Luxury Packaging Market Size, Share & Trends Analysis Report by Packaging Type (Rigid Boxes, Folding Cartons, Tubes & Cylinders, Bags & Pouches, Sleeves & Wraps, Bottles & Jars, Display Packaging, Gift Sets, Others), Material Type, Printing & Finishing Technology, Application, End‑Use Industry, Distribution Channel and Geography (North America, Europe, Asia Pacific, Middle East, Africa, and South America) – Global Industry Data, Trends, and Forecasts, 2026–2035

|

Market Structure & Evolution |

|

|

Segmental Data Insights |

|

|

Demand Trends |

|

|

Competitive Landscape |

|

|

Strategic Development |

|

|

Future Outlook & Opportunities |

|

Luxury Packaging Market Size, Share, and Growth

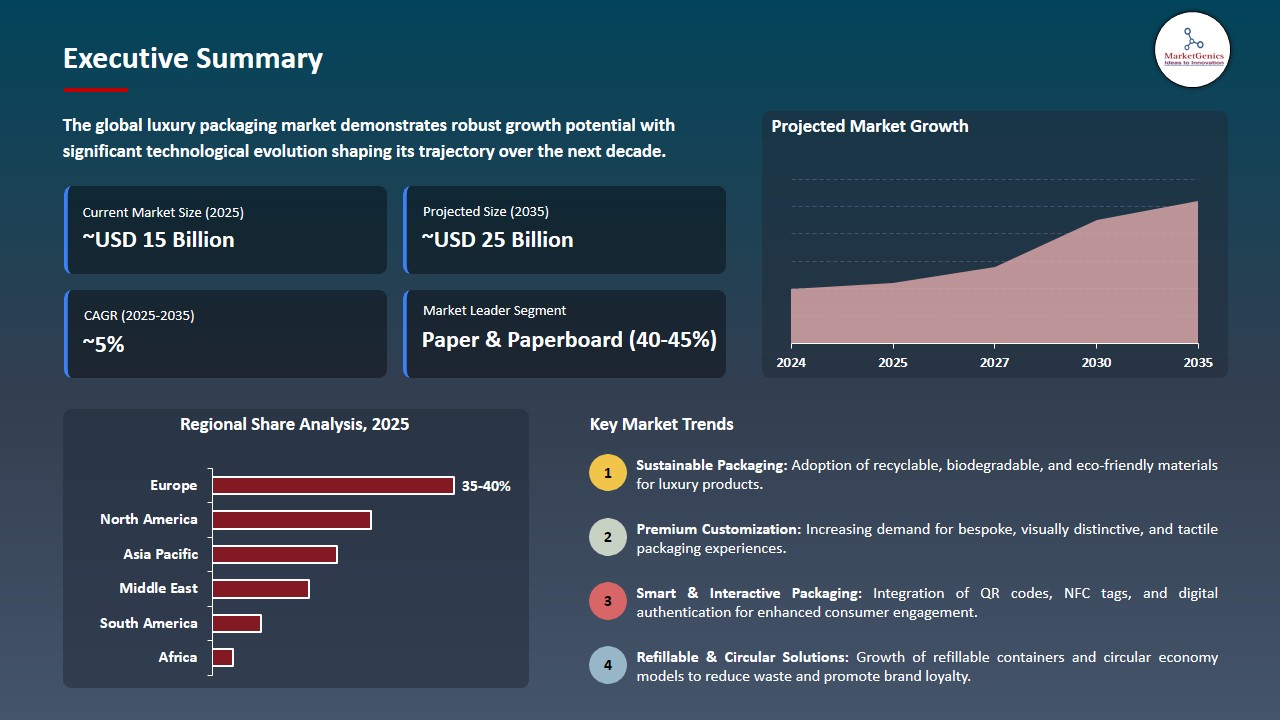

The global luxury packaging market is experiencing robust growth, with its estimated value of USD 15.4 billion in the year 2025 and USD 24.7 billion by 2035, registering a CAGR of 4.8% during the forecast period. There is enormous growth occurring globally in the luxury packaging market.

According to Claudia D'Arpizio, Senior Partner and Global Head of the Fashion & Luxury practice at Bain & Company, "Packaging is evolving as an engaging part of a brand experience." Her statement reflects data from the 2025 Bain/Fedrigoni Report detailing how sustainability and innovative packaging practices will have a greater emphasis on the new retail model for luxury goods, with more than 30% of retailers adopting sustainable options for their luxury product line.

Factors that are driving this growth include the increasing demand for premium brand differentiation, environmentally friendly innovative solutions, and superior quality of packaging materials. There is a trend in luxury brands utilizing eco-designed paperboards, glass, and bio-based packaging solutions which combine aesthetic beauty and environmental responsibility. Notably, LVMH increasing the use of sustainable luxury packaging amongst their brands while focusing on recyclability, utilization of fewer materials, sourcing responsibly and still achieving a premium look.

Additionally, the increase in the global luxury goods sector (in particular, beauty, fragrance, fashion, and premium alcohol) is driving greater demand for sophisticated and unique packaging. Luxury brands such as Chanel and Dior have been creating new product packages that use less plastic and incorporate refillable formats to align with the expectations of consumers regarding sustainability.

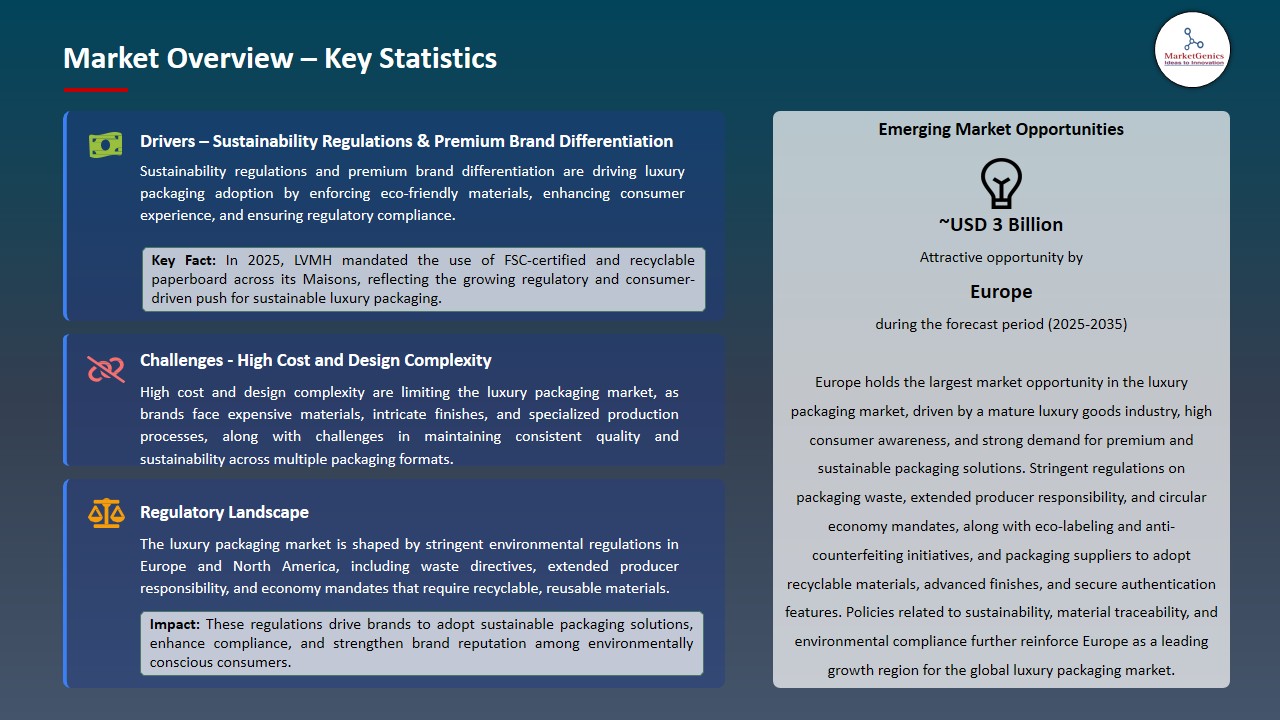

Furthermore, stringent environmental regulations throughout Europe and North America (e.g., packaging waste regulations and extended producer responsibility legislation) are forcing brands to continuously develop and invest in compliance-driven, innovative packaging products.

The combination of innovations driven by sustainability, regulatory drivers, and increasing luxury consumption is fueling growth in this emerging market. There are several adjacent opportunities including smart packaging, premium finishes/labels, refill systems, and new sustainable materials. These opportunities allow packaging manufacturers to add value to their brands and grow their revenue sources.

Luxury Packaging Market Dynamics and Trends

Driver: Sustainability Regulations and Premium Brand Differentiation Driving Luxury Packaging Adoption

-

European and North American environmental regulations related to packaging waste reduction and recyclability are driving the rapid growth of the luxury packaging market as brands are now moving toward eco-designed premium packaging. Manufacturers are creating high-quality, low-impact packaging to meet both brand storytelling objectives and consumer demand for sustainable yet premium unboxing experiences.

- Many luxury brands are transitioning to using high-quality paperboard, glass, or other low-impact materials to produce premium product packaging that meets sustainability objectives without compromising brand equity. For example, Tiffany & Co. has transitioned its prestigious Blue Box packaging from non-FSC-certified paper to FSC-certified paper to help promote sustainability in the decision-making process, while still providing consumers with premium-quality products.

- The increasing consumer preference for premium packaging that offers a unique unboxing experience can be found across many different categories of products; cosmetics, fashion items, and premium beverages are among the categories that have experienced significant increases in demand for premium packaging. All these factors are likely to boost the growth of the luxury packaging market.

Restraint: High Cost and Design Complexity Limiting Scalability

-

Luxury packaging requires highly specialized materials, complex techniques for finishing, and unique structures and designs which translate to dramatically increased production & tooling costs over standard packaging. Many of these complexities lead to longer lead-times and tighter requirements for quality control that create limitations on scalability of luxury packaging, particularly for smaller brands with limited budgets.

- Introduction of sustainable material such as recycled paper, molded fiber or bio resins often adds additional cost due to inconsistent supply chains. For example, several heritage wine & spirit brands postponed planned premium packaging upgrades in 2025 because of increased costs of sourcing sustainable glass & eco-friendly materials.

- This demonstrates the disconnect between meeting sustainability goals and the feasibility of those goals within the current cost structure for the industry. All these elements are expected to restrict the expansion of the luxury packaging market.

Opportunity: Growth in Emerging Markets and Premium Personal Care Segments

-

The market requirement for luxury goods and, consequently, premium packaging formats conveying exclusivity and relevant culture is expected to grow significantly owing to rising affluence in Asia-Pacific, the Middle East and Latin America.

- Further, the demand for region-specific aesthetics and custom finishes are being driven by localized design preferences within the packaging industry. Packaging brands and manufacturers producing premium personal care products are capitalizing on the creation of sustainable and experiential packaging to elevate brand perception.

- A recent example is Estée Lauder Companies' commitment to rolling out refillable and recyclable packaging across its high-end skin and scent product lines in 2025, in China and the UAE, creating a demand for circular luxury packaging solutions, as well as partnerships with local converters. All these elements are expected to create more opportunities for future in the luxury packaging market.

Key Trend: Smart, Refillable, and Circular Luxury Packaging Models

-

The luxury packaging market is quickly transitioning away from traditional systems to include refillable systems, smart interactive elements, and circular economy models that extend product lifecycles as well as create deeper connections between brands and customers than ever before.

- Moreover, connected packaging features including QR Codes (authentication), NFC Tags (brand storytelling), and Traceability Technologies (sustainable claims) have become ubiquitous. For instance, in late 2025 L'Oréal launched smart packaging integrated into their luxury cosmetics product line, which contains built-in QR verification and containers that are designed to allow consumers to source their products locally, refill their containers, and promote the reduction of waste.

- This trend not only enhances customer loyalty, however, also allows luxury brands to remain aligned with sustainability commitments made at the global level and to recent regulatory requirements. All these elements are expected to influence significant trends in the luxury packaging market.

Luxury Packaging Market Analysis and Segmental Data

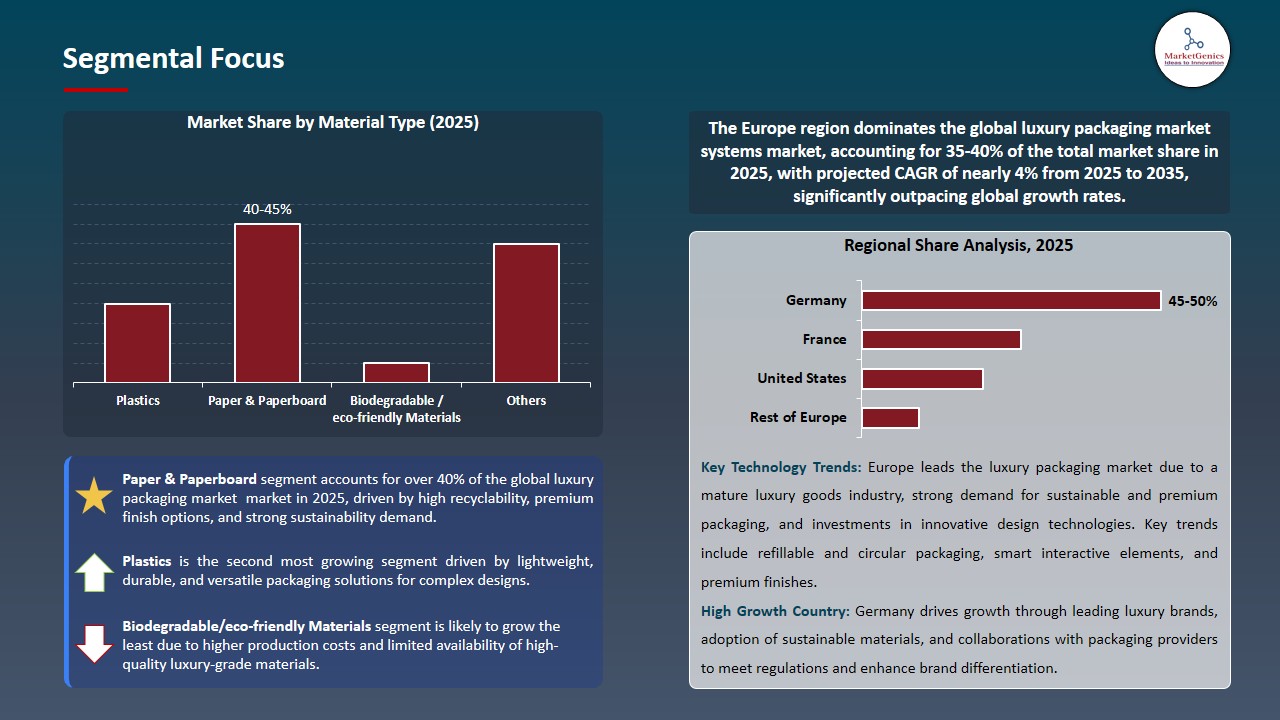

Paper & Paperboard Segment Leads Global Luxury Packaging Market Amid Rising Demand for Sustainable and Premium Consumer Experiences

-

Brands are focusing on the need for eco-sensitive, recyclable and beautifully differentiated materials as a key driver to attract customers who demand sustainable products that are packaged in a premium manner. This is particularly evident in the paperboard area of luxury packaging where paperboard has advantages over plastics such as design flexibility, quality of printed surfaces and lower negative effects on the environment.

- Paperboard is the perfect solution for luxury cosmetics and fragrances because of its low impact on the environment, ability to print well, etc. The innovations in a sustainable coating option on luxury-grade papers introduced by Fedrigoni in 2025 showed paperboard can meet both consumer expectations on aesthetics and environmental performance.

- The increasing adoption of paper-based packaging by luxury brands to lower their carbon footprint is adding to the appeal because of regulatory pressures for recyclability. These factors contribute to growing paperboards’ status as the leader in providing a combination of both sustainable product mandates and exceptional customer experience. Hence, this segment dominates in luxury packaging globally.

Europe Dominates Luxury Packaging Market Amid Strong Sustainability Regulations and Premium Brand Presence

-

With its well-established luxury goods market, Europe dominates the global luxury packaging market, as well as unique customer demand for premium and eco-friendly materials, creating an environment that is extremely conducive for luxury brands and their packaging suppliers to create sustainable and aesthetically pleasing products.

- The requirements of the European Union's circular economy and packaging waste directives, that require recyclable and reusable materials along with materials with lower environmental impact, are providing impetus for luxury brands and their suppliers in France, Italy, Germany and the United Kingdom to innovate in regards to the sustainability of their packaging and the aesthetics of packaging design.

- Moreover, the combined regulatory environment and concentration of globally known luxury brands in Europe's top metro areas creates high demand for sophisticated and responsible packaging formats. For instance, Hermès providing 2025 Forest Stewardship Council (FSC) certified paper and cardboard packaging for its luxury fashion and accessory products in its European market is another example of Europe as a leader in the luxury packaging market.

Luxury Packaging Market Ecosystem

The luxury packaging market is highly fragmented, with Tier 1 players, including Amcor, Smurfit Kappa, and AptarGroup, dominating the market due to their global scales and focus on sustainable innovations; while Tier 2 and 3 players are primarily engaged in niche and regional customized products which shows that the industry is relatively fragmented.

Important stages in the value chain consist of sustainable material procurements/designs, finishing, and branding services, which are vital in establishing premium differentiation. For instance, in 2025, Smurfit Kappa will launch recyclable luxury paperboard solutions that comply with European regulation of circular economies, further solidifying their competitive position and contributing to the ongoing consolidation of luxury packaging market.

Recent Development and Strategic Overview:

-

In April 2025, Mondi launched its Pergraphica Full Spectrum Feels Campaign at LUXE PACK Paris — Édition Spéciale. The campaign features a range of premium uncoated papers with expanded colour palettes and tactile finishes developed specifically for high-end brands. The two innovations in sustainable circular papers will help to enhance the creativity and emotional connection of luxury cosmetics, fragrance and gift packaging while maintaining a sustainable circular economy, reinforcing premium brand identity.

- In September 2025, Stora Enso launched Ensovelvet, a new premium uncoated paperboard for packaging luxury goods. It has a velvet-like surface and combines natural textures with recyclability and excellent embossing and foil-stamping characteristics. Stora Enso's recent material development will enable luxury brands to elevate the visual attractiveness and sustainability performance of their packaging without the use of conventional plastic or composite materials.

Report Scope

|

Attribute |

Detail |

|

Market Size in 2025 |

USD 15.4 Bn |

|

Market Forecast Value in 2035 |

USD 24.7 Bn |

|

Growth Rate (CAGR) |

4.8% |

|

Forecast Period |

2026 – 2035 |

|

Historical Data Available for |

2021 – 2024 |

|

Market Size Units |

USD Bn for Value |

|

Report Format |

Electronic (PDF) + Excel |

|

Regions and Countries Covered |

|||||

|

North America |

Europe |

Asia Pacific |

Middle East |

Africa |

South America |

|

|

|

|

|

|

|

Companies Covered |

|||||

|

|

|

|

|

|

Luxury Packaging Market Segmentation and Highlights

|

Segment |

Sub-segment |

|

Luxury Packaging Market, By Packaging Type |

|

|

Luxury Packaging Market, By Material Type |

|

|

Luxury Packaging Market, By Printing & Finishing Technology |

|

|

Luxury Packaging Market, By Application |

|

|

Luxury Packaging Market, By End‑Use Industry |

|

|

Luxury Packaging Market, By Distribution Channel |

|

Frequently Asked Questions

Table of Contents

- 1. Research Methodology and Assumptions

- 1.1. Definitions

- 1.2. Research Design and Approach

- 1.3. Data Collection Methods

- 1.4. Base Estimates and Calculations

- 1.5. Forecasting Models

- 1.5.1. Key Forecast Factors & Impact Analysis

- 1.6. Secondary Research

- 1.6.1. Open Sources

- 1.6.2. Paid Databases

- 1.6.3. Associations

- 1.7. Primary Research

- 1.7.1. Primary Sources

- 1.7.2. Primary Interviews with Stakeholders across Ecosystem

- 2. Executive Summary

- 2.1. Global Luxury Packaging Market Outlook

- 2.1.1. Luxury Packaging Market Size (Value - US$ Bn), and Forecasts, 2021-2035

- 2.1.2. Compounded Annual Growth Rate Analysis

- 2.1.3. Growth Opportunity Analysis

- 2.1.4. Segmental Share Analysis

- 2.1.5. Geographical Share Analysis

- 2.2. Market Analysis and Facts

- 2.3. Supply-Demand Analysis

- 2.4. Competitive Benchmarking

- 2.5. Go-to- Market Strategy

- 2.5.1. Customer/ End-use Industry Assessment

- 2.5.2. Growth Opportunity Data, 2026-2035

- 2.5.2.1. Regional Data

- 2.5.2.2. Country Data

- 2.5.2.3. Segmental Data

- 2.5.3. Identification of Potential Market Spaces

- 2.5.4. GAP Analysis

- 2.5.5. Potential Attractive Price Points

- 2.5.6. Prevailing Market Risks & Challenges

- 2.5.7. Preferred Sales & Marketing Strategies

- 2.5.8. Key Recommendations and Analysis

- 2.5.9. A Way Forward

- 2.1. Global Luxury Packaging Market Outlook

- 3. Industry Data and Premium Insights

- 3.1. Global Packaging Ecosystem Overview, 2025

- 3.1.1. Packaging Industry Analysis

- 3.1.2. Key Trends for Packaging Industry

- 3.1.3. Regional Distribution for Packaging Industry

- 3.2. Supplier Customer Data

- 3.3. Technology Roadmap and Developments

- 3.4. Trade Analysis

- 3.1. Global Packaging Ecosystem Overview, 2025

- 4. Market Overview

- 4.1. Market Dynamics

- 4.1.1. Drivers

- 4.1.1.1. Rising demand for premium branding, customization, and enhanced consumer experiences.

- 4.1.1.2. Strong sustainability regulations and brand commitments toward recyclable and eco-friendly materials.

- 4.1.1.3. Growth of luxury goods, cosmetics, spirits, and high-end e-commerce globally.

- 4.1.2. Restraints

- 4.1.2.1. Complexity in sourcing sustainable raw materials at scale.

- 4.1.2.2. Longer development cycles due to stringent quality and regulatory requirements.

- 4.1.1. Drivers

- 4.2. Key Trend Analysis

- 4.3. Regulatory Framework

- 4.3.1. Key Regulations, Norms, and Subsidies, by Key Countries

- 4.3.2. Tariffs and Standards

- 4.3.3. Impact Analysis of Regulations on the Market

- 4.4. Value Chain Analysis

- 4.5. Cost Structure Analysis

- 4.6. Porter’s Five Forces Analysis

- 4.7. PESTEL Analysis

- 4.8. Global Luxury Packaging Market Demand

- 4.8.1. Historical Market Size – Value (US$ Bn), 2020-2024

- 4.8.2. Current and Future Market Size – Value (US$ Bn), 2026–2035

- 4.8.2.1. Y-o-Y Growth Trends

- 4.8.2.2. Absolute $ Opportunity Assessment

- 4.1. Market Dynamics

- 5. Competition Landscape

- 5.1. Competition structure

- 5.1.1. Fragmented v/s consolidated

- 5.2. Company Share Analysis, 2025

- 5.2.1. Global Company Market Share

- 5.2.2. By Region

- 5.2.2.1. North America

- 5.2.2.2. Europe

- 5.2.2.3. Asia Pacific

- 5.2.2.4. Middle East

- 5.2.2.5. Africa

- 5.2.2.6. South America

- 5.3. Product Comparison Matrix

- 5.3.1. Specifications

- 5.3.2. Market Positioning

- 5.3.3. Pricing

- 5.1. Competition structure

- 6. Global Luxury Packaging Market Analysis, by Packaging Type

- 6.1. Key Segment Analysis

- 6.2. Luxury Packaging Market Size (Value - US$ Bn), Analysis, and Forecasts, by Packaging Type, 2021-2035

- 6.2.1. Rigid Boxes

- 6.2.2. Folding Cartons

- 6.2.3. Tubes & Cylinders

- 6.2.4. Bags & Pouches

- 6.2.5. Sleeves & Wraps

- 6.2.6. Bottles & Jars

- 6.2.7. Display Packaging

- 6.2.8. Gift Sets

- 6.2.9. Others

- 7. Global Luxury Packaging Market Analysis, by Material Type

- 7.1. Key Segment Analysis

- 7.2. Luxury Packaging Market Size (Value - US$ Bn), Analysis, and Forecasts, by Material Type, 2021-2035

- 7.2.1. Paper & Paperboard

- 7.2.2. Plastics

- 7.2.3. Glass

- 7.2.4. Metal

- 7.2.5. Wood

- 7.2.6. Fabric/ Textile

- 7.2.7. Composite Materials

- 7.2.8. Biodegradable/eco‑friendly Materials

- 7.2.9. Others

- 8. Global Luxury Packaging Market Analysis, by Printing & Finishing Technology

- 8.1. Key Segment Analysis

- 8.2. Luxury Packaging Market Size (Value - US$ Bn), Analysis, and Forecasts, by Printing & Finishing Technology, 2021-2035

- 8.2.1. Offset Printing

- 8.2.2. Flexographic Printing

- 8.2.3. Digital Printing

- 8.2.4. Hot Stamping

- 8.2.5. Embossing/Debossing

- 8.2.6. UV Coating

- 8.2.7. Foil Stamping

- 8.2.8. Laminating

- 8.2.9. Others

- 9. Global Luxury Packaging Market Analysis, by Application

- 9.1. Key Segment Analysis

- 9.2. Luxury Packaging Market Size (Value - US$ Bn), Analysis, and Forecasts, by Application, 2021-2035

- 9.2.1. Primary Packaging

- 9.2.2. Secondary Packaging

- 9.2.3. Tertiary Packaging

- 9.2.4. Gift & Promotional Packaging

- 9.2.5. Seasonal/Holiday Packaging

- 9.2.6. Limited Edition Packaging

- 9.2.7. Custom/Personalized Packaging

- 9.2.8. Others

- 10. Global Luxury Packaging Market Analysis, by End‑Use Industry

- 10.1. Key Segment Analysis

- 10.2. Luxury Packaging Market Size (Value - US$ Bn), Analysis, and Forecasts, by End‑Use Industry, 2021-2035

- 10.2.1. Beauty & Personal Care

- 10.2.2. Food & Beverages

- 10.2.3. Pharmaceuticals

- 10.2.4. Electronics & Gadgets

- 10.2.5. Luxury Goods & Accessories

- 10.2.6. Wines & Spirits

- 10.2.7. Tobacco

- 10.2.8. Others

- 11. Global Luxury Packaging Market Analysis, by Distribution Channel

- 11.1. Key Segment Analysis

- 11.2. Luxury Packaging Market Size (Value - US$ Bn), Analysis, and Forecasts, by Distribution Channel, 2021-2035

- 11.2.1. Direct Sales

- 11.2.2. Retail Stores

- 11.2.3. E‑commerce

- 11.2.4. Wholesale/Distributors

- 11.2.5. Specialty Packaging Stores

- 12. Global Luxury Packaging Market Analysis and Forecasts, by Region

- 12.1. Key Findings

- 12.2. Luxury Packaging Market Size (Value - US$ Bn), Analysis, and Forecasts, by Region, 2021-2035

- 12.2.1. North America

- 12.2.2. Europe

- 12.2.3. Asia Pacific

- 12.2.4. Middle East

- 12.2.5. Africa

- 12.2.6. South America

- 13. North America Luxury Packaging Market Analysis

- 13.1. Key Segment Analysis

- 13.2. Regional Snapshot

- 13.3. North America Luxury Packaging Market Size Value - US$ Bn), Analysis, and Forecasts, 2021-2035

- 13.3.1. Packaging Type

- 13.3.2. Material Type

- 13.3.3. Printing & Finishing Technology

- 13.3.4. Application

- 13.3.5. End‑Use Industry

- 13.3.6. Distribution Channel

- 13.3.7. Country

- 13.3.7.1. USA

- 13.3.7.2. Canada

- 13.3.7.3. Mexico

- 13.4. USA Luxury Packaging Market

- 13.4.1. Country Segmental Analysis

- 13.4.2. Packaging Type

- 13.4.3. Material Type

- 13.4.4. Printing & Finishing Technology

- 13.4.5. Application

- 13.4.6. End‑Use Industry

- 13.4.7. Distribution Channel

- 13.5. Canada Luxury Packaging Market

- 13.5.1. Country Segmental Analysis

- 13.5.2. Packaging Type

- 13.5.3. Material Type

- 13.5.4. Printing & Finishing Technology

- 13.5.5. Application

- 13.5.6. End‑Use Industry

- 13.5.7. Distribution Channel

- 13.6. Mexico Luxury Packaging Market

- 13.6.1. Country Segmental Analysis

- 13.6.2. Packaging Type

- 13.6.3. Material Type

- 13.6.4. Printing & Finishing Technology

- 13.6.5. Application

- 13.6.6. End‑Use Industry

- 13.6.7. Distribution Channel

- 14. Europe Luxury Packaging Market Analysis

- 14.1. Key Segment Analysis

- 14.2. Regional Snapshot

- 14.3. Europe Luxury Packaging Market Size (Value - US$ Bn), Analysis, and Forecasts, 2021-2035

- 14.3.1. Packaging Type

- 14.3.2. Material Type

- 14.3.3. Printing & Finishing Technology

- 14.3.4. Application

- 14.3.5. End‑Use Industry

- 14.3.6. Distribution Channel

- 14.3.7. Country

- 14.3.7.1. Germany

- 14.3.7.2. United Kingdom

- 14.3.7.3. France

- 14.3.7.4. Italy

- 14.3.7.5. Spain

- 14.3.7.6. Netherlands

- 14.3.7.7. Nordic Countries

- 14.3.7.8. Poland

- 14.3.7.9. Russia & CIS

- 14.3.7.10. Rest of Europe

- 14.4. Germany Luxury Packaging Market

- 14.4.1. Country Segmental Analysis

- 14.4.2. Packaging Type

- 14.4.3. Material Type

- 14.4.4. Printing & Finishing Technology

- 14.4.5. Application

- 14.4.6. End‑Use Industry

- 14.4.7. Distribution Channel

- 14.5. United Kingdom Luxury Packaging Market

- 14.5.1. Country Segmental Analysis

- 14.5.2. Packaging Type

- 14.5.3. Material Type

- 14.5.4. Printing & Finishing Technology

- 14.5.5. Application

- 14.5.6. End‑Use Industry

- 14.5.7. Distribution Channel

- 14.6. France Luxury Packaging Market

- 14.6.1. Country Segmental Analysis

- 14.6.2. Packaging Type

- 14.6.3. Material Type

- 14.6.4. Printing & Finishing Technology

- 14.6.5. Application

- 14.6.6. End‑Use Industry

- 14.6.7. Distribution Channel

- 14.7. Italy Luxury Packaging Market

- 14.7.1. Country Segmental Analysis

- 14.7.2. Packaging Type

- 14.7.3. Material Type

- 14.7.4. Printing & Finishing Technology

- 14.7.5. Application

- 14.7.6. End‑Use Industry

- 14.7.7. Distribution Channel

- 14.8. Spain Luxury Packaging Market

- 14.8.1. Country Segmental Analysis

- 14.8.2. Packaging Type

- 14.8.3. Material Type

- 14.8.4. Printing & Finishing Technology

- 14.8.5. Application

- 14.8.6. End‑Use Industry

- 14.8.7. Distribution Channel

- 14.9. Netherlands Luxury Packaging Market

- 14.9.1. Country Segmental Analysis

- 14.9.2. Packaging Type

- 14.9.3. Material Type

- 14.9.4. Printing & Finishing Technology

- 14.9.5. Application

- 14.9.6. End‑Use Industry

- 14.9.7. Distribution Channel

- 14.10. Nordic Countries Luxury Packaging Market

- 14.10.1. Country Segmental Analysis

- 14.10.2. Packaging Type

- 14.10.3. Material Type

- 14.10.4. Printing & Finishing Technology

- 14.10.5. Application

- 14.10.6. End‑Use Industry

- 14.10.7. Distribution Channel

- 14.11. Poland Luxury Packaging Market

- 14.11.1. Country Segmental Analysis

- 14.11.2. Packaging Type

- 14.11.3. Material Type

- 14.11.4. Printing & Finishing Technology

- 14.11.5. Application

- 14.11.6. End‑Use Industry

- 14.11.7. Distribution Channel

- 14.12. Russia & CIS Luxury Packaging Market

- 14.12.1. Country Segmental Analysis

- 14.12.2. Packaging Type

- 14.12.3. Material Type

- 14.12.4. Printing & Finishing Technology

- 14.12.5. Application

- 14.12.6. End‑Use Industry

- 14.12.7. Distribution Channel

- 14.13. Rest of Europe Luxury Packaging Market

- 14.13.1. Country Segmental Analysis

- 14.13.2. Packaging Type

- 14.13.3. Material Type

- 14.13.4. Printing & Finishing Technology

- 14.13.5. Application

- 14.13.6. End‑Use Industry

- 14.13.7. Distribution Channel

- 15. Asia Pacific Luxury Packaging Market Analysis

- 15.1. Key Segment Analysis

- 15.2. Regional Snapshot

- 15.3. Asia Pacific Luxury Packaging Market Size (Value - US$ Bn), Analysis, and Forecasts, 2021-2035

- 15.3.1. Packaging Type

- 15.3.2. Material Type

- 15.3.3. Printing & Finishing Technology

- 15.3.4. Application

- 15.3.5. End‑Use Industry

- 15.3.6. Distribution Channel

- 15.3.7. Country

- 15.3.7.1. China

- 15.3.7.2. India

- 15.3.7.3. Japan

- 15.3.7.4. South Korea

- 15.3.7.5. Australia and New Zealand

- 15.3.7.6. Indonesia

- 15.3.7.7. Malaysia

- 15.3.7.8. Thailand

- 15.3.7.9. Vietnam

- 15.3.7.10. Rest of Asia Pacific

- 15.4. China Luxury Packaging Market

- 15.4.1. Country Segmental Analysis

- 15.4.2. Packaging Type

- 15.4.3. Material Type

- 15.4.4. Printing & Finishing Technology

- 15.4.5. Application

- 15.4.6. End‑Use Industry

- 15.4.7. Distribution Channel

- 15.5. India Luxury Packaging Market

- 15.5.1. Country Segmental Analysis

- 15.5.2. Packaging Type

- 15.5.3. Material Type

- 15.5.4. Printing & Finishing Technology

- 15.5.5. Application

- 15.5.6. End‑Use Industry

- 15.5.7. Distribution Channel

- 15.6. Japan Luxury Packaging Market

- 15.6.1. Country Segmental Analysis

- 15.6.2. Packaging Type

- 15.6.3. Material Type

- 15.6.4. Printing & Finishing Technology

- 15.6.5. Application

- 15.6.6. End‑Use Industry

- 15.6.7. Distribution Channel

- 15.7. South Korea Luxury Packaging Market

- 15.7.1. Country Segmental Analysis

- 15.7.2. Packaging Type

- 15.7.3. Material Type

- 15.7.4. Printing & Finishing Technology

- 15.7.5. Application

- 15.7.6. End‑Use Industry

- 15.7.7. Distribution Channel

- 15.8. Australia and New Zealand Luxury Packaging Market

- 15.8.1. Country Segmental Analysis

- 15.8.2. Packaging Type

- 15.8.3. Material Type

- 15.8.4. Printing & Finishing Technology

- 15.8.5. Application

- 15.8.6. End‑Use Industry

- 15.8.7. Distribution Channel

- 15.9. Indonesia Luxury Packaging Market

- 15.9.1. Country Segmental Analysis

- 15.9.2. Packaging Type

- 15.9.3. Material Type

- 15.9.4. Printing & Finishing Technology

- 15.9.5. Application

- 15.9.6. End‑Use Industry

- 15.9.7. Distribution Channel

- 15.10. Malaysia Luxury Packaging Market

- 15.10.1. Country Segmental Analysis

- 15.10.2. Packaging Type

- 15.10.3. Material Type

- 15.10.4. Printing & Finishing Technology

- 15.10.5. Application

- 15.10.6. End‑Use Industry

- 15.10.7. Distribution Channel

- 15.11. Thailand Luxury Packaging Market

- 15.11.1. Country Segmental Analysis

- 15.11.2. Packaging Type

- 15.11.3. Material Type

- 15.11.4. Printing & Finishing Technology

- 15.11.5. Application

- 15.11.6. End‑Use Industry

- 15.11.7. Distribution Channel

- 15.12. Vietnam Luxury Packaging Market

- 15.12.1. Country Segmental Analysis

- 15.12.2. Packaging Type

- 15.12.3. Material Type

- 15.12.4. Printing & Finishing Technology

- 15.12.5. Application

- 15.12.6. End‑Use Industry

- 15.12.7. Distribution Channel

- 15.13. Rest of Asia Pacific Luxury Packaging Market

- 15.13.1. Country Segmental Analysis

- 15.13.2. Packaging Type

- 15.13.3. Material Type

- 15.13.4. Printing & Finishing Technology

- 15.13.5. Application

- 15.13.6. End‑Use Industry

- 15.13.7. Distribution Channel

- 16. Middle East Luxury Packaging Market Analysis

- 16.1. Key Segment Analysis

- 16.2. Regional Snapshot

- 16.3. Middle East Luxury Packaging Market Size (Value - US$ Bn), Analysis, and Forecasts, 2021-2035

- 16.3.1. Packaging Type

- 16.3.2. Material Type

- 16.3.3. Printing & Finishing Technology

- 16.3.4. Application

- 16.3.5. End‑Use Industry

- 16.3.6. Distribution Channel

- 16.3.7. Country

- 16.3.7.1. Turkey

- 16.3.7.2. UAE

- 16.3.7.3. Saudi Arabia

- 16.3.7.4. Israel

- 16.3.7.5. Rest of Middle East

- 16.4. Turkey Luxury Packaging Market

- 16.4.1. Country Segmental Analysis

- 16.4.2. Packaging Type

- 16.4.3. Material Type

- 16.4.4. Printing & Finishing Technology

- 16.4.5. Application

- 16.4.6. End‑Use Industry

- 16.4.7. Distribution Channel

- 16.5. UAE Luxury Packaging Market

- 16.5.1. Country Segmental Analysis

- 16.5.2. Packaging Type

- 16.5.3. Material Type

- 16.5.4. Printing & Finishing Technology

- 16.5.5. Application

- 16.5.6. End‑Use Industry

- 16.5.7. Distribution Channel

- 16.6. Saudi Arabia Luxury Packaging Market

- 16.6.1. Country Segmental Analysis

- 16.6.2. Packaging Type

- 16.6.3. Material Type

- 16.6.4. Printing & Finishing Technology

- 16.6.5. Application

- 16.6.6. End‑Use Industry

- 16.6.7. Distribution Channel

- 16.7. Israel Luxury Packaging Market

- 16.7.1. Country Segmental Analysis

- 16.7.2. Packaging Type

- 16.7.3. Material Type

- 16.7.4. Printing & Finishing Technology

- 16.7.5. Application

- 16.7.6. End‑Use Industry

- 16.7.7. Distribution Channel

- 16.8. Rest of Middle East Luxury Packaging Market

- 16.8.1. Country Segmental Analysis

- 16.8.2. Packaging Type

- 16.8.3. Material Type

- 16.8.4. Printing & Finishing Technology

- 16.8.5. Application

- 16.8.6. End‑Use Industry

- 16.8.7. Distribution Channel

- 17. Africa Luxury Packaging Market Analysis

- 17.1. Key Segment Analysis

- 17.2. Regional Snapshot

- 17.3. Africa Luxury Packaging Market Size (Value - US$ Bn), Analysis, and Forecasts, 2021-2035

- 17.3.1. Packaging Type

- 17.3.2. Material Type

- 17.3.3. Printing & Finishing Technology

- 17.3.4. Application

- 17.3.5. End‑Use Industry

- 17.3.6. Distribution Channel

- 17.3.7. Country

- 17.3.7.1. South Africa

- 17.3.7.2. Egypt

- 17.3.7.3. Nigeria

- 17.3.7.4. Algeria

- 17.3.7.5. Rest of Africa

- 17.4. South Africa Luxury Packaging Market

- 17.4.1. Country Segmental Analysis

- 17.4.2. Packaging Type

- 17.4.3. Material Type

- 17.4.4. Printing & Finishing Technology

- 17.4.5. Application

- 17.4.6. End‑Use Industry

- 17.4.7. Distribution Channel

- 17.5. Egypt Luxury Packaging Market

- 17.5.1. Country Segmental Analysis

- 17.5.2. Packaging Type

- 17.5.3. Material Type

- 17.5.4. Printing & Finishing Technology

- 17.5.5. Application

- 17.5.6. End‑Use Industry

- 17.5.7. Distribution Channel

- 17.6. Nigeria Luxury Packaging Market

- 17.6.1. Country Segmental Analysis

- 17.6.2. Packaging Type

- 17.6.3. Material Type

- 17.6.4. Printing & Finishing Technology

- 17.6.5. Application

- 17.6.6. End‑Use Industry

- 17.6.7. Distribution Channel

- 17.7. Algeria Luxury Packaging Market

- 17.7.1. Country Segmental Analysis

- 17.7.2. Packaging Type

- 17.7.3. Material Type

- 17.7.4. Printing & Finishing Technology

- 17.7.5. Application

- 17.7.6. End‑Use Industry

- 17.7.7. Distribution Channel

- 17.8. Rest of Africa Luxury Packaging Market

- 17.8.1. Country Segmental Analysis

- 17.8.2. Packaging Type

- 17.8.3. Material Type

- 17.8.4. Printing & Finishing Technology

- 17.8.5. Application

- 17.8.6. End‑Use Industry

- 17.8.7. Distribution Channel

- 18. South America Luxury Packaging Market Analysis

- 18.1. Key Segment Analysis

- 18.2. Regional Snapshot

- 18.3. South America Luxury Packaging Market Size (Value - US$ Bn), Analysis, and Forecasts, 2021-2035

- 18.3.1. Packaging Type

- 18.3.2. Material Type

- 18.3.3. Printing & Finishing Technology

- 18.3.4. Application

- 18.3.5. End‑Use Industry

- 18.3.6. Distribution Channel

- 18.3.7. Country

- 18.3.7.1. Brazil

- 18.3.7.2. Argentina

- 18.3.7.3. Rest of South America

- 18.4. Brazil Luxury Packaging Market

- 18.4.1. Country Segmental Analysis

- 18.4.2. Packaging Type

- 18.4.3. Material Type

- 18.4.4. Printing & Finishing Technology

- 18.4.5. Application

- 18.4.6. End‑Use Industry

- 18.4.7. Distribution Channel

- 18.5. Argentina Luxury Packaging Market

- 18.5.1. Country Segmental Analysis

- 18.5.2. Packaging Type

- 18.5.3. Material Type

- 18.5.4. Printing & Finishing Technology

- 18.5.5. Application

- 18.5.6. End‑Use Industry

- 18.5.7. Distribution Channel

- 18.6. Rest of South America Luxury Packaging Market

- 18.6.1. Country Segmental Analysis

- 18.6.2. Packaging Type

- 18.6.3. Material Type

- 18.6.4. Printing & Finishing Technology

- 18.6.5. Application

- 18.6.6. End‑Use Industry

- 18.6.7. Distribution Channel

- 19. Key Players/ Company Profile

- 19.1. Amcor plc

- 19.1.1. Company Details/ Overview

- 19.1.2. Company Financials

- 19.1.3. Key Customers and Competitors

- 19.1.4. Business/ Industry Portfolio

- 19.1.5. Product Portfolio/ Specification Details

- 19.1.6. Pricing Data

- 19.1.7. Strategic Overview

- 19.1.8. Recent Developments

- 19.2. AptarGroup, Inc.

- 19.3. Ardagh Group S.A.

- 19.4. Ball Corporation

- 19.5. Berry Global Group, Inc.

- 19.6. Braskem S.A.

- 19.7. Constantia Flexibles Group GmbH

- 19.8. Coveris Holdings S.A.

- 19.9. Crown Holdings, Inc.

- 19.10. DS Smith plc

- 19.11. International Paper Company

- 19.12. Mondi Group

- 19.13. Oji Holdings Corporation

- 19.14. Sealed Air Corporation

- 19.15. Smurfit Kappa Group

- 19.16. Sonoco Products Company

- 19.17. Tetra Pak International S.A.

- 19.18. Uflex Limited

- 19.19. WestRock Company

- 19.20. Other Key Players

- 19.1. Amcor plc

Note* - This is just tentative list of players. While providing the report, we will cover more number of players based on their revenue and share for each geography

Research Design

Our research design integrates both demand-side and supply-side analysis through a balanced combination of primary and secondary research methodologies. By utilizing both bottom-up and top-down approaches alongside rigorous data triangulation methods, we deliver robust market intelligence that supports strategic decision-making.

MarketGenics' comprehensive research design framework ensures the delivery of accurate, reliable, and actionable market intelligence. Through the integration of multiple research approaches, rigorous validation processes, and expert analysis, we provide our clients with the insights needed to make informed strategic decisions and capitalize on market opportunities.

MarketGenics leverages a dedicated industry panel of experts and a comprehensive suite of paid databases to effectively collect, consolidate, and analyze market intelligence.

Our approach has consistently proven to be reliable and effective in generating accurate market insights, identifying key industry trends, and uncovering emerging business opportunities.

Through both primary and secondary research, we capture and analyze critical company-level data such as manufacturing footprints, including technical centers, R&D facilities, sales offices, and headquarters.

Our expert panel further enhances our ability to estimate market size for specific brands based on validated field-level intelligence.

Our data mining techniques incorporate both parametric and non-parametric methods, allowing for structured data collection, sorting, processing, and cleaning.

Demand projections are derived from large-scale data sets analyzed through proprietary algorithms, culminating in robust and reliable market sizing.

Research Approach

The bottom-up approach builds market estimates by starting with the smallest addressable market units and systematically aggregating them to create comprehensive market size projections.

This method begins with specific, granular data points and builds upward to create the complete market landscape.

Customer Analysis → Segmental Analysis → Geographical Analysis

The top-down approach starts with the broadest possible market data and systematically narrows it down through a series of filters and assumptions to arrive at specific market segments or opportunities.

This method begins with the big picture and works downward to increasingly specific market slices.

TAM → SAM → SOM

Research Methods

Desk / Secondary Research

While analysing the market, we extensively study secondary sources, directories, and databases to identify and collect information useful for this technical, market-oriented, and commercial report. Secondary sources that we utilize are not only the public sources, but it is a combination of Open Source, Associations, Paid Databases, MG Repository & Knowledgebase, and others.

- Company websites, annual reports, financial reports, broker reports, and investor presentations

- National government documents, statistical databases and reports

- News articles, press releases and web-casts specific to the companies operating in the market, Magazines, reports, and others

- We gather information from commercial data sources for deriving company specific data such as segmental revenue, share for geography, product revenue, and others

- Internal and external proprietary databases (industry-specific), relevant patent, and regulatory databases

- Governing Bodies, Government Organizations

- Relevant Authorities, Country-specific Associations for Industries

We also employ the model mapping approach to estimate the product level market data through the players' product portfolio

Primary Research

Primary research/ interviews is vital in analyzing the market. Most of the cases involves paid primary interviews. Primary sources include primary interviews through e-mail interactions, telephonic interviews, surveys as well as face-to-face interviews with the different stakeholders across the value chain including several industry experts.

| Type of Respondents | Number of Primaries |

|---|---|

| Tier 2/3 Suppliers | ~20 |

| Tier 1 Suppliers | ~25 |

| End-users | ~25 |

| Industry Expert/ Panel/ Consultant | ~30 |

| Total | ~100 |

MG Knowledgebase

• Repository of industry blog, newsletter and case studies

• Online platform covering detailed market reports, and company profiles

Forecasting Factors and Models

Forecasting Factors

- Historical Trends – Past market patterns, cycles, and major events that shaped how markets behave over time. Understanding past trends helps predict future behavior.

- Industry Factors – Specific characteristics of the industry like structure, regulations, and innovation cycles that affect market dynamics.

- Macroeconomic Factors – Economic conditions like GDP growth, inflation, and employment rates that affect how much money people have to spend.

- Demographic Factors – Population characteristics like age, income, and location that determine who can buy your product.

- Technology Factors – How quickly people adopt new technology and how much technology infrastructure exists.

- Regulatory Factors – Government rules, laws, and policies that can help or restrict market growth.

- Competitive Factors – Analyzing competition structure such as degree of competition and bargaining power of buyers and suppliers.

Forecasting Models / Techniques

Multiple Regression Analysis

- Identify and quantify factors that drive market changes

- Statistical modeling to establish relationships between market drivers and outcomes

Time Series Analysis – Seasonal Patterns

- Understand regular cyclical patterns in market demand

- Advanced statistical techniques to separate trend, seasonal, and irregular components

Time Series Analysis – Trend Analysis

- Identify underlying market growth patterns and momentum

- Statistical analysis of historical data to project future trends

Expert Opinion – Expert Interviews

- Gather deep industry insights and contextual understanding

- In-depth interviews with key industry stakeholders

Multi-Scenario Development

- Prepare for uncertainty by modeling different possible futures

- Creating optimistic, pessimistic, and most likely scenarios

Time Series Analysis – Moving Averages

- Sophisticated forecasting for complex time series data

- Auto-regressive integrated moving average models with seasonal components

Econometric Models

- Apply economic theory to market forecasting

- Sophisticated economic models that account for market interactions

Expert Opinion – Delphi Method

- Harness collective wisdom of industry experts

- Structured, multi-round expert consultation process

Monte Carlo Simulation

- Quantify uncertainty and probability distributions

- Thousands of simulations with varying input parameters

Research Analysis

Our research framework is built upon the fundamental principle of validating market intelligence from both demand and supply perspectives. This dual-sided approach ensures comprehensive market understanding and reduces the risk of single-source bias.

Demand-Side Analysis: We understand end-user/application behavior, preferences, and market needs along with the penetration of the product for specific application.

Supply-Side Analysis: We estimate overall market revenue, analyze the segmental share along with industry capacity, competitive landscape, and market structure.

Validation & Evaluation

Data triangulation is a validation technique that uses multiple methods, sources, or perspectives to examine the same research question, thereby increasing the credibility and reliability of research findings. In market research, triangulation serves as a quality assurance mechanism that helps identify and minimize bias, validate assumptions, and ensure accuracy in market estimates.

- Data Source Triangulation – Using multiple data sources to examine the same phenomenon

- Methodological Triangulation – Using multiple research methods to study the same research question

- Investigator Triangulation – Using multiple researchers or analysts to examine the same data

- Theoretical Triangulation – Using multiple theoretical perspectives to interpret the same data

Custom Market Research Services

We will customise the research for you, in case the report listed above does not meet your requirements.

Get 10% Free Customisation