Quantum Photonics Market Size, Share & Trends Analysis Report by Component (Quantum Light Sources, Quantum Detectors, Quantum Processors, Optical Components), Technology, Material Platform, Integration Level, Wavelength Range, Power Consumption, System Configuration, End-use Industry, and Geography (North America, Europe, Asia Pacific, Middle East, Africa, and South America) – Global Industry Data, Trends, and Forecasts, 2026 – 2035

|

Market Structure & Evolution |

|

|

Segmental Data Insights |

|

|

Demand Trends |

|

|

Competitive Landscape |

|

|

Strategic Development |

|

|

Future Outlook & Opportunities |

|

Quantum-Photonics-Market Size, Share, and Growth

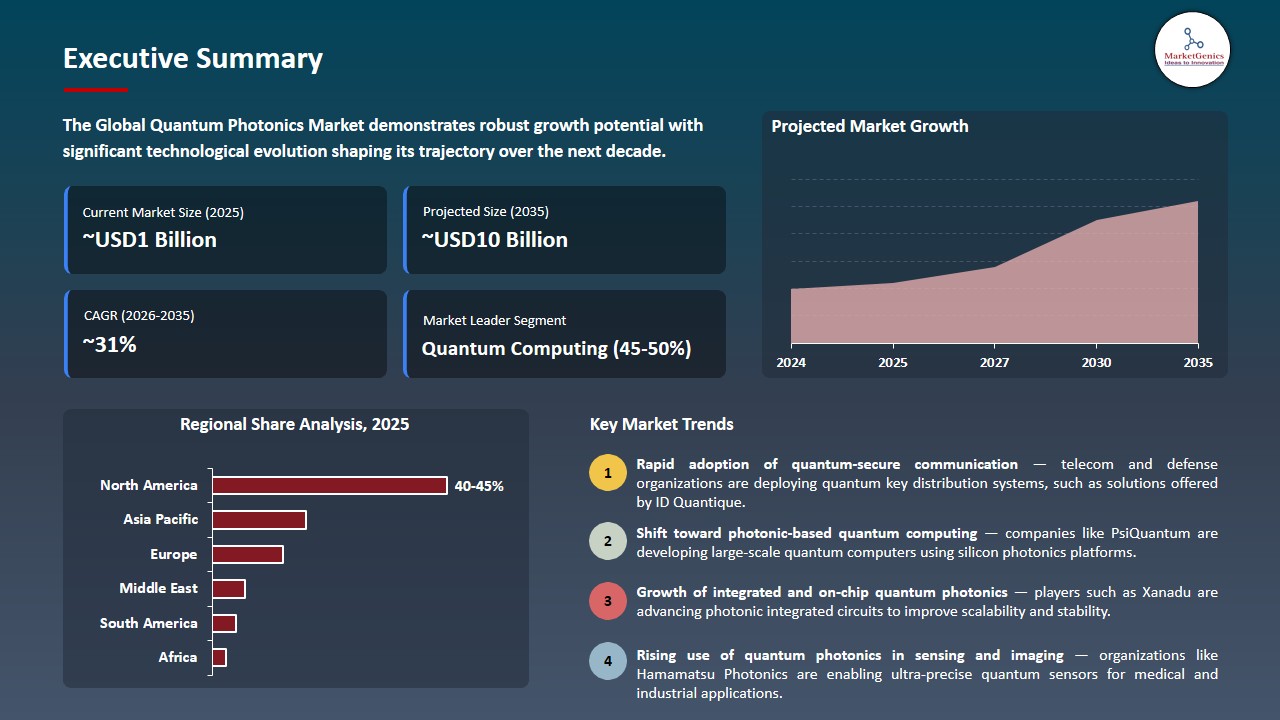

The global quantum photonics market is experiencing robust growth, with its estimated value of USD 0.7 billion in the year 2025 and USD 10.1 billion by the period 2035, registering a CAGR of 30.6% during the forecast period.

“The delivery of Lucy is not just a new milestone – it is a key building block for Europe’s hybrid computing future. In collaboration with attocube systems, we built a photonic quantum processor that will interface with the Joliot-Curie supercomputer, enabling real hybrid HPC-quantum workflows. By providing this capability to a broad community of European researchers and industrial users, we are empowering them to explore new frontiers in simulation, optimization, and machine learning. This achievement strengthens Europe’s technological sovereignty and demonstrates the power of cross-border collaboration to shape the next generation of computing — Niccolo Somaschi, Co-founder & CEO, Quandela”

The quantum photonics market, driven by the quick development of integrated photonic chip design, government-funded quantum communication initiatives, favorable regulatory ecology, and commercialization endeavors undertaken by major manufacturers in an effort to improve quantum computing and communication scalability.

For instance, in March 2024, PsiQuantum raised more capital over USD 600 million to scale-up its photonic quantum chip manufacturing in partnership with GlobalFoundries, to build a fault-tolerable quantum computer based on silicon photonics. Similarly, in June 2024, ID Quantique has achieved implementation of a large-scale Quantum Key Distribution (QKD) network in South Korea in cooperation with SK Telecom, to improve cybersecurity infrastructure with photonic-based encryption.

In addition, in February 2025, Xanadu announced its plans to develop a higher-qubit-lower-error photonic quantum computer, dubbed Borealis 2, as the advancement of industrial operations in the area of optical-based quantum systems. Also, favorable regulatory frameworks like the European Commission’s Quantum Flagship program and the U.S. National Quantum Initiative Act have expedited populace cooperation, guaranteeing conformity as well as security levels, and funding channels to commercial-size quantum photonics infrastructure.

Adjacent opportunities to the global quantum photonics market include quantum communication networks, photonic quantum computing hardware, quantum sensing and imaging, quantum-safe cryptography, and photonic integrated circuit manufacturing. These adjacent markets collectively expand commercialization avenues, amplifying quantum photonics’ economic and technological influence globally.

Quantum Photonics Market Dynamics and Trends

Driver: Rapid Commercial Expansion Supported by Large-Scale Government and Industry Investments

-

The global quantum photonics market is experiencing a strong momentum as a result of strategic investments and the government-business collaboration aimed at speeding up the commercialization of quantum communication and computing systems. Governments have been playing a great role by setting up programs like the U.S. CHIPS and Science Act of 2024 that provided more than USD 1.8 billion to develop quantum technologies, including photonic-based systems.

- In parallel, manufacturers are also scaling, manufacturers are scaling operations PsiQuantum in September 2025 USD 1 billion to scale silicon-photonic quantum chip production with GlobalFoundries with higher yields of fault-tolerant quantum computing. Similarly, Toshiba Digital Solutions declared the release of further developed quantum key distribution (QKD) systems in July 2025 to be implemented in Japanese telecommunication systems with national digital security initiatives.

- There will be coordinated industry and government activities that will result in a powerful ecosystem of innovations and supply, driving the growth of the quantum photonics market globally.

Restraint: High Production Costs and Limited Scalable Manufacturing Infrastructure

-

The high cost and complexity of photonic quantum hardware manufacturing is a critical constraint because the global quantum photonics market is highly constrained. Creation of single-photon sources, low loss waveguides, and superconducting detectors require nanometer accuracy and clean room facilities, making them cost-ineffective and time-consuming to make.

- Industry data from 2025 shows that the yield rate for integrated photonic chips remains below 40% in pilot-scale quantum foundries, resulting in elevated component prices and inconsistent performance. Reports from the UK’s National Quantum Technologies Programme further revealed that production of quantum-grade photonic components faces bottlenecks in cryogenic systems and single-photon detection hardware due to supplier limitations.

- In August 2024, Aegiq Ltd. confirmed delays in commercial rollout of its quantum photonic modules citing supplier constraints and limited industrial-grade packaging facilities. The absence of scalable, high-yield photonic manufacturing facilities prolongs commercialization timelines and restricts global deployment.

Opportunity: Integration of Photonic Processors in Artificial Intelligence Data Centers

-

The convergence of the workloads of photonic processing and AI offers a significant chance to the quantum photonics ecosystem. The increased need in AI data centers due to computational power has led to the study of photonic accelerators that can perform high-speed and low-power matrix computations. In March 2025, Lightmatter launched its Passage M1000 photonic interconnect platform which portrayed a ten-fold decrease in the energy usage of the data movement to train AI models.

- Similarly, in May 2025 Ayar Labs collaborated with NVIDIA to implement optical I/O technology into the cluster of GPUs to improve bandwidth utilization to conduct large-scale neural network computations. These technological breakthroughs show photonic integration as a direct aid to energy efficient data processing as well as taking advantage of current quantum photonics manufacturing infrastructure.

- The cross-domain potential of quantum photonics and AI computing is creating a support of diversified sources of income in the field of semiconductor and optical networking segment

Key Trend: Growing Regulatory and Standardization Initiatives in Quantum Communication Security

-

Global standards and regulations are becoming one of the trends that are defining the quantum photonics industry especially in the communication and cryptographic fields. In April 2025, the program of the European Union extended the Quantum Flagship Program with the EuroQCI (quantum Communication Infrastructure) regulation establishing standards of cross-border quantum network interoperability.

- In parallel, the U.S. the National Institute of Standards and Technology (NIST) completed its post-quantum cryptography standards in 2024, also having an impact on the uptake of photonic-based secure communication systems by the private sector. Concurrently, the Ministry of Industry and Information Technology (MIIT) of China declared that it had over 4,000 km of quantum communication backbone built by photonic quantum Kelly diode (QKD) technology to protect national data infrastructure.

- Expanding regulatory alignment and standards development are reinforcing global confidence in photonic-based quantum communication systems, accelerating infrastructure-level adoption.

Quantum-Photonics-Market Analysis and Segmental Data

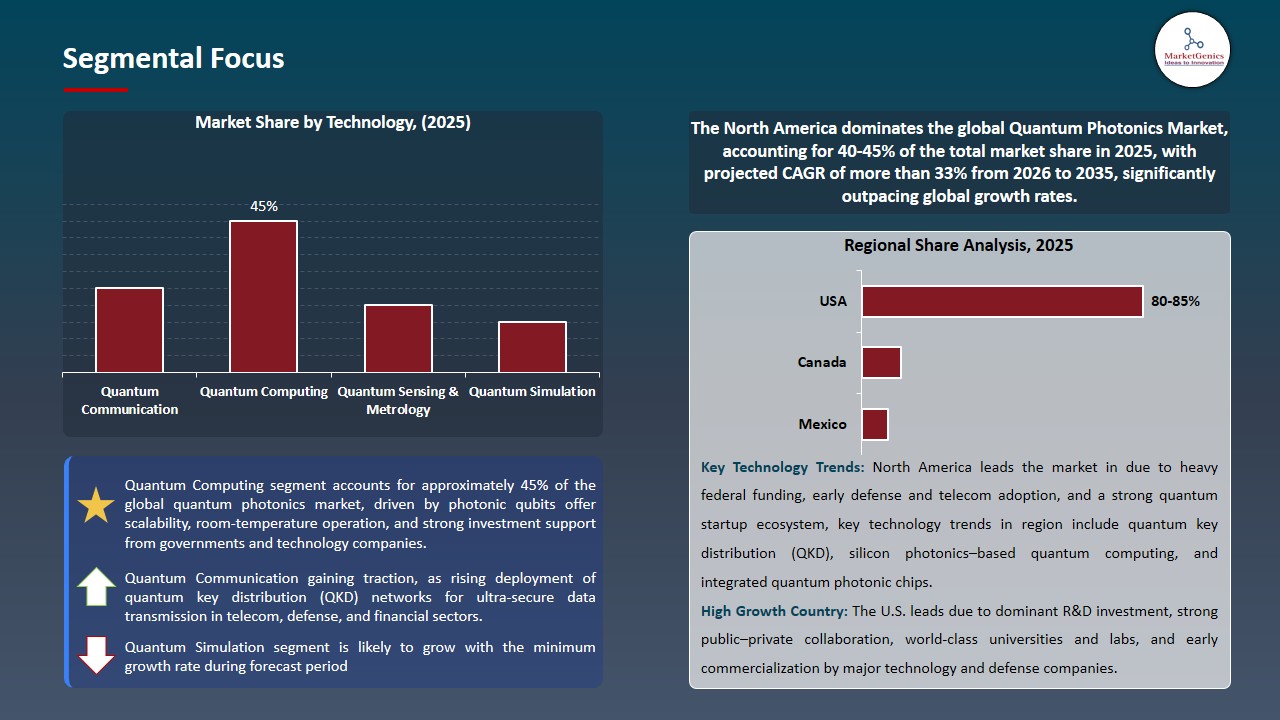

Rising Quantum Integration Across Advanced Technology Infrastructures

-

Demand for quantum computing within the technology segment is highest due to rapid integration of photonic quantum architectures into cloud infrastructure, AI acceleration, and semiconductor fabrication ecosystems. In May 2025, IBM launched its photonic-enhanced “Quantum System Two,” designed for hybrid cloud deployment, enabling faster quantum–classical data exchange.

- Similarly, Google announced the improvements to its quantum data centers through photonic interconnects to improve their computational coherence and energy consumption, which places photonic computing at the center of the next-generation digital technologies.

- The growing use of photonic quantum computing in more complex technology platforms is strengthening the political power of the segment, which is bringing massive digital and industrial change to globally.

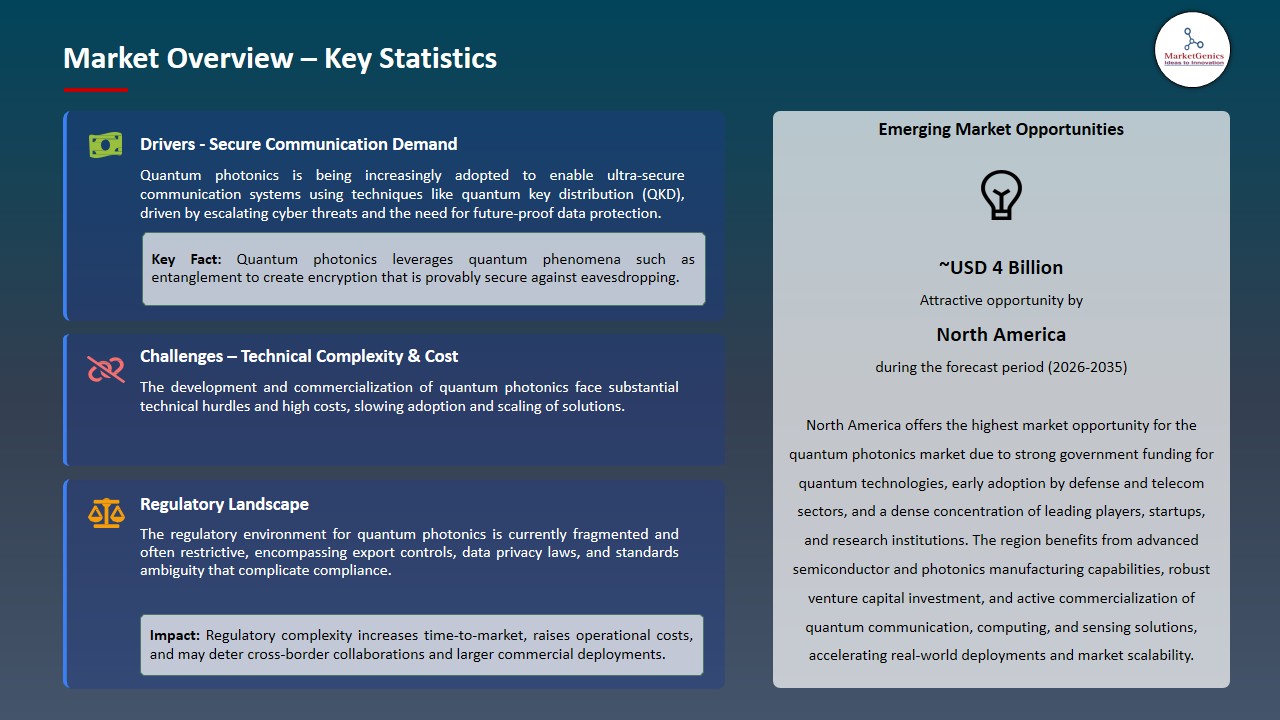

North America Leading Quantum Photonics Adoption through Strategic Innovation and Infrastructure

-

North America leads the global quantum photonics market due to its strong ecosystem of research institutions, defense programs, and technology enterprises accelerating photonic quantum innovation. In March 2025, the U.S. Department of energy awarded an excess of USD 625 million to renew its five National Quantum Information Science (QIS) Research Centers (NQISRCs) over a maximum of five years, by increasing R&D at all centers and by implementing quantum technology to the most urgent scientific and national security issues of the DOE.

- Major firms like Xanadu and Lightmatter have entered into mass production of photonic processors in Canada and North America respectively, respectively, leading to the initial commercialization in computing and communication uses. The region benefits from proactive coordination of national labs, universities, and technological giants that provide a quick transition of prototype to product.

- Furthermore, in May 2025, Amazon Web Services announced its Quantum Photonic Research Center in California to advance cloud-based optical quantum computing infrastructure. Similarly, the National Science Foundation initiated new photonic quantum research centers at universities in the United States of America, which encouraged the development of the workforce and the standardization of hardware.

- Advancing quantum photonic innovation and implementation North America is becoming the global center of quantum photonic funding and research partnerships.

Quantum-Photonics-Market Ecosystem

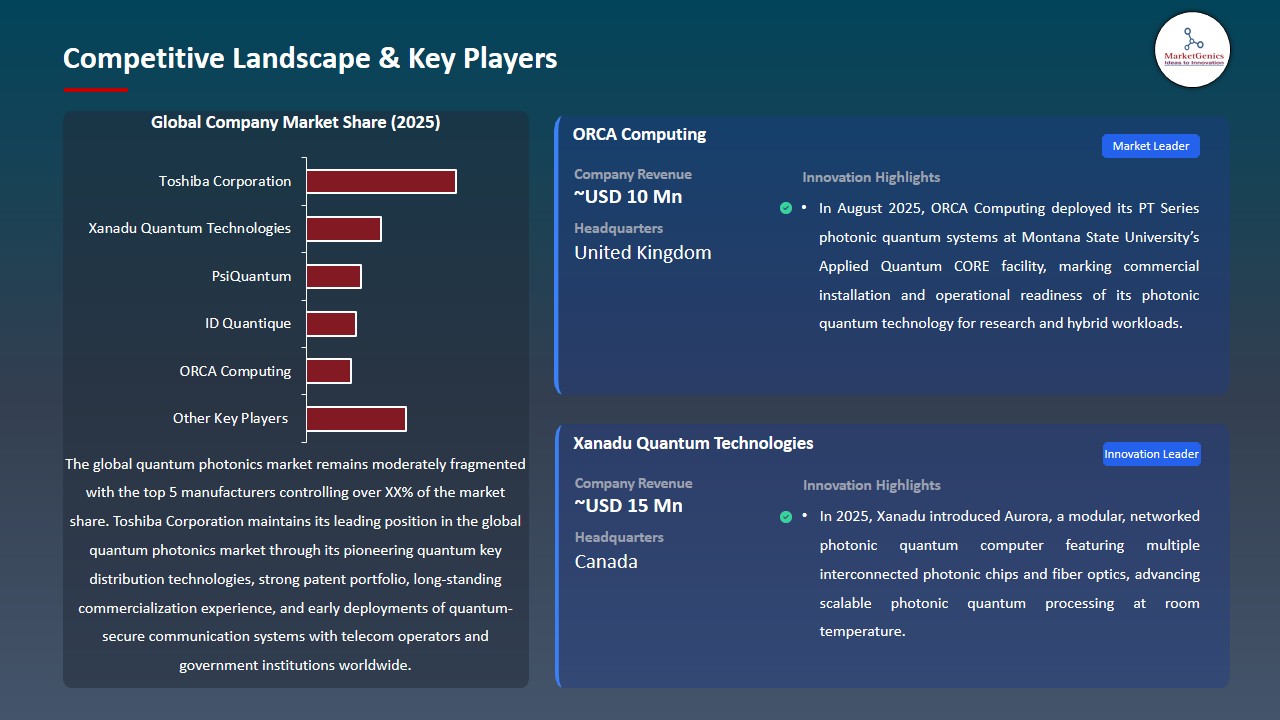

The global quantum photonics Market is moderately consolidated, with Tier 1 players such as PsiQuantum, Xanadu Quantum Technologies, and Toshiba Corporation leading large-scale system development and commercial deployments. Tier 2 companies, including ORCA Computing, Photonic Inc., and ID Quantique, focus on specialized photonic hardware and hybrid integration, while Tier 3 firms such as NuCrypt and Single Quantum address component-level innovations. Buyer concentration remains medium due to limited end-user segments, whereas supplier concentration is high given the scarce availability of advanced photonic fabrication and quantum-grade materials.

Recent Development and Strategic Overview:

-

In November 2025, Quantum Pulse Ventures announced a universal directional coupler for photonic quantum computers (PQC), providing up to $900M savings on each computer, reducing the cost to build PQCs by an order of magnitude and advancing the availability of practical quantum computers by years.

- In November 2024, IonQ partnered with NKT Photonics, to procure next-generation laser systems for IonQ’s trapped-ion quantum computers and networking equipment. The partnership involves NKT Photonics developing and delivering three prototype optical subsystems to IonQ in 2025, designed to support the commercialization of IonQ’s data center-ready quantum computers – such as IonQ Tempo and future barium-based systems.

Report Scope

|

Attribute |

Detail |

|

Market Size in 2025 |

USD 0.7 Bn |

|

Market Forecast Value in 2035 |

USD 10.1 Bn |

|

Growth Rate (CAGR) |

30.6% |

|

Forecast Period |

2026 – 2035 |

|

Historical Data Available for |

2021 – 2024 |

|

Market Size Units |

US$ Billion for Value |

|

Report Format |

Electronic (PDF) + Excel |

|

Regions and Countries Covered |

|||||

|

North America |

Europe |

Asia Pacific |

Middle East |

Africa |

South America |

|

|

|

|

|

|

|

Companies Covered |

|||||

|

|

|

|

|

|

Quantum-Photonics-Market Segmentation and Highlights

|

Segment |

Sub-segment |

|

Quantum Photonics Market, By Component |

|

|

Quantum Photonics Market, By Technology |

|

|

Quantum Photonics Market, By Material Platform |

|

|

Quantum Photonics Market, By Integration Level |

|

|

Quantum Photonics Market, By Wavelength Range |

|

|

Quantum Photonics Market, By Power Consumption |

|

|

Quantum Photonics Market, By System Configuration |

|

|

Quantum Photonics Market, By End-use Industry |

|

Frequently Asked Questions

Table of Contents

- 1. Research Methodology and Assumptions

- 1.1. Definitions

- 1.2. Research Design and Approach

- 1.3. Data Collection Methods

- 1.4. Base Estimates and Calculations

- 1.5. Forecasting Models

- 1.5.1. Key Forecast Factors & Impact Analysis

- 1.6. Secondary Research

- 1.6.1. Open Sources

- 1.6.2. Paid Databases

- 1.6.3. Associations

- 1.7. Primary Research

- 1.7.1. Primary Sources

- 1.7.2. Primary Interviews with Stakeholders across Ecosystem

- 2. Executive Summary

- 2.1. Global Quantum Photonics Market Outlook

- 2.1.1. Quantum Photonics Market Size (Value – US$ Bn), and Forecasts, 2021-2035

- 2.1.2. Compounded Annual Growth Rate Analysis

- 2.1.3. Growth Opportunity Analysis

- 2.1.4. Segmental Share Analysis

- 2.1.5. Geographical Share Analysis

- 2.2. Market Analysis and Facts

- 2.3. Supply-Demand Analysis

- 2.4. Competitive Benchmarking

- 2.5. Go-to- Market Strategy

- 2.5.1. Customer/ End-use Industry Assessment

- 2.5.2. Growth Opportunity Data, 2025-2035

- 2.5.2.1. Regional Data

- 2.5.2.2. Country Data

- 2.5.2.3. Segmental Data

- 2.5.3. Identification of Potential Market Spaces

- 2.5.4. GAP Analysis

- 2.5.5. Potential Attractive Price Points

- 2.5.6. Prevailing Market Risks & Challenges

- 2.5.7. Preferred Sales & Marketing Strategies

- 2.5.8. Key Recommendations and Analysis

- 2.5.9. A Way Forward

- 2.1. Global Quantum Photonics Market Outlook

- 3. Industry Data and Premium Insights

- 3.1. Global Quantum Photonics Industry Overview, 2025

- 3.1.1. Semiconductors & Electronics Industry Ecosystem Analysis

- 3.1.2. Key Trends for Semiconductors & Electronics Industry

- 3.1.3. Regional Distribution for Semiconductors & Electronics Industry

- 3.2. Supplier Customer Data

- 3.3. Technology Roadmap and Developments

- 3.4. Trade Analysis

- 3.4.1. Import & Export Analysis, 2025

- 3.4.2. Top Importing Countries

- 3.4.3. Top Exporting Countries

- 3.5. Trump Tariff Impact Analysis

- 3.5.1. Manufacturer

- 3.5.1.1. Based on the component & Raw material

- 3.5.2. Supply Chain

- 3.5.3. End Consumer

- 3.5.1. Manufacturer

- 3.6. Raw Material Analysis

- 3.1. Global Quantum Photonics Industry Overview, 2025

- 4. Market Overview

- 4.1. Market Dynamics

- 4.1.1. Drivers

- 4.1.1.1. Rising demand for quantum-secure communication and encryption technologies

- 4.1.1.2. Increasing government and private investment in quantum computing and photonics R&D

- 4.1.1.3. Expanding use of quantum photonics in sensing, imaging, and photonic integrated circuits

- 4.1.2. Restraints

- 4.1.2.1. High development costs and technical complexity of quantum photonic systems

- 4.1.2.2. Scalability challenges and shortage of skilled quantum engineering professionals

- 4.1.1. Drivers

- 4.2. Key Trend Analysis

- 4.3. Regulatory Framework

- 4.3.1. Key Regulations, Norms, and Subsidies, by Key Countries

- 4.3.2. Tariffs and Standards

- 4.3.3. Impact Analysis of Regulations on the Market

- 4.4. Ecosystem Analysis

- 4.5. Porter’s Five Forces Analysis

- 4.6. PESTEL Analysis

- 4.7. Global Quantum Photonics Market Demand

- 4.7.1. Historical Market Size – in Value (US$ Bn), 2020-2024

- 4.7.2. Current and Future Market Size – in Value (US$ Bn), 2025–2035

- 4.7.2.1. Y-o-Y Growth Trends

- 4.7.2.2. Absolute $ Opportunity Assessment

- 4.1. Market Dynamics

- 5. Competition Landscape

- 5.1. Competition structure

- 5.1.1. Fragmented v/s consolidated

- 5.2. Company Share Analysis, 2025

- 5.2.1. Global Company Market Share

- 5.2.2. By Region

- 5.2.2.1. North America

- 5.2.2.2. Europe

- 5.2.2.3. Asia Pacific

- 5.2.2.4. Middle East

- 5.2.2.5. Africa

- 5.2.2.6. South America

- 5.3. Product Comparison Matrix

- 5.3.1. Specifications

- 5.3.2. Market Positioning

- 5.3.3. Pricing

- 5.1. Competition structure

- 6. Global Quantum Photonics Market Analysis, by Component

- 6.1. Key Segment Analysis

- 6.2. Quantum Photonics Market Size (Value – US$ Bn), Analysis, and Forecasts, by Component, 2021-2035

- 6.2.1. Quantum Light Sources

- 6.2.1.1. Single Photon Sources

- 6.2.1.2. Entangled Photon Sources

- 6.2.1.3. Squeezed Light Sources

- 6.2.1.4. Others

- 6.2.2. Quantum Detectors

- 6.2.2.1. Single Photon Detectors

- 6.2.2.2. Photon Number Resolving Detectors

- 6.2.2.3. Homodyne Detectors

- 6.2.2.4. Others

- 6.2.3. Quantum Processors

- 6.2.3.1. Photonic Quantum Processors

- 6.2.3.2. Integrated Quantum Photonic Chips

- 6.2.4. Optical Components

- 6.2.4.1. Beam Splitters

- 6.2.4.2. Phase Shifters

- 6.2.4.3. Waveguides

- 6.2.4.4. Optical Filters

- 6.2.4.5. Others

- 6.2.1. Quantum Light Sources

- 7. Global Quantum Photonics Market Analysis, by Technology

- 7.1. Key Segment Analysis

- 7.2. Quantum Photonics Market Size (Value – US$ Bn), Analysis, and Forecasts, by Technology, 2021-2035

- 7.2.1. Quantum Communication

- 7.2.1.1. Quantum Key Distribution (QKD)

- 7.2.1.2. Quantum Teleportation

- 7.2.1.3. Quantum Repeaters

- 7.2.1.4. Others

- 7.2.2. Quantum Computing

- 7.2.2.1. Linear Optical Quantum Computing

- 7.2.2.2. Measurement-Based Quantum Computing

- 7.2.2.3. Continuous Variable Quantum Computing

- 7.2.2.4. Others

- 7.2.3. Quantum Sensing & Metrology

- 7.2.3.1. Quantum Imaging

- 7.2.3.2. Quantum Timing

- 7.2.3.3. Quantum Magnetometry

- 7.2.3.4. Others

- 7.2.4. Quantum Simulation

- 7.2.1. Quantum Communication

- 8. Global Quantum Photonics Market Analysis, by Material Platform

- 8.1. Key Segment Analysis

- 8.2. Quantum Photonics Market Size (Value – US$ Bn), Analysis, and Forecasts, by Material Platform, 2021-2035

- 8.2.1. Silicon Photonics

- 8.2.2. Gallium Arsenide (GaAs)

- 8.2.3. Indium Phosphide (InP)

- 8.2.4. Silicon Nitride (Si3N4)

- 8.2.5. Diamond (NV Centers)

- 8.2.6. Quantum Dots

- 8.2.7. Superconducting Materials

- 8.2.8. Others

- 9. Global Quantum Photonics Market Analysis, by Integration Level

- 9.1. Key Segment Analysis

- 9.2. Quantum Photonics Market Size (Value – US$ Bn), Analysis, and Forecasts, by Integration Level, 2021-2035

- 9.2.1. Discrete Components

- 9.2.2. Hybrid Integrated Systems

- 9.2.3. Monolithic Integrated Circuits

- 9.2.4. Photonic Integrated Circuits (PICs)

- 10. Global Quantum Photonics Market Analysis, by Wavelength Range

- 10.1. Key Segment Analysis

- 10.2. Quantum Photonics Market Size (Value – US$ Bn), Analysis, and Forecasts, by Wavelength Range, 2021-2035

- 10.2.1. Visible Light (400-700 nm)

- 10.2.2. Near-Infrared (700-1400 nm)

- 10.2.3. Telecom Wavelength (1260-1675 nm)

- 10.2.4. Mid-Infrared (>1675 nm)

- 11. Global Quantum Photonics Market Analysis, by Power Consumption

- 11.1. Key Segment Analysis

- 11.2. Quantum Photonics Market Size (Value – US$ Bn), Analysis, and Forecasts, by Power Consumption, 2021-2035

- 11.2.1. Ultra-Low Power (<1W)

- 11.2.2. Low Power (1-10W)

- 11.2.3. Medium Power (10-100W)

- 11.2.4. High Power (>100W)

- 12. Global Quantum Photonics Market Analysis, by System Configuration

- 12.1. Key Segment Analysis

- 12.2. Quantum Photonics Market Size (Value – US$ Bn), Analysis, and Forecasts, by System Configuration, 2021-2035

- 12.2.1. Standalone Systems

- 12.2.2. Networked Systems

- 12.2.3. Cloud-Integrated Systems

- 12.2.4. Hybrid Classical-Quantum Systems

- 13. Global Quantum Photonics Market Analysis, by End-use Industry

- 13.1. Key Segment Analysis

- 13.2. Quantum Photonics Market Size (Value – US$ Bn), Analysis, and Forecasts, by End-use Industry, 2021-2035

- 13.2.1. Defense & Aerospace

- 13.2.1.1. Secure Military Communications

- 13.2.1.2. Satellite Quantum Communication

- 13.2.1.3. Quantum Radar Systems

- 13.2.1.4. Navigation & Positioning Systems

- 13.2.1.5. Intelligence & Surveillance

- 13.2.1.6. Others

- 13.2.2. BFSI

- 13.2.2.1. Secure Financial Transactions

- 13.2.2.2. Quantum-Safe Cryptography

- 13.2.2.3. Fraud Detection & Prevention

- 13.2.2.4. High-Frequency Trading Security

- 13.2.2.5. Digital Asset Protection

- 13.2.2.6. Others

- 13.2.3. Healthcare & Life Sciences

- 13.2.3.1. Medical Imaging Enhancement

- 13.2.3.2. Drug Discovery & Molecular Analysis

- 13.2.3.3. Secure Patient Data Transmission

- 13.2.3.4. DNA Sequencing

- 13.2.3.5. Biosensing Applications

- 13.2.3.6. Others

- 13.2.4. Telecommunications

- 13.2.4.1. Quantum Network Infrastructure

- 13.2.4.2. 5G/6G Security Enhancement

- 13.2.4.3. Long-Distance Secure Communication

- 13.2.4.4. Data Center Security

- 13.2.4.5. Fiber Optic Network Optimization

- 13.2.4.6. Others

- 13.2.5. Information Technology & Data Centers

- 13.2.5.1. Quantum Cloud Computing

- 13.2.5.2. Secure Data Storage

- 13.2.5.3. Quantum-Enhanced AI/ML

- 13.2.5.4. Distributed Computing Networks

- 13.2.5.5. Cybersecurity Solutions

- 13.2.5.6. Others

- 13.2.6. Government & Public Sector

- 13.2.7. Energy & Utilities

- 13.2.8. Manufacturing & Industrial

- 13.2.9. Research & Academia

- 13.2.10. Retail & E-commerce

- 13.2.11. Media & Entertainment

- 13.2.12. Other Industries

- 13.2.1. Defense & Aerospace

- 14. Global Quantum Photonics Market Analysis, by Region

- 14.1. Key Findings

- 14.2. Quantum Photonics Market Size (Value - US$ Mn), Analysis, and Forecasts, by Region, 2021-2035

- 14.2.1. North America

- 14.2.2. Europe

- 14.2.3. Asia Pacific

- 14.2.4. Middle East

- 14.2.5. Africa

- 14.2.6. South America

- 15. North America Quantum Photonics Market Analysis

- 15.1. Key Segment Analysis

- 15.2. Regional Snapshot

- 15.3. North America Quantum Photonics Market Size Value – US$ Bn), Analysis, and Forecasts, 2021-2035

- 15.3.1. Component

- 15.3.2. Technology

- 15.3.3. Material Platform

- 15.3.4. Integration Level

- 15.3.5. Wavelength Range

- 15.3.6. Power Consumption

- 15.3.7. System Configuration

- 15.3.8. End-use Industry

- 15.3.9. Country

- 15.3.9.1. USA

- 15.3.9.2. Canada

- 15.3.9.3. Mexico

- 15.4. USA Quantum Photonics Market

- 15.4.1. Country Segmental Analysis

- 15.4.2. Component

- 15.4.3. Technology

- 15.4.4. Material Platform

- 15.4.5. Integration Level

- 15.4.6. Wavelength Range

- 15.4.7. Power Consumption

- 15.4.8. System Configuration

- 15.4.9. End-use Industry

- 15.5. Canada Quantum Photonics Market

- 15.5.1. Country Segmental Analysis

- 15.5.2. Component

- 15.5.3. Technology

- 15.5.4. Material Platform

- 15.5.5. Integration Level

- 15.5.6. Wavelength Range

- 15.5.7. Power Consumption

- 15.5.8. System Configuration

- 15.5.9. End-use Industry

- 15.6. Mexico Quantum Photonics Market

- 15.6.1. Country Segmental Analysis

- 15.6.2. Component

- 15.6.3. Technology

- 15.6.4. Material Platform

- 15.6.5. Integration Level

- 15.6.6. Wavelength Range

- 15.6.7. Power Consumption

- 15.6.8. System Configuration

- 15.6.9. End-use Industry

- 16. Europe Quantum Photonics Market Analysis

- 16.1. Key Segment Analysis

- 16.2. Regional Snapshot

- 16.3. Europe Quantum Photonics Market Size (Value – US$ Bn), Analysis, and Forecasts, 2021-2035

- 16.3.1. Component

- 16.3.2. Technology

- 16.3.3. Material Platform

- 16.3.4. Integration Level

- 16.3.5. Wavelength Range

- 16.3.6. Power Consumption

- 16.3.7. System Configuration

- 16.3.8. End-use Industry

- 16.3.9. Country

- 16.3.9.1. Germany

- 16.3.9.2. United Kingdom

- 16.3.9.3. France

- 16.3.9.4. Italy

- 16.3.9.5. Spain

- 16.3.9.6. Netherlands

- 16.3.9.7. Nordic Countries

- 16.3.9.8. Poland

- 16.3.9.9. Russia & CIS

- 16.3.9.10. Rest of Europe

- 16.4. Germany Quantum Photonics Market

- 16.4.1. Country Segmental Analysis

- 16.4.2. Component

- 16.4.3. Technology

- 16.4.4. Material Platform

- 16.4.5. Integration Level

- 16.4.6. Wavelength Range

- 16.4.7. Power Consumption

- 16.4.8. System Configuration

- 16.4.9. End-use Industry

- 16.5. United Kingdom Quantum Photonics Market

- 16.5.1. Country Segmental Analysis

- 16.5.2. Component

- 16.5.3. Technology

- 16.5.4. Material Platform

- 16.5.5. Integration Level

- 16.5.6. Wavelength Range

- 16.5.7. Power Consumption

- 16.5.8. System Configuration

- 16.5.9. End-use Industry

- 16.6. France Quantum Photonics Market

- 16.6.1. Country Segmental Analysis

- 16.6.2. Component

- 16.6.3. Technology

- 16.6.4. Material Platform

- 16.6.5. Integration Level

- 16.6.6. Wavelength Range

- 16.6.7. Power Consumption

- 16.6.8. System Configuration

- 16.6.9. End-use Industry

- 16.7. Italy Quantum Photonics Market

- 16.7.1. Country Segmental Analysis

- 16.7.2. Component

- 16.7.3. Technology

- 16.7.4. Material Platform

- 16.7.5. Integration Level

- 16.7.6. Wavelength Range

- 16.7.7. Power Consumption

- 16.7.8. System Configuration

- 16.7.9. End-use Industry

- 16.8. Spain Quantum Photonics Market

- 16.8.1. Country Segmental Analysis

- 16.8.2. Component

- 16.8.3. Technology

- 16.8.4. Material Platform

- 16.8.5. Integration Level

- 16.8.6. Wavelength Range

- 16.8.7. Power Consumption

- 16.8.8. System Configuration

- 16.8.9. End-use Industry

- 16.9. Netherlands Quantum Photonics Market

- 16.9.1. Country Segmental Analysis

- 16.9.2. Component

- 16.9.3. Technology

- 16.9.4. Material Platform

- 16.9.5. Integration Level

- 16.9.6. Wavelength Range

- 16.9.7. Power Consumption

- 16.9.8. System Configuration

- 16.9.9. End-use Industry

- 16.10. Nordic Countries Quantum Photonics Market

- 16.10.1. Country Segmental Analysis

- 16.10.2. Component

- 16.10.3. Technology

- 16.10.4. Material Platform

- 16.10.5. Integration Level

- 16.10.6. Wavelength Range

- 16.10.7. Power Consumption

- 16.10.8. System Configuration

- 16.10.9. End-use Industry

- 16.11. Poland Quantum Photonics Market

- 16.11.1. Country Segmental Analysis

- 16.11.2. Component

- 16.11.3. Technology

- 16.11.4. Material Platform

- 16.11.5. Integration Level

- 16.11.6. Wavelength Range

- 16.11.7. Power Consumption

- 16.11.8. System Configuration

- 16.11.9. End-use Industry

- 16.12. Russia & CIS Quantum Photonics Market

- 16.12.1. Country Segmental Analysis

- 16.12.2. Component

- 16.12.3. Technology

- 16.12.4. Material Platform

- 16.12.5. Integration Level

- 16.12.6. Wavelength Range

- 16.12.7. Power Consumption

- 16.12.8. System Configuration

- 16.12.9. End-use Industry

- 16.13. Rest of Europe Quantum Photonics Market

- 16.13.1. Country Segmental Analysis

- 16.13.2. Component

- 16.13.3. Technology

- 16.13.4. Material Platform

- 16.13.5. Integration Level

- 16.13.6. Wavelength Range

- 16.13.7. Power Consumption

- 16.13.8. System Configuration

- 16.13.9. End-use Industry

- 17. Asia Pacific Quantum Photonics Market Analysis

- 17.1. Key Segment Analysis

- 17.2. Regional Snapshot

- 17.3. Asia Pacific Quantum Photonics Market Size (Value – US$ Bn), Analysis, and Forecasts, 2021-2035

- 17.3.1. Component

- 17.3.2. Technology

- 17.3.3. Material Platform

- 17.3.4. Integration Level

- 17.3.5. Wavelength Range

- 17.3.6. Power Consumption

- 17.3.7. System Configuration

- 17.3.8. End-use Industry

- 17.3.9. Country

- 17.3.9.1. China

- 17.3.9.2. India

- 17.3.9.3. Japan

- 17.3.9.4. South Korea

- 17.3.9.5. Australia and New Zealand

- 17.3.9.6. Indonesia

- 17.3.9.7. Malaysia

- 17.3.9.8. Thailand

- 17.3.9.9. Vietnam

- 17.3.9.10. Rest of Asia Pacific

- 17.4. China Quantum Photonics Market

- 17.4.1. Country Segmental Analysis

- 17.4.2. Component

- 17.4.3. Technology

- 17.4.4. Material Platform

- 17.4.5. Integration Level

- 17.4.6. Wavelength Range

- 17.4.7. Power Consumption

- 17.4.8. System Configuration

- 17.4.9. End-use Industry

- 17.5. India Quantum Photonics Market

- 17.5.1. Country Segmental Analysis

- 17.5.2. Component

- 17.5.3. Technology

- 17.5.4. Material Platform

- 17.5.5. Integration Level

- 17.5.6. Wavelength Range

- 17.5.7. Power Consumption

- 17.5.8. System Configuration

- 17.5.9. End-use Industry

- 17.6. Japan Quantum Photonics Market

- 17.6.1. Country Segmental Analysis

- 17.6.2. Component

- 17.6.3. Technology

- 17.6.4. Material Platform

- 17.6.5. Integration Level

- 17.6.6. Wavelength Range

- 17.6.7. Power Consumption

- 17.6.8. System Configuration

- 17.6.9. End-use Industry

- 17.7. South Korea Quantum Photonics Market

- 17.7.1. Country Segmental Analysis

- 17.7.2. Component

- 17.7.3. Technology

- 17.7.4. Material Platform

- 17.7.5. Integration Level

- 17.7.6. Wavelength Range

- 17.7.7. Power Consumption

- 17.7.8. System Configuration

- 17.7.9. End-use Industry

- 17.8. Australia and New Zealand Quantum Photonics Market

- 17.8.1. Country Segmental Analysis

- 17.8.2. Component

- 17.8.3. Technology

- 17.8.4. Material Platform

- 17.8.5. Integration Level

- 17.8.6. Wavelength Range

- 17.8.7. Power Consumption

- 17.8.8. System Configuration

- 17.8.9. End-use Industry

- 17.9. Indonesia Quantum Photonics Market

- 17.9.1. Country Segmental Analysis

- 17.9.2. Component

- 17.9.3. Technology

- 17.9.4. Material Platform

- 17.9.5. Integration Level

- 17.9.6. Wavelength Range

- 17.9.7. Power Consumption

- 17.9.8. System Configuration

- 17.9.9. End-use Industry

- 17.10. Malaysia Quantum Photonics Market

- 17.10.1. Country Segmental Analysis

- 17.10.2. Component

- 17.10.3. Technology

- 17.10.4. Material Platform

- 17.10.5. Integration Level

- 17.10.6. Wavelength Range

- 17.10.7. Power Consumption

- 17.10.8. System Configuration

- 17.10.9. End-use Industry

- 17.11. Thailand Quantum Photonics Market

- 17.11.1. Country Segmental Analysis

- 17.11.2. Component

- 17.11.3. Technology

- 17.11.4. Material Platform

- 17.11.5. Integration Level

- 17.11.6. Wavelength Range

- 17.11.7. Power Consumption

- 17.11.8. System Configuration

- 17.11.9. End-use Industry

- 17.12. Vietnam Quantum Photonics Market

- 17.12.1. Country Segmental Analysis

- 17.12.2. Component

- 17.12.3. Technology

- 17.12.4. Material Platform

- 17.12.5. Integration Level

- 17.12.6. Wavelength Range

- 17.12.7. Power Consumption

- 17.12.8. System Configuration

- 17.12.9. End-use Industry

- 17.13. Rest of Asia Pacific Quantum Photonics Market

- 17.13.1. Country Segmental Analysis

- 17.13.2. Component

- 17.13.3. Technology

- 17.13.4. Material Platform

- 17.13.5. Integration Level

- 17.13.6. Wavelength Range

- 17.13.7. Power Consumption

- 17.13.8. System Configuration

- 17.13.9. End-use Industry

- 18. Middle East Quantum Photonics Market Analysis

- 18.1. Key Segment Analysis

- 18.2. Regional Snapshot

- 18.3. Middle East Quantum Photonics Market Size (Value – US$ Bn), Analysis, and Forecasts, 2021-2035

- 18.3.1. Component

- 18.3.2. Technology

- 18.3.3. Material Platform

- 18.3.4. Integration Level

- 18.3.5. Wavelength Range

- 18.3.6. Power Consumption

- 18.3.7. System Configuration

- 18.3.8. End-use Industry

- 18.3.9. Country

- 18.3.9.1. Turkey

- 18.3.9.2. UAE

- 18.3.9.3. Saudi Arabia

- 18.3.9.4. Israel

- 18.3.9.5. Rest of Middle East

- 18.4. Turkey Quantum Photonics Market

- 18.4.1. Country Segmental Analysis

- 18.4.2. Component

- 18.4.3. Technology

- 18.4.4. Material Platform

- 18.4.5. Integration Level

- 18.4.6. Wavelength Range

- 18.4.7. Power Consumption

- 18.4.8. System Configuration

- 18.4.9. End-use Industry

- 18.5. UAE Quantum Photonics Market

- 18.5.1. Country Segmental Analysis

- 18.5.2. Component

- 18.5.3. Technology

- 18.5.4. Material Platform

- 18.5.5. Integration Level

- 18.5.6. Wavelength Range

- 18.5.7. Power Consumption

- 18.5.8. System Configuration

- 18.5.9. End-use Industry

- 18.6. Saudi Arabia Quantum Photonics Market

- 18.6.1. Country Segmental Analysis

- 18.6.2. Component

- 18.6.3. Technology

- 18.6.4. Material Platform

- 18.6.5. Integration Level

- 18.6.6. Wavelength Range

- 18.6.7. Power Consumption

- 18.6.8. System Configuration

- 18.6.9. End-use Industry

- 18.7. Israel Quantum Photonics Market

- 18.7.1. Country Segmental Analysis

- 18.7.2. Component

- 18.7.3. Technology

- 18.7.4. Material Platform

- 18.7.5. Integration Level

- 18.7.6. Wavelength Range

- 18.7.7. Power Consumption

- 18.7.8. System Configuration

- 18.7.9. End-use Industry

- 18.8. Rest of Middle East Quantum Photonics Market

- 18.8.1. Country Segmental Analysis

- 18.8.2. Component

- 18.8.3. Technology

- 18.8.4. Material Platform

- 18.8.5. Integration Level

- 18.8.6. Wavelength Range

- 18.8.7. Power Consumption

- 18.8.8. System Configuration

- 18.8.9. End-use Industry

- 19. Africa Quantum Photonics Market Analysis

- 19.1. Key Segment Analysis

- 19.2. Regional Snapshot

- 19.3. Africa Quantum Photonics Market Size (Value – US$ Bn), Analysis, and Forecasts, 2021-2035

- 19.3.1. Component

- 19.3.2. Technology

- 19.3.3. Material Platform

- 19.3.4. Integration Level

- 19.3.5. Wavelength Range

- 19.3.6. Power Consumption

- 19.3.7. System Configuration

- 19.3.8. End-use Industry

- 19.3.9. Country

- 19.3.9.1. South Africa

- 19.3.9.2. Egypt

- 19.3.9.3. Nigeria

- 19.3.9.4. Algeria

- 19.3.9.5. Rest of Africa

- 19.4. South Africa Quantum Photonics Market

- 19.4.1. Country Segmental Analysis

- 19.4.2. Component

- 19.4.3. Technology

- 19.4.4. Material Platform

- 19.4.5. Integration Level

- 19.4.6. Wavelength Range

- 19.4.7. Power Consumption

- 19.4.8. System Configuration

- 19.4.9. End-use Industry

- 19.5. Egypt Quantum Photonics Market

- 19.5.1. Country Segmental Analysis

- 19.5.2. Component

- 19.5.3. Technology

- 19.5.4. Material Platform

- 19.5.5. Integration Level

- 19.5.6. Wavelength Range

- 19.5.7. Power Consumption

- 19.5.8. System Configuration

- 19.5.9. End-use Industry

- 19.6. Nigeria Quantum Photonics Market

- 19.6.1. Country Segmental Analysis

- 19.6.2. Component

- 19.6.3. Technology

- 19.6.4. Material Platform

- 19.6.5. Integration Level

- 19.6.6. Wavelength Range

- 19.6.7. Power Consumption

- 19.6.8. System Configuration

- 19.6.9. End-use Industry

- 19.7. Algeria Quantum Photonics Market

- 19.7.1. Country Segmental Analysis

- 19.7.2. Component

- 19.7.3. Technology

- 19.7.4. Material Platform

- 19.7.5. Integration Level

- 19.7.6. Wavelength Range

- 19.7.7. Power Consumption

- 19.7.8. System Configuration

- 19.7.9. End-use Industry

- 19.8. Rest of Africa Quantum Photonics Market

- 19.8.1. Country Segmental Analysis

- 19.8.2. Component

- 19.8.3. Technology

- 19.8.4. Material Platform

- 19.8.5. Integration Level

- 19.8.6. Wavelength Range

- 19.8.7. Power Consumption

- 19.8.8. System Configuration

- 19.8.9. End-use Industry

- 20. South America Quantum Photonics Market Analysis

- 20.1. Key Segment Analysis

- 20.2. Regional Snapshot

- 20.3. South America Quantum Photonics Market Size (Value – US$ Bn), Analysis, and Forecasts, 2021-2035

- 20.3.1. Component

- 20.3.2. Technology

- 20.3.3. Material Platform

- 20.3.4. Integration Level

- 20.3.5. Wavelength Range

- 20.3.6. Power Consumption

- 20.3.7. System Configuration

- 20.3.8. End-use Industry

- 20.3.9. Country

- 20.3.9.1. Brazil

- 20.3.9.2. Argentina

- 20.3.9.3. Rest of South America

- 20.4. Brazil Quantum Photonics Market

- 20.4.1. Country Segmental Analysis

- 20.4.2. Component

- 20.4.3. Technology

- 20.4.4. Material Platform

- 20.4.5. Integration Level

- 20.4.6. Wavelength Range

- 20.4.7. Power Consumption

- 20.4.8. System Configuration

- 20.4.9. End-use Industry

- 20.5. Argentina Quantum Photonics Market

- 20.5.1. Country Segmental Analysis

- 20.5.2. Component

- 20.5.3. Technology

- 20.5.4. Material Platform

- 20.5.5. Integration Level

- 20.5.6. Wavelength Range

- 20.5.7. Power Consumption

- 20.5.8. System Configuration

- 20.5.9. End-use Industry

- 20.6. Rest of South America Quantum Photonics Market

- 20.6.1. Country Segmental Analysis

- 20.6.2. Component

- 20.6.3. Technology

- 20.6.4. Material Platform

- 20.6.5. Integration Level

- 20.6.6. Wavelength Range

- 20.6.7. Power Consumption

- 20.6.8. System Configuration

- 20.6.9. End-use Industry

- 21. Key Players/ Company Profile

- 21.1. ID Quantique

- 21.1.1. Company Details/ Overview

- 21.1.2. Company Financials

- 21.1.3. Key Customers and Competitors

- 21.1.4. Business/ Industry Portfolio

- 21.1.5. Product Portfolio/ Specification Details

- 21.1.6. Pricing Data

- 21.1.7. Strategic Overview

- 21.1.8. Recent Developments

- 21.2. IonQ

- 21.3. NuCrypt

- 21.4. ORCA Computing

- 21.5. Photonic Inc.

- 21.6. PsiQuantum

- 21.7. Q.ANT

- 21.8. QPhoX

- 21.9. Quandela

- 21.10. Quantum Brilliance

- 21.11. Quantum Xchange

- 21.12. QuantumCTek

- 21.13. QuintessenceLabs

- 21.14. QuiX Quantum

- 21.15. Rigetti Computing

- 21.16. Single Quantum

- 21.17. Toshiba Corporation

- 21.18. Xanadu Quantum Technologies

- 21.19. Other Key Players

- 21.1. ID Quantique

Note* - This is just tentative list of players. While providing the report, we will cover more number of players based on their revenue and share for each geography

Research Design

Our research design integrates both demand-side and supply-side analysis through a balanced combination of primary and secondary research methodologies. By utilizing both bottom-up and top-down approaches alongside rigorous data triangulation methods, we deliver robust market intelligence that supports strategic decision-making.

MarketGenics' comprehensive research design framework ensures the delivery of accurate, reliable, and actionable market intelligence. Through the integration of multiple research approaches, rigorous validation processes, and expert analysis, we provide our clients with the insights needed to make informed strategic decisions and capitalize on market opportunities.

MarketGenics leverages a dedicated industry panel of experts and a comprehensive suite of paid databases to effectively collect, consolidate, and analyze market intelligence.

Our approach has consistently proven to be reliable and effective in generating accurate market insights, identifying key industry trends, and uncovering emerging business opportunities.

Through both primary and secondary research, we capture and analyze critical company-level data such as manufacturing footprints, including technical centers, R&D facilities, sales offices, and headquarters.

Our expert panel further enhances our ability to estimate market size for specific brands based on validated field-level intelligence.

Our data mining techniques incorporate both parametric and non-parametric methods, allowing for structured data collection, sorting, processing, and cleaning.

Demand projections are derived from large-scale data sets analyzed through proprietary algorithms, culminating in robust and reliable market sizing.

Research Approach

The bottom-up approach builds market estimates by starting with the smallest addressable market units and systematically aggregating them to create comprehensive market size projections.

This method begins with specific, granular data points and builds upward to create the complete market landscape.

Customer Analysis → Segmental Analysis → Geographical Analysis

The top-down approach starts with the broadest possible market data and systematically narrows it down through a series of filters and assumptions to arrive at specific market segments or opportunities.

This method begins with the big picture and works downward to increasingly specific market slices.

TAM → SAM → SOM

Research Methods

Desk / Secondary Research

While analysing the market, we extensively study secondary sources, directories, and databases to identify and collect information useful for this technical, market-oriented, and commercial report. Secondary sources that we utilize are not only the public sources, but it is a combination of Open Source, Associations, Paid Databases, MG Repository & Knowledgebase, and others.

- Company websites, annual reports, financial reports, broker reports, and investor presentations

- National government documents, statistical databases and reports

- News articles, press releases and web-casts specific to the companies operating in the market, Magazines, reports, and others

- We gather information from commercial data sources for deriving company specific data such as segmental revenue, share for geography, product revenue, and others

- Internal and external proprietary databases (industry-specific), relevant patent, and regulatory databases

- Governing Bodies, Government Organizations

- Relevant Authorities, Country-specific Associations for Industries

We also employ the model mapping approach to estimate the product level market data through the players' product portfolio

Primary Research

Primary research/ interviews is vital in analyzing the market. Most of the cases involves paid primary interviews. Primary sources include primary interviews through e-mail interactions, telephonic interviews, surveys as well as face-to-face interviews with the different stakeholders across the value chain including several industry experts.

| Type of Respondents | Number of Primaries |

|---|---|

| Tier 2/3 Suppliers | ~20 |

| Tier 1 Suppliers | ~25 |

| End-users | ~25 |

| Industry Expert/ Panel/ Consultant | ~30 |

| Total | ~100 |

MG Knowledgebase

• Repository of industry blog, newsletter and case studies

• Online platform covering detailed market reports, and company profiles

Forecasting Factors and Models

Forecasting Factors

- Historical Trends – Past market patterns, cycles, and major events that shaped how markets behave over time. Understanding past trends helps predict future behavior.

- Industry Factors – Specific characteristics of the industry like structure, regulations, and innovation cycles that affect market dynamics.

- Macroeconomic Factors – Economic conditions like GDP growth, inflation, and employment rates that affect how much money people have to spend.

- Demographic Factors – Population characteristics like age, income, and location that determine who can buy your product.

- Technology Factors – How quickly people adopt new technology and how much technology infrastructure exists.

- Regulatory Factors – Government rules, laws, and policies that can help or restrict market growth.

- Competitive Factors – Analyzing competition structure such as degree of competition and bargaining power of buyers and suppliers.

Forecasting Models / Techniques

Multiple Regression Analysis

- Identify and quantify factors that drive market changes

- Statistical modeling to establish relationships between market drivers and outcomes

Time Series Analysis – Seasonal Patterns

- Understand regular cyclical patterns in market demand

- Advanced statistical techniques to separate trend, seasonal, and irregular components

Time Series Analysis – Trend Analysis

- Identify underlying market growth patterns and momentum

- Statistical analysis of historical data to project future trends

Expert Opinion – Expert Interviews

- Gather deep industry insights and contextual understanding

- In-depth interviews with key industry stakeholders

Multi-Scenario Development

- Prepare for uncertainty by modeling different possible futures

- Creating optimistic, pessimistic, and most likely scenarios

Time Series Analysis – Moving Averages

- Sophisticated forecasting for complex time series data

- Auto-regressive integrated moving average models with seasonal components

Econometric Models

- Apply economic theory to market forecasting

- Sophisticated economic models that account for market interactions

Expert Opinion – Delphi Method

- Harness collective wisdom of industry experts

- Structured, multi-round expert consultation process

Monte Carlo Simulation

- Quantify uncertainty and probability distributions

- Thousands of simulations with varying input parameters

Research Analysis

Our research framework is built upon the fundamental principle of validating market intelligence from both demand and supply perspectives. This dual-sided approach ensures comprehensive market understanding and reduces the risk of single-source bias.

Demand-Side Analysis: We understand end-user/application behavior, preferences, and market needs along with the penetration of the product for specific application.

Supply-Side Analysis: We estimate overall market revenue, analyze the segmental share along with industry capacity, competitive landscape, and market structure.

Validation & Evaluation

Data triangulation is a validation technique that uses multiple methods, sources, or perspectives to examine the same research question, thereby increasing the credibility and reliability of research findings. In market research, triangulation serves as a quality assurance mechanism that helps identify and minimize bias, validate assumptions, and ensure accuracy in market estimates.

- Data Source Triangulation – Using multiple data sources to examine the same phenomenon

- Methodological Triangulation – Using multiple research methods to study the same research question

- Investigator Triangulation – Using multiple researchers or analysts to examine the same data

- Theoretical Triangulation – Using multiple theoretical perspectives to interpret the same data

Custom Market Research Services

We will customise the research for you, in case the report listed above does not meet your requirements.

Get 10% Free Customisation