Fiberglass Insulation Market Size, Share & Trends Analysis Report by Product Type (Glass Wool, Continuous Filament Mat, Chopped Strand Mat, Others), Form, Facing Type, Thermal Conductivity (R-Value), Distribution Channel, End-Use, and Geography (North America, Europe, Asia Pacific, Middle East, Africa, and South America) – Global Industry Data, Trends, and Forecasts, 2026–2035

|

|

|

Segmental Data Insights |

|

|

Demand Trends |

|

|

Competitive Landscape |

|

|

Strategic Development |

|

|

Future Outlook & Opportunities |

|

Fiberglass Insulation Market Size, Share, and Growth

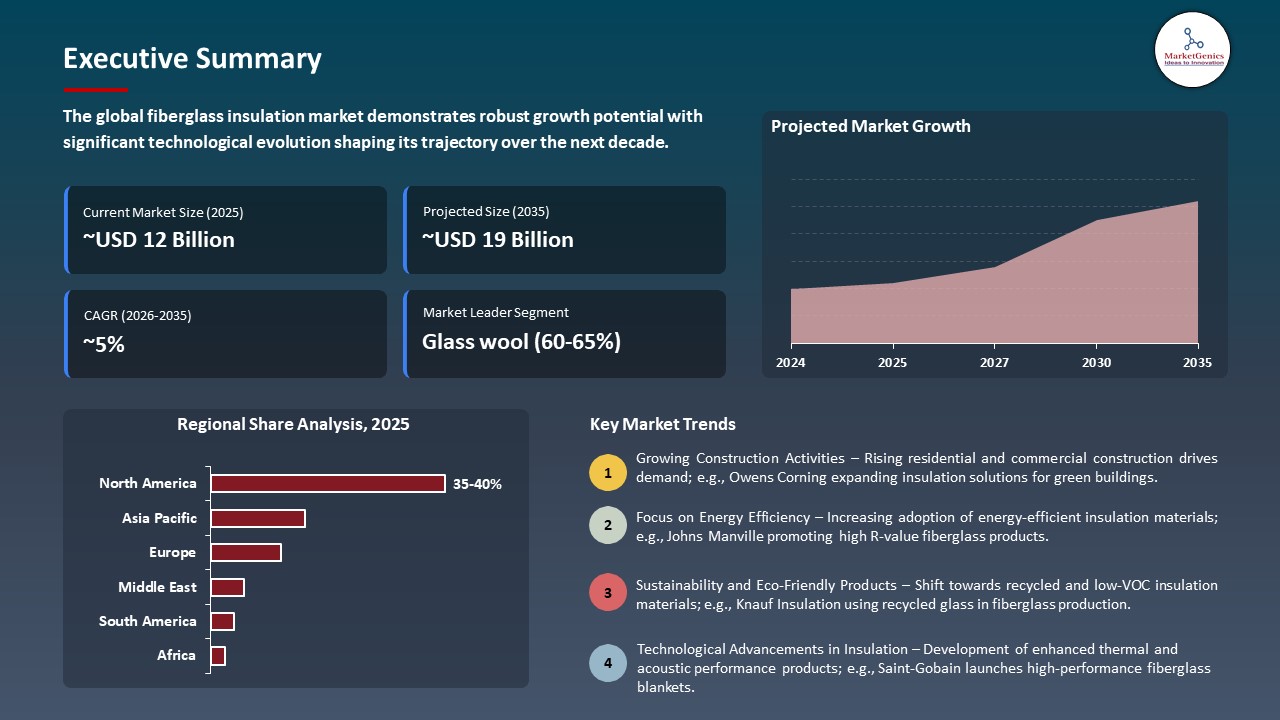

The global fiberglass insulation market is witnessing strong growth, valued at USD 11.8 billion in 2025 and projected to reach USD 18.5 billion by 2035, expanding at a CAGR of 4.6% during the forecast period. Asia Pacific is the fastest-growing fiberglass insulation market due to rapid urbanization, expanding construction activity, rising demand for energy-efficient buildings, supportive building codes, and cost-effective manufacturing across China, India, and Southeast Asia.

Bob Wamboldt, President and CEO of Johns Manville, said, ““Climate Pro insulation continues to see strong growth and demand in the market, This new production line in Winder will help JM meet our customers’ growing demand for blowing wool”.

Fiberglass insulation market is positively impacted by the increasing perception among home owners, architects and builders regarding the advantages of thermal comfort and acoustic performance. Adoption is being encouraged by increasing the information that an effective insulation helps people cut down on their energy use, improve comfort in the building, and limit the amount of noise pollution. This has led to increased demand in fiberglass insulation products in residential, commercial, and industrial construction work all over the world, which is good in facilitating general growth of the market.

The opportunity to introduce insulation systems with smart building technologies and IoT-based energy management systems is an emerging opportunity in the fiberglass insulation market. The high-tech solutions are capable of real-time tracking of the thermal performance, energy consumption, and level of comfort inside, developing high-value applications in residential, commercial, and industrial buildings. Smart insulation systems will have the effect of enhancing market growth by addressing the trends towards energy efficient and technology-oriented constructions in the entire world.

Key adjacent opportunities for the fiberglass insulation market include acoustic insulation solutions, HVAC duct insulation, fire-resistant building materials, energy-efficient building envelopes, and prefabricated construction components. These adjacent markets leverage fiberglass insulation’s thermal and sound-dampening properties. Expansion into these areas strengthens demand resilience, increases application diversity, and supports long-term market growth.

Fiberglass Insulation Market Dynamics and Trends

Fiberglass Insulation Market Dynamics and Trends

Driver: Technological Advancements in Manufacturing

-

The consistent technological innovation in the manufacturing process is actively pushing the fiberglass insulation market to the edge. Automated production lines, refined fiber spinning methods, and better thermal performance methods are among the innovations that are enhancing quality of products, consistency, and durability.

- These developments make fiberglass insulation cheaper, less wasteful, and more energy efficient in the manufacturing process hence it is more affordable and more dependable. Moreover, the manufacturers are also coming up with specially designed insulation products with high-R-value and hybridization to meet various building needs such as residential, commercial, and industrial purposes.

- In February 2025, Johns Manville stated that it will construct a new Climate Pro blowing wool manufacturing unit in Winder, Georgia, to fulfill increased demand of energy efficient blown-in fiberglass insulation. The growth will increase the ability of JM to cater to markets in East Coast and Central U.S. to meet residential energy-saving demands.

- These technological advances allow businesses to comply with more rigorous building codes and sustainability requirements, as well as increase their market presence and competitiveness on the international level.

Restraint: Environmental & Recycling Concerns

-

A major limitation to the fiberglass insulation market is related to environmental and recycling issues related to manufacturing and disposal of fiberglass products. The manufacturing of fiberglass consumes a lot of energy and may also lead to emissions, which makes the manufacturing products have a greater environmental footprint. Government bodies in different jurisdictions are enforcing tougher regulation to restrain emissions, waste and environmental impact and this outcome is setting up more compliance demands on manufacturers.

- The problem of disposing of used or leftover fiberglass insulation also presents challenges because the substance can be disposed of with relative difficulty and the resources to recycle it are few in most locations. Inappropriate disposal may promote landfill accretion and environmental risks, which will further raise the level of regulatory attention. The environmental issues raise the cost of production and operations because the manufacturers are forced to use sustainable production solutions, enhance recycling, and obey the rules.

- This may reduce adoption in cost-conscious markets and limit growth, especially in areas where environmental policies are strict or where there is an increase in awareness about sustainable building practices.

Opportunity: Green & Sustainable Product Innovation

-

The growth and marketing of green and sustainable insulation materials is a major market opportunity in the fiberglass insulation market. Due to the rising environmental consciousness and regulatory demands, manufacturers are also paying more attention to green solutions, like recycled fiberglass, formaldehyde-free formulations, and low-VOC insulation materials.

- These innovations can not only minimise the carbon footprint of buildings; they are also attractive to environmentally conscious consumers, architects and builders seeking to have sustainable construction solutions. Introduction of sustainable fiberglass insulation is also stimulated by green buildings certifications such as LEED and BREEAM which reward eco-friendly and energy efficient practices.

- In April 2025, Knauf Insulation, Inc. added formaldehyde-free pipe and pipe and tank fiberglass insulation to its Performance+ portfolio, certified Asthma and Allergy Friendly and Verified Healthier Air. This introduction emphasizes the sustainable innovation of the products through the enhancement of the quality of indoor air, the minimization of the VOC emissions, and the offering of energy-efficient and eco-friendly residential and industrial insulation systems.

- Investing in sustainable product development enables businesses to draw customers, increase their audience, meet strict regulations, and take advantage of the booming demand of energy saving and environmentally friendly building materials across the globe.

Key Trend: Pre‑Insulated Panels & Hybrid Insulation Solutions

-

A key development in the fiberglass insulation market is the growing use of insulated panels and hybrid insulation systems. These systems are a combination of fiberglass insulation with other materials or are installed insulated into panels, provide better thermal and acoustic performance, are quicker to install, and have consistent coverage in residential and commercial construction.

- Pre-insulated panels make it easier to construct buildings, lessen that of labour, and improve that of power conservation, and thus they prove to be a viable alternative to present-day building developments. Also, there is the possibility of customizing hybrid insulation technologies to a particular use, e.g., walls, roofs and pipelines that broadens the applications of fiberglass insulation.

- In March 2025, Kingspan Insulation Southern Europe introduced a new Therma TA41 polyisocyanurate (PIR) insulation panel, which is aimed at high-performance thermal insulation in building works. The introduction of the product is based on the increasing industry trends to high-technology pre-insulated panel systems and hybrid insulations that have better thermal performance and ease of installation in commercial and residential construction.

- The trend indicates the concern of the industry in terms of innovation, optimization of performance, and adherence to the changing building standards in the world.

Fiberglass-Insulation-Market Analysis and Segmental Data

Fiberglass-Insulation-Market Analysis and Segmental Data

Glass Wool Dominate Global Fiberglass Insulation Market

-

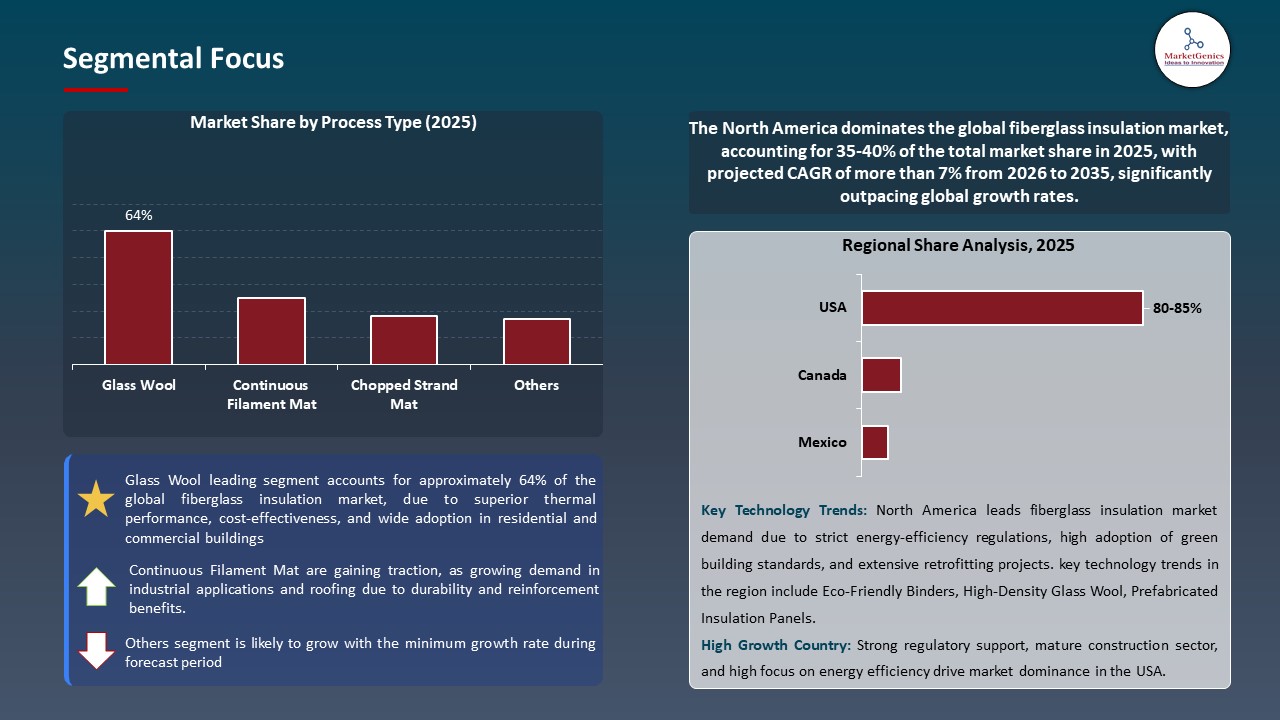

Glass wool dominates the global fiberglass insulation market as the leading segment due to its excellent thermal and acoustic insulation properties, lightweight nature, and cost-effectiveness. It is widely used across residential, commercial, and industrial buildings for walls, roofs, and HVAC systems, supporting energy efficiency and indoor comfort.

- Fire resistivity, moisture control and recyclability of the material are in compliance with high standards of building safety and sustainability. Also, the simple installation, availability, and ongoing product improvements like low dust and formaldehyde free glass wool are also enhancing its adoption, which is making it stronger in terms of leadership in the developed and emerging construction markets of the world.

- In August, 2025, Knauf Insulation declared a significant investment in its Shelbyville, Indiana plant, encompassing a new state-of-the-art pipe production line, improvements to current operations, and a rise in glass capacity to accommodate pipe and blowing wool fiberglass insulation. This project makes manufacturing modernized, enhances production, and incorporates more sustainable and automated technology.

- These inventions and the ability to expand the capacity cement the status of glass wool as the choice of insulation that is preferred, sustainable, and of high performance in the world.

North America Leads Global Fiberglass Insulation Market Demand

-

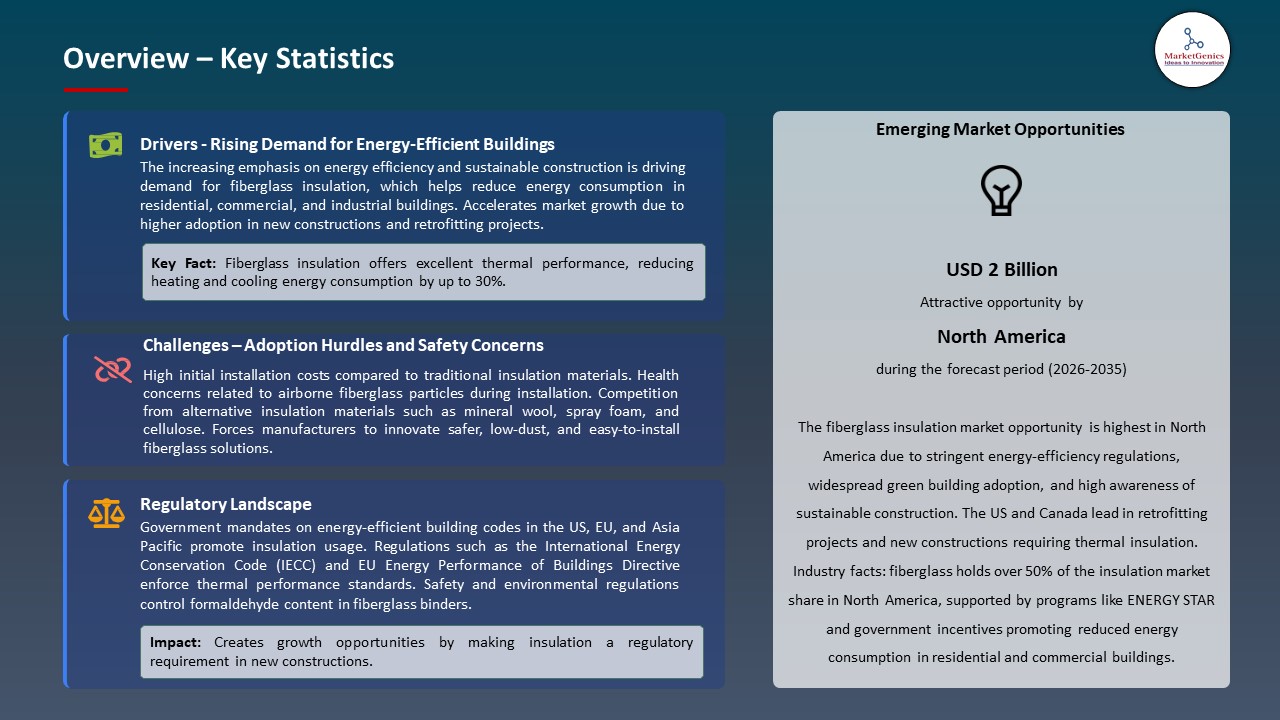

North America dominates the global fiberglass insulation market due to growing investments in energy-efficient residential, commercial, and industrial buildings. Rising awareness of thermal and acoustic insulation benefits, coupled with stringent building energy codes and sustainability regulations, has driven adoption across the U.S. and Canada.

- High-performance fiberglass insulation is increasingly becoming the material of choice in major construction segment areas such as retrofits, new housing and large scale infrastructure projects to save on energy consumption and operational expenses. The growth of the market is also facilitated with the latest technology such as automated production lines, tailor-made products to suit HVAC and piping systems and also sustainable and eco-friendly insulation products.

- Moreover, the construction industry of North America is mature, and the national incentives of the economy to promote green buildings and energy efficiency support the high level of market demand. Growing interest in indoor air quality, fire safety and long-term building performance makes North America the regional market leader in fiberglass insulation in the world.

- These factors collectively reinforce North America’s leadership and sustained demand in the global fiberglass insulation market.

Fiberglass-Insulation-Market Ecosystem

The global fiberglass insulation market is moderately consolidated, with leading players including Owens Corning, Compagnie de Saint-Gobain S.A., Johns Manville, Knauf Gips KG, and China Jushi Co., Ltd. These companies maintain strong competitive positions through extensive manufacturing networks, advanced product portfolios for thermal and acoustic insulation, innovative low-VOC and formaldehyde-free solutions, and the ability to meet stringent building codes and sustainability standards. Their strengths are further reinforced by long-standing relationships with construction firms, distributors, and contractors, as well as global service delivery capabilities and compliance with environmental and safety regulations.

The fiberglass insulation market value chain encompasses raw material procurement, advanced manufacturing processes, product customization for residential, commercial, and industrial applications, distribution to construction sites, installation, and post-installation support including technical guidance and performance verification. These stages ensure consistent product quality, energy efficiency, and compliance with local building codes.

High entry barriers exist due to significant capital investments in manufacturing facilities, adherence to environmental and safety regulations, technological expertise, and established customer trust. Ongoing innovations including formaldehyde-free glass wool, energy-efficient insulation solutions, automated production lines, and sustainable material development are driving product differentiation, enhancing performance, and supporting the market’s sustained growth globally.

Recent Development and Strategic Overview:

Recent Development and Strategic Overview:

-

In September 2025, Saint-Gobain Glass, in partnership with LuxWall, introduced INSIO, a next-generation vacuum glazing solution for energy-efficient buildings in Europe. The product reduces energy loss through windows and façades, supports building decarbonization, and enhances daylighting, marking a significant step in sustainable insulation innovation.

- In April 2025, Arabian Fiberglass Insulation Company (AFICO), part of Gulf Insulation Group and Zamil Industrial, implemented Nanoprecise Sci Corp’s Energy-Centered Predictive Maintenance solution. Leveraging AI and IoT sensors, the system optimizes equipment performance, reduces downtime, and minimizes energy consumption, reinforcing AFICO’s commitment to operational efficiency, sustainability, and smart manufacturing in Saudi Arabia.

Report Scope

|

Detail |

|

|

Market Size in 2025 |

USD 11.8 Bn |

|

Market Forecast Value in 2035 |

USD 18.5 Bn |

|

Growth Rate (CAGR) |

4.6% |

|

Forecast Period |

2026 – 2035 |

|

Historical Data Available for |

2021 – 2024 |

|

Market Size Units |

US$ Billion for Value |

|

Report Format |

Electronic (PDF) + Excel |

|

North America |

Europe |

Asia Pacific |

Middle East |

Africa |

South America |

|

|

|

|

|

|

|

Companies Covered |

|||||

|

|

|

|

|

|

Fiberglass-Insulation-Market Segmentation and Highlights

|

Segment |

Sub-segment |

|

Fiberglass Insulation Market, By Product Type |

|

|

Fiberglass Insulation Market, By Form |

|

|

Fiberglass Insulation Market, By Facing Type |

|

|

Fiberglass Insulation Market, By Thermal Conductivity (R-Value) |

|

|

Fiberglass Insulation Market, By Distribution Channel |

|

|

Fiberglass Insulation Market, By End-use |

|

Frequently Asked Questions

Table of Contents

- 1. Research Methodology and Assumptions

- 1.1. Definitions

- 1.2. Research Design and Approach

- 1.3. Data Collection Methods

- 1.4. Base Estimates and Calculations

- 1.5. Forecasting Models

- 1.5.1. Key Forecast Factors & Impact Analysis

- 1.6. Secondary Research

- 1.6.1. Open Sources

- 1.6.2. Paid Databases

- 1.6.3. Associations

- 1.7. Primary Research

- 1.7.1. Primary Sources

- 1.7.2. Primary Interviews with Stakeholders across Ecosystem

- 2. Executive Summary

- 2.1. Global Fiberglass Insulation Market Outlook

- 2.1.1. Fiberglass Insulation Market Size Value (US$ Bn), and Forecasts, 2021-2035

- 2.1.2. Compounded Annual Growth Rate Analysis

- 2.1.3. Growth Opportunity Analysis

- 2.1.4. Segmental Share Analysis

- 2.1.5. Geographical Share Analysis

- 2.2. Market Analysis and Facts

- 2.3. Supply-Demand Analysis

- 2.4. Competitive Benchmarking

- 2.5. Go-to- Market Strategy

- 2.5.1. Customer/ End-use Industry Assessment

- 2.5.2. Growth Opportunity Data, 2026-2035

- 2.5.2.1. Regional Data

- 2.5.2.2. Country Data

- 2.5.2.3. Segmental Data

- 2.5.3. Identification of Potential Market Spaces

- 2.5.4. GAP Analysis

- 2.5.5. Potential Attractive Price Points

- 2.5.6. Prevailing Market Risks & Challenges

- 2.5.7. Preferred Sales & Marketing Strategies

- 2.5.8. Key Recommendations and Analysis

- 2.5.9. A Way Forward

- 2.1. Global Fiberglass Insulation Market Outlook

- 3. Industry Data and Premium Insights

- 3.1. Global Chemicals & Materials Industry Overview, 2025

- 3.1.1. Chemicals & Materials Industry Ecosystem Analysis

- 3.1.2. Key Trends for Chemicals & Materials Industry

- 3.1.3. Regional Distribution for Chemicals & Materials Industry

- 3.2. Supplier Customer Data

- 3.3. Technology Roadmap and Developments

- 3.4. Trade Analysis

- 3.4.1. Import & Export Analysis, 2025

- 3.4.2. Top Importing Countries

- 3.4.3. Top Exporting Countries

- 3.5. Trump Tariff Impact Analysis

- 3.5.1. Manufacturer

- 3.5.1.1. Based on the component & Raw material

- 3.5.2. Supply Chain

- 3.5.3. End Consumer

- 3.5.1. Manufacturer

- 3.6. Raw Material Analysis

- 3.1. Global Chemicals & Materials Industry Overview, 2025

- 4. Market Overview

- 4.1. Market Dynamics

- 4.1.1. Drivers

- 4.1.1.1. Growing construction and infrastructure activities boosting demand for thermal and acoustic insulation.

- 4.1.1.2. Rising energy efficiency regulations and government initiatives promoting sustainable building materials.

- 4.1.1.3. Increasing awareness of fire-resistant and eco-friendly insulation solutions in residential and commercial sectors.

- 4.1.2. Restraints

- 4.1.2.1. High installation and maintenance costs compared to alternative insulation materials.

- 4.1.2.2. Health and safety concerns related to handling fiberglass, including skin and respiratory irritation.

- 4.1.1. Drivers

- 4.2. Key Trend Analysis

- 4.3. Regulatory Framework

- 4.3.1. Key Regulations, Norms, and Subsidies, by Key Countries

- 4.3.2. Tariffs and Standards

- 4.3.3. Impact Analysis of Regulations on the Market

- 4.4. Value Chain Analysis

- 4.4.1. Raw Material Suppliers

- 4.4.2. Fiberglass Insulation Manufacturers

- 4.4.3. Distribution and Logistics

- 4.4.4. End Users

- 4.5. Porter’s Five Forces Analysis

- 4.6. PESTEL Analysis

- 4.7. Global Fiberglass Insulation Market Demand

- 4.7.1. Historical Market Size – Value (US$ Bn), 2020-2024

- 4.7.2. Current and Future Market Size – Value (US$ Bn), 2026–2035

- 4.7.2.1. Y-o-Y Growth Trends

- 4.7.2.2. Absolute $ Opportunity Assessment

- 4.1. Market Dynamics

- 5. Competition Landscape

- 5.1. Competition structure

- 5.1.1. Fragmented v/s consolidated

- 5.2. Company Share Analysis, 2025

- 5.2.1. Global Company Market Share

- 5.2.2. By Region

- 5.2.2.1. North America

- 5.2.2.2. Europe

- 5.2.2.3. Asia Pacific

- 5.2.2.4. Middle East

- 5.2.2.5. Africa

- 5.2.2.6. South America

- 5.3. Product Comparison Matrix

- 5.3.1. Specifications

- 5.3.2. Market Positioning

- 5.3.3. Pricing

- 5.1. Competition structure

- 6. Global Fiberglass Insulation Market Analysis, by Product Type

- 6.1. Key Segment Analysis

- 6.2. Fiberglass Insulation Market Size Value (US$ Bn), Analysis, and Forecasts, by Product Type, 2021-2035

- 6.2.1. Glass Wool

- 6.2.1.1. Loose-Fill Glass Wool

- 6.2.1.2. Glass Wool Batts

- 6.2.1.3. Glass Wool Rolls

- 6.2.1.4. Glass Wool Boards/Slabs

- 6.2.1.5. Others

- 6.2.2. Continuous Filament Mat

- 6.2.3. Chopped Strand Mat

- 6.2.4. Others

- 6.2.1. Glass Wool

- 7. Global Fiberglass Insulation Market Analysis, by Form

- 7.1. Key Segment Analysis

- 7.2. Fiberglass Insulation Market Size Value (US$ Bn), Analysis, and Forecasts, by Form, 2021-2035

- 7.2.1. Batts and Rolls

- 7.2.2. Loose-Fill/Blown-In

- 7.2.3. Rigid Boards

- 7.2.4. Pre-Formed Shapes

- 7.2.5. Blankets

- 7.2.6. Others

- 8. Global Fiberglass Insulation Market Analysis, by Facing Type

- 8.1. Key Segment Analysis

- 8.2. Fiberglass Insulation Market Size Value (US$ Bn), Analysis, and Forecasts, by Facing Type, 2021-2035

- 8.2.1. Faced Insulation

- 8.2.1.1. Kraft Paper Faced

- 8.2.1.2. Foil Faced

- 8.2.1.3. Vinyl Faced

- 8.2.1.4. Others

- 8.2.2. Unfaced Insulation

- 8.2.1. Faced Insulation

- 9. Global Fiberglass Insulation Market Analysis, by Thermal Conductivity (R-Value)

- 9.1. Key Segment Analysis

- 9.2. Fiberglass Insulation Market Size Value (US$ Bn), Analysis, and Forecasts, by Consumer Gender, 2021-2035

- 9.2.1. R-11 to R-15

- 9.2.2. R-19 to R-21

- 9.2.3. R-25 to R-30

- 9.2.4. R-38 and Above

- 10. Global Fiberglass Insulation Market Analysis, by Distribution Channel

- 10.1. Key Segment Analysis

- 10.2. Fiberglass Insulation Market Size Value (US$ Bn), Analysis, and Forecasts, by Distribution Channel, 2021-2035

- 10.2.1. Direct Sales

- 10.2.2. Distributors

- 10.2.3. Retailers

- 11. Global Fiberglass Insulation Market Analysis, by End-Use

- 11.1. Key Segment Analysis

- 11.2. Fiberglass Insulation Market Size Value (US$ Bn), Analysis, and Forecasts, by End-Use, 2021-2035

- 11.2.1. Residential Buildings

- 11.2.1.1. Wall Insulation

- 11.2.1.2. Roof/Attic Insulation

- 11.2.1.3. Floor Insulation

- 11.2.1.4. Basement Insulation

- 11.2.1.5. Crawl Space Insulation

- 11.2.1.6. Others

- 11.2.2. Commercial Buildings

- 11.2.2.1. Wall Insulation

- 11.2.2.2. Roof Insulation

- 11.2.2.3. HVAC Duct Insulation

- 11.2.2.4. Acoustic Insulation

- 11.2.2.5. Fire Protection

- 11.2.2.6. Others

- 11.2.3. Industrial Facilities

- 11.2.3.1. Equipment Insulation

- 11.2.3.2. Pipe Insulation

- 11.2.3.3. Tank Insulation

- 11.2.3.4. Boiler Insulation

- 11.2.3.5. Furnace Insulation

- 11.2.3.6. Others

- 11.2.4. Infrastructure

- 11.2.4.1. Transportation Infrastructure (Tunnels, Bridges)

- 11.2.4.2. Cold Storage Facilities

- 11.2.4.3. Data Centers

- 11.2.4.4. Warehouses

- 11.2.4.5. Others

- 11.2.5. Automotive & Transportation

- 11.2.5.1. Engine Compartment Insulation

- 11.2.5.2. Cabin Insulation

- 11.2.5.3. Acoustic Insulation

- 11.2.5.4. Firewall Insulation

- 11.2.5.5. Others

- 11.2.6. Aerospace

- 11.2.6.1. Aircraft Fuselage Insulation

- 11.2.6.2. Engine Nacelle Insulation

- 11.2.6.3. Acoustic Damping

- 11.2.6.4. Thermal Barriers

- 11.2.6.5. Others

- 11.2.7. Marine

- 11.2.7.1. Ship Hull Insulation

- 11.2.7.2. Engine Room Insulation

- 11.2.7.3. Cabin Insulation

- 11.2.7.4. Fire-Resistant Barriers

- 11.2.7.5. Others

- 11.2.8. Appliances

- 11.2.8.1. Refrigerator Insulation

- 11.2.8.2. Oven Insulation

- 11.2.8.3. Water Heater Insulation

- 11.2.8.4. HVAC Equipment

- 11.2.8.5. Others

- 11.2.9. Oil & Gas

- 11.2.9.1. Pipeline Insulation

- 11.2.9.2. Refinery Equipment

- 11.2.9.3. Offshore Platform Insulation

- 11.2.9.4. LNG Storage Tanks

- 11.2.9.5. Others

- 11.2.10. Other End-uses

- 11.2.1. Residential Buildings

- 12. Global Fiberglass Insulation Market Analysis and Forecasts, by Region

- 12.1. Key Findings

- 12.2. Fiberglass Insulation Market Size Value (US$ Bn), Analysis, and Forecasts, by Region, 2021-2035

- 12.2.1. North America

- 12.2.2. Europe

- 12.2.3. Asia Pacific

- 12.2.4. Middle East

- 12.2.5. Africa

- 12.2.6. South America

- 13. North America Fiberglass Insulation Market Analysis

- 13.1. Key Segment Analysis

- 13.2. Regional Snapshot

- 13.3. North America Fiberglass Insulation Market Size Value (US$ Bn), Analysis, and Forecasts, 2021-2035

- 13.3.1. Product Type

- 13.3.2. Form

- 13.3.3. Facing Type

- 13.3.4. Thermal Conductivity (R-Value)

- 13.3.5. Distribution Channel

- 13.3.6. End-Use

- 13.3.7. Country

- 13.3.7.1. USA

- 13.3.7.2. Canada

- 13.3.7.3. Mexico

- 13.4. USA Fiberglass Insulation Market

- 13.4.1. Country Segmental Analysis

- 13.4.2. Product Type

- 13.4.3. Form

- 13.4.4. Facing Type

- 13.4.5. Thermal Conductivity (R-Value)

- 13.4.6. Distribution Channel

- 13.4.7. End-Use

- 13.5. Canada Fiberglass Insulation Market

- 13.5.1. Country Segmental Analysis

- 13.5.2. Product Type

- 13.5.3. Form

- 13.5.4. Facing Type

- 13.5.5. Thermal Conductivity (R-Value)

- 13.5.6. Distribution Channel

- 13.5.7. End-Use

- 13.6. Mexico Fiberglass Insulation Market

- 13.6.1. Country Segmental Analysis

- 13.6.2. Product Type

- 13.6.3. Form

- 13.6.4. Facing Type

- 13.6.5. Thermal Conductivity (R-Value)

- 13.6.6. Distribution Channel

- 13.6.7. End-Use

- 14. Europe Fiberglass Insulation Market Analysis

- 14.1. Key Segment Analysis

- 14.2. Regional Snapshot

- 14.3. Europe Fiberglass Insulation Market Size Value (US$ Bn), Analysis, and Forecasts, 2021-2035

- 14.3.1. Product Type

- 14.3.2. Form

- 14.3.3. Facing Type

- 14.3.4. Thermal Conductivity (R-Value)

- 14.3.5. Distribution Channel

- 14.3.6. End-Use

- 14.3.7. Country

- 14.3.7.1. Germany

- 14.3.7.2. United Kingdom

- 14.3.7.3. France

- 14.3.7.4. Italy

- 14.3.7.5. Spain

- 14.3.7.6. Netherlands

- 14.3.7.7. Nordic Countries

- 14.3.7.8. Poland

- 14.3.7.9. Russia & CIS

- 14.3.7.10. Rest of Europe

- 14.4. Germany Fiberglass Insulation Market

- 14.4.1. Country Segmental Analysis

- 14.4.2. Product Type

- 14.4.3. Form

- 14.4.4. Facing Type

- 14.4.5. Thermal Conductivity (R-Value)

- 14.4.6. Distribution Channel

- 14.4.7. End-Use

- 14.5. United Kingdom Fiberglass Insulation Market

- 14.5.1. Country Segmental Analysis

- 14.5.2. Product Type

- 14.5.3. Form

- 14.5.4. Facing Type

- 14.5.5. Thermal Conductivity (R-Value)

- 14.5.6. Distribution Channel

- 14.5.7. End-Use

- 14.6. France Fiberglass Insulation Market

- 14.6.1. Country Segmental Analysis

- 14.6.2. Product Type

- 14.6.3. Form

- 14.6.4. Facing Type

- 14.6.5. Thermal Conductivity (R-Value)

- 14.6.6. Distribution Channel

- 14.6.7. End-Use

- 14.7. Italy Fiberglass Insulation Market

- 14.7.1. Country Segmental Analysis

- 14.7.2. Product Type

- 14.7.3. Form

- 14.7.4. Facing Type

- 14.7.5. Thermal Conductivity (R-Value)

- 14.7.6. Distribution Channel

- 14.7.7. End-Use

- 14.8. Spain Fiberglass Insulation Market

- 14.8.1. Country Segmental Analysis

- 14.8.2. Product Type

- 14.8.3. Form

- 14.8.4. Facing Type

- 14.8.5. Thermal Conductivity (R-Value)

- 14.8.6. Distribution Channel

- 14.8.7. End-Use

- 14.9. Netherlands Fiberglass Insulation Market

- 14.9.1. Country Segmental Analysis

- 14.9.2. Product Type

- 14.9.3. Form

- 14.9.4. Facing Type

- 14.9.5. Thermal Conductivity (R-Value)

- 14.9.6. Distribution Channel

- 14.9.7. End-Use

- 14.10. Nordic Countries Fiberglass Insulation Market

- 14.10.1. Country Segmental Analysis

- 14.10.2. Product Type

- 14.10.3. Form

- 14.10.4. Facing Type

- 14.10.5. Thermal Conductivity (R-Value)

- 14.10.6. Distribution Channel

- 14.10.7. End-Use

- 14.11. Poland Fiberglass Insulation Market

- 14.11.1. Country Segmental Analysis

- 14.11.2. Product Type

- 14.11.3. Form

- 14.11.4. Facing Type

- 14.11.5. Thermal Conductivity (R-Value)

- 14.11.6. Distribution Channel

- 14.11.7. End-Use

- 14.12. Russia & CIS Fiberglass Insulation Market

- 14.12.1. Country Segmental Analysis

- 14.12.2. Product Type

- 14.12.3. Form

- 14.12.4. Facing Type

- 14.12.5. Thermal Conductivity (R-Value)

- 14.12.6. Distribution Channel

- 14.12.7. End-Use

- 14.13. Rest of Europe Fiberglass Insulation Market

- 14.13.1. Country Segmental Analysis

- 14.13.2. Product Type

- 14.13.3. Form

- 14.13.4. Facing Type

- 14.13.5. Thermal Conductivity (R-Value)

- 14.13.6. Distribution Channel

- 14.13.7. End-Use

- 15. Asia Pacific Fiberglass Insulation Market Analysis

- 15.1. Key Segment Analysis

- 15.2. Regional Snapshot

- 15.3. Asia Pacific Fiberglass Insulation Market Size Value (US$ Bn), Analysis, and Forecasts, 2021-2035

- 15.3.1. Product Type

- 15.3.2. Form

- 15.3.3. Facing Type

- 15.3.4. Thermal Conductivity (R-Value)

- 15.3.5. Distribution Channel

- 15.3.6. End-Use

- 15.3.7. Country

- 15.3.7.1. China

- 15.3.7.2. India

- 15.3.7.3. Japan

- 15.3.7.4. South Korea

- 15.3.7.5. Australia and New Zealand

- 15.3.7.6. Indonesia

- 15.3.7.7. Malaysia

- 15.3.7.8. Thailand

- 15.3.7.9. Vietnam

- 15.3.7.10. Rest of Asia Pacific

- 15.4. China Fiberglass Insulation Market

- 15.4.1. Country Segmental Analysis

- 15.4.2. Product Type

- 15.4.3. Form

- 15.4.4. Facing Type

- 15.4.5. Thermal Conductivity (R-Value)

- 15.4.6. Distribution Channel

- 15.4.7. End-Use

- 15.5. India Fiberglass Insulation Market

- 15.5.1. Country Segmental Analysis

- 15.5.2. Product Type

- 15.5.3. Form

- 15.5.4. Facing Type

- 15.5.5. Thermal Conductivity (R-Value)

- 15.5.6. Distribution Channel

- 15.5.7. End-Use

- 15.6. Japan Fiberglass Insulation Market

- 15.6.1. Country Segmental Analysis

- 15.6.2. Product Type

- 15.6.3. Form

- 15.6.4. Facing Type

- 15.6.5. Thermal Conductivity (R-Value)

- 15.6.6. Distribution Channel

- 15.6.7. End-Use

- 15.7. South Korea Fiberglass Insulation Market

- 15.7.1. Country Segmental Analysis

- 15.7.2. Product Type

- 15.7.3. Form

- 15.7.4. Facing Type

- 15.7.5. Thermal Conductivity (R-Value)

- 15.7.6. Distribution Channel

- 15.7.7. End-Use

- 15.8. Australia and New Zealand Fiberglass Insulation Market

- 15.8.1. Country Segmental Analysis

- 15.8.2. Product Type

- 15.8.3. Form

- 15.8.4. Facing Type

- 15.8.5. Thermal Conductivity (R-Value)

- 15.8.6. Distribution Channel

- 15.8.7. End-Use

- 15.9. Indonesia Fiberglass Insulation Market

- 15.9.1. Country Segmental Analysis

- 15.9.2. Product Type

- 15.9.3. Form

- 15.9.4. Facing Type

- 15.9.5. Thermal Conductivity (R-Value)

- 15.9.6. Distribution Channel

- 15.9.7. End-Use

- 15.10. Malaysia Fiberglass Insulation Market

- 15.10.1. Country Segmental Analysis

- 15.10.2. Product Type

- 15.10.3. Form

- 15.10.4. Facing Type

- 15.10.5. Thermal Conductivity (R-Value)

- 15.10.6. Distribution Channel

- 15.10.7. End-Use

- 15.11. Thailand Fiberglass Insulation Market

- 15.11.1. Country Segmental Analysis

- 15.11.2. Product Type

- 15.11.3. Form

- 15.11.4. Facing Type

- 15.11.5. Thermal Conductivity (R-Value)

- 15.11.6. Distribution Channel

- 15.11.7. End-Use

- 15.12. Vietnam Fiberglass Insulation Market

- 15.12.1. Country Segmental Analysis

- 15.12.2. Product Type

- 15.12.3. Form

- 15.12.4. Facing Type

- 15.12.5. Thermal Conductivity (R-Value)

- 15.12.6. Distribution Channel

- 15.12.7. End-Use

- 15.13. Rest of Asia Pacific Fiberglass Insulation Market

- 15.13.1. Country Segmental Analysis

- 15.13.2. Product Type

- 15.13.3. Form

- 15.13.4. Facing Type

- 15.13.5. Thermal Conductivity (R-Value)

- 15.13.6. Distribution Channel

- 15.13.7. End-Use

- 16. Middle East Fiberglass Insulation Market Analysis

- 16.1. Key Segment Analysis

- 16.2. Regional Snapshot

- 16.3. Middle East Fiberglass Insulation Market Size Value (US$ Bn), Analysis, and Forecasts, 2021-2035

- 16.3.1. Product Type

- 16.3.2. Form

- 16.3.3. Facing Type

- 16.3.4. Thermal Conductivity (R-Value)

- 16.3.5. Distribution Channel

- 16.3.6. End-Use

- 16.3.7. Country

- 16.3.7.1. Turkey

- 16.3.7.2. UAE

- 16.3.7.3. Saudi Arabia

- 16.3.7.4. Israel

- 16.3.7.5. Rest of Middle East

- 16.4. Turkey Fiberglass Insulation Market

- 16.4.1. Country Segmental Analysis

- 16.4.2. Product Type

- 16.4.3. Form

- 16.4.4. Facing Type

- 16.4.5. Thermal Conductivity (R-Value)

- 16.4.6. Distribution Channel

- 16.4.7. End-Use

- 16.5. UAE Fiberglass Insulation Market

- 16.5.1. Country Segmental Analysis

- 16.5.2. Product Type

- 16.5.3. Form

- 16.5.4. Facing Type

- 16.5.5. Thermal Conductivity (R-Value)

- 16.5.6. Distribution Channel

- 16.5.7. End-Use

- 16.6. Saudi Arabia Fiberglass Insulation Market

- 16.6.1. Country Segmental Analysis

- 16.6.2. Product Type

- 16.6.3. Form

- 16.6.4. Facing Type

- 16.6.5. Thermal Conductivity (R-Value)

- 16.6.6. Distribution Channel

- 16.6.7. End-Use

- 16.7. Israel Fiberglass Insulation Market

- 16.7.1. Country Segmental Analysis

- 16.7.2. Product Type

- 16.7.3. Form

- 16.7.4. Facing Type

- 16.7.5. Thermal Conductivity (R-Value)

- 16.7.6. Distribution Channel

- 16.7.7. End-Use

- 16.8. Rest of Middle East Fiberglass Insulation Market

- 16.8.1. Country Segmental Analysis

- 16.8.2. Product Type

- 16.8.3. Form

- 16.8.4. Facing Type

- 16.8.5. Thermal Conductivity (R-Value)

- 16.8.6. Distribution Channel

- 16.8.7. End-Use

- 17. Africa Fiberglass Insulation Market Analysis

- 17.1. Key Segment Analysis

- 17.2. Regional Snapshot

- 17.3. Africa Fiberglass Insulation Market Size Value (US$ Bn), Analysis, and Forecasts, 2021-2035

- 17.3.1. Product Type

- 17.3.2. Form

- 17.3.3. Facing Type

- 17.3.4. Thermal Conductivity (R-Value)

- 17.3.5. Distribution Channel

- 17.3.6. End-Use

- 17.3.7. Country

- 17.3.7.1. South Africa

- 17.3.7.2. Egypt

- 17.3.7.3. Nigeria

- 17.3.7.4. Algeria

- 17.3.7.5. Rest of Africa

- 17.4. South Africa Fiberglass Insulation Market

- 17.4.1. Country Segmental Analysis

- 17.4.2. Product Type

- 17.4.3. Form

- 17.4.4. Facing Type

- 17.4.5. Thermal Conductivity (R-Value)

- 17.4.6. Distribution Channel

- 17.4.7. End-Use

- 17.5. Egypt Fiberglass Insulation Market

- 17.5.1. Country Segmental Analysis

- 17.5.2. Product Type

- 17.5.3. Form

- 17.5.4. Facing Type

- 17.5.5. Thermal Conductivity (R-Value)

- 17.5.6. Distribution Channel

- 17.5.7. End-Use

- 17.6. Nigeria Fiberglass Insulation Market

- 17.6.1. Country Segmental Analysis

- 17.6.2. Product Type

- 17.6.3. Form

- 17.6.4. Facing Type

- 17.6.5. Thermal Conductivity (R-Value)

- 17.6.6. Distribution Channel

- 17.6.7. End-Use

- 17.7. Algeria Fiberglass Insulation Market

- 17.7.1. Country Segmental Analysis

- 17.7.2. Product Type

- 17.7.3. Form

- 17.7.4. Facing Type

- 17.7.5. Thermal Conductivity (R-Value)

- 17.7.6. Distribution Channel

- 17.7.7. End-Use

- 17.8. Rest of Africa Fiberglass Insulation Market

- 17.8.1. Country Segmental Analysis

- 17.8.2. Product Type

- 17.8.3. Form

- 17.8.4. Facing Type

- 17.8.5. Thermal Conductivity (R-Value)

- 17.8.6. Distribution Channel

- 17.8.7. End-Use

- 18. South America Fiberglass Insulation Market Analysis

- 18.1. Key Segment Analysis

- 18.2. Regional Snapshot

- 18.3. South America Fiberglass Insulation Market Size Value (US$ Bn), Analysis, and Forecasts, 2021-2035

- 18.3.1. Product Type

- 18.3.2. Form

- 18.3.3. Facing Type

- 18.3.4. Thermal Conductivity (R-Value)

- 18.3.5. Distribution Channel

- 18.3.6. End-Use

- 18.3.7. Country

- 18.3.7.1. Brazil

- 18.3.7.2. Argentina

- 18.3.7.3. Rest of South America

- 18.4. Brazil Fiberglass Insulation Market

- 18.4.1. Country Segmental Analysis

- 18.4.2. Product Type

- 18.4.3. Form

- 18.4.4. Facing Type

- 18.4.5. Thermal Conductivity (R-Value)

- 18.4.6. Distribution Channel

- 18.4.7. End-Use

- 18.5. Argentina Fiberglass Insulation Market

- 18.5.1. Country Segmental Analysis

- 18.5.2. Product Type

- 18.5.3. Form

- 18.5.4. Facing Type

- 18.5.5. Thermal Conductivity (R-Value)

- 18.5.6. Distribution Channel

- 18.5.7. End-Use

- 18.6. Rest of South America Fiberglass Insulation Market

- 18.6.1. Country Segmental Analysis

- 18.6.2. Product Type

- 18.6.3. Form

- 18.6.4. Facing Type

- 18.6.5. Thermal Conductivity (R-Value)

- 18.6.6. Distribution Channel

- 18.6.7. End-Use

- 19. Key Players/ Company Profile

- 19.1. Binani Industries

- 19.1.1. Company Details/ Overview

- 19.1.2. Company Financials

- 19.1.3. Key Customers and Competitors

- 19.1.4. Business/ Industry Portfolio

- 19.1.5. Product Portfolio/ Specification Details

- 19.1.6. Pricing Data

- 19.1.7. Strategic Overview

- 19.1.8. Recent Developments

- 19.2. China Jushi Co., Ltd.

- 19.3. Compagnie de Saint-Gobain S.A.

- 19.4. DBW Advanced Fiber Technologies

- 19.5. GAF Materials Corporation

- 19.6. Guardian Glass

- 19.7. Johns Manville

- 19.8. Knauf Gips KG

- 19.9. Nippon Electric Glass

- 19.10. Owens Corning

- 19.11. Paroc Group

- 19.12. PPG Industries

- 19.13. Sager SpA

- 19.14. Saint-Gobain (CertainTeed)

- 19.15. Shenzhou Energy-Saving Technology Corporation

- 19.16. Superglass Insulation

- 19.17. Taishan Fiberglass Inc.

- 19.18. Taiwan Glass Industry Corporation

- 19.19. Ursa Insulation

- 19.20. Other Key Players

- 19.1. Binani Industries

Note* - This is just tentative list of players. While providing the report, we will cover more number of players based on their revenue and share for each geography

Research Design

Our research design integrates both demand-side and supply-side analysis through a balanced combination of primary and secondary research methodologies. By utilizing both bottom-up and top-down approaches alongside rigorous data triangulation methods, we deliver robust market intelligence that supports strategic decision-making.

MarketGenics' comprehensive research design framework ensures the delivery of accurate, reliable, and actionable market intelligence. Through the integration of multiple research approaches, rigorous validation processes, and expert analysis, we provide our clients with the insights needed to make informed strategic decisions and capitalize on market opportunities.

MarketGenics leverages a dedicated industry panel of experts and a comprehensive suite of paid databases to effectively collect, consolidate, and analyze market intelligence.

Our approach has consistently proven to be reliable and effective in generating accurate market insights, identifying key industry trends, and uncovering emerging business opportunities.

Through both primary and secondary research, we capture and analyze critical company-level data such as manufacturing footprints, including technical centers, R&D facilities, sales offices, and headquarters.

Our expert panel further enhances our ability to estimate market size for specific brands based on validated field-level intelligence.

Our data mining techniques incorporate both parametric and non-parametric methods, allowing for structured data collection, sorting, processing, and cleaning.

Demand projections are derived from large-scale data sets analyzed through proprietary algorithms, culminating in robust and reliable market sizing.

Research Approach

The bottom-up approach builds market estimates by starting with the smallest addressable market units and systematically aggregating them to create comprehensive market size projections.

This method begins with specific, granular data points and builds upward to create the complete market landscape.

Customer Analysis → Segmental Analysis → Geographical Analysis

The top-down approach starts with the broadest possible market data and systematically narrows it down through a series of filters and assumptions to arrive at specific market segments or opportunities.

This method begins with the big picture and works downward to increasingly specific market slices.

TAM → SAM → SOM

Research Methods

Desk / Secondary Research

While analysing the market, we extensively study secondary sources, directories, and databases to identify and collect information useful for this technical, market-oriented, and commercial report. Secondary sources that we utilize are not only the public sources, but it is a combination of Open Source, Associations, Paid Databases, MG Repository & Knowledgebase, and others.

- Company websites, annual reports, financial reports, broker reports, and investor presentations

- National government documents, statistical databases and reports

- News articles, press releases and web-casts specific to the companies operating in the market, Magazines, reports, and others

- We gather information from commercial data sources for deriving company specific data such as segmental revenue, share for geography, product revenue, and others

- Internal and external proprietary databases (industry-specific), relevant patent, and regulatory databases

- Governing Bodies, Government Organizations

- Relevant Authorities, Country-specific Associations for Industries

We also employ the model mapping approach to estimate the product level market data through the players' product portfolio

Primary Research

Primary research/ interviews is vital in analyzing the market. Most of the cases involves paid primary interviews. Primary sources include primary interviews through e-mail interactions, telephonic interviews, surveys as well as face-to-face interviews with the different stakeholders across the value chain including several industry experts.

| Type of Respondents | Number of Primaries |

|---|---|

| Tier 2/3 Suppliers | ~20 |

| Tier 1 Suppliers | ~25 |

| End-users | ~25 |

| Industry Expert/ Panel/ Consultant | ~30 |

| Total | ~100 |

MG Knowledgebase

• Repository of industry blog, newsletter and case studies

• Online platform covering detailed market reports, and company profiles

Forecasting Factors and Models

Forecasting Factors

- Historical Trends – Past market patterns, cycles, and major events that shaped how markets behave over time. Understanding past trends helps predict future behavior.

- Industry Factors – Specific characteristics of the industry like structure, regulations, and innovation cycles that affect market dynamics.

- Macroeconomic Factors – Economic conditions like GDP growth, inflation, and employment rates that affect how much money people have to spend.

- Demographic Factors – Population characteristics like age, income, and location that determine who can buy your product.

- Technology Factors – How quickly people adopt new technology and how much technology infrastructure exists.

- Regulatory Factors – Government rules, laws, and policies that can help or restrict market growth.

- Competitive Factors – Analyzing competition structure such as degree of competition and bargaining power of buyers and suppliers.

Forecasting Models / Techniques

Multiple Regression Analysis

- Identify and quantify factors that drive market changes

- Statistical modeling to establish relationships between market drivers and outcomes

Time Series Analysis – Seasonal Patterns

- Understand regular cyclical patterns in market demand

- Advanced statistical techniques to separate trend, seasonal, and irregular components

Time Series Analysis – Trend Analysis

- Identify underlying market growth patterns and momentum

- Statistical analysis of historical data to project future trends

Expert Opinion – Expert Interviews

- Gather deep industry insights and contextual understanding

- In-depth interviews with key industry stakeholders

Multi-Scenario Development

- Prepare for uncertainty by modeling different possible futures

- Creating optimistic, pessimistic, and most likely scenarios

Time Series Analysis – Moving Averages

- Sophisticated forecasting for complex time series data

- Auto-regressive integrated moving average models with seasonal components

Econometric Models

- Apply economic theory to market forecasting

- Sophisticated economic models that account for market interactions

Expert Opinion – Delphi Method

- Harness collective wisdom of industry experts

- Structured, multi-round expert consultation process

Monte Carlo Simulation

- Quantify uncertainty and probability distributions

- Thousands of simulations with varying input parameters

Research Analysis

Our research framework is built upon the fundamental principle of validating market intelligence from both demand and supply perspectives. This dual-sided approach ensures comprehensive market understanding and reduces the risk of single-source bias.

Demand-Side Analysis: We understand end-user/application behavior, preferences, and market needs along with the penetration of the product for specific application.

Supply-Side Analysis: We estimate overall market revenue, analyze the segmental share along with industry capacity, competitive landscape, and market structure.

Validation & Evaluation

Data triangulation is a validation technique that uses multiple methods, sources, or perspectives to examine the same research question, thereby increasing the credibility and reliability of research findings. In market research, triangulation serves as a quality assurance mechanism that helps identify and minimize bias, validate assumptions, and ensure accuracy in market estimates.

- Data Source Triangulation – Using multiple data sources to examine the same phenomenon

- Methodological Triangulation – Using multiple research methods to study the same research question

- Investigator Triangulation – Using multiple researchers or analysts to examine the same data

- Theoretical Triangulation – Using multiple theoretical perspectives to interpret the same data

Custom Market Research Services

We will customise the research for you, in case the report listed above does not meet your requirements.

Get 10% Free Customisation