Pet Cancer Treatment Market Size, Share & Trends Analysis Report by Pet Type (Dogs, Cats, Other Pets), Cancer Type, Treatment Type, Drug Class, Disease Stage, Formulation, End-use, and Geography (North America, Europe, Asia Pacific, Middle East, Africa, and South America) – Global Industry Data, Trends, and Forecasts, 2026–2035

|

|

|

Segmental Data Insights |

|

|

Demand Trends |

|

|

Competitive Landscape |

|

|

Strategic Development |

|

|

Future Outlook & Opportunities |

|

Pet Cancer Treatment Market Size, Share, and Growth

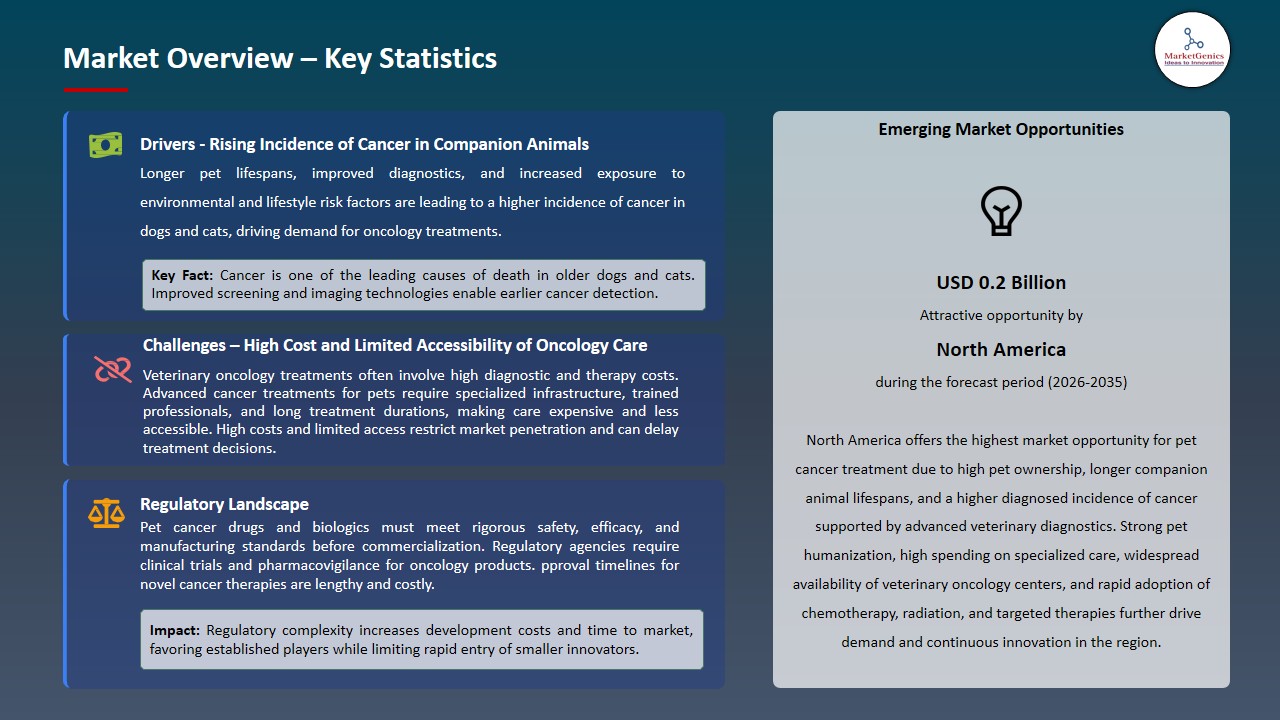

The global pet cancer treatment market is witnessing strong growth, valued at USD 0.5 billion in 2025 and projected to reach ~USD 1 billion by 2035, expanding at a CAGR of 7.1% during the forecast period. Asia Pacific is the fastest-growing region in the pet cancer treatment market due to increasing pet ownership, rising awareness of pet health, expanding veterinary infrastructure, and growing adoption of advanced oncology therapies.

Abhay Nayak, President, Global Diagnostics at Zoetis, said, “y empowering veterinary teams with valuable insights into potentially cancerous cells, we are helping to reduce waiting times and alleviate stress for pet owners facing some of the most challenging moments with their beloved pets. With comprehensive digital cytology capabilities and flexible result delivery options, Vetscan Imagyst AI Masses allows veterinary practices to make timely, individualized treatment decisions”.

The increasing prevalence of cancer in pets is a key motivator to the pet cancer treatment market. As pets are living a long life, they are prone to age related diseases such as cancer. Such a trend is also caused by genetic tendencies and environmental influences including pollutants exposure and lifestyle alterations. Due to increased knowledge about the health of pets, pet owners are demanding higher level of oncology services, which is encouraging innovation in diagnostics, treatment, and therapeutic services.

Telemedicine and remote consultation services create a great opportunity in the market of pet cancer treatment. These online resources enable owners of pets living in remote or under-served communities to seek out specialty veterinary oncology care without, as of now, having to travel long distances. Telehealth could help to increase accessibility by providing advice on time, planning treatment, and post-care follow-ups to promote wider implementation of advanced cancer treatment of pets.

Adjacent opportunities in the pet cancer treatment market include the growth of pet insurance covering oncology treatments, the development of complementary and supportive care solutions such as nutritional and palliative therapies, expansion of specialized veterinary oncology clinics, and the adoption of wearable health monitoring devices. Together, these trends enhance treatment accessibility, improve patient outcomes, and create new avenues for innovation and revenue generation within the market.

Pet Cancer Treatment Market Dynamics and Trends

Driver: Technological Advancements in Cancer Treatment

-

The developments in veterinary oncology technologies largely drive the expansion of the pet cancer treatment market. Immunotherapy, targeted therapy as well as personalized medicine are some of the advanced treatment modalities that are changing the way pets are treated by providing more specific, effective and less invasive treatment options. These inventions enhance better treatment results, minimize adverse effects and increase the quality of life of cancer-affected pets.

- Moreover, molecular diagnostics, genetic profiling, and new drug delivery systems are integrated and allow veterinarians to adjust treatment as per the needs of individual patients. Consequently, the users of these advanced treatments are growing among the pet owners, which leads to the rise of the market on the advanced oncology-based solutions and the increase of the market in general.

- During Q1 2025, Vivos Inc. experienced the highest growth of its IsoPet Animal Cancer Division, which treated 15 pets, which is 150% higher than Q1 2024. The Precision Radionuclide Therapy (PRnT) that is patented by the company involves targeted yttrium-90 radiation therapy in a single-session model, which is an outpatient method that reduces stress in pets. IsoPet also introduced applications in the equine oncology area and three new certified clinics were opened, improving access and also indicating the increasing use of high-end, minimally invasive cancer treatment.

- These innovations combine to highlight the increasing use of new, efficient and affordable treatments, which are a solid force in the pet cancer treatment segment.

Restraint: Limited Specialized Oncology Services

-

The lack of specialized veterinary oncology services is a major issue in the development of a pet cancer treatment market. Lack of qualified veterinary oncologists, especially in rural and semi urban areas limits pets to high-quality cancer treatment. Most pet owners are compelled to use the general veterinary care which might be lacking in oncology services.

- In addition, there is a lack of specialized centers with high-quality diagnostic equipment, radiation therapy, and specific treatment options. This shortage usually leads to the increased waiting time, delayed diagnosis, and the decreased embrace of effective treatments. This is further aggravated by the fact that major metropolitan areas have a high concentration of oncology centers which are geographically and logistically a hindrance to the pet owners.

- Low level of awareness and training facilities to veterans in oncology also serve to worsen the problem of qualified specialists. The general practitioners are not adequately trained to diagnose and provide advanced treatment of early cancer and this limits the reach and effectiveness of specialized oncology services in the Pet Cancer Treatment Market.

- These restrictions together reduce the proliferation of professional cancer care, which suppresses the development of the pet cancer treatment market.

Opportunity: AI & Digital Health Integration

-

The penetration of artificial intelligence (AI) and digital health technologies is an important opportunity to the development of the pet cancer treatment market. Early cancer diagnosis in pets can be improved using AI enabled diagnostic tools and big data analytics, which can provide more accurate and timely diagnoses. The technologies can also aid the individualized treatment planning because they can investigate the data that is patient-specific, forecast therapy results, and streamline the drug choice.

- Moreover, AI and online services can lead to the research and development of new veterinary cancer drugs, which can be introduced faster in the market. Telemedicine and remote monitoring solutions also enhance the delivery of specialized care, especially to pet owners in isolated or underserved areas.

- Zoetis Inc. released AI Masses in June 2025, an AI-based cytology feature that is built into its Vetscan Imagyst analyzer. Within minutes, the technology is able to screen lymph node and skin/subcutaneous lesions of the body in-clinically and precisely. Through deep learning algorithms, AI Masses assists veterinary professionals to make timely and individualized treatment decisions and increase early cancer detection.

- These developments emphasize the fact that AI and digital health technologies are catalyzing early infections, personalized medicine, and expanded use in the market of pet cancer treatment.

Key Trend: Integration of Biomarker & Genetic Testing

-

Biomarker and genetic testing is becoming a significant trend in pet cancer treatment market, and more specific and personalized oncology treatment is being driven. Developed genomic and molecular diagnostics can enable veterinarians to detect specific genetic changes, tumor markers and molecular profiles in individual pets to provide a personalized treatment approach, including targeted therapies or immunotherapies.

- The benefits of these diagnostics are that it enhances the precision of the prognosis, maximizes the impact of treatment and minimizes the side effects through the selection of the most suitable interventions. Moreover, there are continuous innovations in next-generation sequencing and biomarker detection that are improving the possibility of detecting the disease at its early stages and tracking its progression.

- In March 2025, IDEXX Laboratories released IDEXX Cancer Dx, a cheap and easy-to-access blood test to detect early canine lymphoma infection in pets. High-sensitivity high-sensitivity results are obtained in 2-3 days, the panel can be effortlessly incorporated into routine wellness screenings of pets, and it includes tailored advice by providing board-certified oncologists.

- This tendency indicates the transition to accuracy veterinary medicine, which promotes the effectiveness of treatment and the overall development of a market.

Pet-Cancer-Treatment-Market Analysis and Segmental Data

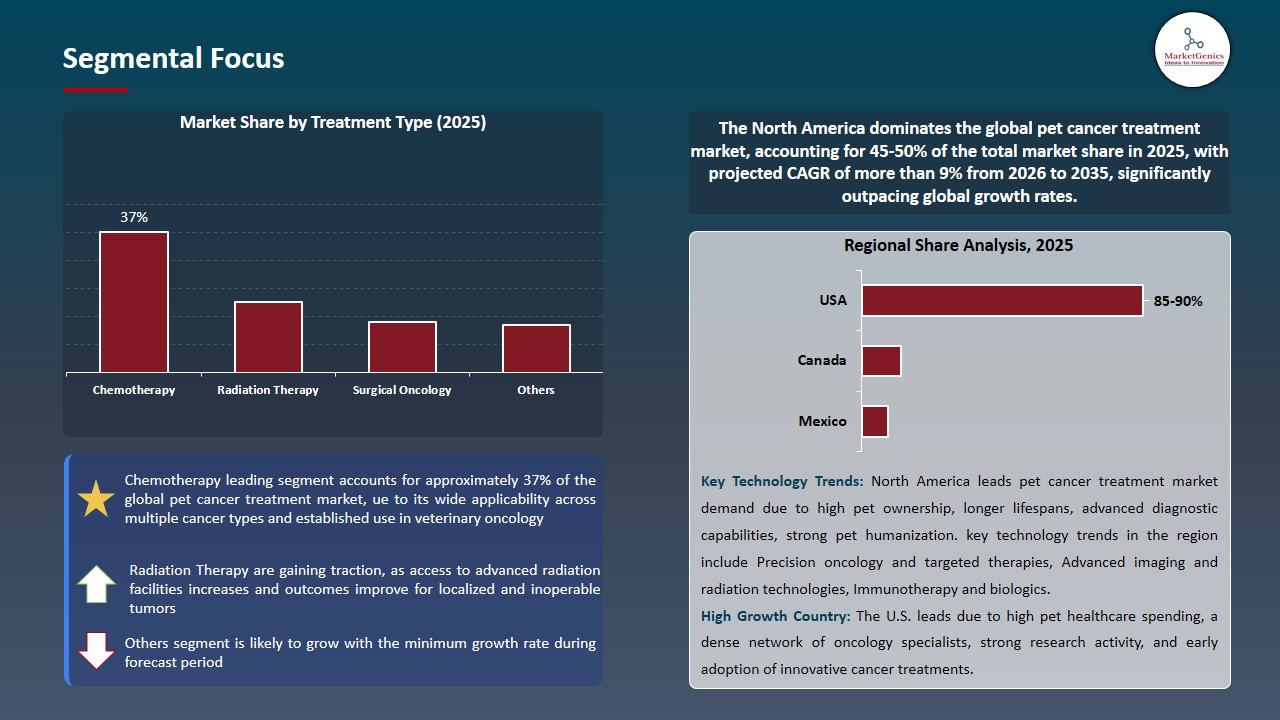

Chemotherapy Dominate Global Pet Cancer Treatment Market

-

Chemotherapy continues to dominate the global pet cancer treatment market as the primary treatment modality for various types of cancers in pets, including dogs and cats. Its widespread adoption is driven by proven efficacy in targeting rapidly dividing cancer cells, reducing tumor size, and complementing other treatment approaches such as surgery and radiation therapy.

- Developments in veterinary forms of chemotherapy routines, dosing regimens, and supportive care plans have greatly enhanced safety standards, reduction of side effects and the overall quality of life of the pets undergoing the therapy.

- The reason is that the administration routes such as oral, injectable, and metronomic chemotherapy are accepted by various clinics because of flexibility to individualize the treatment of patients by veterinarians. Besides, there is the increasing popularity of chemotherapy among pet owners in terms of its advantages, the growing pets number, and the investment in veterinary oncology which are further strengthening its status as the top segment.

- These factors make chemotherapy an indispensable part of the pet cancer management across the globe.

North America Leads Global Pet Cancer Treatment Market Demand

-

North America continues to lead the global pet cancer treatment market, driven by high pet ownership rates, increasing awareness of pet health, and growing expenditure on advanced veterinary care. The region has a well-established veterinary infrastructure, including specialized oncology clinics and access to advanced diagnostic and treatment technologies, which supports early detection and effective management of cancer in pets. Additionally, a large population of aging dogs and cats contributes to the rising incidence of cancer, further boosting demand for veterinary oncology services and treatments.

- Moreover, North American pet owners are increasingly willing to invest in innovative therapies, including chemotherapy, immunotherapy, and precision medicine, to improve outcomes and quality of life for their pets. The presence of supportive regulatory frameworks, insurance coverage for pet health, and active research and development in veterinary oncology also reinforce the region’s leadership.

- Collectively, these factors make North America the dominant market for pet cancer treatment globally.

Pet-Cancer-Treatment-Market Ecosystem

The global pet cancer treatment market is consolidated, with leading players including Elanco Animal Health (including Aratana Therapeutics), Zoetis Inc., Merck Animal Health, Boehringer Ingelheim, and Vetoquinol. These companies maintain competitive advantages through innovative oncology therapies, advanced diagnostics, immunotherapies, targeted and precision medicine solutions, digital health platforms, and specialized veterinary treatment protocols.

The market value chain includes research and development of novel cancer therapies, manufacturing of chemotherapy agents, targeted drugs, immunotherapies, and supportive care products, clinical trials and regulatory compliance, distribution through veterinary clinics, specialty hospitals, and pharmacies, and after-sales services, including pet-owner education, adherence programs, and monitoring support.

Entry barriers are high due to the capital-intensive nature of oncology R&D, the technical expertise required for novel therapy development, strict veterinary safety regulations, and the complexity of integrating treatments across diverse pet species and cancer types.

Ongoing technological innovations such as biomarker-guided therapies, AI-assisted diagnostics, telehealth consultations, and precision medicine approaches continue to drive differentiation, improve outcomes, and increase adoption across the global pet cancer treatment market.

Recent Development and Strategic Overview:

-

In January 2025, Vivesto AB received ethical approval from the US Veterinary Review Board to initiate a dose-finding clinical trial of Paccal Vet for treating cancer in cats. The study, conducted at clinical sites in Washington and Oregon, follows a 3+3 design to determine the maximum tolerated dose, ensuring safety while establishing effective dosing. This trial expands the Paccal Vet program from dogs to cats, providing a promising cancer therapy option for feline patients.

- In August 2025, researchers from UCSF and UC Davis completed the first clinical trial of a novel cancer drug targeting STAT3 in cats with oral squamous cell carcinoma. The study found that 35% of treated cats had their cancer controlled with minimal side effects, a significant improvement over the typical 2–3-month survival. The drug, originally developed for human head and neck cancers, demonstrates potential as a new cancer therapy for cats.

Report Scope

|

Detail |

|

|

Market Size in 2025 |

USD 0.5 Bn |

|

Market Forecast Value in 2035 |

~USD 1 Bn |

|

Growth Rate (CAGR) |

7.1% |

|

Forecast Period |

2026 – 2035 |

|

Historical Data Available for |

2021 – 2024 |

|

Market Size Units |

US$ Billion for Value |

|

Report Format |

Electronic (PDF) + Excel |

|

North America |

Europe |

Asia Pacific |

Middle East |

Africa |

South America |

|

|

|

|

|

|

|

Companies Covered |

|||||

|

|

|

|

|

|

Pet-Cancer-Treatment-Market Segmentation and Highlights

|

Segment |

Sub-segment |

|

Pet Cancer Treatment Market, By Pet Type |

|

|

Pet Cancer Treatment Market, By Cancer Type |

|

|

Pet Cancer Treatment Market, By Treatment Type |

|

|

Pet Cancer Treatment Market, By Drug Class |

|

|

Pet Cancer Treatment Market, By Disease Stage |

|

|

Pet Cancer Treatment Market, By Formulation |

|

|

Pet Cancer Treatment Market, By End-use |

|

Frequently Asked Questions

Table of Contents

- 1. Research Methodology and Assumptions

- 1.1. Definitions

- 1.2. Research Design and Approach

- 1.3. Data Collection Methods

- 1.4. Base Estimates and Calculations

- 1.5. Forecasting Models

- 1.5.1. Key Forecast Factors & Impact Analysis

- 1.6. Secondary Research

- 1.6.1. Open Sources

- 1.6.2. Paid Databases

- 1.6.3. Associations

- 1.7. Primary Research

- 1.7.1. Primary Sources

- 1.7.2. Primary Interviews with Stakeholders across Ecosystem

- 2. Executive Summary

- 2.1. Global Pet Cancer Treatment Market Outlook

- 2.1.1. Pet Cancer Treatment Market Size Value (US$ Bn), and Forecasts, 2021-2035

- 2.1.2. Compounded Annual Growth Rate Analysis

- 2.1.3. Growth Opportunity Analysis

- 2.1.4. Segmental Share Analysis

- 2.1.5. Geographical Share Analysis

- 2.2. Market Analysis and Facts

- 2.3. Supply-Demand Analysis

- 2.4. Competitive Benchmarking

- 2.5. Go-to- Market Strategy

- 2.5.1. Customer/ End-use Industry Assessment

- 2.5.2. Growth Opportunity Data, 2026-2035

- 2.5.2.1. Regional Data

- 2.5.2.2. Country Data

- 2.5.2.3. Segmental Data

- 2.5.3. Identification of Potential Market Spaces

- 2.5.4. GAP Analysis

- 2.5.5. Potential Attractive Price Points

- 2.5.6. Prevailing Market Risks & Challenges

- 2.5.7. Preferred Sales & Marketing Strategies

- 2.5.8. Key Recommendations and Analysis

- 2.5.9. A Way Forward

- 2.1. Global Pet Cancer Treatment Market Outlook

- 3. Industry Data and Premium Insights

- 3.1. Global Healthcare & Pharmaceutical Industry Overview, 2025

- 3.1.1. Healthcare & Pharmaceutical Industry Ecosystem Analysis

- 3.1.2. Key Trends for Healthcare & Pharmaceutical Industry

- 3.1.3. Regional Distribution for Healthcare & Pharmaceutical Industry

- 3.2. Supplier Customer Data

- 3.3. Technology Roadmap and Developments

- 3.4. Trade Analysis

- 3.4.1. Import & Export Analysis, 2025

- 3.4.2. Top Importing Countries

- 3.4.3. Top Exporting Countries

- 3.5. Trump Tariff Impact Analysis

- 3.5.1. Manufacturer

- 3.5.1.1. Based on the component & Raw material

- 3.5.2. Supply Chain

- 3.5.3. End Consumer

- 3.5.1. Manufacturer

- 3.6. Raw Material Analysis

- 3.1. Global Healthcare & Pharmaceutical Industry Overview, 2025

- 4. Market Overview

- 4.1. Market Dynamics

- 4.1.1. Drivers

- 4.1.1.1. Rising incidence of cancer in pets due to longer lifespans and improved diagnostic capabilities.

- 4.1.1.2. Growing pet humanization and willingness of owners to pursue advanced oncology treatments.

- 4.1.1.3. Advancements in veterinary oncology, including targeted therapies and immunotherapies.

- 4.1.2. Restraints

- 4.1.2.1. High cost of cancer diagnostics and treatment limiting affordability.

- 4.1.2.2. Limited availability of specialized veterinary oncology centers and trained professionals.

- 4.1.1. Drivers

- 4.2. Key Trend Analysis

- 4.3. Regulatory Framework

- 4.3.1. Key Regulations, Norms, and Subsidies, by Key Countries

- 4.3.2. Tariffs and Standards

- 4.3.3. Impact Analysis of Regulations on the Market

- 4.4. Value Chain Analysis

- 4.4.1. Raw Material Suppliers

- 4.4.2. Manufacturing & Formulation

- 4.4.3. Distribution & Logistics

- 4.4.4. Retail & E-Commerce Channels

- 4.5. Porter’s Five Forces Analysis

- 4.6. PESTEL Analysis

- 4.7. Global Pet Cancer Treatment Market Demand

- 4.7.1. Historical Market Size – Value (US$ Bn), 2020-2024

- 4.7.2. Current and Future Market Size – Value (US$ Bn), 2026–2035

- 4.7.2.1. Y-o-Y Growth Trends

- 4.7.2.2. Absolute $ Opportunity Assessment

- 4.1. Market Dynamics

- 5. Competition Landscape

- 5.1. Competition structure

- 5.1.1. Fragmented v/s consolidated

- 5.2. Company Share Analysis, 2025

- 5.2.1. Global Company Market Share

- 5.2.2. By Region

- 5.2.2.1. North America

- 5.2.2.2. Europe

- 5.2.2.3. Asia Pacific

- 5.2.2.4. Middle East

- 5.2.2.5. Africa

- 5.2.2.6. South America

- 5.3. Product Comparison Matrix

- 5.3.1. Specifications

- 5.3.2. Market Positioning

- 5.3.3. Pricing

- 5.1. Competition structure

- 6. Global Pet Cancer Treatment Market Analysis, by Pet Type

- 6.1. Key Segment Analysis

- 6.2. Pet Cancer Treatment Market Size Value (US$ Bn), Analysis, and Forecasts, by Product Type, 2021-2035

- 6.2.1. Dogs

- 6.2.1.1. Small Breed Dogs

- 6.2.1.2. Medium Breed Dogs

- 6.2.1.3. Large Breed Dogs

- 6.2.2. Cats

- 6.2.2.1. Domestic Shorthair

- 6.2.2.2. Domestic Longhair

- 6.2.2.3. Purebred Cats

- 6.2.3. Other Pets

- 6.2.3.1. Rabbits

- 6.2.3.2. Ferrets

- 6.2.3.3. Birds

- 6.2.1. Dogs

- 7. Global Pet Cancer Treatment Market Analysis, by Cancer Type

- 7.1. Key Segment Analysis

- 7.2. Pet Cancer Treatment Market Size Value (US$ Bn), Analysis, and Forecasts, by Cancer Type, 2021-2035

- 7.2.1. Lymphoma

- 7.2.1.1. B-cell Lymphoma

- 7.2.1.2. T-cell Lymphoma

- 7.2.1.3. Multicentric Lymphoma

- 7.2.2. Mast Cell Tumors

- 7.2.3. Melanoma

- 7.2.4. Osteosarcoma

- 7.2.5. Mammary Gland Tumors

- 7.2.6. Soft Tissue Sarcomas

- 7.2.7. Hemangiosarcoma

- 7.2.8. Squamous Cell Carcinoma

- 7.2.9. Transitional Cell Carcinoma

- 7.2.10. Others

- 7.2.1. Lymphoma

- 8. Global Pet Cancer Treatment Market Analysis, by Treatment Type

- 8.1. Key Segment Analysis

- 8.2. Pet Cancer Treatment Market Size Value (US$ Bn), Analysis, and Forecasts, by Treatment Type, 2021-2035

- 8.2.1. Chemotherapy

- 8.2.1.1. Single-agent Chemotherapy

- 8.2.1.2. Combination Chemotherapy

- 8.2.1.3. Metronomic Chemotherapy

- 8.2.2. Radiation Therapy

- 8.2.2.1. External Beam Radiation

- 8.2.2.2. Stereotactic Radiation

- 8.2.2.3. Palliative Radiation

- 8.2.3. Surgical Oncology

- 8.2.3.1. Tumor Resection

- 8.2.3.2. Limb Amputation

- 8.2.3.3. Reconstructive Surgery

- 8.2.4. Immunotherapy

- 8.2.4.1. Cancer Vaccines

- 8.2.4.2. Monoclonal Antibodies

- 8.2.4.3. Checkpoint Inhibitors

- 8.2.5. Targeted Therapy

- 8.2.6. Photodynamic Therapy

- 8.2.7. Cryotherapy

- 8.2.8. Palliative Care

- 8.2.1. Chemotherapy

- 9. Global Pet Cancer Treatment Market Analysis, by Drug Class

- 9.1. Key Segment Analysis

- 9.2. Pet Cancer Treatment Market Size Value (US$ Bn), Analysis, and Forecasts, by Drug Class, 2021-2035

- 9.2.1. Alkylating Agents

- 9.2.2. Antimetabolites

- 9.2.3. Anthracyclines

- 9.2.4. Plant Alkaloids

- 9.2.5. Platinum Compounds

- 9.2.6. Tyrosine Kinase Inhibitors

- 9.2.7. Corticosteroids

- 9.2.8. Others

- 10. Global Pet Cancer Treatment Market Analysis, by Disease Stage

- 10.1. Key Segment Analysis

- 10.2. Pet Cancer Treatment Market Size Value (US$ Bn), Analysis, and Forecasts, by Disease Stage, 2021-2035

- 10.2.1. Early Stage (Stage I-II)

- 10.2.2. Advanced Stage (Stage III-IV)

- 10.2.3. Metastatic Cancer

- 10.2.4. Recurrent Cancer

- 11. Global Pet Cancer Treatment Market Analysis, by Formulation

- 11.1. Key Segment Analysis

- 11.2. Pet Cancer Treatment Market Size Value (US$ Bn), Analysis, and Forecasts, by Formulation, 2021-2035

- 11.2.1. Tablets/Capsules

- 11.2.2. Injectable Solutions

- 11.2.3. Suspensions

- 11.2.4. Lyophilized Powder

- 11.2.5. Topical Formulations

- 12. Global Pet Cancer Treatment Market Analysis and Forecasts, by End-use

- 12.1. Key Findings

- 12.2. Pet Cancer Treatment Market Size Value (US$ Bn), Analysis, and Forecasts, by End-use, 2021-2035

- 12.2.1. Veterinary Hospitals

- 12.2.1.1. Diagnostic Oncology

- 12.2.1.2. Surgical Interventions

- 12.2.1.3. Chemotherapy Administration

- 12.2.1.4. Radiation Therapy

- 12.2.1.5. Emergency Cancer Care

- 12.2.1.6. Post-treatment Monitoring

- 12.2.1.7. Others

- 12.2.2. Specialty Veterinary Oncology Centers

- 12.2.2.1. Advanced Cancer Diagnostics

- 12.2.2.2. Complex Surgical Procedures

- 12.2.2.3. Radiation Oncology

- 12.2.2.4. Clinical Trials

- 12.2.2.5. Multimodal Treatment Protocols

- 12.2.2.6. Others

- 12.2.3. Veterinary Clinics

- 12.2.3.1. Cancer Screening

- 12.2.3.2. Basic Oncology Consultations

- 12.2.3.3. Palliative Care

- 12.2.3.4. Others

- 12.2.4. Other End-users

- 12.2.1. Veterinary Hospitals

- 13. Global Pet Cancer Treatment Market Analysis and Forecasts, by Region

- 13.1. Key Findings

- 13.2. Pet Cancer Treatment Market Size Value (US$ Bn), Analysis, and Forecasts, by Region, 2021-2035

- 13.2.1. North America

- 13.2.2. Europe

- 13.2.3. Asia Pacific

- 13.2.4. Middle East

- 13.2.5. Africa

- 13.2.6. South America

- 14. North America Pet Cancer Treatment Market Analysis

- 14.1. Key Segment Analysis

- 14.2. Regional Snapshot

- 14.3. North America Pet Cancer Treatment Market Size Value (US$ Bn), Analysis, and Forecasts, 2021-2035

- 14.3.1. Pet Type

- 14.3.2. Cancer Type

- 14.3.3. Treatment Type

- 14.3.4. Drug Class

- 14.3.5. Disease Stage

- 14.3.6. Formulation

- 14.3.7. End-use

- 14.3.8. Country

- 14.3.8.1. USA

- 14.3.8.2. Canada

- 14.3.8.3. Mexico

- 14.4. USA Pet Cancer Treatment Market

- 14.4.1. Country Segmental Analysis

- 14.4.2. Pet Type

- 14.4.3. Cancer Type

- 14.4.4. Treatment Type

- 14.4.5. Drug Class

- 14.4.6. Disease Stage

- 14.4.7. Formulation

- 14.4.8. End-use

- 14.5. Canada Pet Cancer Treatment Market

- 14.5.1. Country Segmental Analysis

- 14.5.2. Pet Type

- 14.5.3. Cancer Type

- 14.5.4. Treatment Type

- 14.5.5. Drug Class

- 14.5.6. Disease Stage

- 14.5.7. Formulation

- 14.5.8. End-use

- 14.6. Mexico Pet Cancer Treatment Market

- 14.6.1. Country Segmental Analysis

- 14.6.2. Pet Type

- 14.6.3. Cancer Type

- 14.6.4. Treatment Type

- 14.6.5. Drug Class

- 14.6.6. Disease Stage

- 14.6.7. Formulation

- 14.6.8. End-use

- 15. Europe Pet Cancer Treatment Market Analysis

- 15.1. Key Segment Analysis

- 15.2. Regional Snapshot

- 15.3. Europe Pet Cancer Treatment Market Size Value (US$ Bn), Analysis, and Forecasts, 2021-2035

- 15.3.1. Pet Type

- 15.3.2. Cancer Type

- 15.3.3. Treatment Type

- 15.3.4. Drug Class

- 15.3.5. Disease Stage

- 15.3.6. Formulation

- 15.3.7. End-use

- 15.3.8. Country

- 15.3.8.1. Germany

- 15.3.8.2. United Kingdom

- 15.3.8.3. France

- 15.3.8.4. Italy

- 15.3.8.5. Spain

- 15.3.8.6. Netherlands

- 15.3.8.7. Nordic Countries

- 15.3.8.8. Poland

- 15.3.8.9. Russia & CIS

- 15.3.8.10. Rest of Europe

- 15.4. Germany Pet Cancer Treatment Market

- 15.4.1. Country Segmental Analysis

- 15.4.2. Pet Type

- 15.4.3. Cancer Type

- 15.4.4. Treatment Type

- 15.4.5. Drug Class

- 15.4.6. Disease Stage

- 15.4.7. Formulation

- 15.4.8. End-use

- 15.5. United Kingdom Pet Cancer Treatment Market

- 15.5.1. Country Segmental Analysis

- 15.5.2. Pet Type

- 15.5.3. Cancer Type

- 15.5.4. Treatment Type

- 15.5.5. Drug Class

- 15.5.6. Disease Stage

- 15.5.7. Formulation

- 15.5.8. End-use

- 15.6. France Pet Cancer Treatment Market

- 15.6.1. Country Segmental Analysis

- 15.6.2. Pet Type

- 15.6.3. Cancer Type

- 15.6.4. Treatment Type

- 15.6.5. Drug Class

- 15.6.6. Disease Stage

- 15.6.7. Formulation

- 15.6.8. End-use

- 15.7. Italy Pet Cancer Treatment Market

- 15.7.1. Country Segmental Analysis

- 15.7.2. Pet Type

- 15.7.3. Cancer Type

- 15.7.4. Treatment Type

- 15.7.5. Drug Class

- 15.7.6. Disease Stage

- 15.7.7. Formulation

- 15.7.8. End-use

- 15.8. Spain Pet Cancer Treatment Market

- 15.8.1. Country Segmental Analysis

- 15.8.2. Pet Type

- 15.8.3. Cancer Type

- 15.8.4. Treatment Type

- 15.8.5. Drug Class

- 15.8.6. Disease Stage

- 15.8.7. Formulation

- 15.8.8. End-use

- 15.9. Netherlands Pet Cancer Treatment Market

- 15.9.1. Country Segmental Analysis

- 15.9.2. Pet Type

- 15.9.3. Cancer Type

- 15.9.4. Treatment Type

- 15.9.5. Drug Class

- 15.9.6. Disease Stage

- 15.9.7. Formulation

- 15.9.8. End-use

- 15.10. Nordic Countries Pet Cancer Treatment Market

- 15.10.1. Country Segmental Analysis

- 15.10.2. Pet Type

- 15.10.3. Cancer Type

- 15.10.4. Treatment Type

- 15.10.5. Drug Class

- 15.10.6. Disease Stage

- 15.10.7. Formulation

- 15.10.8. End-use

- 15.11. Poland Pet Cancer Treatment Market

- 15.11.1. Country Segmental Analysis

- 15.11.2. Pet Type

- 15.11.3. Cancer Type

- 15.11.4. Treatment Type

- 15.11.5. Drug Class

- 15.11.6. Disease Stage

- 15.11.7. Formulation

- 15.11.8. End-use

- 15.12. Russia & CIS Pet Cancer Treatment Market

- 15.12.1. Country Segmental Analysis

- 15.12.2. Pet Type

- 15.12.3. Cancer Type

- 15.12.4. Treatment Type

- 15.12.5. Drug Class

- 15.12.6. Disease Stage

- 15.12.7. Formulation

- 15.12.8. End-use

- 15.13. Rest of Europe Pet Cancer Treatment Market

- 15.13.1. Country Segmental Analysis

- 15.13.2. Pet Type

- 15.13.3. Cancer Type

- 15.13.4. Treatment Type

- 15.13.5. Drug Class

- 15.13.6. Disease Stage

- 15.13.7. Formulation

- 15.13.8. End-use

- 16. Asia Pacific Pet Cancer Treatment Market Analysis

- 16.1. Key Segment Analysis

- 16.2. Regional Snapshot

- 16.3. Asia Pacific Pet Cancer Treatment Market Size Value (US$ Bn), Analysis, and Forecasts, 2021-2035

- 16.3.1. Pet Type

- 16.3.2. Cancer Type

- 16.3.3. Treatment Type

- 16.3.4. Drug Class

- 16.3.5. Disease Stage

- 16.3.6. Formulation

- 16.3.7. End-use

- 16.3.8. Country

- 16.3.8.1. China

- 16.3.8.2. India

- 16.3.8.3. Japan

- 16.3.8.4. South Korea

- 16.3.8.5. Australia and New Zealand

- 16.3.8.6. Indonesia

- 16.3.8.7. Malaysia

- 16.3.8.8. Thailand

- 16.3.8.9. Vietnam

- 16.3.8.10. Rest of Asia Pacific

- 16.4. China Pet Cancer Treatment Market

- 16.4.1. Country Segmental Analysis

- 16.4.2. Pet Type

- 16.4.3. Cancer Type

- 16.4.4. Treatment Type

- 16.4.5. Drug Class

- 16.4.6. Disease Stage

- 16.4.7. Formulation

- 16.4.8. End-use

- 16.5. India Pet Cancer Treatment Market

- 16.5.1. Country Segmental Analysis

- 16.5.2. Pet Type

- 16.5.3. Cancer Type

- 16.5.4. Treatment Type

- 16.5.5. Drug Class

- 16.5.6. Disease Stage

- 16.5.7. Formulation

- 16.5.8. End-use

- 16.6. Japan Pet Cancer Treatment Market

- 16.6.1. Country Segmental Analysis

- 16.6.2. Pet Type

- 16.6.3. Cancer Type

- 16.6.4. Treatment Type

- 16.6.5. Drug Class

- 16.6.6. Disease Stage

- 16.6.7. Formulation

- 16.6.8. End-use

- 16.7. South Korea Pet Cancer Treatment Market

- 16.7.1. Country Segmental Analysis

- 16.7.2. Pet Type

- 16.7.3. Cancer Type

- 16.7.4. Treatment Type

- 16.7.5. Drug Class

- 16.7.6. Disease Stage

- 16.7.7. Formulation

- 16.7.8. End-use

- 16.8. Australia and New Zealand Pet Cancer Treatment Market

- 16.8.1. Country Segmental Analysis

- 16.8.2. Pet Type

- 16.8.3. Cancer Type

- 16.8.4. Treatment Type

- 16.8.5. Drug Class

- 16.8.6. Disease Stage

- 16.8.7. Formulation

- 16.8.8. End-use

- 16.9. Indonesia Pet Cancer Treatment Market

- 16.9.1. Country Segmental Analysis

- 16.9.2. Pet Type

- 16.9.3. Cancer Type

- 16.9.4. Treatment Type

- 16.9.5. Drug Class

- 16.9.6. Disease Stage

- 16.9.7. Formulation

- 16.9.8. End-use

- 16.10. Malaysia Pet Cancer Treatment Market

- 16.10.1. Country Segmental Analysis

- 16.10.2. Pet Type

- 16.10.3. Cancer Type

- 16.10.4. Treatment Type

- 16.10.5. Drug Class

- 16.10.6. Disease Stage

- 16.10.7. Formulation

- 16.10.8. End-use

- 16.11. Thailand Pet Cancer Treatment Market

- 16.11.1. Country Segmental Analysis

- 16.11.2. Pet Type

- 16.11.3. Cancer Type

- 16.11.4. Treatment Type

- 16.11.5. Drug Class

- 16.11.6. Disease Stage

- 16.11.7. Formulation

- 16.11.8. End-use

- 16.12. Vietnam Pet Cancer Treatment Market

- 16.12.1. Country Segmental Analysis

- 16.12.2. Pet Type

- 16.12.3. Cancer Type

- 16.12.4. Treatment Type

- 16.12.5. Drug Class

- 16.12.6. Disease Stage

- 16.12.7. Formulation

- 16.12.8. End-use

- 16.13. Rest of Asia Pacific Pet Cancer Treatment Market

- 16.13.1. Country Segmental Analysis

- 16.13.2. Pet Type

- 16.13.3. Cancer Type

- 16.13.4. Treatment Type

- 16.13.5. Drug Class

- 16.13.6. Disease Stage

- 16.13.7. Formulation

- 16.13.8. End-use

- 17. Middle East Pet Cancer Treatment Market Analysis

- 17.1. Key Segment Analysis

- 17.2. Regional Snapshot

- 17.3. Middle East Pet Cancer Treatment Market Size Value (US$ Bn), Analysis, and Forecasts, 2021-2035

- 17.3.1. Pet Type

- 17.3.2. Cancer Type

- 17.3.3. Treatment Type

- 17.3.4. Drug Class

- 17.3.5. Disease Stage

- 17.3.6. Formulation

- 17.3.7. End-use

- 17.3.8. Country

- 17.3.8.1. Turkey

- 17.3.8.2. UAE

- 17.3.8.3. Saudi Arabia

- 17.3.8.4. Israel

- 17.3.8.5. Rest of Middle East

- 17.4. Turkey Pet Cancer Treatment Market

- 17.4.1. Country Segmental Analysis

- 17.4.2. Pet Type

- 17.4.3. Cancer Type

- 17.4.4. Treatment Type

- 17.4.5. Drug Class

- 17.4.6. Disease Stage

- 17.4.7. Formulation

- 17.4.8. End-use

- 17.5. UAE Pet Cancer Treatment Market

- 17.5.1. Country Segmental Analysis

- 17.5.2. Pet Type

- 17.5.3. Cancer Type

- 17.5.4. Treatment Type

- 17.5.5. Drug Class

- 17.5.6. Disease Stage

- 17.5.7. Formulation

- 17.5.8. End-use

- 17.6. Saudi Arabia Pet Cancer Treatment Market

- 17.6.1. Country Segmental Analysis

- 17.6.2. Pet Type

- 17.6.3. Cancer Type

- 17.6.4. Treatment Type

- 17.6.5. Drug Class

- 17.6.6. Disease Stage

- 17.6.7. Formulation

- 17.6.8. End-use

- 17.7. Israel Pet Cancer Treatment Market

- 17.7.1. Country Segmental Analysis

- 17.7.2. Pet Type

- 17.7.3. Cancer Type

- 17.7.4. Treatment Type

- 17.7.5. Drug Class

- 17.7.6. Disease Stage

- 17.7.7. Formulation

- 17.7.8. End-use

- 17.8. Rest of Middle East Pet Cancer Treatment Market

- 17.8.1. Country Segmental Analysis

- 17.8.2. Pet Type

- 17.8.3. Cancer Type

- 17.8.4. Treatment Type

- 17.8.5. Drug Class

- 17.8.6. Disease Stage

- 17.8.7. Formulation

- 17.8.8. End-use

- 18. Africa Pet Cancer Treatment Market Analysis

- 18.1. Key Segment Analysis

- 18.2. Regional Snapshot

- 18.3. Africa Pet Cancer Treatment Market Size Value (US$ Bn), Analysis, and Forecasts, 2021-2035

- 18.3.1. Pet Type

- 18.3.2. Cancer Type

- 18.3.3. Treatment Type

- 18.3.4. Drug Class

- 18.3.5. Disease Stage

- 18.3.6. Formulation

- 18.3.7. End-use

- 18.3.8. Country

- 18.3.8.1. South Africa

- 18.3.8.2. Egypt

- 18.3.8.3. Nigeria

- 18.3.8.4. Algeria

- 18.3.8.5. Rest of Africa

- 18.4. South Africa Pet Cancer Treatment Market

- 18.4.1. Country Segmental Analysis

- 18.4.2. Pet Type

- 18.4.3. Cancer Type

- 18.4.4. Treatment Type

- 18.4.5. Drug Class

- 18.4.6. Disease Stage

- 18.4.7. Formulation

- 18.4.8. End-use

- 18.5. Egypt Pet Cancer Treatment Market

- 18.5.1. Country Segmental Analysis

- 18.5.2. Pet Type

- 18.5.3. Cancer Type

- 18.5.4. Treatment Type

- 18.5.5. Drug Class

- 18.5.6. Disease Stage

- 18.5.7. Formulation

- 18.5.8. End-use

- 18.6. Nigeria Pet Cancer Treatment Market

- 18.6.1. Country Segmental Analysis

- 18.6.2. Pet Type

- 18.6.3. Cancer Type

- 18.6.4. Treatment Type

- 18.6.5. Drug Class

- 18.6.6. Disease Stage

- 18.6.7. Formulation

- 18.6.8. End-use

- 18.7. Algeria Pet Cancer Treatment Market

- 18.7.1. Country Segmental Analysis

- 18.7.2. Pet Type

- 18.7.3. Cancer Type

- 18.7.4. Treatment Type

- 18.7.5. Drug Class

- 18.7.6. Disease Stage

- 18.7.7. Formulation

- 18.7.8. End-use

- 18.8. Rest of Africa Pet Cancer Treatment Market

- 18.8.1. Country Segmental Analysis

- 18.8.2. Pet Type

- 18.8.3. Cancer Type

- 18.8.4. Treatment Type

- 18.8.5. Drug Class

- 18.8.6. Disease Stage

- 18.8.7. Formulation

- 18.8.8. End-use

- 19. South America Pet Cancer Treatment Market Analysis

- 19.1. Key Segment Analysis

- 19.2. Regional Snapshot

- 19.3. South America Pet Cancer Treatment Market Size Value (US$ Bn), Analysis, and Forecasts, 2021-2035

- 19.3.1. Pet Type

- 19.3.2. Cancer Type

- 19.3.3. Treatment Type

- 19.3.4. Drug Class

- 19.3.5. Disease Stage

- 19.3.6. Formulation

- 19.3.7. End-use

- 19.3.8. Country

- 19.3.8.1. Brazil

- 19.3.8.2. Argentina

- 19.3.8.3. Rest of South America

- 19.4. Brazil Pet Cancer Treatment Market

- 19.4.1. Country Segmental Analysis

- 19.4.2. Pet Type

- 19.4.3. Cancer Type

- 19.4.4. Treatment Type

- 19.4.5. Drug Class

- 19.4.6. Disease Stage

- 19.4.7. Formulation

- 19.4.8. End-use

- 19.5. Argentina Pet Cancer Treatment Market

- 19.5.1. Country Segmental Analysis

- 19.5.2. Pet Type

- 19.5.3. Cancer Type

- 19.5.4. Treatment Type

- 19.5.5. Drug Class

- 19.5.6. Disease Stage

- 19.5.7. Formulation

- 19.5.8. End-use

- 19.6. Rest of South America Pet Cancer Treatment Market

- 19.6.1. Country Segmental Analysis

- 19.6.2. Pet Type

- 19.6.3. Cancer Type

- 19.6.4. Treatment Type

- 19.6.5. Drug Class

- 19.6.6. Disease Stage

- 19.6.7. Formulation

- 19.6.8. End-use

- 20. Key Players/ Company Profile

- 20.1. Aratana Therapeutics (Elanco)

- 20.1.1. Company Details/ Overview

- 20.1.2. Company Financials

- 20.1.3. Key Customers and Competitors

- 20.1.4. Business/ Industry Portfolio

- 20.1.5. Product Portfolio/ Specification Details

- 20.1.6. Pricing Data

- 20.1.7. Strategic Overview

- 20.1.8. Recent Developments

- 20.2. Aurelius BioTherapeutics

- 20.3. BluePearl Pet Hospital

- 20.4. Boehringer Ingelheim

- 20.5. Dechra Pharmaceuticals

- 20.6. Elanco Animal Health

- 20.7. Ethos Veterinary Health

- 20.8. Karyopharm Therapeutics

- 20.9. Kindred Biosciences

- 20.10. Merck Animal Health

- 20.11. Morphogenesis Inc

- 20.12. Nippon Zenyaku Kogyo

- 20.13. PetCure Oncology

- 20.14. Rhizen Pharmaceuticals

- 20.15. Torigen Pharmaceuticals

- 20.16. TVAX Biomedical

- 20.17. VetDC (Veterinary Dental Center & Oncology Services)

- 20.18. Vetoquinol

- 20.19. Virbac

- 20.20. Zoetis Inc

- 20.21. Other Key Players

- 20.1. Aratana Therapeutics (Elanco)

Note* - This is just tentative list of players. While providing the report, we will cover more number of players based on their revenue and share for each geography

Research Design

Our research design integrates both demand-side and supply-side analysis through a balanced combination of primary and secondary research methodologies. By utilizing both bottom-up and top-down approaches alongside rigorous data triangulation methods, we deliver robust market intelligence that supports strategic decision-making.

MarketGenics' comprehensive research design framework ensures the delivery of accurate, reliable, and actionable market intelligence. Through the integration of multiple research approaches, rigorous validation processes, and expert analysis, we provide our clients with the insights needed to make informed strategic decisions and capitalize on market opportunities.

MarketGenics leverages a dedicated industry panel of experts and a comprehensive suite of paid databases to effectively collect, consolidate, and analyze market intelligence.

Our approach has consistently proven to be reliable and effective in generating accurate market insights, identifying key industry trends, and uncovering emerging business opportunities.

Through both primary and secondary research, we capture and analyze critical company-level data such as manufacturing footprints, including technical centers, R&D facilities, sales offices, and headquarters.

Our expert panel further enhances our ability to estimate market size for specific brands based on validated field-level intelligence.

Our data mining techniques incorporate both parametric and non-parametric methods, allowing for structured data collection, sorting, processing, and cleaning.

Demand projections are derived from large-scale data sets analyzed through proprietary algorithms, culminating in robust and reliable market sizing.

Research Approach

The bottom-up approach builds market estimates by starting with the smallest addressable market units and systematically aggregating them to create comprehensive market size projections.

This method begins with specific, granular data points and builds upward to create the complete market landscape.

Customer Analysis → Segmental Analysis → Geographical Analysis

The top-down approach starts with the broadest possible market data and systematically narrows it down through a series of filters and assumptions to arrive at specific market segments or opportunities.

This method begins with the big picture and works downward to increasingly specific market slices.

TAM → SAM → SOM

Research Methods

Desk / Secondary Research

While analysing the market, we extensively study secondary sources, directories, and databases to identify and collect information useful for this technical, market-oriented, and commercial report. Secondary sources that we utilize are not only the public sources, but it is a combination of Open Source, Associations, Paid Databases, MG Repository & Knowledgebase, and others.

- Company websites, annual reports, financial reports, broker reports, and investor presentations

- National government documents, statistical databases and reports

- News articles, press releases and web-casts specific to the companies operating in the market, Magazines, reports, and others

- We gather information from commercial data sources for deriving company specific data such as segmental revenue, share for geography, product revenue, and others

- Internal and external proprietary databases (industry-specific), relevant patent, and regulatory databases

- Governing Bodies, Government Organizations

- Relevant Authorities, Country-specific Associations for Industries

We also employ the model mapping approach to estimate the product level market data through the players' product portfolio

Primary Research

Primary research/ interviews is vital in analyzing the market. Most of the cases involves paid primary interviews. Primary sources include primary interviews through e-mail interactions, telephonic interviews, surveys as well as face-to-face interviews with the different stakeholders across the value chain including several industry experts.

| Type of Respondents | Number of Primaries |

|---|---|

| Tier 2/3 Suppliers | ~20 |

| Tier 1 Suppliers | ~25 |

| End-users | ~25 |

| Industry Expert/ Panel/ Consultant | ~30 |

| Total | ~100 |

MG Knowledgebase

• Repository of industry blog, newsletter and case studies

• Online platform covering detailed market reports, and company profiles

Forecasting Factors and Models

Forecasting Factors

- Historical Trends – Past market patterns, cycles, and major events that shaped how markets behave over time. Understanding past trends helps predict future behavior.

- Industry Factors – Specific characteristics of the industry like structure, regulations, and innovation cycles that affect market dynamics.

- Macroeconomic Factors – Economic conditions like GDP growth, inflation, and employment rates that affect how much money people have to spend.

- Demographic Factors – Population characteristics like age, income, and location that determine who can buy your product.

- Technology Factors – How quickly people adopt new technology and how much technology infrastructure exists.

- Regulatory Factors – Government rules, laws, and policies that can help or restrict market growth.

- Competitive Factors – Analyzing competition structure such as degree of competition and bargaining power of buyers and suppliers.

Forecasting Models / Techniques

Multiple Regression Analysis

- Identify and quantify factors that drive market changes

- Statistical modeling to establish relationships between market drivers and outcomes

Time Series Analysis – Seasonal Patterns

- Understand regular cyclical patterns in market demand

- Advanced statistical techniques to separate trend, seasonal, and irregular components

Time Series Analysis – Trend Analysis

- Identify underlying market growth patterns and momentum

- Statistical analysis of historical data to project future trends

Expert Opinion – Expert Interviews

- Gather deep industry insights and contextual understanding

- In-depth interviews with key industry stakeholders

Multi-Scenario Development

- Prepare for uncertainty by modeling different possible futures

- Creating optimistic, pessimistic, and most likely scenarios

Time Series Analysis – Moving Averages

- Sophisticated forecasting for complex time series data

- Auto-regressive integrated moving average models with seasonal components

Econometric Models

- Apply economic theory to market forecasting

- Sophisticated economic models that account for market interactions

Expert Opinion – Delphi Method

- Harness collective wisdom of industry experts

- Structured, multi-round expert consultation process

Monte Carlo Simulation

- Quantify uncertainty and probability distributions

- Thousands of simulations with varying input parameters

Research Analysis

Our research framework is built upon the fundamental principle of validating market intelligence from both demand and supply perspectives. This dual-sided approach ensures comprehensive market understanding and reduces the risk of single-source bias.

Demand-Side Analysis: We understand end-user/application behavior, preferences, and market needs along with the penetration of the product for specific application.

Supply-Side Analysis: We estimate overall market revenue, analyze the segmental share along with industry capacity, competitive landscape, and market structure.

Validation & Evaluation

Data triangulation is a validation technique that uses multiple methods, sources, or perspectives to examine the same research question, thereby increasing the credibility and reliability of research findings. In market research, triangulation serves as a quality assurance mechanism that helps identify and minimize bias, validate assumptions, and ensure accuracy in market estimates.

- Data Source Triangulation – Using multiple data sources to examine the same phenomenon

- Methodological Triangulation – Using multiple research methods to study the same research question

- Investigator Triangulation – Using multiple researchers or analysts to examine the same data

- Theoretical Triangulation – Using multiple theoretical perspectives to interpret the same data

Custom Market Research Services

We will customise the research for you, in case the report listed above does not meet your requirements.

Get 10% Free Customisation