Autonomous Construction Equipment Market Size, Share & Trends Analysis Report by Equipment Type (Excavators, Bulldozers, Loaders, Dump Trucks, Compactors, Graders, Cranes, Pavers, Drilling Machines, Others), Autonomy Level, Rated Power, Rated Capacity, Mobility Type, Technology, Propulsion Type, Application, End-Users, Distribution Channel, Ownership Model, and Geography (North America, Europe, Asia Pacific, Middle East, Africa, and South America) – Global Industry Data, Trends, and Forecasts, 2026–2035

|

|

|

Segmental Data Insights |

|

|

Demand Trends |

|

|

Competitive Landscape |

|

|

Strategic Development |

|

|

Future Outlook & Opportunities |

|

Autonomous Construction Equipment Market Size, Share, and Growth

The global autonomous construction equipment market is witnessing strong growth, valued at USD 13.2 billion in 2025 and projected to reach USD 36.8 billion by 2035, expanding at a CAGR of 10.8% during the forecast period. Asia Pacific is the fastest-growing region in the autonomous construction equipment market due to rapid urbanization, large-scale infrastructure development, government-backed smart construction initiatives, rising labor shortages, and increasing adoption of digital and automated technologies across construction projects.

Boris Sofman, co-founder and CEO of Bedrock Robotics, said, “Construction faces exploding demand from data centers, domestic manufacturing, and energy projects, at a time when the availability of skilled operators continues to decline, Developing our technology on active job sites with experienced contractors and their crews means we're addressing the exact challenges that limit project capacity today, while ensuring we do it in a way that is intuitive and non-disruptive to our partners and customers”.

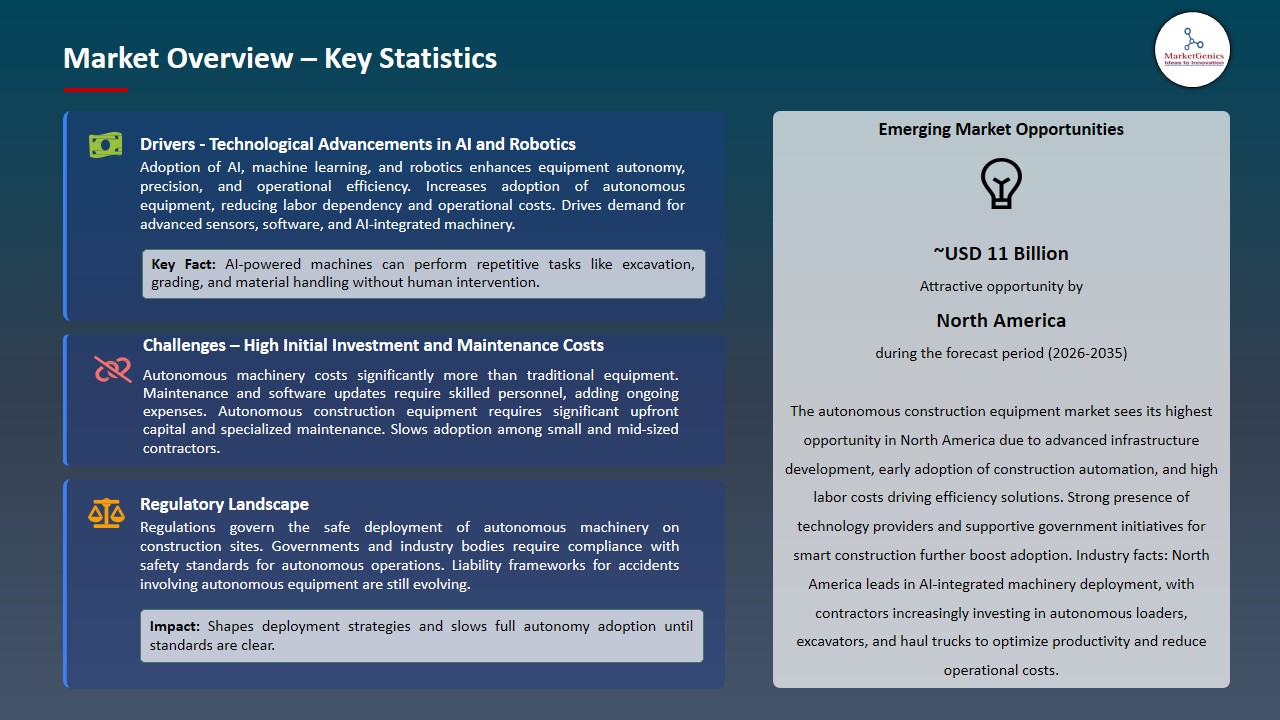

The autonomous construction equipment market is primarily driven by productivity and operational efficiency since the autonomous equipment allows the company to operate continuously with limited breaks, cutting down the project durations. Modern sensors, AI, and real-time data analytics get the machine movements optimized, reduce idle time, and enhance coordination of tasks at worksites. It results in increased use of equipment, reduced operating expenses, and predictability of project implementation by the contractors.

A notable opportunity in the autonomous construction equipment market is found in retrofit solutions to current construction equipment, allowing the contractor to add autonomy to their current equipment without having to replace the entire machine. Operators can convert ordinary excavators, loaders, and trucks into semi- or fully autonomous operations by adding autonomous kits or modular systems to enhance productivity, workflow optimization, and labor-independence, as well as to maximize the profits on the investments of previous excavators, loaders, and trucks.

Adjacent opportunities in the autonomous construction equipment market include the development of retrofit autonomy kits for existing fleets, integration of autonomous systems with electric and hybrid machinery, expansion into structured environments like mining, quarrying, and large-scale earthmoving, deployment of software and data-driven fleet management solutions, and growth in compact or urban construction equipment where labor shortages and space constraints favor automation.

Autonomous Construction Equipment Market Dynamics and Trends

Driver: Digital Construction and Telematics Accelerate Adoption of Autonomous Construction Equipment

-

The development of digital construction and telematics is a major propellant to the Autonomous Construction Equipment Market since, connected machines produce constant data on the place, performance, fuel or energy usage, and working conditions. Real-time monitoring enables autonomous and semi-autonomous equipment to be monitored remotely by the contractor enhancing site visibility and control.

- The predictive maintenance capabilities will notify possible failure prior to the breakdown to minimize unexpected downtime and maintenance expenses. Besides this, sophisticated fleet management software streamlines the scheduling, use, and assignment of equipment in more than one location.

- In 2025, Bedrock Robotics carried out the largest known autonomous deployment of excavation monitoring, teamed with Sundt Construction on a 130-acre manufacturing facility in the U.S. Its self-excavators, which were used on 20- to 80-ton machines, transported more than 65,000 cubic yards of material by loading human-operated dump trucks seamlessly. Such a practical application underscores the effectiveness of supervised autonomy in enhancing productivity, decreasing the intensity of labor in repetitive earthmoving jobs, and commercialization of autonomous construction machines on the working sites.

- This digital ecosystem improves the reliability, scalability, and ROI of autonomous construction equipment deployments.

Restraint: Unstructured and Dynamic Worksite Conditions Limit Full Autonomy Adoption in Construction

-

The complexity in the nature of an unstructured construction worksite is a limitation to the autonomous construction equipment market because most construction conditions are dynamic and, in most cases, cannot be standardized. Active construction sites unlike the controlled environment like mines or quarries have a constantly changing layout, uneven and unstable land, changeable weather patterns, and a constant interplay of workers, vehicles, and equipment.

- These considerations render full autonomy systems difficult to reliably sense the environment, anticipate actions, and arrive at risk-free choices in real-time. Moreover, several concurrent trades and regular changes of designs or schedules contribute to the further rise of unpredictability on the site. Existing technologies of autonomous work frequently cannot withstand these circumstances without external control and, as a result, the efficiency and dependability of these technologies are reduced.

- The variability and unpredictability of active construction sites remain high, limiting the use of fully autonomous construction equipment, and the necessity to rely on supervised or semi-autonomous solutions remains relevant.

Opportunity: Integration of Autonomous and Electric Construction Equipment

-

The potential of electric and hybrid construction equipment to be integrated with autonomous technology to achieve the synergy of automation and low-emission and energy-saving operations is one of the crucial opportunities that await the Autonomous Construction Equipment Market.

- Autonomous machines that are electrically powered offer benefits of using less fuel, reducing maintenance and environmental impact, and as a result, meet the growing regulatory and corporate sustainability demands. The synergy enables the contractors to have a greater level of operational efficiency besides making the projects more economical and environmentally conscious.

- Another benefit is that electric autonomous equipment may work in noise sensitive or emission-limited areas and expands the range of implementation in urban and environment-controlled locations and increases the overall appeal and adoption capacity of autonomous construction solutions.

- In 2025, Gravis Robotics also showed autonomous construction solutions at Bauma, collaborating with key OEMs. Their systems solved shortages in labor, enhanced efficiency and demonstrated scalable, real-life uses, based on successful autonomous dump truck trials in Australian and Canadian mines.

- The integration of autonomy with electric and hybrid machines improves the efficiency of operation, lowers the environmental footprint, and shows scalable, practical application, which places the market in a wider adoption framework.

Key Trend: Gradual Shift from Semi-Autonomous to Supervised Autonomous Operations

-

A trend in the Autonomous Construction Equipment Market is that the semi-autonomous is slowly being replaced with the supervised autonomous operations as a medium of transition to full autonomy. There has been an increase in adoption of systems where human control is an addition to machine autonomy as the autonomous equipment may carry out repetitive or structured operations whilst maintaining safety and reliability in the dynamic construction environment.

- This approach will reduce the consequences of the deployment that is entirely autonomous, develops a trusting relationship between the operator, and offers valuable data to enhance the machine learning algorithms and operational workflows. Gradually, the supervised autonomy allows the contractors to maximize productivity, decrease the dependence on labor and develop trust in the implementation of fully autonomous machines, which is an essential milestone in the overall implementation of autonomous construction solutions.

- In 2025, Komatsu, TIER IV and EARTHBRAIN collaborated to come up with autonomous technology to the Komatsu articulated and rigid dump trucks and this will be applied to civil engineering and quarry locations in Japan with actual implementation scheduled by 2027. The partnership is aimed at working on such issues as the labor shortage, fleet management systems that will help to increase the haulage efficiency, the safety level, and the eco-friendliness.

- The implementation of autonomous operations under supervision is gradually increasing the pace of effectual, efficient and safe implementation of autonomous construction equipment fully.

Autonomous-Construction-Equipment-Market Analysis and Segmental Data

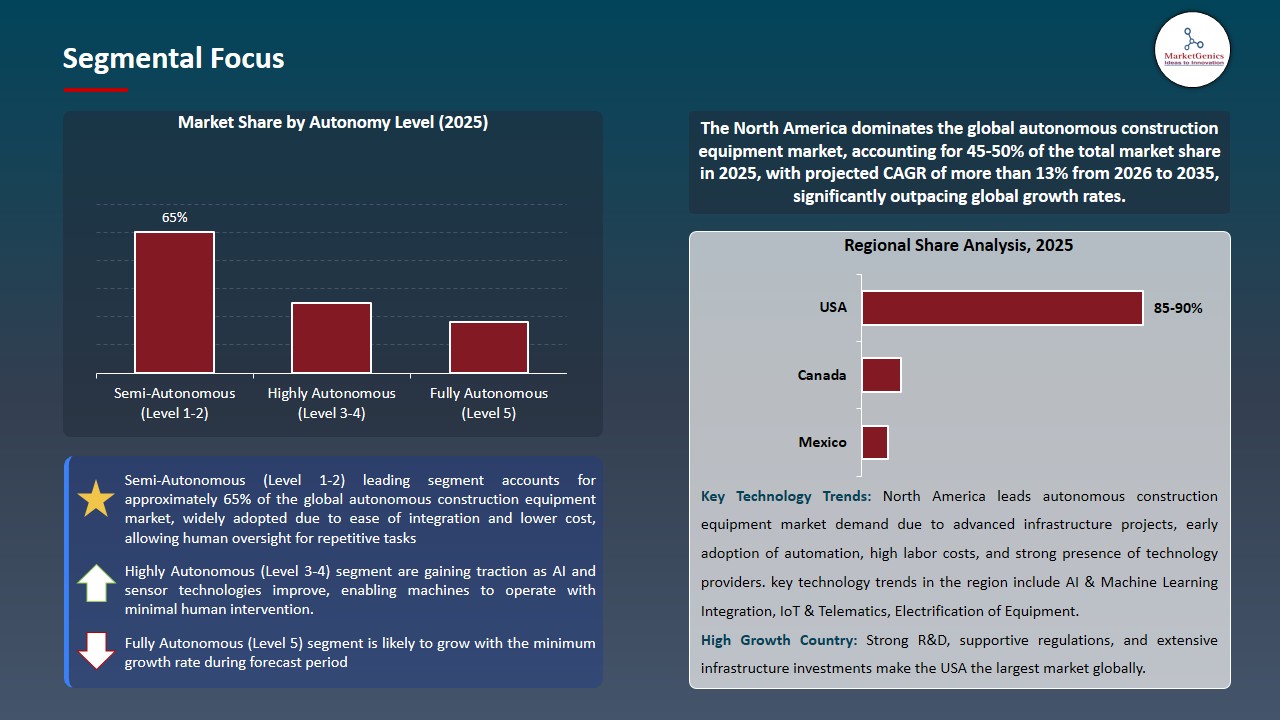

Semi-Autonomous (Level 1-2) Dominate Global Autonomous Construction Equipment Market

-

The semi-autonomous (Level 1-2) segment currently dominates the global autonomous construction equipment market, as it represents the most practical and widely adopted stage of autonomy in construction machinery. These systems combine automated functionalities, such as assisted steering, machine guidance, and basic task automation, with human oversight, allowing operators to retain control while benefiting from increased efficiency and reduced fatigue

- Semi-autonomous equipment offers a less risky point of entry to contractors, such that labor shortages and safety factors are dealt with, but the full investment and operational risk of autonomous machinery is not borne. It is the most popular because of the compatibility with existing fleets and its capability to perform in any of several organized and semi-organized settings, making it the most popular segment, leading to greater level of autonomy in the construction activities.

- In 2025, Hitachi Construction Machinery collaborated with Rio Tinto to come up with remote operation and partial autonomy on ultra-large hydraulic excavators at Pilbara mines in Australia. The interaction is based on operator-assist features, long-range operation, and semi-automation of digging and loading, which allows performing the repetitive activities automatically with human control.

- The semi-autonomous deployment increases the safety, productivity, and operational data gathering, which indicates the leading position of Level 1-2 semi-autonomous systems in construction and mining activities.

North America Leads Global Autonomous Construction Equipment Market Demand

-

The North American is leading region for the global autonomous construction equipment market, driven by strong infrastructure development, early adoption of advanced technologies, and growing labor shortages in the construction sector. Contractors and equipment manufacturers are increasingly implementing semi-autonomous and supervised autonomous machinery to enhance productivity, improve safety, and optimize operational efficiency. The availability of advanced digital construction tools, telematics, and fleet management systems further supports the adoption of autonomous solutions across diverse construction and mining projects.

- Supportive government policies, robust R&D investment, and the presence of key technology providers and OEMs actively piloting autonomous and semi-autonomous equipment have further strengthened the region’s market position.

- Urban infrastructure projects, commercial developments, and large-scale mining operations provide structured environments ideal for the deployment of autonomous machinery, enabling contractors to achieve operational efficiency and cost savings.

- Additionally, the region’s focus on sustainability and efficiency encourages the integration of electric and hybrid autonomous construction equipment, reinforcing North America’s role as a key driver of global market demand.

Autonomous-Construction-Equipment-Market Ecosystem

The global autonomous construction equipment market is consolidated, with leading players including Caterpillar Inc., Komatsu Ltd., Volvo Construction Equipment, Hitachi Construction Machinery, and Bobcat Company (Doosan). These companies maintain competitive advantages through extensive global distribution networks, advanced robotics and AI-enabled construction technologies, fleet management and telematics platforms, integration with digital construction management systems, IoT-enabled monitoring, and operator-friendly interfaces for semi-autonomous and fully autonomous machinery.

The market value chain encompasses the design and R&D of autonomous construction equipment, manufacturing of heavy machinery and sensor systems, software development and AI integration, calibration and testing of autonomous operations, deployment and integration at construction sites, compliance with safety and regulatory standards, and after-sales services such as remote monitoring, predictive maintenance, fleet optimization, and software updates.

Entry barriers are high due to the capital-intensive nature of heavy machinery manufacturing, technical expertise required for AI and autonomy, integration with dynamic worksites, and adherence to safety and operational regulations.

The market continues to evolve through technological innovations, including AI-driven navigation and task planning, multi-machine fleet coordination, advanced sensor integration, real-time performance analytics, and compatibility with digital construction management platforms, driving differentiation and adoption globally.

Recent Development and Strategic Overview:

-

In September 2025, Komatsu partnered with Applied Intuition to co-develop a software-defined vehicle (SDV) and autonomy platform for next-generation mining equipment. The platform integrates AI, machine learning, and flexible autonomy, enabling advanced operator-assist to full autonomy across fleets and site conditions. This collaboration aims to improve equipment performance, reduce downtime, optimize operations, and address labor shortages, marking a significant step toward fully autonomous, software-driven mining operations globally.

- In November 2024, Caterpillar successfully demonstrated fully autonomous operation of its Cat 777 off-highway truck at Luck Stone’s Bull Run quarry in Virginia. This marked Caterpillar’s first deployment of autonomous technology in the aggregates sector, expanding its Cat Command fleet to 100-ton-class trucks. The project, developed collaboratively with Luck Stone, aims to enhance safety, improve productivity, and provide scalable autonomous hauling solutions for quarry operations, while supporting workforce development and attracting the next generation of mining and construction professionals.

Report Scope

|

Detail |

|

|

Market Size in 2025 |

USD 13.2 Bn |

|

Market Forecast Value in 2035 |

USD 36.8 Bn |

|

Growth Rate (CAGR) |

10.8% |

|

Forecast Period |

2026 – 2035 |

|

Historical Data Available for |

2021 – 2024 |

|

Market Size Units |

US$ Billion for Value Thousand Units for Volume |

|

Report Format |

Electronic (PDF) + Excel |

|

North America |

Europe |

Asia Pacific |

Middle East |

Africa |

South America |

|

|

|

|

|

|

|

Companies Covered |

|||||

|

|

|

|

|

|

Autonomous-Construction-Equipment-Market Segmentation and Highlights

|

Segment |

Sub-segment |

|

Autonomous Construction Equipment Market, By Equipment Type |

|

|

Autonomous Construction Equipment Market, By Autonomy Level |

|

|

Autonomous Construction Equipment Market, By Rated Power |

|

|

Autonomous Construction Equipment Market, By Rated Capacity |

|

|

Autonomous Construction Equipment Market, By Technology |

|

|

Autonomous Construction Equipment Market, By Propulsion Type |

|

|

Autonomous Construction Equipment Market, By Application |

|

|

Autonomous Construction Equipment Market, By End-Users |

|

|

Autonomous Construction Equipment Market, By Distribution Channel |

|

|

Autonomous Construction Equipment Market, By Ownership Model |

|

Frequently Asked Questions

Table of Contents

- 1. Research Methodology and Assumptions

- 1.1. Definitions

- 1.2. Research Design and Approach

- 1.3. Data Collection Methods

- 1.4. Base Estimates and Calculations

- 1.5. Forecasting Models

- 1.5.1. Key Forecast Factors & Impact Analysis

- 1.6. Secondary Research

- 1.6.1. Open Sources

- 1.6.2. Paid Databases

- 1.6.3. Associations

- 1.7. Primary Research

- 1.7.1. Primary Sources

- 1.7.2. Primary Interviews with Stakeholders across Ecosystem

- 2. Executive Summary

- 2.1. Global Autonomous Construction Equipment Market Outlook

- 2.1.1. Autonomous Construction Equipment Market Size Volume (Thousand Units) and Value (US$ Bn), and Forecasts, 2021-2035

- 2.1.2. Compounded Annual Growth Rate Analysis

- 2.1.3. Growth Opportunity Analysis

- 2.1.4. Segmental Share Analysis

- 2.1.5. Geographical Share Analysis

- 2.2. Market Analysis and Facts

- 2.3. Supply-Demand Analysis

- 2.4. Competitive Benchmarking

- 2.5. Go-to- Market Strategy

- 2.5.1. Customer/ End-use Industry Assessment

- 2.5.2. Growth Opportunity Data, 2026-2035

- 2.5.2.1. Regional Data

- 2.5.2.2. Country Data

- 2.5.2.3. Segmental Data

- 2.5.3. Identification of Potential Market Spaces

- 2.5.4. GAP Analysis

- 2.5.5. Potential Attractive Price Points

- 2.5.6. Prevailing Market Risks & Challenges

- 2.5.7. Preferred Sales & Marketing Strategies

- 2.5.8. Key Recommendations and Analysis

- 2.5.9. A Way Forward

- 2.1. Global Autonomous Construction Equipment Market Outlook

- 3. Industry Data and Premium Insights

- 3.1. Global Industrial Machinery Overview, 2025

- 3.1.1. Industrial Machinery Ecosystem Analysis

- 3.1.2. Key Trends for Industrial Machinery

- 3.1.3. Regional Distribution for Industrial Machinery

- 3.2. Supplier Customer Data

- 3.3. Technology Roadmap and Developments

- 3.4. Trade Analysis

- 3.4.1. Import & Export Analysis, 2025

- 3.4.2. Top Importing Countries

- 3.4.3. Top Exporting Countries

- 3.5. Trump Tariff Impact Analysis

- 3.5.1. Manufacturer

- 3.5.1.1. Based on the component & Raw material

- 3.5.2. Supply Chain

- 3.5.3. End Consumer

- 3.5.1. Manufacturer

- 3.6. Raw Material Analysis

- 3.1. Global Industrial Machinery Overview, 2025

- 4. Market Overview

- 4.1. Market Dynamics

- 4.1.1. Drivers

- 4.1.1.1. Rising demand for jobsite productivity and reduced labour shortages (higher uptime, continuous operation).

- 4.1.1.2. Improvements in AI, sensors, GPS/RTK and telematics with falling sensor costs.

- 4.1.1.3. Strong safety and efficiency incentives (reduced accidents, rework and operating costs).

- 4.1.2. Restraints

- 4.1.2.1. High upfront system and retrofit costs plus complex integration with existing fleets.

- 4.1.2.2. Regulatory, liability and workforce-acceptance uncertainties slowing large-scale adoption.

- 4.1.1. Drivers

- 4.2. Key Trend Analysis

- 4.3. Regulatory Framework

- 4.3.1. Key Regulations, Norms, and Subsidies, by Key Countries

- 4.3.2. Tariffs and Standards

- 4.3.3. Impact Analysis of Regulations on the Market

- 4.4. Value Chain Analysis

- 4.4.1. Raw Material & Component Suppliers

- 4.4.2. Sensor & Hardware Providers

- 4.4.3. Manufacturers & System Integrators

- 4.4.4. Distributors & Sales Channels

- 4.4.5. End-Users

- 4.5. Cost Structure Analysis

- 4.6. Pricing Analysis

- 4.7. Porter’s Five Forces Analysis

- 4.8. PESTEL Analysis

- 4.9. Global Autonomous Construction Equipment Market Demand

- 4.9.1. Historical Market Size – Volume (Thousand Units) and Value (US$ Bn), 2020-2024

- 4.9.2. Current and Future Market Size – Volume (Thousand Units) and Value (US$ Bn), 2026–2035

- 4.9.2.1. Y-o-Y Growth Trends

- 4.9.2.2. Absolute $ Opportunity Assessment

- 4.1. Market Dynamics

- 5. Competition Landscape

- 5.1. Competition structure

- 5.1.1. Fragmented v/s consolidated

- 5.2. Company Share Analysis, 2025

- 5.2.1. Global Company Market Share

- 5.2.2. By Region

- 5.2.2.1. North America

- 5.2.2.2. Europe

- 5.2.2.3. Asia Pacific

- 5.2.2.4. Middle East

- 5.2.2.5. Africa

- 5.2.2.6. South America

- 5.3. Product Comparison Matrix

- 5.3.1. Specifications

- 5.3.2. Market Positioning

- 5.3.3. Pricing

- 5.1. Competition structure

- 6. Global Autonomous Construction Equipment Market Analysis, by Equipment Type

- 6.1. Key Segment Analysis

- 6.2. Autonomous Construction Equipment Market Size Volume (Thousand Units) and Value (US$ Bn), Analysis, and Forecasts, by Equipment Type, 2021-2035

- 6.2.1. Excavators

- 6.2.2. Bulldozers

- 6.2.3. Loaders

- 6.2.3.1. Wheel Loaders

- 6.2.3.2. Skid-Steer Loaders

- 6.2.3.3. Backhoe Loaders

- 6.2.4. Dump Trucks

- 6.2.5. Compactors

- 6.2.6. Graders

- 6.2.7. Cranes

- 6.2.8. Pavers

- 6.2.9. Drilling Machines

- 6.2.10. Others

- 7. Global Autonomous Construction Equipment Market Analysis, by Autonomy Level

- 7.1. Key Segment Analysis

- 7.2. Autonomous Construction Equipment Market Size Volume (Thousand Units) and Value (US$ Bn), Analysis, and Forecasts, by Autonomy Level, 2021-2035

- 7.2.1. Semi-Autonomous (Level 1-2)

- 7.2.2. Highly Autonomous (Level 3-4)

- 7.2.3. Fully Autonomous (Level 5)

- 8. Global Autonomous Construction Equipment Market Analysis, by Rated Power

- 8.1. Key Segment Analysis

- 8.2. Autonomous Construction Equipment Market Size Volume (Thousand Units) and Value (US$ Bn), Analysis, and Forecasts, by Rated Power, 2021-2035

- 8.2.1. Less than 100 HP

- 8.2.2. 100-200 HP

- 8.2.3. 201-300 HP

- 8.2.4. 301-400 HP

- 8.2.5. Above 400 HP

- 9. Global Autonomous Construction Equipment Market Analysis, by Rated Capacity

- 9.1. Key Segment Analysis

- 9.2. Autonomous Construction Equipment Market Size Volume (Thousand Units) and Value (US$ Bn), Analysis, and Forecasts, by Rated Capacity, 2021-2035

- 9.2.1. Less than 5 Tons

- 9.2.2. 5-10 Tons

- 9.2.3. 11-20 Tons

- 9.2.4. 21-40 Tons

- 9.2.5. 41-60 Tons

- 10. Global Autonomous Construction Equipment Market Analysis, by Technology

- 10.1. Key Segment Analysis

- 10.2. Autonomous Construction Equipment Market Size Volume (Thousand Units) and Value (US$ Bn), Analysis, and Forecasts, by Technology, 2021-2035

- 10.2.1. GPS/GNSS-Based Systems

- 10.2.2. LiDAR-Based Systems

- 10.2.3. Radar-Based Systems

- 10.2.4. Camera/Vision-Based Systems

- 10.2.5. Sensor Fusion Technology

- 10.2.6. AI & Machine Learning Integration

- 10.2.7. Others

- 11. Global Autonomous Construction Equipment Market Analysis, by Propulsion Type

- 11.1. Key Segment Analysis

- 11.2. Autonomous Construction Equipment Market Size Volume (Thousand Units) and Value (US$ Bn), Analysis, and Forecasts, by Propulsion Type, 2021-2035

- 11.2.1. Diesel-Powered

- 11.2.2. Electric-Powered

- 11.2.3. Hybrid-Powered

- 11.2.4. Hydrogen Fuel Cell

- 12. Global Autonomous Construction Equipment Market Analysis, by Application

- 12.1. Key Segment Analysis

- 12.2. Autonomous Construction Equipment Market Size Volume (Thousand Units) and Value (US$ Bn), Analysis, and Forecasts, by Application, 2021-2035

- 12.2.1. Earthmoving & Excavation

- 12.2.2. Material Handling

- 12.2.3. Grading & Leveling

- 12.2.4. Demolition

- 12.2.5. Road Construction

- 12.2.6. Tunneling

- 12.2.7. Mining Operations

- 12.2.8. Site Preparation

- 12.2.9. Other Applications

- 13. Global Autonomous Construction Equipment Market Analysis and Forecasts, by End-Users

- 13.1. Key Findings

- 13.2. Autonomous Construction Equipment Market Size Volume (Thousand Units) and Value (US$ Bn), Analysis, and Forecasts, by End-Users, 2021-2035

- 13.2.1. Construction Industry

- 13.2.1.1. Residential Construction

- 13.2.1.2. Commercial Construction

- 13.2.1.3. Infrastructure Development

- 13.2.2. Mining Industry

- 13.2.2.1. Surface Mining

- 13.2.2.2. Underground Mining

- 13.2.3. Oil & Gas Industry

- 13.2.4. Agriculture

- 13.2.5. Forestry

- 13.2.6. Waste Management

- 13.2.7. Other End-users

- 13.2.1. Construction Industry

- 14. Global Autonomous Construction Equipment Market Analysis and Forecasts, by Distribution Channel

- 14.1. Key Findings

- 14.2. Autonomous Construction Equipment Market Size Volume (Thousand Units) and Value (US$ Bn), Analysis, and Forecasts, by Distribution Channel, 2021-2035

- 14.2.1. Direct Sales

- 14.2.2. Distributors & Dealers

- 14.2.3. Online Sales Platforms

- 14.2.4. Rental/Leasing Services

- 15. Global Autonomous Construction Equipment Market Analysis and Forecasts, by Ownership Model

- 15.1. Key Findings

- 15.2. Autonomous Construction Equipment Market Size Volume (Thousand Units) and Value (US$ Bn), Analysis, and Forecasts, by Ownership Model, 2021-2035

- 15.2.1. Purchase/Owned

- 15.2.2. Rental/Leased

- 15.2.3. Equipment-as-a-Service (EaaS)

- 16. Global Autonomous Construction Equipment Market Analysis and Forecasts, by Region

- 16.1. Key Findings

- 16.2. Autonomous Construction Equipment Market Size Volume (Thousand Units) and Value (US$ Bn), Analysis, and Forecasts, by Region, 2021-2035

- 16.2.1. North America

- 16.2.2. Europe

- 16.2.3. Asia Pacific

- 16.2.4. Middle East

- 16.2.5. Africa

- 16.2.6. South America

- 17. North America Autonomous Construction Equipment Market Analysis

- 17.1. Key Segment Analysis

- 17.2. Regional Snapshot

- 17.3. North America Autonomous Construction Equipment Market Size- Volume (Thousand Units) and Value (US$ Bn), Analysis, and Forecasts, 2021-2035

- 17.3.1. Equipment Type

- 17.3.2. Autonomy Level

- 17.3.3. Rated Power

- 17.3.4. Rated Capacity

- 17.3.5. Technology

- 17.3.6. Propulsion Type

- 17.3.7. Application

- 17.3.8. End-Users

- 17.3.9. Distribution Channel

- 17.3.10. Ownership Model

- 17.3.11. Country

- 17.3.11.1. USA

- 17.3.11.2. Canada

- 17.3.11.3. Mexico

- 17.4. USA Autonomous Construction Equipment Market

- 17.4.1. Country Segmental Analysis

- 17.4.2. Equipment Type

- 17.4.3. Autonomy Level

- 17.4.4. Rated Power

- 17.4.5. Rated Capacity

- 17.4.6. Technology

- 17.4.7. Propulsion Type

- 17.4.8. Application

- 17.4.9. End-Users

- 17.4.10. Distribution Channel

- 17.4.11. Ownership Model

- 17.5. Canada Autonomous Construction Equipment Market

- 17.5.1. Country Segmental Analysis

- 17.5.2. Equipment Type

- 17.5.3. Autonomy Level

- 17.5.4. Rated Power

- 17.5.5. Rated Capacity

- 17.5.6. Technology

- 17.5.7. Propulsion Type

- 17.5.8. Application

- 17.5.9. End-Users

- 17.5.10. Distribution Channel

- 17.5.11. Ownership Model

- 17.6. Mexico Autonomous Construction Equipment Market

- 17.6.1. Country Segmental Analysis

- 17.6.2. Equipment Type

- 17.6.3. Autonomy Level

- 17.6.4. Rated Power

- 17.6.5. Rated Capacity

- 17.6.6. Technology

- 17.6.7. Propulsion Type

- 17.6.8. Application

- 17.6.9. End-Users

- 17.6.10. Distribution Channel

- 17.6.11. Ownership Model

- 18. Europe Autonomous Construction Equipment Market Analysis

- 18.1. Key Segment Analysis

- 18.2. Regional Snapshot

- 18.3. Europe Autonomous Construction Equipment Market Size Volume (Thousand Units) and Value (US$ Bn), Analysis, and Forecasts, 2021-2035

- 18.3.1. Equipment Type

- 18.3.2. Autonomy Level

- 18.3.3. Rated Power

- 18.3.4. Rated Capacity

- 18.3.5. Technology

- 18.3.6. Propulsion Type

- 18.3.7. Application

- 18.3.8. End-Users

- 18.3.9. Distribution Channel

- 18.3.10. Ownership Model

- 18.3.11. Country

- 18.3.11.1. Germany

- 18.3.11.2. United Kingdom

- 18.3.11.3. France

- 18.3.11.4. Italy

- 18.3.11.5. Spain

- 18.3.11.6. Netherlands

- 18.3.11.7. Nordic Countries

- 18.3.11.8. Poland

- 18.3.11.9. Russia & CIS

- 18.3.11.10. Rest of Europe

- 18.4. Germany Autonomous Construction Equipment Market

- 18.4.1. Country Segmental Analysis

- 18.4.2. Equipment Type

- 18.4.3. Autonomy Level

- 18.4.4. Rated Power

- 18.4.5. Rated Capacity

- 18.4.6. Technology

- 18.4.7. Propulsion Type

- 18.4.8. Application

- 18.4.9. End-Users

- 18.4.10. Distribution Channel

- 18.4.11. Ownership Model

- 18.5. United Kingdom Autonomous Construction Equipment Market

- 18.5.1. Country Segmental Analysis

- 18.5.2. Equipment Type

- 18.5.3. Autonomy Level

- 18.5.4. Rated Power

- 18.5.5. Rated Capacity

- 18.5.6. Technology

- 18.5.7. Propulsion Type

- 18.5.8. Application

- 18.5.9. End-Users

- 18.5.10. Distribution Channel

- 18.5.11. Ownership Model

- 18.6. France Autonomous Construction Equipment Market

- 18.6.1. Country Segmental Analysis

- 18.6.2. Equipment Type

- 18.6.3. Autonomy Level

- 18.6.4. Rated Power

- 18.6.5. Rated Capacity

- 18.6.6. Technology

- 18.6.7. Propulsion Type

- 18.6.8. Application

- 18.6.9. End-Users

- 18.6.10. Distribution Channel

- 18.6.11. Ownership Model

- 18.7. Italy Autonomous Construction Equipment Market

- 18.7.1. Country Segmental Analysis

- 18.7.2. Equipment Type

- 18.7.3. Autonomy Level

- 18.7.4. Rated Power

- 18.7.5. Rated Capacity

- 18.7.6. Technology

- 18.7.7. Propulsion Type

- 18.7.8. Application

- 18.7.9. End-Users

- 18.7.10. Distribution Channel

- 18.7.11. Ownership Model

- 18.8. Spain Autonomous Construction Equipment Market

- 18.8.1. Country Segmental Analysis

- 18.8.2. Equipment Type

- 18.8.3. Autonomy Level

- 18.8.4. Rated Power

- 18.8.5. Rated Capacity

- 18.8.6. Technology

- 18.8.7. Propulsion Type

- 18.8.8. Application

- 18.8.9. End-Users

- 18.8.10. Distribution Channel

- 18.8.11. Ownership Model

- 18.9. Netherlands Autonomous Construction Equipment Market

- 18.9.1. Country Segmental Analysis

- 18.9.2. Equipment Type

- 18.9.3. Autonomy Level

- 18.9.4. Rated Power

- 18.9.5. Rated Capacity

- 18.9.6. Technology

- 18.9.7. Propulsion Type

- 18.9.8. Application

- 18.9.9. End-Users

- 18.9.10. Distribution Channel

- 18.9.11. Ownership Model

- 18.10. Nordic Countries Autonomous Construction Equipment Market

- 18.10.1. Country Segmental Analysis

- 18.10.2. Equipment Type

- 18.10.3. Autonomy Level

- 18.10.4. Rated Power

- 18.10.5. Rated Capacity

- 18.10.6. Technology

- 18.10.7. Propulsion Type

- 18.10.8. Application

- 18.10.9. End-Users

- 18.10.10. Distribution Channel

- 18.10.11. Ownership Model

- 18.11. Poland Autonomous Construction Equipment Market

- 18.11.1. Country Segmental Analysis

- 18.11.2. Equipment Type

- 18.11.3. Autonomy Level

- 18.11.4. Rated Power

- 18.11.5. Rated Capacity

- 18.11.6. Technology

- 18.11.7. Propulsion Type

- 18.11.8. Application

- 18.11.9. End-Users

- 18.11.10. Distribution Channel

- 18.11.11. Ownership Model

- 18.12. Russia & CIS Autonomous Construction Equipment Market

- 18.12.1. Country Segmental Analysis

- 18.12.2. Equipment Type

- 18.12.3. Autonomy Level

- 18.12.4. Rated Power

- 18.12.5. Rated Capacity

- 18.12.6. Technology

- 18.12.7. Propulsion Type

- 18.12.8. Application

- 18.12.9. End-Users

- 18.12.10. Distribution Channel

- 18.12.11. Ownership Model

- 18.13. Rest of Europe Autonomous Construction Equipment Market

- 18.13.1. Country Segmental Analysis

- 18.13.2. Equipment Type

- 18.13.3. Autonomy Level

- 18.13.4. Rated Power

- 18.13.5. Rated Capacity

- 18.13.6. Technology

- 18.13.7. Propulsion Type

- 18.13.8. Application

- 18.13.9. End-Users

- 18.13.10. Distribution Channel

- 18.13.11. Ownership Model

- 19. Asia Pacific Autonomous Construction Equipment Market Analysis

- 19.1. Key Segment Analysis

- 19.2. Regional Snapshot

- 19.3. Asia Pacific Autonomous Construction Equipment Market Size Volume (Thousand Units) and Value (US$ Bn), Analysis, and Forecasts, 2021-2035

- 19.3.1. Equipment Type

- 19.3.2. Autonomy Level

- 19.3.3. Rated Power

- 19.3.4. Rated Capacity

- 19.3.5. Technology

- 19.3.6. Propulsion Type

- 19.3.7. Application

- 19.3.8. End-Users

- 19.3.9. Distribution Channel

- 19.3.10. Ownership Model

- 19.3.11. Country

- 19.3.11.1. China

- 19.3.11.2. India

- 19.3.11.3. Japan

- 19.3.11.4. South Korea

- 19.3.11.5. Australia and New Zealand

- 19.3.11.6. Indonesia

- 19.3.11.7. Malaysia

- 19.3.11.8. Thailand

- 19.3.11.9. Vietnam

- 19.3.11.10. Rest of Asia Pacific

- 19.4. China Autonomous Construction Equipment Market

- 19.4.1. Country Segmental Analysis

- 19.4.2. Equipment Type

- 19.4.3. Autonomy Level

- 19.4.4. Rated Power

- 19.4.5. Rated Capacity

- 19.4.6. Technology

- 19.4.7. Propulsion Type

- 19.4.8. Application

- 19.4.9. End-Users

- 19.4.10. Distribution Channel

- 19.4.11. Ownership Model

- 19.5. India Autonomous Construction Equipment Market

- 19.5.1. Country Segmental Analysis

- 19.5.2. Equipment Type

- 19.5.3. Autonomy Level

- 19.5.4. Rated Power

- 19.5.5. Rated Capacity

- 19.5.6. Technology

- 19.5.7. Propulsion Type

- 19.5.8. Application

- 19.5.9. End-Users

- 19.5.10. Distribution Channel

- 19.5.11. Ownership Model

- 19.6. Japan Autonomous Construction Equipment Market

- 19.6.1. Country Segmental Analysis

- 19.6.2. Equipment Type

- 19.6.3. Autonomy Level

- 19.6.4. Rated Power

- 19.6.5. Rated Capacity

- 19.6.6. Technology

- 19.6.7. Propulsion Type

- 19.6.8. Application

- 19.6.9. End-Users

- 19.6.10. Distribution Channel

- 19.6.11. Ownership Model

- 19.7. South Korea Autonomous Construction Equipment Market

- 19.7.1. Country Segmental Analysis

- 19.7.2. Equipment Type

- 19.7.3. Autonomy Level

- 19.7.4. Rated Power

- 19.7.5. Rated Capacity

- 19.7.6. Technology

- 19.7.7. Propulsion Type

- 19.7.8. Application

- 19.7.9. End-Users

- 19.7.10. Distribution Channel

- 19.7.11. Ownership Model

- 19.8. Australia and New Zealand Autonomous Construction Equipment Market

- 19.8.1. Country Segmental Analysis

- 19.8.2. Equipment Type

- 19.8.3. Autonomy Level

- 19.8.4. Rated Power

- 19.8.5. Rated Capacity

- 19.8.6. Technology

- 19.8.7. Propulsion Type

- 19.8.8. Application

- 19.8.9. End-Users

- 19.8.10. Distribution Channel

- 19.8.11. Ownership Model

- 19.9. Indonesia Autonomous Construction Equipment Market

- 19.9.1. Country Segmental Analysis

- 19.9.2. Equipment Type

- 19.9.3. Autonomy Level

- 19.9.4. Rated Power

- 19.9.5. Rated Capacity

- 19.9.6. Technology

- 19.9.7. Propulsion Type

- 19.9.8. Application

- 19.9.9. End-Users

- 19.9.10. Distribution Channel

- 19.9.11. Ownership Model

- 19.10. Malaysia Autonomous Construction Equipment Market

- 19.10.1. Country Segmental Analysis

- 19.10.2. Equipment Type

- 19.10.3. Autonomy Level

- 19.10.4. Rated Power

- 19.10.5. Rated Capacity

- 19.10.6. Technology

- 19.10.7. Propulsion Type

- 19.10.8. Application

- 19.10.9. End-Users

- 19.10.10. Distribution Channel

- 19.10.11. Ownership Model

- 19.11. Thailand Autonomous Construction Equipment Market

- 19.11.1. Country Segmental Analysis

- 19.11.2. Equipment Type

- 19.11.3. Autonomy Level

- 19.11.4. Rated Power

- 19.11.5. Rated Capacity

- 19.11.6. Technology

- 19.11.7. Propulsion Type

- 19.11.8. Application

- 19.11.9. End-Users

- 19.11.10. Distribution Channel

- 19.11.11. Ownership Model

- 19.12. Vietnam Autonomous Construction Equipment Market

- 19.12.1. Country Segmental Analysis

- 19.12.2. Equipment Type

- 19.12.3. Autonomy Level

- 19.12.4. Rated Power

- 19.12.5. Rated Capacity

- 19.12.6. Technology

- 19.12.7. Propulsion Type

- 19.12.8. Application

- 19.12.9. End-Users

- 19.12.10. Distribution Channel

- 19.12.11. Ownership Model

- 19.13. Rest of Asia Pacific Autonomous Construction Equipment Market

- 19.13.1. Country Segmental Analysis

- 19.13.2. Equipment Type

- 19.13.3. Autonomy Level

- 19.13.4. Rated Power

- 19.13.5. Rated Capacity

- 19.13.6. Technology

- 19.13.7. Propulsion Type

- 19.13.8. Application

- 19.13.9. End-Users

- 19.13.10. Distribution Channel

- 19.13.11. Ownership Model

- 20. Middle East Autonomous Construction Equipment Market Analysis

- 20.1. Key Segment Analysis

- 20.2. Regional Snapshot

- 20.3. Middle East Autonomous Construction Equipment Market Size Volume (Thousand Units) and Value (US$ Bn), Analysis, and Forecasts, 2021-2035

- 20.3.1. Equipment Type

- 20.3.2. Autonomy Level

- 20.3.3. Rated Power

- 20.3.4. Rated Capacity

- 20.3.5. Technology

- 20.3.6. Propulsion Type

- 20.3.7. Application

- 20.3.8. End-Users

- 20.3.9. Distribution Channel

- 20.3.10. Ownership Model

- 20.3.11. Country

- 20.3.11.1. Turkey

- 20.3.11.2. UAE

- 20.3.11.3. Saudi Arabia

- 20.3.11.4. Israel

- 20.3.11.5. Rest of Middle East

- 20.4. Turkey Autonomous Construction Equipment Market

- 20.4.1. Country Segmental Analysis

- 20.4.2. Equipment Type

- 20.4.3. Autonomy Level

- 20.4.4. Rated Power

- 20.4.5. Rated Capacity

- 20.4.6. Technology

- 20.4.7. Propulsion Type

- 20.4.8. Application

- 20.4.9. End-Users

- 20.4.10. Distribution Channel

- 20.4.11. Ownership Model

- 20.5. UAE Autonomous Construction Equipment Market

- 20.5.1. Country Segmental Analysis

- 20.5.2. Equipment Type

- 20.5.3. Autonomy Level

- 20.5.4. Rated Power

- 20.5.5. Rated Capacity

- 20.5.6. Technology

- 20.5.7. Propulsion Type

- 20.5.8. Application

- 20.5.9. End-Users

- 20.5.10. Distribution Channel

- 20.5.11. Ownership Model

- 20.6. Saudi Arabia Autonomous Construction Equipment Market

- 20.6.1. Country Segmental Analysis

- 20.6.2. Equipment Type

- 20.6.3. Autonomy Level

- 20.6.4. Rated Power

- 20.6.5. Rated Capacity

- 20.6.6. Technology

- 20.6.7. Propulsion Type

- 20.6.8. Application

- 20.6.9. End-Users

- 20.6.10. Distribution Channel

- 20.6.11. Ownership Model

- 20.7. Israel Autonomous Construction Equipment Market

- 20.7.1. Country Segmental Analysis

- 20.7.2. Equipment Type

- 20.7.3. Autonomy Level

- 20.7.4. Rated Power

- 20.7.5. Rated Capacity

- 20.7.6. Technology

- 20.7.7. Propulsion Type

- 20.7.8. Application

- 20.7.9. End-Users

- 20.7.10. Distribution Channel

- 20.7.11. Ownership Model

- 20.8. Rest of Middle East Autonomous Construction Equipment Market

- 20.8.1. Country Segmental Analysis

- 20.8.2. Equipment Type

- 20.8.3. Autonomy Level

- 20.8.4. Rated Power

- 20.8.5. Rated Capacity

- 20.8.6. Technology

- 20.8.7. Propulsion Type

- 20.8.8. Application

- 20.8.9. End-Users

- 20.8.10. Distribution Channel

- 20.8.11. Ownership Model

- 21. Africa Autonomous Construction Equipment Market Analysis

- 21.1. Key Segment Analysis

- 21.2. Regional Snapshot

- 21.3. Africa Autonomous Construction Equipment Market Size Volume (Thousand Units) and Value (US$ Bn), Analysis, and Forecasts, 2021-2035

- 21.3.1. Equipment Type

- 21.3.2. Autonomy Level

- 21.3.3. Rated Power

- 21.3.4. Rated Capacity

- 21.3.5. Technology

- 21.3.6. Propulsion Type

- 21.3.7. Application

- 21.3.8. End-Users

- 21.3.9. Distribution Channel

- 21.3.10. Ownership Model

- 21.3.11. Country

- 21.3.11.1. South Africa

- 21.3.11.2. Egypt

- 21.3.11.3. Nigeria

- 21.3.11.4. Algeria

- 21.3.11.5. Rest of Africa

- 21.4. South Africa Autonomous Construction Equipment Market

- 21.4.1. Country Segmental Analysis

- 21.4.2. Equipment Type

- 21.4.3. Autonomy Level

- 21.4.4. Rated Power

- 21.4.5. Rated Capacity

- 21.4.6. Technology

- 21.4.7. Propulsion Type

- 21.4.8. Application

- 21.4.9. End-Users

- 21.4.10. Distribution Channel

- 21.4.11. Ownership Model

- 21.5. Egypt Autonomous Construction Equipment Market

- 21.5.1. Country Segmental Analysis

- 21.5.2. Equipment Type

- 21.5.3. Autonomy Level

- 21.5.4. Rated Power

- 21.5.5. Rated Capacity

- 21.5.6. Technology

- 21.5.7. Propulsion Type

- 21.5.8. Application

- 21.5.9. End-Users

- 21.5.10. Distribution Channel

- 21.5.11. Ownership Model

- 21.6. Nigeria Autonomous Construction Equipment Market

- 21.6.1. Country Segmental Analysis

- 21.6.2. Equipment Type

- 21.6.3. Autonomy Level

- 21.6.4. Rated Power

- 21.6.5. Rated Capacity

- 21.6.6. Technology

- 21.6.7. Propulsion Type

- 21.6.8. Application

- 21.6.9. End-Users

- 21.6.10. Distribution Channel

- 21.6.11. Ownership Model

- 21.7. Algeria Autonomous Construction Equipment Market

- 21.7.1. Country Segmental Analysis

- 21.7.2. Equipment Type

- 21.7.3. Autonomy Level

- 21.7.4. Rated Power

- 21.7.5. Rated Capacity

- 21.7.6. Technology

- 21.7.7. Propulsion Type

- 21.7.8. Application

- 21.7.9. End-Users

- 21.7.10. Distribution Channel

- 21.7.11. Ownership Model

- 21.8. Rest of Africa Autonomous Construction Equipment Market

- 21.8.1. Country Segmental Analysis

- 21.8.2. Equipment Type

- 21.8.3. Autonomy Level

- 21.8.4. Rated Power

- 21.8.5. Rated Capacity

- 21.8.6. Technology

- 21.8.7. Propulsion Type

- 21.8.8. Application

- 21.8.9. End-Users

- 21.8.10. Distribution Channel

- 21.8.11. Ownership Model

- 22. South America Autonomous Construction Equipment Market Analysis

- 22.1. Key Segment Analysis

- 22.2. Regional Snapshot

- 22.3. South America Autonomous Construction Equipment Market Size Volume (Thousand Units) and Value (US$ Bn), Analysis, and Forecasts, 2021-2035

- 22.3.1. Equipment Type

- 22.3.2. Autonomy Level

- 22.3.3. Rated Power

- 22.3.4. Rated Capacity

- 22.3.5. Technology

- 22.3.6. Propulsion Type

- 22.3.7. Application

- 22.3.8. End-Users

- 22.3.9. Distribution Channel

- 22.3.10. Ownership Model

- 22.3.11. Country

- 22.3.11.1. Brazil

- 22.3.11.2. Argentina

- 22.3.11.3. Rest of South America

- 22.4. Brazil Autonomous Construction Equipment Market

- 22.4.1. Country Segmental Analysis

- 22.4.2. Equipment Type

- 22.4.3. Autonomy Level

- 22.4.4. Rated Power

- 22.4.5. Rated Capacity

- 22.4.6. Technology

- 22.4.7. Propulsion Type

- 22.4.8. Application

- 22.4.9. End-Users

- 22.4.10. Distribution Channel

- 22.4.11. Ownership Model

- 22.5. Argentina Autonomous Construction Equipment Market

- 22.5.1. Country Segmental Analysis

- 22.5.2. Equipment Type

- 22.5.3. Autonomy Level

- 22.5.4. Rated Power

- 22.5.5. Rated Capacity

- 22.5.6. Technology

- 22.5.7. Propulsion Type

- 22.5.8. Application

- 22.5.9. End-Users

- 22.5.10. Distribution Channel

- 22.5.11. Ownership Model

- 22.6. Rest of South America Autonomous Construction Equipment Market

- 22.6.1. Country Segmental Analysis

- 22.6.2. Equipment Type

- 22.6.3. Autonomy Level

- 22.6.4. Rated Power

- 22.6.5. Rated Capacity

- 22.6.6. Technology

- 22.6.7. Propulsion Type

- 22.6.8. Application

- 22.6.9. End-Users

- 22.6.10. Distribution Channel

- 22.6.11. Ownership Model

- 23. Key Players/ Company Profile

- 23.1. Balfour Beatty

- 23.1.1. Company Details/ Overview

- 23.1.2. Company Financials

- 23.1.3. Key Customers and Competitors

- 23.1.4. Business/ Industry Portfolio

- 23.1.5. Product Portfolio/ Specification Details

- 23.1.6. Pricing Data

- 23.1.7. Strategic Overview

- 23.1.8. Recent Developments

- 23.2. Bell Equipment

- 23.3. Bobcat Company (Doosan)

- 23.4. Built Robotics

- 23.5. Caterpillar Inc.

- 23.6. CNH Industrial N.V.

- 23.7. Deere & Company

- 23.8. Epiroc AB

- 23.9. Fujita Corporation

- 23.10. Hexagon AB

- 23.11. Hitachi Construction Machinery

- 23.12. Hyundai Construction Equipment

- 23.13. JCB (J.C. Bamford Excavators)

- 23.14. Kobelco Construction Machinery

- 23.15. Komatsu Ltd.

- 23.16. Liebherr Group

- 23.17. Obayashi Corporation

- 23.18. Royal Truck & Equipment

- 23.19. Sandvik AB

- 23.20. SANY Group

- 23.21. Shimizu Corporation

- 23.22. Topcon Positioning Systems

- 23.23. Trimble Inc.

- 23.24. Volvo Construction Equipment

- 23.25. XCMG Group

- 23.26. Zoomlion Heavy Industry

- 23.27. Other Key Players

- 23.1. Balfour Beatty

Note* - This is just tentative list of players. While providing the report, we will cover more number of players based on their revenue and share for each geography

Research Design

Our research design integrates both demand-side and supply-side analysis through a balanced combination of primary and secondary research methodologies. By utilizing both bottom-up and top-down approaches alongside rigorous data triangulation methods, we deliver robust market intelligence that supports strategic decision-making.

MarketGenics' comprehensive research design framework ensures the delivery of accurate, reliable, and actionable market intelligence. Through the integration of multiple research approaches, rigorous validation processes, and expert analysis, we provide our clients with the insights needed to make informed strategic decisions and capitalize on market opportunities.

MarketGenics leverages a dedicated industry panel of experts and a comprehensive suite of paid databases to effectively collect, consolidate, and analyze market intelligence.

Our approach has consistently proven to be reliable and effective in generating accurate market insights, identifying key industry trends, and uncovering emerging business opportunities.

Through both primary and secondary research, we capture and analyze critical company-level data such as manufacturing footprints, including technical centers, R&D facilities, sales offices, and headquarters.

Our expert panel further enhances our ability to estimate market size for specific brands based on validated field-level intelligence.

Our data mining techniques incorporate both parametric and non-parametric methods, allowing for structured data collection, sorting, processing, and cleaning.

Demand projections are derived from large-scale data sets analyzed through proprietary algorithms, culminating in robust and reliable market sizing.

Research Approach

The bottom-up approach builds market estimates by starting with the smallest addressable market units and systematically aggregating them to create comprehensive market size projections.

This method begins with specific, granular data points and builds upward to create the complete market landscape.

Customer Analysis → Segmental Analysis → Geographical Analysis

The top-down approach starts with the broadest possible market data and systematically narrows it down through a series of filters and assumptions to arrive at specific market segments or opportunities.

This method begins with the big picture and works downward to increasingly specific market slices.

TAM → SAM → SOM

Research Methods

Desk / Secondary Research

While analysing the market, we extensively study secondary sources, directories, and databases to identify and collect information useful for this technical, market-oriented, and commercial report. Secondary sources that we utilize are not only the public sources, but it is a combination of Open Source, Associations, Paid Databases, MG Repository & Knowledgebase, and others.

- Company websites, annual reports, financial reports, broker reports, and investor presentations

- National government documents, statistical databases and reports

- News articles, press releases and web-casts specific to the companies operating in the market, Magazines, reports, and others

- We gather information from commercial data sources for deriving company specific data such as segmental revenue, share for geography, product revenue, and others

- Internal and external proprietary databases (industry-specific), relevant patent, and regulatory databases

- Governing Bodies, Government Organizations

- Relevant Authorities, Country-specific Associations for Industries

We also employ the model mapping approach to estimate the product level market data through the players' product portfolio

Primary Research

Primary research/ interviews is vital in analyzing the market. Most of the cases involves paid primary interviews. Primary sources include primary interviews through e-mail interactions, telephonic interviews, surveys as well as face-to-face interviews with the different stakeholders across the value chain including several industry experts.

| Type of Respondents | Number of Primaries |

|---|---|

| Tier 2/3 Suppliers | ~20 |

| Tier 1 Suppliers | ~25 |

| End-users | ~25 |

| Industry Expert/ Panel/ Consultant | ~30 |

| Total | ~100 |

MG Knowledgebase

• Repository of industry blog, newsletter and case studies

• Online platform covering detailed market reports, and company profiles

Forecasting Factors and Models

Forecasting Factors

- Historical Trends – Past market patterns, cycles, and major events that shaped how markets behave over time. Understanding past trends helps predict future behavior.

- Industry Factors – Specific characteristics of the industry like structure, regulations, and innovation cycles that affect market dynamics.

- Macroeconomic Factors – Economic conditions like GDP growth, inflation, and employment rates that affect how much money people have to spend.

- Demographic Factors – Population characteristics like age, income, and location that determine who can buy your product.

- Technology Factors – How quickly people adopt new technology and how much technology infrastructure exists.

- Regulatory Factors – Government rules, laws, and policies that can help or restrict market growth.

- Competitive Factors – Analyzing competition structure such as degree of competition and bargaining power of buyers and suppliers.

Forecasting Models / Techniques

Multiple Regression Analysis

- Identify and quantify factors that drive market changes

- Statistical modeling to establish relationships between market drivers and outcomes

Time Series Analysis – Seasonal Patterns

- Understand regular cyclical patterns in market demand

- Advanced statistical techniques to separate trend, seasonal, and irregular components

Time Series Analysis – Trend Analysis

- Identify underlying market growth patterns and momentum

- Statistical analysis of historical data to project future trends

Expert Opinion – Expert Interviews

- Gather deep industry insights and contextual understanding

- In-depth interviews with key industry stakeholders

Multi-Scenario Development

- Prepare for uncertainty by modeling different possible futures

- Creating optimistic, pessimistic, and most likely scenarios

Time Series Analysis – Moving Averages

- Sophisticated forecasting for complex time series data

- Auto-regressive integrated moving average models with seasonal components

Econometric Models

- Apply economic theory to market forecasting

- Sophisticated economic models that account for market interactions

Expert Opinion – Delphi Method

- Harness collective wisdom of industry experts

- Structured, multi-round expert consultation process

Monte Carlo Simulation

- Quantify uncertainty and probability distributions

- Thousands of simulations with varying input parameters

Research Analysis

Our research framework is built upon the fundamental principle of validating market intelligence from both demand and supply perspectives. This dual-sided approach ensures comprehensive market understanding and reduces the risk of single-source bias.

Demand-Side Analysis: We understand end-user/application behavior, preferences, and market needs along with the penetration of the product for specific application.

Supply-Side Analysis: We estimate overall market revenue, analyze the segmental share along with industry capacity, competitive landscape, and market structure.

Validation & Evaluation

Data triangulation is a validation technique that uses multiple methods, sources, or perspectives to examine the same research question, thereby increasing the credibility and reliability of research findings. In market research, triangulation serves as a quality assurance mechanism that helps identify and minimize bias, validate assumptions, and ensure accuracy in market estimates.

- Data Source Triangulation – Using multiple data sources to examine the same phenomenon

- Methodological Triangulation – Using multiple research methods to study the same research question

- Investigator Triangulation – Using multiple researchers or analysts to examine the same data

- Theoretical Triangulation – Using multiple theoretical perspectives to interpret the same data

Custom Market Research Services

We will customise the research for you, in case the report listed above does not meet your requirements.

Get 10% Free Customisation