Urinary Incontinence Treatment Devices Market Size, Share & Trends Analysis Report by Device Type (Electrical Stimulation Devices, Urethral Slings, Artificial Urinary Sphincters, Urethral Inserts, Vaginal Pessaries, Catheters, Bulking Agents Injection Devices), Technology, Rated Power (for Electrical Stimulation Devices), Rated Capacity (for Collection Devices), Incontinence Type, Gender, Material Type, Distribution Channel, End-Use, and Geography (North America, Europe, Asia Pacific, Middle East, Africa, and South America) – Global Industry Data, Trends, and Forecasts, 2026–2035

|

|

|

Segmental Data Insights |

|

|

Demand Trends |

|

|

Competitive Landscape |

|

|

Strategic Development |

|

|

Future Outlook & Opportunities |

|

Urinary Incontinence Treatment Devices Market Size, Share, and Growth

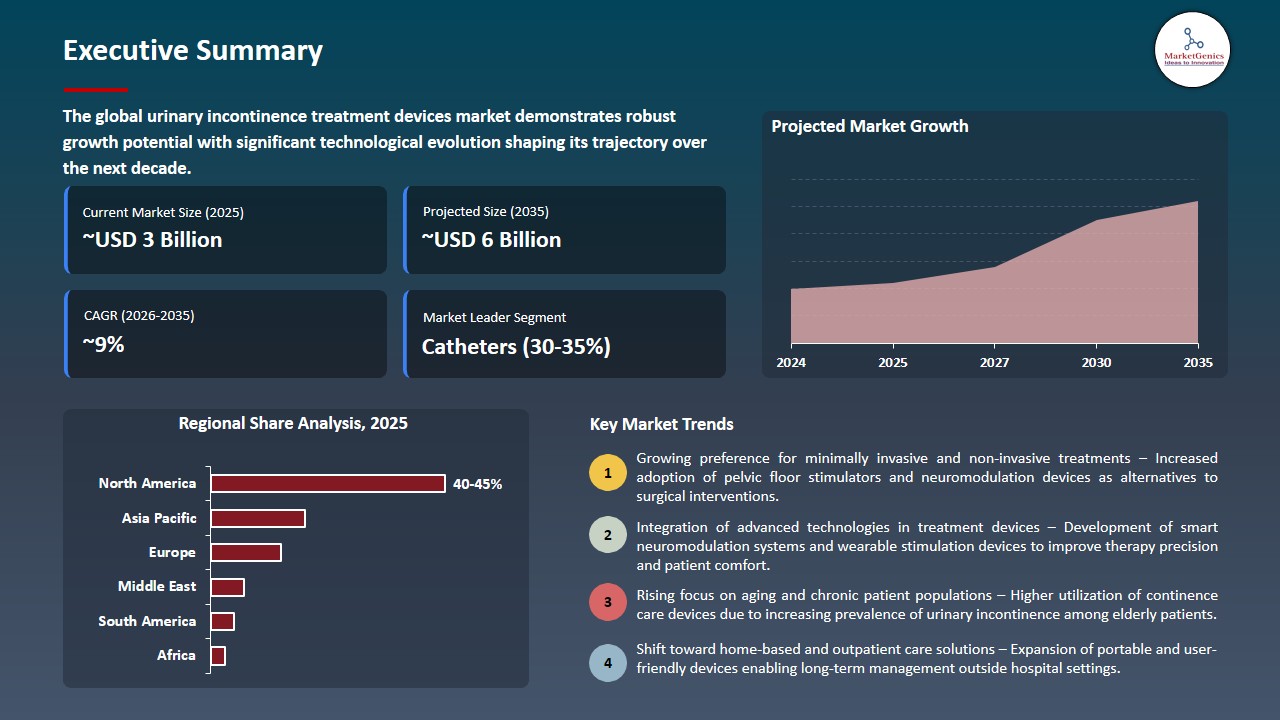

The global urinary incontinence treatment devices market is witnessing strong growth, valued at USD 2.7 billion in 2025 and projected to reach USD 5.9 billion by 2035, expanding at a CAGR of 9.4% during the forecast period. Asia Pacific is the fastest-growing region in the urinary incontinence treatment devices market due to a rapidly aging population, rising prevalence of lifestyle-related disorders, improving healthcare infrastructure, growing awareness of incontinence treatments, and increasing adoption of cost-effective and home-based care solutions.

Mike Cusack, worldwide president of Urology and Critical Care at BD, said, “Urinary incontinence is a common yet under-discussed condition that impacts 25 million Americans and can have profound effects on confidence, social engagement and quality of life, especially among those with mobility challenges, with the launch of the PureWick Portable Collection System, we have an opportunity to help people regain their confidence and independence by delivering a discreet, accessible solution that empowers individuals to participate more fully in everyday activities”.

The urinary incontinence treatment devices market is driven by the increase in the importance of personal hygiene, comfort, and independence. With the focus on the daily quality of life of patients and caregivers, the utilization of supportive equipment like catheters, external collection systems, and minimally invasive solutions is increased. This emphasis promotes the management of incontinence in a timely manner, boosts confidence in patients, and leads to the demand of more advanced and user-friendly devices to treat urinary incontinence.

A major opportunity in the market of urinary incontinence treatment devices is the development of biocompatible and resorbable materials. Such innovations as resorbable slings and implants with antimicrobial coating decrease operative complications, minimize the risk of infections, and increase patient recovery. These developments promote increased utilization of surgical intervention in the treatment of urinary incontinence, patient safety and comfort, and development of minimally invasive and long-term care solutions in the clinical practice.

Adjacent opportunities in urinary incontinence treatment devices market are the development of complementary products, including pelvic floor rehabilitation devices, wearable continence monitors, and smart absorbent products. This can be further improved by integrating with the telehealth platforms, digital therapeutics, and homecare support services which contribute to patient convenience and adherence. Also, gender-specific, pediatric and mobility-specific innovations enable companies to reach underserved groups, broaden market reach, and develop differentiated and patient-centered products.

Urinary Incontinence Treatment Devices Market Dynamics and Trends

Driver: Aging Global Population

-

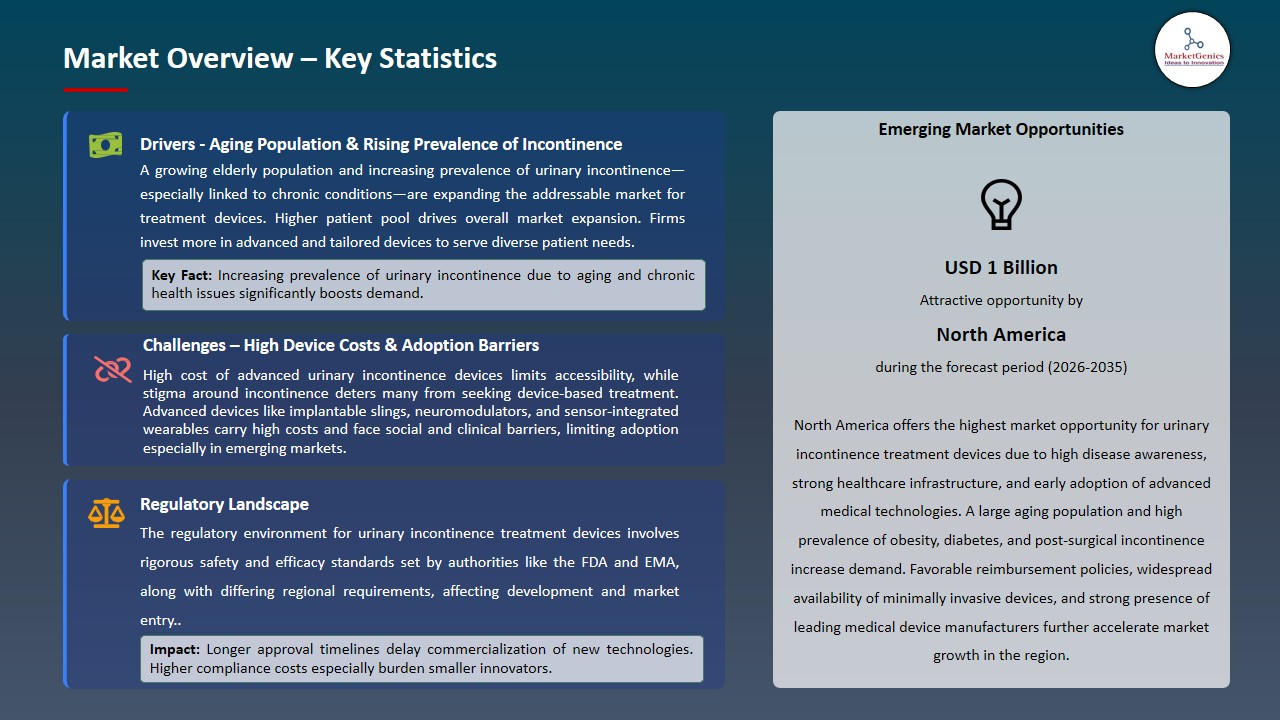

The rising of the global population is considered a key factor in the urinary incontinence treatment devices market since older adults are much more susceptible to urinary incontinence caused by age-related alterations of the bladder functionality, decreased pelvic muscle strength, and increased occurrence of age-related chronic diseases like diabetes, neurological disorders, and prostate problems. As the life expectancy in the world increases, the population of elderly patients in need of proper management of incontinence is growing daily.

- Surgical and non-surgical therapies and devices, such as catheters, external collection systems, slings, and neuromodulation therapies, are also in demand because of this demographic trend. Advanced and user-friendly urinary incontinence treatment devices are on the rise worldwide as patients and caregivers have dissatisfaction with longevity due to their attention towards comfort, independence, and quality of life, which underpin the perpetuation of the market growth.

- Ontex Group introduced its iD Discreet incontinence range in the European healthcare markets in June 2025, which comprised an assortment of absorbent pants and pads that are convenient, discrete, and offer good protection.

- This growth would serve the increasing need of a dignified high-quality continence care among the aging population and offer both home and professional users with quality and dependable products to control urinary incontinence.

Restraint: Regulatory Complexity & Approval Barriers

-

Strict regulatory pressures heavily limit the urinary incontinence treatment devices market. The safety and efficacy of continence devices are closely monitored by regulatory bodies in key markets, such as the FDA in the United States and the European Medicines Agency.

- Other products like slings, catheters and neuromodulation systems require a long and expensive clinical trial and validation procedure to be approved. A delay in the regulatory clearance may delay the product launches and restrict timely availability of new therapies.

- Furthermore, some devices, including mesh-related lawsuits and adverse events, have had a history of related complications, causing regulators to intensify their examination and post-market surveillance to be even more stringent. Manufacturers are forced to spend a lot of money in compliance, documentation and mitigation of risks and this increases the total cost of development and eliminates small players in the market.

- These regulatory issues may obstruct market growth, inhibit innovation and cause uncertainty in the growth rates among healthcare providers and patients and this is a major growth deterrent in the industry.

Opportunity: Technology & Product Innovation

-

The development of sensor-based wearable products, mobile health, and smart monitoring solutions provides substantial prospects to the urinary incontinence treatment devices market. The innovations will help to monitor the bladder activity, symptoms and adherence of therapy in real-time, provide healthcare professionals with the opportunity to create individual treatment regimens and provide remote support.

- It can be integrated with mobile applications and telehealth platforms to provide better patient engagement, convenience, and self-management, as well as better clinical outcomes. Also, intelligent gadgets offer information-based insights to carry out constant product enhancement and innovation.

- BlueWind Medical was cleared in December 2025 with the FDA 510(k) clearance of its improved Revi wearable, an implantable tibial neuromodulation system to urgency urinary incontinence. The device provides personalized, long-term therapy with user-friendly, minimally invasive wearable, and it provides a high level of symptom relief, high level of patient satisfaction, and enhanced convenience.

- Therefore, the increasing patient preference to non-invasive, user-friendly, and connected solutions puts the technology-based development of the urinary incontinence treatment devices in the market to increase market potential.

Key Trend: Minimally Invasive Therapies

-

The use of minimally invasive treatments is a major trend in the urinary incontinence treatment devices market, as patients increasingly prefer less invasive, less risky, and less uncomfortable treatment methods.

- Surgical methods like sacral nerve stimulation (SNS), posterior tibial nerve stimulation (PTNS), and sophisticated sling systems are gaining popularity in comparison to the traditional surgery types because of lower recovery duration, reduced chances of complications, and elevated patient satisfaction. These treatments offer good symptom control and quality of life and independence in the patients.

- In 2025, Boston Scientific increased its urology division by acquiring Axonics, Inc., which provided access to minimally invasive sacral neuromodulation (SNM) devices to treat urinary and bowel dysfunction. The Axonics R20 and F15 systems are targeted SNM therapy afforded to enhance bladder management and quality of life, especially in adults with overactive bladder.

- The trend is also backed by the technological advancements, regulatory clearance and increased clinical evidence that has proven efficacy, which makes minimally invasive interventions a center of interest in the treatment of urinary incontinence across the globe.

Urinary-Incontinence-Treatment-Devices-Market Analysis and Segmental Data

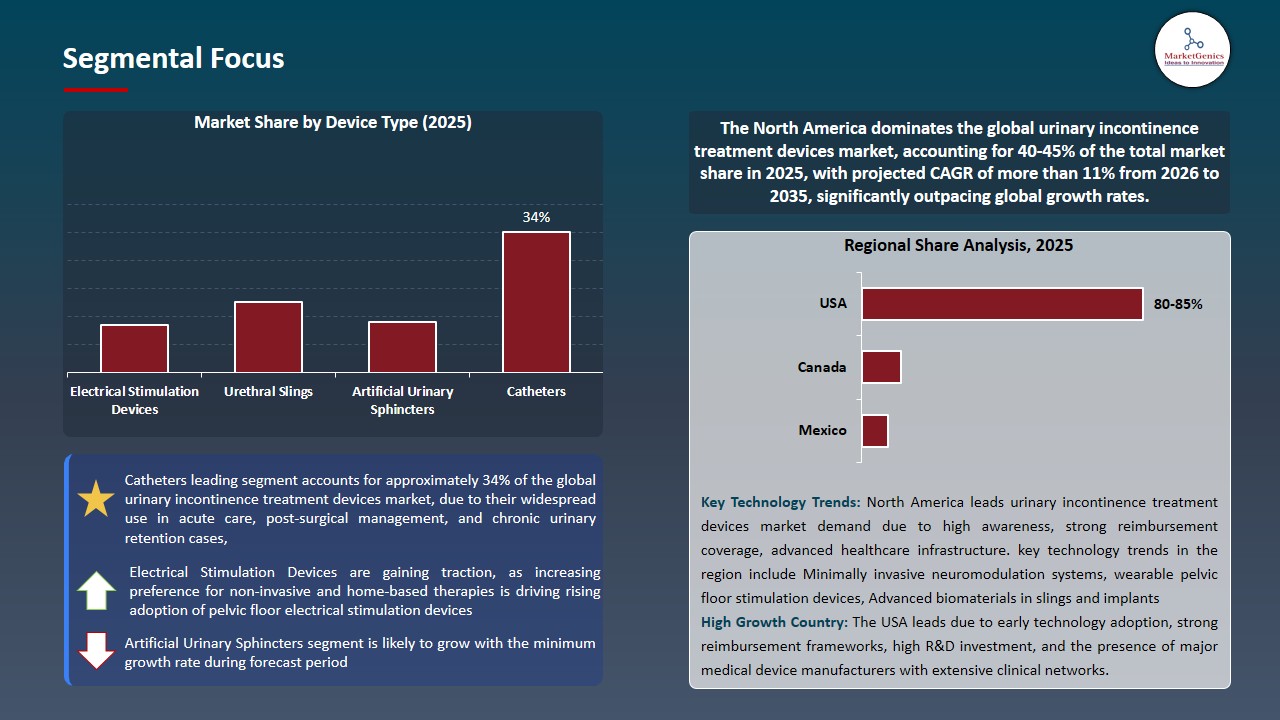

Catheters Dominate Global Urinary Incontinence Treatment Devices Market

-

The catheters is the leading segment in the global urinary incontinence treatment devices Market due to its widespread clinical use and versatility in managing both short-term and long-term incontinence. Catheters are preferred for their ease of use, cost-effectiveness, and suitability across hospital, outpatient, and homecare settings

- The availability of various types, including intermittent, indwelling, and hydrophilic catheters, caters to diverse patient needs, enhancing comfort and compliance. Growing awareness among patients and caregivers about proper catheter use, coupled with continuous product innovations focused on safety, hygiene, and convenience, further strengthens their dominance in the market.

- In November 2025, BD (Becton, Dickinson and Company) launched the PureWick Portable Collection System, a first-of-its-kind, battery-powered urine management device designed for individuals using external catheters to manage urinary incontinence. This innovation extends BD’s trusted PureWick catheter portfolio beyond bedside use, empowering patients to maintain active lifestyles and improving quality of life in urinary incontinence management

- This segment remains a cornerstone of incontinence management worldwide, driving consistent demand and supporting overall market growth.

North America Leads Global Urinary Incontinence Treatment Devices Market Demand

-

North America is the leading region in the global urinary incontinence treatment devices market, driven by advanced healthcare infrastructure, high patient awareness, and early adoption of innovative treatment solutions. The region has a well-established network of specialized urology care centers and hospitals, supporting the widespread use of both surgical and minimally invasive devices.

- A growing aging population with a higher prevalence of urinary incontinence further contributes to market demand, alongside favorable reimbursement policies and strong healthcare coverage that make advanced treatment devices more accessible. Additionally, the integration of digital health technologies and home-based care solutions enhances patient convenience and adherence, supporting sustained market growth.

- Continuous research and development by leading device manufacturers, coupled with patient education initiatives and proactive management of chronic conditions, further reinforce North America’s dominant position.

- These factors collectively ensure that the region maintains strong demand for urinary incontinence treatment devices, fostering innovation and expanded adoption across clinical and home care settings.

Urinary-Incontinence-Treatment-Devices-Market Ecosystem

The global urinary incontinence treatment devices market is moderately consolidated, with key players including Coloplast Group, B. Braun Melsungen AG, Boston Scientific Corporation, Medtronic plc, and Johnson & Johnson. These companies maintain competitive strength through strong research and development capabilities in medical devices, broad portfolios spanning catheters, slings, neuromodulation systems, and wearable solutions, well-established clinical and hospital relationships, and extensive distribution through hospitals, clinics, and home healthcare channels. Continuous innovation in minimally invasive technologies, patient-centric device design, and digital health integration further supports their market presence, while regulatory expertise and strategic partnerships enhance credibility and global reach.

The Urinary Incontinence Treatment Devices value chain spans raw material sourcing and device research, product design and manufacturing under strict quality and safety standards, clinical validation and regulatory compliance, branding and packaging, multi-channel distribution via hospitals, specialty clinics, and homecare suppliers, and post-market activities including patient education, training programs, and device lifecycle management.

Entry barriers remain high due to stringent regulatory requirements, the need for clinical evidence and safety validation, brand reputation, technological expertise, and competition from established device manufacturers. Ongoing innovations in minimally invasive procedures, smart and wearable devices, home-based care solutions, and integration with telehealth platforms continue to drive differentiation and adoption across the global market.

Recent Development and Strategic Overview:

-

In September 2025, Medtronic received FDA approval for the Altaviva implantable tibial neuromodulation (ITNM) device, a minimally invasive therapy for urge urinary incontinence. The device, inserted near the ankle, delivers automated electrical stimulation to regulate bladder control, requires no daily intervention, and offers a long battery life.

- In June 2025, Neuspera Medical received FDA approval for its integrated sacral neuromodulation (iSNM) system for treating urinary urge incontinence (UUI). The device offers a miniaturized, implantable neurostimulator activated via an external disc, eliminating the need for implanted batteries and reducing surgical risks.

Report Scope

|

Detail |

|

|

Market Size in 2025 |

USD 2.7 Bn |

|

Market Forecast Value in 2035 |

USD 5.9 Bn |

|

Growth Rate (CAGR) |

9.4% |

|

Forecast Period |

2026 – 2035 |

|

Historical Data Available for |

2021 – 2024 |

|

Market Size Units |

US$ Billion for Value Thousand Units for Volume |

|

Report Format |

Electronic (PDF) + Excel |

|

North America |

Europe |

Asia Pacific |

Middle East |

Africa |

South America |

|

|

|

|

|

|

|

Companies Covered |

|||||

|

|

|

|

|

|

Urinary-Incontinence-Treatment-Devices-Market Segmentation and Highlights

|

Segment |

Sub-segment |

|

Urinary Incontinence Treatment Devices Market, By Device Type |

|

|

Urinary Incontinence Treatment Devices Market, By Technology |

|

|

Urinary Incontinence Treatment Devices Market, By Rated Power (for Electrical Stimulation Devices) |

|

|

Urinary Incontinence Treatment Devices Market, By Rated Capacity (for Collection Devices) |

|

|

Urinary Incontinence Treatment Devices Market, By Incontinence Type |

|

|

Urinary Incontinence Treatment Devices Market, By Gender |

|

|

Urinary Incontinence Treatment Devices Market, By Material Type |

|

|

Urinary Incontinence Treatment Devices Market, By Distribution Channel |

|

|

Urinary Incontinence Treatment Devices Market, By End-Use |

|

Frequently Asked Questions

Table of Contents

- 1. Research Methodology and Assumptions

- 1.1. Definitions

- 1.2. Research Design and Approach

- 1.3. Data Collection Methods

- 1.4. Base Estimates and Calculations

- 1.5. Forecasting Models

- 1.5.1. Key Forecast Factors & Impact Analysis

- 1.6. Secondary Research

- 1.6.1. Open Sources

- 1.6.2. Paid Databases

- 1.6.3. Associations

- 1.7. Primary Research

- 1.7.1. Primary Sources

- 1.7.2. Primary Interviews with Stakeholders across Ecosystem

- 2. Executive Summary

- 2.1. Global Urinary Incontinence Treatment Devices Market Outlook

- 2.1.1. Urinary Incontinence Treatment Devices Market Size Volume (Thousand Units) and Value (US$ Bn), and Forecasts, 2021-2035

- 2.1.2. Compounded Annual Growth Rate Analysis

- 2.1.3. Growth Opportunity Analysis

- 2.1.4. Segmental Share Analysis

- 2.1.5. Geographical Share Analysis

- 2.2. Market Analysis and Facts

- 2.3. Supply-Demand Analysis

- 2.4. Competitive Benchmarking

- 2.5. Go-to- Market Strategy

- 2.5.1. Customer/ End-use Industry Assessment

- 2.5.2. Growth Opportunity Data, 2026-2035

- 2.5.2.1. Regional Data

- 2.5.2.2. Country Data

- 2.5.2.3. Segmental Data

- 2.5.3. Identification of Potential Market Spaces

- 2.5.4. GAP Analysis

- 2.5.5. Potential Attractive Price Points

- 2.5.6. Prevailing Market Risks & Challenges

- 2.5.7. Preferred Sales & Marketing Strategies

- 2.5.8. Key Recommendations and Analysis

- 2.5.9. A Way Forward

- 2.1. Global Urinary Incontinence Treatment Devices Market Outlook

- 3. Industry Data and Premium Insights

- 3.1. Global Healthcare & Pharmaceutical Industry Overview, 2025

- 3.1.1. Healthcare & Pharmaceutical Industry Ecosystem Analysis

- 3.1.2. Key Trends for Healthcare & Pharmaceutical Industry

- 3.1.3. Regional Distribution for Healthcare & Pharmaceutical Industry

- 3.2. Supplier Customer Data

- 3.3. Technology Roadmap and Developments

- 3.4. Trade Analysis

- 3.4.1. Import & Export Analysis, 2025

- 3.4.2. Top Importing Countries

- 3.4.3. Top Exporting Countries

- 3.5. Trump Tariff Impact Analysis

- 3.5.1. Manufacturer

- 3.5.1.1. Based on the component & Raw material

- 3.5.2. Supply Chain

- 3.5.3. End Consumer

- 3.5.1. Manufacturer

- 3.6. Raw Material Analysis

- 3.1. Global Healthcare & Pharmaceutical Industry Overview, 2025

- 4. Market Overview

- 4.1. Market Dynamics

- 4.1.1. Drivers

- 4.1.1.1. Rising prevalence of urinary incontinence due to aging population and lifestyle-related conditions

- 4.1.1.2. Growing adoption of minimally invasive and home-based incontinence treatment devices

- 4.1.1.3. Increasing awareness, diagnosis rates, and demand for improved quality-of-life solutions

- 4.1.2. Restraints

- 4.1.2.1. Stringent regulatory approval processes and high compliance costs

- 4.1.2.2. Social stigma and underreporting of urinary incontinence limiting treatment adoption

- 4.1.1. Drivers

- 4.2. Key Trend Analysis

- 4.3. Regulatory Framework

- 4.3.1. Key Regulations, Norms, and Subsidies, by Key Countries

- 4.3.2. Tariffs and Standards

- 4.3.3. Impact Analysis of Regulations on the Market

- 4.4. Value Chain Analysis

- 4.4.1. Component Suppliers

- 4.4.2. Manufacturers

- 4.4.3. System Integrators

- 4.4.4. Sales Channel

- 4.4.5. End-users

- 4.5. PricingAnalysis

- 4.6. CostingAnalysis

- 4.7. Porter’s Five Forces Analysis

- 4.8. PESTEL Analysis

- 4.9. Global Urinary Incontinence Treatment Devices Market Demand

- 4.9.1. Historical Market Size – Volume (Thousand Units) and Value (US$ Bn), 2020-2024

- 4.9.2. Current and Future Market Size – Volume (Thousand Units) and Value (US$ Bn), 2026–2035

- 4.9.2.1. Y-o-Y Growth Trends

- 4.9.2.2. Absolute $ Opportunity Assessment

- 4.1. Market Dynamics

- 5. Competition Landscape

- 5.1. Competition structure

- 5.1.1. Fragmented v/s consolidated

- 5.2. Company Share Analysis, 2025

- 5.2.1. Global Company Market Share

- 5.2.2. By Region

- 5.2.2.1. North America

- 5.2.2.2. Europe

- 5.2.2.3. Asia Pacific

- 5.2.2.4. Middle East

- 5.2.2.5. Africa

- 5.2.2.6. South America

- 5.3. Product Comparison Matrix

- 5.3.1. Specifications

- 5.3.2. Market Positioning

- 5.3.3. Pricing

- 5.1. Competition structure

- 6. Global Urinary Incontinence Treatment Devices Market Analysis, by Device Type

- 6.1. Key Segment Analysis

- 6.2. Urinary Incontinence Treatment Devices Market Size Volume (Thousand Units) and Value (US$ Bn), Analysis, and Forecasts, by Device Type, 2021-2035

- 6.2.1. Electrical Stimulation Devices

- 6.2.1.1. Percutaneous Tibial Nerve Stimulation (PTNS) Devices

- 6.2.1.2. Sacral Nerve Stimulation (SNS) Devices

- 6.2.1.3. Vaginal Electrical Stimulation Devices

- 6.2.1.4. Others

- 6.2.2. Urethral Slings

- 6.2.2.1. Mid-Urethral Slings

- 6.2.2.2. Traditional Slings

- 6.2.2.3. Adjustable Slings

- 6.2.3. Artificial Urinary Sphincters

- 6.2.4. Urethral Inserts

- 6.2.5. Vaginal Pessaries

- 6.2.6. Catheters

- 6.2.6.1. Intermittent Catheters

- 6.2.6.2. Indwelling Catheters

- 6.2.6.3. External Catheters

- 6.2.7. Bulking Agents Injection Devices

- 6.2.1. Electrical Stimulation Devices

- 7. Global Urinary Incontinence Treatment Devices Market Analysis, by Technology

- 7.1. Key Segment Analysis

- 7.2. Urinary Incontinence Treatment Devices Market Size Volume (Thousand Units) and Value (US$ Bn), Analysis, and Forecasts, by Technology, 2021-2035

- 7.2.1. Implantable Devices

- 7.2.2. External Devices

- 7.2.3. Minimally Invasive Devices

- 7.2.4. Non-Invasive Devices

- 8. Global Urinary Incontinence Treatment Devices Market Analysis, by Rated Power (for Electrical Stimulation Devices)

- 8.1. Key Segment Analysis

- 8.2. Urinary Incontinence Treatment Devices Market Size Volume (Thousand Units) and Value (US$ Bn), Analysis, and Forecasts, by Rated Power (for Electrical Stimulation Devices), 2021-2035

- 8.2.1. Low Power (0-5 Watts)

- 8.2.2. Medium Power (5-15 Watts)

- 8.2.3. High Power (Above 15 Watts)

- 9. Global Urinary Incontinence Treatment Devices Market Analysis, by Rated Capacity (for Collection Devices)

- 9.1. Key Segment Analysis

- 9.2. Urinary Incontinence Treatment Devices Market Size Volume (Thousand Units) and Value (US$ Bn), Analysis, and Forecasts, by Rated Capacity (for Collection Devices), 2021-2035

- 9.2.1. Small Capacity (Up to 500 ml)

- 9.2.2. Medium Capacity (500-1000 ml)

- 9.2.3. Large Capacity (Above 1000 ml)

- 10. Global Urinary Incontinence Treatment Devices Market Analysis, by Incontinence Type

- 10.1. Key Segment Analysis

- 10.2. Urinary Incontinence Treatment Devices Market Size Volume (Thousand Units) and Value (US$ Bn), Analysis, and Forecasts, by Incontinence Type, 2021-2035

- 10.2.1. Stress Incontinence

- 10.2.2. Urge Incontinence

- 10.2.3. Overflow Incontinence

- 10.2.4. Functional Incontinence

- 10.2.5. Mixed Incontinence

- 11. Global Urinary Incontinence Treatment Devices Market Analysis, by Gender

- 11.1. Key Segment Analysis

- 11.2. Urinary Incontinence Treatment Devices Market Size Volume (Thousand Units) and Value (US$ Bn), Analysis, and Forecasts, by Gender, 2021-2035

- 11.2.1. Female-Specific Devices

- 11.2.2. Male-Specific Devices

- 11.2.3. Unisex Devices

- 12. Global Urinary Incontinence Treatment Devices Market Analysis and Forecasts, by Material Type

- 12.1. Key Findings

- 12.2. Urinary Incontinence Treatment Devices Market Size Volume (Thousand Units) and Value (US$ Bn), Analysis, and Forecasts, by Material Type, 2021-2035

- 12.2.1. Silicone-Based

- 12.2.2. Polyurethane-Based

- 12.2.3. Polypropylene-Based

- 12.2.4. Metal Alloys

- 12.2.5. Bioabsorbable Materials

- 12.2.6. Hybrid Materials

- 13. Global Urinary Incontinence Treatment Devices Market Analysis and Forecasts, by Distribution Channel

- 13.1. Key Findings

- 13.2. Urinary Incontinence Treatment Devices Market Size Volume (Thousand Units) and Value (US$ Bn), Analysis, and Forecasts, by Distribution Channel, 2021-2035

- 13.2.1. Hospitals Pharmacies

- 13.2.2. Retail Pharmacies

- 13.2.3. Online Pharmacies

- 13.2.4. Medical Supply Stores

- 13.2.5. Direct Sales

- 14. Global Urinary Incontinence Treatment Devices Market Analysis and Forecasts, by End-Use

- 14.1. Key Findings

- 14.2. Urinary Incontinence Treatment Devices Market Size Volume (Thousand Units) and Value (US$ Bn), Analysis, and Forecasts, by End-Use, 2021-2035

- 14.2.1. Hospitals

- 14.2.1.1. Surgical Implantation

- 14.2.1.2. Emergency Care

- 14.2.1.3. Outpatient Procedures

- 14.2.1.4. Diagnostic Evaluation

- 14.2.1.5. Post-Operative Management

- 14.2.1.6. Others

- 14.2.2. Specialty Clinics

- 14.2.2.1. Ambulatory Surgical Centers

- 14.2.2.2. Same-Day Surgical Procedures

- 14.2.2.3. Minimally Invasive Treatments

- 14.2.2.4. Follow-Up Care

- 14.2.2.5. Others

- 14.2.3. Home Care Settings

- 14.2.4. Nursing Homes & Assisted Living Facilities

- 14.2.5. Rehabilitation Centers

- 14.2.6. Diagnostic Centers

- 14.2.7. Other End-use

- 14.2.1. Hospitals

- 15. Global Urinary Incontinence Treatment Devices Market Analysis and Forecasts, by Region

- 15.1. Key Findings

- 15.2. Urinary Incontinence Treatment Devices Market Size Volume (Thousand Units) and Value (US$ Bn), Analysis, and Forecasts, by Region, 2021-2035

- 15.2.1. North America

- 15.2.2. Europe

- 15.2.3. Asia Pacific

- 15.2.4. Middle East

- 15.2.5. Africa

- 15.2.6. South America

- 16. North America Urinary Incontinence Treatment Devices Market Analysis

- 16.1. Key Segment Analysis

- 16.2. Regional Snapshot

- 16.3. North America Urinary Incontinence Treatment Devices Market Size Volume (Thousand Units) and Value (US$ Bn), Analysis, and Forecasts, 2021-2035

- 16.3.1. Device Type

- 16.3.2. Technology

- 16.3.3. Rated Power (for Electrical Stimulation Devices)

- 16.3.4. Rated Capacity (for Collection Devices)

- 16.3.5. Incontinence Type

- 16.3.6. Gender

- 16.3.7. Material Type

- 16.3.8. Distribution Channel

- 16.3.9. End-Use

- 16.3.10. Country

- 16.3.10.1. USA

- 16.3.10.2. Canada

- 16.3.10.3. Mexico

- 16.4. USA Urinary Incontinence Treatment Devices Market

- 16.4.1. Country Segmental Analysis

- 16.4.2. Device Type

- 16.4.3. Technology

- 16.4.4. Rated Power (for Electrical Stimulation Devices)

- 16.4.5. Rated Capacity (for Collection Devices)

- 16.4.6. Incontinence Type

- 16.4.7. Gender

- 16.4.8. Material Type

- 16.4.9. Distribution Channel

- 16.4.10. End-Use

- 16.5. Canada Urinary Incontinence Treatment Devices Market

- 16.5.1. Country Segmental Analysis

- 16.5.2. Device Type

- 16.5.3. Technology

- 16.5.4. Rated Power (for Electrical Stimulation Devices)

- 16.5.5. Rated Capacity (for Collection Devices)

- 16.5.6. Incontinence Type

- 16.5.7. Gender

- 16.5.8. Material Type

- 16.5.9. Distribution Channel

- 16.5.10. End-Use

- 16.6. Mexico Urinary Incontinence Treatment Devices Market

- 16.6.1. Country Segmental Analysis

- 16.6.2. Device Type

- 16.6.3. Technology

- 16.6.4. Rated Power (for Electrical Stimulation Devices)

- 16.6.5. Rated Capacity (for Collection Devices)

- 16.6.6. Incontinence Type

- 16.6.7. Gender

- 16.6.8. Material Type

- 16.6.9. Distribution Channel

- 16.6.10. End-Use

- 17. Europe Urinary Incontinence Treatment Devices Market Analysis

- 17.1. Key Segment Analysis

- 17.2. Regional Snapshot

- 17.3. Europe Urinary Incontinence Treatment Devices Market Size Volume (Thousand Units) and Value (US$ Bn), Analysis, and Forecasts, 2021-2035

- 17.3.1. Device Type

- 17.3.2. Technology

- 17.3.3. Rated Power (for Electrical Stimulation Devices)

- 17.3.4. Rated Capacity (for Collection Devices)

- 17.3.5. Incontinence Type

- 17.3.6. Gender

- 17.3.7. Material Type

- 17.3.8. Distribution Channel

- 17.3.9. End-Use

- 17.3.10. Country

- 17.3.10.1. Germany

- 17.3.10.2. United Kingdom

- 17.3.10.3. France

- 17.3.10.4. Italy

- 17.3.10.5. Spain

- 17.3.10.6. Netherlands

- 17.3.10.7. Nordic Countries

- 17.3.10.8. Poland

- 17.3.10.9. Russia & CIS

- 17.3.10.10. Rest of Europe

- 17.4. Germany Urinary Incontinence Treatment Devices Market

- 17.4.1. Country Segmental Analysis

- 17.4.2. Device Type

- 17.4.3. Technology

- 17.4.4. Rated Power (for Electrical Stimulation Devices)

- 17.4.5. Rated Capacity (for Collection Devices)

- 17.4.6. Incontinence Type

- 17.4.7. Gender

- 17.4.8. Material Type

- 17.4.9. Distribution Channel

- 17.4.10. End-Use

- 17.5. United Kingdom Urinary Incontinence Treatment Devices Market

- 17.5.1. Country Segmental Analysis

- 17.5.2. Device Type

- 17.5.3. Technology

- 17.5.4. Rated Power (for Electrical Stimulation Devices)

- 17.5.5. Rated Capacity (for Collection Devices)

- 17.5.6. Incontinence Type

- 17.5.7. Gender

- 17.5.8. Material Type

- 17.5.9. Distribution Channel

- 17.5.10. End-Use

- 17.6. France Urinary Incontinence Treatment Devices Market

- 17.6.1. Country Segmental Analysis

- 17.6.2. Device Type

- 17.6.3. Technology

- 17.6.4. Rated Power (for Electrical Stimulation Devices)

- 17.6.5. Rated Capacity (for Collection Devices)

- 17.6.6. Incontinence Type

- 17.6.7. Gender

- 17.6.8. Material Type

- 17.6.9. Distribution Channel

- 17.6.10. End-Use

- 17.7. Italy Urinary Incontinence Treatment Devices Market

- 17.7.1. Country Segmental Analysis

- 17.7.2. Device Type

- 17.7.3. Technology

- 17.7.4. Rated Power (for Electrical Stimulation Devices)

- 17.7.5. Rated Capacity (for Collection Devices)

- 17.7.6. Incontinence Type

- 17.7.7. Gender

- 17.7.8. Material Type

- 17.7.9. Distribution Channel

- 17.7.10. End-Use

- 17.8. Spain Urinary Incontinence Treatment Devices Market

- 17.8.1. Country Segmental Analysis

- 17.8.2. Device Type

- 17.8.3. Technology

- 17.8.4. Rated Power (for Electrical Stimulation Devices)

- 17.8.5. Rated Capacity (for Collection Devices)

- 17.8.6. Incontinence Type

- 17.8.7. Gender

- 17.8.8. Material Type

- 17.8.9. Distribution Channel

- 17.8.10. End-Use

- 17.9. Netherlands Urinary Incontinence Treatment Devices Market

- 17.9.1. Country Segmental Analysis

- 17.9.2. Device Type

- 17.9.3. Technology

- 17.9.4. Rated Power (for Electrical Stimulation Devices)

- 17.9.5. Rated Capacity (for Collection Devices)

- 17.9.6. Incontinence Type

- 17.9.7. Gender

- 17.9.8. Material Type

- 17.9.9. Distribution Channel

- 17.9.10. End-Use

- 17.10. Nordic Countries Urinary Incontinence Treatment Devices Market

- 17.10.1. Country Segmental Analysis

- 17.10.2. Device Type

- 17.10.3. Technology

- 17.10.4. Rated Power (for Electrical Stimulation Devices)

- 17.10.5. Rated Capacity (for Collection Devices)

- 17.10.6. Incontinence Type

- 17.10.7. Gender

- 17.10.8. Material Type

- 17.10.9. Distribution Channel

- 17.10.10. End-Use

- 17.11. Poland Urinary Incontinence Treatment Devices Market

- 17.11.1. Country Segmental Analysis

- 17.11.2. Device Type

- 17.11.3. Technology

- 17.11.4. Rated Power (for Electrical Stimulation Devices)

- 17.11.5. Rated Capacity (for Collection Devices)

- 17.11.6. Incontinence Type

- 17.11.7. Gender

- 17.11.8. Material Type

- 17.11.9. Distribution Channel

- 17.11.10. End-Use

- 17.12. Russia & CIS Urinary Incontinence Treatment Devices Market

- 17.12.1. Country Segmental Analysis

- 17.12.2. Device Type

- 17.12.3. Technology

- 17.12.4. Rated Power (for Electrical Stimulation Devices)

- 17.12.5. Rated Capacity (for Collection Devices)

- 17.12.6. Incontinence Type

- 17.12.7. Gender

- 17.12.8. Material Type

- 17.12.9. Distribution Channel

- 17.12.10. End-Use

- 17.13. Rest of Europe Urinary Incontinence Treatment Devices Market

- 17.13.1. Country Segmental Analysis

- 17.13.2. Device Type

- 17.13.3. Technology

- 17.13.4. Rated Power (for Electrical Stimulation Devices)

- 17.13.5. Rated Capacity (for Collection Devices)

- 17.13.6. Incontinence Type

- 17.13.7. Gender

- 17.13.8. Material Type

- 17.13.9. Distribution Channel

- 17.13.10. End-Use

- 18. Asia Pacific Urinary Incontinence Treatment Devices Market Analysis

- 18.1. Key Segment Analysis

- 18.2. Regional Snapshot

- 18.3. Asia Pacific Urinary Incontinence Treatment Devices Market Size Volume (Thousand Units) and Value (US$ Bn), Analysis, and Forecasts, 2021-2035

- 18.3.1. Device Type

- 18.3.2. Technology

- 18.3.3. Rated Power (for Electrical Stimulation Devices)

- 18.3.4. Rated Capacity (for Collection Devices)

- 18.3.5. Incontinence Type

- 18.3.6. Gender

- 18.3.7. Material Type

- 18.3.8. Distribution Channel

- 18.3.9. End-Use

- 18.3.10. Country

- 18.3.10.1. China

- 18.3.10.2. India

- 18.3.10.3. Japan

- 18.3.10.4. South Korea

- 18.3.10.5. Australia and New Zealand

- 18.3.10.6. Indonesia

- 18.3.10.7. Malaysia

- 18.3.10.8. Thailand

- 18.3.10.9. Vietnam

- 18.3.10.10. Rest of Asia Pacific

- 18.4. China Urinary Incontinence Treatment Devices Market

- 18.4.1. Country Segmental Analysis

- 18.4.2. Device Type

- 18.4.3. Technology

- 18.4.4. Rated Power (for Electrical Stimulation Devices)

- 18.4.5. Rated Capacity (for Collection Devices)

- 18.4.6. Incontinence Type

- 18.4.7. Gender

- 18.4.8. Material Type

- 18.4.9. Distribution Channel

- 18.4.10. End-Use

- 18.5. India Urinary Incontinence Treatment Devices Market

- 18.5.1. Country Segmental Analysis

- 18.5.2. Device Type

- 18.5.3. Technology

- 18.5.4. Rated Power (for Electrical Stimulation Devices)

- 18.5.5. Rated Capacity (for Collection Devices)

- 18.5.6. Incontinence Type

- 18.5.7. Gender

- 18.5.8. Material Type

- 18.5.9. Distribution Channel

- 18.5.10. End-Use

- 18.6. Japan Urinary Incontinence Treatment Devices Market

- 18.6.1. Country Segmental Analysis

- 18.6.2. Device Type

- 18.6.3. Technology

- 18.6.4. Rated Power (for Electrical Stimulation Devices)

- 18.6.5. Rated Capacity (for Collection Devices)

- 18.6.6. Incontinence Type

- 18.6.7. Gender

- 18.6.8. Material Type

- 18.6.9. Distribution Channel

- 18.6.10. End-Use

- 18.7. South Korea Urinary Incontinence Treatment Devices Market

- 18.7.1. Country Segmental Analysis

- 18.7.2. Device Type

- 18.7.3. Technology

- 18.7.4. Rated Power (for Electrical Stimulation Devices)

- 18.7.5. Rated Capacity (for Collection Devices)

- 18.7.6. Incontinence Type

- 18.7.7. Gender

- 18.7.8. Material Type

- 18.7.9. Distribution Channel

- 18.7.10. End-Use

- 18.8. Australia and New Zealand Urinary Incontinence Treatment Devices Market

- 18.8.1. Country Segmental Analysis

- 18.8.2. Device Type

- 18.8.3. Technology

- 18.8.4. Rated Power (for Electrical Stimulation Devices)

- 18.8.5. Rated Capacity (for Collection Devices)

- 18.8.6. Incontinence Type

- 18.8.7. Gender

- 18.8.8. Material Type

- 18.8.9. Distribution Channel

- 18.8.10. End-Use

- 18.9. Indonesia Urinary Incontinence Treatment Devices Market

- 18.9.1. Country Segmental Analysis

- 18.9.2. Device Type

- 18.9.3. Technology

- 18.9.4. Rated Power (for Electrical Stimulation Devices)

- 18.9.5. Rated Capacity (for Collection Devices)

- 18.9.6. Incontinence Type

- 18.9.7. Gender

- 18.9.8. Material Type

- 18.9.9. Distribution Channel

- 18.9.10. End-Use

- 18.10. Malaysia Urinary Incontinence Treatment Devices Market

- 18.10.1. Country Segmental Analysis

- 18.10.2. Device Type

- 18.10.3. Technology

- 18.10.4. Rated Power (for Electrical Stimulation Devices)

- 18.10.5. Rated Capacity (for Collection Devices)

- 18.10.6. Incontinence Type

- 18.10.7. Gender

- 18.10.8. Material Type

- 18.10.9. Distribution Channel

- 18.10.10. End-Use

- 18.11. Thailand Urinary Incontinence Treatment Devices Market

- 18.11.1. Country Segmental Analysis

- 18.11.2. Device Type

- 18.11.3. Technology

- 18.11.4. Rated Power (for Electrical Stimulation Devices)

- 18.11.5. Rated Capacity (for Collection Devices)

- 18.11.6. Incontinence Type

- 18.11.7. Gender

- 18.11.8. Material Type

- 18.11.9. Distribution Channel

- 18.11.10. End-Use

- 18.12. Vietnam Urinary Incontinence Treatment Devices Market

- 18.12.1. Country Segmental Analysis

- 18.12.2. Device Type

- 18.12.3. Technology

- 18.12.4. Rated Power (for Electrical Stimulation Devices)

- 18.12.5. Rated Capacity (for Collection Devices)

- 18.12.6. Incontinence Type

- 18.12.7. Gender

- 18.12.8. Material Type

- 18.12.9. Distribution Channel

- 18.12.10. End-Use

- 18.13. Rest of Asia Pacific Urinary Incontinence Treatment Devices Market

- 18.13.1. Country Segmental Analysis

- 18.13.2. Device Type

- 18.13.3. Technology

- 18.13.4. Rated Power (for Electrical Stimulation Devices)

- 18.13.5. Rated Capacity (for Collection Devices)

- 18.13.6. Incontinence Type

- 18.13.7. Gender

- 18.13.8. Material Type

- 18.13.9. Distribution Channel

- 18.13.10. End-Use

- 19. Middle East Urinary Incontinence Treatment Devices Market Analysis

- 19.1. Key Segment Analysis

- 19.2. Regional Snapshot

- 19.3. Middle East Urinary Incontinence Treatment Devices Market Size Volume (Thousand Units) and Value (US$ Bn), Analysis, and Forecasts, 2021-2035

- 19.3.1. Device Type

- 19.3.2. Technology

- 19.3.3. Rated Power (for Electrical Stimulation Devices)

- 19.3.4. Rated Capacity (for Collection Devices)

- 19.3.5. Incontinence Type

- 19.3.6. Gender

- 19.3.7. Material Type

- 19.3.8. Distribution Channel

- 19.3.9. End-Use

- 19.3.10. Country

- 19.3.10.1. Turkey

- 19.3.10.2. UAE

- 19.3.10.3. Saudi Arabia

- 19.3.10.4. Israel

- 19.3.10.5. Rest of Middle East

- 19.4. Turkey Urinary Incontinence Treatment Devices Market

- 19.4.1. Country Segmental Analysis

- 19.4.2. Device Type

- 19.4.3. Technology

- 19.4.4. Rated Power (for Electrical Stimulation Devices)

- 19.4.5. Rated Capacity (for Collection Devices)

- 19.4.6. Incontinence Type

- 19.4.7. Gender

- 19.4.8. Material Type

- 19.4.9. Distribution Channel

- 19.4.10. End-Use

- 19.5. UAE Urinary Incontinence Treatment Devices Market

- 19.5.1. Country Segmental Analysis

- 19.5.2. Device Type

- 19.5.3. Technology

- 19.5.4. Rated Power (for Electrical Stimulation Devices)

- 19.5.5. Rated Capacity (for Collection Devices)

- 19.5.6. Incontinence Type

- 19.5.7. Gender

- 19.5.8. Material Type

- 19.5.9. Distribution Channel

- 19.5.10. End-Use

- 19.6. Saudi Arabia Urinary Incontinence Treatment Devices Market

- 19.6.1. Country Segmental Analysis

- 19.6.2. Device Type

- 19.6.3. Technology

- 19.6.4. Rated Power (for Electrical Stimulation Devices)

- 19.6.5. Rated Capacity (for Collection Devices)

- 19.6.6. Incontinence Type

- 19.6.7. Gender

- 19.6.8. Material Type

- 19.6.9. Distribution Channel

- 19.6.10. End-Use

- 19.7. Israel Urinary Incontinence Treatment Devices Market

- 19.7.1. Country Segmental Analysis

- 19.7.2. Device Type

- 19.7.3. Technology

- 19.7.4. Rated Power (for Electrical Stimulation Devices)

- 19.7.5. Rated Capacity (for Collection Devices)

- 19.7.6. Incontinence Type

- 19.7.7. Gender

- 19.7.8. Material Type

- 19.7.9. Distribution Channel

- 19.7.10. End-Use

- 19.8. Rest of Middle East Urinary Incontinence Treatment Devices Market

- 19.8.1. Country Segmental Analysis

- 19.8.2. Device Type

- 19.8.3. Technology

- 19.8.4. Rated Power (for Electrical Stimulation Devices)

- 19.8.5. Rated Capacity (for Collection Devices)

- 19.8.6. Incontinence Type

- 19.8.7. Gender

- 19.8.8. Material Type

- 19.8.9. Distribution Channel

- 19.8.10. End-Use

- 20. Africa Urinary Incontinence Treatment Devices Market Analysis

- 20.1. Key Segment Analysis

- 20.2. Regional Snapshot

- 20.3. Africa Urinary Incontinence Treatment Devices Market Size Volume (Thousand Units) and Value (US$ Bn), Analysis, and Forecasts, 2021-2035

- 20.3.1. Device Type

- 20.3.2. Technology

- 20.3.3. Rated Power (for Electrical Stimulation Devices)

- 20.3.4. Rated Capacity (for Collection Devices)

- 20.3.5. Incontinence Type

- 20.3.6. Gender

- 20.3.7. Material Type

- 20.3.8. Distribution Channel

- 20.3.9. End-Use

- 20.3.10. Country

- 20.3.10.1. South Africa

- 20.3.10.2. Egypt

- 20.3.10.3. Nigeria

- 20.3.10.4. Algeria

- 20.3.10.5. Rest of Africa

- 20.4. South Africa Urinary Incontinence Treatment Devices Market

- 20.4.1. Country Segmental Analysis

- 20.4.2. Device Type

- 20.4.3. Technology

- 20.4.4. Rated Power (for Electrical Stimulation Devices)

- 20.4.5. Rated Capacity (for Collection Devices)

- 20.4.6. Incontinence Type

- 20.4.7. Gender

- 20.4.8. Material Type

- 20.4.9. Distribution Channel

- 20.4.10. End-Use

- 20.5. Egypt Urinary Incontinence Treatment Devices Market

- 20.5.1. Country Segmental Analysis

- 20.5.2. Device Type

- 20.5.3. Technology

- 20.5.4. Rated Power (for Electrical Stimulation Devices)

- 20.5.5. Rated Capacity (for Collection Devices)

- 20.5.6. Incontinence Type

- 20.5.7. Gender

- 20.5.8. Material Type

- 20.5.9. Distribution Channel

- 20.5.10. End-Use

- 20.6. Nigeria Urinary Incontinence Treatment Devices Market

- 20.6.1. Country Segmental Analysis

- 20.6.2. Device Type

- 20.6.3. Technology

- 20.6.4. Rated Power (for Electrical Stimulation Devices)

- 20.6.5. Rated Capacity (for Collection Devices)

- 20.6.6. Incontinence Type

- 20.6.7. Gender

- 20.6.8. Material Type

- 20.6.9. Distribution Channel

- 20.6.10. End-Use

- 20.7. Algeria Urinary Incontinence Treatment Devices Market

- 20.7.1. Country Segmental Analysis

- 20.7.2. Device Type

- 20.7.3. Technology

- 20.7.4. Rated Power (for Electrical Stimulation Devices)

- 20.7.5. Rated Capacity (for Collection Devices)

- 20.7.6. Incontinence Type

- 20.7.7. Gender

- 20.7.8. Material Type

- 20.7.9. Distribution Channel

- 20.7.10. End-Use

- 20.8. Rest of Africa Urinary Incontinence Treatment Devices Market

- 20.8.1. Country Segmental Analysis

- 20.8.2. Device Type

- 20.8.3. Technology

- 20.8.4. Rated Power (for Electrical Stimulation Devices)

- 20.8.5. Rated Capacity (for Collection Devices)

- 20.8.6. Incontinence Type

- 20.8.7. Gender

- 20.8.8. Material Type

- 20.8.9. Distribution Channel

- 20.8.10. End-Use

- 21. South America Urinary Incontinence Treatment Devices Market Analysis

- 21.1. Key Segment Analysis

- 21.2. Regional Snapshot

- 21.3. South America Urinary Incontinence Treatment Devices Market Size Volume (Thousand Units) and Value (US$ Bn), Analysis, and Forecasts, 2021-2035

- 21.3.1. Device Type

- 21.3.2. Technology

- 21.3.3. Rated Power (for Electrical Stimulation Devices)

- 21.3.4. Rated Capacity (for Collection Devices)

- 21.3.5. Incontinence Type

- 21.3.6. Gender

- 21.3.7. Material Type

- 21.3.8. Distribution Channel

- 21.3.9. End-Use

- 21.3.10. Country

- 21.3.10.1. Brazil

- 21.3.10.2. Argentina

- 21.3.10.3. Rest of South America

- 21.4. Brazil Urinary Incontinence Treatment Devices Market

- 21.4.1. Country Segmental Analysis

- 21.4.2. Device Type

- 21.4.3. Technology

- 21.4.4. Rated Power (for Electrical Stimulation Devices)

- 21.4.5. Rated Capacity (for Collection Devices)

- 21.4.6. Incontinence Type

- 21.4.7. Gender

- 21.4.8. Material Type

- 21.4.9. Distribution Channel

- 21.4.10. End-Use

- 21.5. Argentina Urinary Incontinence Treatment Devices Market

- 21.5.1. Country Segmental Analysis

- 21.5.2. Device Type

- 21.5.3. Technology

- 21.5.4. Rated Power (for Electrical Stimulation Devices)

- 21.5.5. Rated Capacity (for Collection Devices)

- 21.5.6. Incontinence Type

- 21.5.7. Gender

- 21.5.8. Material Type

- 21.5.9. Distribution Channel

- 21.5.10. End-Use

- 21.6. Rest of South America Urinary Incontinence Treatment Devices Market

- 21.6.1. Country Segmental Analysis

- 21.6.2. Device Type

- 21.6.3. Technology

- 21.6.4. Rated Power (for Electrical Stimulation Devices)

- 21.6.5. Rated Capacity (for Collection Devices)

- 21.6.6. Incontinence Type

- 21.6.7. Gender

- 21.6.8. Material Type

- 21.6.9. Distribution Channel

- 21.6.10. End-Use

- 22. Key Players/ Company Profile

- 22.1. Boston Scientific Corporation

- 22.1.1. Company Details/ Overview

- 22.1.2. Company Financials

- 22.1.3. Key Customers and Competitors

- 22.1.4. Business/ Industry Portfolio

- 22.1.5. Product Portfolio/ Specification Details

- 22.1.6. Pricing Data

- 22.1.7. Strategic Overview

- 22.1.8. Recent Developments

- 22.2. Medtronic plc

- 22.3. Johnson & Johnson

- 22.4. Coloplast Group

- 22.5. C.R. Bard (BD)

- 22.6. Promedon Group

- 22.7. Cogentix Medical

- 22.8. American Medical Systems

- 22.9. Teleflex Incorporated

- 22.10. Cook Medical

- 22.11. Hollister Incorporated

- 22.12. ConvaTec Group plc

- 22.13. Wellspect HealthCare

- 22.14. B. Braun Melsungen AG

- 22.15. Axonics Modulation Technologies

- 22.16. Caldera Medical

- 22.17. Liberator Medical Supply

- 22.18. InControl Medical

- 22.19. Laborie Medical Technologies

- 22.20. Gedeon Richter Plc.

- 22.21. Other Key Players

- 22.1. Boston Scientific Corporation

Note* - This is just tentative list of players. While providing the report, we will cover more number of players based on their revenue and share for each geography

Research Design

Our research design integrates both demand-side and supply-side analysis through a balanced combination of primary and secondary research methodologies. By utilizing both bottom-up and top-down approaches alongside rigorous data triangulation methods, we deliver robust market intelligence that supports strategic decision-making.

MarketGenics' comprehensive research design framework ensures the delivery of accurate, reliable, and actionable market intelligence. Through the integration of multiple research approaches, rigorous validation processes, and expert analysis, we provide our clients with the insights needed to make informed strategic decisions and capitalize on market opportunities.

MarketGenics leverages a dedicated industry panel of experts and a comprehensive suite of paid databases to effectively collect, consolidate, and analyze market intelligence.

Our approach has consistently proven to be reliable and effective in generating accurate market insights, identifying key industry trends, and uncovering emerging business opportunities.

Through both primary and secondary research, we capture and analyze critical company-level data such as manufacturing footprints, including technical centers, R&D facilities, sales offices, and headquarters.

Our expert panel further enhances our ability to estimate market size for specific brands based on validated field-level intelligence.

Our data mining techniques incorporate both parametric and non-parametric methods, allowing for structured data collection, sorting, processing, and cleaning.

Demand projections are derived from large-scale data sets analyzed through proprietary algorithms, culminating in robust and reliable market sizing.

Research Approach

The bottom-up approach builds market estimates by starting with the smallest addressable market units and systematically aggregating them to create comprehensive market size projections.

This method begins with specific, granular data points and builds upward to create the complete market landscape.

Customer Analysis → Segmental Analysis → Geographical Analysis

The top-down approach starts with the broadest possible market data and systematically narrows it down through a series of filters and assumptions to arrive at specific market segments or opportunities.

This method begins with the big picture and works downward to increasingly specific market slices.

TAM → SAM → SOM

Research Methods

Desk / Secondary Research

While analysing the market, we extensively study secondary sources, directories, and databases to identify and collect information useful for this technical, market-oriented, and commercial report. Secondary sources that we utilize are not only the public sources, but it is a combination of Open Source, Associations, Paid Databases, MG Repository & Knowledgebase, and others.

- Company websites, annual reports, financial reports, broker reports, and investor presentations

- National government documents, statistical databases and reports

- News articles, press releases and web-casts specific to the companies operating in the market, Magazines, reports, and others

- We gather information from commercial data sources for deriving company specific data such as segmental revenue, share for geography, product revenue, and others

- Internal and external proprietary databases (industry-specific), relevant patent, and regulatory databases

- Governing Bodies, Government Organizations

- Relevant Authorities, Country-specific Associations for Industries

We also employ the model mapping approach to estimate the product level market data through the players' product portfolio

Primary Research

Primary research/ interviews is vital in analyzing the market. Most of the cases involves paid primary interviews. Primary sources include primary interviews through e-mail interactions, telephonic interviews, surveys as well as face-to-face interviews with the different stakeholders across the value chain including several industry experts.

| Type of Respondents | Number of Primaries |

|---|---|

| Tier 2/3 Suppliers | ~20 |

| Tier 1 Suppliers | ~25 |

| End-users | ~25 |

| Industry Expert/ Panel/ Consultant | ~30 |

| Total | ~100 |

MG Knowledgebase

• Repository of industry blog, newsletter and case studies

• Online platform covering detailed market reports, and company profiles

Forecasting Factors and Models

Forecasting Factors

- Historical Trends – Past market patterns, cycles, and major events that shaped how markets behave over time. Understanding past trends helps predict future behavior.

- Industry Factors – Specific characteristics of the industry like structure, regulations, and innovation cycles that affect market dynamics.

- Macroeconomic Factors – Economic conditions like GDP growth, inflation, and employment rates that affect how much money people have to spend.

- Demographic Factors – Population characteristics like age, income, and location that determine who can buy your product.

- Technology Factors – How quickly people adopt new technology and how much technology infrastructure exists.

- Regulatory Factors – Government rules, laws, and policies that can help or restrict market growth.

- Competitive Factors – Analyzing competition structure such as degree of competition and bargaining power of buyers and suppliers.

Forecasting Models / Techniques

Multiple Regression Analysis

- Identify and quantify factors that drive market changes

- Statistical modeling to establish relationships between market drivers and outcomes

Time Series Analysis – Seasonal Patterns

- Understand regular cyclical patterns in market demand

- Advanced statistical techniques to separate trend, seasonal, and irregular components

Time Series Analysis – Trend Analysis

- Identify underlying market growth patterns and momentum

- Statistical analysis of historical data to project future trends

Expert Opinion – Expert Interviews

- Gather deep industry insights and contextual understanding

- In-depth interviews with key industry stakeholders

Multi-Scenario Development

- Prepare for uncertainty by modeling different possible futures

- Creating optimistic, pessimistic, and most likely scenarios

Time Series Analysis – Moving Averages

- Sophisticated forecasting for complex time series data

- Auto-regressive integrated moving average models with seasonal components

Econometric Models

- Apply economic theory to market forecasting

- Sophisticated economic models that account for market interactions

Expert Opinion – Delphi Method

- Harness collective wisdom of industry experts

- Structured, multi-round expert consultation process

Monte Carlo Simulation

- Quantify uncertainty and probability distributions

- Thousands of simulations with varying input parameters

Research Analysis

Our research framework is built upon the fundamental principle of validating market intelligence from both demand and supply perspectives. This dual-sided approach ensures comprehensive market understanding and reduces the risk of single-source bias.

Demand-Side Analysis: We understand end-user/application behavior, preferences, and market needs along with the penetration of the product for specific application.

Supply-Side Analysis: We estimate overall market revenue, analyze the segmental share along with industry capacity, competitive landscape, and market structure.

Validation & Evaluation

Data triangulation is a validation technique that uses multiple methods, sources, or perspectives to examine the same research question, thereby increasing the credibility and reliability of research findings. In market research, triangulation serves as a quality assurance mechanism that helps identify and minimize bias, validate assumptions, and ensure accuracy in market estimates.

- Data Source Triangulation – Using multiple data sources to examine the same phenomenon

- Methodological Triangulation – Using multiple research methods to study the same research question

- Investigator Triangulation – Using multiple researchers or analysts to examine the same data

- Theoretical Triangulation – Using multiple theoretical perspectives to interpret the same data

Custom Market Research Services

We will customise the research for you, in case the report listed above does not meet your requirements.

Get 10% Free Customisation