Decentralized Identity (DID) Solutions Market Size, Share & Trends Analysis Report by Component (Wallets, Verifiable Credential Issuers, Verifier Platforms, DID Method & Registry Services, Identity Orchestration & Broker Services, Analytics & Monitoring, Integration Middleware & Connectors and Others), Deployment Mode, Solution Type, Technology/ Protocol, Functionality/ Feature, Organization Size, Application/ Use Case, Industry Vertical and Geography (North America, Europe, Asia Pacific, Middle East, Africa, and South America) – Global Industry Data, Trends, and Forecasts, 2026–2035

|

Market Structure & Evolution |

|

|

Segmental Data Insights |

|

|

Demand Trends |

|

|

Competitive Landscape |

|

|

Strategic Development |

|

|

Future Outlook & Opportunities |

|

Decentralized Identity (DID) Solutions Market Size, Share, and Growth

The global decentralized identity (DID) solutions market is experiencing robust growth, with its estimated value of USD 0.5 billion in the year 2025 and USD 155.6 billion by the period 2035, registering a CAGR of 77.1% during the forecast period. The decentralized identity (DID) solutions market worldwide is expanding rapidly.

Drummond Reed, who serves as the Chief Trust Officer at Gen Digital, and was an active contributor to the W3C DID standards, stated that decentralized identity is becoming a foundation of digital trust, due to the lack of centralized data stores that can be breached. According to Reed, user-controlled identifiers and verifiable credentials enable trust using cryptography and a basis for zero-trust architectures, leading governments and enterprises to adopt W3C-standard DIDs.

The global growth of this decentralized identity (DID) solutions market is mainly caused by factors that converge, among which are: the increased demand for privacy-preserving identity frameworks, regulatory pressures, and security needs for user-controlled authentication. In response to the demand for decentralized identity solutions, the major players in the market have upgraded their offerings and have developed sophisticated systems, for instance, Microsoft's Entra Verified ID, which allows organizations to issue verifiable credentials and, thus, reduce identity fraud risk.

Governments are implementing digital ID programs that depend on W3C-compliant DIDs, whereas companies are adopting verifiable credentials to facilitate secure onboarding, passwordless authentication, and cross-border compliance. The trend towards zero-trust security models, the rise of AI-driven identity fraud, and synthetic identities are some factors that have led to the skyrocketing of demand for DID solutions.

Since organizations view identity as the basic security layer, decentralized identity is turning out to be the key infrastructure element of the next digital ecosystems. Moreover, regulatory contexts lead to the adoption of such technologies. Privacy data laws like GDPR and digital trust frameworks are the main factors behind the encouragement of identity architectures that empower the individual with data control rights. The adoption of standardized models like W3C DIDs and verifiable credentials lead to sector integration, thus being the main driver behind enterprise deployment.

Additionally, the decentralized identity (DID) solutions market has some promising potential areas in which the adjacent markets can be of interest. These markets can include such things as verifiable-credential wallets, zero-knowledge proof systems, decentralized access management platforms, identity governance tools, secure digital wallets, and digital public infrastructure projects. Providers in these adjacent markets can widen their product portfolios while security and privacy benefits can be extended across the broader digital identity landscape.

Decentralized Identity (DID) Solutions Market Dynamics and Trends

Driver: Global Shift Toward Privacy-Preserving Identity Models

- The fast global acceptance of privacy laws like GDPR, the California Consumer Privacy Act (CCPA), and different data-sovereignty regulations in the APAC and Latin America regions, is the main reason for the rapid growth in demand for decentralized identity architectures. These rules focus more than ever on aspects such as data minimization, user consent, and giving control of personal data to the user, which are in full agreement with the core ideas of W3C Decentralized Identifiers (DIDs) and Verifiable Credentials.

- Attributed to which, governments and large businesses are changing over to privacy-by-design identity schemes that do not depend heavily on big centralized databases which have been the most attractive targets for hackers.

- Simultaneously, the increasing costs of fake credentials and identity breaches is the major factor that is causing enterprises to opt for decentralized and cryptographically verifiable identity systems that are less likely to expose their customers' personally identifiable information (PII).

Restraint: Limited Interoperability Across Decentralized Identity Networks

- While W3C DIDs and Verifiable Credentials establish guidelines, there are still differences in real-world implementations across blockchain networks, wallet providers, and trust registries resulting in a lack of consistent interoperability which impedes adoption, particularly among enterprises with interests in supporting a multi-network strategy,

- Many enterprises still rely on centralized identity providers (IdPs) and SSO infrastructure that is SAML or OAuth based, which complicates and consumes resources to plan and execute the migration from centralized to DIDs outside a siloed IdP that may or may not support a more decentralized architectural scheme in blockchain. Moving to DID systems may also involve the need to rework the identity flow, develop new APIs, and possibly retool the legacy IT ecosystem.

- There are other compliance challenges that act as hurdles. A recent assessment in the industry has noted that organizations deploying any DID solutions continue with compliance related issues extending to decentralized identifiers, particularly if attempting to break down or cross a siloed approach or trust layer (Chain) to their business model.

Opportunity: Government Digital Identity Programs Accelerating DID Deployment

- Various governments are testing or implementing decentralized identity structures. The new European Digital Identity (EUDI) Wallet of the European Union is incorporating support ideas aligned with verifiable credentials for cross-border trust services.

- Canada’s Digital ID & Authentication Council (DIACC) initiative, the SingPass enhancements in Singapore, and the Trusted Digital Identity Framework (TDIF) in Australia are gradually leading to the use of verifiable credentials and decentralized trust models.

- Public–private partnerships in sectors such as aviation, travel, and education (e.g., digital travel credentials, digital driver’s licenses, and university credential programs) therefore offer great potential for DID vendors to combine wallet, verifiable ID modules, and trust registries functionalities.

Key Trend: Growth of Wallet-Based Identity and Cross-Platform Verifiable Credentials

- Major technology companies such as Apple, Google, and Microsoft, are embedding support for digital ID wallets and verifiable credentials in operating systems, mobile wallets, and enterprise clouds, thus facilitating the widespread use of decentralized identity. The transition to passwordless authentication and the use of FIDO2 are in harmony with DID solutions, thus allowing for stronger authentication while at the same time the possibilities of phishing are greatly lowered.

- Collaboration between different industries is going on more and more through such groups as Decentralized Identity Foundation (DIF), Trust over IP Foundation (ToIP), and W3C Working Groups, thereby facilitating the implementation of interoperability profiles and governance frameworks.

- Multi-factor digital identity that combines device-binding, biometrics, and verifiable credentials is being heralded as the predominant model for those enterprises that want to obtain identity confirmation to a very high degree while at the same time drastically reducing the risk of data exposure.

Decentralized Identity Solutions Market Analysis and Segmental Data

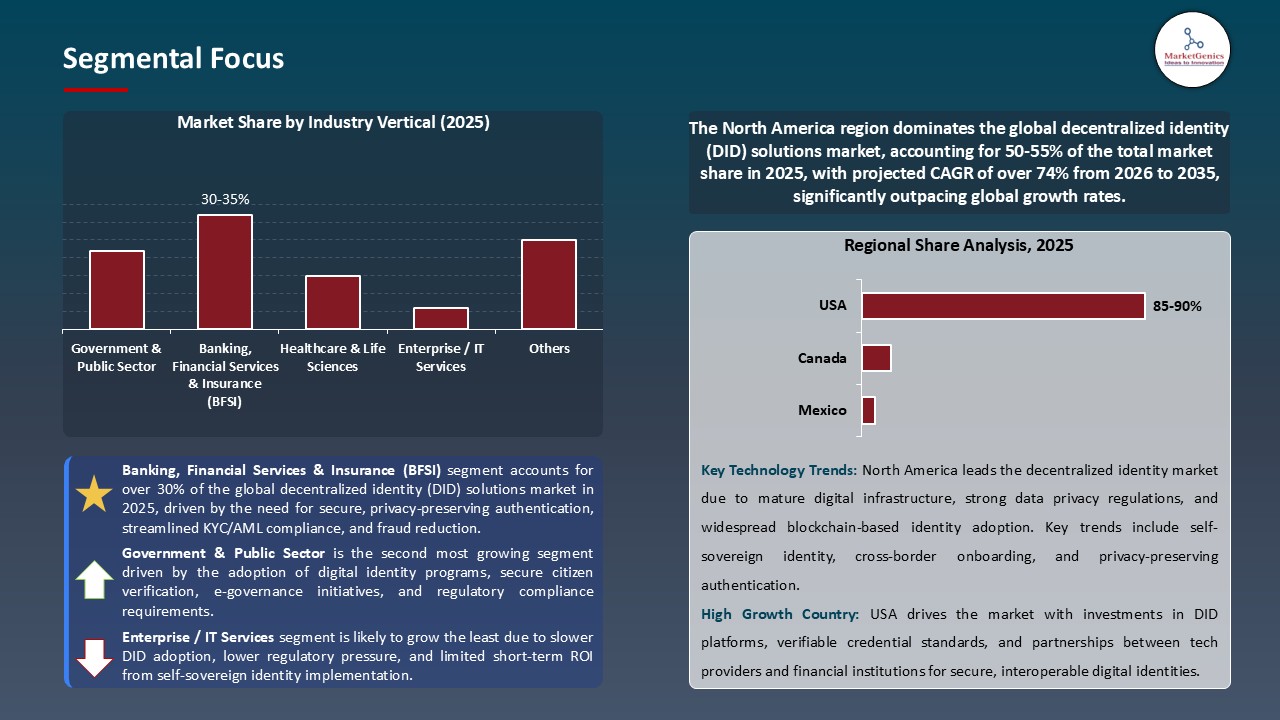

“Banking, Financial Services & Insurance (BFSI) Lead Global Decentralized Identity (DID) Solutions Market amid Rising Regulatory Pressures and Fraud Mitigation Needs"

- The Banking, Financial Services & Insurance (BFSI) sector is the major contributor to the global decentralized identity (DID) solutions market. This is primarily because of its significant exposure to regulatory scrutiny and an increase in the risk of identity fraud.

- Moreover, financial institutions are required to adhere to very strict KYC, AML, and data-protecting mandates, which is the main reason behind the adoption of privacy-preserving and verifiable identity frameworks. DID allows for secure, user-managed credentials that lower the risk of reliant on centralized databases that are vulnerable and make cross-border compliance less complicated.

- The escalation in instances of synthetic identities, account takeovers, and deepfake-driven fraud has been a strong factor in banks and insurers deciding to move toward tamper-resistant, cryptographically verifiable identity models. Besides that, the fast digitalization of payments, lending, insurance onboarding, and fintech ecosystems is what makes decentralized identity a must-have if the industry wants to build trust, lower operational costs, and increase security in digital financial services.

“North America Leads Decentralized Identity (DID) Solutions Market Advanced Regulatory Frameworks and High Adoption of Digital Identity Standards"

- Decentralized identity (DID) solutions market is mainly propelled by United States of America and Canada which is evident in its progressive regulatory scenario, robust digital identity standards, and quick enterprise use of privacy-preserving authentication models.

- Both the U.S. and Canada laid out the digital-identity structures first, an example is the NIST SP 800-63-4 Digital Identity Guidelines update release in 2024, which spotlights phishing-resistant authentication, verifiable credentials, and data exposure minimization. These frameworks compel banks, healthcare providers, and government agencies to update their identity systems and decentralize their architectures.

- The area is also the base of big tech providers who are the trendsetters in the DIDs integration into enterprise workflows, thus speeding real-world implementation. A most recent example is the 2024 expansion of Microsoft Entra’s Verified ID services across U.S. public-sector agencies, facilitating issuance of verifiable credentials for workforce access and contractor verification. Together with firm cybersecurity requirements and zero-trust strategies, these changes make North America a leader in DID deployment and innovation.

Decentralized-Identity-Solutions-Market Ecosystem

The decentralized identity (DID) solutions market is progressively consolidating where the major players like Microsoft Corporation, IBM Corporation, Ping Identity, Accenture, 1Kosmos, Trinsic, and Affinidi leverage their innovations in advanced cryptographic identity technologies, verifiable credential platforms, and secure wallet infrastructures to fortify their positions.

Further, by introducing niche, high-assurance identity tools such as enterprise credential-issuance systems, decentralized identity wallets, trust registry services, and portable digital credential management platforms that foster interoperability and security, these companies are accelerating the market maturity.

Authorities, standard-setting bodies, and R&D organizations are not left behind in this race as they contribute significantly to the ecosystem's evolution. In February 2024, Microsoft broadened its Verified ID Face Check feature - a privacy-preserving biometric verification enhancement - with an AI-driven liveness detection that identifies the source of the face, thus mitigating spoofing risks and elevating the level of credential assurance in the public sector access systems. This move emphasized how important it is for regulated environments to have cryptographically verifiable, user-controlled identities.

The major players are still committed to expanding their portfolio by incorporating decentralized identifiers, biometrics, and zero-trust identity orchestration into single solutions that not only enhance operational efficiency but also lessen the chances of fraud. By the same token, the June 2023 European Digital Identity (EUDI) Wallet reference implementation, which is loaded with features that allow European citizens to move across borders using their digital IDs, has demonstrated measurable improvements in cross-border credential interoperability thus, leaving no hurdles for decentralized identity standards to be deployed at scale in government and enterprise ecosystems.

Recent Development and Strategic Overview:

- In September 2025, Trinsic, Inc. launched its Trusted Identity Cloud 2.0, a cloud-based platform leveraging decentralized identifiers (DIDs) to issue zero-knowledge-proof (ZKP) credentials. This enables individuals to demonstrate they have certain identity characteristics (i.e., age, employment) without sharing the sensitive identity data behind those attributes, increasing privacy while also enabling organizations in banking and healthcare to undertake ability-based identity verification processes.

- In July 2025, 1Kosmos Inc. introduced its BlockID Wallet Suite, a mobile-first self-sovereign identity (SSI) solution that provides interoperable, verifiable credentials across Ethereum-based chains and Hyperledger Indy networks. By allowing the user to immediately present their credentials with cryptographic proof directly from their wallet.

Report Scope

|

Attribute |

Detail |

|

Market Size in 2025 |

USD 0.5 Bn |

|

Market Forecast Value in 2035 |

USD 155.6 Bn |

|

Growth Rate (CAGR) |

77.1% |

|

Forecast Period |

2026 – 2035 |

|

Historical Data Available for |

2021 – 2024 |

|

Market Size Units |

USD Bn for Value |

|

Report Format |

Electronic (PDF) + Excel |

|

Regions and Countries Covered |

|||||

|

North America |

Europe |

Asia Pacific |

Middle East |

Africa |

South America |

|

|

|

|

|

|

|

Companies Covered |

|||||

|

|

|

|

|

|

Decentralized-Identity-Solutions-Market Segmentation and Highlights

|

Segment |

Sub-segment |

|

Decentralized Identity (DID) Solutions Market, By Component |

|

|

Decentralized Identity (DID) Solutions Market, By Deployment Mode |

|

|

Decentralized Identity (DID) Solutions Market, By Solution Type |

|

|

Decentralized Identity (DID) Solutions Market, By Technology/ Protocol |

|

|

Decentralized Identity (DID) Solutions Market, By Functionality/ Feature |

|

|

Decentralized Identity (DID) Solutions Market, By Organization Size |

|

|

Decentralized Identity (DID) Solutions Market, By Application/ Use Case |

|

|

Decentralized Identity (DID) Solutions Market, By Industry Vertical |

|

Frequently Asked Questions

Table of Contents

- 1. Research Methodology and Assumptions

- 1.1. Definitions

- 1.2. Research Design and Approach

- 1.3. Data Collection Methods

- 1.4. Base Estimates and Calculations

- 1.5. Forecasting Models

- 1.5.1. Key Forecast Factors & Impact Analysis

- 1.6. Secondary Research

- 1.6.1. Open Sources

- 1.6.2. Paid Databases

- 1.6.3. Associations

- 1.7. Primary Research

- 1.7.1. Primary Sources

- 1.7.2. Primary Interviews with Stakeholders across Ecosystem

- 2. Executive Summary

- 2.1. Global Decentralized Identity (DID) Solutions Market Outlook

- 2.1.1. Decentralized Identity (DID) Solutions Market Size (Value - US$ Bn), and Forecasts, 2021-2035

- 2.1.2. Compounded Annual Growth Rate Analysis

- 2.1.3. Growth Opportunity Analysis

- 2.1.4. Segmental Share Analysis

- 2.1.5. Geographical Share Analysis

- 2.2. Market Analysis and Facts

- 2.3. Supply-Demand Analysis

- 2.4. Competitive Benchmarking

- 2.5. Go-to- Market Strategy

- 2.5.1. Customer/ End-use Industry Assessment

- 2.5.2. Growth Opportunity Data, 2026-2035

- 2.5.2.1. Regional Data

- 2.5.2.2. Country Data

- 2.5.2.3. Segmental Data

- 2.5.3. Identification of Potential Market Spaces

- 2.5.4. GAP Analysis

- 2.5.5. Potential Attractive Price Points

- 2.5.6. Prevailing Market Risks & Challenges

- 2.5.7. Preferred Sales & Marketing Strategies

- 2.5.8. Key Recommendations and Analysis

- 2.5.9. A Way Forward

- 2.1. Global Decentralized Identity (DID) Solutions Market Outlook

- 3. Industry Data and Premium Insights

- 3.1. Global Information Technology & Media Ecosystem Overview, 2025

- 3.1.1. Information Technology & Media Industry Analysis

- 3.1.2. Key Trends for Information Technology & Media Industry

- 3.1.3. Regional Distribution for Information Technology & Media Industry

- 3.2. Supplier Customer Data

- 3.3. Technology Roadmap and Developments

- 3.1. Global Information Technology & Media Ecosystem Overview, 2025

- 4. Market Overview

- 4.1. Market Dynamics

- 4.1.1. Drivers

- 4.1.1.1. Rising need for secure, privacy-preserving digital identities in banking, healthcare, and government

- 4.1.1.2. Growing adoption of self-sovereign identity (SSI) platforms and verifiable credential frameworks

- 4.1.1.3. Increasing regulatory focus on digital identity verification, KYC/AML compliance, and data privacy

- 4.1.2. Restraints

- 4.1.2.1. High integration costs with legacy identity management systems

- 4.1.2.2. Interoperability challenges across multiple platforms and standards

- 4.1.1. Drivers

- 4.2. Key Trend Analysis

- 4.3. Regulatory Framework

- 4.3.1. Key Regulations, Norms, and Subsidies, by Key Countries

- 4.3.2. Tariffs and Standards

- 4.3.3. Impact Analysis of Regulations on the Market

- 4.4. Value Chain Analysis

- 4.4.1. Identity Credential Creation Providers

- 4.4.2. System Integrators

- 4.4.3. DID Solution Providers

- 4.4.4. End Users

- 4.5. Cost Structure Analysis

- 4.5.1. Parameter’s Share for Cost Associated

- 4.5.2. COGP vs COGS

- 4.5.3. Profit Margin Analysis

- 4.6. Pricing Analysis

- 4.6.1. Regional Pricing Analysis

- 4.6.2. Segmental Pricing Trends

- 4.6.3. Factors Influencing Pricing

- 4.7. Porter’s Five Forces Analysis

- 4.8. PESTEL Analysis

- 4.9. Global Decentralized Identity (DID) Solutions Market Demand

- 4.9.1. Historical Market Size –Value (US$ Bn), 2020-2024

- 4.9.2. Current and Future Market Size –Value (US$ Bn), 2026–2035

- 4.9.2.1. Y-o-Y Growth Trends

- 4.9.2.2. Absolute $ Opportunity Assessment

- 4.1. Market Dynamics

- 5. Competition Landscape

- 5.1. Competition structure

- 5.1.1. Fragmented v/s consolidated

- 5.2. Company Share Analysis, 2025

- 5.2.1. Global Company Market Share

- 5.2.2. By Region

- 5.2.2.1. North America

- 5.2.2.2. Europe

- 5.2.2.3. Asia Pacific

- 5.2.2.4. Middle East

- 5.2.2.5. Africa

- 5.2.2.6. South America

- 5.3. Product Comparison Matrix

- 5.3.1. Specifications

- 5.3.2. Market Positioning

- 5.3.3. Pricing

- 5.1. Competition structure

- 6. Global Decentralized Identity (DID) Solutions Market Analysis, by Component

- 6.1. Key Segment Analysis

- 6.2. Decentralized Identity (DID) Solutions Market Size (Value - US$ Bn), Analysis, and Forecasts, by Component, 2021-2035

- 6.2.1. Wallets

- 6.2.2. Verifiable Credential Issuers

- 6.2.3. Verifier Platforms

- 6.2.4. DID Method & Registry Services

- 6.2.5. Identity Orchestration & Broker Services

- 6.2.6. Analytics & Monitoring

- 6.2.7. Integration Middleware & Connectors

- 6.2.8. Others

- 7. Global Decentralized Identity (DID) Solutions Market Analysis, by Deployment Mode

- 7.1. Key Segment Analysis

- 7.2. Decentralized Identity (DID) Solutions Market Size (Value - US$ Bn), Analysis, and Forecasts, by Deployment Mode, 2021-2035

- 7.2.1. Cloud-Based

- 7.2.2. On-Premises

- 7.2.3. Hybrid

- 8. Global Decentralized Identity (DID) Solutions Market Analysis, by Solution Type

- 8.1. Key Segment Analysis

- 8.2. Decentralized Identity (DID) Solutions Market Size (Value - US$ Bn), Analysis, and Forecasts, by Solution Type, 2021-2035

- 8.2.1. Self-Sovereign Identity (SSI) Solutions

- 8.2.2. Federated Decentralized Identity Solutions

- 8.2.3. Hybrid (SSI + Enterprise IAM integration)

- 9. Global Decentralized Identity (DID) Solutions Market Analysis, by Technology/ Protocol

- 9.1. Key Segment Analysis

- 9.2. Decentralized Identity (DID) Solutions Market Size (Value - US$ Bn), Analysis, and Forecasts, by Technology/ Protocol, 2021-2035

- 9.2.1. DID methods

- 9.2.2. Verifiable Credentials (W3C VC) implementations

- 9.2.3. Decentralized Identifiers on Distributed Ledgers

- 9.2.4. Off-chain storage + on-chain anchoring

- 9.2.5. Cryptographic primitives

- 9.2.6. Others

- 10. Global Decentralized Identity (DID) Solutions Market Analysis, by Functionality/ Feature

- 10.1. Key Segment Analysis

- 10.2. Decentralized Identity (DID) Solutions Market Size (Value - US$ Bn), Analysis, and Forecasts, by Functionality/ Feature, 2021-2035

- 10.2.1. Credential issuance & lifecycle management

- 10.2.2. Presentation & selective disclosure (ZK/paired proofs)

- 10.2.3. Consent & privacy controls

- 10.2.4. Recovery & key management / social recovery

- 10.2.5. Credential revocation & status lists

- 10.2.6. Auditability & provenance tracking

- 10.2.7. Others

- 11. Global Decentralized Identity (DID) Solutions Market Analysis, by Organization Size

- 11.1. Key Segment Analysis

- 11.2. Decentralized Identity (DID) Solutions Market Size (Value - US$ Bn), Analysis, and Forecasts, by Organization Size, 2021-2035

- 11.2.1. Large enterprises

- 11.2.2. Small & Medium-sized Enterprises (SMEs)

- 11.2.3. Individual users / consumers (verification apps)

- 12. Global Decentralized Identity (DID) Solutions Market Analysis, by Application/ Use Case

- 12.1. Key Segment Analysis

- 12.2. Decentralized Identity (DID) Solutions Market Size (Value - US$ Bn), Analysis, and Forecasts, by Application/ Use Case, 2021-2035

- 12.2.1. Consumer identity (wallets, KYC-lite)

- 12.2.2. Workforce / Employee identity & access (enterprise SSO)

- 12.2.3. Government eID / citizen services

- 12.2.4. Education (digital diplomas, credentials)

- 12.2.5. Health (medical credentials, consent)

- 12.2.6. Travel & Hospitality (digital travel credentials)

- 12.2.7. Finance & Banking (KYC, transaction signing)

- 12.2.8. IoT device identity (device DIDs)

- 12.2.9. Others

- 13. Global Decentralized Identity (DID) Solutions Market Analysis, by Industry Vertical

- 13.1. Key Segment Analysis

- 13.2. Decentralized Identity (DID) Solutions Market Size (Value - US$ Bn), Analysis, and Forecasts, by Industry Vertical, 2021-2035

- 13.2.1. Government & Public Sector

- 13.2.2. Banking, Financial Services & Insurance (BFSI)

- 13.2.3. Healthcare & Life Sciences

- 13.2.4. Education

- 13.2.5. Telecommunications

- 13.2.6. Media & Entertainment

- 13.2.7. Retail & eCommerce

- 13.2.8. Travel & Transportation

- 13.2.9. Enterprise / IT Services

- 13.2.10. Others

- 14. Global Decentralized Identity (DID) Solutions Market Analysis and Forecasts, by Region

- 14.1. Key Findings

- 14.2. Decentralized Identity (DID) Solutions Market Size (Value - US$ Bn), Analysis, and Forecasts, by Region, 2021-2035

- 14.2.1. North America

- 14.2.2. Europe

- 14.2.3. Asia Pacific

- 14.2.4. Middle East

- 14.2.5. Africa

- 14.2.6. South America

- 15. North America Decentralized Identity (DID) Solutions Market Analysis

- 15.1. Key Segment Analysis

- 15.2. Regional Snapshot

- 15.3. North America Decentralized Identity (DID) Solutions Market Size Value - US$ Bn), Analysis, and Forecasts, 2021-2035

- 15.3.1. Component

- 15.3.2. Deployment Mode

- 15.3.3. Solution Type

- 15.3.4. Technology/ Protocol

- 15.3.5. Functionality/ Feature

- 15.3.6. Organization Size

- 15.3.7. Application / Use Case

- 15.3.8. Industry Vertical

- 15.3.9. Country

- 15.3.9.1. USA

- 15.3.9.2. Canada

- 15.3.9.3. Mexico

- 15.4. USA Decentralized Identity (DID) Solutions Market

- 15.4.1. Country Segmental Analysis

- 15.4.2. Component

- 15.4.3. Deployment Mode

- 15.4.4. Solution Type

- 15.4.5. Technology/ Protocol

- 15.4.6. Functionality/ Feature

- 15.4.7. Organization Size

- 15.4.8. Application / Use Case

- 15.4.9. Industry Vertical

- 15.5. Canada Decentralized Identity (DID) Solutions Market

- 15.5.1. Country Segmental Analysis

- 15.5.2. Component

- 15.5.3. Deployment Mode

- 15.5.4. Solution Type

- 15.5.5. Technology/ Protocol

- 15.5.6. Functionality/ Feature

- 15.5.7. Organization Size

- 15.5.8. Application / Use Case

- 15.5.9. Industry Vertical

- 15.6. Mexico Decentralized Identity (DID) Solutions Market

- 15.6.1. Country Segmental Analysis

- 15.6.2. Component

- 15.6.3. Deployment Mode

- 15.6.4. Solution Type

- 15.6.5. Technology/ Protocol

- 15.6.6. Functionality/ Feature

- 15.6.7. Organization Size

- 15.6.8. Application / Use Case

- 15.6.9. Industry Vertical

- 16. Europe Decentralized Identity (DID) Solutions Market Analysis

- 16.1. Key Segment Analysis

- 16.2. Regional Snapshot

- 16.3. Europe Decentralized Identity (DID) Solutions Market Size (Value - US$ Bn), Analysis, and Forecasts, 2021-2035

- 16.3.1. Component

- 16.3.2. Deployment Mode

- 16.3.3. Solution Type

- 16.3.4. Technology/ Protocol

- 16.3.5. Functionality/ Feature

- 16.3.6. Organization Size

- 16.3.7. Application / Use Case

- 16.3.8. Industry Vertical

- 16.3.9. Country

- 16.3.9.1. Germany

- 16.3.9.2. United Kingdom

- 16.3.9.3. France

- 16.3.9.4. Italy

- 16.3.9.5. Spain

- 16.3.9.6. Netherlands

- 16.3.9.7. Nordic Countries

- 16.3.9.8. Poland

- 16.3.9.9. Russia & CIS

- 16.3.9.10. Rest of Europe

- 16.4. Germany Decentralized Identity (DID) Solutions Market

- 16.4.1. Country Segmental Analysis

- 16.4.2. Component

- 16.4.3. Deployment Mode

- 16.4.4. Solution Type

- 16.4.5. Technology/ Protocol

- 16.4.6. Functionality/ Feature

- 16.4.7. Organization Size

- 16.4.8. Application / Use Case

- 16.4.9. Industry Vertical

- 16.5. United Kingdom Decentralized Identity (DID) Solutions Market

- 16.5.1. Country Segmental Analysis

- 16.5.2. Component

- 16.5.3. Deployment Mode

- 16.5.4. Solution Type

- 16.5.5. Technology/ Protocol

- 16.5.6. Functionality/ Feature

- 16.5.7. Organization Size

- 16.5.8. Application / Use Case

- 16.5.9. Industry Vertical

- 16.6. France Decentralized Identity (DID) Solutions Market

- 16.6.1. Country Segmental Analysis

- 16.6.2. Component

- 16.6.3. Deployment Mode

- 16.6.4. Solution Type

- 16.6.5. Technology/ Protocol

- 16.6.6. Functionality/ Feature

- 16.6.7. Organization Size

- 16.6.8. Application / Use Case

- 16.6.9. Industry Vertical

- 16.7. Italy Decentralized Identity (DID) Solutions Market

- 16.7.1. Country Segmental Analysis

- 16.7.2. Component

- 16.7.3. Deployment Mode

- 16.7.4. Solution Type

- 16.7.5. Technology/ Protocol

- 16.7.6. Functionality/ Feature

- 16.7.7. Organization Size

- 16.7.8. Application / Use Case

- 16.7.9. Industry Vertical

- 16.8. Spain Decentralized Identity (DID) Solutions Market

- 16.8.1. Country Segmental Analysis

- 16.8.2. Component

- 16.8.3. Deployment Mode

- 16.8.4. Solution Type

- 16.8.5. Technology/ Protocol

- 16.8.6. Functionality/ Feature

- 16.8.7. Organization Size

- 16.8.8. Application / Use Case

- 16.8.9. Industry Vertical

- 16.9. Netherlands Decentralized Identity (DID) Solutions Market

- 16.9.1. Country Segmental Analysis

- 16.9.2. Component

- 16.9.3. Deployment Mode

- 16.9.4. Solution Type

- 16.9.5. Technology/ Protocol

- 16.9.6. Functionality/ Feature

- 16.9.7. Organization Size

- 16.9.8. Application / Use Case

- 16.9.9. Industry Vertical

- 16.10. Nordic Countries Decentralized Identity (DID) Solutions Market

- 16.10.1. Country Segmental Analysis

- 16.10.2. Component

- 16.10.3. Deployment Mode

- 16.10.4. Solution Type

- 16.10.5. Technology/ Protocol

- 16.10.6. Functionality/ Feature

- 16.10.7. Organization Size

- 16.10.8. Application / Use Case

- 16.10.9. Industry Vertical

- 16.11. Poland Decentralized Identity (DID) Solutions Market

- 16.11.1. Country Segmental Analysis

- 16.11.2. Component

- 16.11.3. Deployment Mode

- 16.11.4. Solution Type

- 16.11.5. Technology/ Protocol

- 16.11.6. Functionality/ Feature

- 16.11.7. Organization Size

- 16.11.8. Application / Use Case

- 16.11.9. Industry Vertical

- 16.12. Russia & CIS Decentralized Identity (DID) Solutions Market

- 16.12.1. Country Segmental Analysis

- 16.12.2. Component

- 16.12.3. Deployment Mode

- 16.12.4. Solution Type

- 16.12.5. Technology/ Protocol

- 16.12.6. Functionality/ Feature

- 16.12.7. Organization Size

- 16.12.8. Application / Use Case

- 16.12.9. Industry Vertical

- 16.13. Rest of Europe Decentralized Identity (DID) Solutions Market

- 16.13.1. Country Segmental Analysis

- 16.13.2. Component

- 16.13.3. Deployment Mode

- 16.13.4. Solution Type

- 16.13.5. Technology/ Protocol

- 16.13.6. Functionality/ Feature

- 16.13.7. Organization Size

- 16.13.8. Application / Use Case

- 16.13.9. Industry Vertical

- 17. Asia Pacific Decentralized Identity (DID) Solutions Market Analysis

- 17.1. Key Segment Analysis

- 17.2. Regional Snapshot

- 17.3. Asia Pacific Decentralized Identity (DID) Solutions Market Size (Value - US$ Bn), Analysis, and Forecasts, 2021-2035

- 17.3.1. Component

- 17.3.2. Deployment Mode

- 17.3.3. Solution Type

- 17.3.4. Technology/ Protocol

- 17.3.5. Functionality/ Feature

- 17.3.6. Organization Size

- 17.3.7. Application / Use Case

- 17.3.8. Industry Vertical

- 17.3.9. Country

- 17.3.9.1. China

- 17.3.9.2. India

- 17.3.9.3. Japan

- 17.3.9.4. South Korea

- 17.3.9.5. Australia and New Zealand

- 17.3.9.6. Indonesia

- 17.3.9.7. Malaysia

- 17.3.9.8. Thailand

- 17.3.9.9. Vietnam

- 17.3.9.10. Rest of Asia Pacific

- 17.4. China Decentralized Identity (DID) Solutions Market

- 17.4.1. Country Segmental Analysis

- 17.4.2. Component

- 17.4.3. Deployment Mode

- 17.4.4. Solution Type

- 17.4.5. Technology/ Protocol

- 17.4.6. Functionality/ Feature

- 17.4.7. Organization Size

- 17.4.8. Application / Use Case

- 17.4.9. Industry Vertical

- 17.5. India Decentralized Identity (DID) Solutions Market

- 17.5.1. Country Segmental Analysis

- 17.5.2. Component

- 17.5.3. Deployment Mode

- 17.5.4. Solution Type

- 17.5.5. Technology/ Protocol

- 17.5.6. Functionality/ Feature

- 17.5.7. Organization Size

- 17.5.8. Application / Use Case

- 17.5.9. Industry Vertical

- 17.6. Japan Decentralized Identity (DID) Solutions Market

- 17.6.1. Country Segmental Analysis

- 17.6.2. Component

- 17.6.3. Deployment Mode

- 17.6.4. Solution Type

- 17.6.5. Technology/ Protocol

- 17.6.6. Functionality/ Feature

- 17.6.7. Organization Size

- 17.6.8. Application / Use Case

- 17.6.9. Industry Vertical

- 17.7. South Korea Decentralized Identity (DID) Solutions Market

- 17.7.1. Country Segmental Analysis

- 17.7.2. Component

- 17.7.3. Deployment Mode

- 17.7.4. Solution Type

- 17.7.5. Technology/ Protocol

- 17.7.6. Functionality/ Feature

- 17.7.7. Organization Size

- 17.7.8. Application / Use Case

- 17.7.9. Industry Vertical

- 17.8. Australia and New Zealand Decentralized Identity (DID) Solutions Market

- 17.8.1. Country Segmental Analysis

- 17.8.2. Component

- 17.8.3. Deployment Mode

- 17.8.4. Solution Type

- 17.8.5. Technology/ Protocol

- 17.8.6. Functionality/ Feature

- 17.8.7. Organization Size

- 17.8.8. Application / Use Case

- 17.8.9. Industry Vertical

- 17.9. Indonesia Decentralized Identity (DID) Solutions Market

- 17.9.1. Country Segmental Analysis

- 17.9.2. Component

- 17.9.3. Deployment Mode

- 17.9.4. Solution Type

- 17.9.5. Technology/ Protocol

- 17.9.6. Functionality/ Feature

- 17.9.7. Organization Size

- 17.9.8. Application / Use Case

- 17.9.9. Industry Vertical

- 17.10. Malaysia Decentralized Identity (DID) Solutions Market

- 17.10.1. Country Segmental Analysis

- 17.10.2. Component

- 17.10.3. Deployment Mode

- 17.10.4. Solution Type

- 17.10.5. Technology/ Protocol

- 17.10.6. Functionality/ Feature

- 17.10.7. Organization Size

- 17.10.8. Application / Use Case

- 17.10.9. Industry Vertical

- 17.11. Thailand Decentralized Identity (DID) Solutions Market

- 17.11.1. Country Segmental Analysis

- 17.11.2. Component

- 17.11.3. Deployment Mode

- 17.11.4. Solution Type

- 17.11.5. Technology/ Protocol

- 17.11.6. Functionality/ Feature

- 17.11.7. Organization Size

- 17.11.8. Application / Use Case

- 17.11.9. Industry Vertical

- 17.12. Vietnam Decentralized Identity (DID) Solutions Market

- 17.12.1. Country Segmental Analysis

- 17.12.2. Component

- 17.12.3. Deployment Mode

- 17.12.4. Solution Type

- 17.12.5. Technology/ Protocol

- 17.12.6. Functionality/ Feature

- 17.12.7. Organization Size

- 17.12.8. Application / Use Case

- 17.12.9. Industry Vertical

- 17.13. Rest of Asia Pacific Decentralized Identity (DID) Solutions Market

- 17.13.1. Country Segmental Analysis

- 17.13.2. Component

- 17.13.3. Deployment Mode

- 17.13.4. Solution Type

- 17.13.5. Technology/ Protocol

- 17.13.6. Functionality/ Feature

- 17.13.7. Organization Size

- 17.13.8. Application / Use Case

- 17.13.9. Industry Vertical

- 18. Middle East Decentralized Identity (DID) Solutions Market Analysis

- 18.1. Key Segment Analysis

- 18.2. Regional Snapshot

- 18.3. Middle East Decentralized Identity (DID) Solutions Market Size (Value - US$ Bn), Analysis, and Forecasts, 2021-2035

- 18.3.1. Component

- 18.3.2. Deployment Mode

- 18.3.3. Solution Type

- 18.3.4. Technology/ Protocol

- 18.3.5. Functionality/ Feature

- 18.3.6. Organization Size

- 18.3.7. Application / Use Case

- 18.3.8. Industry Vertical

- 18.3.9. Country

- 18.3.9.1. Turkey

- 18.3.9.2. UAE

- 18.3.9.3. Saudi Arabia

- 18.3.9.4. Israel

- 18.3.9.5. Rest of Middle East

- 18.4. Turkey Decentralized Identity (DID) Solutions Market

- 18.4.1. Country Segmental Analysis

- 18.4.2. Component

- 18.4.3. Deployment Mode

- 18.4.4. Solution Type

- 18.4.5. Technology/ Protocol

- 18.4.6. Functionality/ Feature

- 18.4.7. Organization Size

- 18.4.8. Application / Use Case

- 18.4.9. Industry Vertical

- 18.5. UAE Decentralized Identity (DID) Solutions Market

- 18.5.1. Country Segmental Analysis

- 18.5.2. Component

- 18.5.3. Deployment Mode

- 18.5.4. Solution Type

- 18.5.5. Technology/ Protocol

- 18.5.6. Functionality/ Feature

- 18.5.7. Organization Size

- 18.5.8. Application / Use Case

- 18.5.9. Industry Vertical

- 18.6. Saudi Arabia Decentralized Identity (DID) Solutions Market

- 18.6.1. Country Segmental Analysis

- 18.6.2. Component

- 18.6.3. Deployment Mode

- 18.6.4. Solution Type

- 18.6.5. Technology/ Protocol

- 18.6.6. Functionality/ Feature

- 18.6.7. Organization Size

- 18.6.8. Application / Use Case

- 18.6.9. Industry Vertical

- 18.7. Israel Decentralized Identity (DID) Solutions Market

- 18.7.1. Country Segmental Analysis

- 18.7.2. Component

- 18.7.3. Deployment Mode

- 18.7.4. Solution Type

- 18.7.5. Technology/ Protocol

- 18.7.6. Functionality/ Feature

- 18.7.7. Organization Size

- 18.7.8. Application / Use Case

- 18.7.9. Industry Vertical

- 18.8. Rest of Middle East Decentralized Identity (DID) Solutions Market

- 18.8.1. Country Segmental Analysis

- 18.8.2. Component

- 18.8.3. Deployment Mode

- 18.8.4. Solution Type

- 18.8.5. Technology/ Protocol

- 18.8.6. Functionality/ Feature

- 18.8.7. Organization Size

- 18.8.8. Application / Use Case

- 18.8.9. Industry Vertical

- 19. Africa Decentralized Identity (DID) Solutions Market Analysis

- 19.1. Key Segment Analysis

- 19.2. Regional Snapshot

- 19.3. Africa Decentralized Identity (DID) Solutions Market Size (Value - US$ Bn), Analysis, and Forecasts, 2021-2035

- 19.3.1. Component

- 19.3.2. Deployment Mode

- 19.3.3. Solution Type

- 19.3.4. Technology/ Protocol

- 19.3.5. Functionality/ Feature

- 19.3.6. Organization Size

- 19.3.7. Application / Use Case

- 19.3.8. Industry Vertical

- 19.3.9. Country

- 19.3.9.1. South Africa

- 19.3.9.2. Egypt

- 19.3.9.3. Nigeria

- 19.3.9.4. Algeria

- 19.3.9.5. Rest of Africa

- 19.4. South Africa Decentralized Identity (DID) Solutions Market

- 19.4.1. Country Segmental Analysis

- 19.4.2. Component

- 19.4.3. Deployment Mode

- 19.4.4. Solution Type

- 19.4.5. Technology/ Protocol

- 19.4.6. Functionality/ Feature

- 19.4.7. Organization Size

- 19.4.8. Application / Use Case

- 19.4.9. Industry Vertical

- 19.5. Egypt Decentralized Identity (DID) Solutions Market

- 19.5.1. Country Segmental Analysis

- 19.5.2. Component

- 19.5.3. Deployment Mode

- 19.5.4. Solution Type

- 19.5.5. Technology/ Protocol

- 19.5.6. Functionality/ Feature

- 19.5.7. Organization Size

- 19.5.8. Application / Use Case

- 19.5.9. Industry Vertical

- 19.6. Nigeria Decentralized Identity (DID) Solutions Market

- 19.6.1. Country Segmental Analysis

- 19.6.2. Component

- 19.6.3. Deployment Mode

- 19.6.4. Solution Type

- 19.6.5. Technology/ Protocol

- 19.6.6. Functionality/ Feature

- 19.6.7. Organization Size

- 19.6.8. Application / Use Case

- 19.6.9. Industry Vertical

- 19.7. Algeria Decentralized Identity (DID) Solutions Market

- 19.7.1. Country Segmental Analysis

- 19.7.2. Component

- 19.7.3. Deployment Mode

- 19.7.4. Solution Type

- 19.7.5. Technology/ Protocol

- 19.7.6. Functionality/ Feature

- 19.7.7. Organization Size

- 19.7.8. Application / Use Case

- 19.7.9. Industry Vertical

- 19.8. Rest of Africa Decentralized Identity (DID) Solutions Market

- 19.8.1. Country Segmental Analysis

- 19.8.2. Component

- 19.8.3. Deployment Mode

- 19.8.4. Solution Type

- 19.8.5. Technology/ Protocol

- 19.8.6. Functionality/ Feature

- 19.8.7. Organization Size

- 19.8.8. Application / Use Case

- 19.8.9. Industry Vertical

- 20. South America Decentralized Identity (DID) Solutions Market Analysis

- 20.1. Key Segment Analysis

- 20.2. Regional Snapshot

- 20.3. South America Decentralized Identity (DID) Solutions Market Size (Value - US$ Bn), Analysis, and Forecasts, 2021-2035

- 20.3.1. Component

- 20.3.2. Deployment Mode

- 20.3.3. Solution Type

- 20.3.4. Technology/ Protocol

- 20.3.5. Functionality/ Feature

- 20.3.6. Organization Size

- 20.3.7. Application / Use Case

- 20.3.8. Industry Vertical

- 20.3.9. Country

- 20.3.9.1. Brazil

- 20.3.9.2. Argentina

- 20.3.9.3. Rest of South America

- 20.4. Brazil Decentralized Identity (DID) Solutions Market

- 20.4.1. Country Segmental Analysis

- 20.4.2. Component

- 20.4.3. Deployment Mode

- 20.4.4. Solution Type

- 20.4.5. Technology/ Protocol

- 20.4.6. Functionality/ Feature

- 20.4.7. Organization Size

- 20.4.8. Application / Use Case

- 20.4.9. Industry Vertical

- 20.5. Argentina Decentralized Identity (DID) Solutions Market

- 20.5.1. Country Segmental Analysis

- 20.5.2. Component

- 20.5.3. Deployment Mode

- 20.5.4. Solution Type

- 20.5.5. Technology/ Protocol

- 20.5.6. Functionality/ Feature

- 20.5.7. Organization Size

- 20.5.8. Application / Use Case

- 20.5.9. Industry Vertical

- 20.6. Rest of South America Decentralized Identity (DID) Solutions Market

- 20.6.1. Country Segmental Analysis

- 20.6.2. Component

- 20.6.3. Deployment Mode

- 20.6.4. Solution Type

- 20.6.5. Technology/ Protocol

- 20.6.6. Functionality/ Feature

- 20.6.7. Organization Size

- 20.6.8. Application / Use Case

- 20.6.9. Industry Vertical

- 21. Key Players/ Company Profile

- 21.1. 1Kosmos Inc.

- 21.1.1. Company Details/ Overview

- 21.1.2. Company Financials

- 21.1.3. Key Customers and Competitors

- 21.1.4. Business/ Industry Portfolio

- 21.1.5. Product Portfolio/ Specification Details

- 21.1.6. Pricing Data

- 21.1.7. Strategic Overview

- 21.1.8. Recent Developments

- 21.2. Accenture plc

- 21.3. Affinidi Ltd.

- 21.4. Blockstack PBC

- 21.5. Bloom Protocol

- 21.6. Civic Technologies, Inc.

- 21.7. Evernym, Inc.

- 21.8. IBM Corporation

- 21.9. Jolocom GmbH

- 21.10. Microsoft Corporation

- 21.11. Ping Identity Corporation

- 21.12. R3 LLC

- 21.13. SecureKey Technologies Inc.

- 21.14. SelfKey Foundation

- 21.15. ShoCard, Inc.

- 21.16. Sovrin Foundation

- 21.17. Transmute Industries (Transmute)

- 21.18. Trinsic, Inc.

- 21.19. uPort (ConsenSys)

- 21.20. Veres One Foundation

- 21.21. Others Key Players

- 21.1. 1Kosmos Inc.

Note* - This is just tentative list of players. While providing the report, we will cover more number of players based on their revenue and share for each geography

Research Design

Our research design integrates both demand-side and supply-side analysis through a balanced combination of primary and secondary research methodologies. By utilizing both bottom-up and top-down approaches alongside rigorous data triangulation methods, we deliver robust market intelligence that supports strategic decision-making.

MarketGenics' comprehensive research design framework ensures the delivery of accurate, reliable, and actionable market intelligence. Through the integration of multiple research approaches, rigorous validation processes, and expert analysis, we provide our clients with the insights needed to make informed strategic decisions and capitalize on market opportunities.

MarketGenics leverages a dedicated industry panel of experts and a comprehensive suite of paid databases to effectively collect, consolidate, and analyze market intelligence.

Our approach has consistently proven to be reliable and effective in generating accurate market insights, identifying key industry trends, and uncovering emerging business opportunities.

Through both primary and secondary research, we capture and analyze critical company-level data such as manufacturing footprints, including technical centers, R&D facilities, sales offices, and headquarters.

Our expert panel further enhances our ability to estimate market size for specific brands based on validated field-level intelligence.

Our data mining techniques incorporate both parametric and non-parametric methods, allowing for structured data collection, sorting, processing, and cleaning.

Demand projections are derived from large-scale data sets analyzed through proprietary algorithms, culminating in robust and reliable market sizing.

Research Approach

The bottom-up approach builds market estimates by starting with the smallest addressable market units and systematically aggregating them to create comprehensive market size projections.

This method begins with specific, granular data points and builds upward to create the complete market landscape.

Customer Analysis → Segmental Analysis → Geographical Analysis

The top-down approach starts with the broadest possible market data and systematically narrows it down through a series of filters and assumptions to arrive at specific market segments or opportunities.

This method begins with the big picture and works downward to increasingly specific market slices.

TAM → SAM → SOM

Research Methods

Desk / Secondary Research

While analysing the market, we extensively study secondary sources, directories, and databases to identify and collect information useful for this technical, market-oriented, and commercial report. Secondary sources that we utilize are not only the public sources, but it is a combination of Open Source, Associations, Paid Databases, MG Repository & Knowledgebase, and others.

- Company websites, annual reports, financial reports, broker reports, and investor presentations

- National government documents, statistical databases and reports

- News articles, press releases and web-casts specific to the companies operating in the market, Magazines, reports, and others

- We gather information from commercial data sources for deriving company specific data such as segmental revenue, share for geography, product revenue, and others

- Internal and external proprietary databases (industry-specific), relevant patent, and regulatory databases

- Governing Bodies, Government Organizations

- Relevant Authorities, Country-specific Associations for Industries

We also employ the model mapping approach to estimate the product level market data through the players' product portfolio

Primary Research

Primary research/ interviews is vital in analyzing the market. Most of the cases involves paid primary interviews. Primary sources include primary interviews through e-mail interactions, telephonic interviews, surveys as well as face-to-face interviews with the different stakeholders across the value chain including several industry experts.

| Type of Respondents | Number of Primaries |

|---|---|

| Tier 2/3 Suppliers | ~20 |

| Tier 1 Suppliers | ~25 |

| End-users | ~25 |

| Industry Expert/ Panel/ Consultant | ~30 |

| Total | ~100 |

MG Knowledgebase

• Repository of industry blog, newsletter and case studies

• Online platform covering detailed market reports, and company profiles

Forecasting Factors and Models

Forecasting Factors

- Historical Trends – Past market patterns, cycles, and major events that shaped how markets behave over time. Understanding past trends helps predict future behavior.

- Industry Factors – Specific characteristics of the industry like structure, regulations, and innovation cycles that affect market dynamics.

- Macroeconomic Factors – Economic conditions like GDP growth, inflation, and employment rates that affect how much money people have to spend.

- Demographic Factors – Population characteristics like age, income, and location that determine who can buy your product.

- Technology Factors – How quickly people adopt new technology and how much technology infrastructure exists.

- Regulatory Factors – Government rules, laws, and policies that can help or restrict market growth.

- Competitive Factors – Analyzing competition structure such as degree of competition and bargaining power of buyers and suppliers.

Forecasting Models / Techniques

Multiple Regression Analysis

- Identify and quantify factors that drive market changes

- Statistical modeling to establish relationships between market drivers and outcomes

Time Series Analysis – Seasonal Patterns

- Understand regular cyclical patterns in market demand

- Advanced statistical techniques to separate trend, seasonal, and irregular components

Time Series Analysis – Trend Analysis

- Identify underlying market growth patterns and momentum

- Statistical analysis of historical data to project future trends

Expert Opinion – Expert Interviews

- Gather deep industry insights and contextual understanding

- In-depth interviews with key industry stakeholders

Multi-Scenario Development

- Prepare for uncertainty by modeling different possible futures

- Creating optimistic, pessimistic, and most likely scenarios

Time Series Analysis – Moving Averages

- Sophisticated forecasting for complex time series data

- Auto-regressive integrated moving average models with seasonal components

Econometric Models

- Apply economic theory to market forecasting

- Sophisticated economic models that account for market interactions

Expert Opinion – Delphi Method

- Harness collective wisdom of industry experts

- Structured, multi-round expert consultation process

Monte Carlo Simulation

- Quantify uncertainty and probability distributions

- Thousands of simulations with varying input parameters

Research Analysis

Our research framework is built upon the fundamental principle of validating market intelligence from both demand and supply perspectives. This dual-sided approach ensures comprehensive market understanding and reduces the risk of single-source bias.

Demand-Side Analysis: We understand end-user/application behavior, preferences, and market needs along with the penetration of the product for specific application.

Supply-Side Analysis: We estimate overall market revenue, analyze the segmental share along with industry capacity, competitive landscape, and market structure.

Validation & Evaluation

Data triangulation is a validation technique that uses multiple methods, sources, or perspectives to examine the same research question, thereby increasing the credibility and reliability of research findings. In market research, triangulation serves as a quality assurance mechanism that helps identify and minimize bias, validate assumptions, and ensure accuracy in market estimates.

- Data Source Triangulation – Using multiple data sources to examine the same phenomenon

- Methodological Triangulation – Using multiple research methods to study the same research question

- Investigator Triangulation – Using multiple researchers or analysts to examine the same data

- Theoretical Triangulation – Using multiple theoretical perspectives to interpret the same data

Custom Market Research Services

We will customise the research for you, in case the report listed above does not meet your requirements.

Get 10% Free Customisation