Aerial Firefighting Market Size, Share & Trends Analysis Report by Aircraft Type (Fixed-Wing Aircraft, Rotary-Wing Aircraft, Unmanned Aerial Vehicles (UAVs)), Retardant/Suppressant Type, Capacity, Operation Type, Deployment Mode, Fire Type, Service Type, and Geography (North America, Europe, Asia Pacific, Middle East, Africa, and South America) – Global Industry Data, Trends, and Forecasts, 2026–2035

|

|

|

Segmental Data Insights |

|

|

Demand Trends |

|

|

Competitive Landscape |

|

|

Strategic Development |

|

|

Future Outlook & Opportunities |

|

Aerial Firefighting Market Size, Share, and Growth

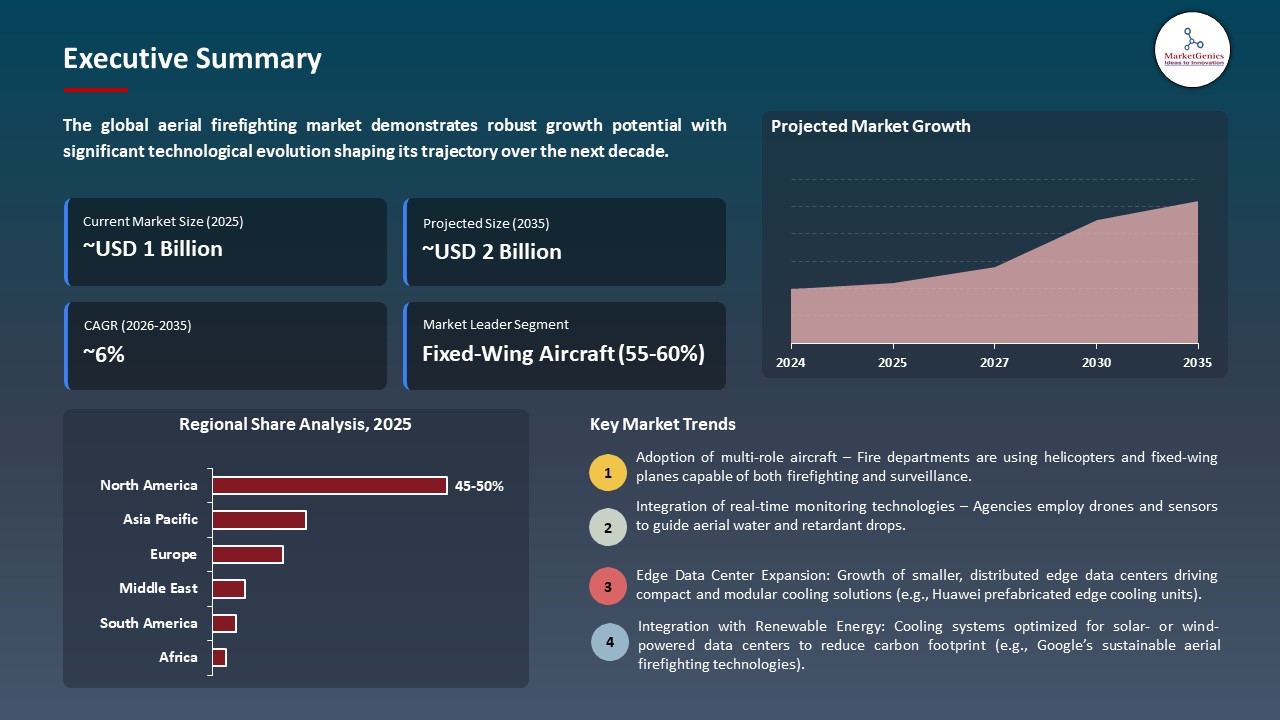

The global aerial firefighting market is experiencing robust growth, with its estimated value of USD 1.3 billion in the year 2025 and USD 2.4 billion by 2035, registering a CAGR of 6.4%, during the forecast period. Sophisticated mission-oriented platforms and integrated UAV-drone systems with real-time fire mapping, AI-driven flight operations, and precise delivery of retardants are driving the global aerial firefighting market toward enhancing the efficiency, speed, and safety of suppression operations in large-scale wildfire response.

Mark Groden, Founder and CEO of Skyryse, said: In firefighting, every second counts. Fires can double in size every 30 seconds — and when fires move faster, we have to move smarter. SkyOS technology provides greater capability, enhances mission profiles, and empowers emergency personnel to fight fires more effectively and safely. We’re honored and privileged to work alongside CAL FIRE, especially as a company founded and headquartered in California, to help leverage our technology in the fight against destructive wildfires. Equipping first responders with the latest and best in class technology isn’t just an investment in tools it’s an investment in lives.

The aerial firefighting market is growing with the rising severity of wildfire seasons all over the world with rising frequency, magnitude, and unpredictability of fire outbreaks triggering investment in the aerial suppression. Governments and commercial operators are replacing fleets with large capacity fixed wing tankers, all-purpose helicopters and long range UAVs to be able to deploy fast into remote and high risk locations. The emerging cross-border cooperation in the form of shared aerial resource and emergency response systems also affects the market growth.

There are technological advances that improve the accuracy and safety of operations, such as AI flight planning, real-time fire mapping, thermal imaging, and automated retardant delivery systems. The UAVs and swarms of drones are becoming more popular in the early detection, situational awareness, and coordinated suppression missions, which are supplemented by the manned aircraft. This kind of development minimizes human works under dangerous situations and enhances effectiveness in the management of wildfires.

The trend makes the market an innovation-driven and high-value market, and has a large potential in the long term. For instance, in September 2025, Sikorsky and CAL FIRE initiated a multi-year collaboration to strengthen autonomous aerial firefighting, the autonomous S-70i FIREHAWK helicopter, and improve situational awareness, reduce workload on pilots, and strengthen effectiveness in wildfire response. The recent developments in the aerial firefighting solutions sector have developed through the involvement of the government and the industrial sector, with the integration of advanced sensor systems and UAV platforms, have set the pace of the global industrial acceptance of aerial firefighting solutions as an essential part of the current wildfire management and disaster mitigation strategies.

Aerial Firefighting Market Dynamics and Trends

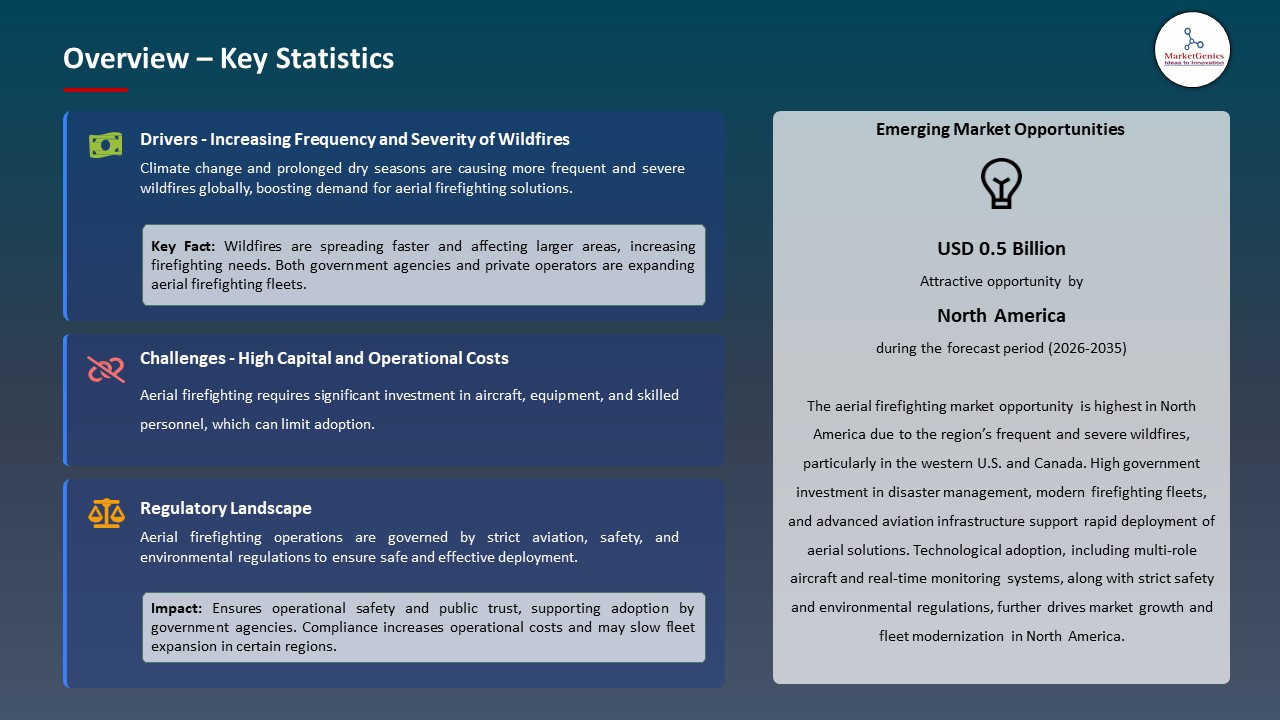

Driver: Increasing Frequency and Severity of Wildfires

-

The global aerial firefighting market is being fuelled by the sheer number and intensity of wildfires is increasing in unprecedented ways because of the proliferation of long dry seasons, high heat, and climate change-driven weather conditions that create conditions that are conducive to the rapid occurrence and spread of fires in a wide variety of locations, which necessitate a greater air response capacity.

- Recent incidents of wildfights have underscored the increasing demand of aerial fighting services. In summer 2025, the government acquired more airtankers and helicopters by leasing them to a private company, as wildfires in Alberta and British Columbia caused unprecedented damage to the country's forests, and the government had to cope with the outbreak of fires in remote and highly forested areas. This reinforces the idea of the increasing severity levels of wildfires causing investment and growth of aerial fire fighting fleets.

- The demands of aerial firefighting solutions are also increasing due to increasing wildland urban interface areas and longer fire seasons.

Restraint: High Operational and Maintenance Costs

-

High operation and maintenance is a serious limitation on the global aerial firefighting market with specialized aircraft and firefighting equipment consuming significant financial resource in terms of fuel, service cycle, inspections and technical maintenance. Maintaining large airtankers and specialized helicopters such as overhauls and avionics checkups may be a cost burden to any budget, especially to the small agencies and developing nations.

- The factors are related to high cost of procurement and lifecycle support. Helicopters may cost millions of dollars to purchase, and the operation costs per year such as fuel, maintenance, and training of pilots is prohibitive; an example is that fuel and maintenance costs have been mentioned by almost a third of firefighting agencies as a significant limitation of their operations.

- Compliance, inspection, and specialized staff needs also make it more expensive and restrict the growth of the fleet.

Opportunity Integration of Advanced Technologies and UAVs

-

The increased use of UAVs and innovations in firefighting is creating opportunities in aerial firefighting because agencies and non-governmental operators are starting to make use of drones and artificial intelligence-powered systems to make wildfire detection, surveillance, and management more efficient. Real-time data analytics and autonomous flight systems can be used to make decisions faster and deploy both manned and unmanned firefighting resources optimally.

- The next-generation aerial firefighting operations are being integrated with such advanced systems. For instance, in September 2024, FireSwarm Solutions Inc contracts with ACC Innovation to create the Thunder Wasp UAS Quadcopter and become the only distributor of ultra-heavy-lift UAVs in North America so that to achieve automated wildfire suppression and real-time tactical surveillance.

- The combination of UAVs and advanced analytics will enhance the efficiency of operations, scaling and early response to wildfires, generating new sources of income and facilitating safer, faster and more efficient aerial firefighting efforts across the globe.

Key Trend: Government Funding and Public‑Private Collaboration

-

Government subsidies and teamwork are propelling the global aerial firefighting market, with governments increasing government spending and engaging privates to enhance efforts to suppress wildfires. Investment is made in the acquisition of aircrafts, fleet preparedness and common operation structures to enhance response and effectiveness.

- Innovation and functioning efficiency in the market are being improved by strategic collaborations. In September 2025, Sikorsky and the California Department of Forestry and Fire Protection (CAL FIRE) announced a five-year partnership to develop and integrate autonomous aerial firefighting technology including exploration of an autonomous Sikorsky S-70i FIREHAWK helicopter that enhances capabilities of wildfire response, safety, and operational efficiency through a shared government-industry innovation.

- The world is witnessing a growth in the use of public-private partnerships which will facilitate sharing of resources, make transfer of technology and deployment of the same to a large scale and hence quick response in times of peak wildfire seasons.

Aerial Firefighting Market Analysis and Segmental Data

Fixed-Wing Aircraft Dominate Global Aerial Firefighting Market

-

Fixed-wing aircraft dominate the major portion of the global aerial firefighting market, owing to the fact that they provide better load carrying capacity, further range and cost-saving operations to address extensive wildfire damaged areas at a relatively low cost.

- The market is growing at a rapid pace due to the major breakthroughs in the technology of fixed-wing firefighting. Important progress in large-scale wildfire suppression capability came in July 2025, as Israel Aerospace Industries (IAI) collaborated with Fire Free Forests to jointly develop the 767FF Fire-Fighter fixed-wing aerial firefighting platform, which with a maximum carrying capacity of around 40 200 tons of retardant was equipped with advanced sensors and built-in command-and-control systems.

- The fixed wing aircrafts remain superior in the world because of the unchallenged coverage, efficiency, and capability in completing large-scale and high intensity of wildfire operations.

North America Leads Global Aerial Firefighting Market Demand

-

North America is dominating the aerial firefighting market as the frequency and severity of wildfires in both United States and Canada continue to rise, which is fueling the use of new rotary and fixed-wing firefighting aircraft, real-time aerial monitoring systems, and targeted retardant delivery platforms.

- The development of the regions has been reinforced through strategic government programs and cross-agency programs. For instance, in March 2025, Bridger Aerospace collaborated with Positive Aviation, making it the sole launch customer in North America of the FF72 amphibious water-scooping aircraft to expand the fleet and technological preparedness to better the efficiency of wild fires.

- Well established operator networks, mutual aid agreements and ongoing fleet modernization have also contributed to the dominance of North America and have made it the largest and very advanced aerial fighting market globally.

Aerial Firefighting Market Ecosystem

The global aerial firefighting market is moderately consolidated, with leading companies leveraging advanced technologies to maintain dominance. Key players such as Aero-Flite Aerial Firefighting, Air Tractor Inc., Babcock International Group, Conair Aerial Firefighting, Coulson Aviation, and Airbus Helicopters command a significant market share through high-performance aircraft, integrated UAV systems, and mission-optimized platforms, enabling rapid deployment and effective wildfire suppression across diverse terrains.

These companies are increasingly focusing on niche and specialized solutions to drive innovation. For instance, Air Tractor and Conair develop precision water and retardant delivery systems, while Airbus Helicopters and Babcock International integrate AI-assisted flight planning and real-time fire mapping into their platforms. Such specialized solutions enhance operational efficiency, safety, and firefighting effectiveness, catering to large-scale wildfire management and emergency response needs.

Government bodies, research institutions, and R&D organizations actively support technological advancement in the sector, funding initiatives that improve aircraft payload efficiency, drone integration, and mission analytics, thereby enhancing response times, accuracy, and resource utilization during wildfire operations. These developments illustrate how technological innovation, niche specialization, and strategic portfolio expansion are shaping the global Aerial Firefighting market, reinforcing efficiency, safety, and competitive differentiation while enabling rapid response to increasingly severe wildfire events worldwide.

Recent Development and Strategic Overview

-

In August 2025, Morocco expands its aerial firefighting capacity with a new Ayres 710P Turbo Thrush aircraft, increasing the number of this type at Salé air base and enhancing wildfire response capability with a turboprop that carries ~2,700 L of water or retardant for low‑altitude operations in rugged terrain.

- In July 2025, Skyryse signed a multi‑year partnership with the California Department of Forestry and Fire Protection (CAL FIRE) to integrate its SkyOS flight operating system into aerial firefighting aircraft enhancing safety, fly‑by‑wire controls, optionally piloted capabilities, payload range, and operational effectiveness for wildfire response missions.

Report Scope

|

Detail |

|

|

Market Size in 2025 |

USD 1.3 Bn |

|

Market Forecast Value in 2035 |

USD 2.4 Bn |

|

Growth Rate (CAGR) |

6.4% |

|

Forecast Period |

2026 – 2035 |

|

Historical Data Available for |

2021 – 2024 |

|

Market Size Units |

US$ Billion for Value |

|

Report Format |

Electronic (PDF) + Excel |

|

North America |

Europe |

Asia Pacific |

Middle East |

Africa |

South America |

|

|

|

|

|

|

|

Companies Covered |

|||||

|

|

|

|

|

|

Aerial Firefighting Market Segmentation and Highlights

|

Segment |

Sub-segment |

|

Aerial Firefighting Market, By Aircraft Type |

|

|

Aerial Firefighting Market, By Retardant/Suppressant Type |

|

|

Aerial Firefighting Market, By Capacity |

|

|

Aerial Firefighting Market, Operation Type |

|

|

Aerial Firefighting Market, By Deployment Mode |

|

|

Aerial Firefighting Market, By Fire Type |

|

|

Aerial Firefighting Market, By Service Type |

|

Frequently Asked Questions

Table of Contents

- 1. Research Methodology and Assumptions

- 1.1. Definitions

- 1.2. Research Design and Approach

- 1.3. Data Collection Methods

- 1.4. Base Estimates and Calculations

- 1.5. Forecasting Models

- 1.5.1. Key Forecast Factors & Impact Analysis

- 1.6. Secondary Research

- 1.6.1. Open Sources

- 1.6.2. Paid Databases

- 1.6.3. Associations

- 1.7. Primary Research

- 1.7.1. Primary Sources

- 1.7.2. Primary Interviews with Stakeholders across Ecosystem

- 2. Executive Summary

- 2.1. Global Aerial firefighting Market Outlook

- 2.1.1. Aerial firefighting Market Size (Value - US$ Bn), and Forecasts, 2021-2035

- 2.1.2. Compounded Annual Growth Rate Analysis

- 2.1.3. Growth Opportunity Analysis

- 2.1.4. Segmental Share Analysis

- 2.1.5. Geographical Share Analysis

- 2.2. Market Analysis and Facts

- 2.3. Supply-Demand Analysis

- 2.4. Competitive Benchmarking

- 2.5. Go-to- Market Strategy

- 2.5.1. Customer/ End-use Industry Assessment

- 2.5.2. Growth Opportunity Data, 2026-2035

- 2.5.2.1. Regional Data

- 2.5.2.2. Country Data

- 2.5.2.3. Segmental Data

- 2.5.3. Identification of Potential Market Spaces

- 2.5.4. GAP Analysis

- 2.5.5. Potential Attractive Price Points

- 2.5.6. Prevailing Market Risks & Challenges

- 2.5.7. Preferred Sales & Marketing Strategies

- 2.5.8. Key Recommendations and Analysis

- 2.5.9. A Way Forward

- 2.1. Global Aerial firefighting Market Outlook

- 3. Industry Data and Premium Insights

- 3.1. Global Aerospace & Defense Industry Overview, 2025

- 3.1.1. Aerospace & Defense Industry Ecosystem Analysis

- 3.1.2. Key Trends for Aerospace & Defense Industry

- 3.1.3. Regional Distribution for Aerospace & Defense Industry

- 3.2. Supplier Customer Data

- 3.3. Technology Roadmap and Developments

- 3.4. Trade Analysis

- 3.4.1. Import & Export Analysis, 2025

- 3.4.2. Top Importing Countries

- 3.4.3. Top Exporting Countries

- 3.5. Trump Tariff Impact Analysis

- 3.5.1. Manufacturer

- 3.5.1.1. Based on the component & Raw material

- 3.5.2. Supply Chain

- 3.5.3. End Consumer

- 3.5.1. Manufacturer

- 3.6. Raw Material Analysis

- 3.1. Global Aerospace & Defense Industry Overview, 2025

- 4. Market Overview

- 4.1. Market Dynamics

- 4.1.1. Drivers

- 4.1.1.1. Increasing frequency and intensity of wildfires driven by climate change and prolonged dry seasons.

- 4.1.1.2. Rising government spending on disaster management, emergency response, and wildfire mitigation programs.

- 4.1.1.3. Technological advancements in aerial platforms, fire-retardant delivery systems, and real-time monitoring capabilities.

- 4.1.2. Restraints

- 4.1.2.1. High capital, operating, and maintenance costs associated with aerial firefighting aircraft.

- 4.1.2.2. Strict regulatory requirements, safety concerns, and limited availability of trained pilots and crew.

- 4.1.1. Drivers

- 4.2. Key Trend Analysis

- 4.3. Regulatory Framework

- 4.3.1. Key Regulations, Norms, and Subsidies, by Key Countries

- 4.3.2. Tariffs and Standards

- 4.3.3. Impact Analysis of Regulations on the Market

- 4.4. Value Chain Analysis

- 4.4.1. Component Suppliers

- 4.4.2. Aircraft Manufacturers

- 4.4.3. Dealers/ Distributors

- 4.4.4. End-Users/ Customers

- 4.5. Porter’s Five Forces Analysis

- 4.6. PESTEL Analysis

- 4.7. Global Aerial firefighting Market Demand

- 4.7.1. Historical Market Size – Value (US$ Bn), 2020-2024

- 4.7.2. Current and Future Market Size – Value (US$ Bn), 2026–2035

- 4.7.2.1. Y-o-Y Growth Trends

- 4.7.2.2. Absolute $ Opportunity Assessment

- 4.1. Market Dynamics

- 5. Competition Landscape

- 5.1. Competition structure

- 5.1.1. Fragmented v/s consolidated

- 5.2. Company Share Analysis, 2025

- 5.2.1. Global Company Market Share

- 5.2.2. By Region

- 5.2.2.1. North America

- 5.2.2.2. Europe

- 5.2.2.3. Asia Pacific

- 5.2.2.4. Middle East

- 5.2.2.5. Africa

- 5.2.2.6. South America

- 5.3. Product Comparison Matrix

- 5.3.1. Specifications

- 5.3.2. Market Positioning

- 5.3.3. Pricing

- 5.1. Competition structure

- 6. Global Aerial firefighting Market Analysis, by Aircraft Type

- 6.1. Key Segment Analysis

- 6.2. Aerial firefighting Market Size (Value - US$ Bn), Analysis, and Forecasts, by Aircraft Type, 2021-2035

- 6.2.1. Fixed-Wing Aircraft

- 6.2.1.1. Air Tankers

- 6.2.1.1.1. Heavy Air Tankers

- 6.2.1.1.2. Medium Air Tankers

- 6.2.1.1.3. Light Air Tankers

- 6.2.1.2. Single Engine Air Tankers (SEATs)

- 6.2.1.3. Very Large Air Tankers (VLATs)

- 6.2.1.4. Scoopers/Amphibious Aircraft

- 6.2.1.1. Air Tankers

- 6.2.2. Rotary-Wing Aircraft

- 6.2.2.1. Heavy Helicopters

- 6.2.2.2. Medium Helicopters

- 6.2.2.3. Light Helicopters

- 6.2.2.4. Helitankers

- 6.2.3. Unmanned Aerial Vehicles (UAVs)

- 6.2.3.1. Fixed-Wing Drones

- 6.2.3.2. Rotary-Wing Drones

- 6.2.1. Fixed-Wing Aircraft

- 7. Global Aerial firefighting Market Analysis, by Retardant/Suppressant Type

- 7.1. Key Segment Analysis

- 7.2. Aerial firefighting Market Size (Value - US$ Bn), Analysis, and Forecasts, by Retardant/Suppressant Type, 2021-2035

- 7.2.1. Long-Term Retardants

- 7.2.1.1. Ammonium Phosphate-Based

- 7.2.1.2. Ammonium Sulfate-Based

- 7.2.1.3. Others

- 7.2.2. Short-Term Retardants

- 7.2.2.1. Foam Concentrates

- 7.2.2.2. Gels

- 7.2.2.3. Others

- 7.2.3. Water

- 7.2.3.1. Plain Water

- 7.2.3.2. Water with Additives

- 7.2.1. Long-Term Retardants

- 8. Global Aerial firefighting Market Analysis, by Capacity

- 8.1. Key Segment Analysis

- 8.2. Aerial firefighting Market Size (Value - US$ Bn), Analysis, and Forecasts, by Capacity, 2021-2035

- 8.2.1. Less than 1,000 Gallons

- 8.2.2. 1,000 - 3,000 Gallons

- 8.2.3. 3,000 - 5,000 Gallons

- 8.2.4. 5,000 - 8,000 Gallons

- 8.2.5. Above 8,000 Gallons

- 9. Global Aerial firefighting Market Analysis, by Operation Type

- 9.1. Key Segment Analysis

- 9.2. Aerial firefighting Market Size (Value - US$ Bn), Analysis, and Forecasts, by Operation Type, 2021-2035

- 9.2.1. Government Operated

- 9.2.1.1. Federal Government

- 9.2.1.2. State/Provincial Government

- 9.2.1.3. Local Government

- 9.2.2. Private Contractors

- 9.2.2.1. Exclusive Use Contracts

- 9.2.2.2. Call-When-Needed Contracts

- 9.2.3. Public-Private Partnership

- 9.2.1. Government Operated

- 10. Global Aerial firefighting Market Analysis, by Deployment Mode

- 10.1. Key Segment Analysis

- 10.2. Aerial firefighting Market Size (Value - US$ Bn), Analysis, and Forecasts, by Deployment Mode, 2021-2035

- 10.2.1. Initial Attack

- 10.2.2. Extended Attack

- 10.2.3. Support Operations

- 10.2.4. Mop-Up Operations

- 10.2.5. Preventive Operations

- 11. Global Aerial firefighting Market Analysis, by Fire Type

- 11.1. Key Segment Analysis

- 11.2. Aerial firefighting Market Size (Value - US$ Bn), Analysis, and Forecasts, by Fire Type, 2021-2035

- 11.2.1. Wildland Fires

- 11.2.1.1. Forest Fires

- 11.2.1.2. Grassland Fires

- 11.2.1.3. Brush Fires

- 11.2.1.4. Others

- 11.2.2. Urban-Interface Fires

- 11.2.3. Agricultural Fires

- 11.2.4. Industrial Fires

- 11.2.5. Peat Fires

- 11.2.1. Wildland Fires

- 12. Global Aerial firefighting Market Analysis, by Service Type

- 12.1. Key Segment Analysis

- 12.2. Aerial firefighting Market Size (Value - US$ Bn), Analysis, and Forecasts, by Service Type, 2021-2035

- 12.2.1. Direct Firefighting Services

- 12.2.2. Support Services

- 12.2.2.1. Personnel Transport

- 12.2.2.2. Equipment Transport

- 12.2.2.3. Medical Evacuation

- 12.2.2.4. Others

- 12.2.3. Training and Simulation Services

- 12.2.4. Maintenance and Repair Services

- 13. Global Aerial firefighting Market Analysis and Forecasts, by Region

- 13.1. Key Findings

- 13.2. Aerial firefighting Market Size (Value - US$ Bn), Analysis, and Forecasts, by Region, 2021-2035

- 13.2.1. North America

- 13.2.2. Europe

- 13.2.3. Asia Pacific

- 13.2.4. Middle East

- 13.2.5. Africa

- 13.2.6. South America

- 14. North America Aerial firefighting Market Analysis

- 14.1. Key Segment Analysis

- 14.2. Regional Snapshot

- 14.3. North America Aerial firefighting Market Size (Value - US$ Bn), Analysis, and Forecasts, 2021-2035

- 14.3.1. Aircraft Type

- 14.3.2. Retardant/Suppressant Type

- 14.3.3. Capacity

- 14.3.4. Operation Type

- 14.3.5. Deployment Mode

- 14.3.6. Fire Type

- 14.3.7. Service Type

- 14.3.8. Country

- 14.3.8.1. USA

- 14.3.8.2. Canada

- 14.3.8.3. Mexico

- 14.4. USA Aerial firefighting Market

- 14.4.1. Country Segmental Analysis

- 14.4.2. Aircraft Type

- 14.4.3. Retardant/Suppressant Type

- 14.4.4. Capacity

- 14.4.5. Operation Type

- 14.4.6. Deployment Mode

- 14.4.7. Fire Type

- 14.4.8. Service Type

- 14.5. Canada Aerial firefighting Market

- 14.5.1. Country Segmental Analysis

- 14.5.2. Aircraft Type

- 14.5.3. Retardant/Suppressant Type

- 14.5.4. Capacity

- 14.5.5. Operation Type

- 14.5.6. Deployment Mode

- 14.5.7. Fire Type

- 14.5.8. Service Type

- 14.6. Mexico Aerial firefighting Market

- 14.6.1. Country Segmental Analysis

- 14.6.2. Aircraft Type

- 14.6.3. Retardant/Suppressant Type

- 14.6.4. Capacity

- 14.6.5. Operation Type

- 14.6.6. Deployment Mode

- 14.6.7. Fire Type

- 14.6.8. Service Type

- 15. Europe Aerial firefighting Market Analysis

- 15.1. Key Segment Analysis

- 15.2. Regional Snapshot

- 15.3. Europe Aerial firefighting Market Size (Value - US$ Bn), Analysis, and Forecasts, 2021-2035

- 15.3.1. Aircraft Type

- 15.3.2. Retardant/Suppressant Type

- 15.3.3. Capacity

- 15.3.4. Operation Type

- 15.3.5. Deployment Mode

- 15.3.6. Fire Type

- 15.3.7. Service Type

- 15.3.8. Country

- 15.3.8.1. Germany

- 15.3.8.2. United Kingdom

- 15.3.8.3. France

- 15.3.8.4. Italy

- 15.3.8.5. Spain

- 15.3.8.6. Netherlands

- 15.3.8.7. Nordic Countries

- 15.3.8.8. Poland

- 15.3.8.9. Russia & CIS

- 15.3.8.10. Rest of Europe

- 15.4. Germany Aerial firefighting Market

- 15.4.1. Country Segmental Analysis

- 15.4.2. Aircraft Type

- 15.4.3. Retardant/Suppressant Type

- 15.4.4. Capacity

- 15.4.5. Operation Type

- 15.4.6. Deployment Mode

- 15.4.7. Fire Type

- 15.4.8. Service Type

- 15.5. United Kingdom Aerial firefighting Market

- 15.5.1. Country Segmental Analysis

- 15.5.2. Aircraft Type

- 15.5.3. Retardant/Suppressant Type

- 15.5.4. Capacity

- 15.5.5. Operation Type

- 15.5.6. Deployment Mode

- 15.5.7. Fire Type

- 15.5.8. Service Type

- 15.6. France Aerial firefighting Market

- 15.6.1. Country Segmental Analysis

- 15.6.2. Aircraft Type

- 15.6.3. Retardant/Suppressant Type

- 15.6.4. Capacity

- 15.6.5. Operation Type

- 15.6.6. Deployment Mode

- 15.6.7. Fire Type

- 15.6.8. Service Type

- 15.7. Italy Aerial firefighting Market

- 15.7.1. Country Segmental Analysis

- 15.7.2. Aircraft Type

- 15.7.3. Retardant/Suppressant Type

- 15.7.4. Capacity

- 15.7.5. Operation Type

- 15.7.6. Deployment Mode

- 15.7.7. Fire Type

- 15.7.8. Service Type

- 15.8. Spain Aerial firefighting Market

- 15.8.1. Country Segmental Analysis

- 15.8.2. Aircraft Type

- 15.8.3. Retardant/Suppressant Type

- 15.8.4. Capacity

- 15.8.5. Operation Type

- 15.8.6. Deployment Mode

- 15.8.7. Fire Type

- 15.8.8. Service Type

- 15.9. Netherlands Aerial firefighting Market

- 15.9.1. Country Segmental Analysis

- 15.9.2. Aircraft Type

- 15.9.3. Retardant/Suppressant Type

- 15.9.4. Capacity

- 15.9.5. Operation Type

- 15.9.6. Deployment Mode

- 15.9.7. Fire Type

- 15.9.8. Service Type

- 15.10. Nordic Countries Aerial firefighting Market

- 15.10.1. Country Segmental Analysis

- 15.10.2. Aircraft Type

- 15.10.3. Retardant/Suppressant Type

- 15.10.4. Capacity

- 15.10.5. Operation Type

- 15.10.6. Deployment Mode

- 15.10.7. Fire Type

- 15.10.8. Service Type

- 15.11. Poland Aerial firefighting Market

- 15.11.1. Country Segmental Analysis

- 15.11.2. Aircraft Type

- 15.11.3. Retardant/Suppressant Type

- 15.11.4. Capacity

- 15.11.5. Operation Type

- 15.11.6. Deployment Mode

- 15.11.7. Fire Type

- 15.11.8. Service Type

- 15.12. Russia & CIS Aerial firefighting Market

- 15.12.1. Country Segmental Analysis

- 15.12.2. Aircraft Type

- 15.12.3. Retardant/Suppressant Type

- 15.12.4. Capacity

- 15.12.5. Operation Type

- 15.12.6. Deployment Mode

- 15.12.7. Fire Type

- 15.12.8. Service Type

- 15.13. Rest of Europe Aerial firefighting Market

- 15.13.1. Country Segmental Analysis

- 15.13.2. Aircraft Type

- 15.13.3. Retardant/Suppressant Type

- 15.13.4. Capacity

- 15.13.5. Operation Type

- 15.13.6. Deployment Mode

- 15.13.7. Fire Type

- 15.13.8. Service Type

- 16. Asia Pacific Aerial firefighting Market Analysis

- 16.1. Key Segment Analysis

- 16.2. Regional Snapshot

- 16.3. Asia Pacific Aerial firefighting Market Size (Value - US$ Bn), Analysis, and Forecasts, 2021-2035

- 16.3.1. Aircraft Type

- 16.3.2. Retardant/Suppressant Type

- 16.3.3. Capacity

- 16.3.4. Operation Type

- 16.3.5. Deployment Mode

- 16.3.6. Fire Type

- 16.3.7. Service Type

- 16.3.8. Country

- 16.3.8.1. China

- 16.3.8.2. India

- 16.3.8.3. Japan

- 16.3.8.4. South Korea

- 16.3.8.5. Australia and New Zealand

- 16.3.8.6. Indonesia

- 16.3.8.7. Malaysia

- 16.3.8.8. Thailand

- 16.3.8.9. Vietnam

- 16.3.8.10. Rest of Asia Pacific

- 16.4. China Aerial firefighting Market

- 16.4.1. Country Segmental Analysis

- 16.4.2. Aircraft Type

- 16.4.3. Retardant/Suppressant Type

- 16.4.4. Capacity

- 16.4.5. Operation Type

- 16.4.6. Deployment Mode

- 16.4.7. Fire Type

- 16.4.8. Service Type

- 16.5. India Aerial firefighting Market

- 16.5.1. Country Segmental Analysis

- 16.5.2. Aircraft Type

- 16.5.3. Retardant/Suppressant Type

- 16.5.4. Capacity

- 16.5.5. Operation Type

- 16.5.6. Deployment Mode

- 16.5.7. Fire Type

- 16.5.8. Service Type

- 16.6. Japan Aerial firefighting Market

- 16.6.1. Country Segmental Analysis

- 16.6.2. Aircraft Type

- 16.6.3. Retardant/Suppressant Type

- 16.6.4. Capacity

- 16.6.5. Operation Type

- 16.6.6. Deployment Mode

- 16.6.7. Fire Type

- 16.6.8. Service Type

- 16.7. South Korea Aerial firefighting Market

- 16.7.1. Country Segmental Analysis

- 16.7.2. Aircraft Type

- 16.7.3. Retardant/Suppressant Type

- 16.7.4. Capacity

- 16.7.5. Operation Type

- 16.7.6. Deployment Mode

- 16.7.7. Fire Type

- 16.7.8. Service Type

- 16.8. Australia and New Zealand Aerial firefighting Market

- 16.8.1. Country Segmental Analysis

- 16.8.2. Aircraft Type

- 16.8.3. Retardant/Suppressant Type

- 16.8.4. Capacity

- 16.8.5. Operation Type

- 16.8.6. Deployment Mode

- 16.8.7. Fire Type

- 16.8.8. Service Type

- 16.9. Indonesia Aerial firefighting Market

- 16.9.1. Country Segmental Analysis

- 16.9.2. Aircraft Type

- 16.9.3. Retardant/Suppressant Type

- 16.9.4. Capacity

- 16.9.5. Operation Type

- 16.9.6. Deployment Mode

- 16.9.7. Fire Type

- 16.9.8. Service Type

- 16.10. Malaysia Aerial firefighting Market

- 16.10.1. Country Segmental Analysis

- 16.10.2. Aircraft Type

- 16.10.3. Retardant/Suppressant Type

- 16.10.4. Capacity

- 16.10.5. Operation Type

- 16.10.6. Deployment Mode

- 16.10.7. Fire Type

- 16.10.8. Service Type

- 16.11. Thailand Aerial firefighting Market

- 16.11.1. Country Segmental Analysis

- 16.11.2. Aircraft Type

- 16.11.3. Retardant/Suppressant Type

- 16.11.4. Capacity

- 16.11.5. Operation Type

- 16.11.6. Deployment Mode

- 16.11.7. Fire Type

- 16.11.8. Service Type

- 16.12. Vietnam Aerial firefighting Market

- 16.12.1. Country Segmental Analysis

- 16.12.2. Aircraft Type

- 16.12.3. Retardant/Suppressant Type

- 16.12.4. Capacity

- 16.12.5. Operation Type

- 16.12.6. Deployment Mode

- 16.12.7. Fire Type

- 16.12.8. Service Type

- 16.13. Rest of Asia Pacific Aerial firefighting Market

- 16.13.1. Country Segmental Analysis

- 16.13.2. Aircraft Type

- 16.13.3. Retardant/Suppressant Type

- 16.13.4. Capacity

- 16.13.5. Operation Type

- 16.13.6. Deployment Mode

- 16.13.7. Fire Type

- 16.13.8. Service Type

- 17. Middle East Aerial firefighting Market Analysis

- 17.1. Key Segment Analysis

- 17.2. Regional Snapshot

- 17.3. Middle East Aerial firefighting Market Size (Value - US$ Bn), Analysis, and Forecasts, 2021-2035

- 17.3.1. Aircraft Type

- 17.3.2. Retardant/Suppressant Type

- 17.3.3. Capacity

- 17.3.4. Operation Type

- 17.3.5. Deployment Mode

- 17.3.6. Fire Type

- 17.3.7. Service Type

- 17.3.8. Country

- 17.3.8.1. Turkey

- 17.3.8.2. UAE

- 17.3.8.3. Saudi Arabia

- 17.3.8.4. Israel

- 17.3.8.5. Rest of Middle East

- 17.4. Turkey Aerial firefighting Market

- 17.4.1. Country Segmental Analysis

- 17.4.2. Aircraft Type

- 17.4.3. Retardant/Suppressant Type

- 17.4.4. Capacity

- 17.4.5. Operation Type

- 17.4.6. Deployment Mode

- 17.4.7. Fire Type

- 17.4.8. Service Type

- 17.5. UAE Aerial firefighting Market

- 17.5.1. Country Segmental Analysis

- 17.5.2. Aircraft Type

- 17.5.3. Retardant/Suppressant Type

- 17.5.4. Capacity

- 17.5.5. Operation Type

- 17.5.6. Deployment Mode

- 17.5.7. Fire Type

- 17.5.8. Service Type

- 17.6. Saudi Arabia Aerial firefighting Market

- 17.6.1. Country Segmental Analysis

- 17.6.2. Aircraft Type

- 17.6.3. Retardant/Suppressant Type

- 17.6.4. Capacity

- 17.6.5. Operation Type

- 17.6.6. Deployment Mode

- 17.6.7. Fire Type

- 17.6.8. Service Type

- 17.7. Israel Aerial firefighting Market

- 17.7.1. Country Segmental Analysis

- 17.7.2. Aircraft Type

- 17.7.3. Retardant/Suppressant Type

- 17.7.4. Capacity

- 17.7.5. Operation Type

- 17.7.6. Deployment Mode

- 17.7.7. Fire Type

- 17.7.8. Service Type

- 17.8. Rest of Middle East Aerial firefighting Market

- 17.8.1. Country Segmental Analysis

- 17.8.2. Aircraft Type

- 17.8.3. Retardant/Suppressant Type

- 17.8.4. Capacity

- 17.8.5. Operation Type

- 17.8.6. Deployment Mode

- 17.8.7. Fire Type

- 17.8.8. Service Type

- 18. Africa Aerial firefighting Market Analysis

- 18.1. Key Segment Analysis

- 18.2. Regional Snapshot

- 18.3. Africa Aerial firefighting Market Size (Value - US$ Bn), Analysis, and Forecasts, 2021-2035

- 18.3.1. Aircraft Type

- 18.3.2. Retardant/Suppressant Type

- 18.3.3. Capacity

- 18.3.4. Operation Type

- 18.3.5. Deployment Mode

- 18.3.6. Fire Type

- 18.3.7. Service Type

- 18.3.8. Country

- 18.3.8.1. South Africa

- 18.3.8.2. Egypt

- 18.3.8.3. Nigeria

- 18.3.8.4. Algeria

- 18.3.8.5. Rest of Africa

- 18.4. South Africa Aerial firefighting Market

- 18.4.1. Country Segmental Analysis

- 18.4.2. Aircraft Type

- 18.4.3. Retardant/Suppressant Type

- 18.4.4. Capacity

- 18.4.5. Operation Type

- 18.4.6. Deployment Mode

- 18.4.7. Fire Type

- 18.4.8. Service Type

- 18.5. Egypt Aerial firefighting Market

- 18.5.1. Country Segmental Analysis

- 18.5.2. Aircraft Type

- 18.5.3. Retardant/Suppressant Type

- 18.5.4. Capacity

- 18.5.5. Operation Type

- 18.5.6. Deployment Mode

- 18.5.7. Fire Type

- 18.5.8. Service Type

- 18.6. Nigeria Aerial firefighting Market

- 18.6.1. Country Segmental Analysis

- 18.6.2. Aircraft Type

- 18.6.3. Retardant/Suppressant Type

- 18.6.4. Capacity

- 18.6.5. Operation Type

- 18.6.6. Deployment Mode

- 18.6.7. Fire Type

- 18.6.8. Service Type

- 18.7. Algeria Aerial firefighting Market

- 18.7.1. Country Segmental Analysis

- 18.7.2. Aircraft Type

- 18.7.3. Retardant/Suppressant Type

- 18.7.4. Capacity

- 18.7.5. Operation Type

- 18.7.6. Deployment Mode

- 18.7.7. Fire Type

- 18.7.8. Service Type

- 18.8. Rest of Africa Aerial firefighting Market

- 18.8.1. Country Segmental Analysis

- 18.8.2. Aircraft Type

- 18.8.3. Retardant/Suppressant Type

- 18.8.4. Capacity

- 18.8.5. Operation Type

- 18.8.6. Deployment Mode

- 18.8.7. Fire Type

- 18.8.8. Service Type

- 19. South America Aerial firefighting Market Analysis

- 19.1. Key Segment Analysis

- 19.2. Regional Snapshot

- 19.3. South America Aerial firefighting Market Size (Value - US$ Bn), Analysis, and Forecasts, 2021-2035

- 19.3.1. Aircraft Type

- 19.3.2. Retardant/Suppressant Type

- 19.3.3. Capacity

- 19.3.4. Operation Type

- 19.3.5. Deployment Mode

- 19.3.6. Fire Type

- 19.3.7. Service Type

- 19.3.8. Country

- 19.3.8.1. Brazil

- 19.3.8.2. Argentina

- 19.3.8.3. Rest of South America

- 19.4. Brazil Aerial firefighting Market

- 19.4.1. Country Segmental Analysis

- 19.4.2. Aircraft Type

- 19.4.3. Retardant/Suppressant Type

- 19.4.4. Capacity

- 19.4.5. Operation Type

- 19.4.6. Deployment Mode

- 19.4.7. Fire Type

- 19.4.8. Service Type

- 19.5. Argentina Aerial firefighting Market

- 19.5.1. Country Segmental Analysis

- 19.5.2. Aircraft Type

- 19.5.3. Retardant/Suppressant Type

- 19.5.4. Capacity

- 19.5.5. Operation Type

- 19.5.6. Deployment Mode

- 19.5.7. Fire Type

- 19.5.8. Service Type

- 19.6. Rest of South America Aerial firefighting Market

- 19.6.1. Country Segmental Analysis

- 19.6.2. Aircraft Type

- 19.6.3. Retardant/Suppressant Type

- 19.6.4. Capacity

- 19.6.5. Operation Type

- 19.6.6. Deployment Mode

- 19.6.7. Fire Type

- 19.6.8. Service Type

- 20. Key Players/ Company Profile

- 20.1. Aero-Flite Aerial Firefighting

- 20.1.1. Company Details/ Overview

- 20.1.2. Company Financials

- 20.1.3. Key Customers and Competitors

- 20.1.4. Business/ Industry Portfolio

- 20.1.5. Product Portfolio/ Specification Details

- 20.1.6. Pricing Data

- 20.1.7. Strategic Overview

- 20.1.8. Recent Developments

- 20.2. Air Spray USA

- 20.3. Air Tractor Inc.

- 20.4. Airbus Helicopters

- 20.5. Babcock International Group

- 20.6. BAE Systems

- 20.7. Bell Textron

- 20.8. Bridger Aerospace

- 20.9. Conair Aerial Firefighting

- 20.10. Coulson Aviation

- 20.11. De Havilland Aircraft of Canada Limited

- 20.12. Helicopter Express

- 20.13. Helimax Aviation

- 20.14. Kaman Corporation

- 20.15. Leonardo S.p.A.

- 20.16. Lockheed Martin Corporation

- 20.17. McDermott Aviation

- 20.18. Neptune Aviation Services

- 20.19. Saab AB

- 20.20. Thrush Aircraft LLC

- 20.21. Other Key Players

- 20.1. Aero-Flite Aerial Firefighting

Note* - This is just tentative list of players. While providing the report, we will cover more number of players based on their revenue and share for each geography

Research Design

Our research design integrates both demand-side and supply-side analysis through a balanced combination of primary and secondary research methodologies. By utilizing both bottom-up and top-down approaches alongside rigorous data triangulation methods, we deliver robust market intelligence that supports strategic decision-making.

MarketGenics' comprehensive research design framework ensures the delivery of accurate, reliable, and actionable market intelligence. Through the integration of multiple research approaches, rigorous validation processes, and expert analysis, we provide our clients with the insights needed to make informed strategic decisions and capitalize on market opportunities.

MarketGenics leverages a dedicated industry panel of experts and a comprehensive suite of paid databases to effectively collect, consolidate, and analyze market intelligence.

Our approach has consistently proven to be reliable and effective in generating accurate market insights, identifying key industry trends, and uncovering emerging business opportunities.

Through both primary and secondary research, we capture and analyze critical company-level data such as manufacturing footprints, including technical centers, R&D facilities, sales offices, and headquarters.

Our expert panel further enhances our ability to estimate market size for specific brands based on validated field-level intelligence.

Our data mining techniques incorporate both parametric and non-parametric methods, allowing for structured data collection, sorting, processing, and cleaning.

Demand projections are derived from large-scale data sets analyzed through proprietary algorithms, culminating in robust and reliable market sizing.

Research Approach

The bottom-up approach builds market estimates by starting with the smallest addressable market units and systematically aggregating them to create comprehensive market size projections.

This method begins with specific, granular data points and builds upward to create the complete market landscape.

Customer Analysis → Segmental Analysis → Geographical Analysis

The top-down approach starts with the broadest possible market data and systematically narrows it down through a series of filters and assumptions to arrive at specific market segments or opportunities.

This method begins with the big picture and works downward to increasingly specific market slices.

TAM → SAM → SOM

Research Methods

Desk / Secondary Research

While analysing the market, we extensively study secondary sources, directories, and databases to identify and collect information useful for this technical, market-oriented, and commercial report. Secondary sources that we utilize are not only the public sources, but it is a combination of Open Source, Associations, Paid Databases, MG Repository & Knowledgebase, and others.

- Company websites, annual reports, financial reports, broker reports, and investor presentations

- National government documents, statistical databases and reports

- News articles, press releases and web-casts specific to the companies operating in the market, Magazines, reports, and others

- We gather information from commercial data sources for deriving company specific data such as segmental revenue, share for geography, product revenue, and others

- Internal and external proprietary databases (industry-specific), relevant patent, and regulatory databases

- Governing Bodies, Government Organizations

- Relevant Authorities, Country-specific Associations for Industries

We also employ the model mapping approach to estimate the product level market data through the players' product portfolio

Primary Research

Primary research/ interviews is vital in analyzing the market. Most of the cases involves paid primary interviews. Primary sources include primary interviews through e-mail interactions, telephonic interviews, surveys as well as face-to-face interviews with the different stakeholders across the value chain including several industry experts.

| Type of Respondents | Number of Primaries |

|---|---|

| Tier 2/3 Suppliers | ~20 |

| Tier 1 Suppliers | ~25 |

| End-users | ~25 |

| Industry Expert/ Panel/ Consultant | ~30 |

| Total | ~100 |

MG Knowledgebase

• Repository of industry blog, newsletter and case studies

• Online platform covering detailed market reports, and company profiles

Forecasting Factors and Models

Forecasting Factors

- Historical Trends – Past market patterns, cycles, and major events that shaped how markets behave over time. Understanding past trends helps predict future behavior.

- Industry Factors – Specific characteristics of the industry like structure, regulations, and innovation cycles that affect market dynamics.

- Macroeconomic Factors – Economic conditions like GDP growth, inflation, and employment rates that affect how much money people have to spend.

- Demographic Factors – Population characteristics like age, income, and location that determine who can buy your product.

- Technology Factors – How quickly people adopt new technology and how much technology infrastructure exists.

- Regulatory Factors – Government rules, laws, and policies that can help or restrict market growth.

- Competitive Factors – Analyzing competition structure such as degree of competition and bargaining power of buyers and suppliers.

Forecasting Models / Techniques

Multiple Regression Analysis

- Identify and quantify factors that drive market changes

- Statistical modeling to establish relationships between market drivers and outcomes

Time Series Analysis – Seasonal Patterns

- Understand regular cyclical patterns in market demand

- Advanced statistical techniques to separate trend, seasonal, and irregular components

Time Series Analysis – Trend Analysis

- Identify underlying market growth patterns and momentum

- Statistical analysis of historical data to project future trends

Expert Opinion – Expert Interviews

- Gather deep industry insights and contextual understanding

- In-depth interviews with key industry stakeholders

Multi-Scenario Development

- Prepare for uncertainty by modeling different possible futures

- Creating optimistic, pessimistic, and most likely scenarios

Time Series Analysis – Moving Averages

- Sophisticated forecasting for complex time series data

- Auto-regressive integrated moving average models with seasonal components

Econometric Models

- Apply economic theory to market forecasting

- Sophisticated economic models that account for market interactions

Expert Opinion – Delphi Method

- Harness collective wisdom of industry experts

- Structured, multi-round expert consultation process

Monte Carlo Simulation

- Quantify uncertainty and probability distributions

- Thousands of simulations with varying input parameters

Research Analysis

Our research framework is built upon the fundamental principle of validating market intelligence from both demand and supply perspectives. This dual-sided approach ensures comprehensive market understanding and reduces the risk of single-source bias.

Demand-Side Analysis: We understand end-user/application behavior, preferences, and market needs along with the penetration of the product for specific application.

Supply-Side Analysis: We estimate overall market revenue, analyze the segmental share along with industry capacity, competitive landscape, and market structure.

Validation & Evaluation

Data triangulation is a validation technique that uses multiple methods, sources, or perspectives to examine the same research question, thereby increasing the credibility and reliability of research findings. In market research, triangulation serves as a quality assurance mechanism that helps identify and minimize bias, validate assumptions, and ensure accuracy in market estimates.

- Data Source Triangulation – Using multiple data sources to examine the same phenomenon

- Methodological Triangulation – Using multiple research methods to study the same research question

- Investigator Triangulation – Using multiple researchers or analysts to examine the same data

- Theoretical Triangulation – Using multiple theoretical perspectives to interpret the same data

Custom Market Research Services

We will customise the research for you, in case the report listed above does not meet your requirements.

Get 10% Free Customisation