Industrial Transmission Market Size, Share & Trends Analysis Report by Product Type (Gears, Belts, Chains, Couplings, Clutches, Shafts & Spindles, Bearings, Others), Power Rating, Transmission Type, End-Use Industry, Installation Type, Distribution Channel and Geography (North America, Europe, Asia Pacific, Middle East, Africa, and South America) – Global Industry Data, Trends, and Forecasts, 2026–2035

|

Market Structure & Evolution |

|

|

Segmental Data Insights |

|

|

Demand Trends |

|

|

Competitive Landscape |

|

|

Strategic Development |

|

|

Future Outlook & Opportunities |

|

Industrial Transmission Market Size, Share, and Growth

The global industrial transmission market is experiencing robust growth, with its estimated value of USD 157.2 billion in the year 2025 and USD 284.2 billion by 2035, registering a CAGR of 6.1% during the forecast period. The global industrial transmission market continues to grow steadily due to technological advances in gearboxes, couplings, and drives that enhance efficiency, dependability, and ability to handle heavy loads.

Siemens AG declared, “Our advanced digital gearbox platform featuring integrated condition monitoring and IoT analytics will allow manufacturers to optimize equipment uptime, decrease maintenance expenses, and expedite automation efforts. Integrating Siemens’ expertise in drive systems with sophisticated predictive diagnostics enables industrial clients to upgrade power transmission infrastructure and enhance operational efficiency in sectors like manufacturing, energy, and logistics.

Manufacturers are focusing on providing compact, high-torque and energy-efficient transmission options with condition monitoring and digital diagnostic for more challenging industrial operations. One example is ABB’s anticipated 2025 launch of a new range of smart gear units with built in sensors and cloud connectivity, allowing real time performance data and predictive maintenance capabilities.

Additionally, to the increase in industrial automation, the growing amount of renewable energy production, primarily through wind energy and the increasing amounts invested into heavy industry (mining, cement, metals, and materials handling) is also contributing to an increase in demand.

Furthermore, stricter efficiency and safety regulations are leading to manufacturers upgrading from traditional mechanical transmission systems to newer, more effective and compliant technologies. Overall, the combination of technological innovation, growth of industrial automation, and regulatory pressure will continue to drive long-term growth of the global industrial transmission market and increase operational efficiencies for all industries.

The continued demand for condition monitoring solutions; predictive maintenance software; electric drives; lubrication systems; and aftermarket services are some adjacent growth opportunities that will allow manufacturers to produce integrated solutions within their drivetrains and thereby increase their recurring revenue sources.

Industrial Transmission Market Dynamics and Trends

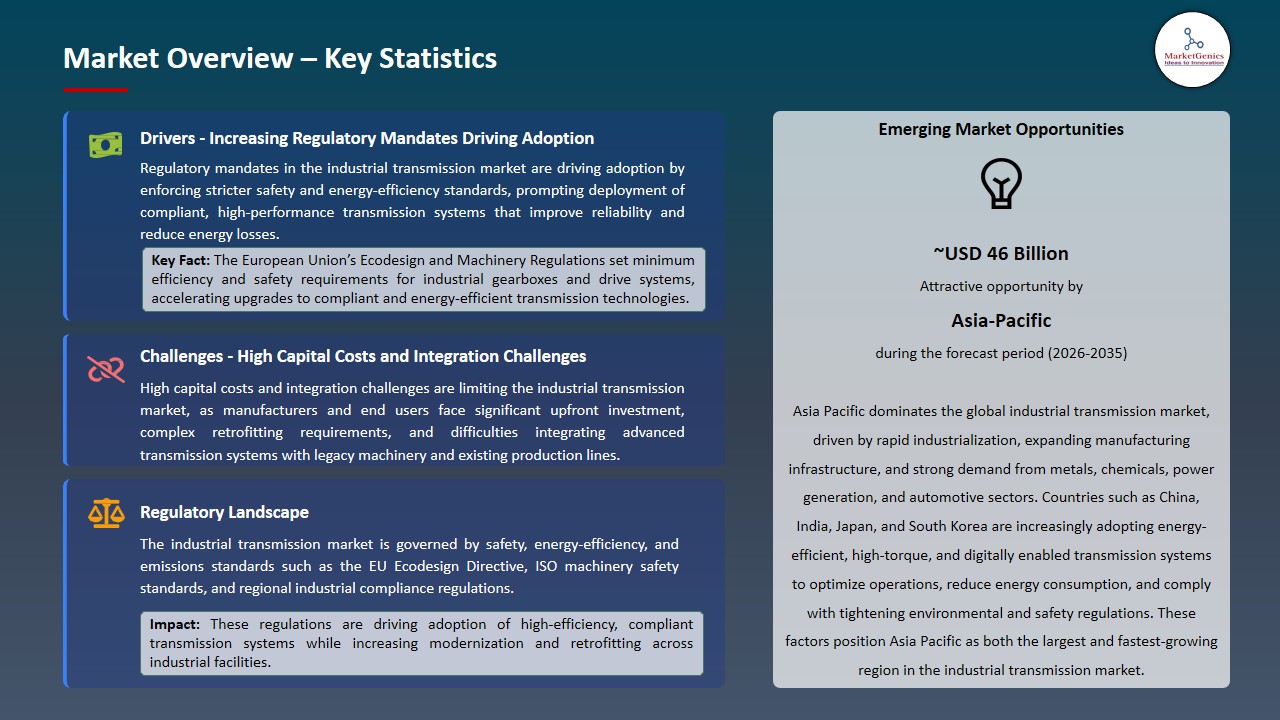

Driver: Increasing Regulatory Mandates Driving Adoption of High-Efficiency and Safe Transmission Systems

-

The industrial transmission market is affected by more demanding compliance with regulations related to machinery efficiency, safety, and emissions; the European Union Ecodesign Directive, as well as ISO standards for the design and operation of industrial gear units, have raised the standard for manufacturers to produce energy-efficient and low-loss gearboxes and drive systems.

- Regulations mandating workplace safety in North America, Europe and Asia-Pacific require that heavier duty equipment, including heavy machinery, mining and material handling equipment, be produced using more reliable and fail-safe transmission components and will cause upgrades to advanced closed-type gear drives and automated systems for monitoring.

- Moreover, to support industries with requirements to meet increasing regulation and sustainability improvement requirements, leading companies, such as SEW-EURODRIVE and Flender, have recently expanded their portfolios of high-efficiency gearboxes and gear drives partners. All these factors are likely to continue to escalate the growth of the industrial transmission market.

Restraint: High Capital Costs and Integration Challenges Limiting Widespread Adoption

-

Advanced industrial transmissions systems are not being introduced to the market because of high initial costs associated with customizing them when fitting newer transmissions into existing industrial plants.

- Examples of difficulties associated with installing advanced transmission systems in legacy machines include the need for skilled workers, the potential for machine downtime, and re-engineering of machinery, all of which may discourage smaller entities from replacing older manufacturing machinery.

- Condition monitoring infrastructure (i.e., sensors and predictive analytics) adds additional capital costs to those companies further delaying widespread implementation of these innovative solutions, even though they will clearly provide long-term benefits. All these elements are expected to restrict the expansion of the industrial transmission market.

Opportunity: Expansion in Renewable Energy and Infrastructure Projects

-

The fast-growing demand for substantial capacity, reliable and long-lasting gearboxes that can be used in turbine applications due to the rapid deployment of renewable energy infrastructure, particularly wind generation.

- The governments of different regions including Asia/ Pacific are increasing their investments in energy and industrial infrastructure therefore providing new avenues for transmission system suppliers to better establish themselves within these markets. Notably, ZF Wind Power located in Coimbatore where they achieved a production capacity of 50 GW of gearboxes. This reinforces the gearboxes position in leading industrial transmission market with the increase in renewable energy and also the fact that much of this growth will occur within local manufacturing.

- The above-mentioned developments present opportunities for transmission manufacturers to provide lower cost compressed air systems and energy savings type solutions with local service networks that will allow for an increase in market penetration and continued growth. And thus, is expected to create more opportunities in future for industrial transmission market.

Key Trend: Digitalization and Condition Monitoring in Industrial Transmissions

-

The next major trend for reduced uptime and extended component life of equipment through predictive maintenance is the implementation of sensor integration into transmission systems as well as the use of IoT connectivity and real-time analytics.

- There is a strong trend across many industries such as mining, logistics, and manufacturing to increasingly utilize both digital twin models and condition-based monitoring platforms for maintenance optimization and equipment performance optimization.

- A prime example of digital transformation within the transmission market is when over 30 % of transmission system orders are now being placed with smart monitoring sensors for continuous, real-time performance improvements. All these elements are expected to influence significant trends in the industrial transmission market.

Industrial Transmission Market Analysis and Segmental Data

Gears Dominates Global Industrial Transmission Market amid Rising Demand for High-Torque and Durable Power Transmission Solutions

-

Gears account for the majority share of the world-wide industrial transmission market because they give the best performance capabilities in transmitting high levels of torque, having precise control over speed, and working reliably under extremely heavy loads and hostile conditions.

- Their robust construction, long life, and flexibility to be applied to multiple industries including: Mining, Cement, Power Generation, Material Handling, and Automotive make them the preferred choice as transmitters when compared to belts or chains. Recently, SEW-EURODRIVE observed expanding their line of heavy-duty industrial gearboxes with added features that allow for integrated condition monitoring in order to provide increased reliability and availability in energy-intensive industries.

- The increasing use of industrial automation and the need for continuous, high load operation will continue to support additional use of gears. These factors collectively reinforce the dominance of gears in the industrial transmission market.

Asia Pacific Dominates Industrial Transmission Market amid Rapid Industrialization and Expanding Manufacturing Infrastructure

-

The industrial transmission market is dominated by the Asia-Pacific region, where fast-paced industrialization, growing manufacturing base and huge investments due to automotive, metals, chemicals and power industries are all prominent contributors.

- The need for high powered drives and gears in heavy industrials and cost-effective manufacture of industrial gearboxes locally and supportive government policies all play a role in this region's overall industrial transmission market. An example of this is ABB's USD 25 million state-of-the-art local facility for manufacturing advanced drive solutions in Vietnam for 2025 to support demand for industrial gear units and electric drives within South East Asia.

- The growth of infrastructure projects such as rail electrification and port modernization creates demand for more installations of transmission systems. These factors collectively underpin Asia Pacific’s leadership in the global industrial transmission market.

Industrial Transmission Market Ecosystem

The industrial transmission market is moderately consolidated; the Tier 1 companies have a medium/high market concentration. The top companies, Siemens, ABB, SEW-EURODRIVE and Flender, provide market-leading technologies and aftermarket service, whereas the Tier 2 and 3 players are primarily located within their individual regions, providing competitive advantages based on low cost or customization. Tier 1 companies are all considered to be global companies.

Key points in value chain include gearbox and drive train manufacturing along with aftermarket services of condition monitoring and maintenance, for example, ABB has expanded its smart drive and gearbox solutions into Asia in 2025; this creates increased delivery of lifecycle value and establishes market placement.

Recent Development and Strategic Overview:

-

In March 2025, NORD DRIVESYSTEMS added new smart gear units (i.e., industrial gearboxes) to their gear unit range that provide integrated condition monitoring and digital interfaces to allow real-time health monitoring, reduce unplanned downtime, and improve energy efficiency of materials handling, food processing, and logistics applications without the need for external condition monitoring equipment.

- In June 2025, Bonfiglioli launched an advanced line of high-torque industrial gearboxes designed for heavy duty mining and renewable energy applications. The modular, sensor-ready design will enable predictive maintenance, increase longevity, and enhance operational reliability for large scale industrial installations.

Report Scope

|

Attribute |

Detail |

|

Market Size in 2025 |

USD 157.2 Bn |

|

Market Forecast Value in 2035 |

USD 284.2 Bn |

|

Growth Rate (CAGR) |

6.1% |

|

Forecast Period |

2026 – 2035 |

|

Historical Data Available for |

2021 – 2024 |

|

Market Size Units |

USD Bn for Value Thousand Units for Volume |

|

Report Format |

Electronic (PDF) + Excel |

|

Regions and Countries Covered |

|||||

|

North America |

Europe |

Asia Pacific |

Middle East |

Africa |

South America |

|

|

|

|

|

|

|

Companies Covered |

|||||

|

|

|

|

|

|

Industrial Transmission Market Segmentation and Highlights

|

Segment |

Sub-segment |

|

Industrial Transmission Market, By Product Type |

|

|

Industrial Transmission Market, By Power Rating |

|

|

Industrial Transmission Market, By Transmission Type |

|

|

Industrial Transmission Market, By End-Use Industry |

|

|

Industrial Transmission Market, By Installation Type |

|

|

Industrial Transmission Market, By Distribution Channel |

|

Frequently Asked Questions

Table of Contents

- 1. Research Methodology and Assumptions

- 1.1. Definitions

- 1.2. Research Design and Approach

- 1.3. Data Collection Methods

- 1.4. Base Estimates and Calculations

- 1.5. Forecasting Models

- 1.5.1. Key Forecast Factors & Impact Analysis

- 1.6. Secondary Research

- 1.6.1. Open Sources

- 1.6.2. Paid Databases

- 1.6.3. Associations

- 1.7. Primary Research

- 1.7.1. Primary Sources

- 1.7.2. Primary Interviews with Stakeholders across Ecosystem

- 2. Executive Summary

- 2.1. Global Industrial Transmission Market Outlook

- 2.1.1. Industrial Transmission Market Size (Volume - Thousand Units & Value - US$ Bn), and Forecasts, 2021-2035

- 2.1.2. Compounded Annual Growth Rate Analysis

- 2.1.3. Growth Opportunity Analysis

- 2.1.4. Segmental Share Analysis

- 2.1.5. Geographical Share Analysis

- 2.2. Market Analysis and Facts

- 2.3. Supply-Demand Analysis

- 2.4. Competitive Benchmarking

- 2.5. Go-to- Market Strategy

- 2.5.1. Customer/ End-use Industry Assessment

- 2.5.2. Growth Opportunity Data, 2026-2035

- 2.5.2.1. Regional Data

- 2.5.2.2. Country Data

- 2.5.2.3. Segmental Data

- 2.5.3. Identification of Potential Market Spaces

- 2.5.4. GAP Analysis

- 2.5.5. Potential Attractive Price Points

- 2.5.6. Prevailing Market Risks & Challenges

- 2.5.7. Preferred Sales & Marketing Strategies

- 2.5.8. Key Recommendations and Analysis

- 2.5.9. A Way Forward

- 2.1. Global Industrial Transmission Market Outlook

- 3. Industry Data and Premium Insights

- 3.1. Global Industrial Machinery Industry Overview, 2025

- 3.1.1. Industrial Machinery Industry Analysis

- 3.1.2. Key Trends for Industrial Machinery Industry

- 3.1.3. Regional Distribution for Industrial Machinery Industry

- 3.2. Supplier Customer Data

- 3.3. Technology Roadmap and Developments

- 3.4. Trade Analysis

- 3.4.1. Import & Export Analysis, 2025

- 3.4.2. Top Importing Countries

- 3.4.3. Top Exporting Countries

- 3.5. Trump Tariff Impact Analysis

- 3.5.1. Manufacturer

- 3.5.1.1. Based on the component & Raw material

- 3.5.2. Supply Chain

- 3.5.3. End Consumer

- 3.5.1. Manufacturer

- 3.6. Raw Material Analysis

- 3.1. Global Industrial Machinery Industry Overview, 2025

- 4. Market Overview

- 4.1. Market Dynamics

- 4.1.1. Drivers

- 4.1.1.1. Rising industrial automation and adoption of smart manufacturing systems.

- 4.1.1.2. Growing demand from heavy industries, renewable energy, and infrastructure projects.

- 4.1.1.3. Increasing focus on energy-efficient, high-torque, and durable transmission solutions.

- 4.1.2. Restraints

- 4.1.2.1. High capital costs and complex retrofitting requirements for legacy machinery.

- 4.1.2.2. Supply chain disruptions and rising component costs due to tariffs and trade tensions.

- 4.1.1. Drivers

- 4.2. Key Trend Analysis

- 4.3. Regulatory Framework

- 4.3.1. Key Regulations, Norms, and Subsidies, by Key Countries

- 4.3.2. Tariffs and Standards

- 4.3.3. Impact Analysis of Regulations on the Market

- 4.4. Value Chain Analysis

- 4.4.1. Component Suppliers

- 4.4.2. System Integrators/ Technology Providers

- 4.4.3. Industrial Transmission Component Manufacturers

- 4.4.4. Distributors

- 4.4.5. End Users

- 4.5. Cost Structure Analysis

- 4.5.1. Parameter’s Share for Cost Associated

- 4.5.2. COGP vs COGS

- 4.5.3. Profit Margin Analysis

- 4.6. Pricing Analysis

- 4.6.1. Regional Pricing Analysis

- 4.6.2. Segmental Pricing Trends

- 4.6.3. Factors Influencing Pricing

- 4.7. Porter’s Five Forces Analysis

- 4.8. PESTEL Analysis

- 4.9. Global Industrial Transmission Market Demand

- 4.9.1. Historical Market Size – Volume (Thousand Units) & Value (US$ Bn), 2020-2024

- 4.9.2. Current and Future Market Size – Volume (Thousand Units) & Value (US$ Bn), 2026–2035

- 4.9.2.1. Y-o-Y Growth Trends

- 4.9.2.2. Absolute $ Opportunity Assessment

- 4.1. Market Dynamics

- 5. Competition Landscape

- 5.1. Competition structure

- 5.1.1. Fragmented v/s consolidated

- 5.2. Company Share Analysis, 2025

- 5.2.1. Global Company Market Share

- 5.2.2. By Region

- 5.2.2.1. North America

- 5.2.2.2. Europe

- 5.2.2.3. Asia Pacific

- 5.2.2.4. Middle East

- 5.2.2.5. Africa

- 5.2.2.6. South America

- 5.3. Product Comparison Matrix

- 5.3.1. Specifications

- 5.3.2. Market Positioning

- 5.3.3. Pricing

- 5.1. Competition structure

- 6. Global Industrial Transmission Market Analysis, by Transmission Type

- 6.1. Key Segment Analysis

- 6.2. Industrial Transmission Market Size (Volume - Thousand Units & Value - US$ Bn), Analysis, and Forecasts, by Transmission Type, 2021-2035

- 6.2.1. Gears

- 6.2.2. Belts

- 6.2.3. Chains

- 6.2.4. Couplings

- 6.2.5. Clutches

- 6.2.6. Shafts & Spindles

- 6.2.7. Bearings

- 6.2.8. Others

- 7. Global Industrial Transmission Market Analysis, by Power Rating

- 7.1. Key Segment Analysis

- 7.2. Industrial Transmission Market Size (Volume - Thousand Units & Value - US$ Bn), Analysis, and Forecasts, by Power Rating, 2021-2035

- 7.2.1. Below 50 HP

- 7.2.2. 50-200 HP

- 7.2.3. Above 200 HP

- 8. Global Industrial Transmission Market Analysis, by Transmission Type

- 8.1. Key Segment Analysis

- 8.2. Industrial Transmission Market Size (Volume - Thousand Units & Value - US$ Bn), Analysis, and Forecasts, by Transmission Type, 2021-2035

- 8.2.1. Mechanical Transmission

- 8.2.2. Hydraulic Transmission

- 8.2.3. Pneumatic Transmission

- 8.2.4. Electrical Transmission

- 9. Global Industrial Transmission Market Analysis, by End-Use Industry

- 9.1. Key Segment Analysis

- 9.2. Industrial Transmission Market Size (Volume - Thousand Units & Value - US$ Bn), Analysis, and Forecasts, by End-Use Industry, 2021-2035

- 9.2.1. Automotive

- 9.2.2. Mining

- 9.2.3. Oil & Gas

- 9.2.4. Power Generation

- 9.2.5. Food & Beverage

- 9.2.6. Chemical & Pharmaceutical

- 9.2.7. Cement & Construction

- 9.2.8. Metal & Mining

- 9.2.9. Pulp & Paper

- 9.2.10. Agriculture

- 9.2.11. Material Handling & Logistics

- 9.2.12. Marine

- 9.2.13. Aerospace & Defense

- 9.2.14. Textile

- 9.2.15. Renewable Energy

- 9.2.16. Other Industries

- 10. Global Industrial Transmission Market Analysis, by Installation Type

- 10.1. Key Segment Analysis

- 10.2. Industrial Transmission Market Size (Volume - Thousand Units & Value - US$ Bn), Analysis, and Forecasts, by Installation Type, 2021-2035

- 10.2.1. New Installation

- 10.2.2. Replacement/Retrofit

- 11. Global Industrial Transmission Market Analysis, by Distribution Channel

- 11.1. Key Segment Analysis

- 11.2. Industrial Transmission Market Size (Volume - Thousand Units & Value - US$ Bn), Analysis, and Forecasts, by Distribution Channel, 2021-2035

- 11.2.1. Direct Sales

- 11.2.2. Distributors

- 11.2.3. Online Channels

- 11.2.4. Aftermarket

- 12. Global Industrial Transmission Market Analysis and Forecasts, by Region

- 12.1. Key Findings

- 12.2. Industrial Transmission Market Size (Volume - Thousand Units & Value - US$ Bn), Analysis, and Forecasts, by Region, 2021-2035

- 12.2.1. North America

- 12.2.2. Europe

- 12.2.3. Asia Pacific

- 12.2.4. Middle East

- 12.2.5. Africa

- 12.2.6. South America

- 13. North America Industrial Transmission Market Analysis

- 13.1. Key Segment Analysis

- 13.2. Regional Snapshot

- 13.3. North America Industrial Transmission Market Size (Volume - Thousand Units & Value - US$ Bn), Analysis, and Forecasts, 2021-2035

- 13.3.1. Product Type

- 13.3.2. Power Rating

- 13.3.3. Transmission Type

- 13.3.4. End-Use Industry

- 13.3.5. Installation Type

- 13.3.6. Distribution Channel

- 13.3.7. Country

- 13.3.7.1. USA

- 13.3.7.2. Canada

- 13.3.7.3. Mexico

- 13.4. USA Industrial Transmission Market

- 13.4.1. Country Segmental Analysis

- 13.4.2. Product Type

- 13.4.3. Power Rating

- 13.4.4. Transmission Type

- 13.4.5. End-Use Industry

- 13.4.6. Installation Type

- 13.4.7. Distribution Channel

- 13.5. Canada Industrial Transmission Market

- 13.5.1. Country Segmental Analysis

- 13.5.2. Product Type

- 13.5.3. Power Rating

- 13.5.4. Transmission Type

- 13.5.5. End-Use Industry

- 13.5.6. Installation Type

- 13.5.7. Distribution Channel

- 13.6. Mexico Industrial Transmission Market

- 13.6.1. Country Segmental Analysis

- 13.6.2. Product Type

- 13.6.3. Power Rating

- 13.6.4. Transmission Type

- 13.6.5. End-Use Industry

- 13.6.6. Installation Type

- 13.6.7. Distribution Channel

- 14. Europe Industrial Transmission Market Analysis

- 14.1. Key Segment Analysis

- 14.2. Regional Snapshot

- 14.3. Europe Industrial Transmission Market Size (Volume - Thousand Units & Value - US$ Bn), Analysis, and Forecasts, 2021-2035

- 14.3.1. Product Type

- 14.3.2. Power Rating

- 14.3.3. Transmission Type

- 14.3.4. End-Use Industry

- 14.3.5. Installation Type

- 14.3.6. Distribution Channel

- 14.3.7. Country

- 14.3.7.1. Germany

- 14.3.7.2. United Kingdom

- 14.3.7.3. France

- 14.3.7.4. Italy

- 14.3.7.5. Spain

- 14.3.7.6. Netherlands

- 14.3.7.7. Nordic Countries

- 14.3.7.8. Poland

- 14.3.7.9. Russia & CIS

- 14.3.7.10. Rest of Europe

- 14.4. Germany Industrial Transmission Market

- 14.4.1. Country Segmental Analysis

- 14.4.2. Product Type

- 14.4.3. Power Rating

- 14.4.4. Transmission Type

- 14.4.5. End-Use Industry

- 14.4.6. Installation Type

- 14.4.7. Distribution Channel

- 14.5. United Kingdom Industrial Transmission Market

- 14.5.1. Country Segmental Analysis

- 14.5.2. Product Type

- 14.5.3. Power Rating

- 14.5.4. Transmission Type

- 14.5.5. End-Use Industry

- 14.5.6. Installation Type

- 14.5.7. Distribution Channel

- 14.6. France Industrial Transmission Market

- 14.6.1. Country Segmental Analysis

- 14.6.2. Product Type

- 14.6.3. Power Rating

- 14.6.4. Transmission Type

- 14.6.5. End-Use Industry

- 14.6.6. Installation Type

- 14.6.7. Distribution Channel

- 14.7. Italy Industrial Transmission Market

- 14.7.1. Country Segmental Analysis

- 14.7.2. Product Type

- 14.7.3. Power Rating

- 14.7.4. Transmission Type

- 14.7.5. End-Use Industry

- 14.7.6. Installation Type

- 14.7.7. Distribution Channel

- 14.8. Spain Industrial Transmission Market

- 14.8.1. Country Segmental Analysis

- 14.8.2. Product Type

- 14.8.3. Power Rating

- 14.8.4. Transmission Type

- 14.8.5. End-Use Industry

- 14.8.6. Installation Type

- 14.8.7. Distribution Channel

- 14.9. Netherlands Industrial Transmission Market

- 14.9.1. Country Segmental Analysis

- 14.9.2. Product Type

- 14.9.3. Power Rating

- 14.9.4. Transmission Type

- 14.9.5. End-Use Industry

- 14.9.6. Installation Type

- 14.9.7. Distribution Channel

- 14.10. Nordic Countries Industrial Transmission Market

- 14.10.1. Country Segmental Analysis

- 14.10.2. Product Type

- 14.10.3. Power Rating

- 14.10.4. Transmission Type

- 14.10.5. End-Use Industry

- 14.10.6. Installation Type

- 14.10.7. Distribution Channel

- 14.11. Poland Industrial Transmission Market

- 14.11.1. Country Segmental Analysis

- 14.11.2. Product Type

- 14.11.3. Power Rating

- 14.11.4. Transmission Type

- 14.11.5. End-Use Industry

- 14.11.6. Installation Type

- 14.11.7. Distribution Channel

- 14.12. Russia & CIS Industrial Transmission Market

- 14.12.1. Country Segmental Analysis

- 14.12.2. Product Type

- 14.12.3. Power Rating

- 14.12.4. Transmission Type

- 14.12.5. End-Use Industry

- 14.12.6. Installation Type

- 14.12.7. Distribution Channel

- 14.13. Rest of Europe Industrial Transmission Market

- 14.13.1. Country Segmental Analysis

- 14.13.2. Product Type

- 14.13.3. Power Rating

- 14.13.4. Transmission Type

- 14.13.5. End-Use Industry

- 14.13.6. Installation Type

- 14.13.7. Distribution Channel

- 15. Asia Pacific Industrial Transmission Market Analysis

- 15.1. Key Segment Analysis

- 15.2. Regional Snapshot

- 15.3. Asia Pacific Industrial Transmission Market Size (Volume - Thousand Units & Value - US$ Bn), Analysis, and Forecasts, 2021-2035

- 15.3.1. Product Type

- 15.3.2. Power Rating

- 15.3.3. Transmission Type

- 15.3.4. End-Use Industry

- 15.3.5. Installation Type

- 15.3.6. Distribution Channel

- 15.3.7. Country

- 15.3.7.1. China

- 15.3.7.2. India

- 15.3.7.3. Japan

- 15.3.7.4. South Korea

- 15.3.7.5. Australia and New Zealand

- 15.3.7.6. Indonesia

- 15.3.7.7. Malaysia

- 15.3.7.8. Thailand

- 15.3.7.9. Vietnam

- 15.3.7.10. Rest of Asia Pacific

- 15.4. China Industrial Transmission Market

- 15.4.1. Country Segmental Analysis

- 15.4.2. Product Type

- 15.4.3. Power Rating

- 15.4.4. Transmission Type

- 15.4.5. End-Use Industry

- 15.4.6. Installation Type

- 15.4.7. Distribution Channel

- 15.5. India Industrial Transmission Market

- 15.5.1. Country Segmental Analysis

- 15.5.2. Product Type

- 15.5.3. Power Rating

- 15.5.4. Transmission Type

- 15.5.5. End-Use Industry

- 15.5.6. Installation Type

- 15.5.7. Distribution Channel

- 15.6. Japan Industrial Transmission Market

- 15.6.1. Country Segmental Analysis

- 15.6.2. Product Type

- 15.6.3. Power Rating

- 15.6.4. Transmission Type

- 15.6.5. End-Use Industry

- 15.6.6. Installation Type

- 15.6.7. Distribution Channel

- 15.7. South Korea Industrial Transmission Market

- 15.7.1. Country Segmental Analysis

- 15.7.2. Product Type

- 15.7.3. Power Rating

- 15.7.4. Transmission Type

- 15.7.5. End-Use Industry

- 15.7.6. Installation Type

- 15.7.7. Distribution Channel

- 15.8. Australia and New Zealand Industrial Transmission Market

- 15.8.1. Country Segmental Analysis

- 15.8.2. Product Type

- 15.8.3. Power Rating

- 15.8.4. Transmission Type

- 15.8.5. End-Use Industry

- 15.8.6. Installation Type

- 15.8.7. Distribution Channel

- 15.9. Indonesia Industrial Transmission Market

- 15.9.1. Country Segmental Analysis

- 15.9.2. Product Type

- 15.9.3. Power Rating

- 15.9.4. Transmission Type

- 15.9.5. End-Use Industry

- 15.9.6. Installation Type

- 15.9.7. Distribution Channel

- 15.10. Malaysia Industrial Transmission Market

- 15.10.1. Country Segmental Analysis

- 15.10.2. Product Type

- 15.10.3. Power Rating

- 15.10.4. Transmission Type

- 15.10.5. End-Use Industry

- 15.10.6. Installation Type

- 15.10.7. Distribution Channel

- 15.11. Thailand Industrial Transmission Market

- 15.11.1. Country Segmental Analysis

- 15.11.2. Product Type

- 15.11.3. Power Rating

- 15.11.4. Transmission Type

- 15.11.5. End-Use Industry

- 15.11.6. Installation Type

- 15.11.7. Distribution Channel

- 15.12. Vietnam Industrial Transmission Market

- 15.12.1. Country Segmental Analysis

- 15.12.2. Product Type

- 15.12.3. Power Rating

- 15.12.4. Transmission Type

- 15.12.5. End-Use Industry

- 15.12.6. Installation Type

- 15.12.7. Distribution Channel

- 15.13. Rest of Asia Pacific Industrial Transmission Market

- 15.13.1. Country Segmental Analysis

- 15.13.2. Product Type

- 15.13.3. Power Rating

- 15.13.4. Transmission Type

- 15.13.5. End-Use Industry

- 15.13.6. Installation Type

- 15.13.7. Distribution Channel

- 16. Middle East Industrial Transmission Market Analysis

- 16.1. Key Segment Analysis

- 16.2. Regional Snapshot

- 16.3. Middle East Industrial Transmission Market Size (Volume - Thousand Units & Value - US$ Bn), Analysis, and Forecasts, 2021-2035

- 16.3.1. Product Type

- 16.3.2. Power Rating

- 16.3.3. Transmission Type

- 16.3.4. End-Use Industry

- 16.3.5. Installation Type

- 16.3.6. Distribution Channel

- 16.3.7. Country

- 16.3.7.1. Turkey

- 16.3.7.2. UAE

- 16.3.7.3. Saudi Arabia

- 16.3.7.4. Israel

- 16.3.7.5. Rest of Middle East

- 16.4. Turkey Industrial Transmission Market

- 16.4.1. Country Segmental Analysis

- 16.4.2. Product Type

- 16.4.3. Power Rating

- 16.4.4. Transmission Type

- 16.4.5. End-Use Industry

- 16.4.6. Installation Type

- 16.4.7. Distribution Channel

- 16.5. UAE Industrial Transmission Market

- 16.5.1. Country Segmental Analysis

- 16.5.2. Product Type

- 16.5.3. Power Rating

- 16.5.4. Transmission Type

- 16.5.5. End-Use Industry

- 16.5.6. Installation Type

- 16.5.7. Distribution Channel

- 16.6. Saudi Arabia Industrial Transmission Market

- 16.6.1. Country Segmental Analysis

- 16.6.2. Product Type

- 16.6.3. Power Rating

- 16.6.4. Transmission Type

- 16.6.5. End-Use Industry

- 16.6.6. Installation Type

- 16.6.7. Distribution Channel

- 16.7. Israel Industrial Transmission Market

- 16.7.1. Country Segmental Analysis

- 16.7.2. Product Type

- 16.7.3. Power Rating

- 16.7.4. Transmission Type

- 16.7.5. End-Use Industry

- 16.7.6. Installation Type

- 16.7.7. Distribution Channel

- 16.8. Rest of Middle East Industrial Transmission Market

- 16.8.1. Country Segmental Analysis

- 16.8.2. Product Type

- 16.8.3. Power Rating

- 16.8.4. Transmission Type

- 16.8.5. End-Use Industry

- 16.8.6. Installation Type

- 16.8.7. Distribution Channel

- 17. Africa Industrial Transmission Market Analysis

- 17.1. Key Segment Analysis

- 17.2. Regional Snapshot

- 17.3. Africa Industrial Transmission Market Size (Volume - Thousand Units & Value - US$ Bn), Analysis, and Forecasts, 2021-2035

- 17.3.1. Product Type

- 17.3.2. Power Rating

- 17.3.3. Transmission Type

- 17.3.4. End-Use Industry

- 17.3.5. Installation Type

- 17.3.6. Distribution Channel

- 17.3.7. Country

- 17.3.7.1. South Africa

- 17.3.7.2. Egypt

- 17.3.7.3. Nigeria

- 17.3.7.4. Algeria

- 17.3.7.5. Rest of Africa

- 17.4. South Africa Industrial Transmission Market

- 17.4.1. Country Segmental Analysis

- 17.4.2. Product Type

- 17.4.3. Power Rating

- 17.4.4. Transmission Type

- 17.4.5. End-Use Industry

- 17.4.6. Installation Type

- 17.4.7. Distribution Channel

- 17.5. Egypt Industrial Transmission Market

- 17.5.1. Country Segmental Analysis

- 17.5.2. Product Type

- 17.5.3. Power Rating

- 17.5.4. Transmission Type

- 17.5.5. End-Use Industry

- 17.5.6. Installation Type

- 17.5.7. Distribution Channel

- 17.6. Nigeria Industrial Transmission Market

- 17.6.1. Country Segmental Analysis

- 17.6.2. Product Type

- 17.6.3. Power Rating

- 17.6.4. Transmission Type

- 17.6.5. End-Use Industry

- 17.6.6. Installation Type

- 17.6.7. Distribution Channel

- 17.7. Algeria Industrial Transmission Market

- 17.7.1. Country Segmental Analysis

- 17.7.2. Product Type

- 17.7.3. Power Rating

- 17.7.4. Transmission Type

- 17.7.5. End-Use Industry

- 17.7.6. Installation Type

- 17.7.7. Distribution Channel

- 17.8. Rest of Africa Industrial Transmission Market

- 17.8.1. Country Segmental Analysis

- 17.8.2. Product Type

- 17.8.3. Power Rating

- 17.8.4. Transmission Type

- 17.8.5. End-Use Industry

- 17.8.6. Installation Type

- 17.8.7. Distribution Channel

- 18. South America Industrial Transmission Market Analysis

- 18.1. Key Segment Analysis

- 18.2. Regional Snapshot

- 18.3. South America Industrial Transmission Market Size (Volume - Thousand Units & Value - US$ Bn), Analysis, and Forecasts, 2021-2035

- 18.3.1. Product Type

- 18.3.2. Power Rating

- 18.3.3. Transmission Type

- 18.3.4. End-Use Industry

- 18.3.5. Installation Type

- 18.3.6. Distribution Channel

- 18.3.7. Country

- 18.3.7.1. Brazil

- 18.3.7.2. Argentina

- 18.3.7.3. Rest of South America

- 18.4. Brazil Industrial Transmission Market

- 18.4.1. Country Segmental Analysis

- 18.4.2. Product Type

- 18.4.3. Power Rating

- 18.4.4. Transmission Type

- 18.4.5. End-Use Industry

- 18.4.6. Installation Type

- 18.4.7. Distribution Channel

- 18.5. Argentina Industrial Transmission Market

- 18.5.1. Country Segmental Analysis

- 18.5.2. Product Type

- 18.5.3. Power Rating

- 18.5.4. Transmission Type

- 18.5.5. End-Use Industry

- 18.5.6. Installation Type

- 18.5.7. Distribution Channel

- 18.6. Rest of South America Industrial Transmission Market

- 18.6.1. Country Segmental Analysis

- 18.6.2. Product Type

- 18.6.3. Power Rating

- 18.6.4. Transmission Type

- 18.6.5. End-Use Industry

- 18.6.6. Installation Type

- 18.6.7. Distribution Channel

- 19. Key Players/ Company Profile

- 19.1. ABB Ltd.

- 19.1.1. Company Details/ Overview

- 19.1.2. Company Financials

- 19.1.3. Key Customers and Competitors

- 19.1.4. Business/ Industry Portfolio

- 19.1.5. Product Portfolio/ Specification Details

- 19.1.6. Pricing Data

- 19.1.7. Strategic Overview

- 19.1.8. Recent Developments

- 19.2. Altra Industrial Motion Corp.

- 19.3. Bonfiglioli Riduttori S.p.A.

- 19.4. Brevini Power Transmission S.p.A.

- 19.5. Continental AG

- 19.6. Eaton Corporation plc

- 19.7. Emerson Electric Co.

- 19.8. Gates Corporation

- 19.9. Heidrive GmbH

- 19.10. KTR Systems GmbH

- 19.11. Nabtesco Corporation

- 19.12. NSK Ltd.

- 19.13. NTN Corporation

- 19.14. Regal Rexnord Corporation

- 19.15. Schaeffler Technologies AG & Co. KG

- 19.16. SEW-Eurodrive GmbH & Co KG

- 19.17. Siemens AG

- 19.18. SKF Group

- 19.19. Sumitomo Heavy Industries, Ltd.

- 19.20. The Timken Company

- 19.21. Tsubakimoto Chain Co.

- 19.22. Voith GmbH & Co. KGaA

- 19.23. Wärtsilä Corporation

- 19.24. Other Key Players

- 19.1. ABB Ltd.

Note* - This is just tentative list of players. While providing the report, we will cover more number of players based on their revenue and share for each geography

Research Design

Our research design integrates both demand-side and supply-side analysis through a balanced combination of primary and secondary research methodologies. By utilizing both bottom-up and top-down approaches alongside rigorous data triangulation methods, we deliver robust market intelligence that supports strategic decision-making.

MarketGenics' comprehensive research design framework ensures the delivery of accurate, reliable, and actionable market intelligence. Through the integration of multiple research approaches, rigorous validation processes, and expert analysis, we provide our clients with the insights needed to make informed strategic decisions and capitalize on market opportunities.

MarketGenics leverages a dedicated industry panel of experts and a comprehensive suite of paid databases to effectively collect, consolidate, and analyze market intelligence.

Our approach has consistently proven to be reliable and effective in generating accurate market insights, identifying key industry trends, and uncovering emerging business opportunities.

Through both primary and secondary research, we capture and analyze critical company-level data such as manufacturing footprints, including technical centers, R&D facilities, sales offices, and headquarters.

Our expert panel further enhances our ability to estimate market size for specific brands based on validated field-level intelligence.

Our data mining techniques incorporate both parametric and non-parametric methods, allowing for structured data collection, sorting, processing, and cleaning.

Demand projections are derived from large-scale data sets analyzed through proprietary algorithms, culminating in robust and reliable market sizing.

Research Approach

The bottom-up approach builds market estimates by starting with the smallest addressable market units and systematically aggregating them to create comprehensive market size projections.

This method begins with specific, granular data points and builds upward to create the complete market landscape.

Customer Analysis → Segmental Analysis → Geographical Analysis

The top-down approach starts with the broadest possible market data and systematically narrows it down through a series of filters and assumptions to arrive at specific market segments or opportunities.

This method begins with the big picture and works downward to increasingly specific market slices.

TAM → SAM → SOM

Research Methods

Desk / Secondary Research

While analysing the market, we extensively study secondary sources, directories, and databases to identify and collect information useful for this technical, market-oriented, and commercial report. Secondary sources that we utilize are not only the public sources, but it is a combination of Open Source, Associations, Paid Databases, MG Repository & Knowledgebase, and others.

- Company websites, annual reports, financial reports, broker reports, and investor presentations

- National government documents, statistical databases and reports

- News articles, press releases and web-casts specific to the companies operating in the market, Magazines, reports, and others

- We gather information from commercial data sources for deriving company specific data such as segmental revenue, share for geography, product revenue, and others

- Internal and external proprietary databases (industry-specific), relevant patent, and regulatory databases

- Governing Bodies, Government Organizations

- Relevant Authorities, Country-specific Associations for Industries

We also employ the model mapping approach to estimate the product level market data through the players' product portfolio

Primary Research

Primary research/ interviews is vital in analyzing the market. Most of the cases involves paid primary interviews. Primary sources include primary interviews through e-mail interactions, telephonic interviews, surveys as well as face-to-face interviews with the different stakeholders across the value chain including several industry experts.

| Type of Respondents | Number of Primaries |

|---|---|

| Tier 2/3 Suppliers | ~20 |

| Tier 1 Suppliers | ~25 |

| End-users | ~25 |

| Industry Expert/ Panel/ Consultant | ~30 |

| Total | ~100 |

MG Knowledgebase

• Repository of industry blog, newsletter and case studies

• Online platform covering detailed market reports, and company profiles

Forecasting Factors and Models

Forecasting Factors

- Historical Trends – Past market patterns, cycles, and major events that shaped how markets behave over time. Understanding past trends helps predict future behavior.

- Industry Factors – Specific characteristics of the industry like structure, regulations, and innovation cycles that affect market dynamics.

- Macroeconomic Factors – Economic conditions like GDP growth, inflation, and employment rates that affect how much money people have to spend.

- Demographic Factors – Population characteristics like age, income, and location that determine who can buy your product.

- Technology Factors – How quickly people adopt new technology and how much technology infrastructure exists.

- Regulatory Factors – Government rules, laws, and policies that can help or restrict market growth.

- Competitive Factors – Analyzing competition structure such as degree of competition and bargaining power of buyers and suppliers.

Forecasting Models / Techniques

Multiple Regression Analysis

- Identify and quantify factors that drive market changes

- Statistical modeling to establish relationships between market drivers and outcomes

Time Series Analysis – Seasonal Patterns

- Understand regular cyclical patterns in market demand

- Advanced statistical techniques to separate trend, seasonal, and irregular components

Time Series Analysis – Trend Analysis

- Identify underlying market growth patterns and momentum

- Statistical analysis of historical data to project future trends

Expert Opinion – Expert Interviews

- Gather deep industry insights and contextual understanding

- In-depth interviews with key industry stakeholders

Multi-Scenario Development

- Prepare for uncertainty by modeling different possible futures

- Creating optimistic, pessimistic, and most likely scenarios

Time Series Analysis – Moving Averages

- Sophisticated forecasting for complex time series data

- Auto-regressive integrated moving average models with seasonal components

Econometric Models

- Apply economic theory to market forecasting

- Sophisticated economic models that account for market interactions

Expert Opinion – Delphi Method

- Harness collective wisdom of industry experts

- Structured, multi-round expert consultation process

Monte Carlo Simulation

- Quantify uncertainty and probability distributions

- Thousands of simulations with varying input parameters

Research Analysis

Our research framework is built upon the fundamental principle of validating market intelligence from both demand and supply perspectives. This dual-sided approach ensures comprehensive market understanding and reduces the risk of single-source bias.

Demand-Side Analysis: We understand end-user/application behavior, preferences, and market needs along with the penetration of the product for specific application.

Supply-Side Analysis: We estimate overall market revenue, analyze the segmental share along with industry capacity, competitive landscape, and market structure.

Validation & Evaluation

Data triangulation is a validation technique that uses multiple methods, sources, or perspectives to examine the same research question, thereby increasing the credibility and reliability of research findings. In market research, triangulation serves as a quality assurance mechanism that helps identify and minimize bias, validate assumptions, and ensure accuracy in market estimates.

- Data Source Triangulation – Using multiple data sources to examine the same phenomenon

- Methodological Triangulation – Using multiple research methods to study the same research question

- Investigator Triangulation – Using multiple researchers or analysts to examine the same data

- Theoretical Triangulation – Using multiple theoretical perspectives to interpret the same data

Custom Market Research Services

We will customise the research for you, in case the report listed above does not meet your requirements.

Get 10% Free Customisation