Fleet Management Market Size, Share & Trends Analysis Report by Solution Type (Software, Hardware, Services), Deployment Mode, Fleet Type, Vehicle Propulsion Type, Fleet Size, Connectivity Technology, Application, End-users, and Geography (North America, Europe, Asia Pacific, Middle East, Africa, and South America) – Global Industry Data, Trends, and Forecasts, 2026–2035

|

|

|

Segmental Data Insights |

|

|

Demand Trends |

|

|

Competitive Landscape |

|

|

Strategic Development |

|

|

Future Outlook & Opportunities |

|

Fleet Management Market Size, Share, and Growth

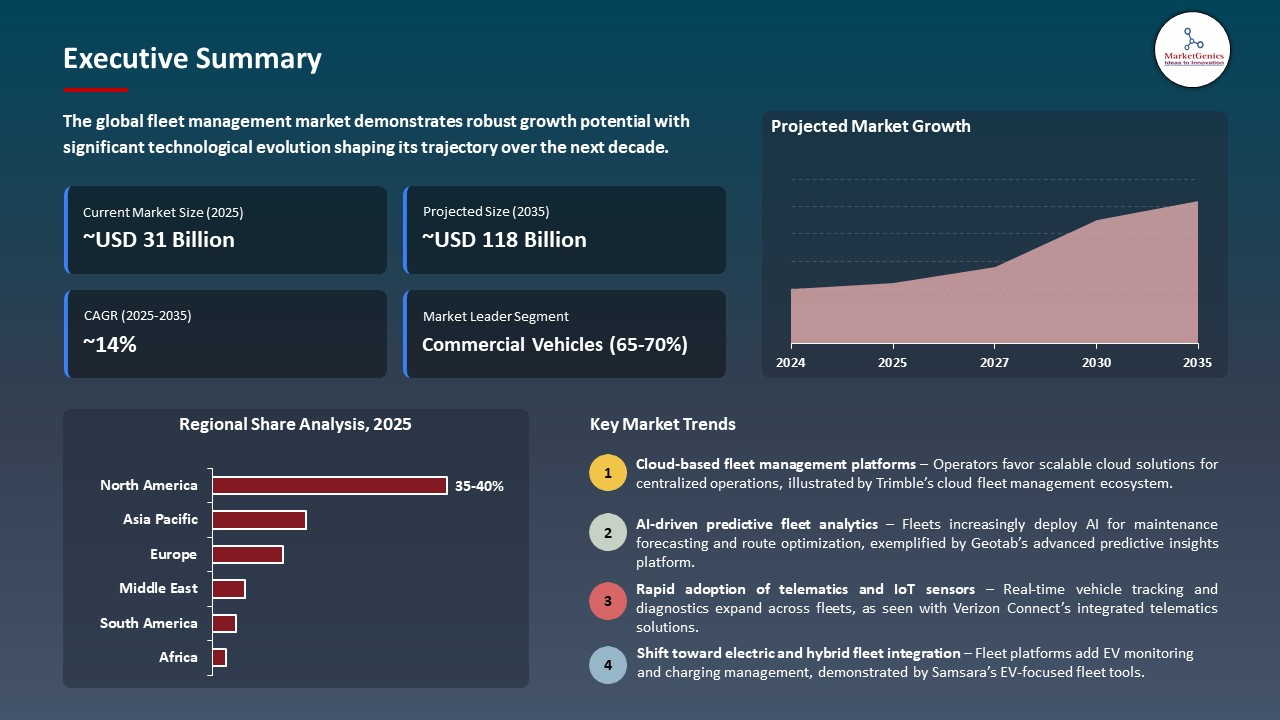

The global fleet management market is witnessing strong growth, valued at USD 30.9 billion in 2025 and projected to reach USD 117.6 billion by 2035, expanding at a CAGR of 14.3% during the forecast period. Asia Pacific is the fastest-growing fleet management market due to rapid expansion of e-commerce and logistics activities, increasing vehicle fleets, and rising adoption of digital telematics solutions across emerging economies.

Andy Yearout, VP of Transportation & Logistics at Mohawk Industries, said, “Samsara has made a significant impact on our operations, saving $7.75 million annually across our three fleets by helping us optimize planned versus actuals route improvements, With the new Route Planning capability, we expect to see a reduction in daily route planning time from hours to minutes.”

The rapid implementation of telematics, IoT and AI technologies is causing pressure in the fleet management marketplace as operators are demanded real time tracking of their vehicles, predictive maintenance, fuel optimization and increased safety as a way to reduce costs and efficiency. Indicatively, Trimble Inc. in 2025 unveiled its forthcoming FleetXPS, an aggregate of superior routing and automated dispatching with cloud analytics, which can assist huge fleets to minimize idle mores and operating expenses. In late 2024, Omnitracs also launched a new version of their Compliance Management Module that will automate regulatory reporting and will also streamline the ELD and Hours-of-Service compliance for commercial trucking operators.

Moreover, the Geotab EV fleet electrification solution of 2024 added more 360-degree charging infrastructure and the optimization of electric routes as the industry trends toward sustainable fleets. These innovations demonstrate that connected hardware and integrated software are making smarter decisions, enhance the overall use of fleets and operational strength, which is driving the growth of the market further. Improved data analytics and automation is having a huge impact on lowering operational costs and enhancing safety outcomes on a global fleet basis.

The fleet management market has adjacent opportunities such as integration of electric vehicle charging infrastructure, telematics-based insurance services, predictive maintenance analytics, autonomous vehicle operations platforms, and smart logistics optimization services. These segments use related vehicle information to maximize efficiency, sustainability, driver safety, and cost management throughout commercial transportation ecosystems around the world that allow transformation.

Fleet Management Market Dynamics and Trends

Fleet Management Market Dynamics and Trends

Driver: Growing Adoption of AI‑Enabled Predictive Maintenance Solutions by Fleet Operators

-

The increasing use of AI-based predictive maintenance technologies is driving the fleet management market by allowing the operator to address the vehicle problems proactively, minimize unexpected downtime, and improve operational efficiency.

- The uses of these advanced systems are based on IoT sensors, telematics, and machine learning as the tools used to analyze real-time data, forecast possible failures, and optimize maintenance schedules. Predictive maintenance is emerging as an essential strategic resource to the contemporary fleet operator around the world by reducing the cost of repairs, increasing vehicle lifecycle, and making the fleet more secure in general.

- Verizon Connect, a subset of Verizon, in November 2025 introduced Operational Insights, a generative AI system in its Reveal platform to convert complicated fleet data into useful knowledge. The tool detects anomalies, inefficiencies, and risks to safety and makes managers have clear and priority insights which help them to optimize operations, cut-down costs, and improve productivity in fleet safety, efficiency, and performance.

- The implementation of predictive maintenance with AI is greatly improving the efficiency, safety, and cost-effectiveness of fleets globally.

Restraint: High Integration Costs and Complexity of Advanced Fleet Telematics Systems

-

High cost of integration and complexity of advanced fleet telematics systems is a major inhibitor of the fleet management market. Full telematics solutions are financially costly to install hardware, software, and network, and may be unaffordable to small and medium fleet operators.

- Besides the financial aspect, to apply telematics systems to the current fleet operations, ERP software, and maintenance schedules, it is necessary to have a specific expertise and constant technical support. The additional implementation burden is further added with complex data management, cybersecurity requirements and interoperability across the various types of vehicles, as well as vendors. The expensive price and technical nature of sophisticated telematics system is also the major barrier to the fleet operator using digital technologies to enhance efficiency and safety.

- Such considerations might slow down the deployment, add to operational disturbance in the process of integration and constrain adoption by low-cost operators, particularly in frontier markets.

Opportunity: Expansion of Electric Vehicle Fleet Monitoring and Charging Optimization Services

-

Rapid uptake of the electric vehicles (EVs) by commercial and general fleets is presenting a massive market opportunity in the fleet management market with EV fleet monitoring and charging optimization services.

- New state-of-the-art fleet management systems combine real-time battery health, route optimization, and the availability of charging stations to keep the downtime to a minimum, decrease the energy spending, and optimize the fleet performance. These services help to enable predictive charging schedules, lessen range anxiety and enhance the efficiency of operations of fleet operators to easily shift to electric mobility and help sustainability objectives, thereby generating a high growth opportunity to providers of fleet management solutions.

- Geotab has made improvements to the EV Fleet Management platform to manage more than 300 different models of electric vehicles, including real-time battery telemetry, state-of-charge monitoring, route optimization, and charging management.

- EV fleet surveillance and charging optimization is making efficiency, cost reduction, and a sustainable fleet operation.

Key Trend: Integration of Autonomous Driving Data Streams into Fleet Operational Platforms

-

Autonomous driving data streams integration in fleet operational platforms is an key trend in the fleet management market. Live information of autonomous vehicles such as sensor data, road data, and route data allows the fleet operators to make decisions about operations and improve the development of safety protocols.

- Implying the possibility of utilizing autonomous vehicle data, companies can optimize their route planning, improve predictive maintenance, track the work of driverless fleets, and, as a result, get more efficiency, reduce operational expenses, and contribute to the move towards smarter and more automated fleet environments.

- Moove effortlessly dispatched its fully autonomous EV fleet to Phoenix in partnership with Waymo in December 2024. Moove manages fleet management, charging infrastructure, and facilities whereas Waymo ensures autonomous driving validation.

- The trend is propelling less risky, efficient, and cost-effective fleet operations besides speeding the implementation of autonomous mobility solutions.

Fleet Management Market Analysis and Segmental Data

Fleet Management Market Analysis and Segmental Data

Commercial Vehicles Dominate Global Fleet Management Market

-

Commercial vehicles represent the leading segment in the global fleet management market, accounting for the largest share due to their extensive use across logistics, transportation, construction, and public services. Businesses operating large fleets of trucks, buses, and vans increasingly rely on fleet management solutions to enhance operational efficiency and reduce overall costs.

- The prevalence of this section is mainly based on the rising demand of real-time tracking of vehicles, optimization of routes, fuel, and driver monitoring. Fleet operators are implementing complex telematics and analytics to enhance productivity and reduce downtime as well as comply with regulations.

- The growing popularity of last-mile delivery service, e-commerce growth, and growing emphasis on safety and sustainability make the commercial vehicles segment the most urgent and the most profitable in the world of fleet management markets.

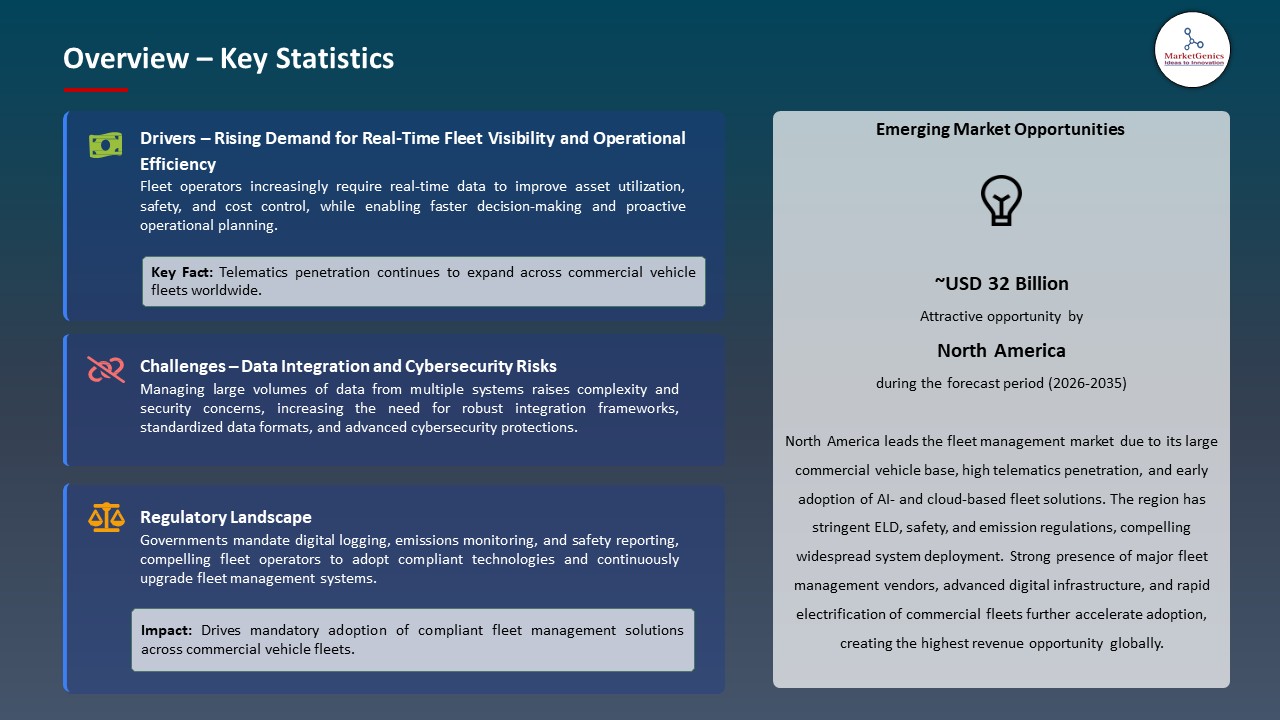

North America Leads Global Fleet Management Market Demand

-

North America dominates the worldwide fleet management market as demand because of the early crossbreeding of advanced telematics technologies and the high presence of developed solution providers. The transport and logistics market is highly developed in the region, which leads to further investment in digital monitoring of the fleet, vehicle tracking, and analytics of the data.

- Increasing regulatory demands to driver safety, vehicle maintenance and emission control are also encouraging the popularity of fleet management systems. These solutions are being adopted by more and more enterprises in industries trying to ensure better operational efficiency, lower fuel consumption, and better use of their fleets. Moreover, the increasing demand of related vehicles, electric fleets, and automated logistics business is opening new growth opportunities in the region.

- The growing attention to real time visibility, predictive maintenance and smart mobility solutions make North America the most developed and profitable market of fleet control worldwide.

Fleet Management Market Ecosystem

The global fleet management market is moderately consolidated, with key players including Verizon Connect, Geotab Inc., Samsara, Trimble Inc., and Omnitracs. These firms keep their competitive edges high by possessing superior telematics systems, built-in hardware and software and large service networks. The market strength is supported by the constant investing in cloud-based analytics, Internet of Things (IoT) solutions, artificial intelligence, and collaboration with automotive and logistics partners.

The market value chain of the fleet management includes solution design and software development, telematics hardware production, system integration, data connectivity services, fleet deployment, and continued support services. Activities like real-time monitoring activities, predictive maintenance, driver behavior, and performance optimization are important in improving fleet efficiency, particularly after deployment. These interrelated phases facilitate smooth operations and enhanced safety levels, as well as enhanced decision making by fleet operators in different industries.

Entry barriers are high because they have large technological requirements, require expensive infrastructure, and data security matters and because they have long-term relationships with customers. Differentiation of markets is being driven by such efforts as continuous innovations like AI-based analytics, route optimization, connected vehicle ecosystems, and electric vehicle fleet integration. These innovations are facilitating smarter fleet management, lowering operations expenses, and contributing to the future expansion of the fleet management business globally.

Recent Development and Strategic Overview:

Recent Development and Strategic Overview:

-

In November 2025, Trimble launched its next-generation cloud-native TMS and AI-driven workflow tools to enhance fleet management operations. The platform integrates order-to-cash management, capacity planning, and shipment tracking, while AI agents automate tasks such as order intake, invoice processing, and roadside breakdown handling.

- In February 2026, Sacramento-based Kooner Fleet Management launched Kooner Mobile AutoCare, a mobile vehicle service targeting everyday drivers. The company, which has grown revenue over 3,000% since 2020, offers on-site maintenance and repair, expanding its services beyond fleet clients.

Report Scope

|

Detail |

|

|

Market Size in 2025 |

USD 30.9 Bn |

|

Market Forecast Value in 2035 |

USD 117.6 Bn |

|

Growth Rate (CAGR) |

14.3% |

|

Forecast Period |

2026 – 2035 |

|

Historical Data Available for |

2021 – 2024 |

|

Market Size Units |

US$ Billion for Value |

|

Report Format |

Electronic (PDF) + Excel |

|

North America |

Europe |

Asia Pacific |

Middle East |

Africa |

South America |

|

|

|

|

|

|

|

Companies Covered |

|||||

|

|

|

|

|

|

Fleet Management Market Segmentation and Highlights

|

Segment |

Sub-segment |

|

Fleet Management Market, By Solution Type |

|

|

Fleet Management Market, By Deployment Mode |

|

|

Fleet Management Market, By Fleet Type |

|

|

Fleet Management Market, By Vehicle Propulsion Type |

|

|

Fleet Management Market, By Fleet Size |

|

|

Fleet Management Market, By Connectivity Technology |

|

|

Fleet Management Market, By Application |

|

|

Fleet Management Market, By End-users |

|

Frequently Asked Questions

Table of Contents

- 1. Research Methodology and Assumptions

- 1.1. Definitions

- 1.2. Research Design and Approach

- 1.3. Data Collection Methods

- 1.4. Base Estimates and Calculations

- 1.5. Forecasting Models

- 1.5.1. Key Forecast Factors & Impact Analysis

- 1.6. Secondary Research

- 1.6.1. Open Sources

- 1.6.2. Paid Databases

- 1.6.3. Associations

- 1.7. Primary Research

- 1.7.1. Primary Sources

- 1.7.2. Primary Interviews with Stakeholders across Ecosystem

- 2. Executive Summary

- 2.1. Global Fleet Management Market Outlook

- 2.1.1. Fleet Management Market Size (Value - US$ Bn), and Forecasts, 2021-2035

- 2.1.2. Compounded Annual Growth Rate Analysis

- 2.1.3. Growth Opportunity Analysis

- 2.1.4. Segmental Share Analysis

- 2.1.5. Geographical Share Analysis

- 2.2. Market Analysis and Facts

- 2.3. Supply-Demand Analysis

- 2.4. Competitive Benchmarking

- 2.5. Go-to- Market Strategy

- 2.5.1. Customer/ End-use Industry Assessment

- 2.5.2. Growth Opportunity Data, 2026-2035

- 2.5.2.1. Regional Data

- 2.5.2.2. Country Data

- 2.5.2.3. Segmental Data

- 2.5.3. Identification of Potential Market Spaces

- 2.5.4. GAP Analysis

- 2.5.5. Potential Attractive Price Points

- 2.5.6. Prevailing Market Risks & Challenges

- 2.5.7. Preferred Sales & Marketing Strategies

- 2.5.8. Key Recommendations and Analysis

- 2.5.9. A Way Forward

- 2.1. Global Fleet Management Market Outlook

- 3. Industry Data and Premium Insights

- 3.1. Global Automotive & Transportation Industry Overview, 2025

- 3.1.1. Automotive & Transportation Industry Ecosystem Analysis

- 3.1.2. Key Trends for Automotive & Transportation Industry

- 3.1.3. Regional Distribution for Automotive & Transportation Industry

- 3.2. Supplier Customer Data

- 3.3. Technology Roadmap and Developments

- 3.4. Trade Analysis

- 3.4.1. Import & Export Analysis, 2025

- 3.4.2. Top Importing Countries

- 3.4.3. Top Exporting Countries

- 3.5. Trump Tariff Impact Analysis

- 3.5.1. Manufacturer

- 3.5.1.1. Based on the component & Raw material

- 3.5.2. Supply Chain

- 3.5.3. End Consumer

- 3.5.1. Manufacturer

- 3.6. Raw Material Analysis

- 3.1. Global Automotive & Transportation Industry Overview, 2025

- 4. Market Overview

- 4.1. Market Dynamics

- 4.1.1. Drivers

- 4.1.1.1. Increasing adoption of connected vehicles and telematics.

- 4.1.1.2. Rising demand for fuel efficiency and cost optimization.

- 4.1.1.3. Growing regulatory focus on vehicle safety and emissions reduction.

- 4.1.2. Restraints

- 4.1.2.1. High implementation and maintenance costs of fleet management systems.

- 4.1.2.2. Data privacy and cybersecurity concerns.

- 4.1.1. Drivers

- 4.2. Key Trend Analysis

- 4.3. Regulatory Framework

- 4.3.1. Key Regulations, Norms, and Subsidies, by Key Countries

- 4.3.2. Tariffs and Standards

- 4.3.3. Impact Analysis of Regulations on the Market

- 4.4. Value Chain Analysis

- 4.4.1. Component Suppliers

- 4.4.2. Solution Providers

- 4.4.3. System Integrators

- 4.4.4. End-Users/ Customers

- 4.5. Porter’s Five Forces Analysis

- 4.6. PESTEL Analysis

- 4.7. Global Fleet Management Market Demand

- 4.7.1. Historical Market Size – Value (US$ Bn), 2020-2024

- 4.7.2. Current and Future Market Size – Value (US$ Bn), 2026–2035

- 4.7.2.1. Y-o-Y Growth Trends

- 4.7.2.2. Absolute $ Opportunity Assessment

- 4.1. Market Dynamics

- 5. Competition Landscape

- 5.1. Competition structure

- 5.1.1. Fragmented v/s consolidated

- 5.2. Company Share Analysis, 2025

- 5.2.1. Global Company Market Share

- 5.2.2. By Region

- 5.2.2.1. North America

- 5.2.2.2. Europe

- 5.2.2.3. Asia Pacific

- 5.2.2.4. Middle East

- 5.2.2.5. Africa

- 5.2.2.6. South America

- 5.3. Product Comparison Matrix

- 5.3.1. Specifications

- 5.3.2. Market Positioning

- 5.3.3. Pricing

- 5.1. Competition structure

- 6. Global Fleet Management Market Analysis, by Solution Type

- 6.1. Key Segment Analysis

- 6.2. Fleet Management Market Size (Value - US$ Bn), Analysis, and Forecasts, by Solution Type, 2021-2035

- 6.2.1. Software

- 6.2.1.1. Fleet Tracking & Telematics

- 6.2.1.2. Fleet Analytics & Reporting

- 6.2.1.3. Fleet Maintenance Management

- 6.2.1.4. Fuel Management

- 6.2.1.5. Driver Management

- 6.2.1.6. Dispatch Management

- 6.2.1.7. Route Optimization

- 6.2.1.8. Others

- 6.2.2. Hardware

- 6.2.2.1. GPS/GNSS Devices

- 6.2.2.2. Onboard Diagnostics (OBD) Devices

- 6.2.2.3. Dashcams & Video Telematics

- 6.2.2.4. Sensors (Fuel, Temperature, Tire Pressure)

- 6.2.2.5. Mobile Data Terminals

- 6.2.2.6. RFID Tags

- 6.2.2.7. Others

- 6.2.3. Services

- 6.2.3.1. Professional Services

- 6.2.3.2. Managed Services

- 6.2.3.3. Consulting Services

- 6.2.3.4. Integration Services

- 6.2.1. Software

- 7. Global Fleet Management Market Analysis, by Deployment Mode

- 7.1. Key Segment Analysis

- 7.2. Fleet Management Market Size (Value - US$ Bn), Analysis, and Forecasts, by Deployment Mode, 2021-2035

- 7.2.1. Cloud-based

- 7.2.1.1. Public Cloud

- 7.2.1.2. Private Cloud

- 7.2.1.3. Hybrid Cloud

- 7.2.2. On-premises

- 7.2.1. Cloud-based

- 8. Global Fleet Management Market Analysis, by Fleet Type

- 8.1. Key Segment Analysis

- 8.2. Fleet Management Market Size (Value - US$ Bn), Analysis, and Forecasts, by Fleet Type, 2021-2035

- 8.2.1. Commercial Vehicles

- 8.2.1.1. Light Commercial Vehicles

- 8.2.1.2. Heavy Commercial Vehicles

- 8.2.1.3. Medium Commercial Vehicles

- 8.2.2. Passenger Vehicles

- 8.2.2.1. Cars

- 8.2.2.2. Taxis & Ride-sharing

- 8.2.2.3. Buses

- 8.2.2.4. Others

- 8.2.3. Specialty Vehicles

- 8.2.3.1. Construction Equipment

- 8.2.3.2. Agricultural Vehicles

- 8.2.3.3. Mining Vehicles

- 8.2.1. Commercial Vehicles

- 9. Global Fleet Management Market Analysis, by Vehicle Propulsion Type

- 9.1. Key Segment Analysis

- 9.2. Fleet Management Market Size (Value - US$ Bn), Analysis, and Forecasts, by Vehicle Propulsion Type, 2021-2035

- 9.2.1. Internal Combustion Engine (ICE)

- 9.2.1.1. Gasoline

- 9.2.1.2. Diesel

- 9.2.2. Electric Vehicles

- 9.2.2.1. Battery Electric Vehicles (BEV)

- 9.2.2.2. Hybrid Electric Vehicles (HEV)

- 9.2.2.3. Plug-in Hybrid Electric Vehicles (PHEV)

- 9.2.3. Alternative Fuel Vehicles

- 9.2.3.1. CNG/LNG

- 9.2.3.2. Hydrogen Fuel Cell

- 9.2.1. Internal Combustion Engine (ICE)

- 10. Global Fleet Management Market Analysis, by Fleet Size

- 10.1. Key Segment Analysis

- 10.2. Fleet Management Market Size (Value - US$ Bn), Analysis, and Forecasts, by Fleet Size, 2021-2035

- 10.2.1. Up to 10 Vehicles

- 10.2.2. 11-50 vehicles

- 10.2.3. 51-200 vehicles

- 10.2.4. 200+ vehicles

- 11. Global Fleet Management Market Analysis, by Connectivity Technology

- 11.1. Key Segment Analysis

- 11.2. Fleet Management Market Size (Value - US$ Bn), Analysis, and Forecasts, by Connectivity Technology, 2021-2035

- 11.2.1. Cellular

- 11.2.1.1. 3G

- 11.2.1.2. 4G/LTE

- 11.2.1.3. 5G

- 11.2.2. Satellite

- 11.2.3. Bluetooth

- 11.2.4. Wi-Fi

- 11.2.5. Others

- 11.2.1. Cellular

- 12. Global Fleet Management Market Analysis, by Application

- 12.1. Key Segment Analysis

- 12.2. Fleet Management Market Size (Value - US$ Bn), Analysis, and Forecasts, by Application, 2021-2035

- 12.2.1. Vehicle Tracking & Monitoring

- 12.2.2. Driver Behavior Monitoring & Safety

- 12.2.3. Fleet Optimization & Planning

- 12.2.4. Fuel Management & Monitoring

- 12.2.5. Preventive Maintenance & Diagnostics

- 12.2.6. Compliance & Regulatory Management

- 12.2.7. Asset Management

- 12.2.8. Insurance Telematics

- 12.2.9. Navigation & Routing

- 12.2.10. Others

- 13. Global Fleet Management Market Analysis, by End-users

- 13.1. Key Segment Analysis

- 13.2. Fleet Management Market Size (Value - US$ Bn), Analysis, and Forecasts, by End-users, 2021-2035

- 13.2.1. Transportation & Logistics

- 13.2.2. Construction

- 13.2.3. Retail & E-commerce

- 13.2.4. Government & Public Sector

- 13.2.5. Oil & Gas

- 13.2.6. Utilities

- 13.2.7. Food & Beverage

- 13.2.8. Manufacturing

- 13.2.9. Field Services

- 13.2.10. Mining

- 13.2.11. Healthcare

- 13.2.12. Waste Management

- 13.2.13. Telecommunications

- 13.2.14. Others

- 14. Global Fleet Management Market Analysis and Forecasts, by Region

- 14.1. Key Findings

- 14.2. Fleet Management Market Size (Value - US$ Bn), Analysis, and Forecasts, by Region, 2021-2035

- 14.2.1. North America

- 14.2.2. Europe

- 14.2.3. Asia Pacific

- 14.2.4. Middle East

- 14.2.5. Africa

- 14.2.6. South America

- 15. North America Fleet Management Market Analysis

- 15.1. Key Segment Analysis

- 15.2. Regional Snapshot

- 15.3. North America Fleet Management Market Size (Value - US$ Bn), Analysis, and Forecasts, 2021-2035

- 15.3.1. Solution Type

- 15.3.2. Deployment Mode

- 15.3.3. Fleet Type

- 15.3.4. Vehicle Propulsion Type

- 15.3.5. Fleet Size

- 15.3.6. Connectivity Technology

- 15.3.7. Application

- 15.3.8. End-users

- 15.3.9. Country

- 15.3.9.1. USA

- 15.3.9.2. Canada

- 15.3.9.3. Mexico

- 15.4. USA Fleet Management Market

- 15.4.1. Country Segmental Analysis

- 15.4.2. Solution Type

- 15.4.3. Deployment Mode

- 15.4.4. Fleet Type

- 15.4.5. Vehicle Propulsion Type

- 15.4.6. Fleet Size

- 15.4.7. Connectivity Technology

- 15.4.8. Application

- 15.4.9. End-users

- 15.5. Canada Fleet Management Market

- 15.5.1. Country Segmental Analysis

- 15.5.2. Solution Type

- 15.5.3. Deployment Mode

- 15.5.4. Fleet Type

- 15.5.5. Vehicle Propulsion Type

- 15.5.6. Fleet Size

- 15.5.7. Connectivity Technology

- 15.5.8. Application

- 15.5.9. End-users

- 15.6. Mexico Fleet Management Market

- 15.6.1. Country Segmental Analysis

- 15.6.2. Solution Type

- 15.6.3. Deployment Mode

- 15.6.4. Fleet Type

- 15.6.5. Vehicle Propulsion Type

- 15.6.6. Fleet Size

- 15.6.7. Connectivity Technology

- 15.6.8. Application

- 15.6.9. End-users

- 16. Europe Fleet Management Market Analysis

- 16.1. Key Segment Analysis

- 16.2. Regional Snapshot

- 16.3. Europe Fleet Management Market Size (Value - US$ Bn), Analysis, and Forecasts, 2021-2035

- 16.3.1. Solution Type

- 16.3.2. Deployment Mode

- 16.3.3. Fleet Type

- 16.3.4. Vehicle Propulsion Type

- 16.3.5. Fleet Size

- 16.3.6. Connectivity Technology

- 16.3.7. Application

- 16.3.8. End-users

- 16.3.9. Country

- 16.3.9.1. Germany

- 16.3.9.2. United Kingdom

- 16.3.9.3. France

- 16.3.9.4. Italy

- 16.3.9.5. Spain

- 16.3.9.6. Netherlands

- 16.3.9.7. Nordic Countries

- 16.3.9.8. Poland

- 16.3.9.9. Russia & CIS

- 16.3.9.10. Rest of Europe

- 16.4. Germany Fleet Management Market

- 16.4.1. Country Segmental Analysis

- 16.4.2. Solution Type

- 16.4.3. Deployment Mode

- 16.4.4. Fleet Type

- 16.4.5. Vehicle Propulsion Type

- 16.4.6. Fleet Size

- 16.4.7. Connectivity Technology

- 16.4.8. Application

- 16.4.9. End-users

- 16.5. United Kingdom Fleet Management Market

- 16.5.1. Country Segmental Analysis

- 16.5.2. Solution Type

- 16.5.3. Deployment Mode

- 16.5.4. Fleet Type

- 16.5.5. Vehicle Propulsion Type

- 16.5.6. Fleet Size

- 16.5.7. Connectivity Technology

- 16.5.8. Application

- 16.5.9. End-users

- 16.6. France Fleet Management Market

- 16.6.1. Country Segmental Analysis

- 16.6.2. Solution Type

- 16.6.3. Deployment Mode

- 16.6.4. Fleet Type

- 16.6.5. Vehicle Propulsion Type

- 16.6.6. Fleet Size

- 16.6.7. Connectivity Technology

- 16.6.8. Application

- 16.6.9. End-users

- 16.7. Italy Fleet Management Market

- 16.7.1. Country Segmental Analysis

- 16.7.2. Solution Type

- 16.7.3. Deployment Mode

- 16.7.4. Fleet Type

- 16.7.5. Vehicle Propulsion Type

- 16.7.6. Fleet Size

- 16.7.7. Connectivity Technology

- 16.7.8. Application

- 16.7.9. End-users

- 16.8. Spain Fleet Management Market

- 16.8.1. Country Segmental Analysis

- 16.8.2. Solution Type

- 16.8.3. Deployment Mode

- 16.8.4. Fleet Type

- 16.8.5. Vehicle Propulsion Type

- 16.8.6. Fleet Size

- 16.8.7. Connectivity Technology

- 16.8.8. Application

- 16.8.9. End-users

- 16.9. Netherlands Fleet Management Market

- 16.9.1. Country Segmental Analysis

- 16.9.2. Solution Type

- 16.9.3. Deployment Mode

- 16.9.4. Fleet Type

- 16.9.5. Vehicle Propulsion Type

- 16.9.6. Fleet Size

- 16.9.7. Connectivity Technology

- 16.9.8. Application

- 16.9.9. End-users

- 16.10. Nordic Countries Fleet Management Market

- 16.10.1. Country Segmental Analysis

- 16.10.2. Solution Type

- 16.10.3. Deployment Mode

- 16.10.4. Fleet Type

- 16.10.5. Vehicle Propulsion Type

- 16.10.6. Fleet Size

- 16.10.7. Connectivity Technology

- 16.10.8. Application

- 16.10.9. End-users

- 16.11. Poland Fleet Management Market

- 16.11.1. Country Segmental Analysis

- 16.11.2. Solution Type

- 16.11.3. Deployment Mode

- 16.11.4. Fleet Type

- 16.11.5. Vehicle Propulsion Type

- 16.11.6. Fleet Size

- 16.11.7. Connectivity Technology

- 16.11.8. Application

- 16.11.9. End-users

- 16.12. Russia & CIS Fleet Management Market

- 16.12.1. Country Segmental Analysis

- 16.12.2. Solution Type

- 16.12.3. Deployment Mode

- 16.12.4. Fleet Type

- 16.12.5. Vehicle Propulsion Type

- 16.12.6. Fleet Size

- 16.12.7. Connectivity Technology

- 16.12.8. Application

- 16.12.9. End-users

- 16.13. Rest of Europe Fleet Management Market

- 16.13.1. Country Segmental Analysis

- 16.13.2. Solution Type

- 16.13.3. Deployment Mode

- 16.13.4. Fleet Type

- 16.13.5. Vehicle Propulsion Type

- 16.13.6. Fleet Size

- 16.13.7. Connectivity Technology

- 16.13.8. Application

- 16.13.9. End-users

- 17. Asia Pacific Fleet Management Market Analysis

- 17.1. Key Segment Analysis

- 17.2. Regional Snapshot

- 17.3. Asia Pacific Fleet Management Market Size (Value - US$ Bn), Analysis, and Forecasts, 2021-2035

- 17.3.1. Solution Type

- 17.3.2. Deployment Mode

- 17.3.3. Fleet Type

- 17.3.4. Vehicle Propulsion Type

- 17.3.5. Fleet Size

- 17.3.6. Connectivity Technology

- 17.3.7. Application

- 17.3.8. End-users

- 17.3.9. Country

- 17.3.9.1. China

- 17.3.9.2. India

- 17.3.9.3. Japan

- 17.3.9.4. South Korea

- 17.3.9.5. Australia and New Zealand

- 17.3.9.6. Indonesia

- 17.3.9.7. Malaysia

- 17.3.9.8. Thailand

- 17.3.9.9. Vietnam

- 17.3.9.10. Rest of Asia Pacific

- 17.4. China Fleet Management Market

- 17.4.1. Country Segmental Analysis

- 17.4.2. Solution Type

- 17.4.3. Deployment Mode

- 17.4.4. Fleet Type

- 17.4.5. Vehicle Propulsion Type

- 17.4.6. Fleet Size

- 17.4.7. Connectivity Technology

- 17.4.8. Application

- 17.4.9. End-users

- 17.5. India Fleet Management Market

- 17.5.1. Country Segmental Analysis

- 17.5.2. Solution Type

- 17.5.3. Deployment Mode

- 17.5.4. Fleet Type

- 17.5.5. Vehicle Propulsion Type

- 17.5.6. Fleet Size

- 17.5.7. Connectivity Technology

- 17.5.8. Application

- 17.5.9. End-users

- 17.6. Japan Fleet Management Market

- 17.6.1. Country Segmental Analysis

- 17.6.2. Solution Type

- 17.6.3. Deployment Mode

- 17.6.4. Fleet Type

- 17.6.5. Vehicle Propulsion Type

- 17.6.6. Fleet Size

- 17.6.7. Connectivity Technology

- 17.6.8. Application

- 17.6.9. End-users

- 17.7. South Korea Fleet Management Market

- 17.7.1. Country Segmental Analysis

- 17.7.2. Solution Type

- 17.7.3. Deployment Mode

- 17.7.4. Fleet Type

- 17.7.5. Vehicle Propulsion Type

- 17.7.6. Fleet Size

- 17.7.7. Connectivity Technology

- 17.7.8. Application

- 17.7.9. End-users

- 17.8. Australia and New Zealand Fleet Management Market

- 17.8.1. Country Segmental Analysis

- 17.8.2. Solution Type

- 17.8.3. Deployment Mode

- 17.8.4. Fleet Type

- 17.8.5. Vehicle Propulsion Type

- 17.8.6. Fleet Size

- 17.8.7. Connectivity Technology

- 17.8.8. Application

- 17.8.9. End-users

- 17.9. Indonesia Fleet Management Market

- 17.9.1. Country Segmental Analysis

- 17.9.2. Solution Type

- 17.9.3. Deployment Mode

- 17.9.4. Fleet Type

- 17.9.5. Vehicle Propulsion Type

- 17.9.6. Fleet Size

- 17.9.7. Connectivity Technology

- 17.9.8. Application

- 17.9.9. End-users

- 17.10. Malaysia Fleet Management Market

- 17.10.1. Country Segmental Analysis

- 17.10.2. Solution Type

- 17.10.3. Deployment Mode

- 17.10.4. Fleet Type

- 17.10.5. Vehicle Propulsion Type

- 17.10.6. Fleet Size

- 17.10.7. Connectivity Technology

- 17.10.8. Application

- 17.10.9. End-users

- 17.11. Thailand Fleet Management Market

- 17.11.1. Country Segmental Analysis

- 17.11.2. Solution Type

- 17.11.3. Deployment Mode

- 17.11.4. Fleet Type

- 17.11.5. Vehicle Propulsion Type

- 17.11.6. Fleet Size

- 17.11.7. Connectivity Technology

- 17.11.8. Application

- 17.11.9. End-users

- 17.12. Vietnam Fleet Management Market

- 17.12.1. Country Segmental Analysis

- 17.12.2. Solution Type

- 17.12.3. Deployment Mode

- 17.12.4. Fleet Type

- 17.12.5. Vehicle Propulsion Type

- 17.12.6. Fleet Size

- 17.12.7. Connectivity Technology

- 17.12.8. Application

- 17.12.9. End-users

- 17.13. Rest of Asia Pacific Fleet Management Market

- 17.13.1. Country Segmental Analysis

- 17.13.2. Solution Type

- 17.13.3. Deployment Mode

- 17.13.4. Fleet Type

- 17.13.5. Vehicle Propulsion Type

- 17.13.6. Fleet Size

- 17.13.7. Connectivity Technology

- 17.13.8. Application

- 17.13.9. End-users

- 18. Middle East Fleet Management Market Analysis

- 18.1. Key Segment Analysis

- 18.2. Regional Snapshot

- 18.3. Middle East Fleet Management Market Size (Value - US$ Bn), Analysis, and Forecasts, 2021-2035

- 18.3.1. Deployment Mode

- 18.3.2. Fleet Type

- 18.3.3. Vehicle Propulsion Type

- 18.3.4. Fleet Size

- 18.3.5. Connectivity Technology

- 18.3.6. Application

- 18.3.7. End-users

- 18.3.8. Country

- 18.3.8.1. Turkey

- 18.3.8.2. UAE

- 18.3.8.3. Saudi Arabia

- 18.3.8.4. Israel

- 18.3.8.5. Rest of Middle East

- 18.4. Turkey Fleet Management Market

- 18.4.1. Country Segmental Analysis

- 18.4.2. Solution Type

- 18.4.3. Deployment Mode

- 18.4.4. Fleet Type

- 18.4.5. Vehicle Propulsion Type

- 18.4.6. Fleet Size

- 18.4.7. Connectivity Technology

- 18.4.8. Application

- 18.4.9. End-users

- 18.5. UAE Fleet Management Market

- 18.5.1. Country Segmental Analysis

- 18.5.2. Solution Type

- 18.5.3. Deployment Mode

- 18.5.4. Fleet Type

- 18.5.5. Vehicle Propulsion Type

- 18.5.6. Fleet Size

- 18.5.7. Connectivity Technology

- 18.5.8. Application

- 18.5.9. End-users

- 18.6. Saudi Arabia Fleet Management Market

- 18.6.1. Country Segmental Analysis

- 18.6.2. Solution Type

- 18.6.3. Deployment Mode

- 18.6.4. Fleet Type

- 18.6.5. Vehicle Propulsion Type

- 18.6.6. Fleet Size

- 18.6.7. Connectivity Technology

- 18.6.8. Application

- 18.6.9. End-users

- 18.7. Israel Fleet Management Market

- 18.7.1. Country Segmental Analysis

- 18.7.2. Solution Type

- 18.7.3. Deployment Mode

- 18.7.4. Fleet Type

- 18.7.5. Vehicle Propulsion Type

- 18.7.6. Fleet Size

- 18.7.7. Connectivity Technology

- 18.7.8. Application

- 18.7.9. End-users

- 18.8. Rest of Middle East Fleet Management Market

- 18.8.1. Country Segmental Analysis

- 18.8.2. Solution Type

- 18.8.3. Deployment Mode

- 18.8.4. Fleet Type

- 18.8.5. Vehicle Propulsion Type

- 18.8.6. Fleet Size

- 18.8.7. Connectivity Technology

- 18.8.8. Application

- 18.8.9. End-users

- 19. Africa Fleet Management Market Analysis

- 19.1. Key Segment Analysis

- 19.2. Regional Snapshot

- 19.3. Africa Fleet Management Market Size (Value - US$ Bn), Analysis, and Forecasts, 2021-2035

- 19.3.1. Solution Type

- 19.3.2. Deployment Mode

- 19.3.3. Fleet Type

- 19.3.4. Vehicle Propulsion Type

- 19.3.5. Fleet Size

- 19.3.6. Connectivity Technology

- 19.3.7. Application

- 19.3.8. End-users

- 19.3.9. Country

- 19.3.9.1. South Africa

- 19.3.9.2. Egypt

- 19.3.9.3. Nigeria

- 19.3.9.4. Algeria

- 19.3.9.5. Rest of Africa

- 19.4. South Africa Fleet Management Market

- 19.4.1. Country Segmental Analysis

- 19.4.2. Solution Type

- 19.4.3. Deployment Mode

- 19.4.4. Fleet Type

- 19.4.5. Vehicle Propulsion Type

- 19.4.6. Fleet Size

- 19.4.7. Connectivity Technology

- 19.4.8. Application

- 19.4.9. End-users

- 19.5. Egypt Fleet Management Market

- 19.5.1. Country Segmental Analysis

- 19.5.2. Solution Type

- 19.5.3. Deployment Mode

- 19.5.4. Fleet Type

- 19.5.5. Vehicle Propulsion Type

- 19.5.6. Fleet Size

- 19.5.7. Connectivity Technology

- 19.5.8. Application

- 19.5.9. End-users

- 19.6. Nigeria Fleet Management Market

- 19.6.1. Country Segmental Analysis

- 19.6.2. Solution Type

- 19.6.3. Deployment Mode

- 19.6.4. Fleet Type

- 19.6.5. Vehicle Propulsion Type

- 19.6.6. Fleet Size

- 19.6.7. Connectivity Technology

- 19.6.8. Application

- 19.6.9. End-users

- 19.7. Algeria Fleet Management Market

- 19.7.1. Country Segmental Analysis

- 19.7.2. Solution Type

- 19.7.3. Deployment Mode

- 19.7.4. Fleet Type

- 19.7.5. Vehicle Propulsion Type

- 19.7.6. Fleet Size

- 19.7.7. Connectivity Technology

- 19.7.8. Application

- 19.7.9. End-users

- 19.8. Rest of Africa Fleet Management Market

- 19.8.1. Country Segmental Analysis

- 19.8.2. Solution Type

- 19.8.3. Deployment Mode

- 19.8.4. Fleet Type

- 19.8.5. Vehicle Propulsion Type

- 19.8.6. Fleet Size

- 19.8.7. Connectivity Technology

- 19.8.8. Application

- 19.8.9. End-users

- 20. South America Fleet Management Market Analysis

- 20.1. Key Segment Analysis

- 20.2. Regional Snapshot

- 20.3. South America Fleet Management Market Size (Value - US$ Bn), Analysis, and Forecasts, 2021-2035

- 20.3.1. Solution Type

- 20.3.2. Deployment Mode

- 20.3.3. Fleet Type

- 20.3.4. Vehicle Propulsion Type

- 20.3.5. Fleet Size

- 20.3.6. Connectivity Technology

- 20.3.7. Application

- 20.3.8. End-users

- 20.3.9. Country

- 20.3.9.1. Brazil

- 20.3.9.2. Argentina

- 20.3.9.3. Rest of South America

- 20.4. Brazil Fleet Management Market

- 20.4.1. Country Segmental Analysis

- 20.4.2. Solution Type

- 20.4.3. Deployment Mode

- 20.4.4. Fleet Type

- 20.4.5. Vehicle Propulsion Type

- 20.4.6. Fleet Size

- 20.4.7. Connectivity Technology

- 20.4.8. Application

- 20.4.9. End-users

- 20.5. Argentina Fleet Management Market

- 20.5.1. Country Segmental Analysis

- 20.5.2. Solution Type

- 20.5.3. Deployment Mode

- 20.5.4. Fleet Type

- 20.5.5. Vehicle Propulsion Type

- 20.5.6. Fleet Size

- 20.5.7. Connectivity Technology

- 20.5.8. Application

- 20.5.9. End-users

- 20.6. Rest of South America Fleet Management Market

- 20.6.1. Country Segmental Analysis

- 20.6.2. Solution Type

- 20.6.3. Deployment Mode

- 20.6.4. Fleet Type

- 20.6.5. Vehicle Propulsion Type

- 20.6.6. Fleet Size

- 20.6.7. Connectivity Technology

- 20.6.8. Application

- 20.6.9. End-users

- 21. Key Players/ Company Profile

- 21.1. Aave.

- 21.1.1. Company Details/ Overview

- 21.1.2. Company Financials

- 21.1.3. Key Customers and Competitors

- 21.1.4. Business/ Industry Portfolio

- 21.1.5. Product Portfolio/ Specification Details

- 21.1.6. Pricing Data

- 21.1.7. Strategic Overview

- 21.1.8. Recent Developments

- 21.2. Alchemy

- 21.3. Animoca Brands

- 21.4. Axie Infinity (Sky Mavis)

- 21.5. Binance

- 21.6. Chainalysis

- 21.7. Chainlink Labs

- 21.8. Circle Internet Financial

- 21.9. Coinbase Global

- 21.10. ConsenSys

- 21.11. Dapper Labs

- 21.12. Decentraland

- 21.13. Infura

- 21.14. MakerDAO

- 21.15. OpenSea

- 21.16. Polygon Technology

- 21.17. QuickNode

- 21.18. Ripple Labs

- 21.19. The Sandbox

- 21.20. Uniswap Labs

- 21.21. Yuga Labs

- 21.22. Other Key Players

- 21.1. Aave.

Note* - This is just tentative list of players. While providing the report, we will cover more number of players based on their revenue and share for each geography

Research Design

Our research design integrates both demand-side and supply-side analysis through a balanced combination of primary and secondary research methodologies. By utilizing both bottom-up and top-down approaches alongside rigorous data triangulation methods, we deliver robust market intelligence that supports strategic decision-making.

MarketGenics' comprehensive research design framework ensures the delivery of accurate, reliable, and actionable market intelligence. Through the integration of multiple research approaches, rigorous validation processes, and expert analysis, we provide our clients with the insights needed to make informed strategic decisions and capitalize on market opportunities.

MarketGenics leverages a dedicated industry panel of experts and a comprehensive suite of paid databases to effectively collect, consolidate, and analyze market intelligence.

Our approach has consistently proven to be reliable and effective in generating accurate market insights, identifying key industry trends, and uncovering emerging business opportunities.

Through both primary and secondary research, we capture and analyze critical company-level data such as manufacturing footprints, including technical centers, R&D facilities, sales offices, and headquarters.

Our expert panel further enhances our ability to estimate market size for specific brands based on validated field-level intelligence.

Our data mining techniques incorporate both parametric and non-parametric methods, allowing for structured data collection, sorting, processing, and cleaning.

Demand projections are derived from large-scale data sets analyzed through proprietary algorithms, culminating in robust and reliable market sizing.

Research Approach

The bottom-up approach builds market estimates by starting with the smallest addressable market units and systematically aggregating them to create comprehensive market size projections.

This method begins with specific, granular data points and builds upward to create the complete market landscape.

Customer Analysis → Segmental Analysis → Geographical Analysis

The top-down approach starts with the broadest possible market data and systematically narrows it down through a series of filters and assumptions to arrive at specific market segments or opportunities.

This method begins with the big picture and works downward to increasingly specific market slices.

TAM → SAM → SOM

Research Methods

Desk / Secondary Research

While analysing the market, we extensively study secondary sources, directories, and databases to identify and collect information useful for this technical, market-oriented, and commercial report. Secondary sources that we utilize are not only the public sources, but it is a combination of Open Source, Associations, Paid Databases, MG Repository & Knowledgebase, and others.

- Company websites, annual reports, financial reports, broker reports, and investor presentations

- National government documents, statistical databases and reports

- News articles, press releases and web-casts specific to the companies operating in the market, Magazines, reports, and others

- We gather information from commercial data sources for deriving company specific data such as segmental revenue, share for geography, product revenue, and others

- Internal and external proprietary databases (industry-specific), relevant patent, and regulatory databases

- Governing Bodies, Government Organizations

- Relevant Authorities, Country-specific Associations for Industries

We also employ the model mapping approach to estimate the product level market data through the players' product portfolio

Primary Research

Primary research/ interviews is vital in analyzing the market. Most of the cases involves paid primary interviews. Primary sources include primary interviews through e-mail interactions, telephonic interviews, surveys as well as face-to-face interviews with the different stakeholders across the value chain including several industry experts.

| Type of Respondents | Number of Primaries |

|---|---|

| Tier 2/3 Suppliers | ~20 |

| Tier 1 Suppliers | ~25 |

| End-users | ~25 |

| Industry Expert/ Panel/ Consultant | ~30 |

| Total | ~100 |

MG Knowledgebase

• Repository of industry blog, newsletter and case studies

• Online platform covering detailed market reports, and company profiles

Forecasting Factors and Models

Forecasting Factors

- Historical Trends – Past market patterns, cycles, and major events that shaped how markets behave over time. Understanding past trends helps predict future behavior.

- Industry Factors – Specific characteristics of the industry like structure, regulations, and innovation cycles that affect market dynamics.

- Macroeconomic Factors – Economic conditions like GDP growth, inflation, and employment rates that affect how much money people have to spend.

- Demographic Factors – Population characteristics like age, income, and location that determine who can buy your product.

- Technology Factors – How quickly people adopt new technology and how much technology infrastructure exists.

- Regulatory Factors – Government rules, laws, and policies that can help or restrict market growth.

- Competitive Factors – Analyzing competition structure such as degree of competition and bargaining power of buyers and suppliers.

Forecasting Models / Techniques

Multiple Regression Analysis

- Identify and quantify factors that drive market changes

- Statistical modeling to establish relationships between market drivers and outcomes

Time Series Analysis – Seasonal Patterns

- Understand regular cyclical patterns in market demand

- Advanced statistical techniques to separate trend, seasonal, and irregular components

Time Series Analysis – Trend Analysis

- Identify underlying market growth patterns and momentum

- Statistical analysis of historical data to project future trends

Expert Opinion – Expert Interviews

- Gather deep industry insights and contextual understanding

- In-depth interviews with key industry stakeholders

Multi-Scenario Development

- Prepare for uncertainty by modeling different possible futures

- Creating optimistic, pessimistic, and most likely scenarios

Time Series Analysis – Moving Averages

- Sophisticated forecasting for complex time series data

- Auto-regressive integrated moving average models with seasonal components

Econometric Models

- Apply economic theory to market forecasting

- Sophisticated economic models that account for market interactions

Expert Opinion – Delphi Method

- Harness collective wisdom of industry experts

- Structured, multi-round expert consultation process

Monte Carlo Simulation

- Quantify uncertainty and probability distributions

- Thousands of simulations with varying input parameters

Research Analysis

Our research framework is built upon the fundamental principle of validating market intelligence from both demand and supply perspectives. This dual-sided approach ensures comprehensive market understanding and reduces the risk of single-source bias.

Demand-Side Analysis: We understand end-user/application behavior, preferences, and market needs along with the penetration of the product for specific application.

Supply-Side Analysis: We estimate overall market revenue, analyze the segmental share along with industry capacity, competitive landscape, and market structure.

Validation & Evaluation

Data triangulation is a validation technique that uses multiple methods, sources, or perspectives to examine the same research question, thereby increasing the credibility and reliability of research findings. In market research, triangulation serves as a quality assurance mechanism that helps identify and minimize bias, validate assumptions, and ensure accuracy in market estimates.

- Data Source Triangulation – Using multiple data sources to examine the same phenomenon

- Methodological Triangulation – Using multiple research methods to study the same research question

- Investigator Triangulation – Using multiple researchers or analysts to examine the same data

- Theoretical Triangulation – Using multiple theoretical perspectives to interpret the same data

Custom Market Research Services

We will customise the research for you, in case the report listed above does not meet your requirements.

Get 10% Free Customisation