviews. Primary sources include primary interviews through e-mail interactions, telephonic interviews, surveys as well as face-to-face interviews with the different stakeholders across the value chain including several industry experts.

| Type of Respondents | Number of Primaries |

|---|---|

| Tier 2/3 Suppliers | ~20 |

| Tier 1 Suppliers | ~25 |

| End-users | ~25 |

| Industry Expert/ Panel/ Consultant | ~30 |

| Total | ~100 |

MG Knowledgebase

• Repository of industry blog, newsletter and case studies

• Online platform covering detailed market reports, and company profiles

Forecasting Factors and Models

Forecasting Factors

- Historical Trends – Past market patterns, cycles, and major events that shaped how markets behave over time. Understanding past trends helps predict future behavior.

- Industry Factors – Specific characteristics of the industry like structure, regulations, and innovation cycles that affect market dynamics.

- Macroeconomic Factors – Economic conditions like GDP growth, inflation, and employment rates that affect how much money people have to spend.

- Demographic Factors – Population characteristics like age, income, and location that determine who can buy your product.

- Technology Factors – How quickly people adopt new technology and how much technology infrastructure exists.

- Regulatory Factors – Government rules, laws, and policies that can help or restrict market growth.

- Competitive Factors – Analyzing competition structure such as degree of competition and bargaining power of buyers and suppliers.

Forecasting Models / Techniques

Multiple Regression Analysis

- Identify and quantify factors that drive market changes

- Statistical modeling to establish relationships between market drivers and outcomes

Time Series Analysis – Seasonal Patterns

- Understand regular cyclical patterns in market demand

- Advanced statistical techniques to separate trend, seasonal, and irregular components

Time Series Analysis – Trend Analysis

- Identify underlying market growth patterns and momentum

- Statistical analysis of historical data to project future trends

Expert Opinion – Expert Interviews

- Gather deep industry insights and contextual understanding

- In-depth interviews with key industry stakeholders

Multi-Scenario Development

- Prepare for uncertainty by modeling different possible futures

- Creating optimistic, pessimistic, and most likely scenarios

Time Series Analysis – Moving Averages

- Sophisticated forecasting for complex time series data

- Auto-regressive integrated moving average models with seasonal components

Econometric Models

- Apply economic theory to market forecasting

- Sophisticated economic models that account for market interactions

Expert Opinion – Delphi Method

- Harness collective wisdom of industry experts

- Structured, multi-round expert consultation process

Monte Carlo Simulation

- Quantify uncertainty and probability distributions

- Thousands of simulations with varying input parameters

Research Analysis

Our research framework is built upon the fundamental principle of validating market intelligence from both demand and supply perspectives. This dual-sided approach ensures comprehensive market understanding and reduces the risk of single-source bias.

Demand-Side Analysis: We understand end-user/application behavior, preferences, and market needs along with the penetration of the product for specific application.

Supply-Side Analysis: We estimate overall market revenue, analyze the segmental share along with industry capacity, competitive landscape, and market structure.

Validation & Evaluation

Data triangulation is a validation technique that uses multiple methods, sources, or perspectives to examine the same research question, thereby increasing the credibility and reliability of research findings. In market research, triangulation serves as a quality assurance mechanism that helps identify and minimize bias, validate assumptions, and ensure accuracy in market estimates.

- Data Source Triangulation – Using multiple data sources to examine the same phenomenon

- Methodological Triangulation – Using multiple research methods to study the same research question

- Investigator Triangulation – Using multiple researchers or analysts to examine the same data

- Theoretical Triangulation – Using multiple theoretical perspectives to interpret the same data

Custom Market Research Services

We will customise the research for you, in case the report listed above does not meet your requirements.

Get 10% Free Customisation