Generative AI Market Size, Share & Trends Analysis Report by Component (Solutions and Services), Deployment Type, Technology, Model Type, Enterprise Size, Function, Application, Industry Vertical and Geography (North America, Europe, Asia Pacific, Middle East, Africa, and South America) – Global Industry Data, Trends, and Forecasts, 2026–2035

Market Overview:

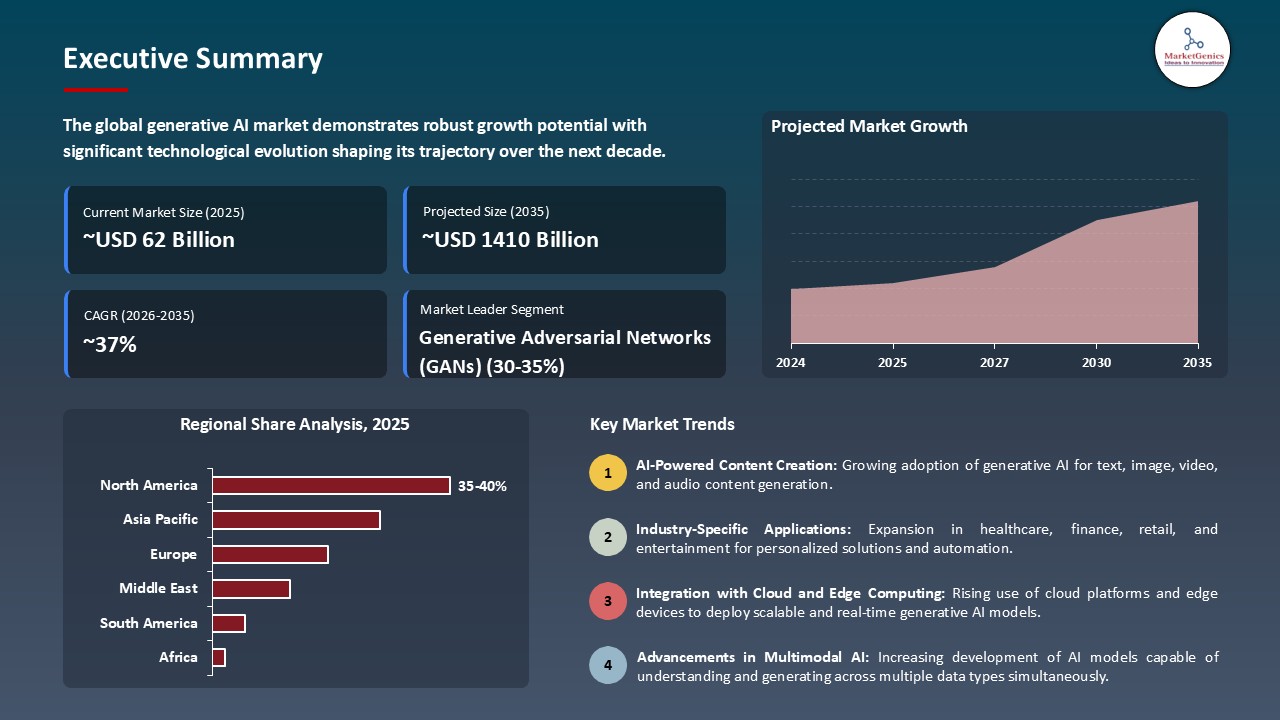

According to MarketGenics analysis, the global generative AI market is experiencing robust growth, with its estimated value of approximately USD 62.3 billion in 2025 projected to reach around USD 1,410.3 billion by 2035, registering a CAGR of 36.6% during the forecast period

|

Market Structure & Evolution |

|

|

Segmental Data Insights |

|

|

Demand Trends |

|

|

Competitive Landscape |

|

|

Strategic Development |

|

|

Future Outlook & Opportunities |

|

Generative AI Market Size, Share, and Growth

Google CEO Sundar Pichai stated that "generative AI is not just about creation—it's about transformation." While highlighting the necessity of responsible and transparent AI to maintain trust and authenticity in the digital age, he pointed out that generative models are transforming innovation across industries.

The generative AI market is growing quickly across the globe in part because leading technology companies are consistently developing new technology that is transforming how we create content, code, and digital assets. In April 2025, OpenAI released GPT-4.1, an enhanced multimodal large language model that can process up to one million tokens of information, which allows for entirely new levels of context handling for complex tasks involved in long-form content generation and software development, as well as data analysis.

Increasing demand for AI-driven creativity, automation, and productivity across industries, including media, gaming, and enterprise solutions, is increasing global adoption. Additionally, in January 2025, NVIDIA expanded its Omniverse platform, introducing new generative physical AI capabilities through its integration of simulation and robotics models for real-time industrial design and digital twin applications, which showcases how AI and 3D computing are coming together.

Increasing enterprise investment into responsible AI development, alongside ethical frameworks and copyright compliance development, is also driving the market's maturity.

Adjacent opportunities (for example, synthetic data generation AI, AI infrastructure optimization development, and creative automation AI tools) are creating opportunities across the generative AI ecosystem for companies to advance transparency, scalability, and innovation in global generative AI market.

Generative AI Market Dynamics and Trends

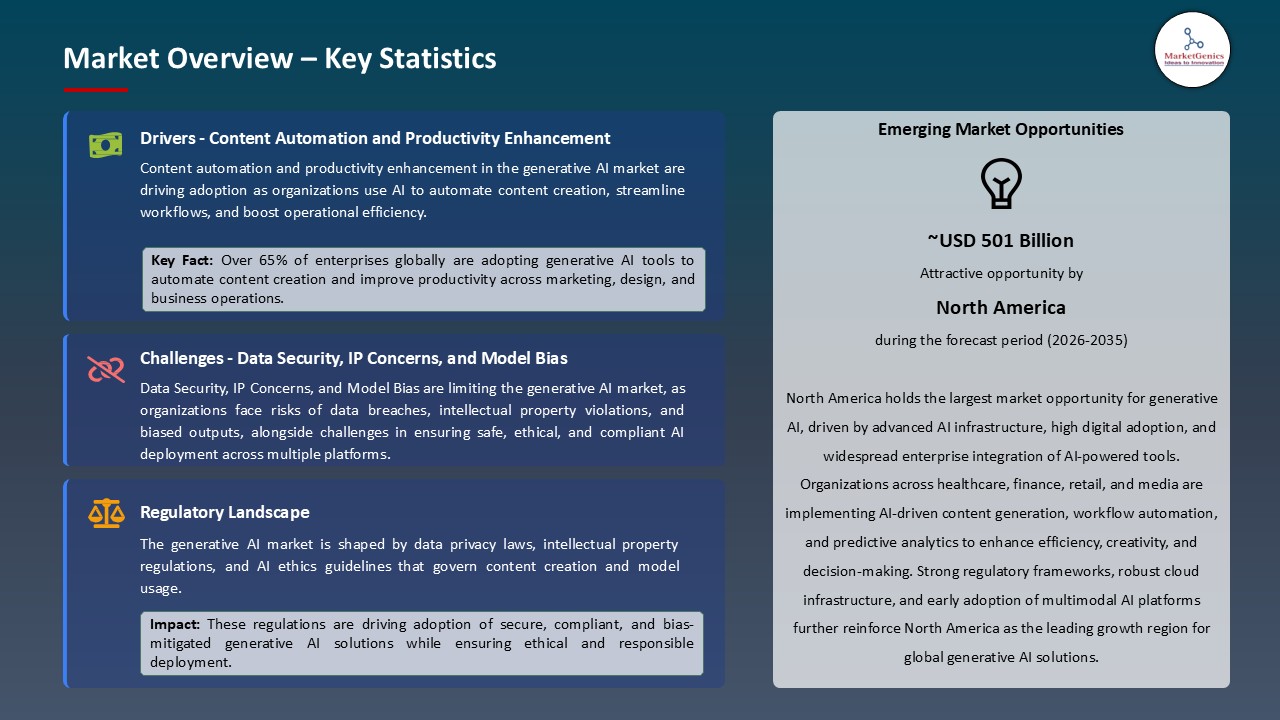

Driver: Growing Enterprise Demand for Content Automation and Productivity Enhancement

- The global generative AI market is experiencing swift growth as companies use AI models for task automation, tailored content generation, and overall productivity enhancement. For example, well-known generative AI innovators like OpenAI, Google, Microsoft, and Anthropic have added generative AI into enterprise tools-Michral Copilot, Google Workspace Duet AI, and Anthropic's Claude 3 models-to facilitate activity in real-time document creation, writing code, and managing workflows.

- Interest in combined text, image, and video generation is encouraging the uptake of such models in media, healthcare, and software engineering. In April 2025, for example, Addiscoll Stagners launched GPT-4.1 for enterprise applications, which provided improved reasoning, long-context understanding, and multimodal capabilities.

- Companies are utilizing generative AI to alleviate manual workloads and enhance innovative activity, with Gartner sources reporting in 2025 that over 80% of organizations plan to incorporate generative AI into operations by 2026, which appears to signal the way to operational efficiency through AI.

Restraint: Data Security, IP Concerns, and Model Bias Hindering Widespread Enterprise Deployment

- Even though the technology is being adopted quickly, data privacy, copyright compliance, and bias are still challenges to large-scale generative AI deployment. Companies are unclear about ownership of intellectual property when it comes to content provided by AI - especially with lawsuits by authors, artists, and code repositories in the U.S. (2024-2025) that have challenged the use of copyrighted material to train AI models.

- The European Union AI Act (with enforcement likely coming in 2026) is expected to impose stricter standards for transparency and accountability, including requirements to provide datasets, protect user data, and ensure fair AI outputs. Owing to which these regulations, compliance costs will increase and adoption will take longer - especially for small and medium-sized businesses.

- Hallucinatory content, misinformation tending to arise from generative AI, and data leakage - particularly for regulated industries like finance and health care - continues to inhibit enterprise-scale adoption of generative AI because of governance and model explainability requirements.

Opportunity: Expansion in Sector-Specific and Regulated Industry Applications

- Generative AI is being customized for safe, domain-specific use in sectors that offer large growth opportunities: healthcare, education, finance, and defense. In July 2025, for example, Google DeepMind presented AlphaFold 3. This was significant, as it applied protein structure-prediction to biomolecules of high complexity and in drug discovery contexts.

- In financial services, internal generative AI tools are being developed by firms such as JP Morgan and Goldman Sachs for document summaries, risk analysis, and compliance automation, which is indicative of greater enterprise investment in private AI infrastructure.

- Governments at all levels - national and regional - are also backing the responsible adoption of generative AI. In 2025, for instance, both the US Department of Commerce and Singapore's AI Verify Foundation will provide funding for the research and development of responsible generative AI policies and certification mechanisms for model reliability and transparency.

Key Trend: Integration of Multimodal AI, Synthetic Data, and Responsible AI Frameworks

- The generative AI ecosystem is advancing quickly towards multimodal systems that merge text, audio, video, and 3D generation, powered by innovations from NVIDIA’s Omniverse, Meta’s Emu Video, and Runway Gen-3 Alpha. These tools enable large-scale content creation, simulation, and digital twin modeling.

- The emergent world of synthetic data generation is changing how we train models to allow enterprises to create high-quality datasets continuity of privacy violations. In September 2023, IBM included synthetic data generation, on its watsonx.data platform, to increase model fairness and accuracy.

- Meanwhile, the increasing focus on responsible AI and transparency, exemplified by frameworks like the AI Alliance (an IBM and Meta initiative launched July 2023), increases demand for humanly auditable, ethical, and explainable generative AI systems, so markets can grow sustainably.

Generative AI Market Analysis and Segmental Data

“Generative Adversarial Networks (GANs) Dominates Global Generative AI Market amid Rising Demand for Realistic Content Generation and Synthetic Data Creation"

- Generative Adversarial Networks (GANs) have rapidly become widely adopted in sectors like media, gaming, retail, and autonomous systems for applications ranging from photorealistic image creation, deepfake implementation, and simulation data creation. For example, NVIDIA's StyleGAN3, released in 2024, continues to underpin applications that leverage photorealistic images and lifelike high-resolution digital avatars in content and media creation.

- The widespread adoption of GAN-generated synthetic datasets is spurring even wider usage in areas around sectors like healthcare and autonomous driving, where privacy and limited data availability remain significant issues. Companies like Google DeepMind and IBM have pioneered GAN methodologies to augment medical imaging datasets and training datasets, while improving model accuracy without revealing sensitive information.

- Enterprises are also utilizing GANs in conjunction with large language and vision models, providing multimodal generative pipelines capable of image synthesis/text-to-image, virtual world simulation, etc. Integrating these methods also creates applications that support innovation in areas such as metaverse applications, advertising, and interactive entertainment.

- Furthermore, as adversarial training becomes faster and simpler to implement and redesign with open-source frameworks like TensorFlow-GAN and PyTorch’s TorchGAN, developers can build and deploy GANs faster than ever before-signifying its importance and future as a generative AI alternative research cornerstone.

“North America Leads Generative AI Market with Strong Enterprise Adoption and Technology Innovation"

- North America is the current leader in the generative AI market, owing to strong corporate buy-in, ongoing investments in R&D, and development of state-of-the-art technologies. In 2025, for example, companies like OpenAI, Microsoft, NVIDIA, and Google will be showcasing generative AI solutions across the spectrum of industries in North America, reinforcing its leadership in developing AI-generated content and automation through AI-based simulations.

- Cross-industrial collaboration has also been stimulating or propelling innovation, as enterprises, cloud service providers, and AI startups, for example, have collaborated to develop large-scale generative models, multimodal and vertical pipelines, and synthetic data solutions to provide organizations with increased efficiency, creativity, and scale.

- In Canada, the Pan-Canadian Artificial Intelligence Strategy, for example, will continue to enhance the overall research and development agenda by promoting responsible generative AI training, use, and research, with a focus on ethical use, bias mitigation, and privacy-preserving without losing sight of the value of U.S. leadership funding for research and the development of innovation in the generative AI field.

- Given the current adoption of generative AI across enterprises, the integration and embedding of GANs and large language models, and ongoing funding investments towards cloud-native and AI infrastructure or devices, North America is on a path to remain the global leader in generative AI market.

Generative-AI-Market Ecosystem

The global generative AI market is becoming more consolidated, dominated by several key players including OpenAI, Google LLC, Microsoft Corporation, NVIDIA Corporation, Adobe Inc. and Amazon Web Services, Inc., that are wasting no time in developing highly capable large-language models, multimodal AI, and cloud-scale infrastructure.

These companies highlight specific innovations: OpenAI provides APIs that enables high-fidelity text-to-image and coding solutions, NVIDIA supports generative 3D simulations through its Omniverse tool, and Google's Gemini models are focused on enterprise-specific generation of AI content. These tools specific to niches, are streamlining productivity, industrial, and creative applications.

Government and institutional support 'speed s up' growth. In July, 2025, U.S. federal government released its America’s AI Action Plan emphasizing investment and regulation to support the development of responsible generative AI, and strengthen enterprise adoption of its use, and its infrastructure.

Meanwhile there is now also an emphasis on product choice and integrated solutions from market leaders. Microsoft has embedded generative AI into its Copilot for Microsoft productivity suite; Adobe has generated features within its products for users to utilize generative AI into creative workflows and produces or can provide AWS/Azure secure frameworks to deploy AI enterprise wide.

Recent Development and Strategic Overview:

- In April 2025, Google / LLC launched its Lyria text‑to‑music model and announced updates to its Veo 2 video creation and Chirp 3 audio models on its Vertex AI platform so enterprises can now generate songs, videos, and voices all from text prompts, greatly enhancing multimodal content creation.

- In May 2025, IBM Corporation revealed its hybrid generative AI platform featuring watsonx.data and LinuxONE 5 architecture, which allowed enterprises to build AI agents with up to 176% ROI and increased model accuracy by about 40% based on early deployments.

Report Scope

|

Attribute |

Detail |

|

Market Size in 2025 |

USD 62.3 Bn |

|

Market Forecast Value in 2035 |

USD 1410.3 Bn |

|

Growth Rate (CAGR) |

36.6% |

|

Forecast Period |

2026 – 2035 |

|

Historical Data Available for |

2021 – 2024 |

|

Market Size Units |

USD Bn for Value |

|

Report Format |

Electronic (PDF) + Excel |

|

Regions and Countries Covered |

|||||

|

North America |

Europe |

Asia Pacific |

Middle East |

Africa |

South America |

|

|

|

|

|

|

|

Companies Covered |

|||||

|

|

|

|

|

|

Generative-AI-Market Segmentation and Highlights

|

Segment |

Sub-segment |

|

Generative AI Market, By Component |

|

|

Generative AI Market, By Deployment Mode |

|

|

Generative AI Market, By Technology |

|

|

Generative AI Market, By Model Type |

|

|

Generative AI Market, By Enterprise Size |

|

|

Generative AI Market, By Function |

|

|

Generative AI Market, By Application |

|

|

Generative AI Market, By Industry Vertical |

|

Frequently Asked Questions

Table of Contents

- 1. Research Methodology and Assumptions

- 1.1. Definitions

- 1.2. Research Design and Approach

- 1.3. Data Collection Methods

- 1.4. Base Estimates and Calculations

- 1.5. Forecasting Models

- 1.5.1. Key Forecast Factors & Impact Analysis

- 1.6. Secondary Research

- 1.6.1. Open Sources

- 1.6.2. Paid Databases

- 1.6.3. Associations

- 1.7. Primary Research

- 1.7.1. Primary Sources

- 1.7.2. Primary Interviews with Stakeholders across Ecosystem

- 2. Executive Summary

- 2.1. Global Generative AI Market Outlook

- 2.1.1. Generative AI Market Size (Value - US$ Bn), and Forecasts, 2021-2035

- 2.1.2. Compounded Annual Growth Rate Analysis

- 2.1.3. Growth Opportunity Analysis

- 2.1.4. Segmental Share Analysis

- 2.1.5. Geographical Share Analysis

- 2.2. Market Analysis and Facts

- 2.3. Supply-Demand Analysis

- 2.4. Competitive Benchmarking

- 2.5. Go-to- Market Strategy

- 2.5.1. Customer/ End-use Industry Assessment

- 2.5.2. Growth Opportunity Data, 2026-2035

- 2.5.2.1. Regional Data

- 2.5.2.2. Country Data

- 2.5.2.3. Segmental Data

- 2.5.3. Identification of Potential Market Spaces

- 2.5.4. GAP Analysis

- 2.5.5. Potential Attractive Price Points

- 2.5.6. Prevailing Market Risks & Challenges

- 2.5.7. Preferred Sales & Marketing Strategies

- 2.5.8. Key Recommendations and Analysis

- 2.5.9. A Way Forward

- 2.1. Global Generative AI Market Outlook

- 3. Industry Data and Premium Insights

- 3.1. Global Information Technology & Media Ecosystem Overview, 2025

- 3.1.1. Information Technology & Media Industry Analysis

- 3.1.2. Key Trends for Information Technology & Media Industry

- 3.1.3. Regional Distribution for Information Technology & Media Industry

- 3.2. Supplier Customer Data

- 3.3. Technology Roadmap and Developments

- 3.1. Global Information Technology & Media Ecosystem Overview, 2025

- 4. Market Overview

- 4.1. Market Dynamics

- 4.1.1. Drivers

- 4.1.1.1. Rising demand for AI-powered content creation and automation

- 4.1.1.2. Growing adoption of multimodal generative AI solutions across industries

- 4.1.1.3. Increasing regulatory focus on AI transparency, ethics, and data privacy compliance

- 4.1.2. Restraints

- 4.1.2.1. High development and deployment costs of advanced generative AI models

- 4.1.2.2. Integration challenges with legacy systems and existing enterprise workflows

- 4.1.1. Drivers

- 4.2. Key Trend Analysis

- 4.3. Regulatory Framework

- 4.3.1. Key Regulations, Norms, and Subsidies, by Key Countries

- 4.3.2. Tariffs and Standards

- 4.3.3. Impact Analysis of Regulations on the Market

- 4.4. Value Chain Analysis

- 4.4.1. Foundation Model Developers

- 4.4.2. System Integrators/ Technology Providers

- 4.4.3. Generative AI Solution Providers

- 4.4.4. End Users

- 4.5. Cost Structure Analysis

- 4.5.1. Parameter’s Share for Cost Associated

- 4.5.2. COGP vs COGS

- 4.5.3. Profit Margin Analysis

- 4.6. Pricing Analysis

- 4.6.1. Regional Pricing Analysis

- 4.6.2. Segmental Pricing Trends

- 4.6.3. Factors Influencing Pricing

- 4.7. Porter’s Five Forces Analysis

- 4.8. PESTEL Analysis

- 4.9. Global Generative AI Market Demand

- 4.9.1. Historical Market Size –Value (US$ Bn), 2020-2024

- 4.9.2. Current and Future Market Size –Value (US$ Bn), 2026–2035

- 4.9.2.1. Y-o-Y Growth Trends

- 4.9.2.2. Absolute $ Opportunity Assessment

- 4.1. Market Dynamics

- 5. Competition Landscape

- 5.1. Competition structure

- 5.1.1. Fragmented v/s consolidated

- 5.2. Company Share Analysis, 2025

- 5.2.1. Global Company Market Share

- 5.2.2. By Region

- 5.2.2.1. North America

- 5.2.2.2. Europe

- 5.2.2.3. Asia Pacific

- 5.2.2.4. Middle East

- 5.2.2.5. Africa

- 5.2.2.6. South America

- 5.3. Product Comparison Matrix

- 5.3.1. Specifications

- 5.3.2. Market Positioning

- 5.3.3. Pricing

- 5.1. Competition structure

- 6. Global Generative AI Market Analysis, by Component

- 6.1. Key Segment Analysis

- 6.2. Generative AI Market Size (Value - US$ Bn), Analysis, and Forecasts, by Component, 2021-2035

- 6.2.1. Solutions

- 6.2.1.1. Generative AI Platforms

- 6.2.1.2. Pre-trained Foundation Models

- 6.2.1.3. Custom Model Development Tools

- 6.2.1.4. Prompt Engineering and Fine-tuning Tools

- 6.2.1.5. Synthetic Data Generation Software

- 6.2.1.6. Content Creation and Automation Tools

- 6.2.1.7. AI Model Management and Monitoring Platforms

- 6.2.1.8. APIs and SDKs for Model Integration

- 6.2.1.9. Visualization and Simulation Tools

- 6.2.1.10. Others

- 6.2.2. Services

- 6.2.2.1. Consulting Services

- 6.2.2.1.1. AI Strategy and Roadmap Consulting

- 6.2.2.1.2. Model Selection and Customization Advisory

- 6.2.2.1.3. Regulatory and Ethical Compliance Consulting

- 6.2.2.1.4. Others

- 6.2.2.2. Integration & Deployment

- 6.2.2.2.1. End-to-End Model Implementation

- 6.2.2.2.2. Platform Integration with Existing Systems

- 6.2.2.2.3. Cloud and On-Premise Deployment Support

- 6.2.2.2.4. Others

- 6.2.2.3. Support & Maintenance

- 6.2.2.3.1. Model Optimization and Performance Tuning

- 6.2.2.3.2. Continuous Updates and Security Management

- 6.2.2.3.3. Technical Support and Troubleshooting

- 6.2.2.3.4. Others

- 6.2.2.1. Consulting Services

- 6.2.1. Solutions

- 7. Global Generative AI Market Analysis, by Deployment Mode

- 7.1. Key Segment Analysis

- 7.2. Generative AI Market Size (Value - US$ Bn), Analysis, and Forecasts, by Deployment Mode, 2021-2035

- 7.2.1. Cloud-Based

- 7.2.2. On-Premises

- 8. Global Generative AI Market Analysis, by Technology

- 8.1. Key Segment Analysis

- 8.2. Generative AI Market Size (Value - US$ Bn), Analysis, and Forecasts, by Technology, 2021-2035

- 8.2.1. Machine Learning

- 8.2.2. Deep Learning

- 8.2.3. Natural Language Processing (NLP)

- 8.2.4. Computer Vision

- 8.2.5. Others

- 9. Global Generative AI Market Analysis, by Model Type

- 9.1. Key Segment Analysis

- 9.2. Generative AI Market Size (Value - US$ Bn), Analysis, and Forecasts, by Model Type, 2021-2035

- 9.2.1. Generative Adversarial Networks (GANs)

- 9.2.2. Transformer Models

- 9.2.3. Variational Autoencoders (VAEs)

- 9.2.4. Diffusion Models

- 9.2.5. Multimodal Models

- 9.2.6. Others

- 10. Global Generative AI Market Analysis, by Enterprise Size

- 10.1. Key Segment Analysis

- 10.2. Generative AI Market Size (Value - US$ Bn), Analysis, and Forecasts, by Enterprise Size, 2021-2035

- 10.2.1. Small and Medium Enterprises (SMEs)

- 10.2.2. Large Enterprises

- 11. Global Generative AI Market Analysis, by Function

- 11.1. Key Segment Analysis

- 11.2. Generative AI Market Size (Value - US$ Bn), Analysis, and Forecasts, by Function, 2021-2035

- 11.2.1. Research and Development

- 11.2.2. Marketing and Advertising

- 11.2.3. Product Design and Prototyping

- 11.2.4. Risk and Compliance Management

- 11.2.5. Others

- 12. Global Generative AI Market Analysis, by Application

- 12.1. Key Segment Analysis

- 12.2. Generative AI Market Size (Value - US$ Bn), Analysis, and Forecasts, by Application, 2021-2035

- 12.2.1. Image and Video Generation

- 12.2.2. Text Generation and Summarization

- 12.2.3. Code Generation

- 12.2.4. Audio and Speech Synthesis

- 12.2.5. Drug Discovery and Molecular Design

- 12.2.6. Content Creation and Marketing

- 12.2.7. Data Augmentation

- 12.2.8. 3D Modeling and Design

- 12.2.9. Others

- 13. Global Generative AI Market Analysis, by Industry Vertical

- 13.1. Key Segment Analysis

- 13.2. Generative AI Market Size (Value - US$ Bn), Analysis, and Forecasts, by Industry Vertical, 2021-2035

- 13.2.1. Media and Entertainment

- 13.2.2. BFSI

- 13.2.3. Healthcare and Life Sciences

- 13.2.4. Retail and E-commerce

- 13.2.5. IT and Telecommunications

- 13.2.6. Automotive and Manufacturing

- 13.2.7. Education

- 13.2.8. Government and Defense

- 13.2.9. Others

- 14. Global Generative AI Market Analysis and Forecasts, by Region

- 14.1. Key Findings

- 14.2. Generative AI Market Size (Value - US$ Bn), Analysis, and Forecasts, by Region, 2021-2035

- 14.2.1. North America

- 14.2.2. Europe

- 14.2.3. Asia Pacific

- 14.2.4. Middle East

- 14.2.5. Africa

- 14.2.6. South America

- 15. North America Generative AI Market Analysis

- 15.1. Key Segment Analysis

- 15.2. Regional Snapshot

- 15.3. North America Generative AI Market Size Value - US$ Bn), Analysis, and Forecasts, 2021-2035

- 15.3.1. Component

- 15.3.2. Authentication Method

- 15.3.3. Technology

- 15.3.4. Deployment Type

- 15.3.5. Enterprise Size

- 15.3.6. Application

- 15.3.7. End-User Industry

- 15.3.8. Country

- 15.3.8.1. USA

- 15.3.8.2. Canada

- 15.3.8.3. Mexico

- 15.4. USA Generative AI Market

- 15.4.1. Country Segmental Analysis

- 15.4.2. Component

- 15.4.3. Deployment Mode

- 15.4.4. Technology

- 15.4.5. Model Type

- 15.4.6. Enterprise Size

- 15.4.7. Function

- 15.4.8. Application

- 15.4.9. Industry Vertical

- 15.5. Canada Generative AI Market

- 15.5.1. Country Segmental Analysis

- 15.5.2. Component

- 15.5.3. Deployment Mode

- 15.5.4. Technology

- 15.5.5. Model Type

- 15.5.6. Enterprise Size

- 15.5.7. Function

- 15.5.8. Application

- 15.5.9. Industry Vertical

- 15.6. Mexico Generative AI Market

- 15.6.1. Country Segmental Analysis

- 15.6.2. Component

- 15.6.3. Deployment Mode

- 15.6.4. Technology

- 15.6.5. Model Type

- 15.6.6. Enterprise Size

- 15.6.7. Function

- 15.6.8. Application

- 15.6.9. Industry Vertical

- 16. Europe Generative AI Market Analysis

- 16.1. Key Segment Analysis

- 16.2. Regional Snapshot

- 16.3. Europe Generative AI Market Size (Value - US$ Bn), Analysis, and Forecasts, 2021-2035

- 16.3.1. Component

- 16.3.2. Deployment Mode

- 16.3.3. Technology

- 16.3.4. Model Type

- 16.3.5. Enterprise Size

- 16.3.6. Function

- 16.3.7. Application

- 16.3.8. Industry Vertical

- 16.3.9. Country

- 16.3.9.1. Germany

- 16.3.9.2. United Kingdom

- 16.3.9.3. France

- 16.3.9.4. Italy

- 16.3.9.5. Spain

- 16.3.9.6. Netherlands

- 16.3.9.7. Nordic Countries

- 16.3.9.8. Poland

- 16.3.9.9. Russia & CIS

- 16.3.9.10. Rest of Europe

- 16.4. Germany Generative AI Market

- 16.4.1. Country Segmental Analysis

- 16.4.2. Component

- 16.4.3. Deployment Mode

- 16.4.4. Technology

- 16.4.5. Model Type

- 16.4.6. Enterprise Size

- 16.4.7. Function

- 16.4.8. Application

- 16.4.9. Industry Vertical

- 16.5. United Kingdom Generative AI Market

- 16.5.1. Country Segmental Analysis

- 16.5.2. Component

- 16.5.3. Deployment Mode

- 16.5.4. Technology

- 16.5.5. Model Type

- 16.5.6. Enterprise Size

- 16.5.7. Function

- 16.5.8. Application

- 16.5.9. Industry Vertical

- 16.6. France Generative AI Market

- 16.6.1. Country Segmental Analysis

- 16.6.2. Component

- 16.6.3. Deployment Mode

- 16.6.4. Technology

- 16.6.5. Model Type

- 16.6.6. Enterprise Size

- 16.6.7. Function

- 16.6.8. Application

- 16.6.9. Industry Vertical

- 16.7. Italy Generative AI Market

- 16.7.1. Country Segmental Analysis

- 16.7.2. Component

- 16.7.3. Deployment Mode

- 16.7.4. Technology

- 16.7.5. Model Type

- 16.7.6. Enterprise Size

- 16.7.7. Function

- 16.7.8. Application

- 16.7.9. Industry Vertical

- 16.8. Spain Generative AI Market

- 16.8.1. Country Segmental Analysis

- 16.8.2. Component

- 16.8.3. Deployment Mode

- 16.8.4. Technology

- 16.8.5. Model Type

- 16.8.6. Enterprise Size

- 16.8.7. Function

- 16.8.8. Application

- 16.8.9. Industry Vertical

- 16.9. Netherlands Generative AI Market

- 16.9.1. Country Segmental Analysis

- 16.9.2. Component

- 16.9.3. Deployment Mode

- 16.9.4. Technology

- 16.9.5. Model Type

- 16.9.6. Enterprise Size

- 16.9.7. Function

- 16.9.8. Application

- 16.9.9. Industry Vertical

- 16.10. Nordic Countries Generative AI Market

- 16.10.1. Country Segmental Analysis

- 16.10.2. Component

- 16.10.3. Deployment Mode

- 16.10.4. Technology

- 16.10.5. Model Type

- 16.10.6. Enterprise Size

- 16.10.7. Function

- 16.10.8. Application

- 16.10.9. Industry Vertical

- 16.11. Poland Generative AI Market

- 16.11.1. Country Segmental Analysis

- 16.11.2. Component

- 16.11.3. Deployment Mode

- 16.11.4. Technology

- 16.11.5. Model Type

- 16.11.6. Enterprise Size

- 16.11.7. Function

- 16.11.8. Application

- 16.11.9. Industry Vertical

- 16.12. Russia & CIS Generative AI Market

- 16.12.1. Country Segmental Analysis

- 16.12.2. Component

- 16.12.3. Deployment Mode

- 16.12.4. Technology

- 16.12.5. Model Type

- 16.12.6. Enterprise Size

- 16.12.7. Function

- 16.12.8. Application

- 16.12.9. Industry Vertical

- 16.13. Rest of Europe Generative AI Market

- 16.13.1. Country Segmental Analysis

- 16.13.2. Component

- 16.13.3. Deployment Mode

- 16.13.4. Technology

- 16.13.5. Model Type

- 16.13.6. Enterprise Size

- 16.13.7. Function

- 16.13.8. Application

- 16.13.9. Industry Vertical

- 17. Asia Pacific Generative AI Market Analysis

- 17.1. Key Segment Analysis

- 17.2. Regional Snapshot

- 17.3. Asia Pacific Generative AI Market Size (Value - US$ Bn), Analysis, and Forecasts, 2021-2035

- 17.3.1. Component

- 17.3.2. Deployment Mode

- 17.3.3. Technology

- 17.3.4. Model Type

- 17.3.5. Enterprise Size

- 17.3.6. Function

- 17.3.7. Application

- 17.3.8. Industry Vertical

- 17.3.9. Country

- 17.3.9.1. China

- 17.3.9.2. India

- 17.3.9.3. Japan

- 17.3.9.4. South Korea

- 17.3.9.5. Australia and New Zealand

- 17.3.9.6. Indonesia

- 17.3.9.7. Malaysia

- 17.3.9.8. Thailand

- 17.3.9.9. Vietnam

- 17.3.9.10. Rest of Asia Pacific

- 17.4. China Generative AI Market

- 17.4.1. Country Segmental Analysis

- 17.4.2. Component

- 17.4.3. Deployment Mode

- 17.4.4. Technology

- 17.4.5. Model Type

- 17.4.6. Enterprise Size

- 17.4.7. Function

- 17.4.8. Application

- 17.4.9. Industry Vertical

- 17.5. India Generative AI Market

- 17.5.1. Country Segmental Analysis

- 17.5.2. Component

- 17.5.3. Deployment Mode

- 17.5.4. Technology

- 17.5.5. Model Type

- 17.5.6. Enterprise Size

- 17.5.7. Function

- 17.5.8. Application

- 17.5.9. Industry Vertical

- 17.6. Japan Generative AI Market

- 17.6.1. Country Segmental Analysis

- 17.6.2. Component

- 17.6.3. Deployment Mode

- 17.6.4. Technology

- 17.6.5. Model Type

- 17.6.6. Enterprise Size

- 17.6.7. Function

- 17.6.8. Application

- 17.6.9. Industry Vertical

- 17.7. South Korea Generative AI Market

- 17.7.1. Country Segmental Analysis

- 17.7.2. Component

- 17.7.3. Deployment Mode

- 17.7.4. Technology

- 17.7.5. Model Type

- 17.7.6. Enterprise Size

- 17.7.7. Function

- 17.7.8. Application

- 17.7.9. Industry Vertical

- 17.8. Australia and New Zealand Generative AI Market

- 17.8.1. Country Segmental Analysis

- 17.8.2. Component

- 17.8.3. Deployment Mode

- 17.8.4. Technology

- 17.8.5. Model Type

- 17.8.6. Enterprise Size

- 17.8.7. Function

- 17.8.8. Application

- 17.8.9. Industry Vertical

- 17.9. Indonesia Generative AI Market

- 17.9.1. Country Segmental Analysis

- 17.9.2. Component

- 17.9.3. Deployment Mode

- 17.9.4. Technology

- 17.9.5. Model Type

- 17.9.6. Enterprise Size

- 17.9.7. Function

- 17.9.8. Application

- 17.9.9. Industry Vertical

- 17.10. Malaysia Generative AI Market

- 17.10.1. Country Segmental Analysis

- 17.10.2. Component

- 17.10.3. Deployment Mode

- 17.10.4. Technology

- 17.10.5. Model Type

- 17.10.6. Enterprise Size

- 17.10.7. Function

- 17.10.8. Application

- 17.10.9. Industry Vertical

- 17.11. Thailand Generative AI Market

- 17.11.1. Country Segmental Analysis

- 17.11.2. Component

- 17.11.3. Deployment Mode

- 17.11.4. Technology

- 17.11.5. Model Type

- 17.11.6. Enterprise Size

- 17.11.7. Function

- 17.11.8. Application

- 17.11.9. Industry Vertical

- 17.12. Vietnam Generative AI Market

- 17.12.1. Country Segmental Analysis

- 17.12.2. Component

- 17.12.3. Deployment Mode

- 17.12.4. Technology

- 17.12.5. Model Type

- 17.12.6. Enterprise Size

- 17.12.7. Function

- 17.12.8. Application

- 17.12.9. Industry Vertical

- 17.13. Rest of Asia Pacific Generative AI Market

- 17.13.1. Country Segmental Analysis

- 17.13.2. Component

- 17.13.3. Deployment Mode

- 17.13.4. Technology

- 17.13.5. Model Type

- 17.13.6. Enterprise Size

- 17.13.7. Function

- 17.13.8. Application

- 17.13.9. Industry Vertical

- 18. Middle East Generative AI Market Analysis

- 18.1. Key Segment Analysis

- 18.2. Regional Snapshot

- 18.3. Middle East Generative AI Market Size (Value - US$ Bn), Analysis, and Forecasts, 2021-2035

- 18.3.1. Component

- 18.3.2. Deployment Mode

- 18.3.3. Technology

- 18.3.4. Model Type

- 18.3.5. Enterprise Size

- 18.3.6. Function

- 18.3.7. Application

- 18.3.8. Industry Vertical

- 18.3.9. Country

- 18.3.9.1. Turkey

- 18.3.9.2. UAE

- 18.3.9.3. Saudi Arabia

- 18.3.9.4. Israel

- 18.3.9.5. Rest of Middle East

- 18.4. Turkey Generative AI Market

- 18.4.1. Country Segmental Analysis

- 18.4.2. Component

- 18.4.3. Deployment Mode

- 18.4.4. Technology

- 18.4.5. Model Type

- 18.4.6. Enterprise Size

- 18.4.7. Function

- 18.4.8. Application

- 18.4.9. Industry Vertical

- 18.5. UAE Generative AI Market

- 18.5.1. Country Segmental Analysis

- 18.5.2. Component

- 18.5.3. Deployment Mode

- 18.5.4. Technology

- 18.5.5. Model Type

- 18.5.6. Enterprise Size

- 18.5.7. Function

- 18.5.8. Application

- 18.5.9. Industry Vertical

- 18.6. Saudi Arabia Generative AI Market

- 18.6.1. Country Segmental Analysis

- 18.6.2. Component

- 18.6.3. Deployment Mode

- 18.6.4. Technology

- 18.6.5. Model Type

- 18.6.6. Enterprise Size

- 18.6.7. Function

- 18.6.8. Application

- 18.6.9. Industry Vertical

- 18.7. Israel Generative AI Market

- 18.7.1. Country Segmental Analysis

- 18.7.2. Component

- 18.7.3. Deployment Mode

- 18.7.4. Technology

- 18.7.5. Model Type

- 18.7.6. Enterprise Size

- 18.7.7. Function

- 18.7.8. Application

- 18.7.9. Industry Vertical

- 18.8. Rest of Middle East Generative AI Market

- 18.8.1. Country Segmental Analysis

- 18.8.2. Component

- 18.8.3. Deployment Mode

- 18.8.4. Technology

- 18.8.5. Model Type

- 18.8.6. Enterprise Size

- 18.8.7. Function

- 18.8.8. Application

- 18.8.9. Industry Vertical

- 19. Africa Generative AI Market Analysis

- 19.1. Key Segment Analysis

- 19.2. Regional Snapshot

- 19.3. Africa Generative AI Market Size (Value - US$ Bn), Analysis, and Forecasts, 2021-2035

- 19.3.1. Component

- 19.3.2. Deployment Mode

- 19.3.3. Technology

- 19.3.4. Model Type

- 19.3.5. Enterprise Size

- 19.3.6. Function

- 19.3.7. Application

- 19.3.8. Industry Vertical

- 19.3.9. Country

- 19.3.9.1. South Africa

- 19.3.9.2. Egypt

- 19.3.9.3. Nigeria

- 19.3.9.4. Algeria

- 19.3.9.5. Rest of Africa

- 19.4. South Africa Generative AI Market

- 19.4.1. Country Segmental Analysis

- 19.4.2. Component

- 19.4.3. Deployment Mode

- 19.4.4. Technology

- 19.4.5. Model Type

- 19.4.6. Enterprise Size

- 19.4.7. Function

- 19.4.8. Application

- 19.4.9. Industry Vertical

- 19.5. Egypt Generative AI Market

- 19.5.1. Country Segmental Analysis

- 19.5.2. Component

- 19.5.3. Deployment Mode

- 19.5.4. Technology

- 19.5.5. Model Type

- 19.5.6. Enterprise Size

- 19.5.7. Function

- 19.5.8. Application

- 19.5.9. Industry Vertical

- 19.6. Nigeria Generative AI Market

- 19.6.1. Country Segmental Analysis

- 19.6.2. Component

- 19.6.3. Deployment Mode

- 19.6.4. Technology

- 19.6.5. Model Type

- 19.6.6. Enterprise Size

- 19.6.7. Function

- 19.6.8. Application

- 19.6.9. Industry Vertical

- 19.7. Algeria Generative AI Market

- 19.7.1. Country Segmental Analysis

- 19.7.2. Component

- 19.7.3. Deployment Mode

- 19.7.4. Technology

- 19.7.5. Model Type

- 19.7.6. Enterprise Size

- 19.7.7. Function

- 19.7.8. Application

- 19.7.9. Industry Vertical

- 19.8. Rest of Africa Generative AI Market

- 19.8.1. Country Segmental Analysis

- 19.8.2. Component

- 19.8.3. Deployment Mode

- 19.8.4. Technology

- 19.8.5. Model Type

- 19.8.6. Enterprise Size

- 19.8.7. Function

- 19.8.8. Application

- 19.8.9. Industry Vertical

- 20. South America Generative AI Market Analysis

- 20.1. Key Segment Analysis

- 20.2. Regional Snapshot

- 20.3. South America Generative AI Market Size (Value - US$ Bn), Analysis, and Forecasts, 2021-2035

- 20.3.1. Component

- 20.3.2. Deployment Mode

- 20.3.3. Technology

- 20.3.4. Model Type

- 20.3.5. Enterprise Size

- 20.3.6. Function

- 20.3.7. Application

- 20.3.8. Industry Vertical

- 20.3.9. Country

- 20.3.9.1. Brazil

- 20.3.9.2. Argentina

- 20.3.9.3. Rest of South America

- 20.4. Brazil Generative AI Market

- 20.4.1. Country Segmental Analysis

- 20.4.2. Component

- 20.4.3. Deployment Mode

- 20.4.4. Technology

- 20.4.5. Model Type

- 20.4.6. Enterprise Size

- 20.4.7. Function

- 20.4.8. Application

- 20.4.9. Industry Vertical

- 20.5. Argentina Generative AI Market

- 20.5.1. Country Segmental Analysis

- 20.5.2. Component

- 20.5.3. Deployment Mode

- 20.5.4. Technology

- 20.5.5. Model Type

- 20.5.6. Enterprise Size

- 20.5.7. Function

- 20.5.8. Application

- 20.5.9. Industry Vertical

- 20.6. Rest of South America Generative AI Market

- 20.6.1. Country Segmental Analysis

- 20.6.2. Component

- 20.6.3. Deployment Mode

- 20.6.4. Technology

- 20.6.5. Model Type

- 20.6.6. Enterprise Size

- 20.6.7. Function

- 20.6.8. Application

- 20.6.9. Industry Vertical

- 21. Key Players/ Company Profile

- 21.1. Adobe Inc.

- 21.1.1. Company Details/ Overview

- 21.1.2. Company Financials

- 21.1.3. Key Customers and Competitors

- 21.1.4. Business/ Industry Portfolio

- 21.1.5. Product Portfolio/ Specification Details

- 21.1.6. Pricing Data

- 21.1.7. Strategic Overview

- 21.1.8. Recent Developments

- 21.2. Amazon Web Services, Inc.

- 21.3. Anthropic PBC

- 21.4. Canva Pty Ltd.

- 21.5. Cohere Inc.

- 21.6. Copy.ai

- 21.7. Google LLC (Alphabet Inc.)

- 21.8. Hugging Face, Inc.

- 21.9. IBM Corporation

- 21.10. Insilico Medicine, Inc.

- 21.11. Jasper AI, Inc.

- 21.12. Microsoft Corporation

- 21.13. Midjourney, Inc.

- 21.14. MOSTLY AI

- 21.15. NVIDIA Corporation

- 21.16. OpenAI

- 21.17. Rephrase.ai

- 21.18. Runway AI, Inc.

- 21.19. Stability AI Ltd.

- 21.20. Synthesia Ltd.

- 21.21. Others Key Players

- 21.1. Adobe Inc.

Note* - This is just tentative list of players. While providing the report, we will cover more number of players based on their revenue and share for each geography

Research Design

Our research design integrates both demand-side and supply-side analysis through a balanced combination of primary and secondary research methodologies. By utilizing both bottom-up and top-down approaches alongside rigorous data triangulation methods, we deliver robust market intelligence that supports strategic decision-making.

MarketGenics' comprehensive research design framework ensures the delivery of accurate, reliable, and actionable market intelligence. Through the integration of multiple research approaches, rigorous validation processes, and expert analysis, we provide our clients with the insights needed to make informed strategic decisions and capitalize on market opportunities.

MarketGenics leverages a dedicated industry panel of experts and a comprehensive suite of paid databases to effectively collect, consolidate, and analyze market intelligence.

Our approach has consistently proven to be reliable and effective in generating accurate market insights, identifying key industry trends, and uncovering emerging business opportunities.

Through both primary and secondary research, we capture and analyze critical company-level data such as manufacturing footprints, including technical centers, R&D facilities, sales offices, and headquarters.

Our expert panel further enhances our ability to estimate market size for specific brands based on validated field-level intelligence.

Our data mining techniques incorporate both parametric and non-parametric methods, allowing for structured data collection, sorting, processing, and cleaning.

Demand projections are derived from large-scale data sets analyzed through proprietary algorithms, culminating in robust and reliable market sizing.

Research Approach

The bottom-up approach builds market estimates by starting with the smallest addressable market units and systematically aggregating them to create comprehensive market size projections.

This method begins with specific, granular data points and builds upward to create the complete market landscape.

Customer Analysis → Segmental Analysis → Geographical Analysis

The top-down approach starts with the broadest possible market data and systematically narrows it down through a series of filters and assumptions to arrive at specific market segments or opportunities.

This method begins with the big picture and works downward to increasingly specific market slices.

TAM → SAM → SOM

Research Methods

Desk / Secondary Research

While analysing the market, we extensively study secondary sources, directories, and databases to identify and collect information useful for this technical, market-oriented, and commercial report. Secondary sources that we utilize are not only the public sources, but it is a combination of Open Source, Associations, Paid Databases, MG Repository & Knowledgebase, and others.

- Company websites, annual reports, financial reports, broker reports, and investor presentations

- National government documents, statistical databases and reports

- News articles, press releases and web-casts specific to the companies operating in the market, Magazines, reports, and others

- We gather information from commercial data sources for deriving company specific data such as segmental revenue, share for geography, product revenue, and others

- Internal and external proprietary databases (industry-specific), relevant patent, and regulatory databases

- Governing Bodies, Government Organizations

- Relevant Authorities, Country-specific Associations for Industries

We also employ the model mapping approach to estimate the product level market data through the players' product portfolio

Primary Research

Primary research/ interviews is vital in analyzing the market. Most of the cases involves paid primary interviews. Primary sources include primary interviews through e-mail interactions, telephonic interviews, surveys as well as face-to-face interviews with the different stakeholders across the value chain including several industry experts.

| Type of Respondents | Number of Primaries |

|---|---|

| Tier 2/3 Suppliers | ~20 |

| Tier 1 Suppliers | ~25 |

| End-users | ~25 |

| Industry Expert/ Panel/ Consultant | ~30 |

| Total | ~100 |

MG Knowledgebase

• Repository of industry blog, newsletter and case studies

• Online platform covering detailed market reports, and company profiles

Forecasting Factors and Models

Forecasting Factors

- Historical Trends – Past market patterns, cycles, and major events that shaped how markets behave over time. Understanding past trends helps predict future behavior.

- Industry Factors – Specific characteristics of the industry like structure, regulations, and innovation cycles that affect market dynamics.

- Macroeconomic Factors – Economic conditions like GDP growth, inflation, and employment rates that affect how much money people have to spend.

- Demographic Factors – Population characteristics like age, income, and location that determine who can buy your product.

- Technology Factors – How quickly people adopt new technology and how much technology infrastructure exists.

- Regulatory Factors – Government rules, laws, and policies that can help or restrict market growth.

- Competitive Factors – Analyzing competition structure such as degree of competition and bargaining power of buyers and suppliers.

Forecasting Models / Techniques

Multiple Regression Analysis

- Identify and quantify factors that drive market changes

- Statistical modeling to establish relationships between market drivers and outcomes

Time Series Analysis – Seasonal Patterns

- Understand regular cyclical patterns in market demand

- Advanced statistical techniques to separate trend, seasonal, and irregular components

Time Series Analysis – Trend Analysis

- Identify underlying market growth patterns and momentum

- Statistical analysis of historical data to project future trends

Expert Opinion – Expert Interviews

- Gather deep industry insights and contextual understanding

- In-depth interviews with key industry stakeholders

Multi-Scenario Development

- Prepare for uncertainty by modeling different possible futures

- Creating optimistic, pessimistic, and most likely scenarios

Time Series Analysis – Moving Averages

- Sophisticated forecasting for complex time series data

- Auto-regressive integrated moving average models with seasonal components

Econometric Models

- Apply economic theory to market forecasting

- Sophisticated economic models that account for market interactions

Expert Opinion – Delphi Method

- Harness collective wisdom of industry experts

- Structured, multi-round expert consultation process

Monte Carlo Simulation

- Quantify uncertainty and probability distributions

- Thousands of simulations with varying input parameters

Research Analysis

Our research framework is built upon the fundamental principle of validating market intelligence from both demand and supply perspectives. This dual-sided approach ensures comprehensive market understanding and reduces the risk of single-source bias.

Demand-Side Analysis: We understand end-user/application behavior, preferences, and market needs along with the penetration of the product for specific application.

Supply-Side Analysis: We estimate overall market revenue, analyze the segmental share along with industry capacity, competitive landscape, and market structure.

Validation & Evaluation

Data triangulation is a validation technique that uses multiple methods, sources, or perspectives to examine the same research question, thereby increasing the credibility and reliability of research findings. In market research, triangulation serves as a quality assurance mechanism that helps identify and minimize bias, validate assumptions, and ensure accuracy in market estimates.

- Data Source Triangulation – Using multiple data sources to examine the same phenomenon

- Methodological Triangulation – Using multiple research methods to study the same research question

- Investigator Triangulation – Using multiple researchers or analysts to examine the same data

- Theoretical Triangulation – Using multiple theoretical perspectives to interpret the same data

Custom Market Research Services

We will customise the research for you, in case the report listed above does not meet your requirements.

Get 10% Free Customisation