Aseptic Packaging Market Size, Share & Trends Analysis Report by Package Type (Cartons, Bottles & Cans, Bags & Pouches, Cups & Tubs, Trays, Vials & Ampoules, Others), Packaging Material, Technology/Process, Rated Capacity, Distribution Channel, End-use Industry X Application, and Geography (North America, Europe, Asia Pacific, Middle East, Africa, and South America) – Global Industry Data, Trends, and Forecasts, 2026–2035

|

|

|

Segmental Data Insights |

|

|

Demand Trends |

|

|

Competitive Landscape |

|

|

Strategic Development |

|

|

Future Outlook & Opportunities |

|

Aseptic Packaging Market Size, Share, and Growth

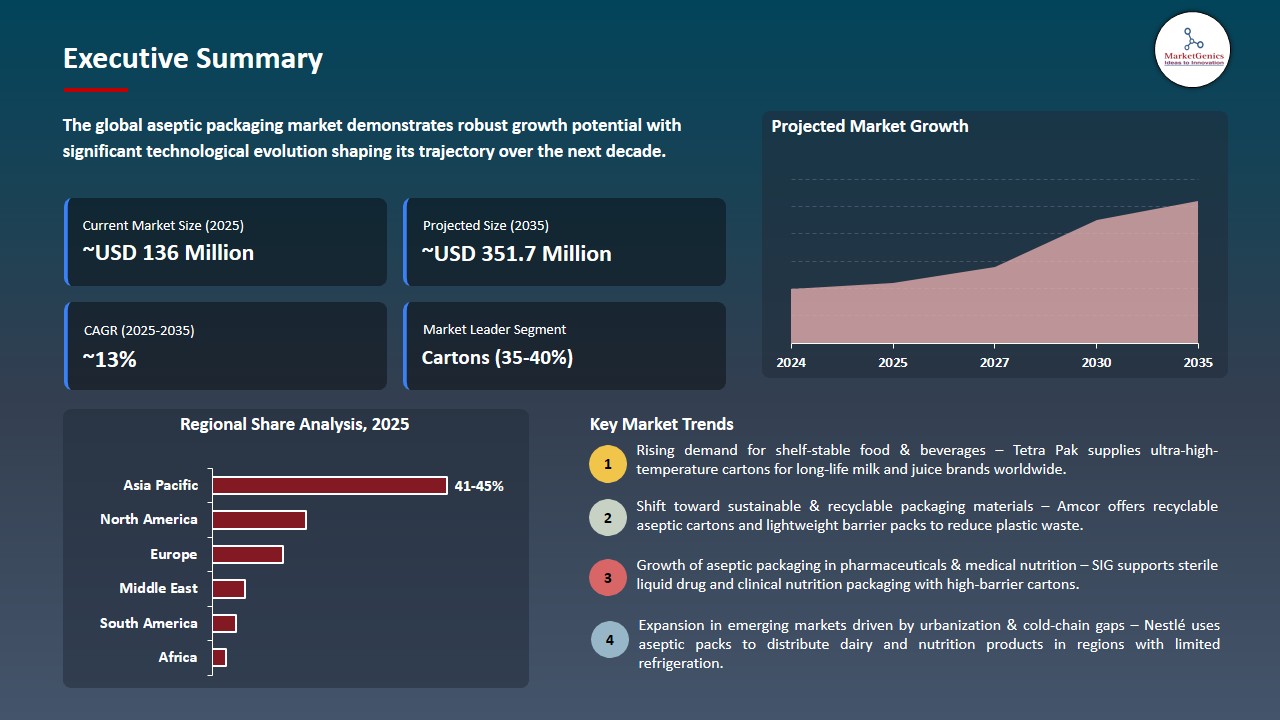

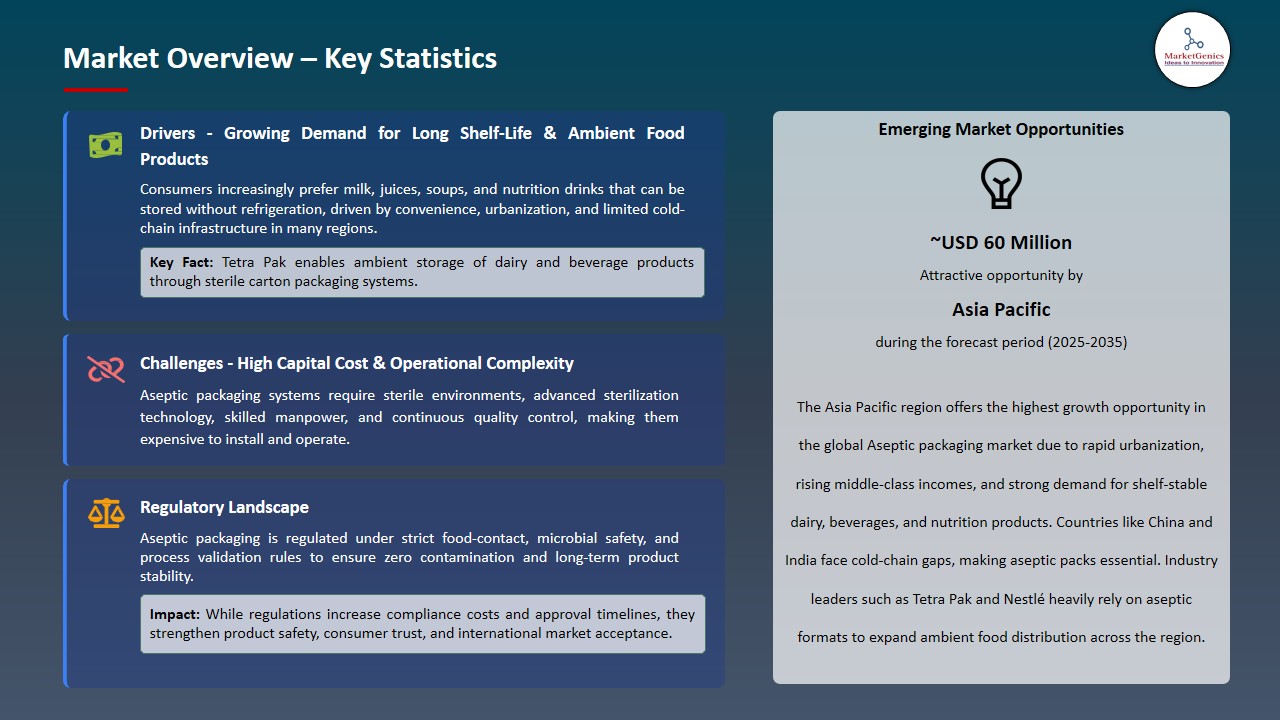

The global aseptic packaging market is experiencing robust growth, with its estimated value of USD 136.8 million in the year 2025 and USD 351.7 million by the period 2035, registering a CAGR of 13.4%, during the forecast period. The global aseptic packaging market is being influenced by the growing demand of safe, convenient, and long shelf life food and beverages solutions among the consumers. Manufacturers are looking to meet the trends of ambient-stable products that do not lose quality through refrigeration, especially in ready-to-drink beverages, dairy and plant-based drinks, and shelf-stable food.

José Matthijsse, President & General Manager Europe at SIG, said: At SIG, one of our goals is to increase the paper content in our aseptic cartons to at least 90% – including the closure – by 2030, allowing further reduction of carbon emissions, and creating a regenerative food packaging system. On the way there, we have developed this packaging structure that is made of more than 80% paper and reduces the number of raw materials from three to two. This breakthrough innovation has the potential to streamline the recycling process for aseptic cartons, only requiring the separation of paperboard and polymers.

The aseptic packaging market is growing at a higher rate in areas of high value and niche use beyond the conventional beverage and dairy products where product safety, shelf stability, and convenience are paramount. The demand is being guided by the increasing consumerism in ready-to-drink beverages, ambient dairy products and long-shelf-life foods especially by the urban population and on the go populations. Aseptic technology is now being exploited by manufacturers to offer high quality products without being refrigerated as a way of offering safe products to the market, allowing them to tap wider market markets and be adopted by more consumers.

The aseptic packaging is focusing product development based on packaging materials, barrier technologies and packaging format. To address both functional and sustainability requirements, multi-layers cartons, foil-free format, and recycling solutions are being embraced. Firms are also designing packaging styles of various products including juices and dairy items to plant based beverages to increase the convenience, portability and usability of the package whilst preserving the integrity of the products during storage and transportation.

The aseptic packaging market is also being oriented by the digital integration, optimization of supply-chains, and sustainability initiatives. These tendencies are placing aseptic packaging as a solution of choice to the present-day food and beverage products, which leads to the repeated buying and brand loyalty as well as the long-term growth of the products and markets in both developed and emerging economies.

Aseptic Packaging Market Dynamics and Trends

Driver: Rising Demand for Shelf-Stable and Convenient Products

-

Aseptic packaging adoption is driven by the increasing trend in consumer preference towards convenience and ready-to-drink drinks and ambient foods. Due to the increasingly busy lifestyles and the continuing need of many to have a long shelf life of products such as juices, plant-based drinks, and ambient dairy, the preference towards the aseptic carton format, which is safe, has a shelf-life and convenient.

- Manufacturers- The manufacturers are countering it with new packaging. For instnace, in July 2025, SIG introduced the first 1-liter aseptic carton in the world manufactured using its own Terra Alu -free + Full barrier, aluminium -free carton that nevertheless provides full barrier protection plus a shelf life of up to 12 months. This illustrates the fact that the increasing demand of convenience, sustainability, and ambient safe storage is being satisfied by the packaging companies thus making aseptic cartons appealing to both the producers and the consumers.

- Aseptic packaging is becoming the preferred option for ready-to-drink and shelf-stable products due to consumer desire for simplicity, safety, and mobility, driving the market growth and product innovation.

Restraint: High Capital and Operational Costs for Aseptic Lines

-

Aseptic packaging has a high capital cost as it inhibits aseptic lines establishment as machines must be installed to fill aseptic packages in multi-layers cartons or pouches, sterilize, and quality control. It might prove to be difficult in investing in these technologies by small and mid-sized manufacturers which restricts entry to the market and slows down adoption in price sensitive markets.

- Growth is also limited by operational costs. Aseptic lines are expensive to operate because they need specialized workforce, high manner of hygiene management, and frequent maintenance of sterilization and filling machines making them costly to run as long-term costs. Compliance with regulations is another cost that manufacturers have to incur because the food industry has strict food safety requirements, such as ISO, HACCP, and local food safety certification, which differ depending on the market.

- High setup and operation costs limit flexibility for experimenting with different pack formats or launching tiny packs. These finance barriers can limit expansion, reduce penetration into new or minor areas, and act as a significant constraint on the market's overall growth.

Opportunity: Expansion into Emerging Markets with Limited Cold-Chain Infrastructure

-

Aseptic packaging has a large growth potential in emerging markets, because of the growing disposable incomes, changing lifestyles, and growing demand of packaged dairy, juices and ready to drink beverages. Where cold-chain services are either inadequate or non-existent in a given region, ambient-safe packaging is necessary to ensure product quality, safety and shelf life, enabling manufacturers to access markets that have been underserved and increase market penetration.

- Some strategies that companies are pursuing to take advantage of this opportunity include the investment in local production plants, improvement of distribution channels, and the packaging that has been designed to suit the local needs. Making strategic investments in manufacturing capacity and logistics support will enable the business to cope with operational problems, lessen reliance on refrigeration, and guarantee a consistent provision of the products.

- Aseptic packaging providers can gain a competitive advantage by adhering to regulatory requirements and catering to consumer demand for convenient, long-shelf-life products. This opportunity positions the industry for long-term growth and value creation in new markets.

Key Trend: Adoption of Sustainable and Recyclable Packaging Solutions

-

The aseptic packaging market is also shifting towards greener and recyclable solutions with manufacturers responding to consumer demands of a sustainable packaging approach, regulatory forces, and corporate ESG requirements. Recyclable cartons, foil-free designs and lightweight multi-layer packaging are transforming the product formats without compromising shelf stability and safety. The innovators have early technological designs and competitive advantages in terms of sustainability and brand perception.

- This tendency can be traced in the recent product innovations. For instance, in January 2025, Tetra Pak, with Lactalis introduced an aseptic carton manufactured with certified recycled polymers, which is a mixture of recycled plastic materials and paperboard to secure total aseptic protection of the milk products. This novelty does not compromise shelf life or product safety as it uses fewer virgin fossils but does not eliminate the need to use them, which points to the movement of the market towards circular-economy and sustainable packaging solutions.

- Sustainable packaging is expected to gain popularity in both mass and high-end markets, allowing for distinction, brand loyalty, and long-term competitive advantage in the aseptic packaging industry.

Aseptic-Packaging-Market Analysis and Segmental Data

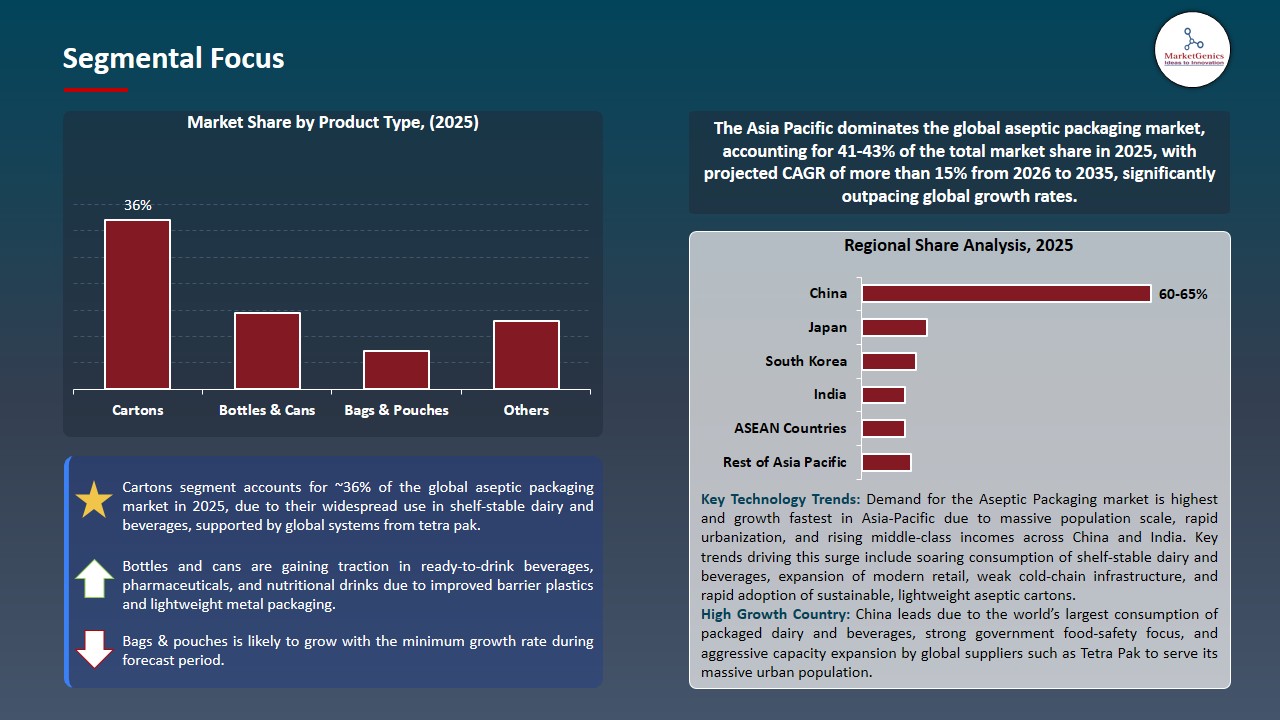

Cartons Dominate Global Aseptic Packaging Market

-

The global aseptic packaging market is dominated by cartons as they offer constant protection to the product by barriers, have a long shelf-life, and retain the products integrity without taking refrigeration. Multi-layered construction, its suitability to sensitive dairy, juice and ready-to-drink beverage formulations and their design efficiency makes them the most opted choice by the manufacturers who need efficient storage at ambient temperatures. Cartons provide a proven and scalable alternative, which enhances the quality of the product and assists in ensuring logistical effectiveness in the supply chains at a global scale.

- Carton preference is indicated in the current product developments and selective innovation. For instance, in May 2025, SIG Combibloc introduced the first alu-layer-free multi-serve beverage full-barrier aseptic carton with a 12-month shelf life, which had a carbon footprint reduction of up to 61% compared to an alu-layered one, yet could work across existing filling lines. This shows that technical reliability, performance, and sustainability of major product launches and packaging solutions are based on the use of cartons even in light of emerging alternatives such as pouches and bottles.

- Cartons are the most widely used aseptic label format globally due to their durability, logistical effectiveness, and ability to consider shelf-life and sustainability.

Asia Pacific Leads Global Aseptic Packaging Market Demand

-

The Asia Pacific leads the aseptic packaging market because of the growing urbanization, rising disposable earnings and boom in the requirements of shelf stable food products and beverages. Consumers are moving towards long shelf life dairy, juices, ready to drink beverages and ambient foods which provide good opportunities to aseptic cartons and pouches. The further increase of the modern retail chains and e-shop services increases the availability of products and the penetration in the regional market.

- Infantile cold-chain infrastructure remains an encouragement to adoption that prompts businesses to invest in local manufacturing. For instance, July 2025, Tetra Pak International S.A. start a second aseptic-carton-manufacturing line at the Binh Duong plant in Vietnam, making an investment of €97 million, increasing the production by more than two times in a year and giving 15 new forms of packaging. This growth enables it to supply faster in Southeast Asia and the rest of the Asia Pacific region, lessen reliance on imports, and increase the efficiency of distribution, and government programs and promotions that support food safety and local manufacturing make it even faster.

- Manufacturers are focusing on sustainable materials, advanced filling technologies, and digital supply-chain monitoring to meet the demand for convenient, hygienic, and eco-friendly packaging and promote regional growth.

Aseptic-Packaging-Market Ecosystem

The global aseptic packaging market is highly consolidated with the existence of giant multinational corporations with regional and specialised players competing in diverse end-use markets and selling products at different price levels. Tetra Pak International S.A., SIG Combibloc Group AG, Amcor plc, Elopak AS, and Uflex Limited are all Tier-1 companies that are well placed in the market courtesy of their economies of scale, futuristic research and development, as well as their wide international distribution networks.

The industry value chain includes suppliers of raw materials, producers of packaging materials, filling equipment, brand owners, logistics partners, retail channels with the support of integrated marketing and digital platforms. The major players are also investing more in verticals, capacity building and sustainable material development to provide supply security and efficiency in operations.

Besides, the increased interest in direct-to-consumer interaction and data-driven brand management is enhancing customer interactions, facilitating product customization, and boosting long-term margin optimization in an incredibly competitive market.

Recent Development and Strategic Overview

-

In February 2025, SIG opened its first plant in Ahmedabad to produce a carton with aseptic filling with a 90 million investment. It has a capacity of at least 4 billion cartons per year whereby it can reinforce local supply in the dairy and beverage sectors in India.

- In September 2024, Tetra Pak introduced its new aseptic carton Tetra Prisma Aseptic 300 Edge, a taller and thinner beverage pack (made out of more than 85 percent renewable material) whose carbon footprint is reduced by approximately 76 percent. Its design is ergonomic, has a tethered closure cap to minimize litter, and is more effective at transportation (up to 10% more units per pallet).

Report Scope

|

Detail |

|

|

Market Size in 2025 |

USD 136.8 Mn |

|

Market Forecast Value in 2035 |

USD 351.7 Mn |

|

Growth Rate (CAGR) |

13.4% |

|

Forecast Period |

2026 – 2035 |

|

Historical Data Available for |

2021 – 2024 |

|

Market Size Units |

US$ Billion for Value |

|

Report Format |

Electronic (PDF) + Excel |

|

North America |

Europe |

Asia Pacific |

Middle East |

Africa |

South America |

|

|

|

|

|

|

|

Companies Covered |

|||||

|

|

|

|

|

|

Aseptic-Packaging-Market Segmentation and Highlights

|

Segment |

Sub-segment |

|

Aseptic Packaging Market, By Package Type |

|

|

Aseptic Packaging Market, By Packaging Material |

|

|

Aseptic Packaging Market, By Technology/Process |

|

|

Aseptic Packaging Market, By Rated Capacity |

|

|

Aseptic Packaging Market, By Distribution Channel |

|

|

Aseptic Packaging Market, By End-use Industry X Application |

|

Frequently Asked Questions

Table of Contents

- 1. Research Methodology and Assumptions

- 1.1. Definitions

- 1.2. Research Design and Approach

- 1.3. Data Collection Methods

- 1.4. Base Estimates and Calculations

- 1.5. Forecasting Models

- 1.5.1. Key Forecast Factors & Impact Analysis

- 1.6. Secondary Research

- 1.6.1. Open Sources

- 1.6.2. Paid Databases

- 1.6.3. Associations

- 1.7. Primary Research

- 1.7.1. Primary Sources

- 1.7.2. Primary Interviews with Stakeholders across Ecosystem

- 2. Executive Summary

- 2.1. Global Aseptic Packaging Market Outlook

- 2.1.1. Aseptic Packaging Market Size Value (US$ Mn), and Forecasts, 2021-2035

- 2.1.2. Compounded Annual Growth Rate Analysis

- 2.1.3. Growth Opportunity Analysis

- 2.1.4. Segmental Share Analysis

- 2.1.5. Geographical Share Analysis

- 2.2. Market Analysis and Facts

- 2.3. Supply-Demand Analysis

- 2.4. Competitive Benchmarking

- 2.5. Go-to- Market Strategy

- 2.5.1. Customer/ End-use Industry Assessment

- 2.5.2. Growth Opportunity Data, 2026-2035

- 2.5.2.1. Regional Data

- 2.5.2.2. Country Data

- 2.5.2.3. Segmental Data

- 2.5.3. Identification of Potential Market Spaces

- 2.5.4. GAP Analysis

- 2.5.5. Potential Attractive Price Points

- 2.5.6. Prevailing Market Risks & Challenges

- 2.5.7. Preferred Sales & Marketing Strategies

- 2.5.8. Key Recommendations and Analysis

- 2.5.9. A Way Forward

- 2.1. Global Aseptic Packaging Market Outlook

- 3. Industry Data and Premium Insights

- 3.1. Global Packaging Industry Overview, 2025

- 3.1.1. Industry Ecosystem Analysis

- 3.1.2. Key Trends for Packaging Industry

- 3.1.3. Regional Distribution for Packaging Industry

- 3.2. Supplier Customer Data

- 3.3. Technology Roadmap and Developments

- 3.4. Trade Analysis

- 3.4.1. Import & Export Analysis, 2025

- 3.4.2. Top Importing Countries

- 3.4.3. Top Exporting Countries

- 3.5. Trump Tariff Impact Analysis

- 3.5.1. Manufacturer

- 3.5.1.1. Based on the component & Raw material

- 3.5.2. Supply Chain

- 3.5.3. End Consumer

- 3.5.1. Manufacturer

- 3.6. Raw Material Analysis

- 3.1. Global Packaging Industry Overview, 2025

- 4. Market Overview

- 4.1. Market Dynamics

- 4.1.1. Drivers

- 4.1.1.1. Rising demand for extended-shelf-life food & beverages without preservatives.

- 4.1.1.2. Growth of ready-to-drink dairy, juices, and functional beverage.

- 4.1.1.3. Expanding food & pharmaceutical packaging requirements in emerging economies.

- 4.1.2. Restraints

- 4.1.2.1. High initial capital investment and equipment costs.

- 4.1.2.2. Recycling challenges due to multi-layer packaging structures.

- 4.1.1. Drivers

- 4.2. Key Trend Analysis

- 4.3. Regulatory Framework

- 4.3.1. Key Regulations, Norms, and Subsidies, by Key Countries

- 4.3.2. Tariffs and Standards

- 4.3.3. Impact Analysis of Regulations on the Market

- 4.4. Value Chain Analysis

- 4.4.1. Raw Material Suppliers

- 4.4.2. Manufacturing

- 4.4.3. Distribution

- 4.4.4. End-Use

- 4.5. Porter’s Five Forces Analysis

- 4.6. PESTEL Analysis

- 4.7. Global Aseptic Packaging Market Demand

- 4.7.1. Historical Market Size –Value (US$ Mn), 2020-2024

- 4.7.2. Current and Future Market Size - Value (US$ Mn), 2026–2035

- 4.7.2.1. Y-o-Y Growth Trends

- 4.7.2.2. Absolute $ Opportunity Assessment

- 4.1. Market Dynamics

- 5. Competition Landscape

- 5.1. Competition structure

- 5.1.1. Fragmented v/s consolidated

- 5.2. Company Share Analysis, 2025

- 5.2.1. Global Company Market Share

- 5.2.2. By Region

- 5.2.2.1. North America

- 5.2.2.2. Europe

- 5.2.2.3. Asia Pacific

- 5.2.2.4. Middle East

- 5.2.2.5. Africa

- 5.2.2.6. South America

- 5.3. Product Comparison Matrix

- 5.3.1. Specifications

- 5.3.2. Market Positioning

- 5.3.3. Pricing

- 5.1. Competition structure

- 6. Global Aseptic Packaging Market Analysis, by Package Type

- 6.1. Key Segment Analysis

- 6.2. Aseptic Packaging Market Size Value (US$ Mn), Analysis, and Forecasts, by Package Type, 2021-2035

- 6.2.1. Cartons

- 6.2.1.1. Brick liquid cartons

- 6.2.1.2. Gable top cartons

- 6.2.1.3. Shaped liquid cartons

- 6.2.1.4. Others

- 6.2.2. Bottles & Cans

- 6.2.2.1. PET bottles

- 6.2.2.2. HDPE bottles

- 6.2.2.3. Glass bottles

- 6.2.2.4. Metal cans

- 6.2.2.5. Others

- 6.2.3. Bags & Pouches

- 6.2.3.1. Stand-up pouches

- 6.2.3.2. Pillow pouches

- 6.2.3.3. Spouted pouches

- 6.2.3.4. Others

- 6.2.4. Cups & Tubs

- 6.2.5. Trays

- 6.2.6. Vials & Ampoules

- 6.2.7. Others

- 6.2.1. Cartons

- 7. Global Aseptic Packaging Market Analysis, by Packaging Material

- 7.1. Key Segment Analysis

- 7.2. Aseptic Packaging Market Size Value (US$ Mn), Analysis, and Forecasts, by Packaging Material, 2021-2035

- 7.2.1. Plastic

- 7.2.1.1. Polyethylene (PE)

- 7.2.1.2. Polypropylene (PP)

- 7.2.1.3. Polyethylene Terephthalate (PET)

- 7.2.1.4. High-Density Polyethylene (HDPE)

- 7.2.1.5. Others

- 7.2.2. Paper & Paperboard

- 7.2.3. Metal

- 7.2.3.1. Aluminum

- 7.2.3.2. Steel

- 7.2.3.3. Others

- 7.2.4. Glass

- 7.2.5. Laminates

- 7.2.6. Multi-layer materials

- 7.2.1. Plastic

- 8. Global Aseptic Packaging Market Analysis, by Technology/Process

- 8.1. Key Segment Analysis

- 8.2. Aseptic Packaging Market Size Value (US$ Mn), Analysis, and Forecasts, by Technology/Process, 2021-2035

- 8.2.1. Form-Fill-Seal (FFS)

- 8.2.2. Blow-Fill-Seal (BFS)

- 8.2.3. Pre-formed containers

- 8.2.4. Thermoforming

- 8.2.5. Hot fill

- 8.2.6. Cold fill

- 9. Global Aseptic Packaging Market Analysis, by Rated Capacity

- 9.1. Key Segment Analysis

- 9.2. Aseptic Packaging Market Size Value (US$ Mn), Analysis, and Forecasts, by Rated Capacity, 2021-2035

- 9.2.1. Up to 250 ml

- 9.2.2. 250 ml - 1 liter

- 9.2.3. 1 liter - 5 liters

- 9.2.4. Above 5 liters

- 9.2.5. Bulk packaging

- 10. Global Aseptic Packaging Market Analysis, by Distribution Channel

- 10.1. Key Segment Analysis

- 10.2. Aseptic Packaging Market Size Value (US$ Mn), Analysis, and Forecasts, by Distribution Channel, 2021-2035

- 10.2.1. Direct sales

- 10.2.2. Distributors

- 10.2.3. Online retail

- 10.2.4. Offline retail

- 11. Global Aseptic Packaging Market Analysis, by End-use Industry X Application

- 11.1. Key Segment Analysis

- 11.2. Aseptic Packaging Market Size Value (US$ Mn), Analysis, and Forecasts, by End-use Industry X Application, 2021-2035

- 11.2.1. Food & Beverage

- 11.2.1.1. Dairy Applications

- 11.2.1.2. Beverage Applications

- 11.2.1.3. Liquid Food Applications

- 11.2.1.4. Others

- 11.2.2. Pharmaceutical Industry

- 11.2.2.1. Injectable Applications

- 11.2.2.2. Parenterals packaging

- 11.2.2.3. IV solutions packaging

- 11.2.2.4. Biologics packaging

- 11.2.2.5. Others

- 11.2.3. Oral Liquid Applications

- 11.2.3.1. Syrups packaging

- 11.2.3.2. Suspensions packaging

- 11.2.3.3. Solutions packaging

- 11.2.3.4. Others

- 11.2.4. Cosmetics & Personal Care Industry

- 11.2.4.1. Liquid cosmetics packaging

- 11.2.4.2. Shampoo & conditioner packaging

- 11.2.4.3. Liquid soap packaging

- 11.2.4.4. Others

- 11.2.5. Chemical Industry

- 11.2.5.1. Laboratory reagents packaging

- 11.2.5.2. Industrial liquids packaging

- 11.2.5.3. Others

- 11.2.1. Food & Beverage

- 12. Global Aseptic Packaging Market Analysis and Forecasts, by Region

- 12.1. Key Findings

- 12.2. Aseptic Packaging Market Size Value (US$ Mn), Analysis, and Forecasts, by Region, 2021-2035

- 12.2.1. North America

- 12.2.2. Europe

- 12.2.3. Asia Pacific

- 12.2.4. Middle East

- 12.2.5. Africa

- 12.2.6. South America

- 13. North America Aseptic Packaging Market Analysis

- 13.1. Key Segment Analysis

- 13.2. Regional Snapshot

- 13.3. North America Aseptic Packaging Market Size- Value (US$ Mn), Analysis, and Forecasts, 2021-2035

- 13.3.1. Package Type

- 13.3.2. Packaging Material

- 13.3.3. Technology/Process

- 13.3.4. Rated Capacity

- 13.3.5. Distribution Channel

- 13.3.6. End-use Industry X Application

- 13.3.7. Country

- 13.3.7.1. USA

- 13.3.7.2. Canada

- 13.3.7.3. Mexico

- 13.4. USA Aseptic Packaging Market

- 13.4.1. Country Segmental Analysis

- 13.4.2. Package Type

- 13.4.3. Packaging Material

- 13.4.4. Technology/Process

- 13.4.5. Rated Capacity

- 13.4.6. Distribution Channel

- 13.4.7. End-use Industry X Application

- 13.5. Canada Aseptic Packaging Market

- 13.5.1. Country Segmental Analysis

- 13.5.2. Package Type

- 13.5.3. Packaging Material

- 13.5.4. Technology/Process

- 13.5.5. Rated Capacity

- 13.5.6. Distribution Channel

- 13.5.7. End-use Industry X Application

- 13.6. Mexico Aseptic Packaging Market

- 13.6.1. Country Segmental Analysis

- 13.6.2. Package Type

- 13.6.3. Packaging Material

- 13.6.4. Technology/Process

- 13.6.5. Rated Capacity

- 13.6.6. Distribution Channel

- 13.6.7. End-use Industry X Application

- 14. Europe Aseptic Packaging Market Analysis

- 14.1. Key Segment Analysis

- 14.2. Regional Snapshot

- 14.3. Europe Aseptic Packaging Market Size Value (US$ Mn), Analysis, and Forecasts, 2021-2035

- 14.3.1. Package Type

- 14.3.2. Packaging Material

- 14.3.3. Technology/Process

- 14.3.4. Rated Capacity

- 14.3.5. Distribution Channel

- 14.3.6. End-use Industry X Application

- 14.3.7. Country

- 14.3.7.1. Germany

- 14.3.7.2. United Kingdom

- 14.3.7.3. France

- 14.3.7.4. Italy

- 14.3.7.5. Spain

- 14.3.7.6. Netherlands

- 14.3.7.7. Nordic Countries

- 14.3.7.8. Poland

- 14.3.7.9. Russia & CIS

- 14.3.7.10. Rest of Europe

- 14.4. Germany Aseptic Packaging Market

- 14.4.1. Country Segmental Analysis

- 14.4.2. Package Type

- 14.4.3. Packaging Material

- 14.4.4. Technology/Process

- 14.4.5. Rated Capacity

- 14.4.6. Distribution Channel

- 14.4.7. End-use Industry X Application

- 14.5. United Kingdom Aseptic Packaging Market

- 14.5.1. Country Segmental Analysis

- 14.5.2. Package Type

- 14.5.3. Packaging Material

- 14.5.4. Technology/Process

- 14.5.5. Rated Capacity

- 14.5.6. Distribution Channel

- 14.5.7. End-use Industry X Application

- 14.6. France Aseptic Packaging Market

- 14.6.1. Country Segmental Analysis

- 14.6.2. Package Type

- 14.6.3. Packaging Material

- 14.6.4. Technology/Process

- 14.6.5. Rated Capacity

- 14.6.6. Distribution Channel

- 14.6.7. End-use Industry X Application

- 14.7. Italy Aseptic Packaging Market

- 14.7.1. Country Segmental Analysis

- 14.7.2. Package Type

- 14.7.3. Packaging Material

- 14.7.4. Technology/Process

- 14.7.5. Rated Capacity

- 14.7.6. Distribution Channel

- 14.7.7. End-use Industry X Application

- 14.8. Spain Aseptic Packaging Market

- 14.8.1. Country Segmental Analysis

- 14.8.2. Package Type

- 14.8.3. Packaging Material

- 14.8.4. Technology/Process

- 14.8.5. Rated Capacity

- 14.8.6. Distribution Channel

- 14.8.7. End-use Industry X Application

- 14.9. Netherlands Aseptic Packaging Market

- 14.9.1. Country Segmental Analysis

- 14.9.2. Package Type

- 14.9.3. Packaging Material

- 14.9.4. Technology/Process

- 14.9.5. Rated Capacity

- 14.9.6. Distribution Channel

- 14.9.7. End-use Industry X Application

- 14.10. Nordic Countries Aseptic Packaging Market

- 14.10.1. Country Segmental Analysis

- 14.10.2. Package Type

- 14.10.3. Packaging Material

- 14.10.4. Technology/Process

- 14.10.5. Rated Capacity

- 14.10.6. Distribution Channel

- 14.10.7. End-use Industry X Application

- 14.11. Poland Aseptic Packaging Market

- 14.11.1. Country Segmental Analysis

- 14.11.2. Package Type

- 14.11.3. Packaging Material

- 14.11.4. Technology/Process

- 14.11.5. Rated Capacity

- 14.11.6. Distribution Channel

- 14.11.7. End-use Industry X Application

- 14.12. Russia & CIS Aseptic Packaging Market

- 14.12.1. Country Segmental Analysis

- 14.12.2. Package Type

- 14.12.3. Packaging Material

- 14.12.4. Technology/Process

- 14.12.5. Rated Capacity

- 14.12.6. Distribution Channel

- 14.12.7. End-use Industry X Application

- 14.13. Rest of Europe Aseptic Packaging Market

- 14.13.1. Country Segmental Analysis

- 14.13.2. Package Type

- 14.13.3. Packaging Material

- 14.13.4. Technology/Process

- 14.13.5. Rated Capacity

- 14.13.6. Distribution Channel

- 14.13.7. End-use Industry X Application

- 15. Asia Pacific Aseptic Packaging Market Analysis

- 15.1. Key Segment Analysis

- 15.2. Regional Snapshot

- 15.3. Asia Pacific Aseptic Packaging Market Size Value (US$ Mn), Analysis, and Forecasts, 2021-2035

- 15.3.1. Package Type

- 15.3.2. Packaging Material

- 15.3.3. Technology/Process

- 15.3.4. Rated Capacity

- 15.3.5. Distribution Channel

- 15.3.6. End-use Industry X Application

- 15.3.7. Country

- 15.3.7.1. China

- 15.3.7.2. India

- 15.3.7.3. Japan

- 15.3.7.4. South Korea

- 15.3.7.5. Australia and New Zealand

- 15.3.7.6. Indonesia

- 15.3.7.7. Malaysia

- 15.3.7.8. Thailand

- 15.3.7.9. Vietnam

- 15.3.7.10. Rest of Asia Pacific

- 15.4. China Aseptic Packaging Market

- 15.4.1. Country Segmental Analysis

- 15.4.2. Package Type

- 15.4.3. Packaging Material

- 15.4.4. Technology/Process

- 15.4.5. Rated Capacity

- 15.4.6. Distribution Channel

- 15.4.7. End-use Industry X Application

- 15.5. India Aseptic Packaging Market

- 15.5.1. Country Segmental Analysis

- 15.5.2. Package Type

- 15.5.3. Packaging Material

- 15.5.4. Technology/Process

- 15.5.5. Rated Capacity

- 15.5.6. Distribution Channel

- 15.5.7. End-use Industry X Application

- 15.6. Japan Aseptic Packaging Market

- 15.6.1. Country Segmental Analysis

- 15.6.2. Package Type

- 15.6.3. Packaging Material

- 15.6.4. Technology/Process

- 15.6.5. Rated Capacity

- 15.6.6. Distribution Channel

- 15.6.7. End-use Industry X Application

- 15.7. South Korea Aseptic Packaging Market

- 15.7.1. Country Segmental Analysis

- 15.7.2. Package Type

- 15.7.3. Packaging Material

- 15.7.4. Technology/Process

- 15.7.5. Rated Capacity

- 15.7.6. Distribution Channel

- 15.7.7. End-use Industry X Application

- 15.8. Australia and New Zealand Aseptic Packaging Market

- 15.8.1. Country Segmental Analysis

- 15.8.2. Package Type

- 15.8.3. Packaging Material

- 15.8.4. Technology/Process

- 15.8.5. Rated Capacity

- 15.8.6. Distribution Channel

- 15.8.7. End-use Industry X Application

- 15.9. Indonesia Aseptic Packaging Market

- 15.9.1. Country Segmental Analysis

- 15.9.2. Package Type

- 15.9.3. Packaging Material

- 15.9.4. Technology/Process

- 15.9.5. Rated Capacity

- 15.9.6. Distribution Channel

- 15.9.7. End-use Industry X Application

- 15.10. Malaysia Aseptic Packaging Market

- 15.10.1. Country Segmental Analysis

- 15.10.2. Package Type

- 15.10.3. Packaging Material

- 15.10.4. Technology/Process

- 15.10.5. Rated Capacity

- 15.10.6. Distribution Channel

- 15.10.7. End-use Industry X Application

- 15.11. Thailand Aseptic Packaging Market

- 15.11.1. Country Segmental Analysis

- 15.11.2. Package Type

- 15.11.3. Packaging Material

- 15.11.4. Technology/Process

- 15.11.5. Rated Capacity

- 15.11.6. Distribution Channel

- 15.11.7. End-use Industry X Application

- 15.12. Vietnam Aseptic Packaging Market

- 15.12.1. Country Segmental Analysis

- 15.12.2. Package Type

- 15.12.3. Packaging Material

- 15.12.4. Technology/Process

- 15.12.5. Rated Capacity

- 15.12.6. Distribution Channel

- 15.12.7. End-use Industry X Application

- 15.13. Rest of Asia Pacific Aseptic Packaging Market

- 15.13.1. Country Segmental Analysis

- 15.13.2. Package Type

- 15.13.3. Packaging Material

- 15.13.4. Technology/Process

- 15.13.5. Rated Capacity

- 15.13.6. Distribution Channel

- 15.13.7. End-use Industry X Application

- 16. Middle East Aseptic Packaging Market Analysis

- 16.1. Key Segment Analysis

- 16.2. Regional Snapshot

- 16.3. Middle East Aseptic Packaging Market Size Value (US$ Mn), Analysis, and Forecasts, 2021-2035

- 16.3.1. Package Type

- 16.3.2. Packaging Material

- 16.3.3. Technology/Process

- 16.3.4. Rated Capacity

- 16.3.5. Distribution Channel

- 16.3.6. End-use Industry X Application

- 16.3.7. Country

- 16.3.7.1. Turkey

- 16.3.7.2. UAE

- 16.3.7.3. Saudi Arabia

- 16.3.7.4. Israel

- 16.3.7.5. Rest of Middle East

- 16.4. Turkey Aseptic Packaging Market

- 16.4.1. Country Segmental Analysis

- 16.4.2. Package Type

- 16.4.3. Packaging Material

- 16.4.4. Technology/Process

- 16.4.5. Rated Capacity

- 16.4.6. Distribution Channel

- 16.4.7. End-use Industry X Application

- 16.5. UAE Aseptic Packaging Market

- 16.5.1. Country Segmental Analysis

- 16.5.2. Package Type

- 16.5.3. Packaging Material

- 16.5.4. Technology/Process

- 16.5.5. Rated Capacity

- 16.5.6. Distribution Channel

- 16.5.7. End-use Industry X Application

- 16.6. Saudi Arabia Aseptic Packaging Market

- 16.6.1. Country Segmental Analysis

- 16.6.2. Package Type

- 16.6.3. Packaging Material

- 16.6.4. Technology/Process

- 16.6.5. Rated Capacity

- 16.6.6. Distribution Channel

- 16.6.7. End-use Industry X Application

- 16.7. Israel Aseptic Packaging Market

- 16.7.1. Country Segmental Analysis

- 16.7.2. Package Type

- 16.7.3. Packaging Material

- 16.7.4. Technology/Process

- 16.7.5. Rated Capacity

- 16.7.6. Distribution Channel

- 16.7.7. End-use Industry X Application

- 16.8. Rest of Middle East Aseptic Packaging Market

- 16.8.1. Country Segmental Analysis

- 16.8.2. Package Type

- 16.8.3. Packaging Material

- 16.8.4. Technology/Process

- 16.8.5. Rated Capacity

- 16.8.6. Distribution Channel

- 16.8.7. End-use Industry X Application

- 17. Africa Aseptic Packaging Market Analysis

- 17.1. Key Segment Analysis

- 17.2. Regional Snapshot

- 17.3. Africa Aseptic Packaging Market Size Value (US$ Mn), Analysis, and Forecasts, 2021-2035

- 17.3.1. Package Type

- 17.3.2. Packaging Material

- 17.3.3. Technology/Process

- 17.3.4. Rated Capacity

- 17.3.5. Distribution Channel

- 17.3.6. End-use Industry X Application

- 17.3.7. End-user/ Customer Type

- 17.3.7.1. South Africa

- 17.3.7.2. Egypt

- 17.3.7.3. Nigeria

- 17.3.7.4. Algeria

- 17.3.7.5. Rest of Africa

- 17.4. South Africa Aseptic Packaging Market

- 17.4.1. Country Segmental Analysis

- 17.4.2. Package Type

- 17.4.3. Packaging Material

- 17.4.4. Technology/Process

- 17.4.5. Rated Capacity

- 17.4.6. Distribution Channel

- 17.4.7. End-use Industry X Application

- 17.5. Egypt Aseptic Packaging Market

- 17.5.1. Country Segmental Analysis

- 17.5.2. Package Type

- 17.5.3. Packaging Material

- 17.5.4. Technology/Process

- 17.5.5. Rated Capacity

- 17.5.6. Distribution Channel

- 17.5.7. End-use Industry X Application

- 17.6. Nigeria Aseptic Packaging Market

- 17.6.1. Country Segmental Analysis

- 17.6.2. Package Type

- 17.6.3. Packaging Material

- 17.6.4. Technology/Process

- 17.6.5. Rated Capacity

- 17.6.6. Distribution Channel

- 17.6.7. End-use Industry X Application

- 17.7. Algeria Aseptic Packaging Market

- 17.7.1. Country Segmental Analysis

- 17.7.2. Package Type

- 17.7.3. Packaging Material

- 17.7.4. Technology/Process

- 17.7.5. Rated Capacity

- 17.7.6. Distribution Channel

- 17.7.7. End-use Industry X Application

- 17.8. Rest of Africa Aseptic Packaging Market

- 17.8.1. Country Segmental Analysis

- 17.8.2. Package Type

- 17.8.3. Packaging Material

- 17.8.4. Technology/Process

- 17.8.5. Rated Capacity

- 17.8.6. Distribution Channel

- 17.8.7. End-use Industry X Application

- 18. South America Aseptic Packaging Market Analysis

- 18.1. Key Segment Analysis

- 18.2. Regional Snapshot

- 18.3. South America Aseptic Packaging Market Size Value (US$ Mn), Analysis, and Forecasts, 2021-2035

- 18.3.1. Package Type

- 18.3.2. Packaging Material

- 18.3.3. Technology/Process

- 18.3.4. Rated Capacity

- 18.3.5. Distribution Channel

- 18.3.6. End-use Industry X Application

- 18.3.7. Country

- 18.3.7.1. Brazil

- 18.3.7.2. Argentina

- 18.3.7.3. Rest of South America

- 18.4. Brazil Aseptic Packaging Market

- 18.4.1. Country Segmental Analysis

- 18.4.2. Package Type

- 18.4.3. Packaging Material

- 18.4.4. Technology/Process

- 18.4.5. Rated Capacity

- 18.4.6. Distribution Channel

- 18.4.7. End-use Industry X Application

- 18.5. Argentina Aseptic Packaging Market

- 18.5.1. Country Segmental Analysis

- 18.5.2. Package Type

- 18.5.3. Packaging Material

- 18.5.4. Technology/Process

- 18.5.5. Rated Capacity

- 18.5.6. Distribution Channel

- 18.5.7. End-use Industry X Application

- 18.6. Rest of South America Aseptic Packaging Market

- 18.6.1. Country Segmental Analysis

- 18.6.2. Package Type

- 18.6.3. Packaging Material

- 18.6.4. Technology/Process

- 18.6.5. Rated Capacity

- 18.6.6. Distribution Channel

- 18.6.7. End-use Industry X Application

- 19. Key Players/ Company Profile

- 19.1. Tetra Pak International S.A.

- 19.1.1. Company Details/ Overview

- 19.1.2. Company Financials

- 19.1.3. Key Customers and Competitors

- 19.1.4. Business/ Industry Portfolio

- 19.1.5. Product Portfolio/ Specification Details

- 19.1.6. Pricing Data

- 19.1.7. Strategic Overview

- 19.1.8. Recent Developments

- 19.2. SIG Combibloc Group AG

- 19.3. Amcor plc

- 19.4. Sealed Air Corporation

- 19.5. Elopak AS

- 19.6. Greatview Aseptic Packaging Company Limited

- 19.7. Scholle IPN (SIG Group)

- 19.8. Becton, Dickinson and Company (BD)

- 19.9. Robert Bosch GmbH (Bosch Packaging Technology)

- 19.10. IPI S.r.l.

- 19.11. Printpack Inc.

- 19.12. Evergreen Packaging LLC

- 19.13. Nippon Paper Industries Co., Ltd.

- 19.14. Lami Packaging Co., Ltd.

- 19.15. Pulisheng Packaging Co., Ltd.

- 19.16. Mondi Group

- 19.17. Uflex Limited

- 19.18. Reynolds Group Holdings

- 19.19. Smurfit Kappa Group

- 19.20. Huhtamaki Oyj

- 19.21. Other Key Players

- 19.1. Tetra Pak International S.A.

Note* - This is just tentative list of players. While providing the report, we will cover more number of players based on their revenue and share for each geography

Research Design

Our research design integrates both demand-side and supply-side analysis through a balanced combination of primary and secondary research methodologies. By utilizing both bottom-up and top-down approaches alongside rigorous data triangulation methods, we deliver robust market intelligence that supports strategic decision-making.

MarketGenics' comprehensive research design framework ensures the delivery of accurate, reliable, and actionable market intelligence. Through the integration of multiple research approaches, rigorous validation processes, and expert analysis, we provide our clients with the insights needed to make informed strategic decisions and capitalize on market opportunities.

MarketGenics leverages a dedicated industry panel of experts and a comprehensive suite of paid databases to effectively collect, consolidate, and analyze market intelligence.

Our approach has consistently proven to be reliable and effective in generating accurate market insights, identifying key industry trends, and uncovering emerging business opportunities.

Through both primary and secondary research, we capture and analyze critical company-level data such as manufacturing footprints, including technical centers, R&D facilities, sales offices, and headquarters.

Our expert panel further enhances our ability to estimate market size for specific brands based on validated field-level intelligence.

Our data mining techniques incorporate both parametric and non-parametric methods, allowing for structured data collection, sorting, processing, and cleaning.

Demand projections are derived from large-scale data sets analyzed through proprietary algorithms, culminating in robust and reliable market sizing.

Research Approach

The bottom-up approach builds market estimates by starting with the smallest addressable market units and systematically aggregating them to create comprehensive market size projections.

This method begins with specific, granular data points and builds upward to create the complete market landscape.

Customer Analysis → Segmental Analysis → Geographical Analysis

The top-down approach starts with the broadest possible market data and systematically narrows it down through a series of filters and assumptions to arrive at specific market segments or opportunities.

This method begins with the big picture and works downward to increasingly specific market slices.

TAM → SAM → SOM

Research Methods

Desk / Secondary Research

While analysing the market, we extensively study secondary sources, directories, and databases to identify and collect information useful for this technical, market-oriented, and commercial report. Secondary sources that we utilize are not only the public sources, but it is a combination of Open Source, Associations, Paid Databases, MG Repository & Knowledgebase, and others.

- Company websites, annual reports, financial reports, broker reports, and investor presentations

- National government documents, statistical databases and reports

- News articles, press releases and web-casts specific to the companies operating in the market, Magazines, reports, and others

- We gather information from commercial data sources for deriving company specific data such as segmental revenue, share for geography, product revenue, and others

- Internal and external proprietary databases (industry-specific), relevant patent, and regulatory databases

- Governing Bodies, Government Organizations

- Relevant Authorities, Country-specific Associations for Industries

We also employ the model mapping approach to estimate the product level market data through the players' product portfolio

Primary Research

Primary research/ interviews is vital in analyzing the market. Most of the cases involves paid primary interviews. Primary sources include primary interviews through e-mail interactions, telephonic interviews, surveys as well as face-to-face interviews with the different stakeholders across the value chain including several industry experts.

| Type of Respondents | Number of Primaries |

|---|---|

| Tier 2/3 Suppliers | ~20 |

| Tier 1 Suppliers | ~25 |

| End-users | ~25 |

| Industry Expert/ Panel/ Consultant | ~30 |

| Total | ~100 |

MG Knowledgebase

• Repository of industry blog, newsletter and case studies

• Online platform covering detailed market reports, and company profiles

Forecasting Factors and Models

Forecasting Factors

- Historical Trends – Past market patterns, cycles, and major events that shaped how markets behave over time. Understanding past trends helps predict future behavior.

- Industry Factors – Specific characteristics of the industry like structure, regulations, and innovation cycles that affect market dynamics.

- Macroeconomic Factors – Economic conditions like GDP growth, inflation, and employment rates that affect how much money people have to spend.

- Demographic Factors – Population characteristics like age, income, and location that determine who can buy your product.

- Technology Factors – How quickly people adopt new technology and how much technology infrastructure exists.

- Regulatory Factors – Government rules, laws, and policies that can help or restrict market growth.

- Competitive Factors – Analyzing competition structure such as degree of competition and bargaining power of buyers and suppliers.

Forecasting Models / Techniques

Multiple Regression Analysis

- Identify and quantify factors that drive market changes

- Statistical modeling to establish relationships between market drivers and outcomes

Time Series Analysis – Seasonal Patterns

- Understand regular cyclical patterns in market demand

- Advanced statistical techniques to separate trend, seasonal, and irregular components

Time Series Analysis – Trend Analysis

- Identify underlying market growth patterns and momentum

- Statistical analysis of historical data to project future trends

Expert Opinion – Expert Interviews

- Gather deep industry insights and contextual understanding

- In-depth interviews with key industry stakeholders

Multi-Scenario Development

- Prepare for uncertainty by modeling different possible futures

- Creating optimistic, pessimistic, and most likely scenarios

Time Series Analysis – Moving Averages

- Sophisticated forecasting for complex time series data

- Auto-regressive integrated moving average models with seasonal components

Econometric Models

- Apply economic theory to market forecasting

- Sophisticated economic models that account for market interactions

Expert Opinion – Delphi Method

- Harness collective wisdom of industry experts

- Structured, multi-round expert consultation process

Monte Carlo Simulation

- Quantify uncertainty and probability distributions

- Thousands of simulations with varying input parameters

Research Analysis

Our research framework is built upon the fundamental principle of validating market intelligence from both demand and supply perspectives. This dual-sided approach ensures comprehensive market understanding and reduces the risk of single-source bias.

Demand-Side Analysis: We understand end-user/application behavior, preferences, and market needs along with the penetration of the product for specific application.

Supply-Side Analysis: We estimate overall market revenue, analyze the segmental share along with industry capacity, competitive landscape, and market structure.

Validation & Evaluation

Data triangulation is a validation technique that uses multiple methods, sources, or perspectives to examine the same research question, thereby increasing the credibility and reliability of research findings. In market research, triangulation serves as a quality assurance mechanism that helps identify and minimize bias, validate assumptions, and ensure accuracy in market estimates.

- Data Source Triangulation – Using multiple data sources to examine the same phenomenon

- Methodological Triangulation – Using multiple research methods to study the same research question

- Investigator Triangulation – Using multiple researchers or analysts to examine the same data

- Theoretical Triangulation – Using multiple theoretical perspectives to interpret the same data

Custom Market Research Services

We will customise the research for you, in case the report listed above does not meet your requirements.

Get 10% Free Customisation