Cell Encapsulation Market Size, Share & Trends Analysis Report by Technology Type (Microencapsulation, Macroencapsulation, Nanoencapsulation), Material Type, Cell Type, Application, Permeability Type, End-users, and Geography (North America, Europe, Asia Pacific, Middle East, Africa, and South America) – Global Industry Data, Trends, and Forecasts, 2026–2035

|

|

|

Segmental Data Insights |

|

|

Demand Trends |

|

|

Competitive Landscape |

|

|

Strategic Development |

|

|

Future Outlook & Opportunities |

|

Cell-Encapsulation-Market Size, Share, and Growth

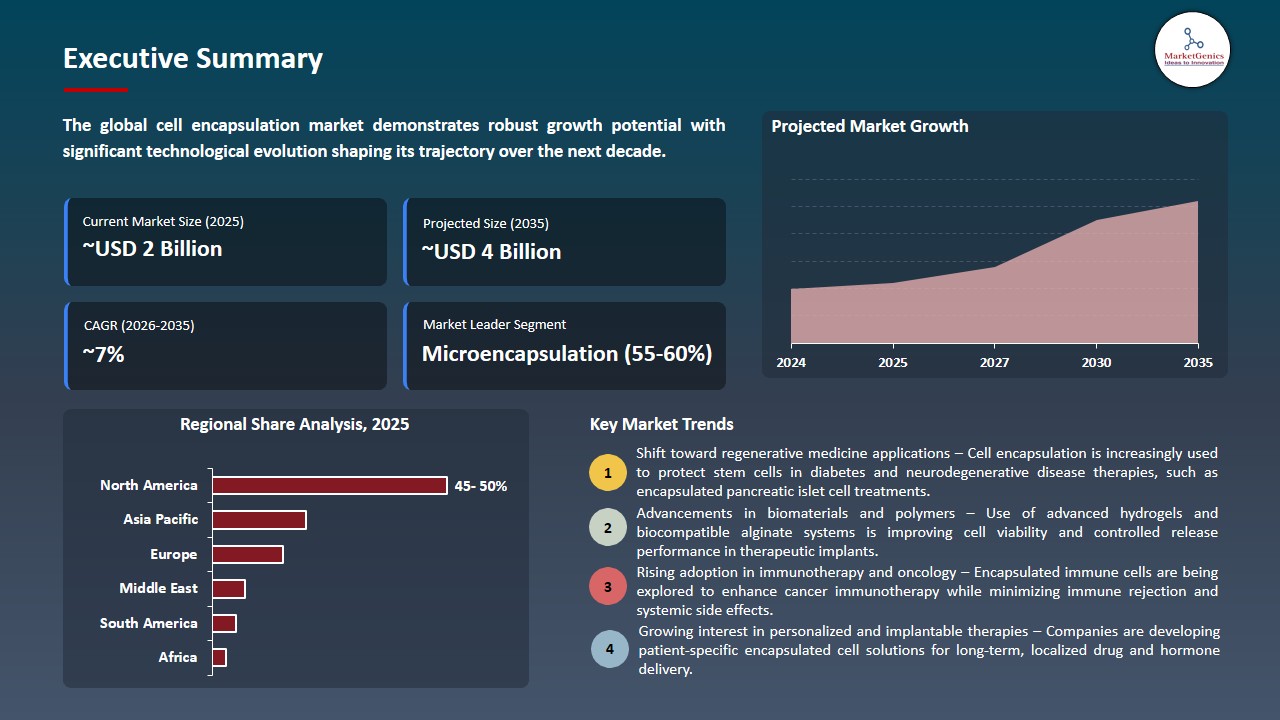

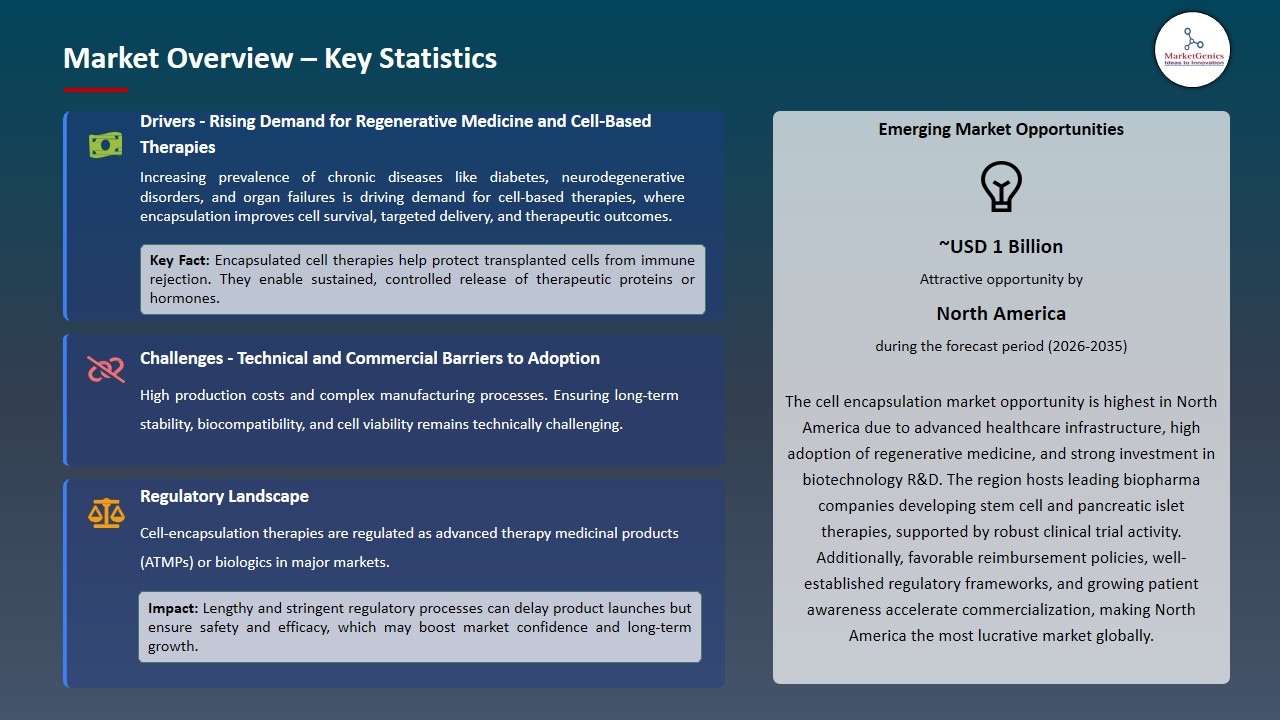

The global cell encapsulation market is experiencing robust growth, with its estimated value of USD 1.8 billion in the year 2025 and USD 3.6 billion by the period 2035, registering a CAGR of 7.2%, during the forecast period. State of the art, performance-based encapsulation platforms, custom therapeutic cell applications, and innovations that are scientifically endorsed are becoming the key drivers of growth in the global cell encapsulation market, allowing companies, specialty clinics, and commercial distribution channels to gain market share, build patient confidence, and increase the uptake of immune-protected and long-acting cell therapies.

Kevin Chinn, Vice President of Cell & Gene Therapy at Cencora, emphasized the company’s commitment to supporting the advancement of cell and gene therapies. He stated that Cencora aims to provide CGT developers with integrated, tailored support to accelerate speed-to-market and ensure product success. Through its partnership with Neurotech, the company plans to leverage its distribution infrastructure and commercialization services to streamline market entry, reduce potential access barriers, and provide secure storage and distribution, ultimately enabling efficient and reliable access to these advanced therapies.

The global cell encapsulation market is a high-performance, innovative, and clinically-oriented sector, and healthcare providers, research centers, and specialty clinics are all engaging in the customized, immune-protected and sustained-release cell therapies. In addition to traditional uses, the more sophisticated encapsulation systems are being prepared in diabetes, neurodegenerative diseases, cancerous and regenerative medicine to provide therapeutic effects that are long-lasting and reduce immune rejection and enhancement of patient outcomes.

Individual therapy planning and cell dosage optimization, as well as predictive treatment response, can be achieved by next-generation encapsulation technologies, including hydrogel matrices, oxygenated microcapsules, and immunoisolative surfaces, along with digital health tools and AI-driven models. For instance, the long-term viability and functional activity of insulin-secreting cells in preclinical models were demonstrated using the oxygen-supported encapsulation platform of Persista Bio, where the increased need of long-lasting, immune-protected therapy can be addressed by novel and improved platforms.

Adjacent opportunities to the cell encapsulation market include regenerative medicine and stem cell therapies, drug delivery systems for controlled release, bioartificial organs and tissue engineering, probiotics and functional food applications, and immunoisolation technologies for transplantation, leveraging encapsulation’s ability to protect and deliver viable cells, thereby expanding therapeutic applications, accelerating clinical adoption, and driving innovation across biotech and healthcare sectors.

Cell Encapsulation Market Dynamics and Trends

Driver: Rising Demand for Immune‑Protected Cell Therapies

-

The global cell encapsulation market is becoming highly motivated by the need to have immune-protected cell therapies that have long-term therapeutic effects and implantation without immune rejection. Its use in chronic disease including diabetes, neurodegenerative disorders, and ophthalmic applications are growing fast and hospitals, specialty clinics, and research institutions are adopting the practice.

- Firms are utilizing improved biomaterials, hydrogel matrices and immunoisolation technologies to improve cell survival, cell functionality and clinical effectiveness. For instance, in August 2025, Persista Bio showed the effectiveness of its oxygen-supported cell encapsulation system in preclinical models of diabetes allowing long-term viability and functional glycemic regulation of insulin-secreting cells without immunosuppression, indicating a high demand of immune-protective therapies.

- Clinically validated, long-acting, immune-protected cell therapies have increased interest, leading to innovation, investment, and repeated adoption, which contributes to the long-term growth and expansion of the global cell encapsulation market in a wide range of therapeutic applications.

Restraint: Complex Regulatory Pathways and Manufacturing Costs

-

The expensive nature of the specialized encapsulated cell products, which is dictated by the incorporation of superior biomaterials, immunoprotective surfaces, and clinically established formulations, makes it unaffordable and inaccessible in price-sensitive healthcare environments, especially in developing markets.

- The existence of long regulatory permits and complicated manufacturing procedures only worsens market development. Encapsulated cell therapies should be subject to strict biologic and combination product regulations, and have to go through both extensive preclinical and clinical validation. Special equipment, sterile production facilities, and expertise make per-unit costs higher and place obstacles on smaller players.

- Additional expenses, including cold-chain logistics, compliance with international quality standards, and packaging that guarantees the safety of live cell products, restrict its large-scale adoption and market penetration in both developed and developing markets.

Opportunity: Expansion into Emerging Clinical Applications

-

The increasing need of individual and targeted cell-based therapies present great chances to the companies to use the most advanced technologies of microencapsulation and biomaterials. The optimal therapeutic effect of encapsulated cells can be achieved by adjusting them to the requirements of a patient with a variety of health issues, including diabetes, neural degenerative disorders, and optical illnesses.

- These tailored methods are becoming more coupled with digital health solutions, AI-based modeling, and predictive analytics to optimize cell choice, encapsulation parameters, and delivery schedules to enhance precision and therapeutic outcomes of treatment.

- Individualized encapsulated cell therapies enhance differentiation, clinical performance, patient compliance, and market penetration. This creates a significant opportunity for personalized treatment solutions in the rapidly evolving field of cell encapsulation.

Key Trend: Strategic Collaborations and Technological Advancements

-

The current trend experienced in the global cell encapsulation business in which there has been a significant shift towards strategic alliances and acquisitions between biotech companies and major pharmaceutical organizations with an aim of furthering encapsulation technology both in medical and commercial use.

- Practices that focus on technology innovation in micro- and macro-encapsulation systems form innovation-driven alliances. For instance, in August 2023, Eli Lilly purchased Sigilon Therapeutics, and incorporated the Sigilon-owned Afibromer immunoprotective microencapsulation technology into the Lilly R&D pipeline.

- The strategic partnerships and acquisitions make the market credible, speed up clinical translation, and promote the uptake of encapsulated cell therapies in more regions of the world.

Cell-Encapsulation-Market Analysis and Segmental Data

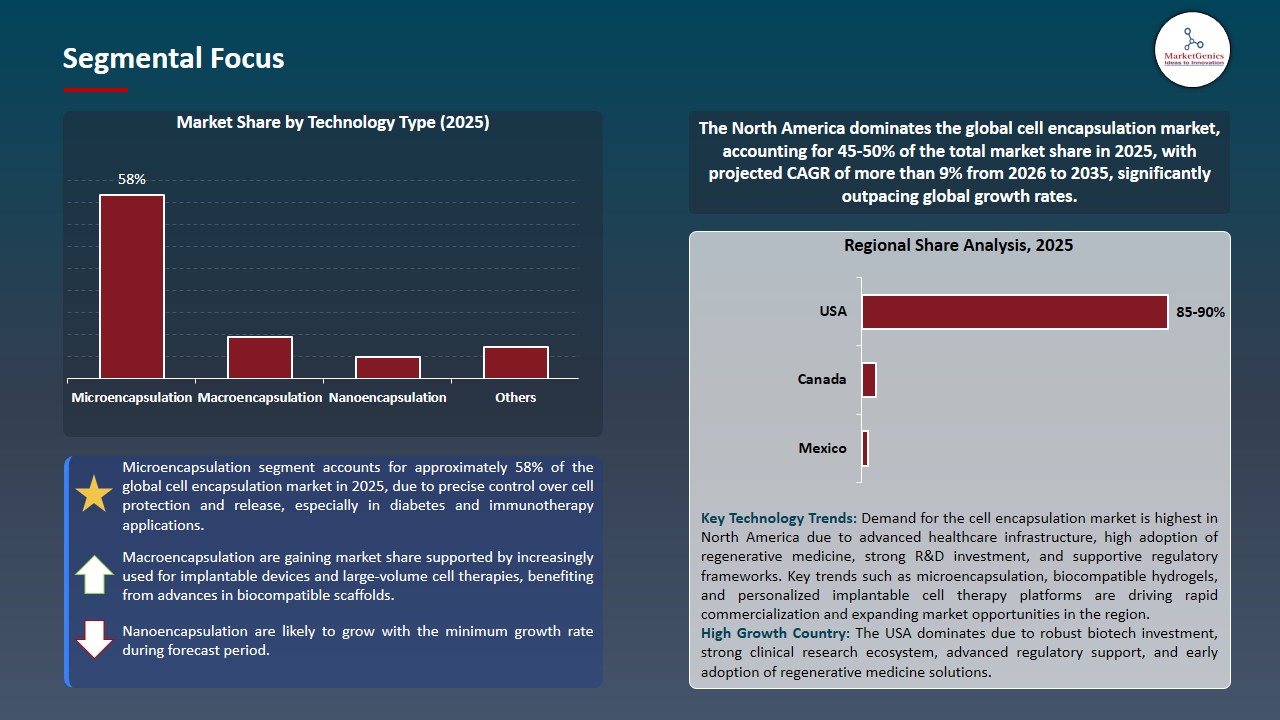

Microencapsulation Dominate Global Cell Encapsulation Market

-

Microencapsulation segment dominates the cell encapsulations market because of its excellent capacity in preserving viable cells, increased regulated release, and prolonged life of cells. Its broad applicability in the clinical and commercial practice in various fields like management of diabetes, immunotherapy, and ocular therapy has led to its high acceptance in clinical and commercial practices.

- Microencapsulation materials and processing technologies continue to be innovative, giving rise to increased application potential. For instance, the dissolvable microcarrier with collagen coating made of alginate developed by Rousselot and IamFluidics in November 2024, which can be used to culture cells at scale, harvest cells efficiently, and in high cell viability to enable advanced manufacture procedures of encapsulated cell therapies and speed up the adoption of translational applications.

- Microencapsulation has managed to preserve its market dominance because of its good clinical validation, capability to be used with a variety of cell types and good performance in controlled release and immunoprotective roles.

North America Leads Global Cell Encapsulation Market Demand

-

North America has dominated the global cell encapsulation market because of high concentration of advanced biotechnology research, earlier adopters of cell based therapies and the high clinical translation of encapsulation technologies. The US and Canada show high levels of demand due to proactive clinical pipelines in diabetes, ophthalmology, oncology and regenerative medicine with a countrywide high level of per-capita healthcare spending and long-term investment in advanced therapeutic platforms.

- The area is also in the advantage of its pivotal position in creating worldwide production and cooperation chains of encapsulated cell therapies. For instance, in December 2025, strategic APAC alliance between Cell Therapies Pty Ltd and ENCell Co., Ltd. to move cell and gene therapies manufacturing forward, reinforcing global production capability to facilitate the scalable deployment of encapsulated cell technologies originating in North American innovation centres.

- North America continues to be the most dominant revenue and innovation generator in the global cell encapsulation market, pursuant to its exceptional biomanufacturing networks, logistics, and robust IP protection.

Cell-Encapsulation-Market Ecosystem

The cell encapsulation market remains moderately consolidated, with a group of technologically advanced players dominating global activity through proprietary platforms and manufacturing expertise. Companies such as ViaCyte, Inc., Sernova Corporation, Eli Lilly and Company, Diatranz Otsuka Ltd., and Living Cell Technologies Limited play a central role by leveraging advanced biomaterials, microencapsulation techniques, and scalable bioprocessing technologies to address therapeutic and research-driven demand.

These leading participants increasingly focus on niche and specialized solutions that accelerate innovation within the market. This includes the development of semi-permeable polymer capsules for immune protection, alginate-based encapsulation systems for cell therapy, and customized microfluidic tools designed to ensure high cell viability and controlled release. Such specialized offerings support applications in diabetes treatment, regenerative medicine, and long-term cell transplantation, thereby expanding the functional scope of encapsulation technologies.

Government agencies, academic institutions, and R&D organizations are also actively investing in advancing encapsulation platforms. For instance, in March 2024, a European public–private research consortium announced progress in hydrogel-based immune-isolation technology for stem cell therapies, demonstrating improved graft survival and reduced inflammatory response, which strengthened translational prospects for encapsulated cell products.

At the corporate level, key players are prioritizing product diversification and integrated solution portfolios that combine encapsulation materials, automated systems, and downstream analytics to improve operational efficiency and reproducibility. In July 2024, a university–industry collaboration reported the use of AI-assisted microcapsule design to optimize capsule uniformity, achieving nearly 20% improvement in encapsulation efficiency and higher consistency in cell viability outcomes. Overall, the market is evolving through consolidation-driven innovation, institutional support, and technology-enabled product expansion.

Recent Development and Strategic Overview

-

In March 2025, Revakinagene taroretcel (ENCELTO), an encapsulated cell-based gene therapy, received its first approval in the United States for the treatment of idiopathic macular telangiectasia (MacTel) type 2 in adults. This is the first FDA-approved therapy using cell encapsulation for this retinal disease.

- In April 2025, Cencora was selected by Neurotech Pharmaceuticals, Inc. to support the commercial launch of its FDA-approved encapsulated cell therapy for adults with idiopathic Macular Telangiectasia type 2 (MacTel) in the United States.

Report Scope

|

Detail |

|

|

Market Size in 2025 |

USD 1.8 Bn |

|

Market Forecast Value in 2035 |

USD 3.6 Bn |

|

Growth Rate (CAGR) |

7.2% |

|

Forecast Period |

2026 – 2035 |

|

Historical Data Available for |

2021 – 2024 |

|

Market Size Units |

US$ Billion for Value |

|

Report Format |

Electronic (PDF) + Excel |

|

North America |

Europe |

Asia Pacific |

Middle East |

Africa |

South America |

|

|

|

|

|

|

|

Companies Covered |

|||||

|

|

|

|

|

|

Cell-Encapsulation-Market Segmentation and Highlights

|

Segment |

Sub-segment |

|

Cell Encapsulation Market, By Technology Type |

|

|

Cell Encapsulation Market, By Material Type |

|

|

Cell Encapsulation Market, By Cell Type |

|

|

Cell Encapsulation Market, By Application |

|

|

Cell Encapsulation Market, By Permeability Type |

|

|

Cell Encapsulation Market, By End-users |

|

Frequently Asked Questions

Table of Contents

- 1. Research Methodology and Assumptions

- 1.1. Definitions

- 1.2. Research Design and Approach

- 1.3. Data Collection Methods

- 1.4. Base Estimates and Calculations

- 1.5. Forecasting Models

- 1.5.1. Key Forecast Factors & Impact Analysis

- 1.6. Secondary Research

- 1.6.1. Open Sources

- 1.6.2. Paid Databases

- 1.6.3. Associations

- 1.7. Primary Research

- 1.7.1. Primary Sources

- 1.7.2. Primary Interviews with Stakeholders across Ecosystem

- 2. Executive Summary

- 2.1. Global Cell Encapsulation Market Outlook

- 2.1.1. Cell Encapsulation Market Size (Value - US$ Bn), and Forecasts, 2021-2035

- 2.1.2. Compounded Annual Growth Rate Analysis

- 2.1.3. Growth Opportunity Analysis

- 2.1.4. Segmental Share Analysis

- 2.1.5. Geographical Share Analysis

- 2.2. Market Analysis and Facts

- 2.3. Supply-Demand Analysis

- 2.4. Competitive Benchmarking

- 2.5. Go-to- Market Strategy

- 2.5.1. Customer/ End-use Industry Assessment

- 2.5.2. Growth Opportunity Data, 2026-2035

- 2.5.2.1. Regional Data

- 2.5.2.2. Country Data

- 2.5.2.3. Segmental Data

- 2.5.3. Identification of Potential Market Spaces

- 2.5.4. GAP Analysis

- 2.5.5. Potential Attractive Price Points

- 2.5.6. Prevailing Market Risks & Challenges

- 2.5.7. Preferred Sales & Marketing Strategies

- 2.5.8. Key Recommendations and Analysis

- 2.5.9. A Way Forward

- 2.1. Global Cell Encapsulation Market Outlook

- 3. Industry Data and Premium Insights

- 3.1. Global Healthcare & Pharmaceutical Industry Overview, 2025

- 3.1.1. Healthcare & Pharmaceutical Industry Ecosystem Analysis

- 3.1.2. Key Trends for Healthcare & Pharmaceutical Industry

- 3.1.3. Regional Distribution for Healthcare & Pharmaceutical Industry

- 3.2. Supplier Customer Data

- 3.3. Technology Roadmap and Developments

- 3.4. Trade Analysis

- 3.4.1. Import & Export Analysis, 2025

- 3.4.2. Top Importing Countries

- 3.4.3. Top Exporting Countries

- 3.5. Trump Tariff Impact Analysis

- 3.5.1. Manufacturer

- 3.5.1.1. Based on the component & Raw material

- 3.5.2. Supply Chain

- 3.5.3. End Consumer

- 3.5.1. Manufacturer

- 3.6. Raw Material Analysis

- 3.1. Global Healthcare & Pharmaceutical Industry Overview, 2025

- 4. Market Overview

- 4.1. Market Dynamics

- 4.1.1. Drivers

- 4.1.1.1. Rising prevalence of chronic and degenerative diseases boosting demand for cell-based therapies.

- 4.1.1.2. Advancements in biomaterials, microencapsulation technologies, and regenerative medicine.

- 4.1.1.3. Growing focus on personalized medicine and long-term targeted drug delivery systems.

- 4.1.2. Restraints

- 4.1.2.1. High manufacturing costs and complex production processes.

- 4.1.2.2. Stringent regulatory requirements and lengthy clinical approval timelines.

- 4.1.1. Drivers

- 4.2. Key Trend Analysis

- 4.3. Regulatory Framework

- 4.3.1. Key Regulations, Norms, and Subsidies, by Key Countries

- 4.3.2. Tariffs and Standards

- 4.3.3. Impact Analysis of Regulations on the Market

- 4.4. Value Chain Analysis

- 4.4.1. Raw Material Suppliers

- 4.4.2. Manufacturers

- 4.4.3. Dealers/ Distributors

- 4.4.4. End-Users/ Customers

- 4.5. Porter’s Five Forces Analysis

- 4.6. PESTEL Analysis

- 4.7. Global Cell Encapsulation Market Demand

- 4.7.1. Historical Market Size – Value (US$ Bn), 2020-2024

- 4.7.2. Current and Future Market Size – Value (US$ Bn), 2026–2035

- 4.7.2.1. Y-o-Y Growth Trends

- 4.7.2.2. Absolute $ Opportunity Assessment

- 4.1. Market Dynamics

- 5. Competition Landscape

- 5.1. Competition structure

- 5.1.1. Fragmented v/s consolidated

- 5.2. Company Share Analysis, 2025

- 5.2.1. Global Company Market Share

- 5.2.2. By Region

- 5.2.2.1. North America

- 5.2.2.2. Europe

- 5.2.2.3. Asia Pacific

- 5.2.2.4. Middle East

- 5.2.2.5. Africa

- 5.2.2.6. South America

- 5.3. Product Comparison Matrix

- 5.3.1. Specifications

- 5.3.2. Market Positioning

- 5.3.3. Pricing

- 5.1. Competition structure

- 6. Global Cell Encapsulation Market Analysis, by Technology Type

- 6.1. Key Segment Analysis

- 6.2. Cell Encapsulation Market Size (Value - US$ Bn), Analysis, and Forecasts, by Technology Type, 2021-2035

- 6.2.1. Microencapsulation

- 6.2.1.1. Spray Drying

- 6.2.1.2. Coacervation

- 6.2.1.3. Emulsion

- 6.2.1.4. Liposome Encapsulation

- 6.2.2. Macroencapsulation

- 6.2.2.1. Hollow Fiber

- 6.2.2.2. Diffusion Chambers

- 6.2.2.3. Immunoisolation Devices

- 6.2.3. Nanoencapsulation

- 6.2.3.1. Polymeric Nanoparticles

- 6.2.3.2. Lipid-based Nanoencapsulation

- 6.2.3.3. Inorganic Nanoencapsulation

- 6.2.1. Microencapsulation

- 7. Global Cell Encapsulation Market Analysis, by Material Type

- 7.1. Key Segment Analysis

- 7.2. Cell Encapsulation Market Size (Value - US$ Bn), Analysis, and Forecasts, by Material Type, 2021-2035

- 7.2.1. Natural Polymers

- 7.2.1.1. Alginate

- 7.2.1.2. Chitosan

- 7.2.1.3. Collagen

- 7.2.1.4. Others

- 7.2.2. Synthetic Polymers

- 7.2.2.1. Polyethylene Glycol (PEG)

- 7.2.2.2. Polylactic Acid (PLA)

- 7.2.2.3. Polylactic-co-Glycolic Acid (PLGA)

- 7.2.2.4. Polyvinyl Alcohol (PVA)

- 7.2.2.5. Others

- 7.2.3. Hybrid Materials

- 7.2.1. Natural Polymers

- 8. Global Cell Encapsulation Market Analysis, by Cell Type

- 8.1. Key Segment Analysis

- 8.2. Cell Encapsulation Market Size (Value - US$ Bn), Analysis, and Forecasts, by Cell Type, 2021-2035

- 8.2.1. Stem Cells

- 8.2.1.1. Embryonic Stem Cells

- 8.2.1.2. Mesenchymal Stem Cells

- 8.2.1.3. Induced Pluripotent Stem Cells

- 8.2.2. Islet Cells

- 8.2.2.1. Pancreatic Beta Cells

- 8.2.2.2. Alpha Cells

- 8.2.3. Hepatocytes

- 8.2.4. Chondrocytes

- 8.2.5. Neural Cells

- 8.2.6. Cancer Cells (for research)

- 8.2.7. Genetically Modified Cells

- 8.2.1. Stem Cells

- 9. Global Cell Encapsulation Market Analysis, by Application

- 9.1. Key Segment Analysis

- 9.2. Cell Encapsulation Market Size (Value - US$ Bn), Analysis, and Forecasts, by Application, 2021-2035

- 9.2.1. Cell Therapy

- 9.2.1.1. Regenerative Medicine

- 9.2.1.2. Immunotherapy

- 9.2.1.3. Gene Therapy

- 9.2.2. Drug Delivery Systems

- 9.2.2.1. Targeted Drug Delivery

- 9.2.2.2. Sustained Release Formulations

- 9.2.2.3. Combination Therapy

- 9.2.3. Tissue Engineering

- 9.2.3.1. Cartilage Regeneration

- 9.2.3.2. Bone Regeneration

- 9.2.3.3. Organ Tissue Development

- 9.2.4. Bioartificial Organs

- 9.2.4.1. Bioartificial Pancreas

- 9.2.4.2. Bioartificial Liver

- 9.2.5. Cell-based Biosensors

- 9.2.6. Research & Development

- 9.2.6.1. In Vitro Studies

- 9.2.6.2. 3D Cell Culture Models

- 9.2.1. Cell Therapy

- 10. Global Cell Encapsulation Market Analysis, by Permeability Type

- 10.1. Key Segment Analysis

- 10.2. Cell Encapsulation Market Size (Value - US$ Bn), Analysis, and Forecasts, by Permeability Type, 2021-2035

- 10.2.1. Immunoprotective

- 10.2.1.1. Selective Permeability

- 10.2.1.2. Complete Immunoisolation

- 10.2.2. Semi-permeable

- 10.2.2.1. Nutrient Permeable

- 10.2.2.2. Oxygen Permeable

- 10.2.3. Controlled Release

- 10.2.3.1. Time-dependent Release

- 10.2.3.2. Stimulus-responsive Release

- 10.2.1. Immunoprotective

- 11. Global Cell Encapsulation Market Analysis, by End-users

- 11.1. Key Segment Analysis

- 11.2. Cell Encapsulation Market Size (Value - US$ Bn), Analysis, and Forecasts, by End-users, 2021-2035

- 11.2.1. Pharmaceutical & Biotechnology

- 11.2.2. Healthcare & Clinical Research

- 11.2.3. Academic & Research Institutions

- 11.2.4. Contract Manufacturing Organizations (CMOs)

- 11.2.5. Diagnostic Industry

- 12. Global Cell Encapsulation Market Analysis and Forecasts, by Region

- 12.1. Key Findings

- 12.2. Cell Encapsulation Market Size (Value - US$ Bn), Analysis, and Forecasts, by Region, 2021-2035

- 12.2.1. North America

- 12.2.2. Europe

- 12.2.3. Asia Pacific

- 12.2.4. Middle East

- 12.2.5. Africa

- 12.2.6. South America

- 13. North America Cell Encapsulation Market Analysis

- 13.1. Key Segment Analysis

- 13.2. Regional Snapshot

- 13.3. North America Cell Encapsulation Market Size (Value - US$ Bn), Analysis, and Forecasts, 2021-2035

- 13.3.1. Technology Type

- 13.3.2. Material Type

- 13.3.3. Cell Type

- 13.3.4. Application

- 13.3.5. Permeability Type

- 13.3.6. End-users

- 13.3.7. Country

- 13.3.7.1. USA

- 13.3.7.2. Canada

- 13.3.7.3. Mexico

- 13.4. USA Cell Encapsulation Market

- 13.4.1. Country Segmental Analysis

- 13.4.2. Technology Type

- 13.4.3. Material Type

- 13.4.4. Cell Type

- 13.4.5. Application

- 13.4.6. Permeability Type

- 13.4.7. End-users

- 13.5. Canada Cell Encapsulation Market

- 13.5.1. Country Segmental Analysis

- 13.5.2. Technology Type

- 13.5.3. Material Type

- 13.5.4. Cell Type

- 13.5.5. Application

- 13.5.6. Permeability Type

- 13.5.7. End-users

- 13.6. Mexico Cell Encapsulation Market

- 13.6.1. Country Segmental Analysis

- 13.6.2. Technology Type

- 13.6.3. Material Type

- 13.6.4. Cell Type

- 13.6.5. Application

- 13.6.6. Permeability Type

- 13.6.7. End-users

- 14. Europe Cell Encapsulation Market Analysis

- 14.1. Key Segment Analysis

- 14.2. Regional Snapshot

- 14.3. Europe Cell Encapsulation Market Size (Value - US$ Bn), Analysis, and Forecasts, 2021-2035

- 14.3.1. Technology Type

- 14.3.2. Material Type

- 14.3.3. Cell Type

- 14.3.4. Application

- 14.3.5. Permeability Type

- 14.3.6. End-users

- 14.3.7. Country

- 14.3.7.1. Germany

- 14.3.7.2. United Kingdom

- 14.3.7.3. France

- 14.3.7.4. Italy

- 14.3.7.5. Spain

- 14.3.7.6. Netherlands

- 14.3.7.7. Nordic Countries

- 14.3.7.8. Poland

- 14.3.7.9. Russia & CIS

- 14.3.7.10. Rest of Europe

- 14.4. Germany Cell Encapsulation Market

- 14.4.1. Country Segmental Analysis

- 14.4.2. Technology Type

- 14.4.3. Material Type

- 14.4.4. Cell Type

- 14.4.5. Application

- 14.4.6. Permeability Type

- 14.4.7. End-users

- 14.5. United Kingdom Cell Encapsulation Market

- 14.5.1. Country Segmental Analysis

- 14.5.2. Technology Type

- 14.5.3. Material Type

- 14.5.4. Cell Type

- 14.5.5. Application

- 14.5.6. Permeability Type

- 14.5.7. End-users

- 14.6. France Cell Encapsulation Market

- 14.6.1. Country Segmental Analysis

- 14.6.2. Technology Type

- 14.6.3. Material Type

- 14.6.4. Cell Type

- 14.6.5. Application

- 14.6.6. Permeability Type

- 14.6.7. End-users

- 14.7. Italy Cell Encapsulation Market

- 14.7.1. Country Segmental Analysis

- 14.7.2. Technology Type

- 14.7.3. Material Type

- 14.7.4. Cell Type

- 14.7.5. Application

- 14.7.6. Permeability Type

- 14.7.7. End-users

- 14.8. Spain Cell Encapsulation Market

- 14.8.1. Country Segmental Analysis

- 14.8.2. Technology Type

- 14.8.3. Material Type

- 14.8.4. Cell Type

- 14.8.5. Application

- 14.8.6. Permeability Type

- 14.8.7. End-users

- 14.9. Netherlands Cell Encapsulation Market

- 14.9.1. Country Segmental Analysis

- 14.9.2. Technology Type

- 14.9.3. Material Type

- 14.9.4. Cell Type

- 14.9.5. Application

- 14.9.6. Permeability Type

- 14.9.7. End-users

- 14.10. Nordic Countries Cell Encapsulation Market

- 14.10.1. Country Segmental Analysis

- 14.10.2. Technology Type

- 14.10.3. Material Type

- 14.10.4. Cell Type

- 14.10.5. Application

- 14.10.6. Permeability Type

- 14.10.7. End-users

- 14.11. Poland Cell Encapsulation Market

- 14.11.1. Country Segmental Analysis

- 14.11.2. Technology Type

- 14.11.3. Material Type

- 14.11.4. Cell Type

- 14.11.5. Application

- 14.11.6. Permeability Type

- 14.11.7. End-users

- 14.12. Russia & CIS Cell Encapsulation Market

- 14.12.1. Country Segmental Analysis

- 14.12.2. Technology Type

- 14.12.3. Material Type

- 14.12.4. Cell Type

- 14.12.5. Application

- 14.12.6. Permeability Type

- 14.12.7. End-users

- 14.13. Rest of Europe Cell Encapsulation Market

- 14.13.1. Country Segmental Analysis

- 14.13.2. Technology Type

- 14.13.3. Material Type

- 14.13.4. Cell Type

- 14.13.5. Application

- 14.13.6. Permeability Type

- 14.13.7. End-users

- 15. Asia Pacific Cell Encapsulation Market Analysis

- 15.1. Key Segment Analysis

- 15.2. Regional Snapshot

- 15.3. Asia Pacific Cell Encapsulation Market Size (Value - US$ Bn), Analysis, and Forecasts, 2021-2035

- 15.3.1. Technology Type

- 15.3.2. Material Type

- 15.3.3. Cell Type

- 15.3.4. Application

- 15.3.5. Permeability Type

- 15.3.6. End-users

- 15.3.7. Country

- 15.3.7.1. China

- 15.3.7.2. India

- 15.3.7.3. Japan

- 15.3.7.4. South Korea

- 15.3.7.5. Australia and New Zealand

- 15.3.7.6. Indonesia

- 15.3.7.7. Malaysia

- 15.3.7.8. Thailand

- 15.3.7.9. Vietnam

- 15.3.7.10. Rest of Asia Pacific

- 15.4. China Cell Encapsulation Market

- 15.4.1. Country Segmental Analysis

- 15.4.2. Technology Type

- 15.4.3. Material Type

- 15.4.4. Cell Type

- 15.4.5. Application

- 15.4.6. Permeability Type

- 15.4.7. End-users

- 15.5. India Cell Encapsulation Market

- 15.5.1. Country Segmental Analysis

- 15.5.2. Technology Type

- 15.5.3. Material Type

- 15.5.4. Cell Type

- 15.5.5. Application

- 15.5.6. Permeability Type

- 15.5.7. End-users

- 15.6. Japan Cell Encapsulation Market

- 15.6.1. Country Segmental Analysis

- 15.6.2. Technology Type

- 15.6.3. Material Type

- 15.6.4. Cell Type

- 15.6.5. Application

- 15.6.6. Permeability Type

- 15.6.7. End-users

- 15.7. South Korea Cell Encapsulation Market

- 15.7.1. Country Segmental Analysis

- 15.7.2. Technology Type

- 15.7.3. Material Type

- 15.7.4. Cell Type

- 15.7.5. Application

- 15.7.6. Permeability Type

- 15.7.7. End-users

- 15.8. Australia and New Zealand Cell Encapsulation Market

- 15.8.1. Country Segmental Analysis

- 15.8.2. Technology Type

- 15.8.3. Material Type

- 15.8.4. Cell Type

- 15.8.5. Application

- 15.8.6. Permeability Type

- 15.8.7. End-users

- 15.9. Indonesia Cell Encapsulation Market

- 15.9.1. Country Segmental Analysis

- 15.9.2. Technology Type

- 15.9.3. Material Type

- 15.9.4. Cell Type

- 15.9.5. Application

- 15.9.6. Permeability Type

- 15.9.7. End-users

- 15.10. Malaysia Cell Encapsulation Market

- 15.10.1. Country Segmental Analysis

- 15.10.2. Technology Type

- 15.10.3. Material Type

- 15.10.4. Cell Type

- 15.10.5. Application

- 15.10.6. Permeability Type

- 15.10.7. End-users

- 15.11. Thailand Cell Encapsulation Market

- 15.11.1. Country Segmental Analysis

- 15.11.2. Technology Type

- 15.11.3. Material Type

- 15.11.4. Cell Type

- 15.11.5. Application

- 15.11.6. Permeability Type

- 15.11.7. End-users

- 15.12. Vietnam Cell Encapsulation Market

- 15.12.1. Country Segmental Analysis

- 15.12.2. Technology Type

- 15.12.3. Material Type

- 15.12.4. Cell Type

- 15.12.5. Application

- 15.12.6. Permeability Type

- 15.12.7. End-users

- 15.13. Rest of Asia Pacific Cell Encapsulation Market

- 15.13.1. Country Segmental Analysis

- 15.13.2. Technology Type

- 15.13.3. Material Type

- 15.13.4. Cell Type

- 15.13.5. Application

- 15.13.6. Permeability Type

- 15.13.7. End-users

- 16. Middle East Cell Encapsulation Market Analysis

- 16.1. Key Segment Analysis

- 16.2. Regional Snapshot

- 16.3. Middle East Cell Encapsulation Market Size (Value - US$ Bn), Analysis, and Forecasts, 2021-2035

- 16.3.1. Technology Type

- 16.3.2. Material Type

- 16.3.3. Cell Type

- 16.3.4. Application

- 16.3.5. Permeability Type

- 16.3.6. End-users

- 16.3.7. Country

- 16.3.7.1. Turkey

- 16.3.7.2. UAE

- 16.3.7.3. Saudi Arabia

- 16.3.7.4. Israel

- 16.3.7.5. Rest of Middle East

- 16.4. Turkey Cell Encapsulation Market

- 16.4.1. Country Segmental Analysis

- 16.4.2. Technology Type

- 16.4.3. Material Type

- 16.4.4. Cell Type

- 16.4.5. Application

- 16.4.6. Permeability Type

- 16.4.7. End-users

- 16.5. UAE Cell Encapsulation Market

- 16.5.1. Country Segmental Analysis

- 16.5.2. Technology Type

- 16.5.3. Material Type

- 16.5.4. Cell Type

- 16.5.5. Application

- 16.5.6. Permeability Type

- 16.5.7. End-users

- 16.6. Saudi Arabia Cell Encapsulation Market

- 16.6.1. Country Segmental Analysis

- 16.6.2. Technology Type

- 16.6.3. Material Type

- 16.6.4. Cell Type

- 16.6.5. Application

- 16.6.6. Permeability Type

- 16.6.7. End-users

- 16.7. Israel Cell Encapsulation Market

- 16.7.1. Country Segmental Analysis

- 16.7.2. Technology Type

- 16.7.3. Material Type

- 16.7.4. Cell Type

- 16.7.5. Application

- 16.7.6. Permeability Type

- 16.7.7. End-users

- 16.8. Rest of Middle East Cell Encapsulation Market

- 16.8.1. Country Segmental Analysis

- 16.8.2. Technology Type

- 16.8.3. Material Type

- 16.8.4. Cell Type

- 16.8.5. Application

- 16.8.6. Permeability Type

- 16.8.7. End-users

- 17. Africa Cell Encapsulation Market Analysis

- 17.1. Key Segment Analysis

- 17.2. Regional Snapshot

- 17.3. Africa Cell Encapsulation Market Size (Value - US$ Bn), Analysis, and Forecasts, 2021-2035

- 17.3.1. Technology Type

- 17.3.2. Material Type

- 17.3.3. Cell Type

- 17.3.4. Application

- 17.3.5. Permeability Type

- 17.3.6. End-users

- 17.3.7. Country

- 17.3.7.1. South Africa

- 17.3.7.2. Egypt

- 17.3.7.3. Nigeria

- 17.3.7.4. Algeria

- 17.3.7.5. Rest of Africa

- 17.4. South Africa Cell Encapsulation Market

- 17.4.1. Country Segmental Analysis

- 17.4.2. Technology Type

- 17.4.3. Material Type

- 17.4.4. Cell Type

- 17.4.5. Application

- 17.4.6. Permeability Type

- 17.4.7. End-users

- 17.5. Egypt Cell Encapsulation Market

- 17.5.1. Country Segmental Analysis

- 17.5.2. Technology Type

- 17.5.3. Material Type

- 17.5.4. Cell Type

- 17.5.5. Application

- 17.5.6. Permeability Type

- 17.5.7. End-users

- 17.6. Nigeria Cell Encapsulation Market

- 17.6.1. Country Segmental Analysis

- 17.6.2. Technology Type

- 17.6.3. Material Type

- 17.6.4. Cell Type

- 17.6.5. Application

- 17.6.6. Permeability Type

- 17.6.7. End-users

- 17.7. Algeria Cell Encapsulation Market

- 17.7.1. Country Segmental Analysis

- 17.7.2. Technology Type

- 17.7.3. Material Type

- 17.7.4. Cell Type

- 17.7.5. Application

- 17.7.6. Permeability Type

- 17.7.7. End-users

- 17.8. Rest of Africa Cell Encapsulation Market

- 17.8.1. Country Segmental Analysis

- 17.8.2. Technology Type

- 17.8.3. Material Type

- 17.8.4. Cell Type

- 17.8.5. Application

- 17.8.6. Permeability Type

- 17.8.7. End-users

- 18. South America Cell Encapsulation Market Analysis

- 18.1. Key Segment Analysis

- 18.2. Regional Snapshot

- 18.3. South America Cell Encapsulation Market Size (Value - US$ Bn), Analysis, and Forecasts, 2021-2035

- 18.3.1. Technology Type

- 18.3.2. Material Type

- 18.3.3. Cell Type

- 18.3.4. Application

- 18.3.5. Permeability Type

- 18.3.6. End-users

- 18.3.7. Country

- 18.3.7.1. Brazil

- 18.3.7.2. Argentina

- 18.3.7.3. Rest of South America

- 18.4. Brazil Cell Encapsulation Market

- 18.4.1. Country Segmental Analysis

- 18.4.2. Technology Type

- 18.4.3. Material Type

- 18.4.4. Cell Type

- 18.4.5. Application

- 18.4.6. Permeability Type

- 18.4.7. End-users

- 18.5. Argentina Cell Encapsulation Market

- 18.5.1. Country Segmental Analysis

- 18.5.2. Technology Type

- 18.5.3. Material Type

- 18.5.4. Cell Type

- 18.5.5. Application

- 18.5.6. Permeability Type

- 18.5.7. End-users

- 18.6. Rest of South America Cell Encapsulation Market

- 18.6.1. Country Segmental Analysis

- 18.6.2. Technology Type

- 18.6.3. Material Type

- 18.6.4. Cell Type

- 18.6.5. Application

- 18.6.6. Permeability Type

- 18.6.7. End-users

- 19. Key Players/ Company Profile

- 19.1. 3M Company

- 19.1.1. Company Details/ Overview

- 19.1.2. Company Financials

- 19.1.3. Key Customers and Competitors

- 19.1.4. Business/ Industry Portfolio

- 19.1.5. Product Portfolio/ Specification Details

- 19.1.6. Pricing Data

- 19.1.7. Strategic Overview

- 19.1.8. Recent Developments

- 19.2. Advanced BioMatrix

- 19.3. Astellas Pharma Inc.

- 19.4. Austrianova Singapore Pte Ltd.

- 19.5. Becton, Dickinson and Company (BD)

- 19.6. Beta-O2 Technologies Ltd.

- 19.7. Biogelx Ltd.

- 19.8. BioTime Inc.

- 19.9. Capsulab

- 19.10. Cellular Dynamics International (Fujifilm)

- 19.11. Corning Incorporated

- 19.12. Defymed

- 19.13. Encapsulife

- 19.14. Evonik Industries AG

- 19.15. GE Healthcare (Cytiva)

- 19.16. Living Cell Technologies Limited

- 19.17. Lonza Group AG

- 19.18. Merck KGaA

- 19.19. Prodigest

- 19.20. PromoCell GmbH

- 19.21. Sartorius AG

- 19.22. Sernova Corp.

- 19.23. Eli Lilly and Company (Sigilon Therapeutics)

- 19.24. Sigma-Aldrich (Merck Millipore)

- 19.25. STEMCELL Technologies Inc.

- 19.26. Thermo Fisher Scientific Inc.

- 19.27. Viacyte Inc.

- 19.28. Other Key Players

- 19.1. 3M Company

Note* - This is just tentative list of players. While providing the report, we will cover more number of players based on their revenue and share for each geography

Research Design

Our research design integrates both demand-side and supply-side analysis through a balanced combination of primary and secondary research methodologies. By utilizing both bottom-up and top-down approaches alongside rigorous data triangulation methods, we deliver robust market intelligence that supports strategic decision-making.

MarketGenics' comprehensive research design framework ensures the delivery of accurate, reliable, and actionable market intelligence. Through the integration of multiple research approaches, rigorous validation processes, and expert analysis, we provide our clients with the insights needed to make informed strategic decisions and capitalize on market opportunities.

MarketGenics leverages a dedicated industry panel of experts and a comprehensive suite of paid databases to effectively collect, consolidate, and analyze market intelligence.

Our approach has consistently proven to be reliable and effective in generating accurate market insights, identifying key industry trends, and uncovering emerging business opportunities.

Through both primary and secondary research, we capture and analyze critical company-level data such as manufacturing footprints, including technical centers, R&D facilities, sales offices, and headquarters.

Our expert panel further enhances our ability to estimate market size for specific brands based on validated field-level intelligence.

Our data mining techniques incorporate both parametric and non-parametric methods, allowing for structured data collection, sorting, processing, and cleaning.

Demand projections are derived from large-scale data sets analyzed through proprietary algorithms, culminating in robust and reliable market sizing.

Research Approach

The bottom-up approach builds market estimates by starting with the smallest addressable market units and systematically aggregating them to create comprehensive market size projections.

This method begins with specific, granular data points and builds upward to create the complete market landscape.

Customer Analysis → Segmental Analysis → Geographical Analysis

The top-down approach starts with the broadest possible market data and systematically narrows it down through a series of filters and assumptions to arrive at specific market segments or opportunities.

This method begins with the big picture and works downward to increasingly specific market slices.

TAM → SAM → SOM

Research Methods

Desk / Secondary Research

While analysing the market, we extensively study secondary sources, directories, and databases to identify and collect information useful for this technical, market-oriented, and commercial report. Secondary sources that we utilize are not only the public sources, but it is a combination of Open Source, Associations, Paid Databases, MG Repository & Knowledgebase, and others.

- Company websites, annual reports, financial reports, broker reports, and investor presentations

- National government documents, statistical databases and reports

- News articles, press releases and web-casts specific to the companies operating in the market, Magazines, reports, and others

- We gather information from commercial data sources for deriving company specific data such as segmental revenue, share for geography, product revenue, and others

- Internal and external proprietary databases (industry-specific), relevant patent, and regulatory databases

- Governing Bodies, Government Organizations

- Relevant Authorities, Country-specific Associations for Industries

We also employ the model mapping approach to estimate the product level market data through the players' product portfolio

Primary Research

Primary research/ interviews is vital in analyzing the market. Most of the cases involves paid primary interviews. Primary sources include primary interviews through e-mail interactions, telephonic interviews, surveys as well as face-to-face interviews with the different stakeholders across the value chain including several industry experts.

| Type of Respondents | Number of Primaries |

|---|---|

| Tier 2/3 Suppliers | ~20 |

| Tier 1 Suppliers | ~25 |

| End-users | ~25 |

| Industry Expert/ Panel/ Consultant | ~30 |

| Total | ~100 |

MG Knowledgebase

• Repository of industry blog, newsletter and case studies

• Online platform covering detailed market reports, and company profiles

Forecasting Factors and Models

Forecasting Factors

- Historical Trends – Past market patterns, cycles, and major events that shaped how markets behave over time. Understanding past trends helps predict future behavior.

- Industry Factors – Specific characteristics of the industry like structure, regulations, and innovation cycles that affect market dynamics.

- Macroeconomic Factors – Economic conditions like GDP growth, inflation, and employment rates that affect how much money people have to spend.

- Demographic Factors – Population characteristics like age, income, and location that determine who can buy your product.

- Technology Factors – How quickly people adopt new technology and how much technology infrastructure exists.

- Regulatory Factors – Government rules, laws, and policies that can help or restrict market growth.

- Competitive Factors – Analyzing competition structure such as degree of competition and bargaining power of buyers and suppliers.

Forecasting Models / Techniques

Multiple Regression Analysis

- Identify and quantify factors that drive market changes

- Statistical modeling to establish relationships between market drivers and outcomes

Time Series Analysis – Seasonal Patterns

- Understand regular cyclical patterns in market demand

- Advanced statistical techniques to separate trend, seasonal, and irregular components

Time Series Analysis – Trend Analysis

- Identify underlying market growth patterns and momentum

- Statistical analysis of historical data to project future trends

Expert Opinion – Expert Interviews

- Gather deep industry insights and contextual understanding

- In-depth interviews with key industry stakeholders

Multi-Scenario Development

- Prepare for uncertainty by modeling different possible futures

- Creating optimistic, pessimistic, and most likely scenarios

Time Series Analysis – Moving Averages

- Sophisticated forecasting for complex time series data

- Auto-regressive integrated moving average models with seasonal components

Econometric Models

- Apply economic theory to market forecasting

- Sophisticated economic models that account for market interactions

Expert Opinion – Delphi Method

- Harness collective wisdom of industry experts

- Structured, multi-round expert consultation process

Monte Carlo Simulation

- Quantify uncertainty and probability distributions

- Thousands of simulations with varying input parameters

Research Analysis

Our research framework is built upon the fundamental principle of validating market intelligence from both demand and supply perspectives. This dual-sided approach ensures comprehensive market understanding and reduces the risk of single-source bias.

Demand-Side Analysis: We understand end-user/application behavior, preferences, and market needs along with the penetration of the product for specific application.

Supply-Side Analysis: We estimate overall market revenue, analyze the segmental share along with industry capacity, competitive landscape, and market structure.

Validation & Evaluation

Data triangulation is a validation technique that uses multiple methods, sources, or perspectives to examine the same research question, thereby increasing the credibility and reliability of research findings. In market research, triangulation serves as a quality assurance mechanism that helps identify and minimize bias, validate assumptions, and ensure accuracy in market estimates.

- Data Source Triangulation – Using multiple data sources to examine the same phenomenon

- Methodological Triangulation – Using multiple research methods to study the same research question

- Investigator Triangulation – Using multiple researchers or analysts to examine the same data

- Theoretical Triangulation – Using multiple theoretical perspectives to interpret the same data

Custom Market Research Services

We will customise the research for you, in case the report listed above does not meet your requirements.

Get 10% Free Customisation