Industrial Control & Factory Automation Market Size, Share & Trends Analysis Report by Component (Industrial Sensors, Industrial Robots, Industrial 3D Printers, Industrial PCs, Machine Vision Systems, Human–Machine Interface (HMI), Control Valves, Actuators & Drives, Relays & Switches, Others), Solution, Communication Protocol, Control System Type, Deployment Mode, Organization Size, Application, Industry Vertical, Distribution Channel and Geography (North America, Europe, Asia Pacific, Middle East, Africa, and South America) – Global Industry Data, Trends, and Forecasts, 2026–2035

|

Market Structure & Evolution |

|

|

Segmental Data Insights |

|

|

Demand Trends |

|

|

Competitive Landscape |

|

|

Strategic Development |

|

|

Future Outlook & Opportunities |

|

Industrial Control & Factory Automation Market Size, Share, and Growth

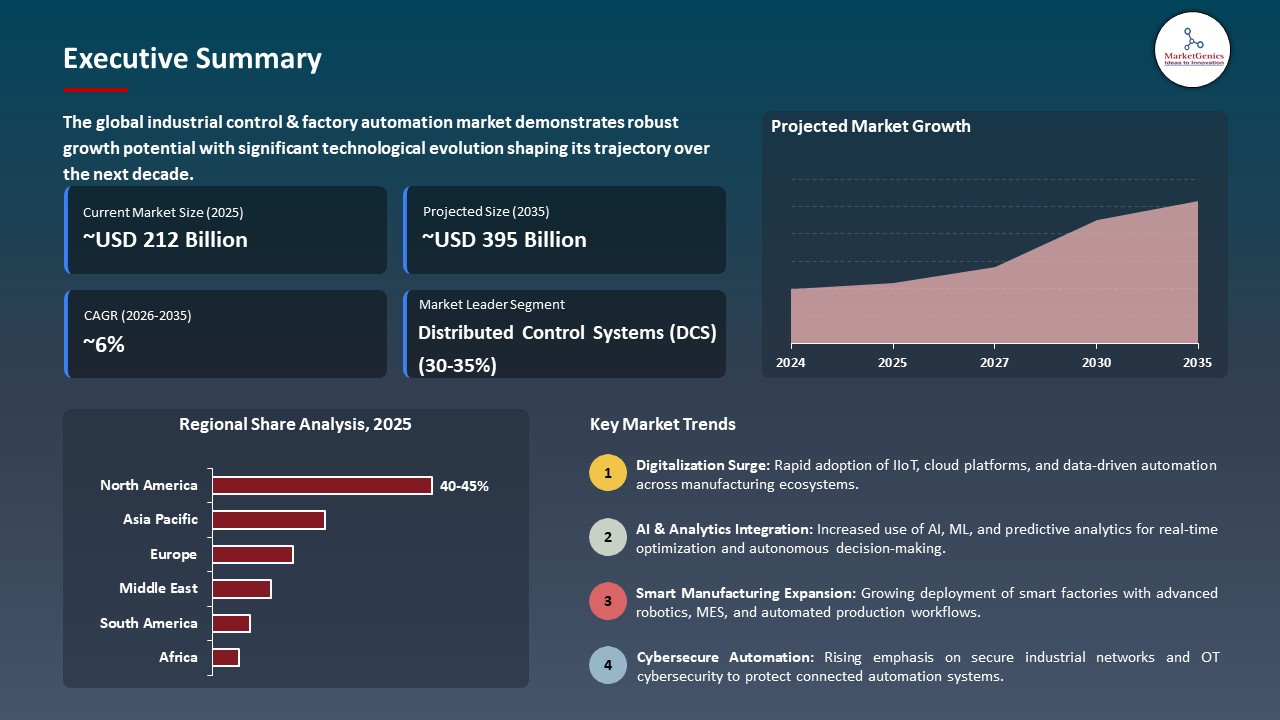

The global industrial control & factory automation market is experiencing robust growth, with its estimated value of USD 212.3 billion in the year 2025 and USD 394.9 billion by the period 2035, registering a CAGR of 6.4% during the forecast period. The industrial control & factory automation market is witnessing a substantial increase in its demand across the globe.

Siemens - In the words of Peter Koerte (Chief Technology Officer & Chief Strategy Officer, Siemens AG), "Industrial AI is a revolutionary concept which will lead to a profound positive impact in the real world, broadly across different industries. With the connection of Industrial AI technologies, we can now access the enormous data streams from industrial settings and convert them into insightful information that has tangible business impact."

The rise in the industrial control & factory automation market is mainly due to various factors that improve the overall operations of the companies in terms of efficiency, safety, and productivity. A few examples are Siemens and Schneider Electric moves to digitize and modularize the automation industry with real-time AI analytics and predictive maintenance capabilities. Besides that, smart manufacturing industry trends, sensor/starter device connectivity (IIOT), and strict regulations & standards in safety & security are the top three drivers of the industrial automation market growth.

Industrial sectors are required to meet the safety and environmental regulations, which lead to investments in automated monitoring, fault detection, and energy-efficient control systems. The industrial control & factory automation market is actually driven by the technological advancements, regulatory requirements, and the quest for operational efficiency. As a result, the market is seeing safer, more reliable, and highly productive manufacturing operations.

Moreover, the global industrial control & factory automation market has some adjacent opportunities that include predictive maintenance solutions, industrial cybersecurity systems, robotics integration, real-time process monitoring platforms, and advanced HMI and SCADA solutions. When manufacturers use these adjacent markets, they become more resilient in their operations, the production quality gets better, and there is additional revenue streams unlocked in the broader industrial automation ecosystem.

Industrial Control & Factory Automation Market Dynamics and Trends

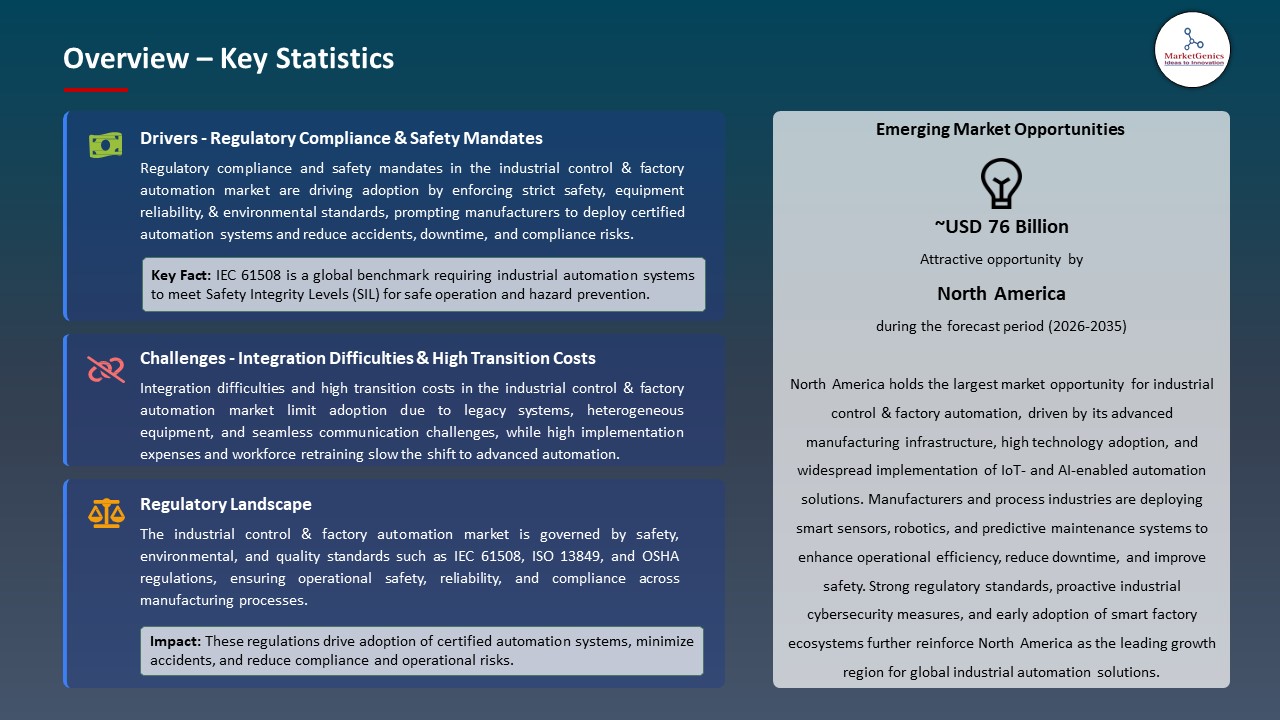

Driver: Regulatory Compliance & Safety Mandates Accelerating Automation Deployment

-

The rapid growth of the industrial control & factory automation market is mainly influenced by worldwide regulatory changes such as the EU Machinery Regulation (EU) 2023/1230, IEC 61508 functional safety standards, and OSHA industrial safety requirements. These regulations require that safety, reliability, and system-integrity controls be very strict, thus manufacturers are compelled to upgrade their control architectures to advanced, automated ones.

- Environmental compliance regulations, such as the EU Energy Efficiency Directive (EED) and various national carbon-reduction plans in the U.S., China and Japan, are leading the way to the adoption of automation systems that can make energy use more efficient, can emit gases continuously and can provide the production process that is eco-friendly.

- The increased use of industrial cybersecurity standards (NIST CSF 2.0, ISA/IEC 62443) is leading to factories installing secure PLCs, authenticated control networks, and continuous threat-monitoring systems as part of their automation stack.

Restraint: Integration Difficulties & High Transition Costs Slowing Modernization

-

Modernization is still moving at a slow pace despite the strong regulatory and efficiency pressure. This is mainly because it is very difficult to combine new digital control systems with a large number of old PLCs, SCADA systems, and proprietary fieldbus networks that are non-interoperable.

- The shift to IIoT-enabled, software-defined automation being done on a pay-as-you-go basis would need a very substantial investment in upgrading industrial networking, strengthening cybersecurity, and reskilling the workforce. These are barriers that are particularly difficult for SMEs and manufacturers in developing countries.

- It is argued that the fear of downtime during system replacement, the shortage of automation engineering talent, and the need for multi-vendor interoperability testing are the reasons for the continuance of the delay in the large-scale deployment of next-generation control platforms.

Opportunity: Growth in Emerging Manufacturing Hubs & Public-Sector Automation Initiatives

-

Expansion of manufacturing in India, Vietnam, Indonesia, Mexico, and Eastern Europe is resulting in a huge demand for PLCs, DCS, SCADA, safety controllers, and robotics, as governments are facilitating the adoption of Industry 4.0 through incentives, smart-factory programs, and industrial corridor developments.

- One of the effects of government-supported programs such as India’s Smart Manufacturing Competitiveness Scheme, China’s Intelligent Manufacturing initiative, and Germany’s Plattform Industrie 4.0 is the rapid investment in automation infrastructure, AI-enabled monitoring, and digital engineering technologies.

- Moreover, there are many adjacent opportunities to become ailed very quickly, such as industrial edge computing, industrial cybersecurity services, condition-based maintenance platforms, robot-as-a-service, and digital twin lifecycle management, which, in turn, are opening up new revenue streams for the automation vendors and system integrators.

Key Trend: Convergence of AI, Edge Computing, Interoperable Architectures & Cyber-Physical Systems

-

The integration of AI/ML into industrial control environments is increasingly standard, thus allowing anomaly detection, process optimization, real-time quality inspection, and adaptive control strategies that exceed what is possible with traditional rule-based PLC programming.

- The use of edge computing and time-sensitive networking (TSN) is facilitating ultra-low-latency performance, thus enabling factories to operate decentralized, autonomous control loops closer to machines while lessening their dependence on the cloud. Open and interoperable automation architectures like OPC UA, MQTT Sparkplug B, and the nascent software-defined control frameworks are leading the industry away from vendor-locked proprietary systems towards modular, future-proof automation.

- The growing use of cyber-physical production systems, digital twins, and AI-powered manufacturing execution systems (MES) is fundamentally changing factory operations by providing the means for continuous optimization, predictive insights, and closed-loop decision automation.

Industrial-Control-&-Factory-Automation-Market Analysis and Segmental Data

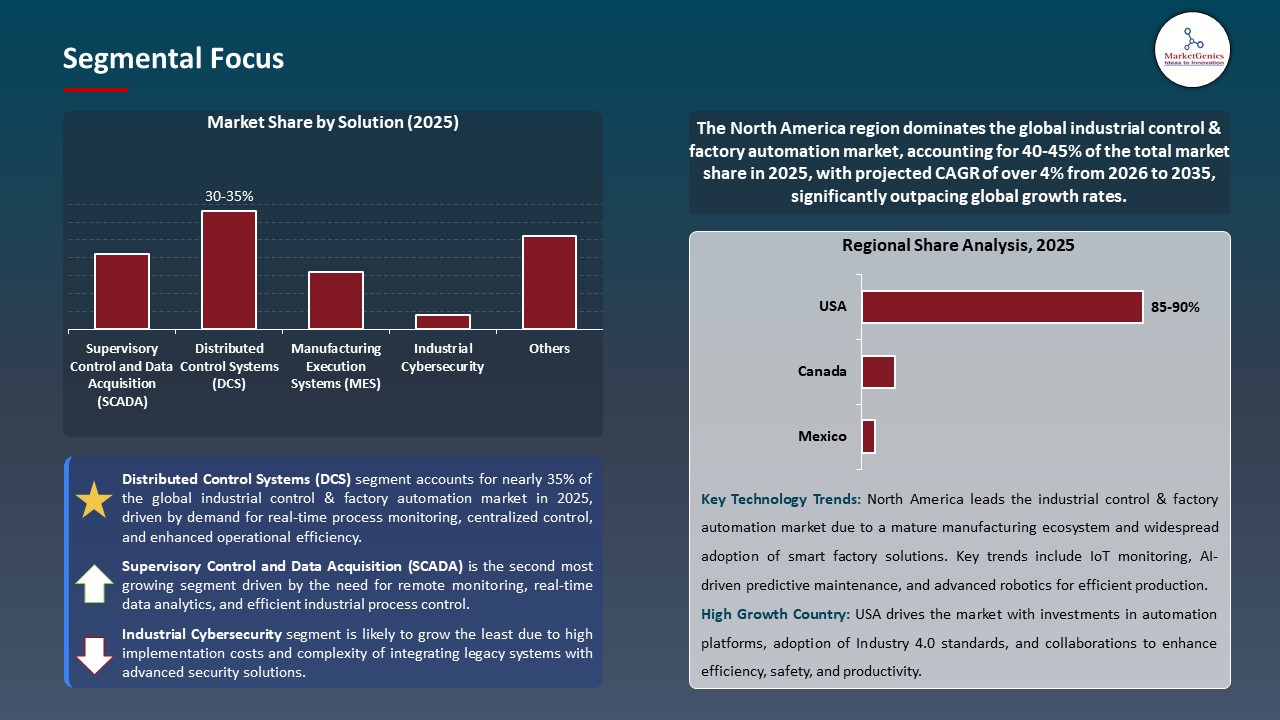

“Distributed Control Systems (DCS) Dominates Global Industrial Control & Factory Automation Market amid Rising Demand for Real-Time Process Optimization"

-

Distributed Control Systems (DCS) are the most sought-after control systems in the market-system segment, as they are the core of the industrial processes management, which are mainly continuous, plus the growing attention to the real-time operational optimization and stability. The recent developments in modular controllers, distributed architectures, and real-time analytics have made the system quicker, more fault-tolerant, and scalable.

- Attributed to the imposition of more stringent safety, quality, and energy-efficiency requirements, the industries, e.g., oil & gas, chemicals, power generation, and pharmaceuticals, are moving towards modern DCS platforms. These systems facilitate continuous monitoring, advanced control strategies, and predictive maintenance, thus, through these measures, the industry is saved from loss of production time and benefits by complying with the standards. Modern DCS packages interconnecting IIoT, cloud computing, and remote diagnostics functions are giving new life to decision-making and that is how Industry 4.0 transformation can be seen in process industries.

- The ongoing innovation in communication protocols, controller architecture, and software-defined automation is reinforcing the DCS role as the most suitable and reliable backbone for complex process operations, thus contributing to safer, more-efficient, and highly-reliable industrial performances.

“North America Dominates Industrial Control & Factory Automation Market amid Rapid Adoption of Advanced Automation and Digital Manufacturing”

-

North America constitutes the largest region for industrial control and factory automation market on a global scale, owing to the presence of major automation vendors, advanced manufacturing facilities, and early adopters in such industries as automotive, pharmaceuticals, energy, and food processing. Companies in the region are encouraged to install advanced automation systems that enhance operational visibility, safety, and efficiency, due to their stringent regulatory frameworks, like OSHA safety standards, NIST cybersecurity guidelines, and EPA environmental compliance.

- Manufacturers' massive-scale usage of industrial IoT, cloud-connected automation, and AI-driven process optimization is a major factor in maintaining North America's leadership position. The main companies in the region are equipping themselves with advanced PLCs, DCS platforms, edge computing, and digital twin technologies to improve throughput, lessen the times of machinery they have to stand idle, and facilitate predictive maintenance in their operations that are industrial and distributed.

- The quick growth of smart factory projects, which is supported by U.S. federal incentives, workforce modernization programs, along with investments in semiconductor, battery, and clean-energy manufacturing, is leading to a rapid automation implementation. Industries are turning to the use of autonomous production lines, connected robotics, and real-time analytics more and more, thus confirming the region's firm resolve when it comes to digital manufacturing transformation.

Industrial-Control-&-Factory-Automation-Market Ecosystem

The industrial control and factory automation market is still mainly composed of very few large companies with Siemens AG, Schneider Electric, Rockwell Automation, ABB Ltd., Mitsubishi Electric, and Honeywell International being the top leaders that are expanding their worldwide presence by using the newest automated, AI and industrial IoT technologies. These firms largely concentrate on areas that require them to offer specialized solutions such as predictive maintenance platforms, edge-AI controllers, high-precision sensors, and advanced PLC-SCADA systems, which, in turn, promote the rapid diffusion of innovation throughout production environments.

Various government organizations and research and development institutions are engaging in activities that can materially support technological advancement: In January 2025, the U.S. DOE made an announcement about nearly USD 13 million that it is willing to spend to incentivize smart-manufacturing programs, thus choosing multiple state projects to scale Industry-4.0 adoption and HPC access. In June 2024, a national industrial innovation consortium unveiled a next-generation AI-powered smart manufacturing testbed aimed for easy robotics coordination and real-time process optimization which, in turn, will dramatically increase production reliability in large-scale factories.

One of the major automation providers, in February 2025, unveiled an industrial IoT analytics engine based on deep learning algorithms, thereby making visible quite a few processes accuracy increases of up to 18% and unplanned downtime reductions across automated production lines.

Recent Development and Strategic Overview:

-

In March 2025, Siemens AG unveiled its EdgeFlow Adaptive Control Suite, an industrial real-time edge computing platform that optimizes production lines of high-speed by using AI-driven anomaly detection and automated process tuning. The system allows factories to carry out data processing on-site without the need for a cloud, thus, improving the response time, reducing the machine downtime, and increasing operational precision in multi-line manufacturing setups.

- In September 2025, Rockwell Automation launched its FlexVision Autonomous Inspection Network, a sophisticated machine-vision solution that integrates deep-learning–based defect recognition with robotic cells that are interconnected. The platform is equipped with cross-device communication and decentralized decision-making capabilities, thus, enabling manufacturers to achieve higher inspection accuracy, simplify quality control, and increase throughput in complex assembly environments at a faster rate.

Report Scope

|

Attribute |

Detail |

|

Market Size in 2025 |

USD 212.3 Bn |

|

Market Forecast Value in 2035 |

USD 394.9 Bn |

|

Growth Rate (CAGR) |

6.4% |

|

Forecast Period |

2026 – 2035 |

|

Historical Data Available for |

2021 – 2024 |

|

Market Size Units |

USD Bn for Value |

|

Report Format |

Electronic (PDF) + Excel |

|

Regions and Countries Covered |

|||||

|

North America |

Europe |

Asia Pacific |

Middle East |

Africa |

South America |

|

|

|

|

|

|

|

Companies Covered |

|||||

|

|

|

|

|

|

Industrial-Control-&-Factory-Automation-Market Segmentation and Highlights

|

Segment |

Sub-segment |

|

Industrial Control & Factory Automation Market, By Component |

|

|

Industrial Control & Factory Automation Market, By Solution |

|

|

Industrial Control & Factory Automation Market, By Communication Protocol |

|

|

Industrial Control & Factory Automation Market, By Control System Type |

|

|

Industrial Control & Factory Automation Market, By Deployment Mode |

|

|

Industrial Control & Factory Automation Market, By Organization Size |

|

|

Industrial Control & Factory Automation Market, By Application |

|

|

Industrial Control & Factory Automation Market, By Industry Vertical |

|

|

Industrial Control & Factory Automation Market, By Distribution Channel |

|

Frequently Asked Questions

Table of Contents

- 1. Research Methodology and Assumptions

- 1.1. Definitions

- 1.2. Research Design and Approach

- 1.3. Data Collection Methods

- 1.4. Base Estimates and Calculations

- 1.5. Forecasting Models

- 1.5.1. Key Forecast Factors & Impact Analysis

- 1.6. Secondary Research

- 1.6.1. Open Sources

- 1.6.2. Paid Databases

- 1.6.3. Associations

- 1.7. Primary Research

- 1.7.1. Primary Sources

- 1.7.2. Primary Interviews with Stakeholders across Ecosystem

- 2. Executive Summary

- 2.1. Global Industrial Control & Factory Automation Market Outlook

- 2.1.1. Industrial Control & Factory Automation Market Size (Value - US$ Bn), and Forecasts, 2021-2035

- 2.1.2. Compounded Annual Growth Rate Analysis

- 2.1.3. Growth Opportunity Analysis

- 2.1.4. Segmental Share Analysis

- 2.1.5. Geographical Share Analysis

- 2.2. Market Analysis and Facts

- 2.3. Supply-Demand Analysis

- 2.4. Competitive Benchmarking

- 2.5. Go-to- Market Strategy

- 2.5.1. Customer/ End-use Industry Assessment

- 2.5.2. Growth Opportunity Data, 2026-2035

- 2.5.2.1. Regional Data

- 2.5.2.2. Country Data

- 2.5.2.3. Segmental Data

- 2.5.3. Identification of Potential Market Spaces

- 2.5.4. GAP Analysis

- 2.5.5. Potential Attractive Price Points

- 2.5.6. Prevailing Market Risks & Challenges

- 2.5.7. Preferred Sales & Marketing Strategies

- 2.5.8. Key Recommendations and Analysis

- 2.5.9. A Way Forward

- 2.1. Global Industrial Control & Factory Automation Market Outlook

- 3. Industry Data and Premium Insights

- 3.1. Global Automation & Process Control Ecosystem Overview, 2025

- 3.1.1. Automation & Process Control Ecosystem Analysis

- 3.1.2. Key Trends for Automation & Process Control Industry

- 3.1.3. Regional Distribution for Automation & Process Control Industry

- 3.2. Supplier Customer Data

- 3.3. Technology Roadmap and Developments

- 3.1. Global Automation & Process Control Ecosystem Overview, 2025

- 4. Market Overview

- 4.1. Market Dynamics

- 4.1.1. Drivers

- 4.1.1.1. Rising demand for real-time monitoring and predictive maintenance in manufacturing.

- 4.1.1.2. Growing adoption of IoT-, AI-, and robotics-based automation across industries.

- 4.1.1.3. Increasing investment in cloud-based software, digital twins, and smart factory platforms.

- 4.1.2. Restraints

- 4.1.2.1. High initial costs for advanced automation systems and integration.

- 4.1.2.2. Challenges in retrofitting legacy machinery and ensuring equipment compatibility.

- 4.1.1. Drivers

- 4.2. Key Trend Analysis

- 4.3. Regulatory Framework

- 4.3.1. Key Regulations, Norms, and Subsidies, by Key Countries

- 4.3.2. Tariffs and Standards

- 4.3.3. Impact Analysis of Regulations on the Market

- 4.4. Value Chain Analysis

- 4.4.1. Component Suppliers

- 4.4.2. System Integrators/ Technology Providers

- 4.4.3. Industrial Control & Factory Automation Solution Providers

- 4.4.4. Distributors

- 4.4.5. End Users

- 4.5. Cost Structure Analysis

- 4.5.1. Parameter’s Share for Cost Associated

- 4.5.2. COGP vs COGS

- 4.5.3. Profit Margin Analysis

- 4.6. Pricing Analysis

- 4.6.1. Regional Pricing Analysis

- 4.6.2. Segmental Pricing Trends

- 4.6.3. Factors Influencing Pricing

- 4.7. Porter’s Five Forces Analysis

- 4.8. PESTEL Analysis

- 4.9. Global Industrial Control & Factory Automation Market Demand

- 4.9.1. Historical Market Size –Value (US$ Bn) and Volume – (Billion Units), 2020-2024

- 4.9.2. Current and Future Market Size –Value (US$ Bn) and Volume – (Billion Units), 2026–2035

- 4.9.2.1. Y-o-Y Growth Trends

- 4.9.2.2. Absolute $ Opportunity Assessment

- 4.1. Market Dynamics

- 5. Competition Landscape

- 5.1. Competition structure

- 5.1.1. Fragmented v/s consolidated

- 5.2. Company Share Analysis, 2025

- 5.2.1. Global Company Market Share

- 5.2.2. By Region

- 5.2.2.1. North America

- 5.2.2.2. Europe

- 5.2.2.3. Asia Pacific

- 5.2.2.4. Middle East

- 5.2.2.5. Africa

- 5.2.2.6. South America

- 5.3. Product Comparison Matrix

- 5.3.1. Specifications

- 5.3.2. Market Positioning

- 5.3.3. Pricing

- 5.1. Competition structure

- 6. Global Industrial Control & Factory Automation Market Analysis, by Component

- 6.1. Key Segment Analysis

- 6.2. Industrial Control & Factory Automation Market Size (Value - US$ Bn), Analysis, and Forecasts, by Component, 2021-2035

- 6.2.1. Industrial Sensors

- 6.2.2. Industrial Robots

- 6.2.3. Industrial 3D Printers

- 6.2.4. Industrial PCs

- 6.2.5. Machine Vision Systems

- 6.2.6. Human–Machine Interface (HMI)

- 6.2.7. Control Valves

- 6.2.8. Actuators & Drives

- 6.2.9. Relays & Switches

- 6.2.10. Others

- 7. Global Industrial Control & Factory Automation Market Analysis, by Solution

- 7.1. Key Segment Analysis

- 7.2. Industrial Control & Factory Automation Market Size (Value - US$ Bn), Analysis, and Forecasts, by Solution, 2021-2035

- 7.2.1. Supervisory Control and Data Acquisition (SCADA)

- 7.2.2. Manufacturing Execution Systems (MES)

- 7.2.3. Distributed Control Systems (DCS)

- 7.2.4. Programmable Logic Controllers (PLC)

- 7.2.5. Industrial Internet of Things (IIoT) Platforms

- 7.2.6. Product Lifecycle Management (PLM)

- 7.2.7. Enterprise Resource Planning (ERP)

- 7.2.8. Industrial Cybersecurity

- 7.2.9. Others

- 8. Global Industrial Control & Factory Automation Market Analysis, by Communication Protocol

- 8.1. Key Segment Analysis

- 8.2. Industrial Control & Factory Automation Market Size (Value - US$ Bn), Analysis, and Forecasts, by Communication Protocol, 2021-2035

- 8.2.1. Fieldbus

- 8.2.2. Industrial Ethernet

- 8.2.3. Wireless Industrial Communication

- 8.2.4. IO-Link

- 8.2.5. Modbus

- 8.2.6. Profibus

- 8.2.7. EtherCAT

- 8.2.8. PROFINET

- 8.2.9. Others

- 9. Global Industrial Control & Factory Automation Market Analysis, by Control System Type

- 9.1. Key Segment Analysis

- 9.2. Industrial Control & Factory Automation Market Size (Value - US$ Bn), Analysis, and Forecasts, by Control System Type, 2021-2035

- 9.2.1. Process Automation Systems

- 9.2.2. Discrete Automation Systems

- 9.2.3. Hybrid Automation Systems

- 9.2.4. Batch Automation Systems

- 9.2.5. Others

- 10. Global Industrial Control & Factory Automation Market Analysis, by Deployment Mode

- 10.1. Key Segment Analysis

- 10.2. Industrial Control & Factory Automation Market Size (Value - US$ Bn), Analysis, and Forecasts, by Deployment Mode, 2021-2035

- 10.2.1. On-premise

- 10.2.2. Cloud-based

- 10.2.3. Hybrid

- 11. Global Industrial Control & Factory Automation Market Analysis, by Organization Size

- 11.1. Key Segment Analysis

- 11.2. Industrial Control & Factory Automation Market Size (Value - US$ Bn), Analysis, and Forecasts, by Organization Size, 2021-2035

- 11.2.1. Small & Medium Enterprises (SMEs)

- 11.2.2. Large Enterprises

- 12. Global Industrial Control & Factory Automation Market Analysis, by Application

- 12.1. Key Segment Analysis

- 12.2. Industrial Control & Factory Automation Market Size (Value - US$ Bn), Analysis, and Forecasts, by Application, 2021-2035

- 12.2.1. Assembly & Handling

- 12.2.2. Material Handling

- 12.2.3. Packaging & Palletizing

- 12.2.4. Welding & Soldering

- 12.2.5. Painting & Coating

- 12.2.6. Quality Inspection

- 12.2.7. Process Control & Monitoring

- 12.2.8. Predictive Maintenance

- 12.2.9. Others

- 13. Global Industrial Control & Factory Automation Market Analysis, by Industry Vertical

- 13.1. Key Segment Analysis

- 13.2. Industrial Control & Factory Automation Market Size (Value - US$ Bn), Analysis, and Forecasts, by Industry Vertical, 2021-2035

- 13.2.1. Automotive

- 13.2.2. Food & Beverage

- 13.2.3. Pharmaceuticals & Biotechnology

- 13.2.4. Chemicals & Petrochemicals

- 13.2.5. Oil & Gas

- 13.2.6. Metals & Mining

- 13.2.7. Energy & Power

- 13.2.8. Electronics & Semiconductors

- 13.2.9. Aerospace & Defense

- 13.2.10. Water & Wastewater

- 13.2.11. Pulp & Paper

- 13.2.12. Others

- 14. Global Industrial Control & Factory Automation Market Analysis and Forecasts, by Distribution Channel

- 14.1. Key Findings

- 14.2. Industrial Control & Factory Automation Market Size (Value - US$ Bn), Analysis, and Forecasts, by Distribution Channel, 2021-2035

- 14.2.1. Direct Sales

- 14.2.2. OEM Sales

- 14.2.3. Distributors

- 15. Global Industrial Control & Factory Automation Market Analysis and Forecasts, by Region

- 15.1. Key Findings

- 15.2. Industrial Control & Factory Automation Market Size (Value - US$ Bn), Analysis, and Forecasts, by Region, 2021-2035

- 15.2.1. North America

- 15.2.2. Europe

- 15.2.3. Asia Pacific

- 15.2.4. Middle East

- 15.2.5. Africa

- 15.2.6. South America

- 16. North America Industrial Control & Factory Automation Market Analysis

- 16.1. Key Segment Analysis

- 16.2. Regional Snapshot

- 16.3. North America Industrial Control & Factory Automation Market Size Value - US$ Bn), Analysis, and Forecasts, 2021-2035

- 16.3.1. Component

- 16.3.2. Solution

- 16.3.3. Communication Protocol

- 16.3.4. Control System Type

- 16.3.5. Deployment Mode

- 16.3.6. Organization Size

- 16.3.7. Application

- 16.3.8. Industry Vertical

- 16.3.9. Country

- 16.3.9.1. USA

- 16.3.9.2. Canada

- 16.3.9.3. Mexico

- 16.4. USA Industrial Control & Factory Automation Market

- 16.4.1. Country Segmental Analysis

- 16.4.2. Component

- 16.4.3. Solution

- 16.4.4. Communication Protocol

- 16.4.5. Control System Type

- 16.4.6. Deployment Mode

- 16.4.7. Organization Size

- 16.4.8. Application

- 16.4.9. Industry Vertical

- 16.5. Canada Industrial Control & Factory Automation Market

- 16.5.1. Country Segmental Analysis

- 16.5.2. Component

- 16.5.3. Solution

- 16.5.4. Communication Protocol

- 16.5.5. Control System Type

- 16.5.6. Deployment Mode

- 16.5.7. Organization Size

- 16.5.8. Application

- 16.5.9. Industry Vertical

- 16.6. Mexico Industrial Control & Factory Automation Market

- 16.6.1. Country Segmental Analysis

- 16.6.2. Component

- 16.6.3. Solution

- 16.6.4. Communication Protocol

- 16.6.5. Control System Type

- 16.6.6. Deployment Mode

- 16.6.7. Organization Size

- 16.6.8. Application

- 16.6.9. Industry Vertical

- 17. Europe Industrial Control & Factory Automation Market Analysis

- 17.1. Key Segment Analysis

- 17.2. Regional Snapshot

- 17.3. Europe Industrial Control & Factory Automation Market Size (Value - US$ Bn), Analysis, and Forecasts, 2021-2035

- 17.3.1. Component

- 17.3.2. Solution

- 17.3.3. Communication Protocol

- 17.3.4. Control System Type

- 17.3.5. Deployment Mode

- 17.3.6. Organization Size

- 17.3.7. Application

- 17.3.8. Industry Vertical

- 17.3.9. Country

- 17.3.9.1. Germany

- 17.3.9.2. United Kingdom

- 17.3.9.3. France

- 17.3.9.4. Italy

- 17.3.9.5. Spain

- 17.3.9.6. Netherlands

- 17.3.9.7. Nordic Countries

- 17.3.9.8. Poland

- 17.3.9.9. Russia & CIS

- 17.3.9.10. Rest of Europe

- 17.4. Germany Industrial Control & Factory Automation Market

- 17.4.1. Country Segmental Analysis

- 17.4.2. Component

- 17.4.3. Solution

- 17.4.4. Communication Protocol

- 17.4.5. Control System Type

- 17.4.6. Deployment Mode

- 17.4.7. Organization Size

- 17.4.8. Application

- 17.4.9. Industry Vertical

- 17.5. United Kingdom Industrial Control & Factory Automation Market

- 17.5.1. Country Segmental Analysis

- 17.5.2. Component

- 17.5.3. Solution

- 17.5.4. Communication Protocol

- 17.5.5. Control System Type

- 17.5.6. Deployment Mode

- 17.5.7. Organization Size

- 17.5.8. Application

- 17.5.9. Industry Vertical

- 17.6. France Industrial Control & Factory Automation Market

- 17.6.1. Country Segmental Analysis

- 17.6.2. Component

- 17.6.3. Solution

- 17.6.4. Communication Protocol

- 17.6.5. Control System Type

- 17.6.6. Deployment Mode

- 17.6.7. Organization Size

- 17.6.8. Application

- 17.6.9. Industry Vertical

- 17.7. Italy Industrial Control & Factory Automation Market

- 17.7.1. Country Segmental Analysis

- 17.7.2. Component

- 17.7.3. Solution

- 17.7.4. Communication Protocol

- 17.7.5. Control System Type

- 17.7.6. Deployment Mode

- 17.7.7. Organization Size

- 17.7.8. Application

- 17.7.9. Industry Vertical

- 17.8. Spain Industrial Control & Factory Automation Market

- 17.8.1. Country Segmental Analysis

- 17.8.2. Component

- 17.8.3. Solution

- 17.8.4. Communication Protocol

- 17.8.5. Control System Type

- 17.8.6. Deployment Mode

- 17.8.7. Organization Size

- 17.8.8. Application

- 17.8.9. Industry Vertical

- 17.9. Netherlands Industrial Control & Factory Automation Market

- 17.9.1. Country Segmental Analysis

- 17.9.2. Component

- 17.9.3. Solution

- 17.9.4. Communication Protocol

- 17.9.5. Control System Type

- 17.9.6. Deployment Mode

- 17.9.7. Organization Size

- 17.9.8. Application

- 17.9.9. Industry Vertical

- 17.10. Nordic Countries Industrial Control & Factory Automation Market

- 17.10.1. Country Segmental Analysis

- 17.10.2. Component

- 17.10.3. Solution

- 17.10.4. Communication Protocol

- 17.10.5. Control System Type

- 17.10.6. Deployment Mode

- 17.10.7. Organization Size

- 17.10.8. Application

- 17.10.9. Industry Vertical

- 17.11. Poland Industrial Control & Factory Automation Market

- 17.11.1. Country Segmental Analysis

- 17.11.2. Component

- 17.11.3. Solution

- 17.11.4. Communication Protocol

- 17.11.5. Control System Type

- 17.11.6. Deployment Mode

- 17.11.7. Organization Size

- 17.11.8. Application

- 17.11.9. Industry Vertical

- 17.12. Russia & CIS Industrial Control & Factory Automation Market

- 17.12.1. Country Segmental Analysis

- 17.12.2. Component

- 17.12.3. Solution

- 17.12.4. Communication Protocol

- 17.12.5. Control System Type

- 17.12.6. Deployment Mode

- 17.12.7. Organization Size

- 17.12.8. Application

- 17.12.9. Industry Vertical

- 17.13. Rest of Europe Industrial Control & Factory Automation Market

- 17.13.1. Country Segmental Analysis

- 17.13.2. Component

- 17.13.3. Solution

- 17.13.4. Communication Protocol

- 17.13.5. Control System Type

- 17.13.6. Deployment Mode

- 17.13.7. Organization Size

- 17.13.8. Application

- 17.13.9. Industry Vertical

- 18. Asia Pacific Industrial Control & Factory Automation Market Analysis

- 18.1. Key Segment Analysis

- 18.2. Regional Snapshot

- 18.3. Asia Pacific Industrial Control & Factory Automation Market Size (Value - US$ Bn), Analysis, and Forecasts, 2021-2035

- 18.3.1. Component

- 18.3.2. Solution

- 18.3.3. Communication Protocol

- 18.3.4. Control System Type

- 18.3.5. Deployment Mode

- 18.3.6. Organization Size

- 18.3.7. Application

- 18.3.8. Industry Vertical

- 18.3.9. Country

- 18.3.9.1. China

- 18.3.9.2. India

- 18.3.9.3. Japan

- 18.3.9.4. South Korea

- 18.3.9.5. Australia and New Zealand

- 18.3.9.6. Indonesia

- 18.3.9.7. Malaysia

- 18.3.9.8. Thailand

- 18.3.9.9. Vietnam

- 18.3.9.10. Rest of Asia Pacific

- 18.4. China Industrial Control & Factory Automation Market

- 18.4.1. Country Segmental Analysis

- 18.4.2. Component

- 18.4.3. Solution

- 18.4.4. Communication Protocol

- 18.4.5. Control System Type

- 18.4.6. Deployment Mode

- 18.4.7. Organization Size

- 18.4.8. Application

- 18.4.9. Industry Vertical

- 18.5. India Industrial Control & Factory Automation Market

- 18.5.1. Country Segmental Analysis

- 18.5.2. Component

- 18.5.3. Solution

- 18.5.4. Communication Protocol

- 18.5.5. Control System Type

- 18.5.6. Deployment Mode

- 18.5.7. Organization Size

- 18.5.8. Application

- 18.5.9. Industry Vertical

- 18.6. Japan Industrial Control & Factory Automation Market

- 18.6.1. Country Segmental Analysis

- 18.6.2. Component

- 18.6.3. Solution

- 18.6.4. Communication Protocol

- 18.6.5. Control System Type

- 18.6.6. Deployment Mode

- 18.6.7. Organization Size

- 18.6.8. Application

- 18.6.9. Industry Vertical

- 18.7. South Korea Industrial Control & Factory Automation Market

- 18.7.1. Country Segmental Analysis

- 18.7.2. Component

- 18.7.3. Solution

- 18.7.4. Communication Protocol

- 18.7.5. Control System Type

- 18.7.6. Deployment Mode

- 18.7.7. Organization Size

- 18.7.8. Application

- 18.7.9. Industry Vertical

- 18.8. Australia and New Zealand Industrial Control & Factory Automation Market

- 18.8.1. Country Segmental Analysis

- 18.8.2. Component

- 18.8.3. Solution

- 18.8.4. Communication Protocol

- 18.8.5. Control System Type

- 18.8.6. Deployment Mode

- 18.8.7. Organization Size

- 18.8.8. Application

- 18.8.9. Industry Vertical

- 18.9. Indonesia Industrial Control & Factory Automation Market

- 18.9.1. Country Segmental Analysis

- 18.9.2. Component

- 18.9.3. Solution

- 18.9.4. Communication Protocol

- 18.9.5. Control System Type

- 18.9.6. Deployment Mode

- 18.9.7. Organization Size

- 18.9.8. Application

- 18.9.9. Industry Vertical

- 18.10. Malaysia Industrial Control & Factory Automation Market

- 18.10.1. Country Segmental Analysis

- 18.10.2. Component

- 18.10.3. Solution

- 18.10.4. Communication Protocol

- 18.10.5. Control System Type

- 18.10.6. Deployment Mode

- 18.10.7. Organization Size

- 18.10.8. Application

- 18.10.9. Industry Vertical

- 18.11. Thailand Industrial Control & Factory Automation Market

- 18.11.1. Country Segmental Analysis

- 18.11.2. Component

- 18.11.3. Solution

- 18.11.4. Communication Protocol

- 18.11.5. Control System Type

- 18.11.6. Deployment Mode

- 18.11.7. Organization Size

- 18.11.8. Application

- 18.11.9. Industry Vertical

- 18.12. Vietnam Industrial Control & Factory Automation Market

- 18.12.1. Country Segmental Analysis

- 18.12.2. Component

- 18.12.3. Solution

- 18.12.4. Communication Protocol

- 18.12.5. Control System Type

- 18.12.6. Deployment Mode

- 18.12.7. Organization Size

- 18.12.8. Application

- 18.12.9. Industry Vertical

- 18.13. Rest of Asia Pacific Industrial Control & Factory Automation Market

- 18.13.1. Country Segmental Analysis

- 18.13.2. Component

- 18.13.3. Solution

- 18.13.4. Communication Protocol

- 18.13.5. Control System Type

- 18.13.6. Deployment Mode

- 18.13.7. Organization Size

- 18.13.8. Application

- 18.13.9. Industry Vertical

- 19. Middle East Industrial Control & Factory Automation Market Analysis

- 19.1. Key Segment Analysis

- 19.2. Regional Snapshot

- 19.3. Middle East Industrial Control & Factory Automation Market Size (Value - US$ Bn), Analysis, and Forecasts, 2021-2035

- 19.3.1. Component

- 19.3.2. Solution

- 19.3.3. Communication Protocol

- 19.3.4. Control System Type

- 19.3.5. Deployment Mode

- 19.3.6. Organization Size

- 19.3.7. Application

- 19.3.8. Industry Vertical

- 19.3.9. Country

- 19.3.9.1. Turkey

- 19.3.9.2. UAE

- 19.3.9.3. Saudi Arabia

- 19.3.9.4. Israel

- 19.3.9.5. Rest of Middle East

- 19.4. Turkey Industrial Control & Factory Automation Market

- 19.4.1. Country Segmental Analysis

- 19.4.2. Component

- 19.4.3. Solution

- 19.4.4. Communication Protocol

- 19.4.5. Control System Type

- 19.4.6. Deployment Mode

- 19.4.7. Organization Size

- 19.4.8. Application

- 19.4.9. Industry Vertical

- 19.5. UAE Industrial Control & Factory Automation Market

- 19.5.1. Country Segmental Analysis

- 19.5.2. Component

- 19.5.3. Solution

- 19.5.4. Communication Protocol

- 19.5.5. Control System Type

- 19.5.6. Deployment Mode

- 19.5.7. Organization Size

- 19.5.8. Application

- 19.5.9. Industry Vertical

- 19.6. Saudi Arabia Industrial Control & Factory Automation Market

- 19.6.1. Country Segmental Analysis

- 19.6.2. Component

- 19.6.3. Solution

- 19.6.4. Communication Protocol

- 19.6.5. Control System Type

- 19.6.6. Deployment Mode

- 19.6.7. Organization Size

- 19.6.8. Application

- 19.6.9. Industry Vertical

- 19.7. Israel Industrial Control & Factory Automation Market

- 19.7.1. Country Segmental Analysis

- 19.7.2. Component

- 19.7.3. Solution

- 19.7.4. Communication Protocol

- 19.7.5. Control System Type

- 19.7.6. Deployment Mode

- 19.7.7. Organization Size

- 19.7.8. Application

- 19.7.9. Industry Vertical

- 19.8. Rest of Middle East Industrial Control & Factory Automation Market

- 19.8.1. Country Segmental Analysis

- 19.8.2. Component

- 19.8.3. Solution

- 19.8.4. Communication Protocol

- 19.8.5. Control System Type

- 19.8.6. Deployment Mode

- 19.8.7. Organization Size

- 19.8.8. Application

- 19.8.9. Industry Vertical

- 20. Africa Industrial Control & Factory Automation Market Analysis

- 20.1. Key Segment Analysis

- 20.2. Regional Snapshot

- 20.3. Africa Industrial Control & Factory Automation Market Size (Value - US$ Bn), Analysis, and Forecasts, 2021-2035

- 20.3.1. Component

- 20.3.2. Solution

- 20.3.3. Communication Protocol

- 20.3.4. Control System Type

- 20.3.5. Deployment Mode

- 20.3.6. Organization Size

- 20.3.7. Application

- 20.3.8. Industry Vertical

- 20.3.9. Country

- 20.3.9.1. South Africa

- 20.3.9.2. Egypt

- 20.3.9.3. Nigeria

- 20.3.9.4. Algeria

- 20.3.9.5. Rest of Africa

- 20.4. South Africa Industrial Control & Factory Automation Market

- 20.4.1. Country Segmental Analysis

- 20.4.2. Component

- 20.4.3. Solution

- 20.4.4. Communication Protocol

- 20.4.5. Control System Type

- 20.4.6. Deployment Mode

- 20.4.7. Organization Size

- 20.4.8. Application

- 20.4.9. Industry Vertical

- 20.5. Egypt Industrial Control & Factory Automation Market

- 20.5.1. Country Segmental Analysis

- 20.5.2. Component

- 20.5.3. Solution

- 20.5.4. Communication Protocol

- 20.5.5. Control System Type

- 20.5.6. Deployment Mode

- 20.5.7. Organization Size

- 20.5.8. Application

- 20.5.9. Industry Vertical

- 20.6. Nigeria Industrial Control & Factory Automation Market

- 20.6.1. Country Segmental Analysis

- 20.6.2. Component

- 20.6.3. Solution

- 20.6.4. Communication Protocol

- 20.6.5. Control System Type

- 20.6.6. Deployment Mode

- 20.6.7. Organization Size

- 20.6.8. Application

- 20.6.9. Industry Vertical

- 20.7. Algeria Industrial Control & Factory Automation Market

- 20.7.1. Country Segmental Analysis

- 20.7.2. Component

- 20.7.3. Solution

- 20.7.4. Communication Protocol

- 20.7.5. Control System Type

- 20.7.6. Deployment Mode

- 20.7.7. Organization Size

- 20.7.8. Application

- 20.7.9. Industry Vertical

- 20.8. Rest of Africa Industrial Control & Factory Automation Market

- 20.8.1. Country Segmental Analysis

- 20.8.2. Component

- 20.8.3. Solution

- 20.8.4. Communication Protocol

- 20.8.5. Control System Type

- 20.8.6. Deployment Mode

- 20.8.7. Organization Size

- 20.8.8. Application

- 20.8.9. Industry Vertical

- 21. South America Industrial Control & Factory Automation Market Analysis

- 21.1. Key Segment Analysis

- 21.2. Regional Snapshot

- 21.3. South America Industrial Control & Factory Automation Market Size (Value - US$ Bn), Analysis, and Forecasts, 2021-2035

- 21.3.1. Component

- 21.3.2. Solution

- 21.3.3. Communication Protocol

- 21.3.4. Control System Type

- 21.3.5. Deployment Mode

- 21.3.6. Organization Size

- 21.3.7. Application

- 21.3.8. Industry Vertical

- 21.3.9. Country

- 21.3.9.1. Brazil

- 21.3.9.2. Argentina

- 21.3.9.3. Rest of South America

- 21.4. Brazil Industrial Control & Factory Automation Market

- 21.4.1. Country Segmental Analysis

- 21.4.2. Component

- 21.4.3. Solution

- 21.4.4. Communication Protocol

- 21.4.5. Control System Type

- 21.4.6. Deployment Mode

- 21.4.7. Organization Size

- 21.4.8. Application

- 21.4.9. Industry Vertical

- 21.5. Argentina Industrial Control & Factory Automation Market

- 21.5.1. Country Segmental Analysis

- 21.5.2. Component

- 21.5.3. Solution

- 21.5.4. Communication Protocol

- 21.5.5. Control System Type

- 21.5.6. Deployment Mode

- 21.5.7. Organization Size

- 21.5.8. Application

- 21.5.9. Industry Vertical

- 21.6. Rest of South America Industrial Control & Factory Automation Market

- 21.6.1. Country Segmental Analysis

- 21.6.2. Component

- 21.6.3. Solution

- 21.6.4. Communication Protocol

- 21.6.5. Control System Type

- 21.6.6. Deployment Mode

- 21.6.7. Organization Size

- 21.6.8. Application

- 21.6.9. Industry Vertical

- 22. Key Players/ Company Profile

- 22.1. ABB Ltd.

- 22.1.1. Company Details/ Overview

- 22.1.2. Company Financials

- 22.1.3. Key Customers and Competitors

- 22.1.4. Business/ Industry Portfolio

- 22.1.5. Product Portfolio/ Specification Details

- 22.1.6. Pricing Data

- 22.1.7. Strategic Overview

- 22.1.8. Recent Developments

- 22.2. Advantech Co., Ltd.

- 22.3. Beckhoff Automation

- 22.4. Bosch Rexroth

- 22.5. Danfoss Group

- 22.6. Delta Electronics

- 22.7. Emerson Electric Co.

- 22.8. FANUC Corporation

- 22.9. General Electric

- 22.10. Hitachi Industrial Equipment Systems

- 22.11. Honeywell International

- 22.12. Keyence Corporation

- 22.13. Mitsubishi Electric Corporation

- 22.14. Omron Corporation

- 22.15. Phoenix Contact

- 22.16. Rockwell Automation

- 22.17. Schneider Electric

- 22.18. Siemens AG

- 22.19. Yokogawa Electric Corporation

- 22.20. Other Key Players

- 22.1. ABB Ltd.

Note* - This is just tentative list of players. While providing the report, we will cover more number of players based on their revenue and share for each geography

Research Design

Our research design integrates both demand-side and supply-side analysis through a balanced combination of primary and secondary research methodologies. By utilizing both bottom-up and top-down approaches alongside rigorous data triangulation methods, we deliver robust market intelligence that supports strategic decision-making.

MarketGenics' comprehensive research design framework ensures the delivery of accurate, reliable, and actionable market intelligence. Through the integration of multiple research approaches, rigorous validation processes, and expert analysis, we provide our clients with the insights needed to make informed strategic decisions and capitalize on market opportunities.

MarketGenics leverages a dedicated industry panel of experts and a comprehensive suite of paid databases to effectively collect, consolidate, and analyze market intelligence.

Our approach has consistently proven to be reliable and effective in generating accurate market insights, identifying key industry trends, and uncovering emerging business opportunities.

Through both primary and secondary research, we capture and analyze critical company-level data such as manufacturing footprints, including technical centers, R&D facilities, sales offices, and headquarters.

Our expert panel further enhances our ability to estimate market size for specific brands based on validated field-level intelligence.

Our data mining techniques incorporate both parametric and non-parametric methods, allowing for structured data collection, sorting, processing, and cleaning.

Demand projections are derived from large-scale data sets analyzed through proprietary algorithms, culminating in robust and reliable market sizing.

Research Approach

The bottom-up approach builds market estimates by starting with the smallest addressable market units and systematically aggregating them to create comprehensive market size projections.

This method begins with specific, granular data points and builds upward to create the complete market landscape.

Customer Analysis → Segmental Analysis → Geographical Analysis

The top-down approach starts with the broadest possible market data and systematically narrows it down through a series of filters and assumptions to arrive at specific market segments or opportunities.

This method begins with the big picture and works downward to increasingly specific market slices.

TAM → SAM → SOM

Research Methods

Desk / Secondary Research

While analysing the market, we extensively study secondary sources, directories, and databases to identify and collect information useful for this technical, market-oriented, and commercial report. Secondary sources that we utilize are not only the public sources, but it is a combination of Open Source, Associations, Paid Databases, MG Repository & Knowledgebase, and others.

- Company websites, annual reports, financial reports, broker reports, and investor presentations

- National government documents, statistical databases and reports

- News articles, press releases and web-casts specific to the companies operating in the market, Magazines, reports, and others

- We gather information from commercial data sources for deriving company specific data such as segmental revenue, share for geography, product revenue, and others

- Internal and external proprietary databases (industry-specific), relevant patent, and regulatory databases

- Governing Bodies, Government Organizations

- Relevant Authorities, Country-specific Associations for Industries

We also employ the model mapping approach to estimate the product level market data through the players' product portfolio

Primary Research

Primary research/ interviews is vital in analyzing the market. Most of the cases involves paid primary interviews. Primary sources include primary interviews through e-mail interactions, telephonic interviews, surveys as well as face-to-face interviews with the different stakeholders across the value chain including several industry experts.

| Type of Respondents | Number of Primaries |

|---|---|

| Tier 2/3 Suppliers | ~20 |

| Tier 1 Suppliers | ~25 |

| End-users | ~25 |

| Industry Expert/ Panel/ Consultant | ~30 |

| Total | ~100 |

MG Knowledgebase

• Repository of industry blog, newsletter and case studies

• Online platform covering detailed market reports, and company profiles

Forecasting Factors and Models

Forecasting Factors

- Historical Trends – Past market patterns, cycles, and major events that shaped how markets behave over time. Understanding past trends helps predict future behavior.

- Industry Factors – Specific characteristics of the industry like structure, regulations, and innovation cycles that affect market dynamics.

- Macroeconomic Factors – Economic conditions like GDP growth, inflation, and employment rates that affect how much money people have to spend.

- Demographic Factors – Population characteristics like age, income, and location that determine who can buy your product.

- Technology Factors – How quickly people adopt new technology and how much technology infrastructure exists.

- Regulatory Factors – Government rules, laws, and policies that can help or restrict market growth.

- Competitive Factors – Analyzing competition structure such as degree of competition and bargaining power of buyers and suppliers.

Forecasting Models / Techniques

Multiple Regression Analysis

- Identify and quantify factors that drive market changes

- Statistical modeling to establish relationships between market drivers and outcomes

Time Series Analysis – Seasonal Patterns

- Understand regular cyclical patterns in market demand

- Advanced statistical techniques to separate trend, seasonal, and irregular components

Time Series Analysis – Trend Analysis

- Identify underlying market growth patterns and momentum

- Statistical analysis of historical data to project future trends

Expert Opinion – Expert Interviews

- Gather deep industry insights and contextual understanding

- In-depth interviews with key industry stakeholders

Multi-Scenario Development

- Prepare for uncertainty by modeling different possible futures

- Creating optimistic, pessimistic, and most likely scenarios

Time Series Analysis – Moving Averages

- Sophisticated forecasting for complex time series data

- Auto-regressive integrated moving average models with seasonal components

Econometric Models

- Apply economic theory to market forecasting

- Sophisticated economic models that account for market interactions

Expert Opinion – Delphi Method

- Harness collective wisdom of industry experts

- Structured, multi-round expert consultation process

Monte Carlo Simulation

- Quantify uncertainty and probability distributions

- Thousands of simulations with varying input parameters

Research Analysis

Our research framework is built upon the fundamental principle of validating market intelligence from both demand and supply perspectives. This dual-sided approach ensures comprehensive market understanding and reduces the risk of single-source bias.

Demand-Side Analysis: We understand end-user/application behavior, preferences, and market needs along with the penetration of the product for specific application.

Supply-Side Analysis: We estimate overall market revenue, analyze the segmental share along with industry capacity, competitive landscape, and market structure.

Validation & Evaluation

Data triangulation is a validation technique that uses multiple methods, sources, or perspectives to examine the same research question, thereby increasing the credibility and reliability of research findings. In market research, triangulation serves as a quality assurance mechanism that helps identify and minimize bias, validate assumptions, and ensure accuracy in market estimates.

- Data Source Triangulation – Using multiple data sources to examine the same phenomenon

- Methodological Triangulation – Using multiple research methods to study the same research question

- Investigator Triangulation – Using multiple researchers or analysts to examine the same data

- Theoretical Triangulation – Using multiple theoretical perspectives to interpret the same data

Custom Market Research Services

We will customise the research for you, in case the report listed above does not meet your requirements.

Get 10% Free Customisation