Health Data Interoperability Platforms Market Size, Share & Trends Analysis Report by Component (Software/Platform, Services), Interoperability Level, Deployment Mode, Data Type, Standard Type, Integration Type, Functionality, Technology, End-Use Industry, and Geography (North America, Europe, Asia Pacific, Middle East, Africa, and South America) – Global Industry Data, Trends, and Forecasts, 2025–2035

|

|

|

Segmental Data Insights |

|

|

Demand Trends |

|

|

Competitive Landscape |

|

|

Strategic Development |

|

|

Future Outlook & Opportunities |

|

Health Data Interoperability Platforms Market Size, Share, and Growth

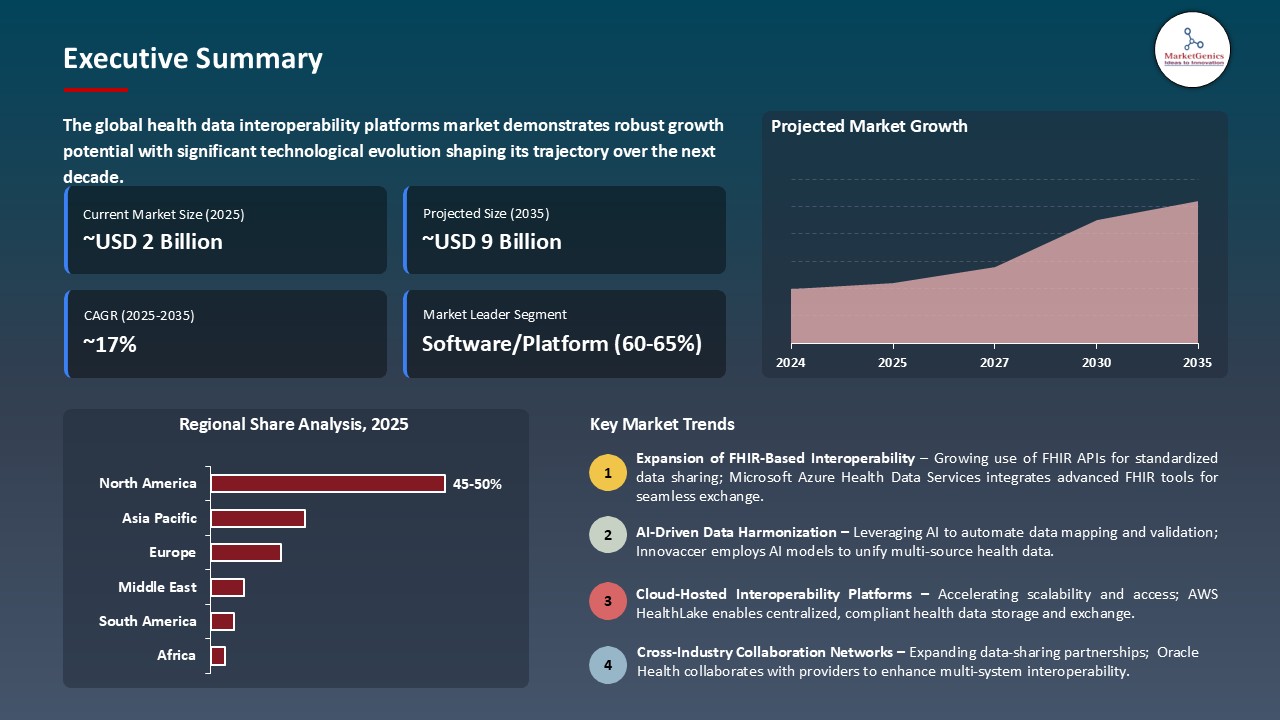

The global health data interoperability platforms market is witnessing strong growth, valued at USD 1.9 billion in 2025 and projected to reach USD 8.8 billion by 2035, expanding at a CAGR of 16.5% during the forecast period. The health data interoperability platforms market is highly competitive, characterized by strong vendor dominance, rising regulatory compliance needs, and increasing adoption of cloud-based, FHIR-enabled integration solutions across healthcare ecosystems.

“Spurred by government mandates, economic pressure, and the continued pursuit of better patient outcomes, the healthcare industry is prioritizing interoperability as a critical foundation for transformation” said Chris Lance, chief product officer, Edifecs.

Patients are growing more empowered to manage their own health information, with smooth access to their medical history, test results and treatment history. This increased awareness and digital literacy is compelling healthcare organizations to implement interoperability platforms, which allow them to share data securely and in real-time between systems and apps that result in the expansion of health data interoperability platforms market. As an example, The Ayushman Bharat Digital Mission (ABDM) in India is launching the ABHA app which enables the patients to register, digitize their medical history, and use a unique health identifier that is inter-facility linked.

The regulators are not only promoting interoperability but they are imposing it now with tangible rules, enforcement avenues, and actual punishment that alters the business incentives of EHR vendors, health systems, payers and app developers. An example is the 21st Century Cures Act and the rules it implements that ban information blocking, which are, business, technical, or organizational action or practice that unreasonably restricts access to, exchange of, or use of electronic health information (EHI).

The health data interoperability platforms market has a high potential of creating standardized ingestion pipelines to smoothly gather, standardize, and combine data gathered through wearables and Internet of Medical Things (IoMT) devices into interoperable standards like FHIR resources. As an example, At the 2025 Asia Healthcare Summit, InterSystems demonstrated the application of their platform to hospitals in Indonesia that use global data standards like HL7 FHIR to bring together data in various systems.

Health Data Interoperability Platforms Market Dynamics and Trends

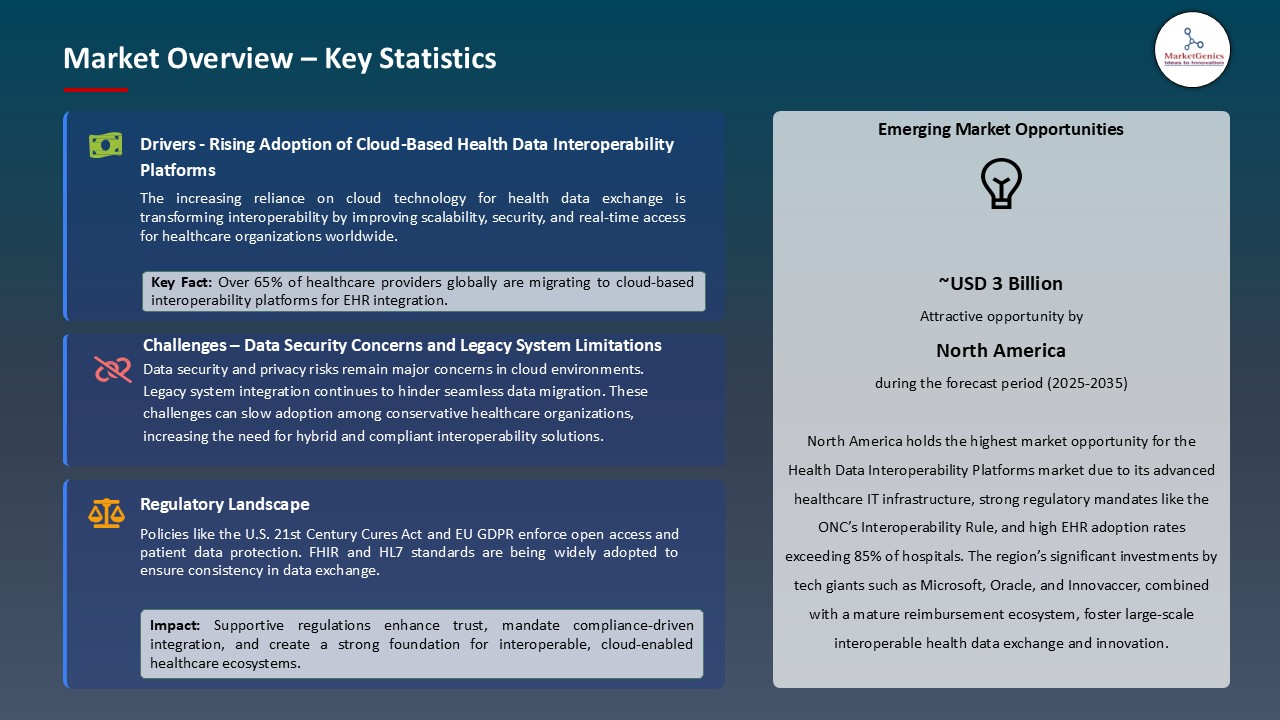

Driver: Cloud Migration Accelerates Platform-Based Integration Adoption

- The healthcare organizations that have been shifting their clinical and administrative systems to cloud environments need contemporary integration platforms that embrace distributed structures and API-first connectivity frameworks that trigger the development of health information interoperability frameworks industry. Older integration engines used in on-premise setups are not flexible and scalable to cloud-native application environments.

- Philips has further enhanced its HealthSuite Imaging services throughout Europe in 2025 providing hospitals with cloud access to enterprise imaging on Amazon Web Services (AWS) platform. The relocation facilitates the easy exchange of data, scalable storage and AI-driven diagnostic processes and eliminates the need to use expensive on-premise systems. Cloud-based integration engines lower the infrastructure cost relative to on-premise integration engines and allow quick scaling at times of peak transactions.

- Platform-as-a-service models open access to enterprise-level integration functionality to smaller healthcare organizations that could not previously afford its own integration infrastructure. Subscriptions remove the use of large capital expenditures and automatically update and issue security patches, which also reduces the need of IT resources to maintain and operate the platform.

Restraint: Data Governance Complexity Creates Implementation Challenges

- Healthcare organizations experience great challenges to implement interoperability platforms because of the complexity of data governance. Dealing with huge amounts of sensitive health information in various systems needs fully established regulations on ownership, access levels and how this data should be used. Lack of consistent policies among departments, vendors and jurisdictions usually cause confusion and inefficiencies, and all these result in impeding health data interoperability platforms market.

- Additionally, there is a high level of regulation such as HIPAA, GDPR, and regional privacy laws that increase the level of difficulty. Both frameworks require consent, sharing, retention, and auditability controls, which require a lot of legal and administrative supervision. Incorporating these requirements into one interoperable system is time and money-consuming.

- Issues with healthcare providers similar to those with other organizations include the inability to guarantee data quality standards, metadata control, and access control. Lack of close alignment between governance can create inaccurate and duplicate information that undermines the integrity of shared data.

- In conclusion, poor data governance decelerates the digital transformation process, slows interoperability adoption, and places organizations in compliance risks.

Opportunity: Population Health Management Drives Advanced Analytics Integration

- Population health management (PHM) is becoming an increasingly popular area of interest, which creates a key opportunity to introduce the concept of advanced analytics into the healthcare system, and the market of health data interoperability platforms expands. With the shift to value-based care offered by providers instead of volume-based care, the concerns about data collection, aggregation, and analysis are growing in volume regarding the type of data sources, including electronic health records (EHRs), wearables, insurance claims, and social determinants of health.

- Arcadia is a pioneering healthcare data platform and in 2025, it collaborated with Nordic Capital to speed up the development of population health management and advanced analytics. Arcadia combines clinical and financial data based on AI insights to optimize the outcomes, efficiency, and costs. The alliance highlights the growing market traction toward data-centric, value-based care, making analytics a core approach to sustainable health change.

- Thus, the implementation of PHM strategies allows the healthcare organizations to enhance care coordination, decrease readmissions, decrease costs, and increase interoperability of health data through data-driven, evidence-based insights drive development of health data interoperability platforms market.

Key Trend: FHIR-Native Architectures Replace Legacy Integration Approaches

- The migration of traditional and monolithic systems of integration to FHIR-native systems is a significant trend in digital health transformation, which is rapidly happening within the healthcare industry. The Fast Healthcare Interoperability Resources (FHIR) has become the universal standard of organized data exchange that is flexible, scalable, and API-driven.

- Orion Health and HEALWELL AI introduced a FHIR-based Pan-Canadian Patient Summary (PS-CA) in 2025, which will allow the exchange of data in real-time and across regions safely. It is based on the ISO 27269 standard and substitutes the old systems with scaling API-first architecture aimed at advancing the health data interoperability platforms market globally. Organizations in healthcare implement the APIs of FHIR to share the data more effectively, get real-time access, and integrate it with AI and telehealth systems more easily.

- Thus, modernizing infrastructure, the need to use FHIR-enabled interoperability platforms in care systems is gaining momentum, and solution providers specializing in secure, scalable and API-first data ecosystems have new business prospects.

Health-Data-Interoperability-Platforms-Market Analysis and Segmental Data

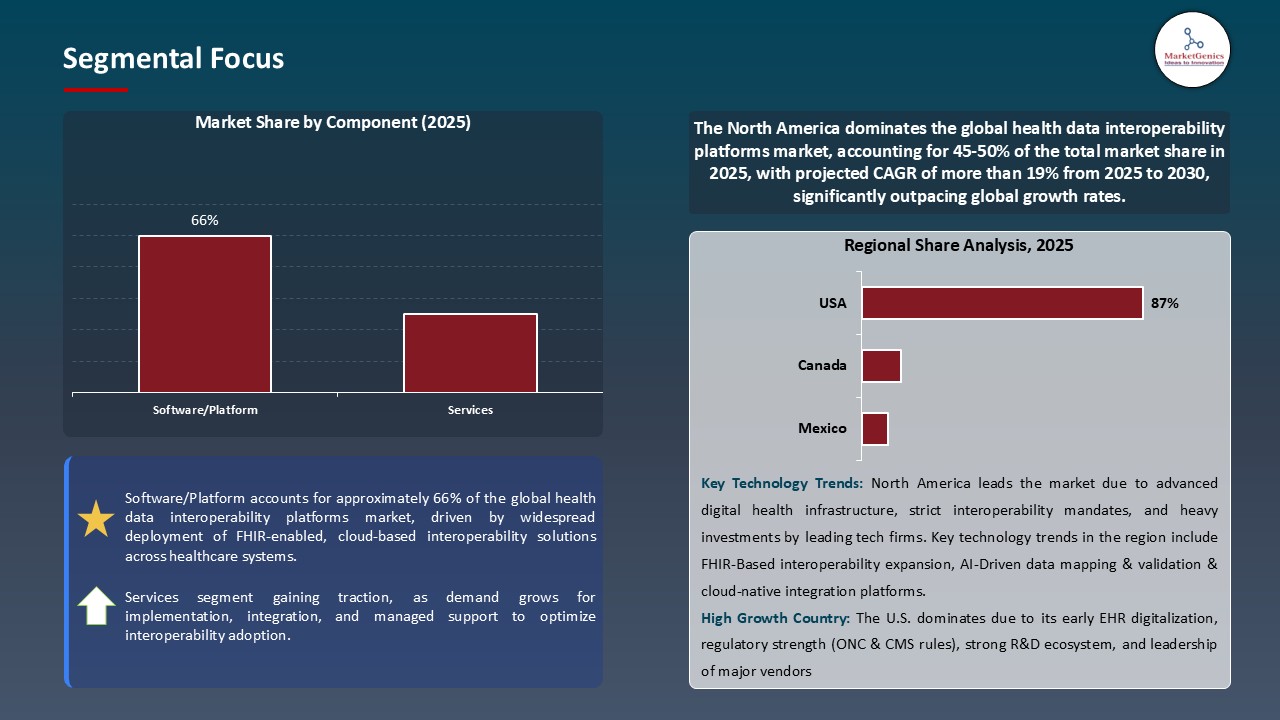

Software/Platform Dominate Global Health Data Interoperability Platforms Market

- The software/platform segment forms the basis of the global health data interoperability platforms market due to the increasing demand to achieve founded data integration, exchange, and analytics in healthcare systems. These sites act as the fundamental infrastructure that facilitates the interoperability between electronic health records (EHRs), payor systems and patient applications.

- Moreover, clinicians and health insurers are increasingly moving to the use of interoperable software platforms to streamline clinical processes, increase patient interaction, and fulfill regulatory requirements in frameworks such as TEFCA and EHDS. An example is the Microsoft which had improved its FHIR service in 2025 in the Azure Health Data Services which is a managed cloud platform that facilitates the secure and real-time exchange of health data using the FHIR standard. The service embraces the combination of EHR, imaging, and IoT information, aligning with the compliance and scalability.

- Since organizations focus on real-time, secure, and standardized data sharing, the software/platform category remains the largest market share with the greatest innovation in the interoperability landscape.

North America Leads Global Health Data Interoperability Platforms Market Demand

- North America maintains leadership role in the health data interoperability platforms market by early adoption of cloud, high healthcare IT expenditure levels, and platform vendor concentration. Huge investments in integration infrastructure by regional healthcare organizations form the basis of digital health programs and value-based care programs.

- Innovaccer Consortium introduced its Social and Community Health Information Exchange (SHIE) in 2025, an interoperable, FHIR-native system, which links healthcare, housing, justice, and social service systems to provide whole-person and community-centered care. This development demonstrates the revolution of data sharing among industries using interoperability-based platforms, which strengthens the leadership of North America in the health data interoperability market.

- Various regulatory demands such as information blocking prevention and patient access data requirements generate a sense of urgency in terms of making platform investments in North America. The nationwide enforcement of agencies against organizations that do not comply, as required by the federal government, supports the necessity of full interoperability capabilities, which motivates the further growth of the market despite any economic uncertainties surrounding other healthcare IT spending options.

Health-Data-Interoperability-Platforms-Market Ecosystem

The market of global health data interoperability platforms is relatively consolidated with the presence of the major players like Epic Systems Corporation, Cerner Corporation (Oracle Health), InterSystems Corporation, Rhapsody (Lyniate), and Redox Inc. that have a market share of about 42. These companies are leading in development of healthcare interoperability by providing complete platforms, which facilitate free flow of data across EHR, payers and digital health ecosystems. Their solutions combine with the FHIR and HL7 and API-based architecture, enabling real-time data exchange, analytics, and insights based on AI. These vendors have successfully created extensive penetration within leading healthcare systems and IT networks with the help of strong technical skills, compliance with the regulations, and partnerships. The fact that they are proven to be scalable, large integration libraries, and enterprise level capabilities poses a substantial barrier to entry to new participants.

Also, interoperability service providers and cloud infrastructure partners are also critical in facilitating deployment flexibility, compliance assurance and scalability. As an example, Rhapsody (Lyniate) provides its cloud interoperability platform and integration network implemented at a global level to simplify integrations and offer secure data connections.

Large health systems and major IT suppliers have a high level of buyer concentration and possess high negotiating power and control the feature priorities. Smaller healthcare organizations tend to use standardized prices and subscription-based methods, which are preferable to fast implementation and low-maintenance. Supplier concentration is moderate yet becoming more intense, as the large cloud services providers (AWS, Google Cloud, Microsoft Azure) are venturing in the interoperability space, providing scalable infrastructures and interoperability software sets.

Recent Development and Strategic Overview:

- In February 2025, Edifecs launched its Healthcare Interoperability Cloud, a cloud-native platform designed to unify clinical and administrative data across FHIR, EDI, and HL7v2 standards. The platform enables seamless, scalable information exchange among payers, providers, and partners strengthening data integration capabilities and driving growth in the health data interoperability platforms market.

- In September 2025, 1upHealth partnered with CommunityCare, Oklahoma’s largest locally owned health plan, to deploy its full FHIR-based interoperability suite. The collaboration enables seamless data exchange across providers, payers, and patients, improving compliance, reporting, and care coordination while supporting innovation and ROI in the health data interoperability platforms market.

Report Scope

|

Detail |

|

|

Market Size in 2025 |

USD 1.9 Bn |

|

Market Forecast Value in 2035 |

USD 8.8 Bn |

|

Growth Rate (CAGR) |

16.5% |

|

Forecast Period |

2025 – 2035 |

|

Historical Data Available for |

2021 – 2024 |

|

Market Size Units |

US$ Billion for Value |

|

Report Format |

Electronic (PDF) + Excel |

|

North America |

Europe |

Asia Pacific |

Middle East |

Africa |

South America |

|

|

|

|

|

|

|

Companies Covered |

|||||

|

|

|

|

|

|

Health-Data-Interoperability-Platforms-Market Segmentation and Highlights

|

Segment |

Sub-segment |

|

Health Data Interoperability Platforms Market, By Component |

|

|

Health Data Interoperability Platforms Market, By Interoperability Level |

|

|

Health Data Interoperability Platforms Market, By Deployment Mode |

|

|

Health Data Interoperability Platforms Market, By Data Type |

|

|

Health Data Interoperability Platforms Market, By Standard Type |

|

|

Health Data Interoperability Platforms Market, By Integration Type |

|

|

Health Data Interoperability Platforms Market, By Functionality |

|

|

Health Data Interoperability Platforms Market, By Technology |

|

|

Health Data Interoperability Platforms Market, By End-Use Industry |

|

Frequently Asked Questions

Table of Contents

- 1. Research Methodology and Assumptions

- 1.1. Definitions

- 1.2. Research Design and Approach

- 1.3. Data Collection Methods

- 1.4. Base Estimates and Calculations

- 1.5. Forecasting Models

- 1.5.1. Key Forecast Factors & Impact Analysis

- 1.6. Secondary Research

- 1.6.1. Open Sources

- 1.6.2. Paid Databases

- 1.6.3. Associations

- 1.7. Primary Research

- 1.7.1. Primary Sources

- 1.7.2. Primary Interviews with Stakeholders across Ecosystem

- 2. Executive Summary

- 2.1. Global Health Data Interoperability Platforms Market Outlook

- 2.1.1. Health Data Interoperability Platforms Market Size (Value - US$ Bn), and Forecasts, 2021-2035

- 2.1.2. Compounded Annual Growth Rate Analysis

- 2.1.3. Growth Opportunity Analysis

- 2.1.4. Segmental Share Analysis

- 2.1.5. Geographical Share Analysis

- 2.2. Market Analysis and Facts

- 2.3. Supply-Demand Analysis

- 2.4. Competitive Benchmarking

- 2.5. Go-to- Market Strategy

- 2.5.1. Customer/ End-use Industry Assessment

- 2.5.2. Growth Opportunity Data, 2025-2035

- 2.5.2.1. Regional Data

- 2.5.2.2. Country Data

- 2.5.2.3. Segmental Data

- 2.5.3. Identification of Potential Market Spaces

- 2.5.4. GAP Analysis

- 2.5.5. Potential Attractive Price Points

- 2.5.6. Prevailing Market Risks & Challenges

- 2.5.7. Preferred Sales & Marketing Strategies

- 2.5.8. Key Recommendations and Analysis

- 2.5.9. A Way Forward

- 2.1. Global Health Data Interoperability Platforms Market Outlook

- 3. Industry Data and Premium Insights

- 3.1. Global Healthcare & Pharmaceutical Industry Overview, 2025

- 3.1.1. Healthcare & Pharmaceutical Industry Ecosystem Analysis

- 3.1.2. Key Trends for Healthcare & Pharmaceutical Industry

- 3.1.3. Regional Distribution for Healthcare & Pharmaceutical Industry

- 3.2. Supplier Customer Data

- 3.3. Technology Roadmap and Developments

- 3.4. Trade Analysis

- 3.4.1. Import & Export Analysis, 2025

- 3.4.2. Top Importing Countries

- 3.4.3. Top Exporting Countries

- 3.5. Trump Tariff Impact Analysis

- 3.5.1. Manufacturer

- 3.5.1.1. Based on the component & Raw material

- 3.5.2. Supply Chain

- 3.5.3. End Consumer

- 3.5.1. Manufacturer

- 3.6. Raw Material Analysis

- 3.1. Global Healthcare & Pharmaceutical Industry Overview, 2025

- 4. Market Overview

- 4.1. Market Dynamics

- 4.1.1. Drivers

- 4.1.1.1. Rising demand for seamless patient data exchange across healthcare ecosystems

- 4.1.1.2. Rapid adoption of cloud-based healthcare IT infrastructure

- 4.1.1.3. Regulatory mandates promoting standardized interoperability

- 4.1.2. Restraints

- 4.1.2.1. High integration costs and data migration complexities

- 4.1.2.2. Lack of uniform data standards and semantic consistency across systems

- 4.1.1. Drivers

- 4.2. Key Trend Analysis

-

- 4.2.1.1. Regulatory Framework

- 4.2.2. Key Regulations, Norms, and Subsidies, by Key Countries

- 4.2.3. Tariffs and Standards

- 4.2.4. Impact Analysis of Regulations on the Market

-

- 4.3. Ecosystem Analysis

- 4.4. Porter’s Five Forces Analysis

- 4.5. PESTEL Analysis

- 4.6. Global Health Data Interoperability Platforms Market Demand

- 4.6.1. Historical Market Size - in Value (US$ Bn), 2020-2024

- 4.6.2. Current and Future Market Size - in Value (US$ Bn), 2025–2035

- 4.6.2.1. Y-o-Y Growth Trends

- 4.6.2.2. Absolute $ Opportunity Assessment

- 4.1. Market Dynamics

- 5. Competition Landscape

- 5.1. Competition structure

- 5.1.1. Fragmented v/s consolidated

- 5.2. Company Share Analysis, 2025

- 5.2.1. Global Company Market Share

- 5.2.2. By Region

- 5.2.2.1. North America

- 5.2.2.2. Europe

- 5.2.2.3. Asia Pacific

- 5.2.2.4. Middle East

- 5.2.2.5. Africa

- 5.2.2.6. South America

- 5.3. Product Comparison Matrix

- 5.3.1. Specifications

- 5.3.2. Market Positioning

- 5.3.3. Pricing

- 5.1. Competition structure

- 6. Global Health Data Interoperability Platforms Market Analysis, By Component

- 6.1. Key Segment Analysis

- 6.2. Health Data Interoperability Platforms Market Size (Value - US$ Bn), Analysis, and Forecasts, By Component, 2021-2035

- 6.2.1. Software/Platform

- 6.2.1.1. Standalone Software

- 6.2.1.2. Integrated Software

- 6.2.2. Services

- 6.2.2.1. Implementation Services

- 6.2.2.2. Training & Education

- 6.2.2.3. Support & Maintenance

- 6.2.2.4. Consulting Services

- 6.2.1. Software/Platform

- 7. Global Health Data Interoperability Platforms Market Analysis, By Interoperability Level

- 7.1. Key Segment Analysis

- 7.2. Health Data Interoperability Platforms Market Size (Value - US$ Bn), Analysis, and Forecasts, By Interoperability Level, 2021-2035

- 7.2.1. Foundational Interoperability

- 7.2.2. Structural Interoperability

- 7.2.3. Semantic Interoperability

- 7.2.4. Organizational Interoperability

- 8. Global Health Data Interoperability Platforms Market Analysis and Forecasts,By Deployment Mode

- 8.1. Key Findings

- 8.2. Health Data Interoperability Platforms Market Size (Value - US$ Mn), Analysis, and Forecasts, By Deployment Mode, 2021-2035

- 8.2.1. On-Premises

- 8.2.2. Cloud-Based

- 9. Global Health Data Interoperability Platforms Market Analysis and Forecasts, By Data Type

- 9.1. Key Findings

- 9.2. Health Data Interoperability Platforms Market Size (Vo Value - US$ Mn), Analysis, and Forecasts, By Data Type, 2021-2035

- 9.2.1. Clinical Data

- 9.2.2. Administrative Data

- 9.2.3. Financial Data

- 9.2.4. Patient-Generated Health Data

- 9.2.5. Laboratory Data

- 9.2.6. Imaging Data

- 9.2.7. Pharmacy Data

- 10. Global Health Data Interoperability Platforms Market Analysis and Forecasts, By Standard Type

- 10.1. Key Findings

- 10.2. Health Data Interoperability Platforms Market Size (Value - US$ Mn), Analysis, and Forecasts, By Standard Type, 2021-2035

- 10.2.1. HL7 (Health Level Seven)

- 10.2.1.1. HL7 V2

- 10.2.1.2. HL7 V3

- 10.2.1.3. HL7 FHIR

- 10.2.2. DICOM

- 10.2.3. CDA

- 10.2.4. SNOMED CT

- 10.2.5. IHE

- 10.2.6. NCPDP

- 10.2.7. X12N Standards

- 10.2.8. Others

- 10.2.1. HL7 (Health Level Seven)

- 11. Global Health Data Interoperability Platforms Market Analysis and Forecasts, By Integration Type

- 11.1. Key Findings

- 11.2. Health Data Interoperability Platforms Market Size (Value - US$ Mn), Analysis, and Forecasts, By Integration Type, 2021-2035

- 11.2.1. EHR Integration

- 11.2.2. Laboratory Information System Integration

- 11.2.3. Radiology Information System Integration

- 11.2.4. Pharmacy System Integration

- 11.2.5. Billing System Integration

- 11.2.6. Medical Device Integration

- 12. Global Health Data Interoperability Platforms Market Analysis and Forecasts, By Functionality

- 12.1. Key Findings

- 12.2. Health Data Interoperability Platforms Market Size (Value - US$ Mn), Analysis, and Forecasts, By Functionality, 2021-2035

- 12.2.1. Data Exchange & Sharing

- 12.2.2. Patient Matching & Identification

- 12.2.3. Document Management

- 12.2.4. Workflow Management

- 12.2.5. Analytics & Reporting

- 12.2.6. Consent Management

- 12.2.7. Master Data Management

- 12.2.8. Others

- 13. Global Health Data Interoperability Platforms Market Analysis and Forecasts, By Technology

- 13.1. Key Findings

- 13.2. Health Data Interoperability Platforms Market Size (Value - US$ Mn), Analysis, and Forecasts, By Technology, 2021-2035

- 13.2.1. API-Based Solutions

- 13.2.2. Middleware Solutions

- 13.2.3. Interface Engines

- 13.2.4. Enterprise Service Bus (ESB)

- 13.2.5. Blockchain-Based Solutions

- 13.2.6. AI/ML-Enabled Platforms

- 13.2.7. Others

- 14. Global Health Data Interoperability Platforms Market Analysis and Forecasts, By End-Use Industry

- 14.1. Key Findings

- 14.2. Health Data Interoperability Platforms Market Size (Value - US$ Mn), Analysis, and Forecasts, By End-Use Industry, 2021-2035

- 14.2.1. Healthcare Providers

- 14.2.1.1. Hospitals

- 14.2.1.2. Ambulatory Care Centers

- 14.2.1.3. Diagnostic and Imaging Centers

- 14.2.1.4. Long-Term Care Facilities

- 14.2.1.5. Others

- 14.2.1.6. Healthcare Payers

- 14.2.1.7. Insurance Companies

- 14.2.1.8. Government Payers

- 14.2.1.9. Others

- 14.2.2. Pharmaceutical Companies

- 14.2.2.1. Medical Device Manufacturers

- 14.2.2.2. Clinical Laboratories

- 14.2.2.3. Health Information Exchanges (HIEs)

- 14.2.2.4. Government & Public Health Agencies

- 14.2.2.5. Others

- 14.2.1. Healthcare Providers

- 15. Global Health Data Interoperability Platforms Market Analysis and Forecasts, by Region

- 15.1. Key Findings

- 15.2. Health Data Interoperability Platforms Market Size (Value - US$ Mn), Analysis, and Forecasts, by Region, 2021-2035

- 15.2.1. North America

- 15.2.2. Europe

- 15.2.3. Asia Pacific

- 15.2.4. Middle East

- 15.2.5. Africa

- 15.2.6. South America

- 16. North America Health Data Interoperability Platforms Market Analysis

- 16.1. Key Segment Analysis

- 16.2. Regional Snapshot

- 16.3. North America Health Data Interoperability Platforms Market Size (Value - US$ Bn), Analysis, and Forecasts, 2021-2035

- 16.3.1. Component

- 16.3.2. Interoperability Level

- 16.3.3. Deployment Mode

- 16.3.4. Data Type

- 16.3.5. Standard Type

- 16.3.6. Integration Type

- 16.3.7. Functionality

- 16.3.8. Technology

- 16.3.9. End-Use Industry

- 16.3.10. Country

- 16.3.10.1. USA

- 16.3.10.2. Canada

- 16.3.10.3. Mexico

- 16.4. USA Health Data Interoperability Platforms Market

- 16.4.1. Country Segmental Analysis

- 16.4.2. Component

- 16.4.3. Interoperability Level

- 16.4.4. Deployment Mode

- 16.4.5. Data Type

- 16.4.6. Standard Type

- 16.4.7. Integration Type

- 16.4.8. Functionality

- 16.4.9. Technology

- 16.4.10. End-Use Industry

- 16.5. Canada Health Data Interoperability Platforms Market

- 16.5.1. Country Segmental Analysis

- 16.5.2. Component

- 16.5.3. Interoperability Level

- 16.5.4. Deployment Mode

- 16.5.5. Data Type

- 16.5.6. Standard Type

- 16.5.7. Integration Type

- 16.5.8. Functionality

- 16.5.9. Technology

- 16.5.10. End-Use Industry

- 16.6. Mexico Health Data Interoperability Platforms Market

- 16.6.1. Country Segmental Analysis

- 16.6.2. Component

- 16.6.3. Interoperability Level

- 16.6.4. Deployment Mode

- 16.6.5. Data Type

- 16.6.6. Standard Type

- 16.6.7. Integration Type

- 16.6.8. Functionality

- 16.6.9. Technology

- 16.6.10. End-Use Industry

- 17. Europe Health Data Interoperability Platforms Market Analysis

- 17.1. Key Segment Analysis

- 17.2. Regional Snapshot

- 17.3. Europe Health Data Interoperability Platforms Market Size (Value - US$ Bn), Analysis, and Forecasts, 2021-2035

- 17.3.1. Component

- 17.3.2. Interoperability Level

- 17.3.3. Deployment Mode

- 17.3.4. Data Type

- 17.3.5. Standard Type

- 17.3.6. Integration Type

- 17.3.7. Functionality

- 17.3.8. Technology

- 17.3.9. End-Use Industry

- 17.3.10. Country

- 17.3.10.1. Germany

- 17.3.10.2. United Kingdom

- 17.3.10.3. France

- 17.3.10.4. Italy

- 17.3.10.5. Spain

- 17.3.10.6. Netherlands

- 17.3.10.7. Nordic Countries

- 17.3.10.8. Poland

- 17.3.10.9. Russia & CIS

- 17.3.10.10. Rest of Europe

- 17.4. Germany Health Data Interoperability Platforms Market

- 17.4.1. Country Segmental Analysis

- 17.4.2. Component

- 17.4.3. Interoperability Level

- 17.4.4. Deployment Mode

- 17.4.5. Data Type

- 17.4.6. Standard Type

- 17.4.7. Integration Type

- 17.4.8. Functionality

- 17.4.9. Technology

- 17.4.10. End-Use Industry

- 17.5. United Kingdom Health Data Interoperability Platforms Market

- 17.5.1. Country Segmental Analysis

- 17.5.2. Component

- 17.5.3. Interoperability Level

- 17.5.4. Deployment Mode

- 17.5.5. Data Type

- 17.5.6. Standard Type

- 17.5.7. Integration Type

- 17.5.8. Functionality

- 17.5.9. Technology

- 17.5.10. End-Use Industry

- 17.6. France Health Data Interoperability Platforms Market

- 17.6.1. Country Segmental Analysis

- 17.6.2. Component

- 17.6.3. Interoperability Level

- 17.6.4. Deployment Mode

- 17.6.5. Data Type

- 17.6.6. Standard Type

- 17.6.7. Integration Type

- 17.6.8. Functionality

- 17.6.9. Technology

- 17.6.10. End-Use Industry

- 17.7. Italy Health Data Interoperability Platforms Market

- 17.7.1. Country Segmental Analysis

- 17.7.2. Component

- 17.7.3. Interoperability Level

- 17.7.4. Deployment Mode

- 17.7.5. Data Type

- 17.7.6. Standard Type

- 17.7.7. Integration Type

- 17.7.8. Functionality

- 17.7.9. Technology

- 17.7.10. End-Use Industry

- 17.8. Spain Health Data Interoperability Platforms Market

- 17.8.1. Therapeutic Application

- 17.8.2. Component

- 17.8.3. Interoperability Level

- 17.8.4. Deployment Mode

- 17.8.5. Data Type

- 17.8.6. Standard Type

- 17.8.7. Integration Type

- 17.8.8. Functionality

- 17.8.9. Technology

- 17.8.10. End-Use Industry

- 17.9. Netherlands Health Data Interoperability Platforms Market

- 17.9.1. Country Segmental Analysis

- 17.9.2. Component

- 17.9.3. Interoperability Level

- 17.9.4. Deployment Mode

- 17.9.5. Data Type

- 17.9.6. Standard Type

- 17.9.7. Integration Type

- 17.9.8. Functionality

- 17.9.9. Technology

- 17.9.10. End-Use Industry

- 17.10. Nordic Countries Health Data Interoperability Platforms Market

- 17.10.1. Country Segmental Analysis

- 17.10.2. Component

- 17.10.3. Interoperability Level

- 17.10.4. Deployment Mode

- 17.10.5. Data Type

- 17.10.6. Standard Type

- 17.10.7. Integration Type

- 17.10.8. Functionality

- 17.10.9. Technology

- 17.10.10. End-Use Industry

- 17.11. Poland Health Data Interoperability Platforms Market

- 17.11.1. Country Segmental Analysis

- 17.11.2. Component

- 17.11.3. Interoperability Level

- 17.11.4. Deployment Mode

- 17.11.5. Data Type

- 17.11.6. Standard Type

- 17.11.7. Integration Type

- 17.11.8. Functionality

- 17.11.9. Technology

- 17.11.10. End-Use Industry

- 17.12. Russia & CIS Health Data Interoperability Platforms Market

- 17.12.1. Country Segmental Analysis

- 17.12.2. Component

- 17.12.3. Interoperability Level

- 17.12.4. Deployment Mode

- 17.12.5. Data Type

- 17.12.6. Standard Type

- 17.12.7. Integration Type

- 17.12.8. Functionality

- 17.12.9. Technology

- 17.12.10. End-Use Industry

- 17.13. Rest of Europe Health Data Interoperability Platforms Market

- 17.13.1. Country Segmental Analysis

- 17.13.2. Component

- 17.13.3. Interoperability Level

- 17.13.4. Deployment Mode

- 17.13.5. Data Type

- 17.13.6. Standard Type

- 17.13.7. Integration Type

- 17.13.8. Functionality

- 17.13.9. Technology

- 17.13.10. End-Use Industry

- 18. Asia Pacific Health Data Interoperability Platforms Market Analysis

- 18.1. Key Segment Analysis

- 18.2. Regional Snapshot

- 18.3. East Asia Health Data Interoperability Platforms Market Size (Value - US$ Bn), Analysis, and Forecasts, 2021-2035

- 18.3.1. Component

- 18.3.2. Interoperability Level

- 18.3.3. Deployment Mode

- 18.3.4. Data Type

- 18.3.5. Standard Type

- 18.3.6. Integration Type

- 18.3.7. Functionality

- 18.3.8. Technology

- 18.3.9. End-Use Industry

- 18.3.10. Country

- 18.3.10.1. China

- 18.3.10.2. India

- 18.3.10.3. Japan

- 18.3.10.4. South Korea

- 18.3.10.5. Australia and New Zealand

- 18.3.10.6. Indonesia

- 18.3.10.7. Malaysia

- 18.3.10.8. Thailand

- 18.3.10.9. Vietnam

- 18.3.10.10. Rest of Asia Pacific

- 18.4. China Health Data Interoperability Platforms Market

- 18.4.1. Country Segmental Analysis

- 18.4.2. Component

- 18.4.3. Interoperability Level

- 18.4.4. Deployment Mode

- 18.4.5. Data Type

- 18.4.6. Standard Type

- 18.4.7. Integration Type

- 18.4.8. Functionality

- 18.4.9. Technology

- 18.4.10. End-Use Industry

- 18.5. India Health Data Interoperability Platforms Market

- 18.5.1. Country Segmental Analysis

- 18.5.2. Component

- 18.5.3. Interoperability Level

- 18.5.4. Deployment Mode

- 18.5.5. Data Type

- 18.5.6. Standard Type

- 18.5.7. Integration Type

- 18.5.8. Functionality

- 18.5.9. Technology

- 18.5.10. End-Use Industry

- 18.6. Japan Health Data Interoperability Platforms Market

- 18.6.1. Country Segmental Analysis

- 18.6.2. Component

- 18.6.3. Interoperability Level

- 18.6.4. Deployment Mode

- 18.6.5. Data Type

- 18.6.6. Standard Type

- 18.6.7. Integration Type

- 18.6.8. Functionality

- 18.6.9. Technology

- 18.6.10. End-Use Industry

- 18.7. South Korea Health Data Interoperability Platforms Market

- 18.7.1. Country Segmental Analysis

- 18.7.2. Component

- 18.7.3. Interoperability Level

- 18.7.4. Deployment Mode

- 18.7.5. Data Type

- 18.7.6. Standard Type

- 18.7.7. Integration Type

- 18.7.8. Functionality

- 18.7.9. Technology

- 18.7.10. End-Use Industry

- 18.8. Australia and New Zealand Health Data Interoperability Platforms Market

- 18.8.1. Country Segmental Analysis

- 18.8.2. Component

- 18.8.3. Interoperability Level

- 18.8.4. Deployment Mode

- 18.8.5. Data Type

- 18.8.6. Standard Type

- 18.8.7. Integration Type

- 18.8.8. Functionality

- 18.8.9. Technology

- 18.8.10. End-Use Industry

- 18.9. Indonesia Health Data Interoperability Platforms Market

- 18.9.1. Country Segmental Analysis

- 18.9.2. Component

- 18.9.3. Interoperability Level

- 18.9.4. Deployment Mode

- 18.9.5. Data Type

- 18.9.6. Standard Type

- 18.9.7. Integration Type

- 18.9.8. Functionality

- 18.9.9. Technology

- 18.9.10. End-Use Industry

- 18.10. Malaysia Health Data Interoperability Platforms Market

- 18.10.1. Country Segmental Analysis

- 18.10.2. Component

- 18.10.3. Interoperability Level

- 18.10.4. Deployment Mode

- 18.10.5. Data Type

- 18.10.6. Standard Type

- 18.10.7. Integration Type

- 18.10.8. Functionality

- 18.10.9. Technology

- 18.10.10. End-Use Industry

- 18.11. Thailand Health Data Interoperability Platforms Market

- 18.11.1. Country Segmental Analysis

- 18.11.2. Component

- 18.11.3. Interoperability Level

- 18.11.4. Deployment Mode

- 18.11.5. Data Type

- 18.11.6. Standard Type

- 18.11.7. Integration Type

- 18.11.8. Functionality

- 18.11.9. Technology

- 18.11.10. End-Use Industry

- 18.12. Vietnam Health Data Interoperability Platforms Market

- 18.12.1. Country Segmental Analysis

- 18.12.2. Component

- 18.12.3. Interoperability Level

- 18.12.4. Deployment Mode

- 18.12.5. Data Type

- 18.12.6. Standard Type

- 18.12.7. Integration Type

- 18.12.8. Functionality

- 18.12.9. Technology

- 18.12.10. End-Use Industry

- 18.13. Rest of Asia Pacific Health Data Interoperability Platforms Market

- 18.13.1. Country Segmental Analysis

- 18.13.2. Component

- 18.13.3. Interoperability Level

- 18.13.4. Deployment Mode

- 18.13.5. Data Type

- 18.13.6. Standard Type

- 18.13.7. Integration Type

- 18.13.8. Functionality

- 18.13.9. Technology

- 18.13.10. End-Use Industry

- 19. Middle East Health Data Interoperability Platforms Market Analysis

- 19.1. Key Segment Analysis

- 19.2. Regional Snapshot

- 19.3. Middle East Health Data Interoperability Platforms Market Size (Value - US$ Bn), Analysis, and Forecasts, 2021-2035

- 19.3.1. Component

- 19.3.2. Interoperability Level

- 19.3.3. Deployment Mode

- 19.3.4. Data Type

- 19.3.5. Standard Type

- 19.3.6. Integration Type

- 19.3.7. Functionality

- 19.3.8. Technology

- 19.3.9. End-Use Industry

- 19.3.10. Country

- 19.3.10.1. Turkey

- 19.3.10.2. UAE

- 19.3.10.3. Saudi Arabia

- 19.3.10.4. Israel

- 19.3.10.5. Rest of Middle East

- 19.4. Turkey Health Data Interoperability Platforms Market

- 19.4.1. Country Segmental Analysis

- 19.4.2. Component

- 19.4.3. Interoperability Level

- 19.4.4. Deployment Mode

- 19.4.5. Data Type

- 19.4.6. Standard Type

- 19.4.7. Integration Type

- 19.4.8. Functionality

- 19.4.9. Technology

- 19.4.10. End-Use Industry

- 19.5. UAE Health Data Interoperability Platforms Market

- 19.5.1. Country Segmental Analysis

- 19.5.2. Component

- 19.5.3. Interoperability Level

- 19.5.4. Deployment Mode

- 19.5.5. Data Type

- 19.5.6. Standard Type

- 19.5.7. Integration Type

- 19.5.8. Functionality

- 19.5.9. Technology

- 19.5.10. End-Use Industry

- 19.6. Saudi Arabia Health Data Interoperability Platforms Market

- 19.6.1. Country Segmental Analysis

- 19.6.2. Component

- 19.6.3. Interoperability Level

- 19.6.4. Deployment Mode

- 19.6.5. Data Type

- 19.6.6. Standard Type

- 19.6.7. Integration Type

- 19.6.8. Functionality

- 19.6.9. Technology

- 19.6.10. End-Use Industry

- 19.7. Israel Health Data Interoperability Platforms Market

- 19.7.1. Country Segmental Analysis

- 19.7.2. Component

- 19.7.3. Interoperability Level

- 19.7.4. Deployment Mode

- 19.7.5. Data Type

- 19.7.6. Standard Type

- 19.7.7. Integration Type

- 19.7.8. Functionality

- 19.7.9. Technology

- 19.7.10. End-Use Industry

- 19.8. Rest of Middle East Health Data Interoperability Platforms Market

- 19.8.1. Country Segmental Analysis

- 19.8.2. Component

- 19.8.3. Interoperability Level

- 19.8.4. Deployment Mode

- 19.8.5. Data Type

- 19.8.6. Standard Type

- 19.8.7. Integration Type

- 19.8.8. Functionality

- 19.8.9. Technology

- 19.8.10. End-Use Industry

- 20. Africa Health Data Interoperability Platforms Market Analysis

- 20.1. Key Segment Analysis

- 20.2. Regional Snapshot

- 20.3. Africa Health Data Interoperability Platforms Market Size (Value - US$ Bn), Analysis, and Forecasts, 2021-2035

- 20.3.1. Component

- 20.3.2. Interoperability Level

- 20.3.3. Deployment Mode

- 20.3.4. Data Type

- 20.3.5. Standard Type

- 20.3.6. Integration Type

- 20.3.7. Functionality

- 20.3.8. Technology

- 20.3.9. End-Use Industry

- 20.3.10. Country

- 20.3.10.1. South Africa

- 20.3.10.2. Egypt

- 20.3.10.3. Nigeria

- 20.3.10.4. Algeria

- 20.3.10.5. Rest of Africa

- 20.4. South Africa Health Data Interoperability Platforms Market

- 20.4.1. Country Segmental Analysis

- 20.4.2. Component

- 20.4.3. Interoperability Level

- 20.4.4. Deployment Mode

- 20.4.5. Data Type

- 20.4.6. Standard Type

- 20.4.7. Integration Type

- 20.4.8. Functionality

- 20.4.9. Technology

- 20.4.10. End-Use Industry

- 20.5. Egypt Health Data Interoperability Platforms Market

- 20.5.1. Country Segmental Analysis

- 20.5.2. Component

- 20.5.3. Interoperability Level

- 20.5.4. Deployment Mode

- 20.5.5. Data Type

- 20.5.6. Standard Type

- 20.5.7. Integration Type

- 20.5.8. Functionality

- 20.5.9. Technology

- 20.5.10. End-Use Industry

- 20.6. Nigeria Health Data Interoperability Platforms Market

- 20.6.1. Country Segmental Analysis

- 20.6.2. Component

- 20.6.3. Interoperability Level

- 20.6.4. Deployment Mode

- 20.6.5. Data Type

- 20.6.6. Standard Type

- 20.6.7. Integration Type

- 20.6.8. Functionality

- 20.6.9. Technology

- 20.6.10. End-Use Industry

- 20.7. Algeria Health Data Interoperability Platforms Market

- 20.7.1. Country Segmental Analysis

- 20.7.2. Component

- 20.7.3. Interoperability Level

- 20.7.4. Deployment Mode

- 20.7.5. Data Type

- 20.7.6. Standard Type

- 20.7.7. Integration Type

- 20.7.8. Functionality

- 20.7.9. Technology

- 20.7.10. End-Use Industry

- 20.8. Rest of Africa Health Data Interoperability Platforms Market

- 20.8.1. Country Segmental Analysis

- 20.8.2. Component

- 20.8.3. Interoperability Level

- 20.8.4. Deployment Mode

- 20.8.5. Data Type

- 20.8.6. Standard Type

- 20.8.7. Integration Type

- 20.8.8. Functionality

- 20.8.9. Technology

- 20.8.10. End-Use Industry

- 21. South America Health Data Interoperability Platforms Market Analysis

- 21.1. Key Segment Analysis

- 21.2. Regional Snapshot

- 21.3. Central and South Africa Health Data Interoperability Platforms Market Size (Value - US$ Bn), Analysis, and Forecasts, 2021-2035

- 21.3.1. Component

- 21.3.2. Interoperability Level

- 21.3.3. Deployment Mode

- 21.3.4. Data Type

- 21.3.5. Standard Type

- 21.3.6. Integration Type

- 21.3.7. Functionality

- 21.3.8. Technology

- 21.3.9. End-Use Industry

- 21.3.10. Country

- 21.3.10.1. Brazil

- 21.3.10.2. Argentina

- 21.3.10.3. Rest of South America

- 21.4. Brazil Health Data Interoperability Platforms Market

- 21.4.1. Country Segmental Analysis

- 21.4.2. Component

- 21.4.3. Interoperability Level

- 21.4.4. Deployment Mode

- 21.4.5. Data Type

- 21.4.6. Standard Type

- 21.4.7. Integration Type

- 21.4.8. Functionality

- 21.4.9. Technology

- 21.4.10. End-Use Industry

- 21.5. Argentina Health Data Interoperability Platforms Market

- 21.5.1. Country Segmental Analysis

- 21.5.2. Component

- 21.5.3. Interoperability Level

- 21.5.4. Deployment Mode

- 21.5.5. Data Type

- 21.5.6. Standard Type

- 21.5.7. Integration Type

- 21.5.8. Functionality

- 21.5.9. Technology

- 21.5.10. End-Use Industry

- 21.6. Rest of South America Health Data Interoperability Platforms Market

- 21.6.1. Country Segmental Analysis

- 21.6.2. Component

- 21.6.3. Interoperability Level

- 21.6.4. Deployment Mode

- 21.6.5. Data Type

- 21.6.6. Standard Type

- 21.6.7. Integration Type

- 21.6.8. Functionality

- 21.6.9. Technology

- 21.6.10. End-Use Industry

- 22. Key Players/ Company Profile

- 22.1. Allscripts Healthcare Solutions

- 22.1.1. Company Details/ Overview

- 22.1.2. Company Financials

- 22.1.3. Key Customers and Competitors

- 22.1.4. Business/ Industry Portfolio

- 22.1.5. Product Portfolio/ Specification Details

- 22.1.6. Pricing Data

- 22.1.7. Strategic Overview

- 22.1.8. Recent Developments

- 22.2. athenahealth Inc.

- 22.3. Cerner Corporation (Oracle Health)

- 22.4. Conduent Inc.

- 22.5. Corepoint Health

- 22.6. Epic Systems Corporation

- 22.7. Infor (Cloverleaf Integration Suite)

- 22.8. Informatica

- 22.9. InterSystems Corporation

- 22.10. Jitterbit

- 22.11. Koninklijke Philips N.V.

- 22.12. Meditech

- 22.13. Mirth Corporation

- 22.14. NextGen Healthcare

- 22.15. Optum Inc. (UnitedHealth Group)

- 22.16. Orion Health

- 22.17. OSP Labs

- 22.18. Rhapsody (Lyniate)

- 22.19. Summit Healthcare

- 22.20. ViSolve Inc.

- 22.21. Other Key Players

- 22.1. Allscripts Healthcare Solutions

Note* - This is just tentative list of players. While providing the report, we will cover more number of players based on their revenue and share for each geography

Research Design

Our research design integrates both demand-side and supply-side analysis through a balanced combination of primary and secondary research methodologies. By utilizing both bottom-up and top-down approaches alongside rigorous data triangulation methods, we deliver robust market intelligence that supports strategic decision-making.

MarketGenics' comprehensive research design framework ensures the delivery of accurate, reliable, and actionable market intelligence. Through the integration of multiple research approaches, rigorous validation processes, and expert analysis, we provide our clients with the insights needed to make informed strategic decisions and capitalize on market opportunities.

MarketGenics leverages a dedicated industry panel of experts and a comprehensive suite of paid databases to effectively collect, consolidate, and analyze market intelligence.

Our approach has consistently proven to be reliable and effective in generating accurate market insights, identifying key industry trends, and uncovering emerging business opportunities.

Through both primary and secondary research, we capture and analyze critical company-level data such as manufacturing footprints, including technical centers, R&D facilities, sales offices, and headquarters.

Our expert panel further enhances our ability to estimate market size for specific brands based on validated field-level intelligence.

Our data mining techniques incorporate both parametric and non-parametric methods, allowing for structured data collection, sorting, processing, and cleaning.

Demand projections are derived from large-scale data sets analyzed through proprietary algorithms, culminating in robust and reliable market sizing.

Research Approach

The bottom-up approach builds market estimates by starting with the smallest addressable market units and systematically aggregating them to create comprehensive market size projections.

This method begins with specific, granular data points and builds upward to create the complete market landscape.

Customer Analysis → Segmental Analysis → Geographical Analysis

The top-down approach starts with the broadest possible market data and systematically narrows it down through a series of filters and assumptions to arrive at specific market segments or opportunities.

This method begins with the big picture and works downward to increasingly specific market slices.

TAM → SAM → SOM

Research Methods

Desk / Secondary Research

While analysing the market, we extensively study secondary sources, directories, and databases to identify and collect information useful for this technical, market-oriented, and commercial report. Secondary sources that we utilize are not only the public sources, but it is a combination of Open Source, Associations, Paid Databases, MG Repository & Knowledgebase, and others.

- Company websites, annual reports, financial reports, broker reports, and investor presentations

- National government documents, statistical databases and reports

- News articles, press releases and web-casts specific to the companies operating in the market, Magazines, reports, and others

- We gather information from commercial data sources for deriving company specific data such as segmental revenue, share for geography, product revenue, and others

- Internal and external proprietary databases (industry-specific), relevant patent, and regulatory databases

- Governing Bodies, Government Organizations

- Relevant Authorities, Country-specific Associations for Industries

We also employ the model mapping approach to estimate the product level market data through the players' product portfolio

Primary Research

Primary research/ interviews is vital in analyzing the market. Most of the cases involves paid primary interviews. Primary sources include primary interviews through e-mail interactions, telephonic interviews, surveys as well as face-to-face interviews with the different stakeholders across the value chain including several industry experts.

| Type of Respondents | Number of Primaries |

|---|---|

| Tier 2/3 Suppliers | ~20 |

| Tier 1 Suppliers | ~25 |

| End-users | ~25 |

| Industry Expert/ Panel/ Consultant | ~30 |

| Total | ~100 |

MG Knowledgebase

• Repository of industry blog, newsletter and case studies

• Online platform covering detailed market reports, and company profiles

Forecasting Factors and Models

Forecasting Factors

- Historical Trends – Past market patterns, cycles, and major events that shaped how markets behave over time. Understanding past trends helps predict future behavior.

- Industry Factors – Specific characteristics of the industry like structure, regulations, and innovation cycles that affect market dynamics.

- Macroeconomic Factors – Economic conditions like GDP growth, inflation, and employment rates that affect how much money people have to spend.

- Demographic Factors – Population characteristics like age, income, and location that determine who can buy your product.

- Technology Factors – How quickly people adopt new technology and how much technology infrastructure exists.

- Regulatory Factors – Government rules, laws, and policies that can help or restrict market growth.

- Competitive Factors – Analyzing competition structure such as degree of competition and bargaining power of buyers and suppliers.

Forecasting Models / Techniques

Multiple Regression Analysis

- Identify and quantify factors that drive market changes

- Statistical modeling to establish relationships between market drivers and outcomes

Time Series Analysis – Seasonal Patterns

- Understand regular cyclical patterns in market demand

- Advanced statistical techniques to separate trend, seasonal, and irregular components

Time Series Analysis – Trend Analysis

- Identify underlying market growth patterns and momentum

- Statistical analysis of historical data to project future trends

Expert Opinion – Expert Interviews

- Gather deep industry insights and contextual understanding

- In-depth interviews with key industry stakeholders

Multi-Scenario Development

- Prepare for uncertainty by modeling different possible futures

- Creating optimistic, pessimistic, and most likely scenarios

Time Series Analysis – Moving Averages

- Sophisticated forecasting for complex time series data

- Auto-regressive integrated moving average models with seasonal components

Econometric Models

- Apply economic theory to market forecasting

- Sophisticated economic models that account for market interactions

Expert Opinion – Delphi Method

- Harness collective wisdom of industry experts

- Structured, multi-round expert consultation process

Monte Carlo Simulation

- Quantify uncertainty and probability distributions

- Thousands of simulations with varying input parameters

Research Analysis

Our research framework is built upon the fundamental principle of validating market intelligence from both demand and supply perspectives. This dual-sided approach ensures comprehensive market understanding and reduces the risk of single-source bias.

Demand-Side Analysis: We understand end-user/application behavior, preferences, and market needs along with the penetration of the product for specific application.

Supply-Side Analysis: We estimate overall market revenue, analyze the segmental share along with industry capacity, competitive landscape, and market structure.

Validation & Evaluation

Data triangulation is a validation technique that uses multiple methods, sources, or perspectives to examine the same research question, thereby increasing the credibility and reliability of research findings. In market research, triangulation serves as a quality assurance mechanism that helps identify and minimize bias, validate assumptions, and ensure accuracy in market estimates.

- Data Source Triangulation – Using multiple data sources to examine the same phenomenon

- Methodological Triangulation – Using multiple research methods to study the same research question

- Investigator Triangulation – Using multiple researchers or analysts to examine the same data

- Theoretical Triangulation – Using multiple theoretical perspectives to interpret the same data

Custom Market Research Services

We will customise the research for you, in case the report listed above does not meet your requirements.

Get 10% Free Customisation