Fitness Equipment Market Size, Share & Trends Analysis Report by Product Type (Cardiovascular Training Equipment, Strength Training Equipment, Fitness Accessories), Material Type, Distribution Channel, End-user, and Geography (North America, Europe, Asia Pacific, Middle East, Africa, and South America) – Global Industry Data, Trends, and Forecasts, 2026–2035

Market Overview:

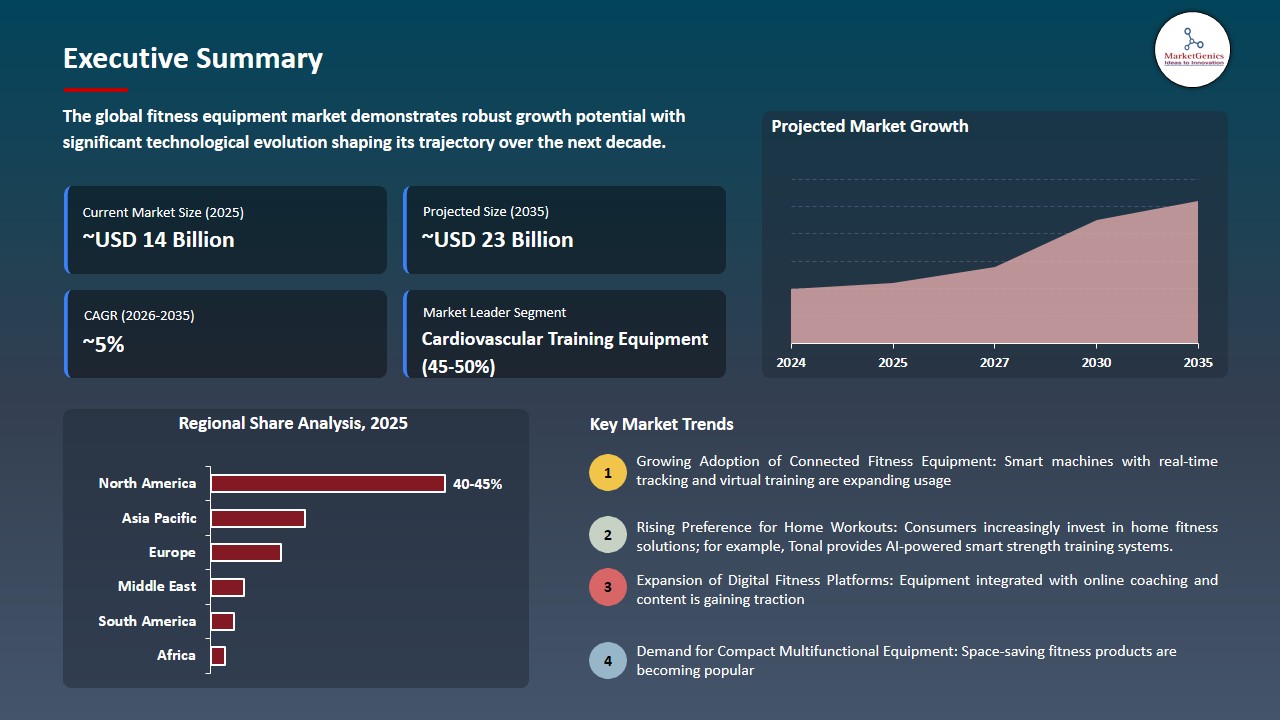

According to Marketgenics analysis, the global fitness equipment market is experiencing steady growth, with a valuation of approximately USD 14.2 billion in 2025 and is projected to reach nearly USD 22.5 billion by 2035, expanding at a CAGR of around 4.7% during the forecast period.

|

|

|

Segmental Data Insights |

|

|

Demand Trends |

|

|

Competitive Landscape |

|

|

Strategic Development |

|

|

Future Outlook & Opportunities |

|

Fitness Equipment Market Size, Share, and Growth

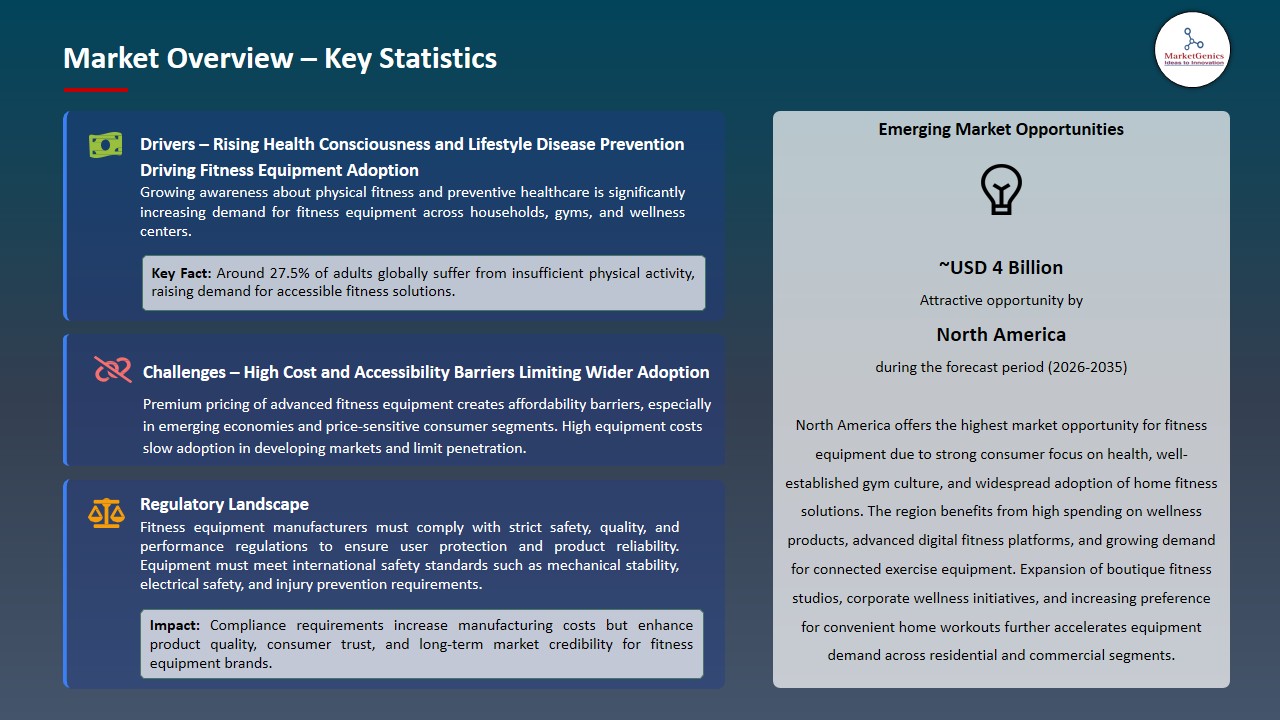

Asia Pacific is the fastest-growing due to rapid urbanization, rising disposable incomes, expanding middle-class population, increasing gym and health club penetration, and growing awareness of preventive healthcare and active lifestyles.

Peter Stern, Peloton CEO, said, "We're doubling the value of our hardware with the Cross-Training Series by delivering world-class cardio and strength in a single machine. With Peloton IQ, we're introducing a new level of intelligent personalization to become the ultimate partner in our Members' wellness journeys. This is more than an upgrade; it's a relaunch"

The growth in health awareness, the escalating obesity cases and the transition to preventive care is fueling an expedited uptake of fitness equipment both at home and in commercial environments, which is being aided by the digital connection and the interconnected training environment. The smart and interactive product portfolios are becoming bigger to attract the needs of personalized workouts, and hybrid fitness model.

In October 2025, Peloton Interactive, Inc. launched improved connected strength and cardio offering better content and AI-based training capabilities to reinforce its equipment environment based on subscriptions. Johnson health tech Co. introduced new Matrix and Horizon with treadmills and connected strength systems as an extension of the existing lines to the commercial gyms and high-end home customers. These are enhancing faster replacement cycles of equipment and increasing recurring revenue capabilities via connected and subscription-based fitness ecosystems.

Adjacent opportunities to the fitness equipment market include connected fitness software platforms, wearable fitness tracking devices, corporate wellness programs, physiotherapy and rehabilitation equipment, and smart home wellness ecosystems integrating AI-driven coaching and health monitoring. These segments complement equipment demand through data-driven engagement and preventive care integration.

Fitness Equipment Market Dynamics and Trends

Driver: Rapid Expansion of Corporate Wellness Infrastructure and Institutional Fitness Integration

-

The rapid growth of corporate fitness facilities and institutional fitness incorporation is increasing the needs of commercial fitness equipment at the corporate offices, universities, and healthcare centers, and hotel and hospital settings. Organizations are giving emphasis on employee and user wellness in order to enhance productivity, save healthcare expenses and enhance engagement with organized access to fitness.

- This trend is not only leading to massive deployment of long-life cardio and strength training units that are intended to be used repeatedly by multiple individuals but also facilitating long-term facility upgrades and wellness-based infrastructure expansion in an institutional setting.

- Technogym S.p.A. introduced its Healthness ecosystem in 2025 using the power of AI-based accuracy training and connected devices to connect 25 million users with corporate, healthcare, and wellness operators, reinforcing the use of institutional fitness.

- The tendency is the acceleration of institutional procurement of activity cycles and high, consistent demand of commercial fitness equipment in the corporate and healthcare market.

Restraint: High Equipment Acquisition Costs and Replacement Investment Burden Limiting Adoption

-

High cost of equipment acquisition and replacement investment mainly is a limiting factor especially on small gyms, independent operations and low-cost institutional purchasers. Commercial cardio and strength machines would demand hefty initial investments, and additional costs of installation, upgrading of the facility, and long service contracts, adding to overall ownership costs.

- Other periodic reinvestments need to be made to maintain performance, safety, and digital compatibility especially as linked and technology-enabled systems assume a leading role in the industry. Such financial strains postpone the decision-making processes of procurement, limit expansion strategies, and motivate certain operators to operate equipment beyond the best lifecycle levels, further decelerating market penetration and growth of new equipment sales.

- High capital and replacement expense is decelerating the purchase and adoption of new equipment, especially in the case of small and mid-sized fitness operator.

Opportunity: Integration of Fitness Equipment with Preventive Healthcare and Rehabilitation Ecosystems

-

Rapid adoption of artificial intelligence-assisted personalized and connected training equipment is changing the fitness equipment sector as it can generate data and customized workout experiences based on it. Smart machines with sensors, cloud communication and AI algorithms evaluate the performance of the user and automatically change the resistance, speed, and the intensity of the training to achieve the best results.

- There is also a growing trend towards enhancing integration with mobile apps and digital coaching tools whereby users can access bespoke workout plans, real-time feedback, and remote coaching and training both at home and commercial fitness settings.

- In 2025, iFIT Inc. will launch its iFIT AI Coach in 19 countries based on machine learning and user performance data, and provide hyper-personalized training programs and real-time feedback based on NordicTrack and Proform connected fitness devices.

- AI-powered interaction and personalization are growing user interaction, expediating uptake of smart equipment, and recurring digital fitness ecosystem earnings.

Key Trend: Accelerating Adoption of Artificial Intelligence Enabled Personalized and Connected Training Equipment Solutions

-

Accelerating adoption of artificial intelligence–enabled personalized and connected training equipment is transforming the fitness equipment industry by enabling data-driven and adaptive workout experiences. Smart machines equipped with sensors, cloud connectivity, and AI algorithms analyze user performance and automatically adjust resistance, speed, and training intensity to optimize results.

- This trend is also strengthening integration with mobile applications and digital coaching platforms, allowing users to access personalized workout plans, real-time feedback, and remote training support across both home and commercial fitness environments.

- For instance, in 2025, iFIT Inc. expanded its iFIT AI Coach across 19 countries, using machine learning and user performance data to deliver hyper-personalized training plans and real-time feedback integrated with NordicTrack and ProForm connected fitness equipment.

- AI-enabled personalization and connectivity are increasing user engagement, accelerating smart equipment adoption, and driving recurring digital fitness ecosystem revenues.

Fitness Equipment Market Analysis and Segmental Data

Cardiovascular Training Equipment Dominate Global Fitness Equipment Market

-

Cardiovascular training equipment takes the leading position in the global fitness equipment market because it is significantly important in enhancing the health of the heart, stamina, and caloric burning. Treadmills, stationary bikes, ellipticals and rowing machine are examples of equipment that are commonly found in commercial gyms, fitness studios, hotels, and home fitness systems since they facilitate effective aerobic exercises to users of all fitness levels.

- Additional factor is the growing health awareness, obesity concerns and the rising demand of weight management solutions among the segment. Also, the manufacturers are adopting new technologies, including AI-based training apps, cardiovascular monitors, interactive screens, and connected fitness platforms to increase the user engagement and provide them with customized workout experiences.

- The high level of consumer preference of cardio exercises and the constant technological boosts are maintaining the dominant portion of the segment in the global fitness equipment market.

North America Leads Global Fitness Equipment Market Demand

-

North America dominates the world in the fitness equipment market because of good health and wellness awareness, high disposable income, and the extensive involvement in fitness activities. The area already has an extensive chain of business gyms, boutique fitness studios, and corporate fitness centers engaged in constant investment in the modern system of fitness equipment to improve the experience of the users and the effectiveness of training.

- The strong presence of large fitness equipment manufacturers, high rates of adoption of connected and smart fitness technologies, increasing demand of home fitness solutions all support the market. There are also rising obesity issues and the government programs that spread active lifestyles are also motivating people to do some physical exercises, which, in turn, will push the cardio and strength training equipment demand on the residential and commercial market.

- North America remains the fitness equipment market leader with strong fitness culture, superior infrastructure and quick uptake of connected fitness technologies.

Fitness Equipment Market Ecosystem

The global fitness equipment market is moderately consolidated, with leading players including Technogym S.p.A., Life Fitness / Hammer Strength, iFIT Inc., Johnson Health Tech Co., Ltd., and Peloton Interactive, Inc. These companies ensure competitive advantage due to high product engineering, robust commercial gym relationships, integrated digital fitness, and global distribution channels. Their leadership is strengthened by the sustained investment in the related fitness technologies, AI-based training, engaging workout content, and digital training ecosystems through subscription.

The value chain of the fitness equipment consists of sourcing of raw materials (steel frames, electronics, sensors, and displays), product design and engineering, the fabrication of the equipment, the integration of the software and the digital platform, distribution of the equipment via commercial gyms and retail outlets, and after sales services. Connected training plans, virtual trainings, performance analytics, and equipment maintenance programs are examples of post-purchase services that help increase user engagement and recurring revenue streams on a long-term basis.

The barriers to entry are high since brand loyalty is high, the engineering factors are high, the training platforms are proprietary and a lot is invested on product innovation as well as global distribution infrastructure. The ongoing advancement of AI-based training applications, full-body digital exercise, the network of connected devices, and custom fitness apps is facilitating product differentiation, improving customer retention, and promoting the long-term growth of the global fitness equipment sector.

Recent Development and Strategic Overview:

-

In March 2026, Jerai Fitness Limited partnered with Plus Fitness India to roll out 100 gyms across India, introducing an integrated franchise and equipment model that simplifies gym setup, supports domestic equipment manufacturing, and accelerates expansion of standardized fitness infrastructure nationwide.

- In September 2025, Eleiko Group AB introduced its next-generation barbells with sensor integration capability, enabling performance data tracking for lifters and coaches, while incorporating durability innovations such as a Force Redistribution System and manufacturing using 97% recycled steel with fossil-free energy.

Report Scope

|

Detail |

|

|

Market Size in 2025 |

USD 14.2 Bn |

|

Market Forecast Value in 2035 |

USD 22.5 Bn |

|

Growth Rate (CAGR) |

4.7% |

|

Forecast Period |

2026 – 2035 |

|

Historical Data Available for |

2021 – 2024 |

|

Market Size Units |

US$ Billion for Value Thousand Units for Volume |

|

Report Format |

Electronic (PDF) + Excel |

|

North America |

Europe |

Asia Pacific |

Middle East |

Africa |

South America |

|

|

|

|

|

|

|

Companies Covered |

|||||

|

|

|

|

|

|

Fitness Equipment Market Segmentation and Highlights

|

Segment |

Sub-segment |

|

Fitness Equipment Market, By Product Type |

|

|

Fitness Equipment Market, By Material Type |

|

|

Fitness Equipment Market, By Distribution Channel |

|

|

Fitness Equipment Market, By End-User |

|

Frequently Asked Questions

Table of Contents

- 1. Research Methodology and Assumptions

- 1.1. Definitions

- 1.2. Research Design and Approach

- 1.3. Data Collection Methods

- 1.4. Base Estimates and Calculations

- 1.5. Forecasting Models

- 1.5.1. Key Forecast Factors & Impact Analysis

- 1.6. Secondary Research

- 1.6.1. Open Sources

- 1.6.2. Paid Databases

- 1.6.3. Associations

- 1.7. Primary Research

- 1.7.1. Primary Sources

- 1.7.2. Primary Interviews with Stakeholders across Ecosystem

- 2. Executive Summary

- 2.1. Global Fitness Equipment Market Outlook

- 2.1.1. Fitness Equipment Market Size (Volume (Thousand Units) and Value (US$ Bn)), and Forecasts, 2021-2035

- 2.1.2. Compounded Annual Growth Rate Analysis

- 2.1.3. Growth Opportunity Analysis

- 2.1.4. Segmental Share Analysis

- 2.1.5. Geographical Share Analysis

- 2.2. Market Analysis and Facts

- 2.3. Supply-Demand Analysis

- 2.4. Competitive Benchmarking

- 2.5. Go-to- Market Strategy

- 2.5.1. Customer/ End-use Industry Assessment

- 2.5.2. Growth Opportunity Data, 2026-2035

- 2.5.2.1. Regional Data

- 2.5.2.2. Country Data

- 2.5.2.3. Segmental Data

- 2.5.3. Identification of Potential Market Spaces

- 2.5.4. GAP Analysis

- 2.5.5. Potential Attractive Price Points

- 2.5.6. Prevailing Market Risks & Challenges

- 2.5.7. Preferred Sales & Marketing Strategies

- 2.5.8. Key Recommendations and Analysis

- 2.5.9. A Way Forward

- 2.1. Global Fitness Equipment Market Outlook

- 3. Industry Data and Premium Insights

- 3.1. Global Consumer Goods & Services Industry Overview, 2025

- 3.1.1. Consumer Goods & Services Industry Ecosystem Analysis

- 3.1.2. Key Trends for Consumer Goods & Services Industry

- 3.1.3. Regional Distribution for Consumer Goods & Services Industry

- 3.2. Supplier Customer Data

- 3.3. Technology Roadmap and Developments

- 3.4. Trade Analysis

- 3.4.1. Import & Export Analysis, 2025

- 3.4.2. Top Importing Countries

- 3.4.3. Top Exporting Countries

- 3.5. Trump Tariff Impact Analysis

- 3.5.1. Manufacturer

- 3.5.1.1. Based on the component & Raw material

- 3.5.2. Supply Chain

- 3.5.3. End Consumer

- 3.5.1. Manufacturer

- 3.6. Raw Material Analysis

- 3.1. Global Consumer Goods & Services Industry Overview, 2025

- 4. Market Overview

- 4.1. Market Dynamics

- 4.1.1. Drivers

- 4.1.1.1. Rising health awareness and increasing adoption of home and commercial fitness routines.

- 4.1.1.2. Growing demand for connected and smart fitness equipment with tracking capabilities.

- 4.1.1.3. Expansion of gyms, wellness centers, and corporate fitness programs globally.

- 4.1.2. Restraints

- 4.1.2.1. High equipment costs limiting affordability for some consumer segments.

- 4.1.2.2. Market saturation in developed regions and competition from digital fitness apps.

- 4.1.1. Drivers

- 4.2. Key Trend Analysis

- 4.3. Regulatory Framework

- 4.3.1. Key Regulations, Norms, and Subsidies, by Key Countries

- 4.3.2. Tariffs and Standards

- 4.3.3. Impact Analysis of Regulations on the Market

- 4.4. Value Chain Analysis

- 4.4.1. Raw Material & Component Suppliers

- 4.4.2. Equipment Manufacturers / OEMs

- 4.4.3. Distributors & Wholesalers

- 4.4.4. End Users

- 4.5. Cost Structure Analysis

- 4.5.1. Parameter’s Share for Cost Associated

- 4.5.2. COGP vs COGS

- 4.5.3. Profit Margin Analysis

- 4.6. Pricing Analysis

- 4.6.1. Regional Pricing Analysis

- 4.6.2. Segmental Pricing Trends

- 4.6.3. Factors Influencing Pricing

- 4.7. Porter’s Five Forces Analysis

- 4.8. PESTEL Analysis

- 4.9. Global Fitness Equipment Market Demand

- 4.9.1. Historical Market Size – Volume (Thousand Units) and Value (US$ Bn), 2020-2024

- 4.9.2. Current and Future Market Size – Volume (Thousand Units) and Value (US$ Bn), 2026–2035

- 4.9.2.1. Y-o-Y Growth Trends

- 4.9.2.2. Absolute $ Opportunity Assessment

- 4.1. Market Dynamics

- 5. Competition Landscape

- 5.1. Competition structure

- 5.1.1. Fragmented v/s consolidated

- 5.2. Company Share Analysis, 2025

- 5.2.1. Global Company Market Share

- 5.2.2. By Region

- 5.2.2.1. North America

- 5.2.2.2. Europe

- 5.2.2.3. Asia Pacific

- 5.2.2.4. Middle East

- 5.2.2.5. Africa

- 5.2.2.6. South America

- 5.3. Product Comparison Matrix

- 5.3.1. Specifications

- 5.3.2. Market Positioning

- 5.3.3. Pricing

- 5.1. Competition structure

- 6. Global Fitness Equipment Market Analysis, by Product Type

- 6.1. Key Segment Analysis

- 6.2. Fitness Equipment Market Size (Volume (Thousand Units) and Value (US$ Bn)), Analysis, and Forecasts, by Product Type, 2021-2035

- 6.2.1. Cardiovascular Training Equipment

- 6.2.1.1. Treadmills

- 6.2.1.2. Elliptical Trainers

- 6.2.1.3. Stationary Bikes

- 6.2.1.4. Rowing Machines

- 6.2.1.5. Stair Steppers

- 6.2.1.6. Others

- 6.2.2. Strength Training Equipment

- 6.2.2.1. Free Weights (Dumbbells, Barbells, Kettlebells)

- 6.2.2.2. Weight Machines

- 6.2.2.3. Resistance Bands

- 6.2.2.4. Power Racks & Cages

- 6.2.2.5. Benches

- 6.2.2.6. Others

- 6.2.3. Fitness Accessories

- 6.2.3.1. Yoga Mats

- 6.2.3.2. Foam Rollers

- 6.2.3.3. Exercise Balls

- 6.2.3.4. Jump Ropes

- 6.2.3.5. Resistance Tubes

- 6.2.3.6. Others

- 6.2.1. Cardiovascular Training Equipment

- 7. Global Fitness Equipment Market Analysis, by Material Type

- 7.1. Key Segment Analysis

- 7.2. Fitness Equipment Market Size (Volume (Thousand Units) and Value (US$ Bn)), Analysis, and Forecasts, by Material Type, 2021-2035

- 7.2.1. Metal

- 7.2.2. Plastic/Polymer

- 7.2.3. Composite Materials

- 7.2.4. Natural Materials (Wood, Cork, Rubber)

- 8. Global Fitness Equipment Market Analysis, by Distribution Channel

- 8.1. Key Segment Analysis

- 8.2. Fitness Equipment Market Size (Volume (Thousand Units) and Value (US$ Bn)), Analysis, and Forecasts, by Distribution Channel, 2021-2035

- 8.2.1. Online

- 8.2.1.1. Company Websites

- 8.2.1.2. Fitness Equipment Platforms

- 8.2.2. Offline

- 8.2.2.1. Sporting Goods Stores

- 8.2.2.2. Department Stores

- 8.2.2.3. Hypermarkets/Supermarkets

- 8.2.2.4. Direct Sales

- 8.2.1. Online

- 9. Global Fitness Equipment Market Analysis, by End-User

- 9.1. Key Segment Analysis

- 9.2. Fitness Equipment Market Size (Volume (Thousand Units) and Value (US$ Bn)), Analysis, and Forecasts, by End-User, 2021-2035

- 9.2.1. Hospitality Industry

- 9.2.1.1. Hotels

- 9.2.1.2. Resorts

- 9.2.1.3. Cruise Ships

- 9.2.1.4. Others

- 9.2.2. Corporate Wellness Programs

- 9.2.3. Educational Institutions

- 9.2.3.1. Schools

- 9.2.3.2. Colleges & Universities

- 9.2.4. Fitness & Health Clubs

- 9.2.4.1. Boutique Studios

- 9.2.4.2. Large Gym Chains

- 9.2.4.3. Personal Training Studios

- 9.2.4.4. Others

- 9.2.5. Sports Training Facilities

- 9.2.6. Government & Military Facilities

- 9.2.7. Residential/Home Fitness

- 9.2.1. Hospitality Industry

- 10. Global Fitness Equipment Market Analysis and Forecasts, by Region

- 10.1. Key Findings

- 10.2. Fitness Equipment Market Size (Volume (Thousand Units) and Value (US$ Bn)), Analysis, and Forecasts, by Region, 2021-2035

- 10.2.1. North America

- 10.2.2. Europe

- 10.2.3. Asia Pacific

- 10.2.4. Middle East

- 10.2.5. Africa

- 10.2.6. South America

- 11. North America Fitness Equipment Market Analysis

- 11.1. Key Segment Analysis

- 11.2. Regional Snapshot

- 11.3. North America Fitness Equipment Market Size (Volume (Thousand Units) and Value (US$ Bn)), Analysis, and Forecasts, 2021-2035

- 11.3.1. Product Type

- 11.3.2. Material Type

- 11.3.3. Distribution Channel

- 11.3.4. End-User

- 11.3.5. Country

- 11.3.5.1. USA

- 11.3.5.2. Canada

- 11.3.5.3. Mexico

- 11.4. USA Fitness Equipment Market

- 11.4.1. Country Segmental Analysis

- 11.4.2. Product Type

- 11.4.3. Material Type

- 11.4.4. Distribution Channel

- 11.4.5. End-User

- 11.5. Canada Fitness Equipment Market

- 11.5.1. Country Segmental Analysis

- 11.5.2. Product Type

- 11.5.3. Material Type

- 11.5.4. Distribution Channel

- 11.5.5. End-User

- 11.6. Mexico Fitness Equipment Market

- 11.6.1. Country Segmental Analysis

- 11.6.2. Product Type

- 11.6.3. Material Type

- 11.6.4. Distribution Channel

- 11.6.5. End-User

- 12. Europe Fitness Equipment Market Analysis

- 12.1. Key Segment Analysis

- 12.2. Regional Snapshot

- 12.3. Europe Fitness Equipment Market Size (Volume (Thousand Units) and Value (US$ Bn)), Analysis, and Forecasts, 2021-2035

- 12.3.1. Product Type

- 12.3.2. Material Type

- 12.3.3. Distribution Channel

- 12.3.4. End-User

- 12.3.5. Country

- 12.3.5.1. Germany

- 12.3.5.2. United Kingdom

- 12.3.5.3. France

- 12.3.5.4. Italy

- 12.3.5.5. Spain

- 12.3.5.6. Netherlands

- 12.3.5.7. Nordic Countries

- 12.3.5.8. Poland

- 12.3.5.9. Russia & CIS

- 12.3.5.10. Rest of Europe

- 12.4. Germany Fitness Equipment Market

- 12.4.1. Country Segmental Analysis

- 12.4.2. Product Type

- 12.4.3. Material Type

- 12.4.4. Distribution Channel

- 12.4.5. End-User

- 12.5. United Kingdom Fitness Equipment Market

- 12.5.1. Country Segmental Analysis

- 12.5.2. Product Type

- 12.5.3. Material Type

- 12.5.4. Distribution Channel

- 12.5.5. End-User

- 12.6. France Fitness Equipment Market

- 12.6.1. Country Segmental Analysis

- 12.6.2. Product Type

- 12.6.3. Material Type

- 12.6.4. Distribution Channel

- 12.6.5. End-User

- 12.7. Italy Fitness Equipment Market

- 12.7.1. Country Segmental Analysis

- 12.7.2. Product Type

- 12.7.3. Material Type

- 12.7.4. Distribution Channel

- 12.7.5. End-User

- 12.8. Spain Fitness Equipment Market

- 12.8.1. Country Segmental Analysis

- 12.8.2. Product Type

- 12.8.3. Material Type

- 12.8.4. Distribution Channel

- 12.8.5. End-User

- 12.9. Netherlands Fitness Equipment Market

- 12.9.1. Country Segmental Analysis

- 12.9.2. Product Type

- 12.9.3. Material Type

- 12.9.4. Distribution Channel

- 12.9.5. End-User

- 12.10. Nordic Countries Fitness Equipment Market

- 12.10.1. Country Segmental Analysis

- 12.10.2. Product Type

- 12.10.3. Material Type

- 12.10.4. Distribution Channel

- 12.10.5. End-User

- 12.11. Poland Fitness Equipment Market

- 12.11.1. Country Segmental Analysis

- 12.11.2. Product Type

- 12.11.3. Material Type

- 12.11.4. Distribution Channel

- 12.11.5. End-User

- 12.12. Russia & CIS Fitness Equipment Market

- 12.12.1. Country Segmental Analysis

- 12.12.2. Product Type

- 12.12.3. Material Type

- 12.12.4. Distribution Channel

- 12.12.5. End-User

- 12.13. Rest of Europe Fitness Equipment Market

- 12.13.1. Country Segmental Analysis

- 12.13.2. Product Type

- 12.13.3. Material Type

- 12.13.4. Distribution Channel

- 12.13.5. End-User

- 13. Asia Pacific Fitness Equipment Market Analysis

- 13.1. Key Segment Analysis

- 13.2. Regional Snapshot

- 13.3. Asia Pacific Fitness Equipment Market Size (Volume (Thousand Units) and Value (US$ Bn)), Analysis, and Forecasts, 2021-2035

- 13.3.1. Product Type

- 13.3.2. Material Type

- 13.3.3. Distribution Channel

- 13.3.4. End-User

- 13.3.5. Country

- 13.3.5.1. China

- 13.3.5.2. India

- 13.3.5.3. Japan

- 13.3.5.4. South Korea

- 13.3.5.5. Australia and New Zealand

- 13.3.5.6. Indonesia

- 13.3.5.7. Malaysia

- 13.3.5.8. Thailand

- 13.3.5.9. Vietnam

- 13.3.5.10. Rest of Asia Pacific

- 13.4. China Fitness Equipment Market

- 13.4.1. Country Segmental Analysis

- 13.4.2. Product Type

- 13.4.3. Material Type

- 13.4.4. Distribution Channel

- 13.4.5. End-User

- 13.5. India Fitness Equipment Market

- 13.5.1. Country Segmental Analysis

- 13.5.2. Product Type

- 13.5.3. Material Type

- 13.5.4. Distribution Channel

- 13.5.5. End-User

- 13.6. Japan Fitness Equipment Market

- 13.6.1. Country Segmental Analysis

- 13.6.2. Product Type

- 13.6.3. Material Type

- 13.6.4. Distribution Channel

- 13.6.5. End-User

- 13.7. South Korea Fitness Equipment Market

- 13.7.1. Country Segmental Analysis

- 13.7.2. Product Type

- 13.7.3. Material Type

- 13.7.4. Distribution Channel

- 13.7.5. End-User

- 13.8. Australia and New Zealand Fitness Equipment Market

- 13.8.1. Country Segmental Analysis

- 13.8.2. Product Type

- 13.8.3. Material Type

- 13.8.4. Distribution Channel

- 13.8.5. End-User

- 13.9. Indonesia Fitness Equipment Market

- 13.9.1. Country Segmental Analysis

- 13.9.2. Product Type

- 13.9.3. Material Type

- 13.9.4. Distribution Channel

- 13.9.5. End-User

- 13.10. Malaysia Fitness Equipment Market

- 13.10.1. Country Segmental Analysis

- 13.10.2. Product Type

- 13.10.3. Material Type

- 13.10.4. Distribution Channel

- 13.10.5. End-User

- 13.11. Thailand Fitness Equipment Market

- 13.11.1. Country Segmental Analysis

- 13.11.2. Product Type

- 13.11.3. Material Type

- 13.11.4. Distribution Channel

- 13.11.5. End-User

- 13.12. Vietnam Fitness Equipment Market

- 13.12.1. Country Segmental Analysis

- 13.12.2. Product Type

- 13.12.3. Material Type

- 13.12.4. Distribution Channel

- 13.12.5. End-User

- 13.13. Rest of Asia Pacific Fitness Equipment Market

- 13.13.1. Country Segmental Analysis

- 13.13.2. Product Type

- 13.13.3. Material Type

- 13.13.4. Distribution Channel

- 13.13.5. End-User

- 14. Middle East Fitness Equipment Market Analysis

- 14.1. Key Segment Analysis

- 14.2. Regional Snapshot

- 14.3. Middle East Fitness Equipment Market Size (Volume (Thousand Units) and Value (US$ Bn)), Analysis, and Forecasts, 2021-2035

- 14.3.1. Product Type

- 14.3.2. Material Type

- 14.3.3. Distribution Channel

- 14.3.4. End-User

- 14.3.5. Country

- 14.3.5.1. Turkey

- 14.3.5.2. UAE

- 14.3.5.3. Saudi Arabia

- 14.3.5.4. Israel

- 14.3.5.5. Rest of Middle East

- 14.4. Turkey Fitness Equipment Market

- 14.4.1. Country Segmental Analysis

- 14.4.2. Product Type

- 14.4.3. Material Type

- 14.4.4. Distribution Channel

- 14.4.5. End-User

- 14.5. UAE Fitness Equipment Market

- 14.5.1. Country Segmental Analysis

- 14.5.2. Product Type

- 14.5.3. Material Type

- 14.5.4. Distribution Channel

- 14.5.5. End-User

- 14.6. Saudi Arabia Fitness Equipment Market

- 14.6.1. Country Segmental Analysis

- 14.6.2. Product Type

- 14.6.3. Material Type

- 14.6.4. Distribution Channel

- 14.6.5. End-User

- 14.7. Israel Fitness Equipment Market

- 14.7.1. Country Segmental Analysis

- 14.7.2. Product Type

- 14.7.3. Material Type

- 14.7.4. Distribution Channel

- 14.7.5. End-User

- 14.8. Rest of Middle East Fitness Equipment Market

- 14.8.1. Country Segmental Analysis

- 14.8.2. Product Type

- 14.8.3. Material Type

- 14.8.4. Distribution Channel

- 14.8.5. End-User

- 15. Africa Fitness Equipment Market Analysis

- 15.1. Key Segment Analysis

- 15.2. Regional Snapshot

- 15.3. Africa Fitness Equipment Market Size (Volume (Thousand Units) and Value (US$ Bn)), Analysis, and Forecasts, 2021-2035

- 15.3.1. Product Type

- 15.3.2. Material Type

- 15.3.3. Distribution Channel

- 15.3.4. End-User

- 15.3.5. Country

- 15.3.5.1. South Africa

- 15.3.5.2. Egypt

- 15.3.5.3. Nigeria

- 15.3.5.4. Algeria

- 15.3.5.5. Rest of Africa

- 15.4. South Africa Fitness Equipment Market

- 15.4.1. Country Segmental Analysis

- 15.4.2. Product Type

- 15.4.3. Material Type

- 15.4.4. Distribution Channel

- 15.4.5. End-User

- 15.5. Egypt Fitness Equipment Market

- 15.5.1. Country Segmental Analysis

- 15.5.2. Product Type

- 15.5.3. Material Type

- 15.5.4. Distribution Channel

- 15.5.5. End-User

- 15.6. Nigeria Fitness Equipment Market

- 15.6.1. Country Segmental Analysis

- 15.6.2. Product Type

- 15.6.3. Material Type

- 15.6.4. Distribution Channel

- 15.6.5. End-User

- 15.7. Algeria Fitness Equipment Market

- 15.7.1. Country Segmental Analysis

- 15.7.2. Product Type

- 15.7.3. Material Type

- 15.7.4. Distribution Channel

- 15.7.5. End-User

- 15.8. Rest of Africa Fitness Equipment Market

- 15.8.1. Country Segmental Analysis

- 15.8.2. Product Type

- 15.8.3. Material Type

- 15.8.4. Distribution Channel

- 15.8.5. End-User

- 16. South America Fitness Equipment Market Analysis

- 16.1. Key Segment Analysis

- 16.2. Regional Snapshot

- 16.3. South America Fitness Equipment Market Size (Volume (Thousand Units) and Value (US$ Bn)), Analysis, and Forecasts, 2021-2035

- 16.3.1. Product Type

- 16.3.2. Material Type

- 16.3.3. Distribution Channel

- 16.3.4. End-User

- 16.3.5. Country

- 16.3.5.1. Brazil

- 16.3.5.2. Argentina

- 16.3.5.3. Rest of South America

- 16.4. Brazil Fitness Equipment Market

- 16.4.1. Country Segmental Analysis

- 16.4.2. Product Type

- 16.4.3. Material Type

- 16.4.4. Distribution Channel

- 16.4.5. End-User

- 16.5. Argentina Fitness Equipment Market

- 16.5.1. Country Segmental Analysis

- 16.5.2. Product Type

- 16.5.3. Material Type

- 16.5.4. Distribution Channel

- 16.5.5. End-User

- 16.6. Rest of South America Fitness Equipment Market

- 16.6.1. Country Segmental Analysis

- 16.6.2. Product Type

- 16.6.3. Material Type

- 16.6.4. Distribution Channel

- 16.6.5. End-User

- 17. Key Players/ Company Profile

- 17.1. Body-Solid, Inc.

- 17.1.1. Company Details/ Overview

- 17.1.2. Company Financials

- 17.1.3. Key Customers and Competitors

- 17.1.4. Business/ Industry Portfolio

- 17.1.5. Product Portfolio/ Specification Details

- 17.1.6. Pricing Data

- 17.1.7. Strategic Overview

- 17.1.8. Recent Developments

- 17.2. BowFlex, Inc.

- 17.3. Concept2, Inc.

- 17.4. Core Health & Fitness, LLC

- 17.5. Cybex International

- 17.6. HOIST Fitness Systems

- 17.7. ICON Health & Fitness

- 17.8. Johnson Health Tech

- 17.9. Keiser Corporation

- 17.10. Life Fitness / Hammer Strength

- 17.11. Matrix Fitness

- 17.12. Nautilus, Inc.

- 17.13. NordicTrack

- 17.14. Octane Fitness

- 17.15. Peloton Interactive

- 17.16. Precor Incorporated

- 17.17. Rogue Fitness

- 17.18. Technogym S.p.A.

- 17.19. TRUE Fitness Technology

- 17.20. Other Key Players

- 17.1. Body-Solid, Inc.

Note* - This is just tentative list of players. While providing the report, we will cover more number of players based on their revenue and share for each geography

Research Design

Our research design integrates both demand-side and supply-side analysis through a balanced combination of primary and secondary research methodologies. By utilizing both bottom-up and top-down approaches alongside rigorous data triangulation methods, we deliver robust market intelligence that supports strategic decision-making.

MarketGenics' comprehensive research design framework ensures the delivery of accurate, reliable, and actionable market intelligence. Through the integration of multiple research approaches, rigorous validation processes, and expert analysis, we provide our clients with the insights needed to make informed strategic decisions and capitalize on market opportunities.

MarketGenics leverages a dedicated industry panel of experts and a comprehensive suite of paid databases to effectively collect, consolidate, and analyze market intelligence.

Our approach has consistently proven to be reliable and effective in generating accurate market insights, identifying key industry trends, and uncovering emerging business opportunities.

Through both primary and secondary research, we capture and analyze critical company-level data such as manufacturing footprints, including technical centers, R&D facilities, sales offices, and headquarters.

Our expert panel further enhances our ability to estimate market size for specific brands based on validated field-level intelligence.

Our data mining techniques incorporate both parametric and non-parametric methods, allowing for structured data collection, sorting, processing, and cleaning.

Demand projections are derived from large-scale data sets analyzed through proprietary algorithms, culminating in robust and reliable market sizing.

Research Approach

The bottom-up approach builds market estimates by starting with the smallest addressable market units and systematically aggregating them to create comprehensive market size projections.

This method begins with specific, granular data points and builds upward to create the complete market landscape.

Customer Analysis → Segmental Analysis → Geographical Analysis

The top-down approach starts with the broadest possible market data and systematically narrows it down through a series of filters and assumptions to arrive at specific market segments or opportunities.

This method begins with the big picture and works downward to increasingly specific market slices.

TAM → SAM → SOM

Research Methods

Desk / Secondary Research

While analysing the market, we extensively study secondary sources, directories, and databases to identify and collect information useful for this technical, market-oriented, and commercial report. Secondary sources that we utilize are not only the public sources, but it is a combination of Open Source, Associations, Paid Databases, MG Repository & Knowledgebase, and others.

- Company websites, annual reports, financial reports, broker reports, and investor presentations

- National government documents, statistical databases and reports

- News articles, press releases and web-casts specific to the companies operating in the market, Magazines, reports, and others

- We gather information from commercial data sources for deriving company specific data such as segmental revenue, share for geography, product revenue, and others

- Internal and external proprietary databases (industry-specific), relevant patent, and regulatory databases

- Governing Bodies, Government Organizations

- Relevant Authorities, Country-specific Associations for Industries

We also employ the model mapping approach to estimate the product level market data through the players' product portfolio

Primary Research

Primary research/ interviews is vital in analyzing the market. Most of the cases involves paid primary interviews. Primary sources include primary interviews through e-mail interactions, telephonic interviews, surveys as well as face-to-face interviews with the different stakeholders across the value chain including several industry experts.

| Type of Respondents | Number of Primaries |

|---|---|

| Tier 2/3 Suppliers | ~20 |

| Tier 1 Suppliers | ~25 |

| End-users | ~25 |

| Industry Expert/ Panel/ Consultant | ~30 |

| Total | ~100 |

MG Knowledgebase

• Repository of industry blog, newsletter and case studies

• Online platform covering detailed market reports, and company profiles

Forecasting Factors and Models

Forecasting Factors

- Historical Trends – Past market patterns, cycles, and major events that shaped how markets behave over time. Understanding past trends helps predict future behavior.

- Industry Factors – Specific characteristics of the industry like structure, regulations, and innovation cycles that affect market dynamics.

- Macroeconomic Factors – Economic conditions like GDP growth, inflation, and employment rates that affect how much money people have to spend.

- Demographic Factors – Population characteristics like age, income, and location that determine who can buy your product.

- Technology Factors – How quickly people adopt new technology and how much technology infrastructure exists.

- Regulatory Factors – Government rules, laws, and policies that can help or restrict market growth.

- Competitive Factors – Analyzing competition structure such as degree of competition and bargaining power of buyers and suppliers.

Forecasting Models / Techniques

Multiple Regression Analysis

- Identify and quantify factors that drive market changes

- Statistical modeling to establish relationships between market drivers and outcomes

Time Series Analysis – Seasonal Patterns

- Understand regular cyclical patterns in market demand

- Advanced statistical techniques to separate trend, seasonal, and irregular components

Time Series Analysis – Trend Analysis

- Identify underlying market growth patterns and momentum

- Statistical analysis of historical data to project future trends

Expert Opinion – Expert Interviews

- Gather deep industry insights and contextual understanding

- In-depth interviews with key industry stakeholders

Multi-Scenario Development

- Prepare for uncertainty by modeling different possible futures

- Creating optimistic, pessimistic, and most likely scenarios

Time Series Analysis – Moving Averages

- Sophisticated forecasting for complex time series data

- Auto-regressive integrated moving average models with seasonal components

Econometric Models

- Apply economic theory to market forecasting

- Sophisticated economic models that account for market interactions

Expert Opinion – Delphi Method

- Harness collective wisdom of industry experts

- Structured, multi-round expert consultation process

Monte Carlo Simulation

- Quantify uncertainty and probability distributions

- Thousands of simulations with varying input parameters

Research Analysis

Our research framework is built upon the fundamental principle of validating market intelligence from both demand and supply perspectives. This dual-sided approach ensures comprehensive market understanding and reduces the risk of single-source bias.

Demand-Side Analysis: We understand end-user/application behavior, preferences, and market needs along with the penetration of the product for specific application.

Supply-Side Analysis: We estimate overall market revenue, analyze the segmental share along with industry capacity, competitive landscape, and market structure.

Validation & Evaluation

Data triangulation is a validation technique that uses multiple methods, sources, or perspectives to examine the same research question, thereby increasing the credibility and reliability of research findings. In market research, triangulation serves as a quality assurance mechanism that helps identify and minimize bias, validate assumptions, and ensure accuracy in market estimates.

- Data Source Triangulation – Using multiple data sources to examine the same phenomenon

- Methodological Triangulation – Using multiple research methods to study the same research question

- Investigator Triangulation – Using multiple researchers or analysts to examine the same data

- Theoretical Triangulation – Using multiple theoretical perspectives to interpret the same data

Custom Market Research Services

We will customise the research for you, in case the report listed above does not meet your requirements.

Get 10% Free Customisation