Hematology Analyzers and Reagents Market Size, Share & Trends Analysis Report by Product Type (Hematology Analyzers, Hematology Reagents), Technology, Test Type, Sample Type, End-Users, Distribution Channel, and Geography (North America, Europe, Asia Pacific, Middle East, Africa, and South America) – Global Industry Data, Trends, and Forecasts, 2026–2035

|

|

|

Segmental Data Insights |

|

|

Demand Trends |

|

|

Competitive Landscape |

|

|

Strategic Development |

|

|

Future Outlook & Opportunities |

|

Hematology Analyzers and Reagents Market Size, Share, and Growth

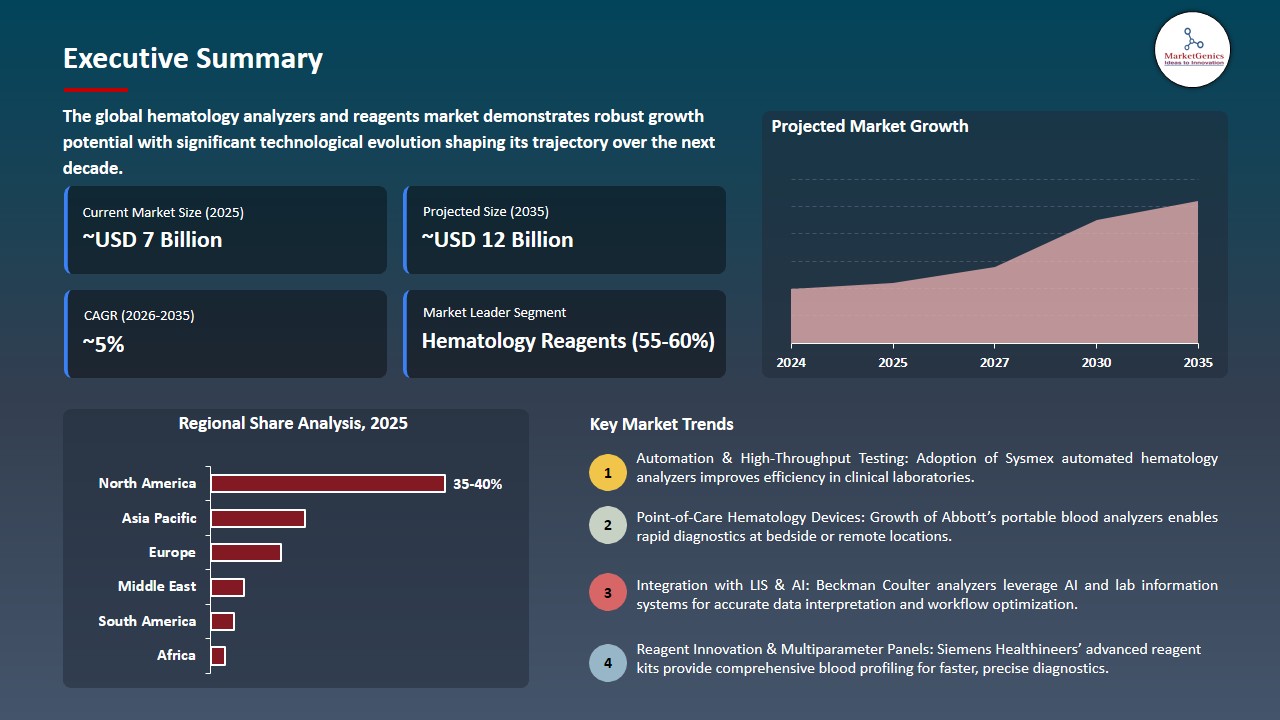

The global hematology analyzers and reagents market is witnessing strong growth, valued at USD 7.3 billion in 2025 and projected to reach USD 12.4 billion by 2035, expanding at a CAGR of 5.4% during the forecast period. Asia Pacific is the fastest-growing hematology analyzers and reagents market due to rising healthcare infrastructure, increasing prevalence of blood disorders, rapid adoption of advanced diagnostic technologies, and growing demand for affordable and efficient laboratory solutions.

Dan Zortman, CEO of Sysmex America, said, “Efficiency and precision are key to the fast and accurate diagnostic results that laboratorians rely on to support healthcare providers so they can deliver quality care, Sysmex America’s XQ-320 provides low volume labs and hospitals the opportunity to deliver high quality results with a shorter turnaround time”.

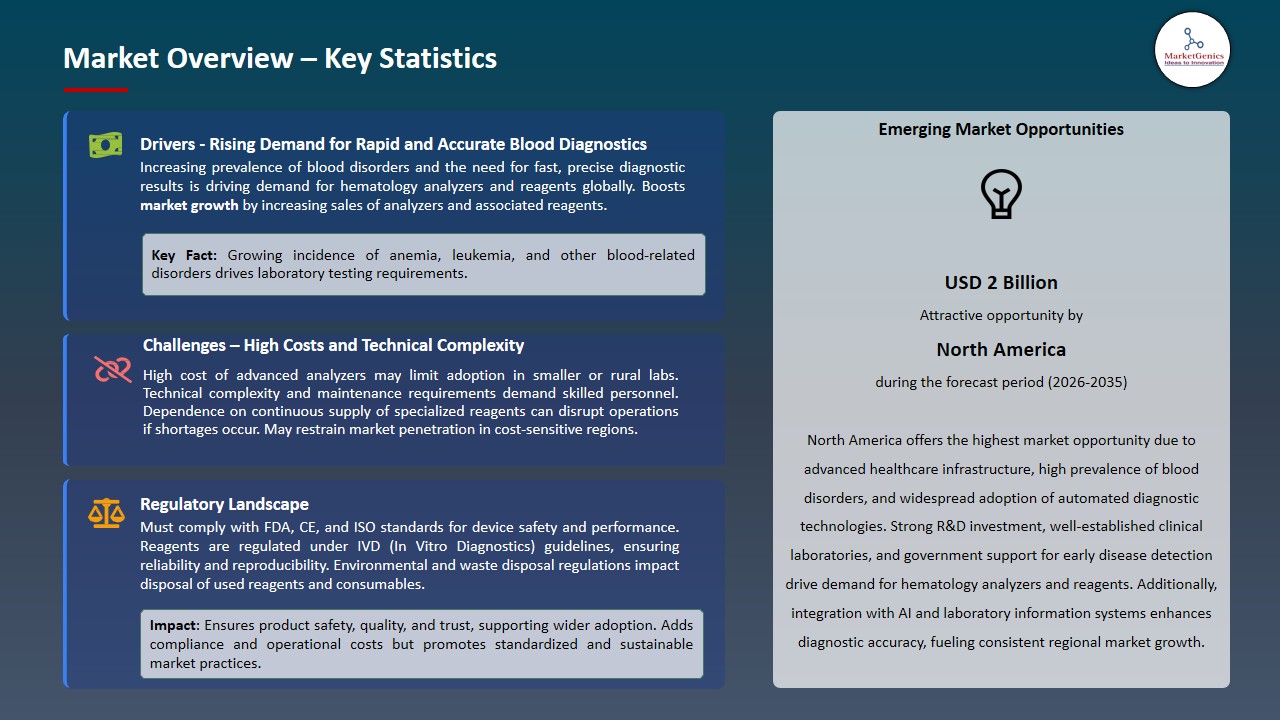

The increasing prevalence of blood-related diseases like anemia, leukemia, hemophilia, thalassemia and other hematologic diseases is a significant contributor to the hematology analyzers and reagents market. These conditions necessitate constant blood profiling, surveillance, and early-stage diagnosis, placing a strain on automated hematology analyzers and special reagents in hospitals, diagnostic labs, and research institutions.

The hematology analyzers and reagents market is experiencing tremendous growth prospects especially in the terms of reagent development such as environmentally friendly formulations, high specificity assays, and compatibility with several platforms. New reagents improve the quality of the diagnosis, minimize waste and operating expenses, and promote wider interoperability of the analyzers, promoting repeat business and long-term demand of the consumables by the clinical laboratories and healthcare providers.

Key adjacent opportunities for the hematology analyzers and reagents market include expansion of point-of-care and decentralized diagnostics, integration with digital pathology, AI, and laboratory information systems, growth of companion diagnostics in oncology and personalized medicine, outsourcing of diagnostic services to reference labs, rising demand from clinical research and biopharma trials, and increasing adoption of preventive health screening programs in emerging economies.

Hematology Analyzers and Reagents Market Dynamics and Trends

Driver: Advancements in Automated High-Throughput Hematology Systems Enhance Diagnostic Efficiency

-

Technological development in high-throughput automated hematology analyzers is one of the major forces behind the hematology analyzers and reagents market, with healthcare organizations demanding more and more rapid, accurate and scalable diagnostic technologies. Such systems allow high volumes of samples to be processed with little human involvement and hence shortening turnaround time and enhancing laboratory productivity.

- Improved quality control, use of digital data and accurate cell differentiation are some improved features that ensure that the test results are uniform and reliable. The increasing need of blood tests at regular intervals, early detection and management of diseases at hospitals and diagnostic laboratories is driving the implementation of sophisticated automated hematology instruments, which are contributing to the long-term demand of related reagents.

- Sysmex America added the XQ-320 3-part differential analyzer with BeyondCare Quality Monitor, maximum throughput of 70 samples per hour, and sub-60-second CBC results to their automated hematology portfolio in March 2025 and is suitable in the physician office and stat laboratory to facilitate faster and accurate diagnostics with minimal maintenance.

- The new technology of automated high-throughput hematology systems has had a remarkable boost in efficiency in the diagnostic process; faster adoption of analyzers and the long-term increase in reagent usage in clinical labs.

Restraint: Integration Complexity and Regulatory Barriers

-

The hematology analyzers and reagents market is experiencing a significant inhibitory factor because of the capital investment involved in acquiring the sophisticated diagnostic systems. Recent automated hematology analyzers are associated with high upfront expenditures such as purchase of equipment, upgrade of laboratory infrastructure and installation cost. These financial obligations may be daunting on small and mid-sized laboratories, physician office labs and healthcare facilities with limited budgets, especially in emerging and cost-sensitive areas.

- Other factors that limit adoption include the cost of acquisition besides the cost of continuing to operate. Requested routine maintenance, calibration, service contracts and continuous purchase of proprietary reagents greatly add to the overall cost of ownership. High-level systems usually involve highly trained staff and tough compliance on quality, which complicates and increases the cost of operation. Consequently, numerous labs defer upgrades on the system or persist in using older technology with poor functionality and delay the adoption of high-end hematology analyzers.

- The economic obstacles inhibit the growth of markets and prevent their fair access to the latest hematology diagnostics.

Opportunity: Artificial Intelligence Integration Enabling Predictive Analytics and Clinical Decision Support

-

Artificial intelligence integration is an enormous opportunity in the development of hematology analyzers and reagents market because it increases diagnostic quality, workflow, and clinical decision support. Smart systems in hematology, supported by AI, can identify complex patterns of blood cells, detect minor abnormalities, and minimize the idea of manual review of slides with the help of intelligent flagging and classification. Predictive analytics is capable of early disease diagnosis and trend analysis that will facilitate patient management ahead of time.

- Moreover, AI-based data interpretation enhances inter-laboratory standardization and aids in remote monitoring and quality control. With the rising approach to data-driven and precision medicine in healthcare systems, AI-based hematology platforms also provide manufacturers with a chance to provide value-added services, increase services, and build customer retention in the long-term perspective.

- Siemens Healthineers reinforced its leadership in AI-driven diagnostics by advancing its enterprise-wide AI strategy, embedding AI throughout imaging, diagnostics, and clinical decision support platforms in 2025. Utilizing its large installed hardware footprint, proprietary clinical data and AI-enhanced systems like workflow automation and disease pathway management systems.

- AI application is revolutionizing the hematology diagnostics process by enhancing accuracy, providing predictive insights and generating long-term value with sophisticated, data-driven clinical decision support solutions.

Key Trend: Expansion of Compact and Decentralized Hematology Testing Solutions

-

The hematology analyzers and reagents market has been experiencing a robust trend of compact and decentralized testing products as healthcare delivery moves out of the centralized laboratories. Hospitals, outpatient clinics, emergency departments and remote care environments need quick diagnostic outcomes in order to facilitate timely clinical judgments. Small hematology analyzers provide low profile design and high turnaround and reduced complexity of use but did not compromise on analytical performance.

- These systems minimize sampling transportation delays, facilitate near-patient testing, and increase accessibility in resource-constrained settings. Also, reagents optimized on ease and stability are used in complement to decentralized workflows. With the increasing focus on healthcare systems on point of care testing, operational scalability, and quicker handling of patients, small-scale hematology platforms are becoming indispensable elements of diagnostic infrastructure in the modern world.

- In January 2025, the Vcheck H in-clinic hematology analyzer was introduced by Bionote USA, providing 35 CBC and differential parameters in less than 90 seconds with high throughput (up to 60 samples/hour) and advanced technologies, including fluorescence flow cytometry, sheath flow impedance, and colorimetry, supporting rapid, reliable, decentralized point-of-care diagnostics.

- Point-of-care testing is being made easier, more accessible and timely clinical decisions are being made faster across various healthcare environments due to the adoption of compact and decentralized hematology analyzers.

Hematology-Analyzers-and-Reagents-Market Analysis and Segmental Data

Hematology Reagents Dominate Global Hematology Analyzers and Reagents Market

-

The hematology reagents segment holds a leading position in the global hematology analyzers and reagents market due to its critical role in ensuring accurate and reliable blood analysis. Reagents are essential for performing complete blood counts (CBC), differential counts, reticulocyte analysis, and other specialized tests, which form the backbone of clinical diagnostics.

- Their accuracy is the direct cause of diagnostic outcome, so they are essential in hospitals, diagnostics laboratories and research centers. The rising occurrence of blood disorders, rising routine blood testing and the rising need to detect diseases early is prompting sustained demand of hematology reagents worldwide.

- High-end reagents that are compatible with automated hematology analyzers enhance the accuracy of tests, reproducibility, and efficiency in working with them. Manufacturers keep improving by making reagents more stable, having longer shelf life and multi-parameter analysis. The Sysmex Corporation opened Sysmex Sanand II in April 2025 located in India to make hematology reagents locally to enhance supply chain effectiveness and accessibility to the emerging markets.

- This strengthens the dominance of the segment and its criticality in facilitating operations of diagnosis worldwide.

North America Leads Global Hematology Analyzers and Reagents Market Demand

-

North America continues to dominate the global hematology analyzers and reagents market due to its well-developed healthcare infrastructure, high healthcare spending, and early adoption of advanced diagnostic technologies. Hospitals, clinical laboratories, and research institutions across the region prioritize accurate, rapid, and high-throughput hematology testing, driving steady demand for both analyzers and reagents. The prevalence of chronic diseases, increasing blood disorder cases, and growing routine screening programs further contribute to the region’s strong market growth.

- The strong position of leadership in North America is reinforced by supportive regulatory frameworks, effective reimbursement policies and having a significant market presence. The research and development is continuously invested in to create an innovative approach in analyzer automation, reagent quality and optimization of the workflow. Also, the efforts to raise awareness among patients and the trend of a more personalized possible medicine promote the use of some of the latest solutions in hematology, which further strengthens the need to find a stable and effective diagnostic level.

- These factors collectively ensure North America remains the largest and most influential market for hematology analyzers and reagents globally.

Hematology-Analyzers-and-Reagents-Market Ecosystem

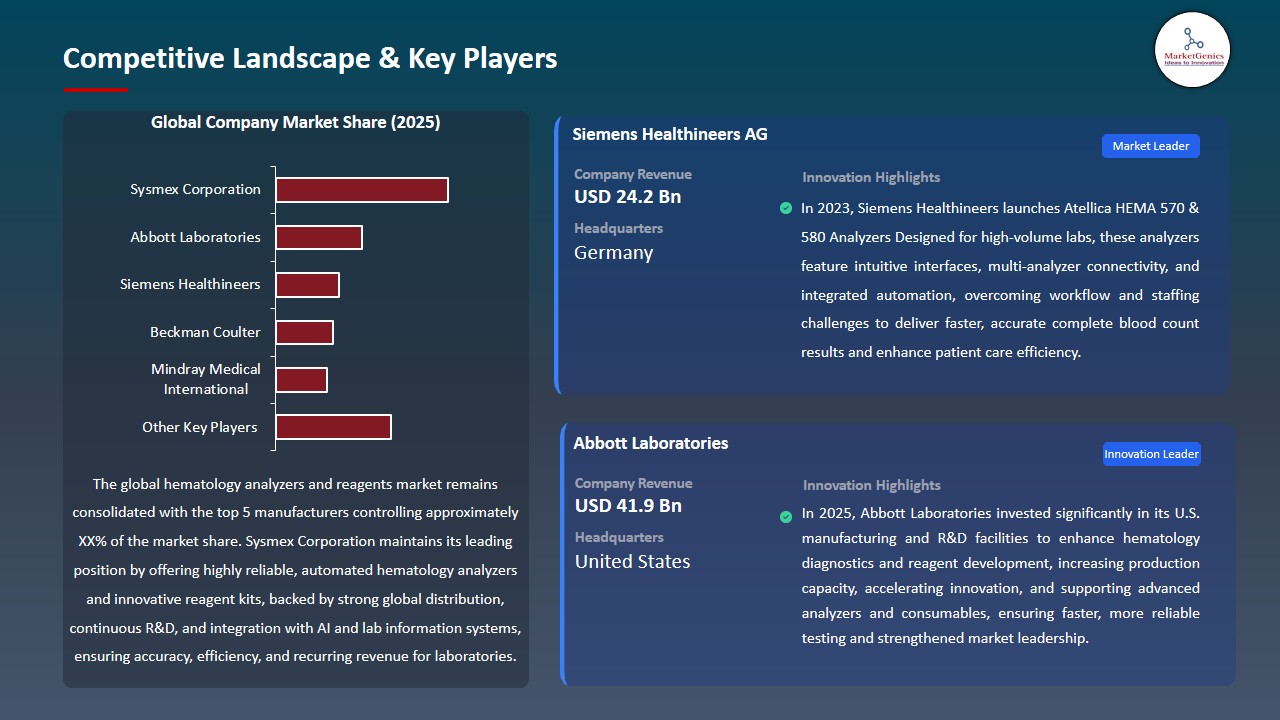

The global hematology analyzers and reagents market is consolidated, with key players including Sysmex Corporation, Abbott Laboratories, Siemens Healthineers, Beckman Coulter, and Mindray Medical International. These companies maintain competitive positions through extensive research and development capabilities, advanced automated and high-throughput hematology systems, and strong expertise in reagent formulation and diagnostic accuracy. Their market leadership is further reinforced by long-standing relationships with hospitals, diagnostic laboratories, and healthcare providers, as well as global distribution networks and strict compliance with regulatory standards such as FDA, CE, and ISO certifications.

The market value chain encompasses the design and development of automated analyzers, reagent formulation and testing, software and AI integration for predictive diagnostics, system customization for diverse laboratory workflows, on-site installation and commissioning, and post-deployment services including training, maintenance, and remote monitoring. These stages ensure accurate test results, regulatory compliance, and efficient laboratory operations.

High entry barriers exist due to substantial capital investments, specialized technological expertise, and stringent regulatory requirements. Continuous innovations such as AI-enabled data analytics, compact point-of-care analyzers, and advanced multi-parameter reagents are driving product differentiation, improving operational efficiency, and supporting sustained market growth globally.

Recent Development and Strategic Overview:

-

In June 2025, Sysmex Corporation received Health Canada approval for its CN-3000 and CN-6000 automated blood coagulation analyzers, offering high-throughput, fully automated hemostasis testing with smart workflow features and expandable sample capacity, enhancing laboratory efficiency, accuracy, and patient care.

- In June 2024, Horiba launched the updated Yumizen H550 hematology analyzer range, including H550E, H500E CT, and H500E OT, featuring CoRA technology, AI-based infectious disease screening, and DoubleDiff analysis, delivering CBC/DIFF with ESR in 60 seconds for compact, affordable, and versatile use in small to mid-throughput laboratories.

Report Scope

|

Detail |

|

|

Market Size in 2025 |

USD 7.3 Bn |

|

Market Forecast Value in 2035 |

USD 12.4 Bn |

|

Growth Rate (CAGR) |

5.4% |

|

Forecast Period |

2026 – 2035 |

|

Historical Data Available for |

2021 – 2024 |

|

Market Size Units |

US$ Billion for Value Thousand Units for Volume |

|

Report Format |

Electronic (PDF) + Excel |

|

North America |

Europe |

Asia Pacific |

Middle East |

Africa |

South America |

|

|

|

|

|

|

|

Companies Covered |

|||||

|

|

|

|

|

|

Nuclear-Robots-Market Segmentation and Highlights

|

Segment |

Sub-segment |

|

Hematology Analyzers and Reagents Market, By Product Type |

|

|

Hematology Analyzers and Reagents Market, By Technology |

|

|

Hematology Analyzers and Reagents Market, By Test Type |

|

|

Hematology Analyzers and Reagents Market, By Sample Type |

|

|

Hematology Analyzers and Reagents Market, By End-Users |

|

|

Hematology Analyzers and Reagents Market, By Distribution Channel |

|

Frequently Asked Questions

Table of Contents

- 1. Research Methodology and Assumptions

- 1.1. Definitions

- 1.2. Research Design and Approach

- 1.3. Data Collection Methods

- 1.4. Base Estimates and Calculations

- 1.5. Forecasting Models

- 1.5.1. Key Forecast Factors & Impact Analysis

- 1.6. Secondary Research

- 1.6.1. Open Sources

- 1.6.2. Paid Databases

- 1.6.3. Associations

- 1.7. Primary Research

- 1.7.1. Primary Sources

- 1.7.2. Primary Interviews with Stakeholders across Ecosystem

- 2. Executive Summary

- 2.1. Global Hematology Analyzers and Reagents Market Outlook

- 2.1.1. Hematology Analyzers and Reagents Market Size Value (US$ Bn), and Forecasts, 2021-2035

- 2.1.2. Compounded Annual Growth Rate Analysis

- 2.1.3. Growth Opportunity Analysis

- 2.1.4. Segmental Share Analysis

- 2.1.5. Geographical Share Analysis

- 2.2. Market Analysis and Facts

- 2.3. Supply-Demand Analysis

- 2.4. Competitive Benchmarking

- 2.5. Go-to- Market Strategy

- 2.5.1. Customer/ End-use Industry Assessment

- 2.5.2. Growth Opportunity Data, 2026-2035

- 2.5.2.1. Regional Data

- 2.5.2.2. Country Data

- 2.5.2.3. Segmental Data

- 2.5.3. Identification of Potential Market Spaces

- 2.5.4. GAP Analysis

- 2.5.5. Potential Attractive Price Points

- 2.5.6. Prevailing Market Risks & Challenges

- 2.5.7. Preferred Sales & Marketing Strategies

- 2.5.8. Key Recommendations and Analysis

- 2.5.9. A Way Forward

- 2.1. Global Hematology Analyzers and Reagents Market Outlook

- 3. Industry Data and Premium Insights

- 3.1. Global Healthcare & Pharmaceutical Industry Overview, 2025

- 3.1.1. Healthcare & Pharmaceutical Industry Ecosystem Analysis

- 3.1.2. Key Trends for Healthcare & Pharmaceutical Industry

- 3.1.3. Regional Distribution for Healthcare & Pharmaceutical Industry

- 3.2. Supplier Customer Data

- 3.3. Technology Roadmap and Developments

- 3.4. Trade Analysis

- 3.4.1. Import & Export Analysis, 2025

- 3.4.2. Top Importing Countries

- 3.4.3. Top Exporting Countries

- 3.5. Trump Tariff Impact Analysis

- 3.5.1. Manufacturer

- 3.5.1.1. Based on the component & Raw material

- 3.5.2. Supply Chain

- 3.5.3. End Consumer

- 3.5.1. Manufacturer

- 3.6. Raw Material Analysis

- 3.1. Global Healthcare & Pharmaceutical Industry Overview, 2025

- 4. Market Overview

- 4.1. Market Dynamics

- 4.1.1. Drivers

- 4.1.1.1. Increasing prevalence of blood disorders and chronic diseases driving diagnostic testing demand.

- 4.1.1.2. Technological advancements in automated and high-throughput hematology analyzers improving efficiency.

- 4.1.1.3. Growing adoption of point-of-care and decentralized diagnostic solutions in healthcare settings.

- 4.1.2. Restraints

- 4.1.2.1. High acquisition, maintenance, and reagent costs of advanced hematology systems.

- 4.1.2.2. Shortage of skilled laboratory professionals and complex regulatory compliance requirements.

- 4.1.1. Drivers

- 4.2. Key Trend Analysis

- 4.3. Regulatory Framework

- 4.3.1. Key Regulations, Norms, and Subsidies, by Key Countries

- 4.3.2. Tariffs and Standards

- 4.3.3. Impact Analysis of Regulations on the Market

- 4.4. Value Chain/ Ecosystem Analysis

- 4.5. Porter’s Five Forces Analysis

- 4.6. PESTEL Analysis

- 4.7. Global Hematology Analyzers and Reagents Market Demand

- 4.7.1. Historical Market Size – Value (US$ Bn), 2020-2024

- 4.7.2. Current and Future Market Size – Value (US$ Bn), 2026–2035

- 4.7.2.1. Y-o-Y Growth Trends

- 4.7.2.2. Absolute $ Opportunity Assessment

- 4.1. Market Dynamics

- 5. Competition Landscape

- 5.1. Competition structure

- 5.1.1. Fragmented v/s consolidated

- 5.2. Company Share Analysis, 2025

- 5.2.1. Global Company Market Share

- 5.2.2. By Region

- 5.2.2.1. North America

- 5.2.2.2. Europe

- 5.2.2.3. Asia Pacific

- 5.2.2.4. Middle East

- 5.2.2.5. Africa

- 5.2.2.6. South America

- 5.3. Product Comparison Matrix

- 5.3.1. Specifications

- 5.3.2. Market Positioning

- 5.3.3. Pricing

- 5.1. Competition structure

- 6. Global Hematology Analyzers and Reagents Market Analysis, by Product Type

- 6.1. Key Segment Analysis

- 6.2. Hematology Analyzers and Reagents Market Size Value (US$ Bn), Analysis, and Forecasts, by Product Type, 2021-2035

- 6.2.1. Hematology Analyzers

- 6.2.1.1. Automatic Hematology Analyzers

- 6.2.1.2. 3-Part Differential Analyzers

- 6.2.1.3. 5-Part Differential Analyzers

- 6.2.1.4. 6-Part Differential Analyzers

- 6.2.1.5. Semi-Automatic Hematology Analyzers

- 6.2.1.6. Point-of-Care Hematology Analyzers

- 6.2.1.7. Others

- 6.2.2. Hematology Reagents

- 6.2.2.1. Diluents

- 6.2.2.2. Lysing Reagents

- 6.2.2.3. Stains

- 6.2.2.4. Calibrators

- 6.2.2.5. Controls

- 6.2.2.6. Cleaners

- 6.2.2.7. Others

- 6.2.1. Hematology Analyzers

- 7. Global Hematology Analyzers and Reagents Market Analysis, by Technology

- 7.1. Key Segment Analysis

- 7.2. Hematology Analyzers and Reagents Market Size Value (US$ Bn), Analysis, and Forecasts, by Technology, 2021-2035

- 7.2.1. Electrical Impedance Technology

- 7.2.2. Flow Cytometry

- 7.2.3. Optical Light Scatter

- 7.2.4. Fluorescence Technology

- 7.2.5. Image-Based Analysis

- 7.2.6. Others

- 8. Global Hematology Analyzers and Reagents Market Analysis, by Test Type

- 8.1. Key Segment Analysis

- 8.2. Hematology Analyzers and Reagents Market Size Value (US$ Bn), Analysis, and Forecasts, by Test Type, 2021-2035

- 8.2.1. Complete Blood Count (CBC)

- 8.2.2. Hemoglobin Testing

- 8.2.3. White Blood Cell (WBC) Differential

- 8.2.4. Platelet Count

- 8.2.5. Reticulocyte Count

- 8.2.6. Erythrocyte Sedimentation Rate (ESR)

- 8.2.7. Coagulation Testing

- 8.2.8. Others

- 9. Global Hematology Analyzers and Reagents Market Analysis, by Sample Type

- 9.1. Key Segment Analysis

- 9.2. Hematology Analyzers and Reagents Market Size Value (US$ Bn), Analysis, and Forecasts, by Sample Type, 2021-2035

- 9.2.1. Whole Blood

- 9.2.2. Bone Marrow

- 9.2.3. Body Fluids

- 9.2.3.1. Cerebrospinal Fluid

- 9.2.3.2. Synovial Fluid

- 9.2.3.3. Pleural Fluid

- 10. Global Hematology Analyzers and Reagents Market Analysis, by End-Users

- 10.1. Key Segment Analysis

- 10.2. Hematology Analyzers and Reagents Market Size Value (US$ Bn), Analysis, and Forecasts, by End-Users, 2021-2035

- 10.2.1. Hospitals

- 10.2.1.1. Public Hospitals

- 10.2.1.2. Private Hospitals

- 10.2.1.3. Specialty Hospitals

- 10.2.2. Diagnostic Laboratories

- 10.2.2.1. Independent Laboratories

- 10.2.2.2. Hospital-Based Laboratories

- 10.2.2.3. Reference Laboratories

- 10.2.3. Blood Banks

- 10.2.4. Clinical Pathology Laboratories

- 10.2.5. Home Care Settings

- 10.2.6. Ambulatory Surgical Centers

- 10.2.7. Point-of-Care Testing Facilities

- 10.2.8. Others

- 10.2.1. Hospitals

- 11. Global Hematology Analyzers and Reagents Market Analysis, by Distribution Channel

- 11.1. Key Segment Analysis

- 11.2. Hematology Analyzers and Reagents Market Size Value (US$ Bn), Analysis, and Forecasts, by Distribution Channel, 2021-2035

- 11.2.1. Direct Sales

- 11.2.2. Distributors and Dealers

- 11.2.3. Online Channels

- 11.2.4. Group Purchasing Organizations (GPOs)

- 12. Global Hematology Analyzers and Reagents Market Analysis and Forecasts, by Region

- 12.1. Key Findings

- 12.2. Hematology Analyzers and Reagents Market Size Value (US$ Bn), Analysis, and Forecasts, by Region, 2021-2035

- 12.2.1. North America

- 12.2.2. Europe

- 12.2.3. Asia Pacific

- 12.2.4. Middle East

- 12.2.5. Africa

- 12.2.6. South America

- 13. North America Hematology Analyzers and Reagents Market Analysis

- 13.1. Key Segment Analysis

- 13.2. Regional Snapshot

- 13.3. North America Hematology Analyzers and Reagents Market Size Value (US$ Bn), Analysis, and Forecasts, 2021-2035

- 13.3.1. Product Type

- 13.3.2. Technology

- 13.3.3. Test Type

- 13.3.4. Sample Type

- 13.3.5. End-Users

- 13.3.6. Distribution Channel

- 13.3.7. Country

- 13.3.7.1. USA

- 13.3.7.2. Canada

- 13.3.7.3. Mexico

- 13.4. USA Hematology Analyzers and Reagents Market

- 13.4.1. Country Segmental Analysis

- 13.4.2. Product Type

- 13.4.3. Technology

- 13.4.4. Test Type

- 13.4.5. Sample Type

- 13.4.6. End-Users

- 13.4.7. Distribution Channel

- 13.5. Canada Hematology Analyzers and Reagents Market

- 13.5.1. Country Segmental Analysis

- 13.5.2. Product Type

- 13.5.3. Technology

- 13.5.4. Test Type

- 13.5.5. Sample Type

- 13.5.6. End-Users

- 13.5.7. Distribution Channel

- 13.6. Mexico Hematology Analyzers and Reagents Market

- 13.6.1. Country Segmental Analysis

- 13.6.2. Product Type

- 13.6.3. Technology

- 13.6.4. Test Type

- 13.6.5. Sample Type

- 13.6.6. End-Users

- 13.6.7. Distribution Channel

- 14. Europe Hematology Analyzers and Reagents Market Analysis

- 14.1. Key Segment Analysis

- 14.2. Regional Snapshot

- 14.3. Europe Hematology Analyzers and Reagents Market Size Value (US$ Bn), Analysis, and Forecasts, 2021-2035

- 14.3.1. Product Type

- 14.3.2. Technology

- 14.3.3. Test Type

- 14.3.4. Sample Type

- 14.3.5. End-Users

- 14.3.6. Distribution Channel

- 14.3.7. Country

- 14.3.7.1. Germany

- 14.3.7.2. United Kingdom

- 14.3.7.3. France

- 14.3.7.4. Italy

- 14.3.7.5. Spain

- 14.3.7.6. Netherlands

- 14.3.7.7. Nordic Countries

- 14.3.7.8. Poland

- 14.3.7.9. Russia & CIS

- 14.3.7.10. Rest of Europe

- 14.4. Germany Hematology Analyzers and Reagents Market

- 14.4.1. Country Segmental Analysis

- 14.4.2. Product Type

- 14.4.3. Technology

- 14.4.4. Test Type

- 14.4.5. Sample Type

- 14.4.6. End-Users

- 14.4.7. Distribution Channel

- 14.5. United Kingdom Hematology Analyzers and Reagents Market

- 14.5.1. Country Segmental Analysis

- 14.5.2. Product Type

- 14.5.3. Technology

- 14.5.4. Test Type

- 14.5.5. Sample Type

- 14.5.6. End-Users

- 14.5.7. Distribution Channel

- 14.6. France Hematology Analyzers and Reagents Market

- 14.6.1. Country Segmental Analysis

- 14.6.2. Product Type

- 14.6.3. Technology

- 14.6.4. Test Type

- 14.6.5. Sample Type

- 14.6.6. End-Users

- 14.6.7. Distribution Channel

- 14.7. Italy Hematology Analyzers and Reagents Market

- 14.7.1. Country Segmental Analysis

- 14.7.2. Product Type

- 14.7.3. Technology

- 14.7.4. Test Type

- 14.7.5. Sample Type

- 14.7.6. End-Users

- 14.7.7. Distribution Channel

- 14.8. Spain Hematology Analyzers and Reagents Market

- 14.8.1. Country Segmental Analysis

- 14.8.2. Robot Product Type

- 14.8.3. Technology

- 14.8.4. Test Type

- 14.8.5. Sample Type

- 14.8.6. End-Users

- 14.8.7. Distribution Channel

- 14.9. Netherlands Hematology Analyzers and Reagents Market

- 14.9.1. Country Segmental Analysis

- 14.9.2. Product Type

- 14.9.3. Technology

- 14.9.4. Test Type

- 14.9.5. Sample Type

- 14.9.6. End-Users

- 14.9.7. Distribution Channel

- 14.10. Nordic Countries Hematology Analyzers and Reagents Market

- 14.10.1. Country Segmental Analysis

- 14.10.2. Product Type

- 14.10.3. Technology

- 14.10.4. Test Type

- 14.10.5. Sample Type

- 14.10.6. End-Users

- 14.10.7. Distribution Channel

- 14.11. Poland Hematology Analyzers and Reagents Market

- 14.11.1. Country Segmental Analysis

- 14.11.2. Product Type

- 14.11.3. Technology

- 14.11.4. Test Type

- 14.11.5. Sample Type

- 14.11.6. End-Users

- 14.11.7. Distribution Channel

- 14.12. Russia & CIS Hematology Analyzers and Reagents Market

- 14.12.1. Country Segmental Analysis

- 14.12.2. Product Type

- 14.12.3. Technology

- 14.12.4. Test Type

- 14.12.5. Sample Type

- 14.12.6. End-Users

- 14.12.7. Distribution Channel

- 14.13. Rest of Europe Hematology Analyzers and Reagents Market

- 14.13.1. Country Segmental Analysis

- 14.13.2. Product Type

- 14.13.3. Technology

- 14.13.4. Test Type

- 14.13.5. Sample Type

- 14.13.6. End-Users

- 14.13.7. Distribution Channel

- 15. Asia Pacific Hematology Analyzers and Reagents Market Analysis

- 15.1. Key Segment Analysis

- 15.2. Regional Snapshot

- 15.3. Asia Pacific Hematology Analyzers and Reagents Market Size Value (US$ Bn), Analysis, and Forecasts, 2021-2035

- 15.3.1. Product Type

- 15.3.2. Technology

- 15.3.3. Test Type

- 15.3.4. Sample Type

- 15.3.5. End-Users

- 15.3.6. Distribution Channel

- 15.3.7. Country

- 15.3.7.1. China

- 15.3.7.2. India

- 15.3.7.3. Japan

- 15.3.7.4. South Korea

- 15.3.7.5. Australia and New Zealand

- 15.3.7.6. Indonesia

- 15.3.7.7. Malaysia

- 15.3.7.8. Thailand

- 15.3.7.9. Vietnam

- 15.3.7.10. Rest of Asia Pacific

- 15.4. China Hematology Analyzers and Reagents Market

- 15.4.1. Country Segmental Analysis

- 15.4.2. Product Type

- 15.4.3. Technology

- 15.4.4. Test Type

- 15.4.5. Sample Type

- 15.4.6. End-Users

- 15.4.7. Distribution Channel

- 15.5. India Hematology Analyzers and Reagents Market

- 15.5.1. Country Segmental Analysis

- 15.5.2. Product Type

- 15.5.3. Technology

- 15.5.4. Test Type

- 15.5.5. Sample Type

- 15.5.6. End-Users

- 15.5.7. Distribution Channel

- 15.6. Japan Hematology Analyzers and Reagents Market

- 15.6.1. Country Segmental Analysis

- 15.6.2. Product Type

- 15.6.3. Technology

- 15.6.4. Test Type

- 15.6.5. Sample Type

- 15.6.6. End-Users

- 15.6.7. Distribution Channel

- 15.7. South Korea Hematology Analyzers and Reagents Market

- 15.7.1. Country Segmental Analysis

- 15.7.2. Product Type

- 15.7.3. Technology

- 15.7.4. Test Type

- 15.7.5. Sample Type

- 15.7.6. End-Users

- 15.7.7. Distribution Channel

- 15.8. Australia and New Zealand Hematology Analyzers and Reagents Market

- 15.8.1. Country Segmental Analysis

- 15.8.2. Product Type

- 15.8.3. Technology

- 15.8.4. Test Type

- 15.8.5. Sample Type

- 15.8.6. End-Users

- 15.8.7. Distribution Channel

- 15.9. Indonesia Hematology Analyzers and Reagents Market

- 15.9.1. Country Segmental Analysis

- 15.9.2. Product Type

- 15.9.3. Technology

- 15.9.4. Test Type

- 15.9.5. Sample Type

- 15.9.6. End-Users

- 15.9.7. Distribution Channel

- 15.10. Malaysia Hematology Analyzers and Reagents Market

- 15.10.1. Country Segmental Analysis

- 15.10.2. Product Type

- 15.10.3. Technology

- 15.10.4. Test Type

- 15.10.5. Sample Type

- 15.10.6. End-Users

- 15.10.7. Distribution Channel

- 15.11. Thailand Hematology Analyzers and Reagents Market

- 15.11.1. Country Segmental Analysis

- 15.11.2. Product Type

- 15.11.3. Technology

- 15.11.4. Test Type

- 15.11.5. Sample Type

- 15.11.6. End-Users

- 15.11.7. Distribution Channel

- 15.12. Vietnam Hematology Analyzers and Reagents Market

- 15.12.1. Country Segmental Analysis

- 15.12.2. Product Type

- 15.12.3. Technology

- 15.12.4. Test Type

- 15.12.5. Sample Type

- 15.12.6. End-Users

- 15.12.7. Distribution Channel

- 15.13. Rest of Asia Pacific Hematology Analyzers and Reagents Market

- 15.13.1. Country Segmental Analysis

- 15.13.2. Product Type

- 15.13.3. Technology

- 15.13.4. Test Type

- 15.13.5. Sample Type

- 15.13.6. End-Users

- 15.13.7. Distribution Channel

- 16. Middle East Hematology Analyzers and Reagents Market Analysis

- 16.1. Key Segment Analysis

- 16.2. Regional Snapshot

- 16.3. Middle East Hematology Analyzers and Reagents Market Size Value (US$ Bn), Analysis, and Forecasts, 2021-2035

- 16.3.1. Product Type

- 16.3.2. Technology

- 16.3.3. Test Type

- 16.3.4. Sample Type

- 16.3.5. End-Users

- 16.3.6. Distribution Channel

- 16.3.7. Country

- 16.3.7.1. Turkey

- 16.3.7.2. UAE

- 16.3.7.3. Saudi Arabia

- 16.3.7.4. Israel

- 16.3.7.5. Rest of Middle East

- 16.4. Turkey Hematology Analyzers and Reagents Market

- 16.4.1. Country Segmental Analysis

- 16.4.2. Product Type

- 16.4.3. Technology

- 16.4.4. Test Type

- 16.4.5. Sample Type

- 16.4.6. End-Users

- 16.4.7. Distribution Channel

- 16.5. UAE Hematology Analyzers and Reagents Market

- 16.5.1. Country Segmental Analysis

- 16.5.2. Product Type

- 16.5.3. Technology

- 16.5.4. Test Type

- 16.5.5. Sample Type

- 16.5.6. End-Users

- 16.5.7. Distribution Channel

- 16.6. Saudi Arabia Hematology Analyzers and Reagents Market

- 16.6.1. Country Segmental Analysis

- 16.6.2. Product Type

- 16.6.3. Technology

- 16.6.4. Test Type

- 16.6.5. Sample Type

- 16.6.6. End-Users

- 16.6.7. Distribution Channel

- 16.7. Israel Hematology Analyzers and Reagents Market

- 16.7.1. Country Segmental Analysis

- 16.7.2. Product Type

- 16.7.3. Technology

- 16.7.4. Test Type

- 16.7.5. Sample Type

- 16.7.6. End-Users

- 16.7.7. Distribution Channel

- 16.8. Rest of Middle East Hematology Analyzers and Reagents Market

- 16.8.1. Country Segmental Analysis

- 16.8.2. Product Type

- 16.8.3. Technology

- 16.8.4. Test Type

- 16.8.5. Sample Type

- 16.8.6. End-Users

- 16.8.7. Distribution Channel

- 17. Africa Hematology Analyzers and Reagents Market Analysis

- 17.1. Key Segment Analysis

- 17.2. Regional Snapshot

- 17.3. Africa Hematology Analyzers and Reagents Market Size Value (US$ Bn), Analysis, and Forecasts, 2021-2035

- 17.3.1. Product Type

- 17.3.2. Technology

- 17.3.3. Test Type

- 17.3.4. Sample Type

- 17.3.5. End-Users

- 17.3.6. Distribution Channel

- 17.3.7. Country

- 17.3.7.1. South Africa

- 17.3.7.2. Egypt

- 17.3.7.3. Nigeria

- 17.3.7.4. Algeria

- 17.3.7.5. Rest of Africa

- 17.4. South Africa Hematology Analyzers and Reagents Market

- 17.4.1. Country Segmental Analysis

- 17.4.2. Product Type

- 17.4.3. Technology

- 17.4.4. Test Type

- 17.4.5. Sample Type

- 17.4.6. End-Users

- 17.4.7. Distribution Channel

- 17.5. Egypt Hematology Analyzers and Reagents Market

- 17.5.1. Country Segmental Analysis

- 17.5.2. Product Type

- 17.5.3. Technology

- 17.5.4. Test Type

- 17.5.5. Sample Type

- 17.5.6. End-Users

- 17.5.7. Distribution Channel

- 17.6. Nigeria Hematology Analyzers and Reagents Market

- 17.6.1. Country Segmental Analysis

- 17.6.2. Product Type

- 17.6.3. Technology

- 17.6.4. Test Type

- 17.6.5. Sample Type

- 17.6.6. End-Users

- 17.6.7. Distribution Channel

- 17.7. Algeria Hematology Analyzers and Reagents Market

- 17.7.1. Country Segmental Analysis

- 17.7.2. Product Type

- 17.7.3. Technology

- 17.7.4. Test Type

- 17.7.5. Sample Type

- 17.7.6. End-Users

- 17.7.7. Distribution Channel

- 17.8. Rest of Africa Hematology Analyzers and Reagents Market

- 17.8.1. Country Segmental Analysis

- 17.8.2. Product Type

- 17.8.3. Technology

- 17.8.4. Test Type

- 17.8.5. Sample Type

- 17.8.6. End-Users

- 17.8.7. Distribution Channel

- 18. South America Hematology Analyzers and Reagents Market Analysis

- 18.1. Key Segment Analysis

- 18.2. Regional Snapshot

- 18.3. South America Hematology Analyzers and Reagents Market Size Value (US$ Bn), Analysis, and Forecasts, 2021-2035

- 18.3.1. Product Type

- 18.3.2. Technology

- 18.3.3. Test Type

- 18.3.4. Sample Type

- 18.3.5. End-Users

- 18.3.6. Distribution Channel

- 18.3.7. Country

- 18.3.7.1. Brazil

- 18.3.7.2. Argentina

- 18.3.7.3. Rest of South America

- 18.4. Brazil Hematology Analyzers and Reagents Market

- 18.4.1. Country Segmental Analysis

- 18.4.2. Product Type

- 18.4.3. Technology

- 18.4.4. Test Type

- 18.4.5. Sample Type

- 18.4.6. End-Users

- 18.4.7. Distribution Channel

- 18.5. Argentina Hematology Analyzers and Reagents Market

- 18.5.1. Country Segmental Analysis

- 18.5.2. Product Type

- 18.5.3. Technology

- 18.5.4. Test Type

- 18.5.5. Sample Type

- 18.5.6. End-Users

- 18.5.7. Distribution Channel

- 18.6. Rest of South America Hematology Analyzers and Reagents Market

- 18.6.1. Country Segmental Analysis

- 18.6.2. Product Type

- 18.6.3. Technology

- 18.6.4. Test Type

- 18.6.5. Sample Type

- 18.6.6. End-Users

- 18.6.7. Distribution Channel

- 19. Key Players/ Company Profile

- 19.1. Abbott Laboratories

- 19.1.1. Company Details/ Overview

- 19.1.2. Company Financials

- 19.1.3. Key Customers and Competitors

- 19.1.4. Business/ Industry Portfolio

- 19.1.5. Product Portfolio/ Specification Details

- 19.1.6. Pricing Data

- 19.1.7. Strategic Overview

- 19.1.8. Recent Developments

- 19.2. Beckman Coulter (Danaher Corporation)

- 19.3. Bio-Rad Laboratories

- 19.4. Boule Diagnostics

- 19.5. Diatron

- 19.6. Drew Scientific

- 19.7. EKF Diagnostics

- 19.8. Erba Mannheim

- 19.9. Healgen Scientific

- 19.10. Horiba Medical

- 19.11. HUMAN Diagnostics

- 19.12. Maccura Biotechnology

- 19.13. Mindray Medical International

- 19.14. Nihon Kohden Corporation

- 19.15. Orphée SA

- 19.16. Roche Diagnostics

- 19.17. Shenzhen Mindray Bio-Medical Electronics

- 19.18. Siemens Healthineers

- 19.19. Sinnowa Medical Science & Technology

- 19.20. Sysmex Corporation

- 19.21. Other Key Players

- 19.1. Abbott Laboratories

Note* - This is just tentative list of players. While providing the report, we will cover more number of players based on their revenue and share for each geography

Research Design

Our research design integrates both demand-side and supply-side analysis through a balanced combination of primary and secondary research methodologies. By utilizing both bottom-up and top-down approaches alongside rigorous data triangulation methods, we deliver robust market intelligence that supports strategic decision-making.

MarketGenics' comprehensive research design framework ensures the delivery of accurate, reliable, and actionable market intelligence. Through the integration of multiple research approaches, rigorous validation processes, and expert analysis, we provide our clients with the insights needed to make informed strategic decisions and capitalize on market opportunities.

MarketGenics leverages a dedicated industry panel of experts and a comprehensive suite of paid databases to effectively collect, consolidate, and analyze market intelligence.

Our approach has consistently proven to be reliable and effective in generating accurate market insights, identifying key industry trends, and uncovering emerging business opportunities.

Through both primary and secondary research, we capture and analyze critical company-level data such as manufacturing footprints, including technical centers, R&D facilities, sales offices, and headquarters.

Our expert panel further enhances our ability to estimate market size for specific brands based on validated field-level intelligence.

Our data mining techniques incorporate both parametric and non-parametric methods, allowing for structured data collection, sorting, processing, and cleaning.

Demand projections are derived from large-scale data sets analyzed through proprietary algorithms, culminating in robust and reliable market sizing.

Research Approach

The bottom-up approach builds market estimates by starting with the smallest addressable market units and systematically aggregating them to create comprehensive market size projections.

This method begins with specific, granular data points and builds upward to create the complete market landscape.

Customer Analysis → Segmental Analysis → Geographical Analysis

The top-down approach starts with the broadest possible market data and systematically narrows it down through a series of filters and assumptions to arrive at specific market segments or opportunities.

This method begins with the big picture and works downward to increasingly specific market slices.

TAM → SAM → SOM

Research Methods

Desk / Secondary Research

While analysing the market, we extensively study secondary sources, directories, and databases to identify and collect information useful for this technical, market-oriented, and commercial report. Secondary sources that we utilize are not only the public sources, but it is a combination of Open Source, Associations, Paid Databases, MG Repository & Knowledgebase, and others.

- Company websites, annual reports, financial reports, broker reports, and investor presentations

- National government documents, statistical databases and reports

- News articles, press releases and web-casts specific to the companies operating in the market, Magazines, reports, and others

- We gather information from commercial data sources for deriving company specific data such as segmental revenue, share for geography, product revenue, and others

- Internal and external proprietary databases (industry-specific), relevant patent, and regulatory databases

- Governing Bodies, Government Organizations

- Relevant Authorities, Country-specific Associations for Industries

We also employ the model mapping approach to estimate the product level market data through the players' product portfolio

Primary Research

Primary research/ interviews is vital in analyzing the market. Most of the cases involves paid primary interviews. Primary sources include primary interviews through e-mail interactions, telephonic interviews, surveys as well as face-to-face interviews with the different stakeholders across the value chain including several industry experts.

| Type of Respondents | Number of Primaries |

|---|---|

| Tier 2/3 Suppliers | ~20 |

| Tier 1 Suppliers | ~25 |

| End-users | ~25 |

| Industry Expert/ Panel/ Consultant | ~30 |

| Total | ~100 |

MG Knowledgebase

• Repository of industry blog, newsletter and case studies

• Online platform covering detailed market reports, and company profiles

Forecasting Factors and Models

Forecasting Factors

- Historical Trends – Past market patterns, cycles, and major events that shaped how markets behave over time. Understanding past trends helps predict future behavior.

- Industry Factors – Specific characteristics of the industry like structure, regulations, and innovation cycles that affect market dynamics.

- Macroeconomic Factors – Economic conditions like GDP growth, inflation, and employment rates that affect how much money people have to spend.

- Demographic Factors – Population characteristics like age, income, and location that determine who can buy your product.

- Technology Factors – How quickly people adopt new technology and how much technology infrastructure exists.

- Regulatory Factors – Government rules, laws, and policies that can help or restrict market growth.

- Competitive Factors – Analyzing competition structure such as degree of competition and bargaining power of buyers and suppliers.

Forecasting Models / Techniques

Multiple Regression Analysis

- Identify and quantify factors that drive market changes

- Statistical modeling to establish relationships between market drivers and outcomes

Time Series Analysis – Seasonal Patterns

- Understand regular cyclical patterns in market demand

- Advanced statistical techniques to separate trend, seasonal, and irregular components

Time Series Analysis – Trend Analysis

- Identify underlying market growth patterns and momentum

- Statistical analysis of historical data to project future trends

Expert Opinion – Expert Interviews

- Gather deep industry insights and contextual understanding

- In-depth interviews with key industry stakeholders

Multi-Scenario Development

- Prepare for uncertainty by modeling different possible futures

- Creating optimistic, pessimistic, and most likely scenarios

Time Series Analysis – Moving Averages

- Sophisticated forecasting for complex time series data

- Auto-regressive integrated moving average models with seasonal components

Econometric Models

- Apply economic theory to market forecasting

- Sophisticated economic models that account for market interactions

Expert Opinion – Delphi Method

- Harness collective wisdom of industry experts

- Structured, multi-round expert consultation process

Monte Carlo Simulation

- Quantify uncertainty and probability distributions

- Thousands of simulations with varying input parameters

Research Analysis

Our research framework is built upon the fundamental principle of validating market intelligence from both demand and supply perspectives. This dual-sided approach ensures comprehensive market understanding and reduces the risk of single-source bias.

Demand-Side Analysis: We understand end-user/application behavior, preferences, and market needs along with the penetration of the product for specific application.

Supply-Side Analysis: We estimate overall market revenue, analyze the segmental share along with industry capacity, competitive landscape, and market structure.

Validation & Evaluation

Data triangulation is a validation technique that uses multiple methods, sources, or perspectives to examine the same research question, thereby increasing the credibility and reliability of research findings. In market research, triangulation serves as a quality assurance mechanism that helps identify and minimize bias, validate assumptions, and ensure accuracy in market estimates.

- Data Source Triangulation – Using multiple data sources to examine the same phenomenon

- Methodological Triangulation – Using multiple research methods to study the same research question

- Investigator Triangulation – Using multiple researchers or analysts to examine the same data

- Theoretical Triangulation – Using multiple theoretical perspectives to interpret the same data

Custom Market Research Services

We will customise the research for you, in case the report listed above does not meet your requirements.

Get 10% Free Customisation