Green Building Materials Market Size, Share & Trends Analysis Report by Product Type (Structural Materials, Insulation Materials, Roofing Materials, Flooring Materials, Interior & Exterior Cladding, Windows, Doors & Glazing, Paints, Coatings & Adhesives, Mechanical, Electrical & Plumbing (MEP) Green Materials, Others), Material Type, Construction Type, Sales Channel, End-users, and Geography (North America, Europe, Asia Pacific, Middle East, Africa, and South America) – Global Industry Data, Trends, and Forecasts, 2026–2035

Green Building Materials Market Overview:

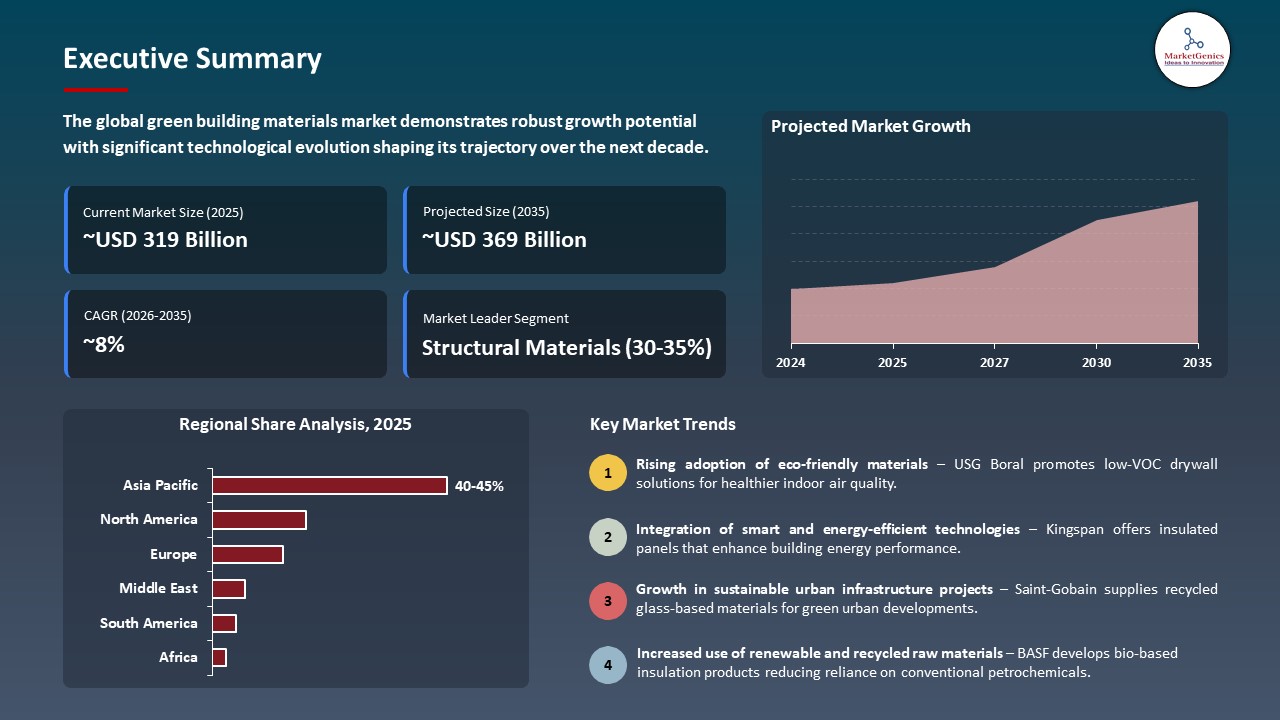

The global green building materials market is exhibiting strong growth, with an estimated value of USD 318.5 billion in 2025 and USD 668.8 billion by 2035, achieving a CAGR of 7.7%, during the forecast period.

|

|

|

Segmental Data Insights |

|

|

Demand Trends |

|

|

Competitive Landscape |

|

|

Strategic Development |

|

|

Future Outlook & Opportunities |

|

Green Building Materials Market Size, Share, and Growth

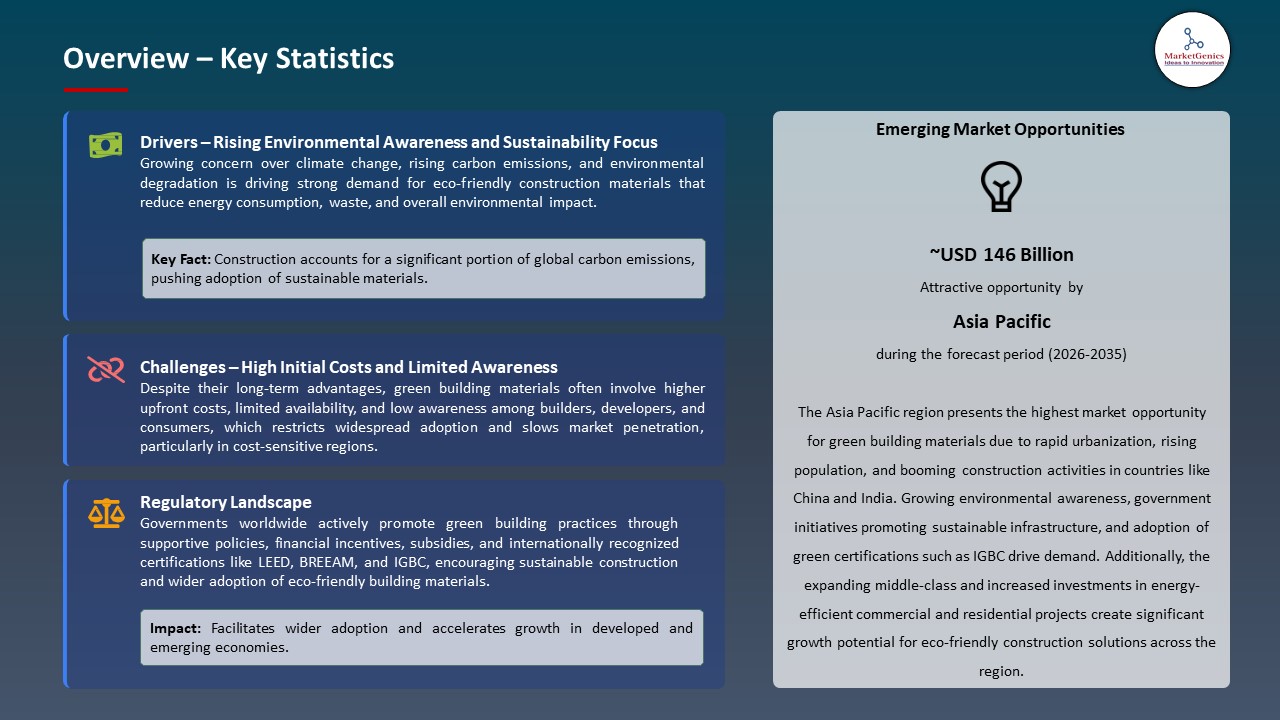

The global green building materials market is driven by stricter environmental regulations, rising energy efficiency and sustainability requirements, growing adoption of eco-friendly construction practices, increasing awareness of carbon footprint reduction, and government incentives promoting renewable, low‑emission, and recyclable building materials.

Miljan Gutovic, Holcim CEO: “Holcim is the leading partner for sustainable construction, and we work with stakeholders across the value chain to deliver innovative and sustainable solutions for our customers. Through our partnership with Alejandro Aravena and the ELEMENTAL team, we have demonstrated how Holcim’s new carbon sink technology can shape the future of construction.”

Rising prioritization of low-embodied-carbon and sustainable construction inputs by developers and manufacturers is driving accelerated adoption of green building materials, as stakeholders seek to reduce lifecycle emissions, enhance energy efficiency, and align projects with corporate decarbonization and sustainability performance targets. For instance, in July 2025, CRH plc completed a US$2.1 billion acquisition of Eco Material Technologies to expand its low-carbon cement and supplementary cementitious materials portfolio and address growing market demand for sustainable construction solutions. This driver is accelerating market expansion while shifting competitive advantage toward manufacturers with scalable low-carbon material technologies.

Moreover, the escalating stringency of environmental regulations and deepening corporate sustainability commitments are driving increased adoption of green building materials, as companies seek regulatory compliance, risk mitigation, and measurable reductions in construction-related environmental impact. For instance, Holcim Group is embedding net-zero-aligned targets into its core strategy while scaling its low-carbon ECOPlanet and ECOPact solutions to advance circular construction and meet regulatory and customer demand for greener materials. This driver is strengthening long-term demand for compliant, low-carbon materials and reinforcing sustainability-led differentiation across the construction value chain.

Key adjacent market opportunities to the global green building materials market include renewable energy integration materials, energy-efficient insulation and envelope systems, circular construction and recycled-content materials, smart building materials with embedded sensors, and water-efficient plumbing and surface solutions, as sustainability-driven construction expands across residential, commercial, and infrastructure sectors. These adjacencies broaden revenue streams, accelerate innovation, and reinforce long-term growth for green material manufacturers.

Green Building Materials Market Dynamics and Trends

Driver: Increasing Focus on End-to-End Lifecycle Carbon Reduction in Construction Materials

-

Regulatory sustainability requirements and growing customer expectations for verifiable lifecycle carbon performance are compelling material manufacturers to move beyond conventional green offerings and systematically integrate low-emission technologies across their product portfolios. This shift is driving intensified investment in solutions that address both embodied carbon and operational environmental impact across the full construction lifecycle.

- The industry’s strategic transition toward high-performance materials that deliver measurable environmental benefits without compromising technical performance. For example, in March 2025, BASF SE, in collaboration with Sika, commercially launched Baxxodur EC 151, an ultra-low-VOC hardener enabling flooring coatings with up to 90% lower VOC emissions versus conventional solutions and designed to support compliance with leading green building standards.

- Accelerated focus on lifecycle carbon performance is boosting demand for advanced sustainable materials and reinforcing competitive advantage for manufacturers with scalable low-carbon innovations.

Restraint: Cost and Supply Chain Constraints Limiting Large-Scale Adoption

-

Elevated production costs and volatility in raw material pricing for advanced green building materials continue to constrain large-scale adoption, particularly across price-sensitive construction segments. Many low-carbon cement formulations, high-performance recycled composites, and specialty sustainable inputs command a premium relative to conventional materials and rely on supply chains that remain underdeveloped, fragmented, or geographically concentrated, increasing procurement risk and lead times.

- These structural cost and supply challenges restrict penetration in high-volume applications such as affordable housing and public infrastructure, where short-term capital expenditure considerations frequently outweigh long-term sustainability returns. To mitigate these barriers, manufacturers and stakeholders are increasingly pursuing localized sourcing, process optimization, and strategic partnerships to improve cost efficiency and supply reliability.

- Cost and supply limitations may temper near-term market expansion and necessitate targeted strategies to align sustainability objectives with commercial viability.

Opportunity: Growth of Circular Construction and Recycled Content Materials Market

-

The accelerating shift toward circular construction models is creating substantial opportunity for materials derived from recycled and recovered waste streams, as the industry prioritizes resource efficiency, waste reduction, and lower embodied carbon. Demand is increasing for products that integrate recycled content while maintaining performance parity with conventional materials, supporting both regulatory compliance and corporate sustainability objectives.

- For instance, in December 2025, Holcim Ltd announced the acquisition of three recycling businesses across the UK, Germany, and France to convert demolition waste into construction-grade inputs, adding more than 1.3 million tons of recycling capacity and advancing its target to recycle 20 million tons of materials annually by 2030.

- Circular construction materials create new revenue pathways, support compliance with tightening sustainability requirements, and reduce dependence on virgin raw materials.

Key Trend: Comprehensive Corporate Sustainability Programs Driving Product Innovation

-

Sustainability is being institutionalized as a core strategic pillar across leading building material manufacturers, with corporate environmental commitments increasingly shaping product development priorities, capital allocation decisions, and long-term growth roadmaps. Innovation pipelines are progressively aligned with defined decarbonization, resource efficiency, and circularity targets, reflecting heightened expectations from regulators, customers, and the investment community.

- For example, Kingspan Group plc continues to advance its long-term Planet Passionate sustainability programme, focused on achieving ambitious carbon, energy, water, and circularity objectives by 2030, including expanding recycled PET usage and enhancing the thermal performance of insulation solutions. This approach demonstrates how structured sustainability frameworks are translating directly into differentiated, high-performance green product portfolios.

- Strategic integration of sustainability is accelerating innovation cycles and reinforcing competitive differentiation, shaping future portfolios toward deeper and measurable environmental performance.

Green Building Materials Market Analysis and Segmental Data

Structural Materials Dominate Global Green Building Materials Market

-

The structural materials segment dominates the global green building materials market because they constitute the core load‑bearing and foundational components of buildings, accounting for the largest share by revenue and use. Structural products such as low‑carbon concrete, recycled steel, engineered timber, and composites are essential for meeting safety standards while substantially reducing a building’s embodied carbon throughout its lifecycle.

- For instance, Holcim’s low‑carbon concrete range “ECOPact”, which reduces embodied CO₂ by at least 30% compared with traditional concrete without sacrificing performance, and is available across more than 30 global markets demonstrating the critical role structural solutions play in decarbonizing construction.

- structural materials lead demand because they directly address both environmental targets and fundamental construction requirements, making them central to sustainable building strategies worldwide.

Asia Pacific Leads Global Green Building Materials Market Demand

-

Asia Pacific leads the green building materials market, because of major manufacturers are responding with tailored regional offerings that drive green material adoption. For instance, Saint‑Gobain Glass launched India’s first low‑carbon glass, reducing carbon footprint by ~40% compared with conventional glass, supporting energy‑efficient building façades and lowering embodied emissions in construction.

- Additionally, leading suppliers are boosting local production in Asia Pacific to enhance availability of sustainable materials and accelerate adoption of low‑carbon, energy-efficient construction solutions. For instance, in February 2026, BASF SE announced expansion of its Mangalore dispersions plant in India to supply low‑VOC architectural coatings and advanced construction chemicals, improving regional supply and sustainable material availability.

- These initiatives are accelerating the adoption of eco-friendly construction practices, reducing regional carbon emissions, and strengthening the supply chain for sustainable materials, thereby positioning Asia Pacific as the fastest-growing hub in the global green building materials market.

Green Building Materials Market Ecosystem

The global green building materials market is highly fragmented, with major players such as Saint‑Gobain S.A., Holcim Group, Kingspan Group plc, Owens Corning, and BASF SE dominating through extensive global footprints and advanced technologies in low‑carbon and sustainable materials. These leaders leverage innovation, digitalization, and sustainability certifications to maintain competitive advantage amid rising environmental regulations and certification demands.

Key players are increasingly focusing on specialized solutions and technologies to drive innovation. This includes high-performance insulation systems, low-VOC coatings, solar-integrated roofing, and recycled or bio-based construction products that enhance energy efficiency and lifecycle sustainability. Their strategic product development supports niche market demands such as net-zero buildings and circular economy initiatives.

Government bodies, institutions, and R&D organizations also play a pivotal role in advancing technologies across the sector. For instance, in August 2025, the Indian Institute of Technology Kanpur (IIT-Kanpur) initiated a LEED Platinum‑certified, net-zero energy building project incorporating engineered wood and mycelium-based materials, accelerating research collaboration and sustainable construction practices.

These combined efforts are driving the adoption of eco-friendly construction practices, reducing carbon emissions, and promoting scalable, high-performance sustainable materials, positioning the market for long-term growth and environmental resilience.

Recent Development and Strategic Overview:

Recent Development and Strategic Overview:

- In January 2025, Saint‑Gobain introduced Gyproc SoundBloc Infinaé 100, the company’s inaugural plasterboard manufactured entirely from recycled plaster in the UK, enhancing circular economy initiatives and advancing sustainable construction by transforming construction waste into high‑performance building solutions.

- In April 2024, Holcim introduced Vertua Ultra Zero, a carbon‑neutral concrete solution featuring advanced mix design and integrated carbon offsetting, aimed at supporting net‑zero construction initiatives and broadening the company’s global portfolio of sustainable concrete products.

Report Scope

|

Detail |

|

|

Market Size in 2025 |

USD 318.5 Bn |

|

Market Forecast Value in 2035 |

USD 668.8 Bn |

|

Growth Rate (CAGR) |

7.7% |

|

Forecast Period |

2026 – 2035 |

|

Historical Data Available for |

2021 – 2024 |

|

Market Size Units |

US$ Billion for Value |

|

Report Format |

Electronic (PDF) + Excel |

|

North America |

Europe |

Asia Pacific |

Middle East |

Africa |

South America |

|

|

|

|

|

|

|

Companies Covered |

|||||

|

|

|

|

|

|

Green Building Materials Market Segmentation and Highlights

|

Segment |

Sub-segment |

|

Green Building Materials Market, By Product Type |

|

|

Green Building Materials Market, By Material Type |

|

|

Green Building Materials Market, By Construction Type |

|

|

Green Building Materials Market, By Sales Channel |

|

|

Green Building Materials Market, By End-users |

|

Frequently Asked Questions

Table of Contents

- 1. Research Methodology and Assumptions

- 1.1. Definitions

- 1.2. Research Design and Approach

- 1.3. Data Collection Methods

- 1.4. Base Estimates and Calculations

- 1.5. Forecasting Models

- 1.5.1. Key Forecast Factors & Impact Analysis

- 1.6. Secondary Research

- 1.6.1. Open Sources

- 1.6.2. Paid Databases

- 1.6.3. Associations

- 1.7. Primary Research

- 1.7.1. Primary Sources

- 1.7.2. Primary Interviews with Stakeholders across Ecosystem

- 2. Executive Summary

- 2.1. Global Green Building Materials Market Outlook

- 2.1.1. Green Building Materials Market Size (Value - US$ Bn), and Forecasts, 2021-2035

- 2.1.2. Compounded Annual Growth Rate Analysis

- 2.1.3. Growth Opportunity Analysis

- 2.1.4. Segmental Share Analysis

- 2.1.5. Geographical Share Analysis

- 2.2. Market Analysis and Facts

- 2.3. Supply-Demand Analysis

- 2.4. Competitive Benchmarking

- 2.5. Go-to- Market Strategy

- 2.5.1. Customer/ End-use Industry Assessment

- 2.5.2. Growth Opportunity Data, 2026-2035

- 2.5.2.1. Regional Data

- 2.5.2.2. Country Data

- 2.5.2.3. Segmental Data

- 2.5.3. Identification of Potential Market Spaces

- 2.5.4. GAP Analysis

- 2.5.5. Potential Attractive Price Points

- 2.5.6. Prevailing Market Risks & Challenges

- 2.5.7. Preferred Sales & Marketing Strategies

- 2.5.8. Key Recommendations and Analysis

- 2.5.9. A Way Forward

- 2.1. Global Green Building Materials Market Outlook

- 3. Industry Data and Premium Insights

- 3.1. Global Chemicals & Materials Industry Overview, 2025

- 3.1.1. Chemicals & Materials Ecosystem Analysis

- 3.1.2. Key Trends for Chemicals & Materials Industry

- 3.1.3. Regional Distribution for Chemicals & Materials Industry

- 3.2. Supplier Customer Data

- 3.3. Technology Roadmap and Developments

- 3.4. Trade Analysis

- 3.4.1. Import & Export Analysis, 2025

- 3.4.2. Top Importing Countries

- 3.4.3. Top Exporting Countries

- 3.5. Trump Tariff Impact Analysis

- 3.5.1. Manufacturer

- 3.5.1.1. Based on the component & Raw material

- 3.5.2. Supply Chain

- 3.5.3. End Consumer

- 3.5.1. Manufacturer

- 3.6. Raw Material Analysis

- 3.1. Global Chemicals & Materials Industry Overview, 2025

- 4. Market Overview

- 4.1. Market Dynamics

- 4.1.1. Drivers

- 4.1.1.1. Growing focus on sustainability, environmental awareness, and carbon reduction efforts

- 4.1.1.2. Government policies, regulations, incentives, and green certification programs (e.g., LEED, BREEAM)

- 4.1.1.3. Rapid urbanization and infrastructure development increasing demand for eco‑friendly construction solutions

- 4.1.2. Restraints

- 4.1.2.1. High initial costs of green building materials compared to traditional alternatives

- 4.1.2.2. Limited availability of materials, supply chain challenges, and lack of technical expertise

- 4.1.1. Drivers

- 4.2. Key Trend Analysis

- 4.3. Regulatory Framework

- 4.3.1. Key Regulations, Norms, and Subsidies, by Key Countries

- 4.3.2. Tariffs and Standards

- 4.3.3. Impact Analysis of Regulations on the Market

- 4.4. Value Chain Analysis

- 4.4.1. Raw Material Suppliers

- 4.4.2. Manufacturers

- 4.4.3. Dealers/ Distributors

- 4.4.4. End-Users

- 4.5. Porter’s Five Forces Analysis

- 4.6. PESTEL Analysis

- 4.7. Global Green Building Materials Market Demand

- 4.7.1. Historical Market Size – in Value (US$ Bn), 2020-2024

- 4.7.2. Current and Future Market Size – in Value (US$ Bn), 2026–2035

- 4.7.2.1. Y-o-Y Growth Trends

- 4.7.2.2. Absolute $ Opportunity Assessment

- 4.1. Market Dynamics

- 5. Competition Landscape

- 5.1. Competition structure

- 5.1.1. Fragmented v/s consolidated

- 5.2. Company Share Analysis, 2025

- 5.2.1. Global Company Market Share

- 5.2.2. By Region

- 5.2.2.1. North America

- 5.2.2.2. Europe

- 5.2.2.3. Asia Pacific

- 5.2.2.4. Middle East

- 5.2.2.5. Africa

- 5.2.2.6. South America

- 5.3. Product Comparison Matrix

- 5.3.1. Specifications

- 5.3.2. Market Positioning

- 5.3.3. Pricing

- 5.1. Competition structure

- 6. Global Green Building Materials Market Analysis, by Product Type

- 6.1. Key Segment Analysis

- 6.2. Green Building Materials Market Size (Value - US$ Bn), Analysis, and Forecasts, by Product Type, 2021-2035

- 6.2.1. Structural Materials

- 6.2.2. Insulation Materials

- 6.2.3. Roofing Materials

- 6.2.4. Flooring Materials

- 6.2.5. Interior & Exterior Cladding

- 6.2.6. Windows, Doors & Glazing

- 6.2.7. Paints, Coatings & Adhesives

- 6.2.8. Mechanical, Electrical & Plumbing (MEP) Green Materials

- 6.2.9. Others

- 7. Global Green Building Materials Market Analysis, by Material Type

- 7.1. Key Segment Analysis

- 7.2. Green Building Materials Market Size (Value - US$ Bn), Analysis, and Forecasts, by Material Type, 2021-2035

- 7.2.1. Bio-Based Materials

- 7.2.2. Recycled & Upcycled Materials

- 7.2.3. Low-Carbon Materials

- 7.2.4. Rapidly Renewable Materials

- 7.2.5. Reclaimed & Salvaged Materials

- 7.2.6. Others

- 8. Global Green Building Materials Market Analysis, by Construction Type

- 8.1. Key Segment Analysis

- 8.2. Green Building Materials Market Size (Value - US$ Bn), Analysis, and Forecasts, by Construction Type, 2021-2035

- 8.2.1. New Green Construction

- 8.2.2. Green Renovation & Retrofit

- 9. Global Green Building Materials Market Analysis, by Sales Channel

- 9.1. Key Segment Analysis

- 9.2. Green Building Materials Market Size (Value - US$ Bn), Analysis, and Forecasts, by Sales Channel, 2021-2035

- 9.2.1. Direct Sales

- 9.2.2. Distributors

- 9.2.3. Online/E-Commerce

- 10. Global Green Building Materials Market Analysis, by End-users

- 10.1. Key Segment Analysis

- 10.2. Green Building Materials Market Size (Value - US$ Bn), Analysis, and Forecasts, by End-users, 2021-2035

- 10.2.1. Residential Construction

- 10.2.1.1. Single-Family Housing

- 10.2.1.2. Multi-Family & Apartment Buildings

- 10.2.1.3. Affordable & Social Housing

- 10.2.1.4. Others

- 10.2.2. Commercial Construction

- 10.2.2.1. Office Buildings & Corporate Campuses

- 10.2.2.2. Retail & Shopping Centers

- 10.2.2.3. Hospitality

- 10.2.2.4. Healthcare Facilities

- 10.2.2.5. Data Centers

- 10.2.2.6. Others

- 10.2.3. Industrial Construction

- 10.2.3.1. Manufacturing Plants

- 10.2.3.2. Warehouses & Logistics Centers

- 10.2.3.3. Processing Facilities

- 10.2.3.4. Energy & Power Generation Facilities

- 10.2.3.5. Others

- 10.2.4. Institutional & Public Buildings

- 10.2.4.1. Educational Institutions

- 10.2.4.2. Government & Civic Buildings

- 10.2.4.3. Religious & Cultural Institutions

- 10.2.4.4. Sports & Fitness Facilities

- 10.2.4.5. Others

- 10.2.5. Infrastructure & Civil Construction

- 10.2.6. Transportation Hubs

- 10.2.7. Roads, Bridges & Urban Hardscaping

- 10.2.8. Others

- 10.2.1. Residential Construction

- 11. Global Green Building Materials Market Analysis, by Region

- 11.1. Key Findings

- 11.2. Green Building Materials Market Size (Value - US$ Bn), Analysis, and Forecasts, by Region, 2021-2035

- 11.2.1. North America

- 11.2.2. Europe

- 11.2.3. Asia Pacific

- 11.2.4. Middle East

- 11.2.5. Africa

- 11.2.6. South America

- 12. North America Green Building Materials Market Analysis

- 12.1. Key Segment Analysis

- 12.2. Regional Snapshot

- 12.3. North America Green Building Materials Market Size (Value - US$ Bn), Analysis, and Forecasts, 2021-2035

- 12.3.1. Product Type

- 12.3.2. Material Type

- 12.3.3. Construction Type

- 12.3.4. Sales Channel

- 12.3.5. End-users

- 12.3.6. Country

- 12.3.6.1. USA

- 12.3.6.2. Canada

- 12.3.6.3. Mexico

- 12.4. USA Green Building Materials Market

- 12.4.1. Country Segmental Analysis

- 12.4.2. Product Type

- 12.4.3. Material Type

- 12.4.4. Construction Type

- 12.4.5. Sales Channel

- 12.4.6. End-users

- 12.5. Canada Green Building Materials Market

- 12.5.1. Country Segmental Analysis

- 12.5.2. Product Type

- 12.5.3. Material Type

- 12.5.4. Construction Type

- 12.5.5. Sales Channel

- 12.5.6. End-users

- 12.6. Mexico Green Building Materials Market

- 12.6.1. Country Segmental Analysis

- 12.6.2. Product Type

- 12.6.3. Material Type

- 12.6.4. Construction Type

- 12.6.5. Sales Channel

- 12.6.6. End-users

- 13. Europe Green Building Materials Market Analysis

- 13.1. Key Segment Analysis

- 13.2. Regional Snapshot

- 13.3. Europe Green Building Materials Market Size (Value - US$ Bn), Analysis, and Forecasts, 2021-2035

- 13.3.1. Product Type

- 13.3.2. Material Type

- 13.3.3. Construction Type

- 13.3.4. Sales Channel

- 13.3.5. End-users

- 13.3.6. Country

- 13.3.6.1. Germany

- 13.3.6.2. United Kingdom

- 13.3.6.3. France

- 13.3.6.4. Italy

- 13.3.6.5. Spain

- 13.3.6.6. Netherlands

- 13.3.6.7. Nordic Countries

- 13.3.6.8. Poland

- 13.3.6.9. Russia & CIS

- 13.3.6.10. Rest of Europe

- 13.4. Germany Green Building Materials Market

- 13.4.1. Country Segmental Analysis

- 13.4.2. Product Type

- 13.4.3. Material Type

- 13.4.4. Construction Type

- 13.4.5. Sales Channel

- 13.4.6. End-users

- 13.5. United Kingdom Green Building Materials Market

- 13.5.1. Country Segmental Analysis

- 13.5.2. Product Type

- 13.5.3. Material Type

- 13.5.4. Construction Type

- 13.5.5. Sales Channel

- 13.5.6. End-users

- 13.6. France Green Building Materials Market

- 13.6.1. Country Segmental Analysis

- 13.6.2. Product Type

- 13.6.3. Material Type

- 13.6.4. Construction Type

- 13.6.5. Sales Channel

- 13.6.6. End-users

- 13.7. Italy Green Building Materials Market

- 13.7.1. Country Segmental Analysis

- 13.7.2. Product Type

- 13.7.3. Material Type

- 13.7.4. Construction Type

- 13.7.5. Sales Channel

- 13.7.6. End-users

- 13.8. Spain Green Building Materials Market

- 13.8.1. Country Segmental Analysis

- 13.8.2. Product Type

- 13.8.3. Material Type

- 13.8.4. Construction Type

- 13.8.5. Sales Channel

- 13.8.6. End-users

- 13.9. Netherlands Green Building Materials Market

- 13.9.1. Country Segmental Analysis

- 13.9.2. Product Type

- 13.9.3. Material Type

- 13.9.4. Construction Type

- 13.9.5. Sales Channel

- 13.9.6. End-users

- 13.10. Nordic Countries Green Building Materials Market

- 13.10.1. Country Segmental Analysis

- 13.10.2. Product Type

- 13.10.3. Material Type

- 13.10.4. Construction Type

- 13.10.5. Sales Channel

- 13.10.6. End-users

- 13.11. Poland Green Building Materials Market

- 13.11.1. Country Segmental Analysis

- 13.11.2. Product Type

- 13.11.3. Material Type

- 13.11.4. Construction Type

- 13.11.5. Sales Channel

- 13.11.6. End-users

- 13.12. Russia & CIS Green Building Materials Market

- 13.12.1. Country Segmental Analysis

- 13.12.2. Product Type

- 13.12.3. Material Type

- 13.12.4. Construction Type

- 13.12.5. Sales Channel

- 13.12.6. End-users

- 13.13. Rest of Europe Green Building Materials Market

- 13.13.1. Country Segmental Analysis

- 13.13.2. Product Type

- 13.13.3. Material Type

- 13.13.4. Construction Type

- 13.13.5. Sales Channel

- 13.13.6. End-users

- 14. Asia Pacific Green Building Materials Market Analysis

- 14.1. Key Segment Analysis

- 14.2. Regional Snapshot

- 14.3. Asia Pacific Green Building Materials Market Size (Value - US$ Bn), Analysis, and Forecasts, 2021-2035

- 14.3.1. Product Type

- 14.3.2. Material Type

- 14.3.3. Construction Type

- 14.3.4. Sales Channel

- 14.3.5. End-users

- 14.3.6. Country

- 14.3.6.1. China

- 14.3.6.2. India

- 14.3.6.3. Japan

- 14.3.6.4. South Korea

- 14.3.6.5. Australia and New Zealand

- 14.3.6.6. Indonesia

- 14.3.6.7. Malaysia

- 14.3.6.8. Thailand

- 14.3.6.9. Vietnam

- 14.3.6.10. Rest of Asia Pacific

- 14.4. China Green Building Materials Market

- 14.4.1. Country Segmental Analysis

- 14.4.2. Product Type

- 14.4.3. Material Type

- 14.4.4. Construction Type

- 14.4.5. Sales Channel

- 14.4.6. End-users

- 14.5. India Green Building Materials Market

- 14.5.1. Country Segmental Analysis

- 14.5.2. Product Type

- 14.5.3. Material Type

- 14.5.4. Construction Type

- 14.5.5. Sales Channel

- 14.5.6. End-users

- 14.6. Japan Green Building Materials Market

- 14.6.1. Country Segmental Analysis

- 14.6.2. Product Type

- 14.6.3. Material Type

- 14.6.4. Construction Type

- 14.6.5. Sales Channel

- 14.6.6. End-users

- 14.7. South Korea Green Building Materials Market

- 14.7.1. Country Segmental Analysis

- 14.7.2. Product Type

- 14.7.3. Material Type

- 14.7.4. Construction Type

- 14.7.5. Sales Channel

- 14.7.6. End-users

- 14.8. Australia and New Zealand Green Building Materials Market

- 14.8.1. Country Segmental Analysis

- 14.8.2. Product Type

- 14.8.3. Material Type

- 14.8.4. Construction Type

- 14.8.5. Sales Channel

- 14.8.6. End-users

- 14.9. Indonesia Green Building Materials Market

- 14.9.1. Country Segmental Analysis

- 14.9.2. Product Type

- 14.9.3. Material Type

- 14.9.4. Construction Type

- 14.9.5. Sales Channel

- 14.9.6. End-users

- 14.10. Malaysia Green Building Materials Market

- 14.10.1. Country Segmental Analysis

- 14.10.2. Product Type

- 14.10.3. Material Type

- 14.10.4. Construction Type

- 14.10.5. Sales Channel

- 14.10.6. End-users

- 14.11. Thailand Green Building Materials Market

- 14.11.1. Country Segmental Analysis

- 14.11.2. Product Type

- 14.11.3. Material Type

- 14.11.4. Construction Type

- 14.11.5. Sales Channel

- 14.11.6. End-users

- 14.12. Vietnam Green Building Materials Market

- 14.12.1. Country Segmental Analysis

- 14.12.2. Product Type

- 14.12.3. Material Type

- 14.12.4. Construction Type

- 14.12.5. Sales Channel

- 14.12.6. End-users

- 14.13. Rest of Asia Pacific Green Building Materials Market

- 14.13.1. Country Segmental Analysis

- 14.13.2. Product Type

- 14.13.3. Material Type

- 14.13.4. Construction Type

- 14.13.5. Sales Channel

- 14.13.6. End-users

- 15. Middle East Green Building Materials Market Analysis

- 15.1. Key Segment Analysis

- 15.2. Regional Snapshot

- 15.3. Middle East Green Building Materials Market Size (Value - US$ Bn), Analysis, and Forecasts, 2021-2035

- 15.3.1. Product Type

- 15.3.2. Material Type

- 15.3.3. Construction Type

- 15.3.4. Sales Channel

- 15.3.5. End-users

- 15.3.6. Country

- 15.3.6.1. Turkey

- 15.3.6.2. UAE

- 15.3.6.3. Saudi Arabia

- 15.3.6.4. Israel

- 15.3.6.5. Rest of Middle East

- 15.4. Turkey Green Building Materials Market

- 15.4.1. Country Segmental Analysis

- 15.4.2. Product Type

- 15.4.3. Material Type

- 15.4.4. Construction Type

- 15.4.5. Sales Channel

- 15.4.6. End-users

- 15.5. UAE Green Building Materials Market

- 15.5.1. Country Segmental Analysis

- 15.5.2. Product Type

- 15.5.3. Material Type

- 15.5.4. Construction Type

- 15.5.5. Sales Channel

- 15.5.6. End-users

- 15.6. Saudi Arabia Green Building Materials Market

- 15.6.1. Country Segmental Analysis

- 15.6.2. Product Type

- 15.6.3. Material Type

- 15.6.4. Construction Type

- 15.6.5. Sales Channel

- 15.6.6. End-users

- 15.7. Israel Green Building Materials Market

- 15.7.1. Country Segmental Analysis

- 15.7.2. Product Type

- 15.7.3. Material Type

- 15.7.4. Construction Type

- 15.7.5. Sales Channel

- 15.7.6. End-users

- 15.8. Rest of Middle East Green Building Materials Market

- 15.8.1. Country Segmental Analysis

- 15.8.2. Product Type

- 15.8.3. Material Type

- 15.8.4. Construction Type

- 15.8.5. Sales Channel

- 15.8.6. End-users

- 16. Africa Green Building Materials Market Analysis

- 16.1. Key Segment Analysis

- 16.2. Regional Snapshot

- 16.3. Africa Green Building Materials Market Size (Value - US$ Bn), Analysis, and Forecasts, 2021-2035

- 16.3.1. Product Type

- 16.3.2. Material Type

- 16.3.3. Construction Type

- 16.3.4. Sales Channel

- 16.3.5. End-users

- 16.3.6. Country

- 16.3.6.1. South Africa

- 16.3.6.2. Egypt

- 16.3.6.3. Nigeria

- 16.3.6.4. Algeria

- 16.3.6.5. Rest of Africa

- 16.4. South Africa Green Building Materials Market

- 16.4.1. Country Segmental Analysis

- 16.4.2. Product Type

- 16.4.3. Material Type

- 16.4.4. Construction Type

- 16.4.5. Sales Channel

- 16.4.6. End-users

- 16.5. Egypt Green Building Materials Market

- 16.5.1. Country Segmental Analysis

- 16.5.2. Product Type

- 16.5.3. Material Type

- 16.5.4. Construction Type

- 16.5.5. Sales Channel

- 16.5.6. End-users

- 16.6. Nigeria Green Building Materials Market

- 16.6.1. Country Segmental Analysis

- 16.6.2. Product Type

- 16.6.3. Material Type

- 16.6.4. Construction Type

- 16.6.5. Sales Channel

- 16.6.6. End-users

- 16.7. Algeria Green Building Materials Market

- 16.7.1. Country Segmental Analysis

- 16.7.2. Product Type

- 16.7.3. Material Type

- 16.7.4. Construction Type

- 16.7.5. Sales Channel

- 16.7.6. End-users

- 16.8. Rest of Africa Green Building Materials Market

- 16.8.1. Country Segmental Analysis

- 16.8.2. Product Type

- 16.8.3. Material Type

- 16.8.4. Construction Type

- 16.8.5. Sales Channel

- 16.8.6. End-users

- 17. South America Green Building Materials Market Analysis

- 17.1. Key Segment Analysis

- 17.2. Regional Snapshot

- 17.3. South America Green Building Materials Market Size (Value - US$ Bn), Analysis, and Forecasts, 2021-2035

- 17.3.1. Product Type

- 17.3.2. Material Type

- 17.3.3. Construction Type

- 17.3.4. Sales Channel

- 17.3.5. End-users

- 17.3.6. Country

- 17.3.6.1. Brazil

- 17.3.6.2. Argentina

- 17.3.6.3. Rest of South America

- 17.4. Brazil Green Building Materials Market

- 17.4.1. Country Segmental Analysis

- 17.4.2. Product Type

- 17.4.3. Material Type

- 17.4.4. Construction Type

- 17.4.5. Sales Channel

- 17.4.6. End-users

- 17.5. Argentina Green Building Materials Market

- 17.5.1. Country Segmental Analysis

- 17.5.2. Product Type

- 17.5.3. Material Type

- 17.5.4. Construction Type

- 17.5.5. Sales Channel

- 17.5.6. End-users

- 17.6. Rest of South America Green Building Materials Market

- 17.6.1. Country Segmental Analysis

- 17.6.2. Product Type

- 17.6.3. Material Type

- 17.6.4. Construction Type

- 17.6.5. Sales Channel

- 17.6.6. End-users

- 18. Key Players/ Company Profile

- 18.1. 3M Company

- 18.1.1. Company Details/ Overview

- 18.1.2. Company Financials

- 18.1.3. Key Customers and Competitors

- 18.1.4. Business/ Industry Portfolio

- 18.1.5. Product Portfolio/ Specification Details

- 18.1.6. Pricing Data

- 18.1.7. Strategic Overview

- 18.1.8. Recent Developments

- 18.2. Armstrong World Industries

- 18.3. BASF SE

- 18.4. Boise Cascade Company

- 18.5. Dow Inc.

- 18.6. Forbo Holding AG

- 18.7. HeidelbergMaterials AG

- 18.8. Interface Inc.

- 18.9. Kingspan Group plc

- 18.10. LafargeHolcim (Holcim Group)

- 18.11. Owens Corning

- 18.12. PPG Industries Inc.

- 18.13. Rockwool International A/S

- 18.14. RPM International Inc.

- 18.15. Saint-Gobain S.A.

- 18.16. Sherwin-Williams Company

- 18.17. Steelcase Inc.

- 18.18. Tremco Incorporated

- 18.19. Trex Company Inc.

- 18.20. USG Corporation (Knauf)

- 18.21. Weyerhaeuser Company

- 18.22. Other Key Players

- 18.1. 3M Company

Note* - This is just tentative list of players. While providing the report, we will cover more number of players based on their revenue and share for each geography

Research Design

Our research design integrates both demand-side and supply-side analysis through a balanced combination of primary and secondary research methodologies. By utilizing both bottom-up and top-down approaches alongside rigorous data triangulation methods, we deliver robust market intelligence that supports strategic decision-making.

MarketGenics' comprehensive research design framework ensures the delivery of accurate, reliable, and actionable market intelligence. Through the integration of multiple research approaches, rigorous validation processes, and expert analysis, we provide our clients with the insights needed to make informed strategic decisions and capitalize on market opportunities.

MarketGenics leverages a dedicated industry panel of experts and a comprehensive suite of paid databases to effectively collect, consolidate, and analyze market intelligence.

Our approach has consistently proven to be reliable and effective in generating accurate market insights, identifying key industry trends, and uncovering emerging business opportunities.

Through both primary and secondary research, we capture and analyze critical company-level data such as manufacturing footprints, including technical centers, R&D facilities, sales offices, and headquarters.

Our expert panel further enhances our ability to estimate market size for specific brands based on validated field-level intelligence.

Our data mining techniques incorporate both parametric and non-parametric methods, allowing for structured data collection, sorting, processing, and cleaning.

Demand projections are derived from large-scale data sets analyzed through proprietary algorithms, culminating in robust and reliable market sizing.

Research Approach

The bottom-up approach builds market estimates by starting with the smallest addressable market units and systematically aggregating them to create comprehensive market size projections.

This method begins with specific, granular data points and builds upward to create the complete market landscape.

Customer Analysis → Segmental Analysis → Geographical Analysis

The top-down approach starts with the broadest possible market data and systematically narrows it down through a series of filters and assumptions to arrive at specific market segments or opportunities.

This method begins with the big picture and works downward to increasingly specific market slices.

TAM → SAM → SOM

Research Methods

Desk / Secondary Research

While analysing the market, we extensively study secondary sources, directories, and databases to identify and collect information useful for this technical, market-oriented, and commercial report. Secondary sources that we utilize are not only the public sources, but it is a combination of Open Source, Associations, Paid Databases, MG Repository & Knowledgebase, and others.

- Company websites, annual reports, financial reports, broker reports, and investor presentations

- National government documents, statistical databases and reports

- News articles, press releases and web-casts specific to the companies operating in the market, Magazines, reports, and others

- We gather information from commercial data sources for deriving company specific data such as segmental revenue, share for geography, product revenue, and others

- Internal and external proprietary databases (industry-specific), relevant patent, and regulatory databases

- Governing Bodies, Government Organizations

- Relevant Authorities, Country-specific Associations for Industries

We also employ the model mapping approach to estimate the product level market data through the players' product portfolio

Primary Research

Primary research/ interviews is vital in analyzing the market. Most of the cases involves paid primary interviews. Primary sources include primary interviews through e-mail interactions, telephonic interviews, surveys as well as face-to-face interviews with the different stakeholders across the value chain including several industry experts.

| Type of Respondents | Number of Primaries |

|---|---|

| Tier 2/3 Suppliers | ~20 |

| Tier 1 Suppliers | ~25 |

| End-users | ~25 |

| Industry Expert/ Panel/ Consultant | ~30 |

| Total | ~100 |

MG Knowledgebase

• Repository of industry blog, newsletter and case studies

• Online platform covering detailed market reports, and company profiles

Forecasting Factors and Models

Forecasting Factors

- Historical Trends – Past market patterns, cycles, and major events that shaped how markets behave over time. Understanding past trends helps predict future behavior.

- Industry Factors – Specific characteristics of the industry like structure, regulations, and innovation cycles that affect market dynamics.

- Macroeconomic Factors – Economic conditions like GDP growth, inflation, and employment rates that affect how much money people have to spend.

- Demographic Factors – Population characteristics like age, income, and location that determine who can buy your product.

- Technology Factors – How quickly people adopt new technology and how much technology infrastructure exists.

- Regulatory Factors – Government rules, laws, and policies that can help or restrict market growth.

- Competitive Factors – Analyzing competition structure such as degree of competition and bargaining power of buyers and suppliers.

Forecasting Models / Techniques

Multiple Regression Analysis

- Identify and quantify factors that drive market changes

- Statistical modeling to establish relationships between market drivers and outcomes

Time Series Analysis – Seasonal Patterns

- Understand regular cyclical patterns in market demand

- Advanced statistical techniques to separate trend, seasonal, and irregular components

Time Series Analysis – Trend Analysis

- Identify underlying market growth patterns and momentum

- Statistical analysis of historical data to project future trends

Expert Opinion – Expert Interviews

- Gather deep industry insights and contextual understanding

- In-depth interviews with key industry stakeholders

Multi-Scenario Development

- Prepare for uncertainty by modeling different possible futures

- Creating optimistic, pessimistic, and most likely scenarios

Time Series Analysis – Moving Averages

- Sophisticated forecasting for complex time series data

- Auto-regressive integrated moving average models with seasonal components

Econometric Models

- Apply economic theory to market forecasting

- Sophisticated economic models that account for market interactions

Expert Opinion – Delphi Method

- Harness collective wisdom of industry experts

- Structured, multi-round expert consultation process

Monte Carlo Simulation

- Quantify uncertainty and probability distributions

- Thousands of simulations with varying input parameters

Research Analysis

Our research framework is built upon the fundamental principle of validating market intelligence from both demand and supply perspectives. This dual-sided approach ensures comprehensive market understanding and reduces the risk of single-source bias.

Demand-Side Analysis: We understand end-user/application behavior, preferences, and market needs along with the penetration of the product for specific application.

Supply-Side Analysis: We estimate overall market revenue, analyze the segmental share along with industry capacity, competitive landscape, and market structure.

Validation & Evaluation

Data triangulation is a validation technique that uses multiple methods, sources, or perspectives to examine the same research question, thereby increasing the credibility and reliability of research findings. In market research, triangulation serves as a quality assurance mechanism that helps identify and minimize bias, validate assumptions, and ensure accuracy in market estimates.

- Data Source Triangulation – Using multiple data sources to examine the same phenomenon

- Methodological Triangulation – Using multiple research methods to study the same research question

- Investigator Triangulation – Using multiple researchers or analysts to examine the same data

- Theoretical Triangulation – Using multiple theoretical perspectives to interpret the same data

Custom Market Research Services

We will customise the research for you, in case the report listed above does not meet your requirements.

Get 10% Free Customisation