Intermediate Bulk Container Market Size, Share, Growth Opportunity Analysis Report by Product Type (Rigid IBCs, Flexible IBCs (FIBCs or Bulk Bags), Foldable/ Collapsible IBCs and Others), Material Type, Capacity, Design, Content Type, End Use Industry, Distribution Channel and Geography (North America, Europe, Asia Pacific, Middle East, Africa, and South America) – Global Industry Data, Trends, and Forecasts, 2025–2035

|

|

|

Segmental Data Insights |

|

|

Demand Trends |

|

|

Competitive Landscape |

|

|

Strategic Development |

|

|

Future Outlook & Opportunities |

|

Intermediate Bulk Container Market Size, Share, and Growth

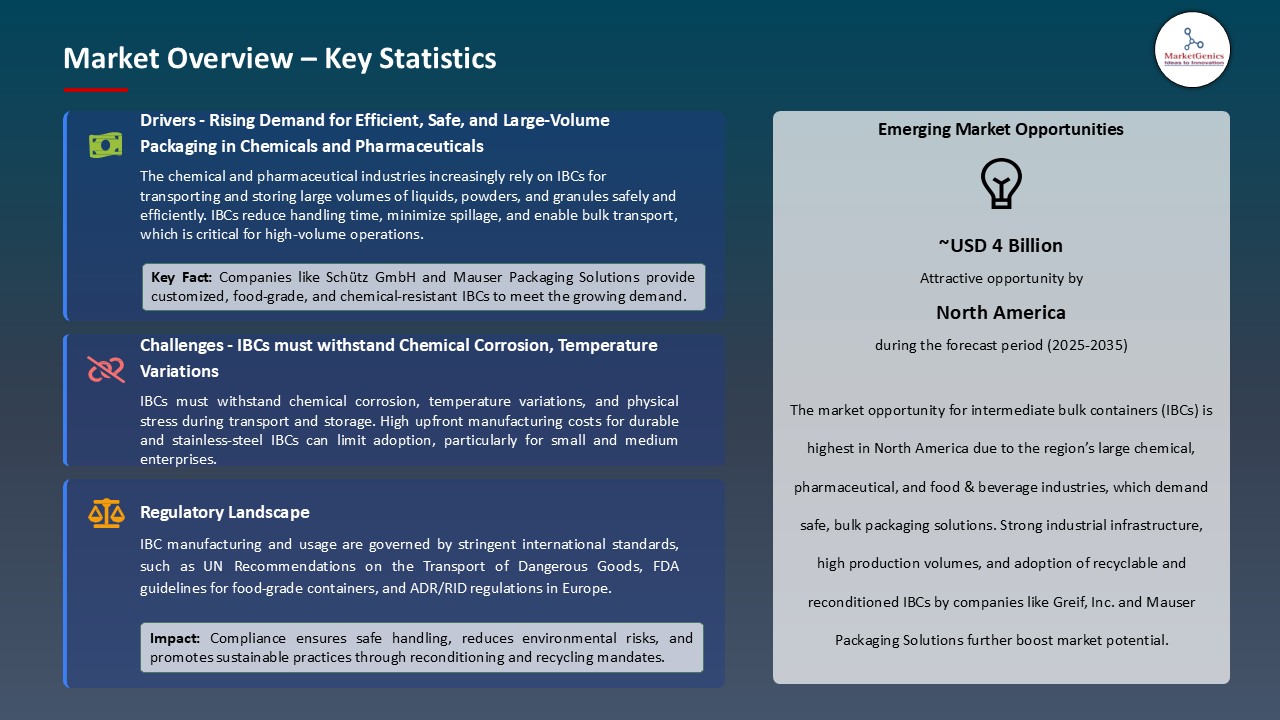

The growth of global intermediate-bulk-container-market is likely to create a significant opportunity of USD 9.6 Billion during the forecasting period, 2026-2035. Increasing demand from the chemical and pharmaceutical industries toward secure and efficient bulk material handling is the key driving factor for the global intermediate-bulk-container-market. For instance, in 2024, Greif, Inc. has further extended the IBC product line to serve the surging demand from chemical manufacturers in Europe and North America.

In March 2025, Nefab AB launched a modular, returnable Intermediate Bulk Container solution designed for automotive and electronics industries to reduce packaging waste and optimize logistics, including transport efficiency improvements relevant to the Automotive Wiring Harness. The strategy aligns with Nefab’s focus on sustainable supply chains. Per Öhagen, President and CEO of Nefab Group, emphasized this launch as a step toward achieving circular packaging targets across global operations. This development strengthens Nefab’s position in eco-efficient industrial packaging, addressing growing demand for sustainable IBC solutions.

A push for reusable and sustainable packaging for food and beverage logistics: Mauser Packaging Solutions has launched a new line of reconditioned IBCs targeting the sustainability goals of major F&B clients in 2024. These factors are opening up new industrial sectors for IBC adoption, which, in turn, is growing the market globally.

The major operating opportunities existing for the global intermediate bulk container (IBC) market are flexible packaging for industrial use, automated material handling systems, and smart logistics solutions with IoT integration. These segments promote cost-efficiency, automation, and real-time tracking in utility for IBC. This then boosts the value of IBC across modern supply chains.

Intermediate Bulk Container Market Dynamics and Trends

Driver: Expansion of Agrochemical and Fertilizer Industry

- One of the key factors affecting the worldwide Intermediate-Bulk-Container-market is the need in the agrochemical and fertilizer industries for safe and efficient bulk packaging. IBCs are seeing a demand because liquid fertilizers, crop protection chemicals, and pesticides all require large-scale and safe transport.

- An entirely new one was rolled out by Schoeller Allibert in 2024 for agrochemical application, with an improved chemical resistance and UV protection. This was in response to the bigger agribusinesses in Latin America and Asia-Pacific demanding for strong containers that are reusable to lessen packaging wastes and to minimize cost per use. For multiple cycles of agricultural chemical use, IBCs stack well and have longevity.

- With the growth of the agrochemical industry comes the need for durable IBCs which in return drives the growth of this market.

Restraint: Fluctuating Raw Material Prices

- One of the major restraints affecting the IBC (Intermediate Bulk Containers) market internationally would be the drastic nature of price fluctuations of the raw materials, especially those affecting the production of rigid and composite IBCs: plastics and steel. As crude oil price varies, variations in polymer prices take their course, and these polymers matter a lot when it comes to manufacturing plastic-based IBCs.

- In 2025, Myers Industries, Inc., one of the leading manufacturers of IBCs, announced a dip in profit margins due to sudden hikes in resin costs, which aggravated production costs and hampered the timely order fulfillment thereof. All these fluctuations give rise to cost uncertainties for manufacturers and distributors, thus hitting price stability and holding down long-term contracts.

- Moreover, with this up-and-down pricing scenario, a small-to-medium-scale producer is at disadvantage to a larger one, who either hedge procurement or actually goes vertical.

- In this way, the varying pricings of raw materials impeded production efficacy and profitability; hence, this restriction not only hinders smooth growth and development of the market but also causes it'll slow down.

Opportunity: Rise in Cross-Border E-commerce Logistics

- One evolving opportunity for the IBC market lies in the cross-border e-commerce logistics, especially for bulk liquids and semi-solids, reflecting structural demand patterns within the E-commerce Logistics Market. As industrial-grade goods and bulk consumables are increasingly exported worldwide, there is demand for reliable standardized transport containers such as IBCs.

- In 2024, the global logistics company and an Indian supplier of plastic intermediates namely Time Technoplast Ltd. entered into an arrangement to supply UN-certified IBCs for cross-border shipment of lubricants and specialty chemicals to Southeast Asia and the Middle East. The containers are designed for long-haul transportation under stringent international safety standards. Industrial supply platforms, driven by e-commerce, want the packaging to be stackable and recyclable to keep costs low during shipping and storage.

- A growing demand for standardized packaging coming from cross-border industrial logistics is therefore opening new avenues for revenue generation for IBC manufacturers.

Key Trend: Integration of Smart Monitoring in IBCs

- On the side of the IBC market, a key trend is the incorporation of smart technologies for the real-time monitoring of contents, location, and temperature. IoT-enabled IBCs are therefore surfacing as a general demand from manufacturers who want to bring traceability and visibility to their supply chains.

- In 2025, Greif, Inc. introduced a new line of smart IBCs with RFID tags and temperature sensors for customers in the pharmaceutical and food-grade chemical industries. Remote tracking and alert notification systems inhibit loss by warning the operator should the container leak or be exposed to unauthorized transit conditions, thus providing increased safety compliance. The trend follows digital transformation in industries as the use of predictive analytics and asset tracking optimizing the logistics and maintenance aspects.

- With IoT entering the picture and setting in with advanced asset tracking, the packaging industry will, therefore, have to modernize and increase its offering in the tech-integrated and value-oriented segment.

Intermediate-Bulk-Container-Market Analysis and Segmental Data

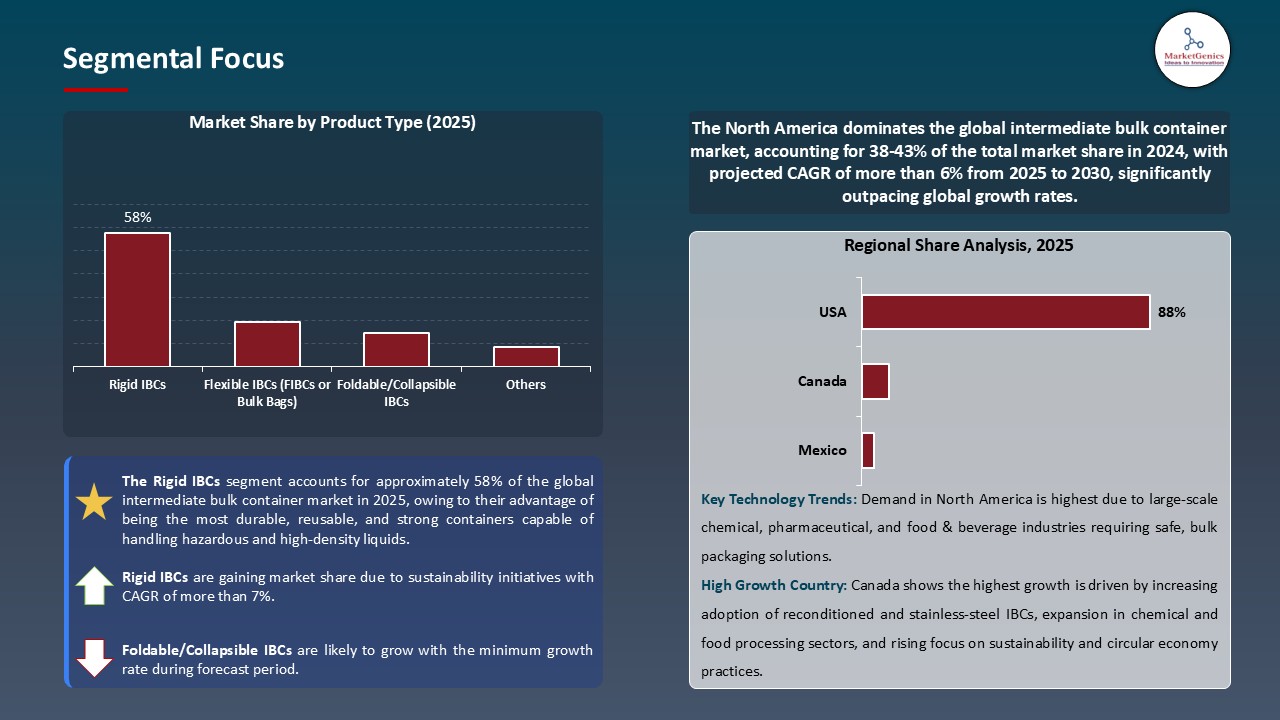

Based on Product Type, the rigid IBCs Segment Retains the Largest Share

- The rigid IBCs segment holds major share of ~58% in the global intermediate bulk container market, owing to their advantage of being the most durable, reusable, and strong containers capable of handling hazardous and high-density liquids. These containers possess enhanced structural integrity, making them most suitable for industrial uses across chemicals, pharmaceuticals, and food processing sectors. In 2024, Mauser Packaging Solutions ramped up the production of rigid IBCs in North America to fulfill increased demand coming from chemical manufacturers, requiring UN-certified containers for the safe transport and storage of their substances. They can be stacked very efficiently owing to their robust design, thereby saving shipping and warehouse space.

- More importantly, rigid IBCs are the primary choice in closed-loop supply-chain systems, whereby containers are retrieved from the users, cleaned, and re-used several times, hence reducing long-term operating costs. They are further preferred due to their compatibility with automation systems in warehousing and transport hubs. Many global players are embedding RFID as well as smart sensors within rigid IBCs for traceability. Moreover, the segment is favored by regulations in sectors at high risk, where secure and tamper-evident packaging is mandated.

- High strength, reusability, and compliance needs are driving the dominance of rigid IBCs in global industrial packaging.

North America Dominates Global Intermediate-Bulk-Container-Market in 2025 and Beyond

- Demand for intermediate bulk containers (IBCs) is high in North America, as the chemical, pharmaceutical, and food processing industries are well established in the region, requiring safe and efficient bulk packaging. Stringent regulations for transportation of hazardous materials on the part of the U.S. make IBCs a preferred packaging option. In 2024, Schütz Container Systems announced the expansion of its capacity at its Texas plant to cater to the mounting demand from petrochemical clients along the Gulf Coast. The region stands behind IBC adoption because of its thrust on cheap and reusable packaging and supply chain efficiency.

- Further, the growing B2B logistics under e-commerce and the adoption of automated warehousing solutions in North America favor standardized, stackable containers such as IBCs. The region's stand for sustainability also encourages the demand for IBC formats that are reusable and recyclable. Trading across borders with Canada and Mexico is increasing with the demand for more durable bulk packaging adhering to regulations.

- Having a strong industrial base, the necessity of regulations, and a continuous focus on sustainability make North America the leading region for IBC consumption.

Intermediate Bulk Container Market Ecosystem

Key players in the global intermediate bulk container market include prominent companies such as Autoliv Inc., Joyson Safety Systems, ZF Friedrichshafen AG (TRW), Toyoda Gosei Co., Ltd. and Other Key Players.

The intermediate bulk container (IBC) market has moderately consolidated, Tier 1 companies such as SCHÜTZ GmbH, Mauser Packaging Solutions, and Greif, Inc. leading through worldwide distribution networks and diverse industrial applications. Regional and niche markets are catered by Tier 2 and Tier 3 players such as CESA and Infinite Solutions. There is a moderate concentration of buyers on account of demands coming from chemicals, food, and pharmaceuticals, while there is a high concentration of suppliers due to specialized materials, UN certification standards, and requirements for durable designs of containers.

Recent Development and Strategic Overview:

- In May 2024, the acquiring of a majority stake by Greif, Inc. in Delta Containers Manchester provided a huge boost to its reconditioning and recycling of IBC services in the UK and Ireland, favoring its circular economy position.

- In May 2025, Mauser Packaging Solutions introduced its first stainless-steel IBC line for high-purity pharma and food applications responding to the rising demand in hygienic and sustainable packaging.

Report Scope

|

Detail |

|

|

Market Size in 2025 |

USD 12.8 Bn |

|

Market Forecast Value in 2035 |

USD 22.4 Bn |

|

Growth Rate (CAGR) |

5.2% |

|

Forecast Period |

2025 – 2035 |

|

Historical Data Available for |

2021 – 2024 |

|

Market Size Units |

US$ Billion for Value Thousand Units for Volume |

|

Report Format |

Electronic (PDF) + Excel |

|

North America |

Europe |

Asia Pacific |

Middle East |

Africa |

South America |

|

|

|

|

|

|

|

Companies Covered |

|||||

|

|

|

|

|

|

Intermediate Bulk Container Market Segmentation and Highlights

|

Segment |

Sub-segment |

|

By Material Type |

|

|

By Product Type |

|

|

By Capacity |

|

|

By Design |

|

|

By Content Type |

|

|

By End Use Industry |

|

|

By Distribution Channel |

|

Frequently Asked Questions

Table of Contents

- 1. Research Methodology and Assumptions

- 1.1. Definitions

- 1.2. Research Design and Approach

- 1.3. Data Collection Methods

- 1.4. Base Estimates and Calculations

- 1.5. Forecasting Models

- 1.5.1. Key Forecast Factors & Impact Analysis

- 1.6. Secondary Research

- 1.6.1. Open Sources

- 1.6.2. Paid Databases

- 1.6.3. Associations

- 1.7. Primary Research

- 1.7.1. Primary Sources

- 1.7.2. Primary Interviews with Stakeholders across Ecosystem

- 2. Executive Summary

- 2.1. Global Intermediate Bulk Container Market Outlook

- 2.1.1. Intermediate Bulk Container Market Size (Volume - Thousand Units & Value - US$ Billion), and Forecasts, 2021-2035

- 2.1.2. Compounded Annual Growth Rate Analysis

- 2.1.3. Growth Opportunity Analysis

- 2.1.4. Segmental Share Analysis

- 2.1.5. Geographical Share Analysis

- 2.2. Market Analysis and Facts

- 2.3. Supply-Demand Analysis

- 2.4. Competitive Benchmarking

- 2.5. Go-to- Market Strategy

- 2.5.1. Customer/ End Use Industry Assessment

- 2.5.2. Growth Opportunity Data, 2025-2035

- 2.5.2.1. Regional Data

- 2.5.2.2. Country Data

- 2.5.2.3. Segmental Data

- 2.5.3. Identification of Potential Market Spaces

- 2.5.4. GAP Analysis

- 2.5.5. Potential Attractive Price Points

- 2.5.6. Prevailing Market Risks & Challenges

- 2.5.7. Preferred Sales & Marketing Strategies

- 2.5.8. Key Recommendations and Analysis

- 2.5.9. A Way Forward

- 2.1. Global Intermediate Bulk Container Market Outlook

- 3. Industry Data and Premium Insights

- 3.1. Global Automotive & Transportation Overview, 2025

- 3.1.1. Industry Ecosystem Analysis

- 3.1.2. Key Trends for Automotive & Transportation Industry

- 3.1.3. Regional Distribution for Automotive & Transportation

- 3.2. Supplier Customer Data

- 3.3. Technology Roadmap and Developments

- 3.1. Global Automotive & Transportation Overview, 2025

- 4. Market Overview

- 4.1. Market Dynamics

- 4.1.1. Drivers

- 4.1.1.1. Rising demand for bulk packaging in chemicals, food, and pharmaceutical industries

- 4.1.1.2. Growth of global trade and cross-border industrial logistics

- 4.1.1.3. Increasing adoption of reusable and sustainable packaging solutions

- 4.1.2. Restraints

- 4.1.2.1. Volatility in raw material prices (plastics and metals)

- 4.1.1. Drivers

- 4.2. Key Trend Analysis

- 4.3. Regulatory Framework

- 4.3.1. Key Regulations, Norms, and Subsidies, by Key Countries

- 4.3.2. Tariffs and Standards

- 4.3.3. Impact Analysis of Regulations on the Market

- 4.4. Value Chain Analysis/ Ecosystem Analysis

- 4.4.1. Raw Material Suppliers

- 4.4.2. Intermediate Bulk Container Manufacturers

- 4.4.3. Distributors & Logistic Providers

- 4.4.4. End Users/ Customers

- 4.5. Cost Structure Analysis

- 4.5.1. Parameter’s Share for Cost Associated

- 4.5.2. COGP vs COGS

- 4.5.3. Profit Margin Analysis

- 4.6. Porter’s Five Forces Analysis

- 4.7. PESTEL Analysis

- 4.8. Global Intermediate Bulk Container Market Demand

- 4.8.1. Historical Market Size - in Value (Volume - Thousand Units & Value - US$ Billion), 2021-2024

- 4.8.2. Current and Future Market Size - in Value (Volume - Thousand Units & Value - US$ Billion), 2025–2035

- 4.8.2.1. Y-o-Y Growth Trends

- 4.8.2.2. Absolute $ Opportunity Assessment

- 4.1. Market Dynamics

- 5. Competition Landscape

- 5.1. Competition structure

- 5.1.1. Fragmented v/s consolidated

- 5.2. Company Share Analysis, 2025

- 5.2.1. Global Company Market Share

- 5.2.2. By Region

- 5.2.2.1. North America

- 5.2.2.2. Europe

- 5.2.2.3. Asia Pacific

- 5.2.2.4. Middle East

- 5.2.2.5. Africa

- 5.2.2.6. South America

- 5.3. Product Comparison Matrix

- 5.3.1. Specifications

- 5.3.2. Market Positioning

- 5.3.3. Pricing

- 5.1. Competition structure

- 6. Global Intermediate Bulk Container Market Analysis, by Material Type

- 6.1. Key Segment Analysis

- 6.2. Intermediate Bulk Container Market Size (Volume - Thousand Units & Value - US$ Billion), Analysis, and Forecasts, by Material Type, 2021-2035

- 6.2.1. Plastic

- 6.2.1.1. HDPE

- 6.2.1.2. PP

- 6.2.1.3. Others

- 6.2.2. Metal

- 6.2.2.1. Stainless Steel

- 6.2.2.2. Carbon Steel

- 6.2.2.3. Others

- 6.2.3. Composite (Plastic + Metal Frames)

- 6.2.4. Fiberboard / Paperboard

- 6.2.5. Others

- 6.2.1. Plastic

- 7. Global Intermediate Bulk Container Market Analysis, by Product Type

- 7.1. Key Segment Analysis

- 7.2. Intermediate Bulk Container Market Size (Volume - Thousand Units & Value - US$ Billion), Analysis, and Forecasts, by Product Type, 2021-2035

- 7.2.1. Rigid IBCs

- 7.2.2. Flexible IBCs (FIBCs or Bulk Bags)

- 7.2.3. Foldable/Collapsible IBCs

- 7.2.4. Others

- 8. Global Intermediate Bulk Container Market Analysis, by Capacity

- 8.1. Key Segment Analysis

- 8.2. Intermediate Bulk Container Market Size (Volume - Thousand Units & Value - US$ Billion), Analysis, and Forecasts, by Capacity, 2021-2035

- 8.2.1. Up to 500 Liters

- 8.2.2. 501 to 1,000 Liters

- 8.2.3. 1,001 to 1,500 Liters

- 8.2.4. Above 1,500 Liters

- 9. Global Intermediate Bulk Container Market Analysis, by Design

- 9.1. Key Segment Analysis

- 9.2. Intermediate Bulk Container Market Size (Volume - Thousand Units & Value - US$ Billion), Analysis, and Forecasts, by Design, 2021-2035

- 9.2.1. Caged IBCs

- 9.2.2. Bottled IBCs

- 9.2.3. Baffled IBCs

- 9.2.4. Valve-Fitted IBCs

- 9.2.5. Open Top/Closed Top

- 9.2.6. Others

- 10. Global Intermediate Bulk Container Market Analysis, by Content Type

- 10.1. Key Segment Analysis

- 10.2. Intermediate Bulk Container Market Size (Volume - Thousand Units & Value - US$ Billion), Analysis, and Forecasts, by Content Type, 2021-2035

- 10.2.1. Liquids

- 10.2.2. Semi-Solids

- 10.2.3. Solids (Granules, Powders)

- 10.2.4. Others

- 11. Global Intermediate Bulk Container Market Analysis, by End Use Industry

- 11.1. Key Segment Analysis

- 11.2. Intermediate Bulk Container Market Size (Volume - Thousand Units & Value - US$ Billion), Analysis, and Forecasts, by End Use Industry, 2021-2035

- 11.2.1. Automotive

- 11.2.2. Aerospace & Defense

- 11.2.3. Industrial Machinery

- 11.2.4. Construction

- 11.2.5. Electronics

- 11.2.6. Consumer Goods

- 11.2.7. Healthcare & Medical Devices

- 11.2.8. Others

- 12. Global Intermediate Bulk Container Market Analysis, by Distribution Channel

- 12.1. Key Segment Analysis

- 12.2. Intermediate Bulk Container Market Size (Volume - Thousand Units & Value - US$ Billion), Analysis, and Forecasts, by Distribution Channel, 2021-2035

- 12.2.1. Direct Sales (OEMs and Integrators)

- 12.2.2. Distributors & Dealers

- 12.2.3. E-commerce Channels

- 13. Global Intermediate Bulk Container Market Analysis and Forecasts, by Region

- 13.1. Key Findings

- 13.2. Intermediate Bulk Container Market Size (Volume - Thousand Units & Value - US$ Billion), Analysis, and Forecasts, by Region, 2021-2035

- 13.2.1. North America

- 13.2.2. Europe

- 13.2.3. Asia Pacific

- 13.2.4. Middle East

- 13.2.5. Africa

- 13.2.6. South America

- 14. North America Intermediate Bulk Container Market Analysis

- 14.1. Key Segment Analysis

- 14.2. Regional Snapshot

- 14.3. North America Intermediate Bulk Container Market Size Volume - Thousand Units & Value - US$ Billion), Analysis, and Forecasts, 2021-2035

- 14.3.1. Material Type

- 14.3.2. Product Type

- 14.3.3. Capacity

- 14.3.4. Design

- 14.3.5. Content Type

- 14.3.6. End Use Industry

- 14.3.7. Distribution Channel

- 14.3.8. Country

- 14.3.8.1. USA

- 14.3.8.2. Canada

- 14.3.8.3. Mexico

- 14.4. USA Intermediate Bulk Container Market

- 14.4.1. Country Segmental Analysis

- 14.4.2. Material Type

- 14.4.3. Product Type

- 14.4.4. Capacity

- 14.4.5. Design

- 14.4.6. Content Type

- 14.4.7. End Use Industry

- 14.4.8. Distribution Channel

- 14.5. Canada Intermediate Bulk Container Market

- 14.5.1. Country Segmental Analysis

- 14.5.2. Material Type

- 14.5.3. Product Type

- 14.5.4. Capacity

- 14.5.5. Design

- 14.5.6. Content Type

- 14.5.7. End Use Industry

- 14.5.8. Distribution Channel

- 14.6. Mexico Intermediate Bulk Container Market

- 14.6.1. Country Segmental Analysis

- 14.6.2. Material Type

- 14.6.3. Product Type

- 14.6.4. Capacity

- 14.6.5. Design

- 14.6.6. Content Type

- 14.6.7. End Use Industry

- 14.6.8. Distribution Channel

- 15. Europe Intermediate Bulk Container Market Analysis

- 15.1. Key Segment Analysis

- 15.2. Regional Snapshot

- 15.3. Europe Intermediate Bulk Container Market Size (Volume - Thousand Units & Value - US$ Billion), Analysis, and Forecasts, 2021-2035

- 15.3.1. Material Type

- 15.3.2. Product Type

- 15.3.3. Capacity

- 15.3.4. Design

- 15.3.5. Content Type

- 15.3.6. End Use Industry

- 15.3.7. Distribution Channel

- 15.3.8. Country

- 15.3.8.1. Germany

- 15.3.8.2. United Kingdom

- 15.3.8.3. France

- 15.3.8.4. Italy

- 15.3.8.5. Spain

- 15.3.8.6. Netherlands

- 15.3.8.7. Nordic Countries

- 15.3.8.8. Poland

- 15.3.8.9. Russia & CIS

- 15.3.8.10. Rest of Europe

- 15.4. Germany Intermediate Bulk Container Market

- 15.4.1. Country Segmental Analysis

- 15.4.2. Material Type

- 15.4.3. Product Type

- 15.4.4. Capacity

- 15.4.5. Design

- 15.4.6. Content Type

- 15.4.7. End Use Industry

- 15.4.8. Distribution Channel

- 15.5. United Kingdom Intermediate Bulk Container Market

- 15.5.1. Country Segmental Analysis

- 15.5.2. Material Type

- 15.5.3. Product Type

- 15.5.4. Capacity

- 15.5.5. Design

- 15.5.6. Content Type

- 15.5.7. End Use Industry

- 15.5.8. Distribution Channel

- 15.6. France Intermediate Bulk Container Market

- 15.6.1. Country Segmental Analysis

- 15.6.2. Material Type

- 15.6.3. Product Type

- 15.6.4. Capacity

- 15.6.5. Design

- 15.6.6. Content Type

- 15.6.7. End Use Industry

- 15.6.8. Distribution Channel

- 15.7. Italy Intermediate Bulk Container Market

- 15.7.1. Country Segmental Analysis

- 15.7.2. Material Type

- 15.7.3. Product Type

- 15.7.4. Capacity

- 15.7.5. Design

- 15.7.6. Content Type

- 15.7.7. End Use Industry

- 15.7.8. Distribution Channel

- 15.8. Spain Intermediate Bulk Container Market

- 15.8.1. Country Segmental Analysis

- 15.8.2. Material Type

- 15.8.3. Product Type

- 15.8.4. Capacity

- 15.8.5. Design

- 15.8.6. Content Type

- 15.8.7. End Use Industry

- 15.8.8. Distribution Channel

- 15.9. Netherlands Intermediate Bulk Container Market

- 15.9.1. Country Segmental Analysis

- 15.9.2. Material Type

- 15.9.3. Product Type

- 15.9.4. Capacity

- 15.9.5. Design

- 15.9.6. Content Type

- 15.9.7. End Use Industry

- 15.9.8. Distribution Channel

- 15.10. Nordic Countries Intermediate Bulk Container Market

- 15.10.1. Country Segmental Analysis

- 15.10.2. Material Type

- 15.10.3. Product Type

- 15.10.4. Capacity

- 15.10.5. Design

- 15.10.6. Content Type

- 15.10.7. End Use Industry

- 15.10.8. Distribution Channel

- 15.11. Poland Intermediate Bulk Container Market

- 15.11.1. Country Segmental Analysis

- 15.11.2. Material Type

- 15.11.3. Product Type

- 15.11.4. Capacity

- 15.11.5. Design

- 15.11.6. Content Type

- 15.11.7. End Use Industry

- 15.11.8. Distribution Channel

- 15.12. Russia & CIS Intermediate Bulk Container Market

- 15.12.1. Country Segmental Analysis

- 15.12.2. Material Type

- 15.12.3. Product Type

- 15.12.4. Capacity

- 15.12.5. Design

- 15.12.6. Content Type

- 15.12.7. End Use Industry

- 15.12.8. Distribution Channel

- 15.13. Rest of Europe Intermediate Bulk Container Market

- 15.13.1. Country Segmental Analysis

- 15.13.2. Material Type

- 15.13.3. Product Type

- 15.13.4. Capacity

- 15.13.5. Design

- 15.13.6. Content Type

- 15.13.7. End Use Industry

- 15.13.8. Distribution Channel

- 16. Asia Pacific Intermediate Bulk Container Market Analysis

- 16.1. Key Segment Analysis

- 16.2. Regional Snapshot

- 16.3. East Asia Intermediate Bulk Container Market Size (Volume - Thousand Units & Value - US$ Billion), Analysis, and Forecasts, 2021-2035

- 16.3.1. Material Type

- 16.3.2. Product Type

- 16.3.3. Capacity

- 16.3.4. Design

- 16.3.5. Content Type

- 16.3.6. End Use Industry

- 16.3.7. Distribution Channel

- 16.3.8. Country

- 16.3.8.1. China

- 16.3.8.2. India

- 16.3.8.3. Japan

- 16.3.8.4. South Korea

- 16.3.8.5. Australia and New Zealand

- 16.3.8.6. Indonesia

- 16.3.8.7. Malaysia

- 16.3.8.8. Thailand

- 16.3.8.9. Vietnam

- 16.3.8.10. Rest of Asia Pacific

- 16.4. China Intermediate Bulk Container Market

- 16.4.1. Country Segmental Analysis

- 16.4.2. Material Type

- 16.4.3. Product Type

- 16.4.4. Capacity

- 16.4.5. Design

- 16.4.6. Content Type

- 16.4.7. End Use Industry

- 16.4.8. Distribution Channel

- 16.5. India Intermediate Bulk Container Market

- 16.5.1. Country Segmental Analysis

- 16.5.2. Material Type

- 16.5.3. Product Type

- 16.5.4. Capacity

- 16.5.5. Design

- 16.5.6. Content Type

- 16.5.7. End Use Industry

- 16.5.8. Distribution Channel

- 16.6. Japan Intermediate Bulk Container Market

- 16.6.1. Country Segmental Analysis

- 16.6.2. Material Type

- 16.6.3. Product Type

- 16.6.4. Capacity

- 16.6.5. Design

- 16.6.6. Content Type

- 16.6.7. End Use Industry

- 16.6.8. Distribution Channel

- 16.7. South Korea Intermediate Bulk Container Market

- 16.7.1. Country Segmental Analysis

- 16.7.2. Material Type

- 16.7.3. Product Type

- 16.7.4. Capacity

- 16.7.5. Design

- 16.7.6. Content Type

- 16.7.7. End Use Industry

- 16.7.8. Distribution Channel

- 16.8. Australia and New Zealand Intermediate Bulk Container Market

- 16.8.1. Country Segmental Analysis

- 16.8.2. Material Type

- 16.8.3. Product Type

- 16.8.4. Capacity

- 16.8.5. Design

- 16.8.6. Content Type

- 16.8.7. End Use Industry

- 16.8.8. Distribution Channel

- 16.9. Indonesia Intermediate Bulk Container Market

- 16.9.1. Country Segmental Analysis

- 16.9.2. Material Type

- 16.9.3. Product Type

- 16.9.4. Capacity

- 16.9.5. Design

- 16.9.6. Content Type

- 16.9.7. End Use Industry

- 16.9.8. Distribution Channel

- 16.10. Malaysia Intermediate Bulk Container Market

- 16.10.1. Country Segmental Analysis

- 16.10.2. Material Type

- 16.10.3. Product Type

- 16.10.4. Capacity

- 16.10.5. Design

- 16.10.6. Content Type

- 16.10.7. End Use Industry

- 16.10.8. Distribution Channel

- 16.11. Thailand Intermediate Bulk Container Market

- 16.11.1. Country Segmental Analysis

- 16.11.2. Material Type

- 16.11.3. Product Type

- 16.11.4. Capacity

- 16.11.5. Design

- 16.11.6. Content Type

- 16.11.7. End Use Industry

- 16.11.8. Distribution Channel

- 16.12. Vietnam Intermediate Bulk Container Market

- 16.12.1. Country Segmental Analysis

- 16.12.2. Material Type

- 16.12.3. Product Type

- 16.12.4. Capacity

- 16.12.5. Design

- 16.12.6. Content Type

- 16.12.7. End Use Industry

- 16.12.8. Distribution Channel

- 16.13. Rest of Asia Pacific Intermediate Bulk Container Market

- 16.13.1. Country Segmental Analysis

- 16.13.2. Material Type

- 16.13.3. Product Type

- 16.13.4. Capacity

- 16.13.5. Design

- 16.13.6. Content Type

- 16.13.7. End Use Industry

- 16.13.8. Distribution Channel

- 17. Middle East Intermediate Bulk Container Market Analysis

- 17.1. Key Segment Analysis

- 17.2. Regional Snapshot

- 17.3. Middle East Intermediate Bulk Container Market Size (Volume - Thousand Units & Value - US$ Billion), Analysis, and Forecasts, 2021-2035

- 17.3.1. Material Type

- 17.3.2. Product Type

- 17.3.3. Capacity

- 17.3.4. Design

- 17.3.5. Content Type

- 17.3.6. End Use Industry

- 17.3.7. Distribution Channel

- 17.3.8. Country

- 17.3.8.1. Turkey

- 17.3.8.2. UAE

- 17.3.8.3. Saudi Arabia

- 17.3.8.4. Israel

- 17.3.8.5. Rest of Middle East

- 17.4. Turkey Intermediate Bulk Container Market

- 17.4.1. Country Segmental Analysis

- 17.4.2. Material Type

- 17.4.3. Product Type

- 17.4.4. Capacity

- 17.4.5. Design

- 17.4.6. Content Type

- 17.4.7. End Use Industry

- 17.4.8. Distribution Channel

- 17.5. UAE Intermediate Bulk Container Market

- 17.5.1. Country Segmental Analysis

- 17.5.2. Material Type

- 17.5.3. Product Type

- 17.5.4. Capacity

- 17.5.5. Design

- 17.5.6. Content Type

- 17.5.7. End Use Industry

- 17.5.8. Distribution Channel

- 17.6. Saudi Arabia Intermediate Bulk Container Market

- 17.6.1. Country Segmental Analysis

- 17.6.2. Material Type

- 17.6.3. Product Type

- 17.6.4. Capacity

- 17.6.5. Design

- 17.6.6. Content Type

- 17.6.7. End Use Industry

- 17.6.8. Distribution Channel

- 17.7. Israel Intermediate Bulk Container Market

- 17.7.1. Country Segmental Analysis

- 17.7.2. Material Type

- 17.7.3. Product Type

- 17.7.4. Capacity

- 17.7.5. Design

- 17.7.6. Content Type

- 17.7.7. End Use Industry

- 17.7.8. Distribution Channel

- 17.8. Rest of Middle East Intermediate Bulk Container Market

- 17.8.1. Country Segmental Analysis

- 17.8.2. Material Type

- 17.8.3. Product Type

- 17.8.4. Capacity

- 17.8.5. Design

- 17.8.6. Content Type

- 17.8.7. End Use Industry

- 17.8.8. Distribution Channel

- 18. Africa Intermediate Bulk Container Market Analysis

- 18.1. Key Segment Analysis

- 18.2. Regional Snapshot

- 18.3. Africa Intermediate Bulk Container Market Size (Volume - Thousand Units & Value - US$ Billion), Analysis, and Forecasts, 2021-2035

- 18.3.1. Material Type

- 18.3.2. Product Type

- 18.3.3. Capacity

- 18.3.4. Design

- 18.3.5. Content Type

- 18.3.6. End Use Industry

- 18.3.7. Distribution Channel

- 18.3.8. Country

- 18.3.8.1. South Africa

- 18.3.8.2. Egypt

- 18.3.8.3. Nigeria

- 18.3.8.4. Algeria

- 18.3.8.5. Rest of Africa

- 18.4. South Africa Intermediate Bulk Container Market

- 18.4.1. Country Segmental Analysis

- 18.4.2. Material Type

- 18.4.3. Product Type

- 18.4.4. Capacity

- 18.4.5. Design

- 18.4.6. Content Type

- 18.4.7. End Use Industry

- 18.4.8. Distribution Channel

- 18.5. Egypt Intermediate Bulk Container Market

- 18.5.1. Country Segmental Analysis

- 18.5.2. Material Type

- 18.5.3. Product Type

- 18.5.4. Capacity

- 18.5.5. Design

- 18.5.6. Content Type

- 18.5.7. End Use Industry

- 18.5.8. Distribution Channel

- 18.6. Nigeria Intermediate Bulk Container Market

- 18.6.1. Country Segmental Analysis

- 18.6.2. Material Type

- 18.6.3. Product Type

- 18.6.4. Capacity

- 18.6.5. Design

- 18.6.6. Content Type

- 18.6.7. End Use Industry

- 18.6.8. Distribution Channel

- 18.7. Algeria Intermediate Bulk Container Market

- 18.7.1. Country Segmental Analysis

- 18.7.2. Material Type

- 18.7.3. Product Type

- 18.7.4. Capacity

- 18.7.5. Design

- 18.7.6. Content Type

- 18.7.7. End Use Industry

- 18.7.8. Distribution Channel

- 18.8. Rest of Africa Intermediate Bulk Container Market

- 18.8.1. Country Segmental Analysis

- 18.8.2. Material Type

- 18.8.3. Product Type

- 18.8.4. Capacity

- 18.8.5. Design

- 18.8.6. Content Type

- 18.8.7. End Use Industry

- 18.8.8. Distribution Channel

- 19. South America Intermediate Bulk Container Market Analysis

- 19.1. Key Segment Analysis

- 19.2. Regional Snapshot

- 19.3. Central and South Africa Intermediate Bulk Container Market Size (Volume - Thousand Units & Value - US$ Billion), Analysis, and Forecasts, 2021-2035

- 19.3.1. Material Type

- 19.3.2. Product Type

- 19.3.3. Capacity

- 19.3.4. Design

- 19.3.5. Content Type

- 19.3.6. End Use Industry

- 19.3.7. Distribution Channel

- 19.3.8. Country

- 19.3.8.1. Brazil

- 19.3.8.2. Argentina

- 19.3.8.3. Rest of South America

- 19.4. Brazil Intermediate Bulk Container Market

- 19.4.1. Country Segmental Analysis

- 19.4.2. Material Type

- 19.4.3. Product Type

- 19.4.4. Capacity

- 19.4.5. Design

- 19.4.6. Content Type

- 19.4.7. End Use Industry

- 19.4.8. Distribution Channel

- 19.5. Argentina Intermediate Bulk Container Market

- 19.5.1. Country Segmental Analysis

- 19.5.2. Material Type

- 19.5.3. Product Type

- 19.5.4. Capacity

- 19.5.5. Design

- 19.5.6. Content Type

- 19.5.7. End Use Industry

- 19.5.8. Distribution Channel

- 19.6. Rest of South America Intermediate Bulk Container Market

- 19.6.1. Country Segmental Analysis

- 19.6.2. Material Type

- 19.6.3. Product Type

- 19.6.4. Capacity

- 19.6.5. Design

- 19.6.6. Content Type

- 19.6.7. End Use Industry

- 19.6.8. Distribution Channel

- 20. Key Players/ Company Profile

- 20.1. Bramlage GmbH

- 20.1.1. Company Details/ Overview

- 20.1.2. Company Financials

- 20.1.3. Key Customers and Competitors

- 20.1.4. Business/ Industry Portfolio

- 20.1.5. Product Portfolio/ Specification Details

- 20.1.6. Pricing Data

- 20.1.7. Strategic Overview

- 20.1.8. Recent Developments

- 20.2. CESA S.p.A.

- 20.3. Cole-Parmer Instrument Company

- 20.4. Crosado Packaging GmbH

- 20.5. Emton Packaging Solutions

- 20.6. FIBCs Inc.

- 20.7. Greif, Inc.

- 20.8. Henshaw Tank & Equipment Co.

- 20.9. Hoover Ferguson Group

- 20.10. Hoover Ferguson U.S.A., Inc.

- 20.11. Infinite Solutions UK Ltd

- 20.12. Korsini Group

- 20.13. Mauser Germany GmbH

- 20.14. Mauser Packaging Solutions

- 20.15. Nefab AB

- 20.16. Peerless Packaging International

- 20.17. ReFood Technologies GmbH

- 20.18. SCHÜTZ GmbH & Co. KGaA

- 20.19. W&P Group

- 20.20. Wefco Packaging, Inc..

- 20.21. Other Key Players

- 20.1. Bramlage GmbH

Note* - This is just tentative list of players. While providing the report, we will cover a greater number of players based on their revenue and share for each geography

Research Design

Our research design integrates both demand-side and supply-side analysis through a balanced combination of primary and secondary research methodologies. By utilizing both bottom-up and top-down approaches alongside rigorous data triangulation methods, we deliver robust market intelligence that supports strategic decision-making.

MarketGenics' comprehensive research design framework ensures the delivery of accurate, reliable, and actionable market intelligence. Through the integration of multiple research approaches, rigorous validation processes, and expert analysis, we provide our clients with the insights needed to make informed strategic decisions and capitalize on market opportunities.

MarketGenics leverages a dedicated industry panel of experts and a comprehensive suite of paid databases to effectively collect, consolidate, and analyze market intelligence.

Our approach has consistently proven to be reliable and effective in generating accurate market insights, identifying key industry trends, and uncovering emerging business opportunities.

Through both primary and secondary research, we capture and analyze critical company-level data such as manufacturing footprints, including technical centers, R&D facilities, sales offices, and headquarters.

Our expert panel further enhances our ability to estimate market size for specific brands based on validated field-level intelligence.

Our data mining techniques incorporate both parametric and non-parametric methods, allowing for structured data collection, sorting, processing, and cleaning.

Demand projections are derived from large-scale data sets analyzed through proprietary algorithms, culminating in robust and reliable market sizing.

Research Approach

The bottom-up approach builds market estimates by starting with the smallest addressable market units and systematically aggregating them to create comprehensive market size projections.

This method begins with specific, granular data points and builds upward to create the complete market landscape.

Customer Analysis → Segmental Analysis → Geographical Analysis

The top-down approach starts with the broadest possible market data and systematically narrows it down through a series of filters and assumptions to arrive at specific market segments or opportunities.

This method begins with the big picture and works downward to increasingly specific market slices.

TAM → SAM → SOM

Research Methods

Desk / Secondary Research

While analysing the market, we extensively study secondary sources, directories, and databases to identify and collect information useful for this technical, market-oriented, and commercial report. Secondary sources that we utilize are not only the public sources, but it is a combination of Open Source, Associations, Paid Databases, MG Repository & Knowledgebase, and others.

- Company websites, annual reports, financial reports, broker reports, and investor presentations

- National government documents, statistical databases and reports

- News articles, press releases and web-casts specific to the companies operating in the market, Magazines, reports, and others

- We gather information from commercial data sources for deriving company specific data such as segmental revenue, share for geography, product revenue, and others

- Internal and external proprietary databases (industry-specific), relevant patent, and regulatory databases

- Governing Bodies, Government Organizations

- Relevant Authorities, Country-specific Associations for Industries

We also employ the model mapping approach to estimate the product level market data through the players' product portfolio

Primary Research

Primary research/ interviews is vital in analyzing the market. Most of the cases involves paid primary interviews. Primary sources include primary interviews through e-mail interactions, telephonic interviews, surveys as well as face-to-face interviews with the different stakeholders across the value chain including several industry experts.

| Type of Respondents | Number of Primaries |

|---|---|

| Tier 2/3 Suppliers | ~20 |

| Tier 1 Suppliers | ~25 |

| End-users | ~25 |

| Industry Expert/ Panel/ Consultant | ~30 |

| Total | ~100 |

MG Knowledgebase

• Repository of industry blog, newsletter and case studies

• Online platform covering detailed market reports, and company profiles

Forecasting Factors and Models

Forecasting Factors

- Historical Trends – Past market patterns, cycles, and major events that shaped how markets behave over time. Understanding past trends helps predict future behavior.

- Industry Factors – Specific characteristics of the industry like structure, regulations, and innovation cycles that affect market dynamics.

- Macroeconomic Factors – Economic conditions like GDP growth, inflation, and employment rates that affect how much money people have to spend.

- Demographic Factors – Population characteristics like age, income, and location that determine who can buy your product.

- Technology Factors – How quickly people adopt new technology and how much technology infrastructure exists.

- Regulatory Factors – Government rules, laws, and policies that can help or restrict market growth.

- Competitive Factors – Analyzing competition structure such as degree of competition and bargaining power of buyers and suppliers.

Forecasting Models / Techniques

Multiple Regression Analysis

- Identify and quantify factors that drive market changes

- Statistical modeling to establish relationships between market drivers and outcomes

Time Series Analysis – Seasonal Patterns

- Understand regular cyclical patterns in market demand

- Advanced statistical techniques to separate trend, seasonal, and irregular components

Time Series Analysis – Trend Analysis

- Identify underlying market growth patterns and momentum

- Statistical analysis of historical data to project future trends

Expert Opinion – Expert Interviews

- Gather deep industry insights and contextual understanding

- In-depth interviews with key industry stakeholders

Multi-Scenario Development

- Prepare for uncertainty by modeling different possible futures

- Creating optimistic, pessimistic, and most likely scenarios

Time Series Analysis – Moving Averages

- Sophisticated forecasting for complex time series data

- Auto-regressive integrated moving average models with seasonal components

Econometric Models

- Apply economic theory to market forecasting

- Sophisticated economic models that account for market interactions

Expert Opinion – Delphi Method

- Harness collective wisdom of industry experts

- Structured, multi-round expert consultation process

Monte Carlo Simulation

- Quantify uncertainty and probability distributions

- Thousands of simulations with varying input parameters

Research Analysis

Our research framework is built upon the fundamental principle of validating market intelligence from both demand and supply perspectives. This dual-sided approach ensures comprehensive market understanding and reduces the risk of single-source bias.

Demand-Side Analysis: We understand end-user/application behavior, preferences, and market needs along with the penetration of the product for specific application.

Supply-Side Analysis: We estimate overall market revenue, analyze the segmental share along with industry capacity, competitive landscape, and market structure.

Validation & Evaluation

Data triangulation is a validation technique that uses multiple methods, sources, or perspectives to examine the same research question, thereby increasing the credibility and reliability of research findings. In market research, triangulation serves as a quality assurance mechanism that helps identify and minimize bias, validate assumptions, and ensure accuracy in market estimates.

- Data Source Triangulation – Using multiple data sources to examine the same phenomenon

- Methodological Triangulation – Using multiple research methods to study the same research question

- Investigator Triangulation – Using multiple researchers or analysts to examine the same data

- Theoretical Triangulation – Using multiple theoretical perspectives to interpret the same data

Custom Market Research Services

We will customise the research for you, in case the report listed above does not meet your requirements.

Get 10% Free Customisation