Electric Vehicle Semiconductor Market Size, Share & Trends Analysis Report by Component Type (Power Semiconductors, Microcontrollers (MCUs), Analog ICs, Digital ICs / Processors, Sensors (MEMS, Image Sensors), Memory Devices, Communication & Interface ICs, Gate Driver ICs, Others), Device Type, Semiconductor Material, Voltage Range, Packaging Type, Technology Type, Integration Level, Vehicle Type, Electric Vehicle Type, Sales Channel, and Geography (North America, Europe, Asia Pacific, Middle East, Africa, and South America) – Global Industry Data, Trends, and Forecasts, 2026–2035

|

|

|

Segmental Data Insights |

|

|

Demand Trends |

|

|

Competitive Landscape |

|

|

Strategic Development |

|

|

Future Outlook & Opportunities |

|

Electric Vehicle Semiconductor Market Size, Share, and Growth

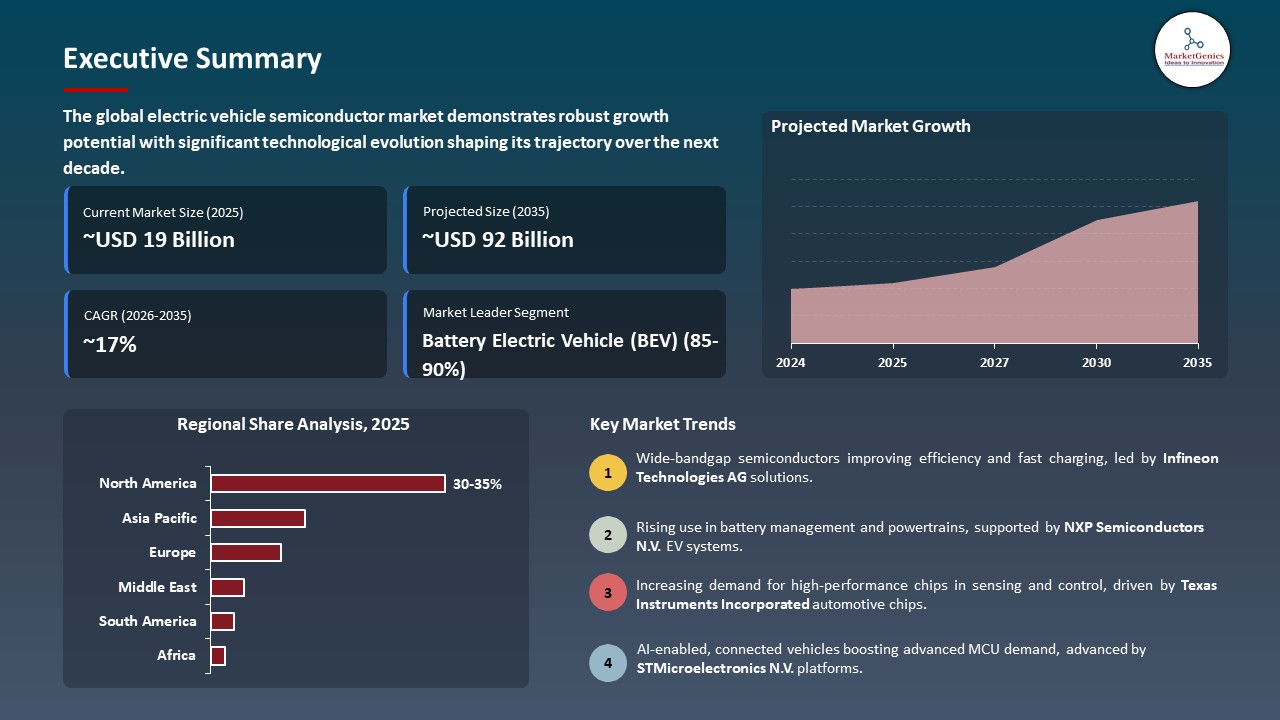

The global electric vehicle semiconductor market is witnessing strong growth, valued at USD 18.8 billion in 2025 and projected to reach USD 92 billion by 2035, expanding at a CAGR of 17.2% during the forecast period. Asia Pacific is the fastest-growing region for the electric vehicle semiconductor market due to rapid EV adoption, strong government support, large-scale automotive manufacturing, and expansion of semiconductor production capacities.

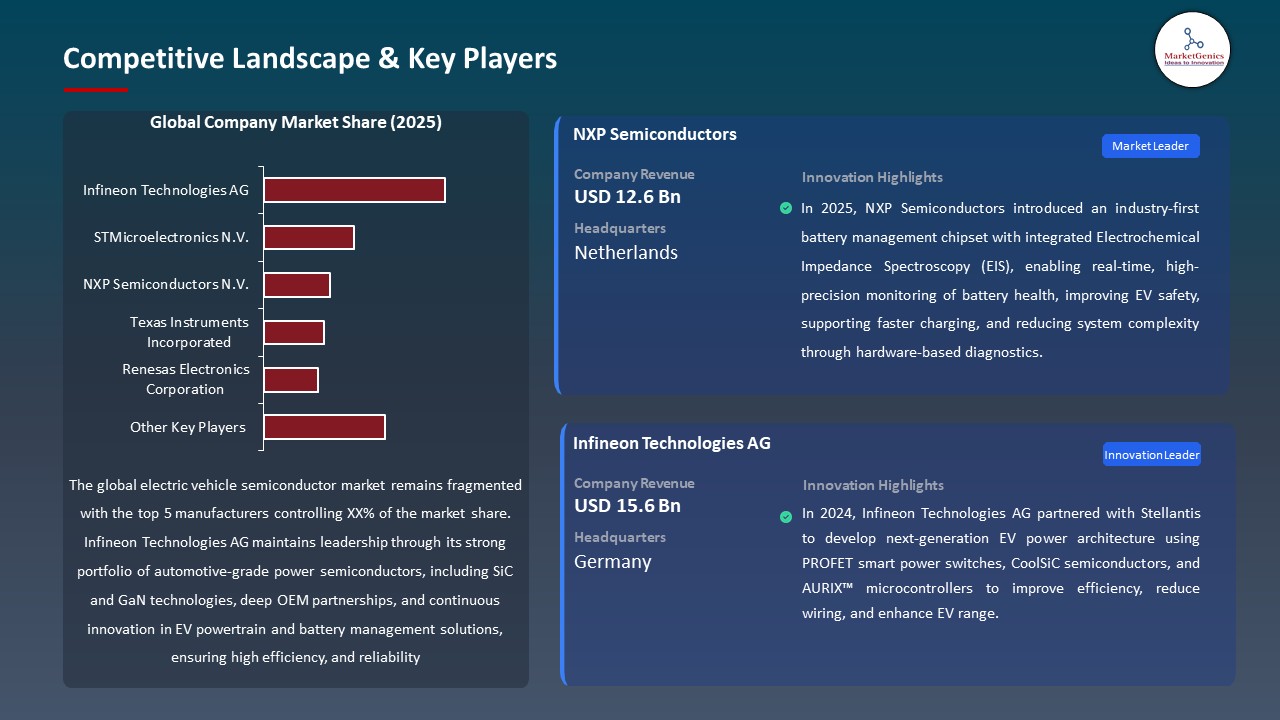

Naomi Smit, VP and GM, Drivers and Energy System, NXP Semiconductors, said, "The EIS solution brings a powerful lab-grade diagnostic tool into the vehicle. It simplifies system design by reducing the need for additional temperature sensors and supports the shift toward faster, safer and more reliable charging without compromising battery health. The chipset also offers a low-barrier upgrade path, with pin-to-pin compatible packages that can be directly upgraded to on cell module and battery junction box control units."

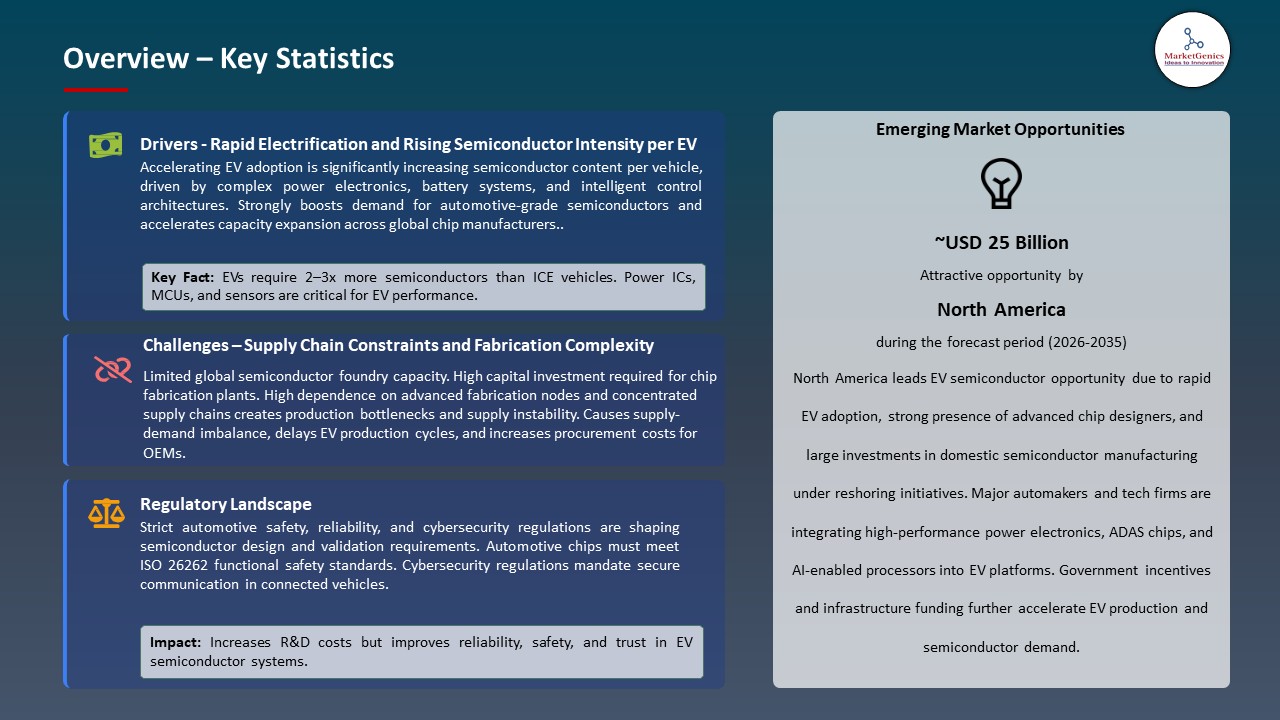

The electric vehicle semiconductor market is growing at rapid speed because of three factors which include the shift to electric transportation and the higher use of power electronics and the increasing need for energy-efficient high-performance components. Advanced driver assistance systems and battery management systems and onboard chargers need semiconductors which operate at high voltage and high efficiency because they need to boost their power conversion and thermal efficiency.

Automakers are also focusing on improving vehicle range and charging speed, which drives the adoption of next-generation semiconductor solutions. Infineon Technologies AG established its silicon carbide power module production in 2025 to manufacture EV traction inverters, while ON Semiconductor developed advanced SiC MOSFET solutions which power high-efficiency EV platforms and deliver better energy density and lower power losses. The semiconductor manufacturing capacity expansion through increased investments together with the strategic partnerships between OEMs and chipmakers, which drive supply chain innovation, enhance operational effectiveness.

Adjacent opportunities for electric vehicle semiconductors include renewable energy inverters, energy storage systems, charging infrastructure, industrial power electronics, and smart grid applications, all leveraging high-efficiency power devices such as SiC and GaN to improve energy conversion, system performance, and reliability across electrified ecosystems.

Electric Vehicle Semiconductor Market Dynamics and Trends

Driver: Rapid Transition Toward High-Voltage Electric Vehicle Architectures Enhancing Semiconductor Demand

- The automotive industry is moving towards electric vehicle systems that use 800V and higher voltage operations because these advanced semiconductors can handle increased power requirements while delivering better energy efficiency. The systems provide three main benefits which include faster charging times and reduced energy waste and smaller powertrain systems.

- Automakers are increasingly adopting wide-bandgap semiconductors such as silicon carbide to support these architectures because these materials provide better thermal management and system dependability which leads to improved vehicle range and performance.

- Infineon Technologies AG launched their trench-based silicon carbide superjunction technology for EV traction inverters in 2025 which enables higher power density and up to 25% higher current capacity and requires smaller systems for high-voltage electric vehicle designs.

- High-voltage EV architectures are creating greater need for semiconductors which drives expansion in the semiconductor market.

Restraint: Supply Chain Volatility and High Capital Intensity Limiting Scalable Production Expansion

- The electric vehicle semiconductor market encounters major difficulties because supply chains experience unpredictable changes and semiconductor manufacturing requires extensive financial resources for production. Production schedules face disruption and component costs face increase because critical raw materials which include silicon wafers and rare-earth elements and specialty chemicals experience availability fluctuations.

- The establishment of advanced semiconductor fabrication facilities requires companies to make large financial investments for cleanroom facilities and testing equipment and expert staff members. The financial requirements together with operational challenges create obstacles that prevent companies from meeting their electric vehicle production needs through rapid production expansion.

- Supply chain disruptions together with extended delivery times for unique parts create obstacles that hinder market expansion while they postpone product introductions and limit manufacturers' ability to adapt to changing customer requirements.

- The EV semiconductor market faces two main obstacles which include high capital needs and supply chain hazards which stop companies from growing their business and expanding their operations.

Opportunity: Expansion of Wide-Bandgap Semiconductor Applications Across Energy and Mobility Ecosystems

- The increasing utilization of wide-bandgap semiconductors which include silicon carbide and gallium nitride creates substantial business opportunities for electric vehicles and renewable energy systems and industrial power applications. The materials deliver better performance because they maintain higher operational efficiency while experiencing less thermal waste and they occupy less physical space than conventional silicon components.

- Wide-Bandgap semiconductors provide benefits which include quicker charging times and lighter weight power systems and improved energy conversion efficiency as automakers and energy companies work to increase performance and reliability and energy capacity.

- In 2025 onsemi and Schaeffler expanded their partnership to create an EliteSiC-based traction inverter which enables PHEVs to drive longer distances while delivering higher reliability and compact inverter design for advanced hybrid systems.

- Wide-Bandgap semiconductors drive market expansion through their application in electric vehicles and their use in energy management solutions.

Key Trend: Increasing Adoption of AI‑Enabled Semiconductor Solutions for Enhanced Vehicle Intelligence

- The adoption of artificial intelligence (AI) within semiconductor solutions produces advanced electric vehicle systems which deliver intelligent power distribution and advanced fault detection and superior operational performance.

- The AI-enabled chips in vehicles enable drivers to control battery power consumption while improving thermal regulation and making autonomous and connected system operation possible through real-time complex data processing.

- The 2025 partnership between Qualcomm and HARMAN established an integration between Qualcomm's Snapdragon Cockpit Elite platform and HARMAN's Ready product portfolio which delivers AI-powered experiences for in-vehicle spaces and advanced driver assistance systems.

- The development of AI-powered semiconductor technology creates advanced electric vehicle systems which deliver greater efficiency and safety and enhanced vehicle intelligence.

Electric Vehicle Semiconductor Market Analysis and Segmental Data

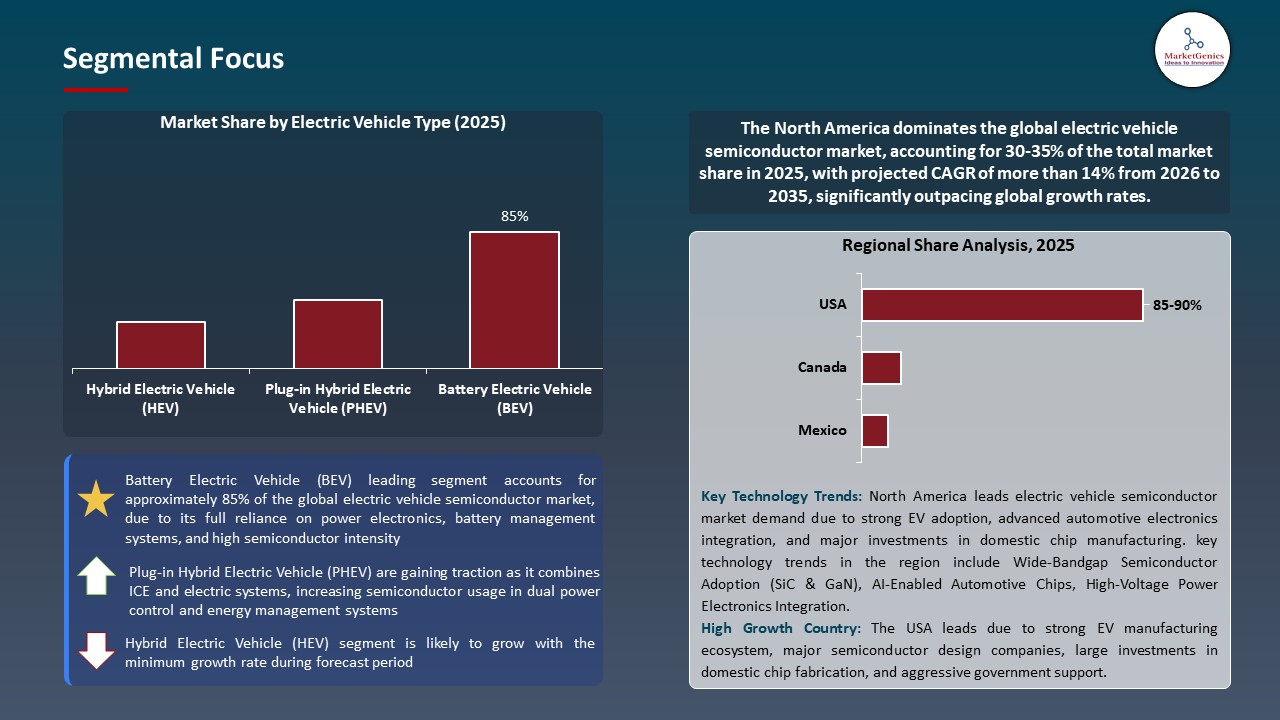

Battery Electric Vehicle (BEV) Dominate Global Electric Vehicle Semiconductor Market

- The battery electric vehicle (BEV) segment dominates the global Electric Vehicle (EV) semiconductor market because fully electric vehicles are increasingly adopted for passenger and commercial and industrial use.

- BEVs need advanced power semiconductors which provide high performance to control their energy storage systems and electric motors and charging stations. The increasing demand for longer driving ranges, faster charging, and enhanced safety features drives semiconductor integration in BEV systems, which includes inverters and on-board chargers and battery management units.

- BEV manufacturers use advanced semiconductors which include silicon carbide (SiC) and gallium nitride (GaN) devices to achieve better energy efficiency and thermal management and higher system reliability. As governments and OEMs push for electrification and stricter emission regulations, BEVs continue to outpace hybrid and plug-in hybrid vehicles in semiconductor utilization, cementing their position as the leading segment in the EV semiconductor market.

- BEV dominance accelerates semiconductor innovation and drives sustained global market growth.

North America Leads Global Electric Vehicle Semiconductor Market Demand

- North America leads the global electric vehicle semiconductor market due to a strong push for EV adoption, robust government incentives, and advanced automotive manufacturing infrastructure. The region has increased its ability to implement high-performance electric vehicle systems through its extensive investments in charging infrastructure and smart grid development and domestic semiconductor manufacturing capabilities.

- The United States and Canada host major original equipment manufacturers together with semiconductor companies which creates a need for power semiconductors and battery management units and advanced sensors.

- The combination of environmental regulations and increasing consumer demand for sustainable transportation solutions drives higher semiconductor usage in electric vehicles. North America maintains its position as the top global market for electric vehicle semiconductors because the region prioritizes electric vehicle development and renewable energy adoption and technological advancements.

- North America’s leadership in electric vehicle semiconductors drives global industry progress because it accelerates research and establishes performance standards for worldwide semiconductor adoption.

Electric Vehicle Semiconductor Market Ecosystem

The global electric vehicle semiconductor market is consolidated, with leading players including Infineon Technologies AG, STMicroelectronics N.V., NXP Semiconductors N.V., Texas Instruments Incorporated, and Renesas Electronics Corporation. The companies maintain their market position through their complete control of semiconductor development their creation of advanced power electronics and their development of energy-efficient microcontrollers which executives designed for electric vehicle use.

The company maintains its competitive advantage through continuous investment in automotive-grade silicon and power management integrated circuits and artificial intelligence-powered processors which provide them with advantages against their competitors. The company establishes partnerships with original equipment manufacturers and charging network operators and mobility technology companies to speed up the market introduction of their innovative electric vehicle semiconductor products.

The EV Semiconductor value chain includes raw material procurement for silicon wafers and specialty components, semiconductor fabrication, chip assembly, system integration into EV platforms, software deployment for powertrain and battery management, and after-sales services such as firmware updates, diagnostics, and performance optimization. Every phase of the process guarantees systems operate with high energy efficiency while they handle data streams in real time and maintain operational dependability for both passenger electric vehicles and commercial electric vehicles and hybrid systems.

The industry creates high entry obstacles because companies must invest in expensive production processes which require automotive-grade certification and complex research and development operations. The industry achieves market expansion through its continuous development of high-voltage integrated circuits and battery management solutions and smart power management modules.

Recent Development and Strategic Overview:

- In October 2025, NXP Semiconductors introduced an industry-first battery management chipset with integrated Electrochemical Impedance Spectroscopy (EIS), enabling real-time, high-precision monitoring of battery health, improving EV safety, supporting faster charging, and reducing system complexity through hardware-based diagnostics.

- In April 2025, Texas Instruments (TI) expanded its automotive semiconductor portfolio with advanced lidar, clock, and radar chips to enhance vehicle autonomy and safety. The new LMH13000 lidar driver enables 30% longer detection range with improved real-time response, while BAW-based clocks and the AWR2944P radar sensor strengthen ADAS reliability and sensing accuracy.

Report Scope

|

Detail |

|

|

Market Size in 2025 |

USD 18.8 Bn |

|

Market Forecast Value in 2035 |

USD 92 Bn |

|

Growth Rate (CAGR) |

17.2% |

|

Forecast Period |

2026 – 2035 |

|

Historical Data Available for |

2021 – 2024 |

|

Market Size Units |

US$ Billion for Value Million Units for Volume |

|

Report Format |

Electronic (PDF) + Excel |

|

North America |

Europe |

Asia Pacific |

Middle East |

Africa |

South America |

|

|

|

|

|

|

|

Companies Covered |

|||||

|

|

|

|

|

|

Electric Vehicle Semiconductor Market Segmentation and Highlights

|

Segment |

Sub-segment |

|

Electric Vehicle Semiconductor Market, By Component Type |

|

|

Electric Vehicle Semiconductor Market, By Device Type |

|

|

Electric Vehicle Semiconductor Market, By Semiconductor Material |

|

|

Electric Vehicle Semiconductor Market, By Voltage Range |

|

|

Electric Vehicle Semiconductor Market, By Packaging Type |

|

|

Electric Vehicle Semiconductor Market, By Technology Type |

|

|

Electric Vehicle Semiconductor Market, By Integration Level |

|

|

Electric Vehicle Semiconductor Market, By Vehicle Type |

|

|

Electric Vehicle Semiconductor Market, By Electric Vehicle Type |

|

|

Electric Vehicle Semiconductor Market, By Sales Channel |

|

Frequently Asked Questions

Table of Contents

- 1. Research Methodology and Assumptions

- 1.1. Definitions

- 1.2. Research Design and Approach

- 1.3. Data Collection Methods

- 1.4. Base Estimates and Calculations

- 1.5. Forecasting Models

- 1.5.1. Key Forecast Factors & Impact Analysis

- 1.6. Secondary Research

- 1.6.1. Open Sources

- 1.6.2. Paid Databases

- 1.6.3. Associations

- 1.7. Primary Research

- 1.7.1. Primary Sources

- 1.7.2. Primary Interviews with Stakeholders across Ecosystem

- 2. Executive Summary

- 2.1. Global Electric Vehicle Semiconductor Market Outlook

- 2.1.1. Electric Vehicle Semiconductor Market Size Volume (Million Units) and Value (US$ Bn), and Forecasts, 2021-2035

- 2.1.2. Compounded Annual Growth Rate Analysis

- 2.1.3. Growth Opportunity Analysis

- 2.1.4. Segmental Share Analysis

- 2.1.5. Geographical Share Analysis

- 2.2. Market Analysis and Facts

- 2.3. Supply-Demand Analysis

- 2.4. Competitive Benchmarking

- 2.5. Go-to- Market Strategy

- 2.5.1. Customer/ End-use Industry Assessment

- 2.5.2. Growth Opportunity Data, 2026-2035

- 2.5.2.1. Regional Data

- 2.5.2.2. Country Data

- 2.5.2.3. Segmental Data

- 2.5.3. Identification of Potential Market Spaces

- 2.5.4. GAP Analysis

- 2.5.5. Potential Attractive Price Points

- 2.5.6. Prevailing Market Risks & Challenges

- 2.5.7. Preferred Sales & Marketing Strategies

- 2.5.8. Key Recommendations and Analysis

- 2.5.9. A Way Forward

- 2.1. Global Electric Vehicle Semiconductor Market Outlook

- 3. Industry Data and Premium Insights

- 3.1. Global Automotive & Transportation Industry Overview, 2025

- 3.1.1. Automotive & Transportation Ecosystem Analysis

- 3.1.2. Key Trends for Automotive & Transportation Industry

- 3.1.3. Regional Distribution for Automotive & Transportation Industry

- 3.2. Supplier Customer Data

- 3.3. Technology Roadmap and Developments

- 3.4. Trade Analysis

- 3.4.1. Import & Export Analysis, 2025

- 3.4.2. Top Importing Countries

- 3.4.3. Top Exporting Countries

- 3.5. Trump Tariff Impact Analysis

- 3.5.1. Manufacturer

- 3.5.1.1. Based on the component & Raw material

- 3.5.2. Supply Chain

- 3.5.3. End Consumer

- 3.5.1. Manufacturer

- 3.6. Raw Material Analysis

- 3.1. Global Automotive & Transportation Industry Overview, 2025

- 4. Market Overview

- 4.1. Market Dynamics

- 4.1.1. Drivers

- 4.1.1.1. Rapid adoption of electric vehicles (EVs) globally.

- 4.1.1.2. Growing demand for advanced driver-assistance systems (ADAS) and infotainment.

- 4.1.1.3. Government incentives and supportive policies for EVs and green technologies.

- 4.1.2. Restraints

- 4.1.2.1. High semiconductor costs impacting EV production affordability.

- 4.1.2.2. Supply chain disruptions and global chip shortages.

- 4.1.1. Drivers

- 4.2. Key Trend Analysis

- 4.3. Regulatory Framework

- 4.3.1. Key Regulations, Norms, and Subsidies, by Key Countries

- 4.3.2. Tariffs and Standards

- 4.3.3. Impact Analysis of Regulations on the Market

- 4.4. Value Chain Analysis

- 4.4.1. Raw Material Suppliers

- 4.4.2. EV Semiconductor Component Manufacturers

- 4.4.3. System Integrators/ Technology Providers

- 4.4.4. Vehicle Manufacturers/ OEM

- 4.4.5. Distributors & Dealers

- 4.4.6. End Users/ Customers

- 4.5. Cost Structure Analysis

- 4.5.1. Parameter’s Share for Cost Associated

- 4.5.2. COGP vs COGS

- 4.5.3. Profit Margin Analysis

- 4.6. Pricing Analysis

- 4.6.1. Regional Pricing Analysis

- 4.6.2. Segmental Pricing Trends

- 4.6.3. Factors Influencing Pricing

- 4.7. Porter’s Five Forces Analysis

- 4.8. PESTEL Analysis

- 4.9. Global Electric Vehicle Semiconductor Market Demand

- 4.9.1. Historical Market Size – Volume (Million Units) and Value (US$ Bn), 2020-2024

- 4.9.2. Current and Future Market Size – Volume (Million Units) and Value (US$ Bn), 2026–2035

- 4.9.2.1. Y-o-Y Growth Trends

- 4.9.2.2. Absolute $ Opportunity Assessment

- 4.1. Market Dynamics

- 5. Competition Landscape

- 5.1. Competition structure

- 5.1.1. Fragmented v/s consolidated

- 5.2. Company Share Analysis, 2025

- 5.2.1. Global Company Market Share

- 5.2.2. By Region

- 5.2.2.1. North America

- 5.2.2.2. Europe

- 5.2.2.3. Asia Pacific

- 5.2.2.4. Middle East

- 5.2.2.5. Africa

- 5.2.2.6. South America

- 5.3. Product Comparison Matrix

- 5.3.1. Specifications

- 5.3.2. Market Positioning

- 5.3.3. Pricing

- 5.1. Competition structure

- 6. Global Electric Vehicle Semiconductor Market Analysis, by Component Type

- 6.1. Key Segment Analysis

- 6.2. Electric Vehicle Semiconductor Market Size Volume (Million Units) and Value (US$ Bn), Analysis, and Forecasts, by Component Type, 2021-2035

- 6.2.1. Power Semiconductors

- 6.2.2. Microcontrollers (MCUs)

- 6.2.3. Analog ICs

- 6.2.4. Digital ICs / Processors

- 6.2.5. Sensors (MEMS, Image Sensors)

- 6.2.6. Memory Devices

- 6.2.7. Communication & Interface ICs

- 6.2.8. Gate Driver ICs

- 6.2.9. Others

- 7. Global Electric Vehicle Semiconductor Market Analysis, by Device Type

- 7.1. Key Segment Analysis

- 7.2. Electric Vehicle Semiconductor Market Size Volume (Million Units) and Value (US$ Bn), Analysis, and Forecasts, by Device Type, 2021-2035

- 7.2.1. Power Semiconductor Devices

- 7.2.2. Analog Semiconductor Devices

- 7.2.3. Digital Semiconductor Devices

- 7.2.4. MEMS Sensors

- 7.2.5. Microcontrollers

- 7.2.6. Others

- 8. Global Electric Vehicle Semiconductor Market Analysis, by Semiconductor Material

- 8.1. Key Segment Analysis

- 8.2. Electric Vehicle Semiconductor Market Size Volume (Million Units) and Value (US$ Bn), Analysis, and Forecasts, by Semiconductor Material, 2021-2035

- 8.2.1. Silicon (Si)

- 8.2.2. Silicon Carbide (SiC)

- 8.2.3. Gallium Nitride (GaN)

- 8.2.4. Others

- 9. Global Electric Vehicle Semiconductor Market Analysis, by Voltage Range

- 9.1. Key Segment Analysis

- 9.2. Electric Vehicle Semiconductor Market Size Volume (Million Units) and Value (US$ Bn), Analysis, and Forecasts, by Voltage Range, 2021-2035

- 9.2.1. Low Voltage (<400V)

- 9.2.2. Medium Voltage (400V–800V)

- 9.2.3. High Voltage (>800V)

- 10. Global Electric Vehicle Semiconductor Market Analysis, by Packaging Type

- 10.1. Key Segment Analysis

- 10.2. Electric Vehicle Semiconductor Market Size Volume (Million Units) and Value (US$ Bn), Analysis, and Forecasts, by Packaging Type, 2021-2035

- 10.2.1. Surface Mount Technology (SMT)

- 10.2.2. Through-Hole Technology

- 10.2.3. Chip-on-Board (COB)

- 10.2.4. Ball Grid Array (BGA)

- 10.2.5. Dual In-line Package (DIP)

- 10.2.6. Others

- 11. Global Electric Vehicle Semiconductor Market Analysis, by Technology Type

- 11.1. Key Segment Analysis

- 11.2. Electric Vehicle Semiconductor Market Size Volume (Million Units) and Value (US$ Bn), Analysis, and Forecasts, by Technology Type, 2021-2035

- 11.2.1. Discrete Semiconductors

- 11.2.2. Integrated Circuits (ICs)

- 11.2.3. Mixed-Signal Technology

- 11.2.4. Power Modules

- 11.2.5. Intelligent Power Modules (IPMs)

- 11.2.6. Others

- 12. Global Electric Vehicle Semiconductor Market Analysis, by Integration Level

- 12.1. Key Segment Analysis

- 12.2. Electric Vehicle Semiconductor Market Size Volume (Million Units) and Value (US$ Bn), Analysis, and Forecasts, by Integration Level, 2021-2035

- 12.2.1. Discrete Components

- 12.2.2. Integrated Power Units

- 12.2.3. System-on-Chip (SoC) Solutions

- 13. Global Electric Vehicle Semiconductor Market Analysis, by Vehicle Type

- 13.1. Key Segment Analysis

- 13.2. Electric Vehicle Semiconductor Market Size Volume (Million Units) and Value (US$ Bn), Analysis, and Forecasts, by Vehicle Type, 2021-2035

- 13.2.1. Two Wheelers/ Three Wheelers

- 13.2.2. Passenger Vehicles

- 13.2.2.1. Hatchback

- 13.2.2.2. Sedan

- 13.2.2.3. SUVs

- 13.2.3. Light Commercial Vehicles

- 13.2.4. Heavy Duty Trucks

- 13.2.5. Buses & Coaches

- 13.2.6. Off-road Vehicles

- 14. Global Electric Vehicle Semiconductor Market Analysis, by Electric Vehicle Type

- 14.1. Key Segment Analysis

- 14.2. Electric Vehicle Semiconductor Market Size Volume (Million Units) and Value (US$ Bn), Analysis, and Forecasts, by Electric Vehicle Type, 2021-2035

- 14.2.1. Hybrid Electric Vehicle (HEV)

- 14.2.2. Plug-in Hybrid Electric Vehicle (PHEV)

- 14.2.3. Battery Electric Vehicle (BEV)

- 15. Global Electric Vehicle Semiconductor Market Analysis, by Sales Channel

- 15.1. Key Segment Analysis

- 15.2. Electric Vehicle Semiconductor Market Size Volume (Million Units) and Value (US$ Bn), Analysis, and Forecasts, by Sales Channel, 2021-2035

- 15.2.1. Direct Sales

- 15.2.2. Authorized Distributors

- 15.2.3. Semiconductor Foundries

- 15.2.4. Online Channels

- 16. Global Electric Vehicle Semiconductor Market Analysis and Forecasts, by Region

- 16.1. Key Findings

- 16.2. Electric Vehicle Semiconductor Market Size Volume (Million Units) and Value (US$ Bn), Analysis, and Forecasts, by Region, 2021-2035

- 16.2.1. North America

- 16.2.2. Europe

- 16.2.3. Asia Pacific

- 16.2.4. Middle East

- 16.2.5. Africa

- 16.2.6. South America

- 17. North America Electric Vehicle Semiconductor Market Analysis

- 17.1. Key Segment Analysis

- 17.2. Regional Snapshot

- 17.3. North America Electric Vehicle Semiconductor Market Size- Volume (Million Units) and Value (US$ Bn), Analysis, and Forecasts, 2021-2035

- 17.3.1. Component Type

- 17.3.2. Device Type

- 17.3.3. Semiconductor Material

- 17.3.4. Voltage Range

- 17.3.5. Packaging Type

- 17.3.6. Technology Type

- 17.3.7. Integration Level

- 17.3.8. Vehicle Type

- 17.3.9. Electric Vehicle Type

- 17.3.10. Sales Channel

- 17.3.11. Country

- 17.3.11.1. USA

- 17.3.11.2. Canada

- 17.3.11.3. Mexico

- 17.4. USA Electric Vehicle Semiconductor Market

- 17.4.1. Country Segmental Analysis

- 17.4.2. Device Type

- 17.4.3. Semiconductor Material

- 17.4.4. Voltage Range

- 17.4.5. Packaging Type

- 17.4.6. Technology Type

- 17.4.7. Integration Level

- 17.4.8. Vehicle Type

- 17.4.9. Electric Vehicle Type

- 17.4.10. Sales Channel

- 17.5. Canada Electric Vehicle Semiconductor Market

- 17.5.1. Country Segmental Analysis

- 17.5.2. Device Type

- 17.5.3. Semiconductor Material

- 17.5.4. Voltage Range

- 17.5.5. Packaging Type

- 17.5.6. Technology Type

- 17.5.7. Integration Level

- 17.5.8. Vehicle Type

- 17.5.9. Electric Vehicle Type

- 17.5.10. Sales Channel

- 17.6. Mexico Electric Vehicle Semiconductor Market

- 17.6.1. Country Segmental Analysis

- 17.6.2. Device Type

- 17.6.3. Semiconductor Material

- 17.6.4. Voltage Range

- 17.6.5. Packaging Type

- 17.6.6. Technology Type

- 17.6.7. Integration Level

- 17.6.8. Vehicle Type

- 17.6.9. Electric Vehicle Type

- 17.6.10. Sales Channel

- 18. Europe Electric Vehicle Semiconductor Market Analysis

- 18.1. Key Segment Analysis

- 18.2. Regional Snapshot

- 18.3. Europe Electric Vehicle Semiconductor Market Size Volume (Million Units) and Value (US$ Bn), Analysis, and Forecasts, 2021-2035

- 18.3.1. Device Type

- 18.3.2. Semiconductor Material

- 18.3.3. Voltage Range

- 18.3.4. Packaging Type

- 18.3.5. Technology Type

- 18.3.6. Integration Level

- 18.3.7. Vehicle Type

- 18.3.8. Electric Vehicle Type

- 18.3.9. Sales Channel

- 18.3.10. Country

- 18.3.10.1. Germany

- 18.3.10.2. United Kingdom

- 18.3.10.3. France

- 18.3.10.4. Italy

- 18.3.10.5. Spain

- 18.3.10.6. Netherlands

- 18.3.10.7. Nordic Countries

- 18.3.10.8. Poland

- 18.3.10.9. Russia & CIS

- 18.3.10.10. Rest of Europe

- 18.4. Germany Electric Vehicle Semiconductor Market

- 18.4.1. Country Segmental Analysis

- 18.4.2. Device Type

- 18.4.3. Semiconductor Material

- 18.4.4. Voltage Range

- 18.4.5. Packaging Type

- 18.4.6. Technology Type

- 18.4.7. Integration Level

- 18.4.8. Vehicle Type

- 18.4.9. Electric Vehicle Type

- 18.4.10. Sales Channel

- 18.5. United Kingdom Electric Vehicle Semiconductor Market

- 18.5.1. Country Segmental Analysis

- 18.5.2. Device Type

- 18.5.3. Semiconductor Material

- 18.5.4. Voltage Range

- 18.5.5. Packaging Type

- 18.5.6. Technology Type

- 18.5.7. Integration Level

- 18.5.8. Vehicle Type

- 18.5.9. Electric Vehicle Type

- 18.5.10. Sales Channel

- 18.6. France Electric Vehicle Semiconductor Market

- 18.6.1. Country Segmental Analysis

- 18.6.2. Device Type

- 18.6.3. Semiconductor Material

- 18.6.4. Voltage Range

- 18.6.5. Packaging Type

- 18.6.6. Technology Type

- 18.6.7. Integration Level

- 18.6.8. Vehicle Type

- 18.6.9. Electric Vehicle Type

- 18.6.10. Sales Channel

- 18.7. Italy Electric Vehicle Semiconductor Market

- 18.7.1. Country Segmental Analysis

- 18.7.2. Device Type

- 18.7.3. Semiconductor Material

- 18.7.4. Voltage Range

- 18.7.5. Packaging Type

- 18.7.6. Technology Type

- 18.7.7. Integration Level

- 18.7.8. Vehicle Type

- 18.7.9. Electric Vehicle Type

- 18.7.10. Sales Channel

- 18.8. Spain Electric Vehicle Semiconductor Market

- 18.8.1. Country Segmental Analysis

- 18.8.2. Device Type

- 18.8.3. Semiconductor Material

- 18.8.4. Voltage Range

- 18.8.5. Packaging Type

- 18.8.6. Technology Type

- 18.8.7. Integration Level

- 18.8.8. Vehicle Type

- 18.8.9. Electric Vehicle Type

- 18.8.10. Sales Channel

- 18.9. Netherlands Electric Vehicle Semiconductor Market

- 18.9.1. Country Segmental Analysis

- 18.9.2. Device Type

- 18.9.3. Semiconductor Material

- 18.9.4. Voltage Range

- 18.9.5. Packaging Type

- 18.9.6. Technology Type

- 18.9.7. Integration Level

- 18.9.8. Vehicle Type

- 18.9.9. Electric Vehicle Type

- 18.9.10. Sales Channel

- 18.10. Nordic Countries Electric Vehicle Semiconductor Market

- 18.10.1. Country Segmental Analysis

- 18.10.2. Device Type

- 18.10.3. Semiconductor Material

- 18.10.4. Voltage Range

- 18.10.5. Packaging Type

- 18.10.6. Technology Type

- 18.10.7. Integration Level

- 18.10.8. Vehicle Type

- 18.10.9. Electric Vehicle Type

- 18.10.10. Sales Channel

- 18.11. Poland Electric Vehicle Semiconductor Market

- 18.11.1. Country Segmental Analysis

- 18.11.2. Device Type

- 18.11.3. Semiconductor Material

- 18.11.4. Voltage Range

- 18.11.5. Packaging Type

- 18.11.6. Technology Type

- 18.11.7. Integration Level

- 18.11.8. Vehicle Type

- 18.11.9. Electric Vehicle Type

- 18.11.10. Sales Channel

- 18.12. Russia & CIS Electric Vehicle Semiconductor Market

- 18.12.1. Country Segmental Analysis

- 18.12.2. Device Type

- 18.12.3. Semiconductor Material

- 18.12.4. Voltage Range

- 18.12.5. Packaging Type

- 18.12.6. Technology Type

- 18.12.7. Integration Level

- 18.12.8. Vehicle Type

- 18.12.9. Electric Vehicle Type

- 18.12.10. Sales Channel

- 18.13. Rest of Europe Electric Vehicle Semiconductor Market

- 18.13.1. Country Segmental Analysis

- 18.13.2. Device Type

- 18.13.3. Semiconductor Material

- 18.13.4. Voltage Range

- 18.13.5. Packaging Type

- 18.13.6. Technology Type

- 18.13.7. Integration Level

- 18.13.8. Vehicle Type

- 18.13.9. Electric Vehicle Type

- 18.13.10. Sales Channel

- 19. Asia Pacific Electric Vehicle Semiconductor Market Analysis

- 19.1. Key Segment Analysis

- 19.2. Regional Snapshot

- 19.3. Asia Pacific Electric Vehicle Semiconductor Market Size Volume (Million Units) and Value (US$ Bn), Analysis, and Forecasts, 2021-2035

- 19.3.1. Device Type

- 19.3.2. Semiconductor Material

- 19.3.3. Voltage Range

- 19.3.4. Packaging Type

- 19.3.5. Technology Type

- 19.3.6. Integration Level

- 19.3.7. Vehicle Type

- 19.3.8. Electric Vehicle Type

- 19.3.9. Sales Channel

- 19.3.10. Country

- 19.3.10.1. China

- 19.3.10.2. India

- 19.3.10.3. Japan

- 19.3.10.4. South Korea

- 19.3.10.5. Australia and New Zealand

- 19.3.10.6. Indonesia

- 19.3.10.7. Malaysia

- 19.3.10.8. Thailand

- 19.3.10.9. Vietnam

- 19.3.10.10. Rest of Asia Pacific

- 19.4. China Electric Vehicle Semiconductor Market

- 19.4.1. Country Segmental Analysis

- 19.4.2. Device Type

- 19.4.3. Semiconductor Material

- 19.4.4. Voltage Range

- 19.4.5. Packaging Type

- 19.4.6. Technology Type

- 19.4.7. Integration Level

- 19.4.8. Vehicle Type

- 19.4.9. Electric Vehicle Type

- 19.4.10. Sales Channel

- 19.5. India Electric Vehicle Semiconductor Market

- 19.5.1. Country Segmental Analysis

- 19.5.2. Device Type

- 19.5.3. Semiconductor Material

- 19.5.4. Voltage Range

- 19.5.5. Packaging Type

- 19.5.6. Technology Type

- 19.5.7. Integration Level

- 19.5.8. Vehicle Type

- 19.5.9. Electric Vehicle Type

- 19.5.10. Sales Channel

- 19.6. Japan Electric Vehicle Semiconductor Market

- 19.6.1. Country Segmental Analysis

- 19.6.2. Device Type

- 19.6.3. Semiconductor Material

- 19.6.4. Voltage Range

- 19.6.5. Packaging Type

- 19.6.6. Technology Type

- 19.6.7. Integration Level

- 19.6.8. Vehicle Type

- 19.6.9. Electric Vehicle Type

- 19.6.10. Sales Channel

- 19.7. South Korea Electric Vehicle Semiconductor Market

- 19.7.1. Country Segmental Analysis

- 19.7.2. Device Type

- 19.7.3. Semiconductor Material

- 19.7.4. Voltage Range

- 19.7.5. Packaging Type

- 19.7.6. Technology Type

- 19.7.7. Integration Level

- 19.7.8. Vehicle Type

- 19.7.9. Electric Vehicle Type

- 19.7.10. Sales Channel

- 19.8. Australia and New Zealand Electric Vehicle Semiconductor Market

- 19.8.1. Country Segmental Analysis

- 19.8.2. Device Type

- 19.8.3. Semiconductor Material

- 19.8.4. Voltage Range

- 19.8.5. Packaging Type

- 19.8.6. Technology Type

- 19.8.7. Integration Level

- 19.8.8. Vehicle Type

- 19.8.9. Electric Vehicle Type

- 19.8.10. Sales Channel

- 19.9. Indonesia Electric Vehicle Semiconductor Market

- 19.9.1. Country Segmental Analysis

- 19.9.2. Device Type

- 19.9.3. Semiconductor Material

- 19.9.4. Voltage Range

- 19.9.5. Packaging Type

- 19.9.6. Technology Type

- 19.9.7. Integration Level

- 19.9.8. Vehicle Type

- 19.9.9. Electric Vehicle Type

- 19.9.10. Sales Channel

- 19.10. Malaysia Electric Vehicle Semiconductor Market

- 19.10.1. Country Segmental Analysis

- 19.10.2. Device Type

- 19.10.3. Semiconductor Material

- 19.10.4. Voltage Range

- 19.10.5. Packaging Type

- 19.10.6. Technology Type

- 19.10.7. Integration Level

- 19.10.8. Vehicle Type

- 19.10.9. Electric Vehicle Type

- 19.10.10. Sales Channel

- 19.11. Thailand Electric Vehicle Semiconductor Market

- 19.11.1. Country Segmental Analysis

- 19.11.2. Device Type

- 19.11.3. Semiconductor Material

- 19.11.4. Voltage Range

- 19.11.5. Packaging Type

- 19.11.6. Technology Type

- 19.11.7. Integration Level

- 19.11.8. Vehicle Type

- 19.11.9. Electric Vehicle Type

- 19.11.10. Sales Channel

- 19.12. Vietnam Electric Vehicle Semiconductor Market

- 19.12.1. Country Segmental Analysis

- 19.12.2. Device Type

- 19.12.3. Semiconductor Material

- 19.12.4. Voltage Range

- 19.12.5. Packaging Type

- 19.12.6. Technology Type

- 19.12.7. Integration Level

- 19.12.8. Vehicle Type

- 19.12.9. Electric Vehicle Type

- 19.12.10. Sales Channel

- 19.13. Rest of Asia Pacific Electric Vehicle Semiconductor Market

- 19.13.1. Country Segmental Analysis

- 19.13.2. Device Type

- 19.13.3. Semiconductor Material

- 19.13.4. Voltage Range

- 19.13.5. Packaging Type

- 19.13.6. Technology Type

- 19.13.7. Integration Level

- 19.13.8. Vehicle Type

- 19.13.9. Electric Vehicle Type

- 19.13.10. Sales Channel

- 20. Middle East Electric Vehicle Semiconductor Market Analysis

- 20.1. Key Segment Analysis

- 20.2. Regional Snapshot

- 20.3. Middle East Electric Vehicle Semiconductor Market Size Volume (Million Units) and Value (US$ Bn), Analysis, and Forecasts, 2021-2035

- 20.3.1. Device Type

- 20.3.2. Semiconductor Material

- 20.3.3. Voltage Range

- 20.3.4. Packaging Type

- 20.3.5. Technology Type

- 20.3.6. Integration Level

- 20.3.7. Vehicle Type

- 20.3.8. Electric Vehicle Type

- 20.3.9. Sales Channel

- 20.3.10. Country

- 20.3.10.1. Turkey

- 20.3.10.2. UAE

- 20.3.10.3. Saudi Arabia

- 20.3.10.4. Israel

- 20.3.10.5. Rest of Middle East

- 20.4. Turkey Electric Vehicle Semiconductor Market

- 20.4.1. Country Segmental Analysis

- 20.4.2. Device Type

- 20.4.3. Semiconductor Material

- 20.4.4. Voltage Range

- 20.4.5. Packaging Type

- 20.4.6. Technology Type

- 20.4.7. Integration Level

- 20.4.8. Vehicle Type

- 20.4.9. Electric Vehicle Type

- 20.4.10. Sales Channel

- 20.5. UAE Electric Vehicle Semiconductor Market

- 20.5.1. Country Segmental Analysis

- 20.5.2. Device Type

- 20.5.3. Semiconductor Material

- 20.5.4. Voltage Range

- 20.5.5. Packaging Type

- 20.5.6. Technology Type

- 20.5.7. Integration Level

- 20.5.8. Vehicle Type

- 20.5.9. Electric Vehicle Type

- 20.5.10. Sales Channel

- 20.6. Saudi Arabia Electric Vehicle Semiconductor Market

- 20.6.1. Country Segmental Analysis

- 20.6.2. Device Type

- 20.6.3. Semiconductor Material

- 20.6.4. Voltage Range

- 20.6.5. Packaging Type

- 20.6.6. Technology Type

- 20.6.7. Integration Level

- 20.6.8. Vehicle Type

- 20.6.9. Electric Vehicle Type

- 20.6.10. Sales Channel

- 20.7. Israel Electric Vehicle Semiconductor Market

- 20.7.1. Country Segmental Analysis

- 20.7.2. Device Type

- 20.7.3. Semiconductor Material

- 20.7.4. Voltage Range

- 20.7.5. Packaging Type

- 20.7.6. Technology Type

- 20.7.7. Integration Level

- 20.7.8. Vehicle Type

- 20.7.9. Electric Vehicle Type

- 20.7.10. Sales Channel

- 20.8. Rest of Middle East Electric Vehicle Semiconductor Market

- 20.8.1. Country Segmental Analysis

- 20.8.2. Device Type

- 20.8.3. Semiconductor Material

- 20.8.4. Voltage Range

- 20.8.5. Packaging Type

- 20.8.6. Technology Type

- 20.8.7. Integration Level

- 20.8.8. Vehicle Type

- 20.8.9. Electric Vehicle Type

- 20.8.10. Sales Channel

- 21. Africa Electric Vehicle Semiconductor Market Analysis

- 21.1. Key Segment Analysis

- 21.2. Regional Snapshot

- 21.3. Africa Electric Vehicle Semiconductor Market Size Volume (Million Units) and Value (US$ Bn), Analysis, and Forecasts, 2021-2035

- 21.3.1. Device Type

- 21.3.2. Semiconductor Material

- 21.3.3. Voltage Range

- 21.3.4. Packaging Type

- 21.3.5. Technology Type

- 21.3.6. Integration Level

- 21.3.7. Vehicle Type

- 21.3.8. Electric Vehicle Type

- 21.3.9. Sales Channel

- 21.3.10. Country

- 21.3.10.1. South Africa

- 21.3.10.2. Egypt

- 21.3.10.3. Nigeria

- 21.3.10.4. Algeria

- 21.3.10.5. Rest of Africa

- 21.4. South Africa Electric Vehicle Semiconductor Market

- 21.4.1. Country Segmental Analysis

- 21.4.2. Device Type

- 21.4.3. Semiconductor Material

- 21.4.4. Voltage Range

- 21.4.5. Packaging Type

- 21.4.6. Technology Type

- 21.4.7. Integration Level

- 21.4.8. Vehicle Type

- 21.4.9. Electric Vehicle Type

- 21.4.10. Sales Channel

- 21.5. Egypt Electric Vehicle Semiconductor Market

- 21.5.1. Country Segmental Analysis

- 21.5.2. Device Type

- 21.5.3. Semiconductor Material

- 21.5.4. Voltage Range

- 21.5.5. Packaging Type

- 21.5.6. Technology Type

- 21.5.7. Integration Level

- 21.5.8. Vehicle Type

- 21.5.9. Electric Vehicle Type

- 21.5.10. Sales Channel

- 21.6. Nigeria Electric Vehicle Semiconductor Market

- 21.6.1. Country Segmental Analysis

- 21.6.2. Device Type

- 21.6.3. Semiconductor Material

- 21.6.4. Voltage Range

- 21.6.5. Packaging Type

- 21.6.6. Technology Type

- 21.6.7. Integration Level

- 21.6.8. Vehicle Type

- 21.6.9. Electric Vehicle Type

- 21.6.10. Sales Channel

- 21.7. Algeria Electric Vehicle Semiconductor Market

- 21.7.1. Country Segmental Analysis

- 21.7.2. Device Type

- 21.7.3. Semiconductor Material

- 21.7.4. Voltage Range

- 21.7.5. Packaging Type

- 21.7.6. Technology Type

- 21.7.7. Integration Level

- 21.7.8. Vehicle Type

- 21.7.9. Electric Vehicle Type

- 21.7.10. Sales Channel

- 21.8. Rest of Africa Electric Vehicle Semiconductor Market

- 21.8.1. Country Segmental Analysis

- 21.8.2. Device Type

- 21.8.3. Semiconductor Material

- 21.8.4. Voltage Range

- 21.8.5. Packaging Type

- 21.8.6. Technology Type

- 21.8.7. Integration Level

- 21.8.8. Vehicle Type

- 21.8.9. Electric Vehicle Type

- 21.8.10. Sales Channel

- 22. South America Electric Vehicle Semiconductor Market Analysis

- 22.1. Key Segment Analysis

- 22.2. Regional Snapshot

- 22.3. South America Electric Vehicle Semiconductor Market Size Volume (Million Units) and Value (US$ Bn), Analysis, and Forecasts, 2021-2035

- 22.3.1. Device Type

- 22.3.2. Semiconductor Material

- 22.3.3. Voltage Range

- 22.3.4. Packaging Type

- 22.3.5. Technology Type

- 22.3.6. Integration Level

- 22.3.7. Vehicle Type

- 22.3.8. Electric Vehicle Type

- 22.3.9. Sales Channel

- 22.3.10. Country

- 22.3.10.1. Brazil

- 22.3.10.2. Argentina

- 22.3.10.3. Rest of South America

- 22.4. Brazil Electric Vehicle Semiconductor Market

- 22.4.1. Country Segmental Analysis

- 22.4.2. Device Type

- 22.4.3. Semiconductor Material

- 22.4.4. Voltage Range

- 22.4.5. Packaging Type

- 22.4.6. Technology Type

- 22.4.7. Integration Level

- 22.4.8. Vehicle Type

- 22.4.9. Electric Vehicle Type

- 22.4.10. Sales Channel

- 22.5. Argentina Electric Vehicle Semiconductor Market

- 22.5.1. Country Segmental Analysis

- 22.5.2. Device Type

- 22.5.3. Semiconductor Material

- 22.5.4. Voltage Range

- 22.5.5. Packaging Type

- 22.5.6. Technology Type

- 22.5.7. Integration Level

- 22.5.8. Vehicle Type

- 22.5.9. Electric Vehicle Type

- 22.5.10. Sales Channel

- 22.6. Rest of South America Electric Vehicle Semiconductor Market

- 22.6.1. Country Segmental Analysis

- 22.6.2. Device Type

- 22.6.3. Semiconductor Material

- 22.6.4. Voltage Range

- 22.6.5. Packaging Type

- 22.6.6. Technology Type

- 22.6.7. Integration Level

- 22.6.8. Vehicle Type

- 22.6.9. Electric Vehicle Type

- 22.6.10. Sales Channel

- 23. Key Players/ Company Profile

- 23.1. Analog Devices, Inc.

- 23.1.1. Company Details/ Overview

- 23.1.2. Company Financials

- 23.1.3. Key Customers and Competitors

- 23.1.4. Business/ Industry Portfolio

- 23.1.5. Product Portfolio/ Specification Details

- 23.1.6. Pricing Data

- 23.1.7. Strategic Overview

- 23.1.8. Recent Developments

- 23.2. Broadcom Inc.

- 23.3. Fuji Electric Co., Ltd.

- 23.4. Infineon Technologies AG

- 23.5. Intel Corporation

- 23.6. Littelfuse, Inc.

- 23.7. Microchip Technology Incorporated

- 23.8. Micron Technology, Inc.

- 23.9. Mitsubishi Electric Corporation

- 23.10. NVIDIA Corporation

- 23.11. NXP Semiconductors N.V.

- 23.12. Qualcomm Technologies, Inc.

- 23.13. Renesas Electronics Corporation

- 23.14. Robert Bosch GmbH

- 23.15. ROHM Co., Ltd.

- 23.16. Semiconductor Components Industries, LLC (onsemi)

- 23.17. STMicroelectronics N.V.

- 23.18. Texas Instruments Incorporated

- 23.19. Toshiba Electronic Devices & Storage Corporation

- 23.20. Wolfspeed, Inc.

- 23.21. Other Key Players

- 23.1. Analog Devices, Inc.

Note* - This is just tentative list of players. While providing the report, we will cover more number of players based on their revenue and share for each geography

Research Design

Our research design integrates both demand-side and supply-side analysis through a balanced combination of primary and secondary research methodologies. By utilizing both bottom-up and top-down approaches alongside rigorous data triangulation methods, we deliver robust market intelligence that supports strategic decision-making.

MarketGenics' comprehensive research design framework ensures the delivery of accurate, reliable, and actionable market intelligence. Through the integration of multiple research approaches, rigorous validation processes, and expert analysis, we provide our clients with the insights needed to make informed strategic decisions and capitalize on market opportunities.

MarketGenics leverages a dedicated industry panel of experts and a comprehensive suite of paid databases to effectively collect, consolidate, and analyze market intelligence.

Our approach has consistently proven to be reliable and effective in generating accurate market insights, identifying key industry trends, and uncovering emerging business opportunities.

Through both primary and secondary research, we capture and analyze critical company-level data such as manufacturing footprints, including technical centers, R&D facilities, sales offices, and headquarters.

Our expert panel further enhances our ability to estimate market size for specific brands based on validated field-level intelligence.

Our data mining techniques incorporate both parametric and non-parametric methods, allowing for structured data collection, sorting, processing, and cleaning.

Demand projections are derived from large-scale data sets analyzed through proprietary algorithms, culminating in robust and reliable market sizing.

Research Approach

The bottom-up approach builds market estimates by starting with the smallest addressable market units and systematically aggregating them to create comprehensive market size projections.

This method begins with specific, granular data points and builds upward to create the complete market landscape.

Customer Analysis → Segmental Analysis → Geographical Analysis

The top-down approach starts with the broadest possible market data and systematically narrows it down through a series of filters and assumptions to arrive at specific market segments or opportunities.

This method begins with the big picture and works downward to increasingly specific market slices.

TAM → SAM → SOM

Research Methods

Desk / Secondary Research

While analysing the market, we extensively study secondary sources, directories, and databases to identify and collect information useful for this technical, market-oriented, and commercial report. Secondary sources that we utilize are not only the public sources, but it is a combination of Open Source, Associations, Paid Databases, MG Repository & Knowledgebase, and others.

- Company websites, annual reports, financial reports, broker reports, and investor presentations

- National government documents, statistical databases and reports

- News articles, press releases and web-casts specific to the companies operating in the market, Magazines, reports, and others

- We gather information from commercial data sources for deriving company specific data such as segmental revenue, share for geography, product revenue, and others

- Internal and external proprietary databases (industry-specific), relevant patent, and regulatory databases

- Governing Bodies, Government Organizations

- Relevant Authorities, Country-specific Associations for Industries

We also employ the model mapping approach to estimate the product level market data through the players' product portfolio

Primary Research

Primary research/ interviews is vital in analyzing the market. Most of the cases involves paid primary interviews. Primary sources include primary interviews through e-mail interactions, telephonic interviews, surveys as well as face-to-face interviews with the different stakeholders across the value chain including several industry experts.

| Type of Respondents | Number of Primaries |

|---|---|

| Tier 2/3 Suppliers | ~20 |

| Tier 1 Suppliers | ~25 |

| End-users | ~25 |

| Industry Expert/ Panel/ Consultant | ~30 |

| Total | ~100 |

MG Knowledgebase

• Repository of industry blog, newsletter and case studies

• Online platform covering detailed market reports, and company profiles

Forecasting Factors and Models

Forecasting Factors

- Historical Trends – Past market patterns, cycles, and major events that shaped how markets behave over time. Understanding past trends helps predict future behavior.

- Industry Factors – Specific characteristics of the industry like structure, regulations, and innovation cycles that affect market dynamics.

- Macroeconomic Factors – Economic conditions like GDP growth, inflation, and employment rates that affect how much money people have to spend.

- Demographic Factors – Population characteristics like age, income, and location that determine who can buy your product.

- Technology Factors – How quickly people adopt new technology and how much technology infrastructure exists.

- Regulatory Factors – Government rules, laws, and policies that can help or restrict market growth.

- Competitive Factors – Analyzing competition structure such as degree of competition and bargaining power of buyers and suppliers.

Forecasting Models / Techniques

Multiple Regression Analysis

- Identify and quantify factors that drive market changes

- Statistical modeling to establish relationships between market drivers and outcomes

Time Series Analysis – Seasonal Patterns

- Understand regular cyclical patterns in market demand

- Advanced statistical techniques to separate trend, seasonal, and irregular components

Time Series Analysis – Trend Analysis

- Identify underlying market growth patterns and momentum

- Statistical analysis of historical data to project future trends

Expert Opinion – Expert Interviews

- Gather deep industry insights and contextual understanding

- In-depth interviews with key industry stakeholders

Multi-Scenario Development

- Prepare for uncertainty by modeling different possible futures

- Creating optimistic, pessimistic, and most likely scenarios

Time Series Analysis – Moving Averages

- Sophisticated forecasting for complex time series data

- Auto-regressive integrated moving average models with seasonal components

Econometric Models

- Apply economic theory to market forecasting

- Sophisticated economic models that account for market interactions

Expert Opinion – Delphi Method

- Harness collective wisdom of industry experts

- Structured, multi-round expert consultation process

Monte Carlo Simulation

- Quantify uncertainty and probability distributions

- Thousands of simulations with varying input parameters

Research Analysis

Our research framework is built upon the fundamental principle of validating market intelligence from both demand and supply perspectives. This dual-sided approach ensures comprehensive market understanding and reduces the risk of single-source bias.

Demand-Side Analysis: We understand end-user/application behavior, preferences, and market needs along with the penetration of the product for specific application.

Supply-Side Analysis: We estimate overall market revenue, analyze the segmental share along with industry capacity, competitive landscape, and market structure.

Validation & Evaluation

Data triangulation is a validation technique that uses multiple methods, sources, or perspectives to examine the same research question, thereby increasing the credibility and reliability of research findings. In market research, triangulation serves as a quality assurance mechanism that helps identify and minimize bias, validate assumptions, and ensure accuracy in market estimates.

- Data Source Triangulation – Using multiple data sources to examine the same phenomenon

- Methodological Triangulation – Using multiple research methods to study the same research question

- Investigator Triangulation – Using multiple researchers or analysts to examine the same data

- Theoretical Triangulation – Using multiple theoretical perspectives to interpret the same data

Custom Market Research Services

We will customise the research for you, in case the report listed above does not meet your requirements.

Get 10% Free Customisation