Military Robotics Market Size, Share & Trends Analysis Report by Platform Type (Unmanned Ground Vehicles (UGVs), Unmanned Aerial Vehicles (UAVs), Unmanned Maritime Vehicles (UMVs), Unmanned Space Vehicles), Operational Mode, Payload Capacity, Operating Range, Endurance/Operating Duration, Propulsion System, Technology Integration, Deployment Environment, System Components, End-Use, and Geography (North America, Europe, Asia Pacific, Middle East, Africa, and South America) – Global Industry Data, Trends, and Forecasts, 2026–2035

|

|

|

Segmental Data Insights |

|

|

Demand Trends |

|

|

Competitive Landscape |

|

|

Strategic Development |

|

|

Future Outlook & Opportunities |

|

Military-Robotics-Market Size, Share, and Growth

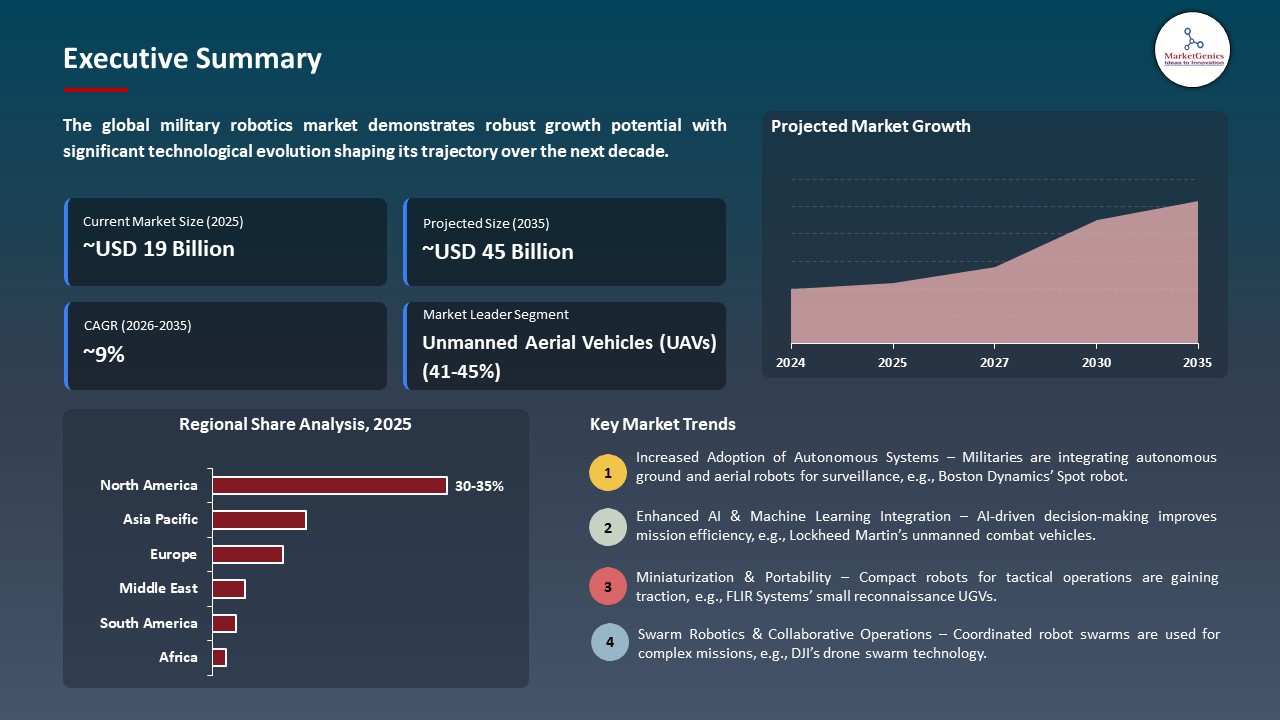

The global military robotics market is witnessing strong growth, valued at USD 19.3 billion in 2025 and projected to reach USD 44.9 billion by 2035, expanding at a CAGR of 8.8% during the forecast period. The military robotics market has AI-based autonomous units with adaptive sensors and encrypted communications that increase surveillance, target tracking, and quick tactical reaction and decrease the danger to troops in areas with high threats.

Kuldar Väärsi, CEO of Milrem Robotics, said that the company understands the complexity involved in developing reliable autonomous navigation for military applications. He added that TII and SteerAI have demonstrated strong capabilities in this area and that integrating their solution into Milrem Robotics’ vehicles will support UAE customers with advanced autonomous functionality.

The military robotics market is changing at a high rate since autonomous and semi-autonomous systems are taking center place in the modern defense policies. The military is moving towards using such platforms to conduct operations over long geographical regions with minimum risk to human life. The development of AI, machine learning, and sensor processing enables robots to do sophisticated tasks, such as assisting in urban interactions, intense monitoring in GPS-denied areas or high-risk environments.

Artificial intelligence which aids in decision support, strong encrypted messages, and multi-sensory fusion are all technological advancements that are increasing operational independence and responsiveness. The next-generation robotic systems are extending to the maritime application, urban, and off-road missions, and are used in anti-submarine surveillance, threat detection, and autonomous logistics. AI-based UGVs with sophisticated terrain mapping and autonomous navigation are used more often to assist ground troops to operate in complicated combat zones.

The adjacent opportunities in the market are interoperable human-robot teaming, autonomous logistics and medevac assistance, AI-driven anti-UAV systems, and underwater robots. These inventions increase operational efficiency, scalability of the missions and strategic flexibility. An increased use of modular systems, multi-domain systems and swarm-able systems is making military robotics an important force multiplier within defense and security contexts globally.

Military Robotics Market Dynamics and Trends

Military Robotics Market Dynamics and Trends

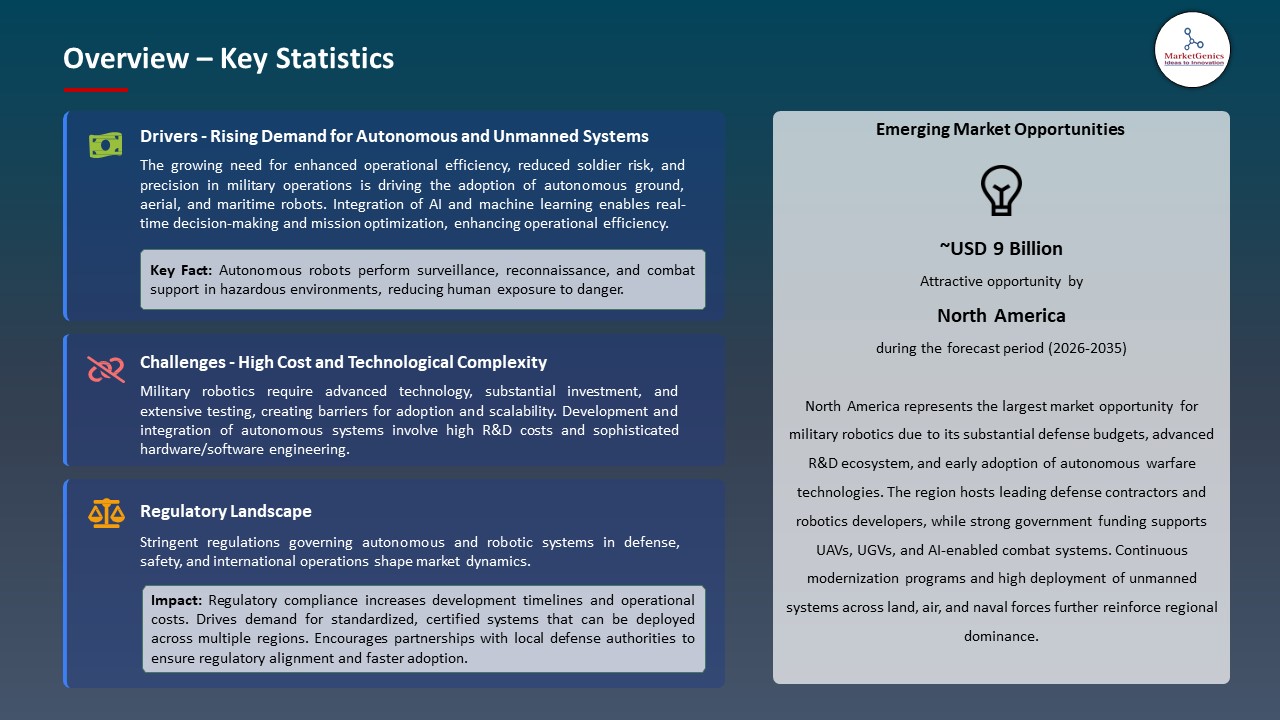

Driver: Increasing Adoption of Autonomous Systems and AI-Enabled Robotics

-

Growing requirements to maintain presence over vast maritime areas, unstable border zones, and urbanized war environments are driving the use of autonomous systems into the global military robotics market as military organizations attempt to find the means of extending peak operation range without exposing humans to extreme-risk operations.

- Use of sophisticated autonomous systems is gaining momentum with the military trying to get AI-based systems to complete tricky tasks. For instance, in December 2025, the Proteus autonomous helicopter of the Royal Navy of the UK was introduced, during its ground tests and the first autonomous flight, and presents the large-scale navigation, environmental awareness, and decision-making using AI in maritime operations.

- Autonomous platforms are gaining popularity in terms of persistent situational awareness, adaptive mission planning, and resilient operations in contested environments.

Restraint: High Cost of Development and Maintenance

-

The steep price of developing, certifying, and implementing sophisticated military robotic systems is still one of the significant inhibitors because the AI integration, secure communications, sensors, and special equipment make the acquisition cost far higher than traditional equipment.

- Ongoing lifecycle costs such as data fusion software updates, secure network provisioning, operator training, and mission rehearsal simulations continue to strain defense budgets, for example in allowing autonomous operation in the form of an autonomous multi-sensor UGV brigade with AI navigation, payload swap kits, and secure control stations can cost tens of millions of dollars in annual expenditures, and only well-funded services can afford it.

- Specialized Human Resources, certification and infrastructure are also costly and restrict may restrict mass adoption in emerging markets.

Opportunity: Expansion in Multi-Domain and Swarm Robotics

-

Multi-domain unmanned systems achieved by operating coordinated swarms of ground, aerial, and maritime robots using shared autonomy and AI are creating growing opportunities in the global military robotics market, increasing operational effectiveness, decreasing response time, and mission success in multi-threat environments.

- Real-time information sharing, decentralized autonomy, and collective decision-making can allow robotic swarms to perform distributed ISR, adaptive threat engagement, and resilient reconnaissance. For instance, in October 2025, Norwegian Army choosing and initiating deployment of the Valkyrie drone swarm system of Six Robotics, which they used to prove the practical use of coordinated UAVs in complex ISR and reconnaissance missions.

- AI and autonomous systems are enhancing the speed of the mission planning, scalable deployment and operational performance of military robotics programs across the globe.

Key Trend: Modular and Upgradable Robotics Platforms

-

Defense agencies, technology companies and prime contractors are fuelling the global military robotics market with investing into modular structures and open systems so that sensors, payloads, autonomy software and mission specific kits may be rapidly integrated to meet current and future operation requirements both in air, land, and sea.

- The elements of collaboration and platform customization are creating performance gains. For instance, in October 2025, AM General, Carnegie Robotics, and Textron Systems invented a modular unmanned ground vehicle, with drive-by-wire control and MOSA-compliant modular payloads, enabling flexible reconfiguration of missions to support logistics, energy distribution, and autonomous support.

- Modular systems and standards allow quicker upgrades, worldwide implementation, and interoperability of superior military robotic systems.

Military Robotics Market Analysis and Segmental Data

Military Robotics Market Analysis and Segmental Data

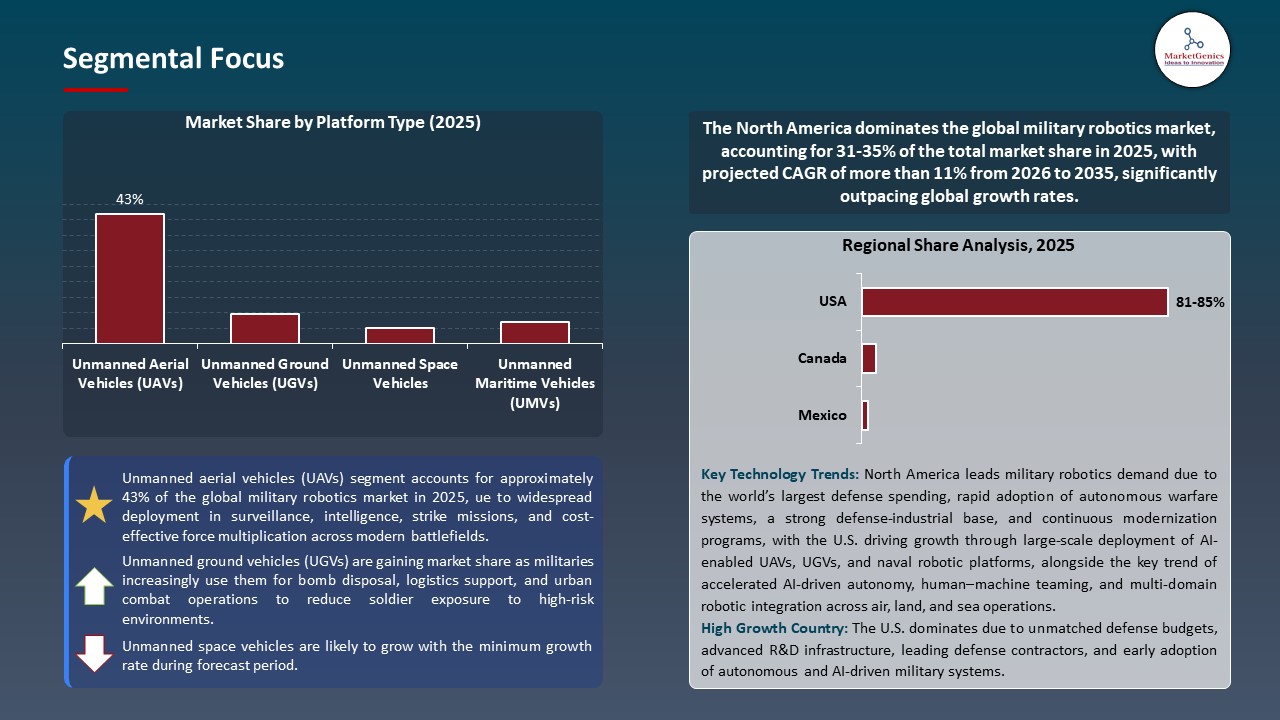

Unmanned Aerial Vehicles (UAVs) Dominate Global Military Robotics Market

-

Unmanned aerial vehicles dominate the global military robotics market as the world defence forces continue to invest in autonomous air platforms to perform persistent ISR, long-range strike, electronic warfare support, and manned transmission-unmanned teaming missions without exposing pilots to dangerous conditions.

- Segment development A developed combat-capable UAV platform, such as in December 2025, Boeing demonstrated a successful autonomous launch of a missile by the MQ-28 Ghost Bat collaborative combat fighting jet with the Royal Australian Air Force, showcasing the increasingly growing role of UAVs in the coordinated use of military air strikes, surveillance and combat operations.

- UAVs control the market of military robots worldwide because of its stamina, versatile cargo, quick deployability and capability to serve various missions in different environments.

North America Leads Global Military Robotics Market Demand

-

North America leads the global military robotics market because the U.S. Department of Defense and other allied agencies are expediting the deployment of autonomous ground, aerial, and maritime systems to support contested logistics, force protection, electronic warfare support, and operations in multiple domains beyond the typical functions of the ISR.

- Recent autonomous ground vehicle developments have highlighted the fact that regional demand exists. For instance, in October 2025, The AM General jointly developed with Carnegie Robotics and Textron Systems a modular unmanned ground vehicle to be used in the U.S. Army Medium Modular Equipment Transport (M-MET) modernization program, intended to independently deliver supplies and energy to scattered forward forces.

- Intense defense industrial foundation, intense investment in R&D and strong co-ordination between primes and start-ups entrench North America as the top global military robotics market.

Military Robotics Market Ecosystem

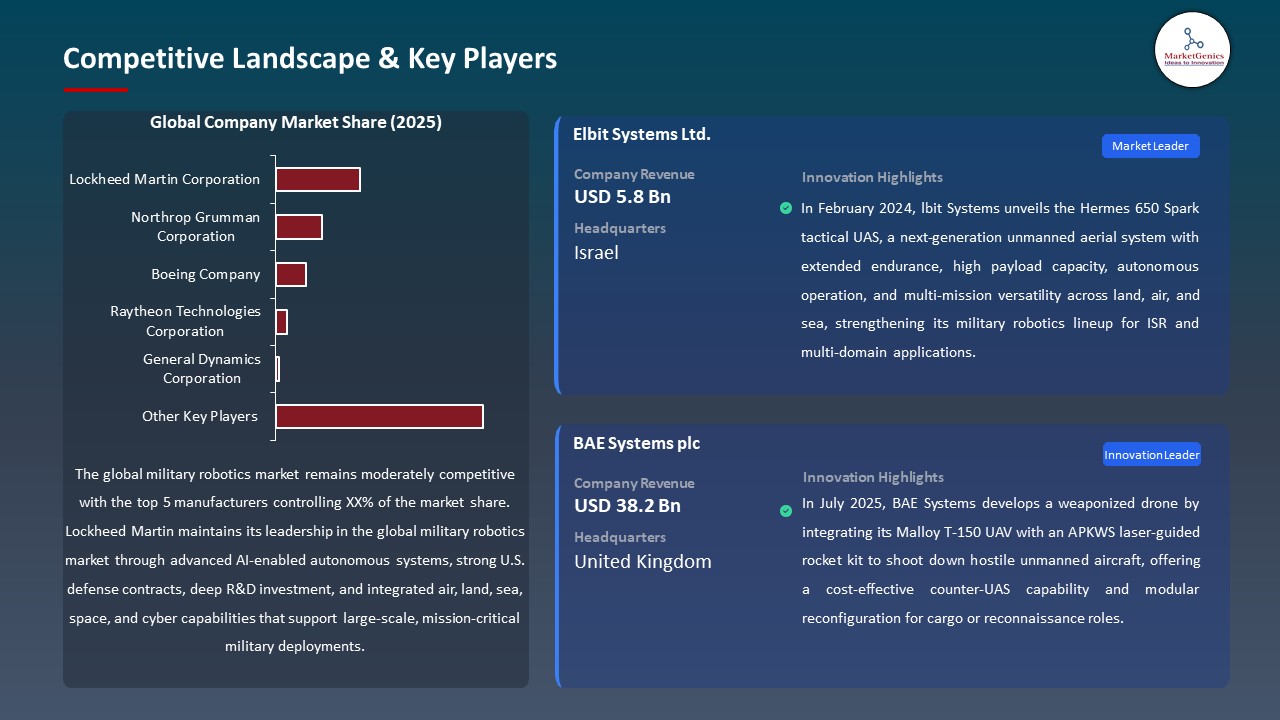

The global military robotics market is moderately consolidated with competition being based on sophisticated autonomous systems, artificially intelligent robotics and multi-domain sensor fusion. Lockheed Martin Corporation, Northrop Grumman Corporation, Boeing Company, Raytheon Technologies Corporation and General Dynamics Corporation have a combined share in the market with the provision of mission critical unmanned systems in the air, land, sea and space operations, to aid in surveillance, combat, logistics and force protection operations.

High-end, specialized robotic solutions are emphasized in these companies so as to lead technologically. Lockheed Martin is developing AI-enabled autonomy and manned-unmanned teaming into combat robotics platforms and Northrop Grumman is developing long-endurance autonomous ISR and multi-domain robotic systems, and Boeing is developing autonomous air combat, loyal wingman concepts, and unmanned mission support platforms. Raytheon Technologies complements military robotics by sensor fusion, guidance systems and AI-enabled command-and-control integration whereas General Dynamics complements ground and naval robotics with secure communications, modular payloads and survivable autonomous architectures.

Government-funded robust research and development efforts, programmes to modernize defence and partnerships with research organizations keep increasing the pace of innovation in autonomous navigation, swarm intelligence, human-machine teaming, and future payload integration. These ecosystem processes strengthen competitive differentiation, technological resilience, and deployment of operation in a short time, and place the global military robotics market to meet current demands of security and battlefield.

Recent Development and Strategic Overview

Recent Development and Strategic Overview

- In April 2025, Milrem Robotics partnered with SteerAI to equip THeMIS unmanned ground vehicles with SteerAI’s AI-powered autonomy solution for a UAE Land Forces trial program, strengthening autonomous navigation, perception, and remote operational capabilities in complex military environments.

- In October 2025, DEUTZ and ARX Robotics entered a strategic collaboration to advance digitalized drive technologies and unmanned defense systems, focusing on integrating DEUTZ’s electric and hybrid power solutions with ARX Robotics’ AI-driven autonomous platforms to enhance performance, mobility, and operational efficiency of unmanned ground vehicles.

Report Scope

|

Detail |

|

|

Market Size in 2025 |

USD 19.3 Bn |

|

Market Forecast Value in 2035 |

USD 44.9 Bn |

|

Growth Rate (CAGR) |

8.8% |

|

Forecast Period |

2026 – 2035 |

|

Historical Data Available for |

2021 – 2024 |

|

Market Size Units |

US$ Billion for Value Thousand Units for Volume |

|

Report Format |

Electronic (PDF) + Excel |

|

North America |

Europe |

Asia Pacific |

Middle East |

Africa |

South America |

|

|

|

|

|

|

|

Companies Covered |

|||||

|

|

|

|

|

|

Military Robotics Market Segmentation and Highlights

|

Segment |

Sub-segment |

|

Military Robotics Market, By Platform Type |

|

|

Military Robotics Market, By Operational Mode |

|

|

Military Robotics Market, By Payload Capacity |

|

|

Military Robotics Market, By Operating Range |

|

|

Military Robotics Market, By Endurance/Operating Duration |

|

|

Military Robotics Market, By Propulsion System |

|

|

Military Robotics Market, By Technology Integration |

|

|

Military Robotics Market, By Deployment Environment |

|

|

Military Robotics Market, By System Components |

|

|

Military Robotics Market, By End-Use |

|

Frequently Asked Questions

Table of Contents

- 1. Research Methodology and Assumptions

- 1.1. Definitions

- 1.2. Research Design and Approach

- 1.3. Data Collection Methods

- 1.4. Base Estimates and Calculations

- 1.5. Forecasting Models

- 1.5.1. Key Forecast Factors & Impact Analysis

- 1.6. Secondary Research

- 1.6.1. Open Sources

- 1.6.2. Paid Databases

- 1.6.3. Associations

- 1.7. Primary Research

- 1.7.1. Primary Sources

- 1.7.2. Primary Interviews with Stakeholders across Ecosystem

- 2. Executive Summary

- 2.1. Global Military Robotics Market Outlook

- 2.1.1. Military Robotics Market Size Volume (Thousand Units) and Value (US$ Bn), and Forecasts, 2021-2035

- 2.1.2. Compounded Annual Growth Rate Analysis

- 2.1.3. Growth Opportunity Analysis

- 2.1.4. Segmental Share Analysis

- 2.1.5. Geographical Share Analysis

- 2.2. Market Analysis and Facts

- 2.3. Supply-Demand Analysis

- 2.4. Competitive Benchmarking

- 2.5. Go-to- Market Strategy

- 2.5.1. Customer/ End-use Industry Assessment

- 2.5.2. Growth Opportunity Data, 2026-2035

- 2.5.2.1. Regional Data

- 2.5.2.2. Country Data

- 2.5.2.3. Segmental Data

- 2.5.3. Identification of Potential Market Spaces

- 2.5.4. GAP Analysis

- 2.5.5. Potential Attractive Price Points

- 2.5.6. Prevailing Market Risks & Challenges

- 2.5.7. Preferred Sales & Marketing Strategies

- 2.5.8. Key Recommendations and Analysis

- 2.5.9. A Way Forward

- 2.1. Global Military Robotics Market Outlook

- 3. Industry Data and Premium Insights

- 3.1. Global Aerospace & Defense Industry Overview, 2025

- 3.1.1. Industry Ecosystem Analysis

- 3.1.2. Key Trends for Aerospace & Defense Industry

- 3.1.3. Regional Distribution for Aerospace & Defense Industry

- 3.2. Supplier Customer Data

- 3.3. Technology Roadmap and Developments

- 3.4. Trade Analysis

- 3.4.1. Import & Export Analysis, 2025

- 3.4.2. Top Importing Countries

- 3.4.3. Top Exporting Countries

- 3.5. Trump Tariff Impact Analysis

- 3.5.1. Manufacturer

- 3.5.1.1. Based on the component & Raw material

- 3.5.2. Supply Chain

- 3.5.3. End Consumer

- 3.5.1. Manufacturer

- 3.6. Raw Material Analysis

- 3.1. Global Aerospace & Defense Industry Overview, 2025

- 4. Market Overview

- 4.1. Market Dynamics

- 4.1.1. Drivers

- 4.1.1.1. Growing demand for unmanned and autonomous systems to reduce soldier risk and enhance mission effectiveness.

- 4.1.1.2. Rapid advancements in AI, sensors, and autonomous navigation technologies.

- 4.1.1.3. Increasing global defense spending and military modernization initiatives.

- 4.1.2. Restraints

- 4.1.2.1. High development, procurement, and lifecycle maintenance costs.

- 4.1.2.2. Ethical, legal, and regulatory concerns surrounding autonomous weapon systems.

- 4.1.1. Drivers

- 4.2. Key Trend Analysis

- 4.3. Regulatory Framework

- 4.3.1. Key Regulations, Norms, and Subsidies, by Key Countries

- 4.3.2. Tariffs and Standards

- 4.3.3. Impact Analysis of Regulations on the Market

- 4.4. Value Chain Analysis

- 4.4.1. Component Suppliers

- 4.4.2. Manufacturers

- 4.4.3. Technology Integrators

- 4.4.4. Dealers/ Distributors

- 4.4.5. End-Users

- 4.5. Cost Structure Analysis

- 4.5.1. Parameter’s Share for Cost Associated

- 4.5.2. COGP vs COGS

- 4.5.3. Profit Margin Analysis

- 4.6. Pricing Analysis

- 4.6.1. Regional Pricing Analysis

- 4.6.2. Segmental Pricing Trends

- 4.6.3. Factors Influencing Pricing

- 4.7. Porter’s Five Forces Analysis

- 4.8. PESTEL Analysis

- 4.9. Global Military Robotics Market Demand

- 4.9.1. Historical Market Size – Volume (Thousand Units) and Value (US$ Bn), 2020-2024

- 4.9.2. Current and Future Market Size – Volume (Thousand Units) and Value (US$ Bn), 2026–2035

- 4.9.2.1. Y-o-Y Growth Trends

- 4.9.2.2. Absolute $ Opportunity Assessment

- 4.1. Market Dynamics

- 5. Competition Landscape

- 5.1. Competition structure

- 5.1.1. Fragmented v/s consolidated

- 5.2. Company Share Analysis, 2025

- 5.2.1. Global Company Market Share

- 5.2.2. By Region

- 5.2.2.1. North America

- 5.2.2.2. Europe

- 5.2.2.3. Asia Pacific

- 5.2.2.4. Middle East

- 5.2.2.5. Africa

- 5.2.2.6. South America

- 5.3. Product Comparison Matrix

- 5.3.1. Specifications

- 5.3.2. Market Positioning

- 5.3.3. Pricing

- 5.1. Competition structure

- 6. Global Military Robotics Market Analysis, by Platform Type

- 6.1. Key Segment Analysis

- 6.2. Military Robotics Market Size Volume (Thousand Units) and Value (US$ Bn), Analysis, and Forecasts, by Platform Type, 2021-2035

- 6.2.1. Unmanned Ground Vehicles (UGVs)

- 6.2.1.1. Tracked UGVs

- 6.2.1.2. Wheeled UGVs

- 6.2.1.3. Legged UGVs

- 6.2.1.4. Hybrid UGVs

- 6.2.2. Unmanned Aerial Vehicles (UAVs)

- 6.2.2.1. Fixed-wing UAVs

- 6.2.2.2. Rotary-wing UAVs

- 6.2.2.3. Hybrid VTOL UAVs

- 6.2.2.4. Nano/Micro UAVs

- 6.2.3. Unmanned Maritime Vehicles (UMVs)

- 6.2.3.1. Unmanned Surface Vehicles (USVs)

- 6.2.3.2. Unmanned Underwater Vehicles (UUVs)

- 6.2.3.3. Autonomous Underwater Vehicles (AUVs)

- 6.2.4. Unmanned Space Vehicles

- 6.2.1. Unmanned Ground Vehicles (UGVs)

- 7. Global Military Robotics Market Analysis, by Operational Mode

- 7.1. Key Segment Analysis

- 7.2. Military Robotics Market Size Volume (Thousand Units) and Value (US$ Bn), Analysis, and Forecasts, by Operational Mode, 2021-2035

- 7.2.1. Autonomous Systems

- 7.2.1.1. Fully Autonomous

- 7.2.1.2. Semi-Autonomous

- 7.2.2. Remote Controlled Systems

- 7.2.2.1. Line-of-Sight Control

- 7.2.2.2. Beyond Line-of-Sight Control

- 7.2.3. Human-on-the-Loop Systems

- 7.2.4. Swarm Robotics Systems

- 7.2.1. Autonomous Systems

- 8. Global Military Robotics Market Analysis, by Payload Capacity

- 8.1. Key Segment Analysis

- 8.2. Military Robotics Market Size Volume (Thousand Units) and Value (US$ Bn), Analysis, and Forecasts, by Payload Capacity, 2021-2035

- 8.2.1. Up to 50 kg

- 8.2.2. 50-200 kg

- 8.2.3. 200-500 kg

- 8.2.4. Above 500 kg

- 9. Global Military Robotics Market Analysis, by Operating Range

- 9.1. Key Segment Analysis

- 9.2. Military Robotics Market Size Volume (Thousand Units) and Value (US$ Bn), Analysis, and Forecasts, by Operating Range, 2021-2035

- 9.2.1. Up to 10 km

- 9.2.2. 10-50 km

- 9.2.3. 50-200 km

- 9.2.4. Above 200 km

- 10. Global Military Robotics Market Analysis, by Endurance/Operating Duration

- 10.1. Key Segment Analysis

- 10.2. Military Robotics Market Size Volume (Thousand Units) and Value (US$ Bn), Analysis, and Forecasts, by Endurance/Operating Duration, 2021-2035

- 10.2.1. Up to 2 hours

- 10.2.2. 2-8 hours

- 10.2.3. 8-24 hours

- 10.2.4. Above 24 hours

- 11. Global Military Robotics Market Analysis, by Propulsion System

- 11.1. Key Segment Analysis

- 11.2. Military Robotics Market Size Volume (Thousand Units) and Value (US$ Bn), Analysis, and Forecasts, by Propulsion System, 2021-2035

- 11.2.1. Battery-Electric Propulsion

- 11.2.1.1. Lithium-ion Batteries

- 11.2.1.2. Solid-state Batteries

- 11.2.1.3. Fuel Cells

- 11.2.2. Hybrid-Electric Propulsion

- 11.2.3. Internal Combustion Engine

- 11.2.4. Solar-Powered Systems

- 11.2.5. Jet/Turbine Propulsion

- 11.2.1. Battery-Electric Propulsion

- 12. Global Military Robotics Market Analysis, by Technology Integration

- 12.1. Key Segment Analysis

- 12.2. Military Robotics Market Size Volume (Thousand Units) and Value (US$ Bn), Analysis, and Forecasts, by Technology Integration, 2021-2035

- 12.2.1. Artificial Intelligence & Machine Learning

- 12.2.2. Computer Vision & Image Recognition

- 12.2.3. Sensor Fusion Systems

- 12.2.4. Advanced Navigation Systems (GPS/INS)

- 12.2.5. Communication Systems (Radio/Satellite)

- 12.2.6. Weapon Integration Systems

- 13. Global Military Robotics Market Analysis, by Deployment Environment

- 13.1. Key Segment Analysis

- 13.2. Military Robotics Market Size Volume (Thousand Units) and Value (US$ Bn), Analysis, and Forecasts, by Deployment Environment, 2021-2035

- 13.2.1. Land-based Operations

- 13.2.1.1. Desert Terrain

- 13.2.1.2. Urban Terrain

- 13.2.1.3. Forest/Jungle Terrain

- 13.2.1.4. Arctic/Cold Weather

- 13.2.2. Aerial Operations

- 13.2.2.1. Low Altitude

- 13.2.2.2. Medium Altitude

- 13.2.2.3. High Altitude

- 13.2.3. Maritime Operations

- 13.2.3.1. Surface Operations

- 13.2.3.2. Underwater Operations

- 13.2.3.3. Amphibious Operations

- 13.2.1. Land-based Operations

- 14. Global Military Robotics Market Analysis, by System Components

- 14.1. Key Segment Analysis

- 14.2. Military Robotics Market Size Volume (Thousand Units) and Value (US$ Bn), Analysis, and Forecasts, by System Components, 2021-2035

- 14.2.1. Hardware

- 14.2.1.1. Platforms/Chassis

- 14.2.1.2. Sensors & Cameras

- 14.2.1.3. Control Systems

- 14.2.1.4. Propulsion Units

- 14.2.1.5. Power Systems

- 14.2.1.6. Others

- 14.2.2. Software

- 14.2.2.1. Operating Systems

- 14.2.2.2. Mission Planning Software

- 14.2.2.3. Data Analytics Software

- 14.2.2.4. AI/ML Algorithms

- 14.2.2.5. Others

- 14.2.3. Services

- 14.2.3.1. Maintenance & Support

- 14.2.3.2. Training & Simulation

- 14.2.3.3. Upgrades & Modernization

- 14.2.1. Hardware

- 15. Global Military Robotics Market Analysis, by End-Use

- 15.1. Key Segment Analysis

- 15.2. Military Robotics Market Size Volume (Thousand Units) and Value (US$ Bn), Analysis, and Forecasts, by End-Use, 2021-2035

- 15.2.1. Defense Forces

- 15.2.1.1. Army

- 15.2.1.2. Navy

- 15.2.1.3. Air Force

- 15.2.1.4. Special Forces

- 15.2.2. Homeland Security

- 15.2.2.1. Border Patrol & Surveillance

- 15.2.2.2. Counter-Terrorism Operations

- 15.2.2.3. Emergency Response

- 15.2.2.4. Others

- 15.2.3. Law Enforcement

- 15.2.4. Private Military & Security Companies

- 15.2.5. Others

- 15.2.1. Defense Forces

- 16. Global Military Robotics Market Analysis and Forecasts, by Region

- 16.1. Key Findings

- 16.2. Military Robotics Market Size Volume (Thousand Units) and Value (US$ Bn), Analysis, and Forecasts, by Region, 2021-2035

- 16.2.1. North America

- 16.2.2. Europe

- 16.2.3. Asia Pacific

- 16.2.4. Middle East

- 16.2.5. Africa

- 16.2.6. South America

- 17. North America Military Robotics Market Analysis

- 17.1. Key Segment Analysis

- 17.2. Regional Snapshot

- 17.3. North America Military Robotics Market Size- Volume (Thousand Units) and Value (US$ Bn), Analysis, and Forecasts, 2021-2035

- 17.3.1. Platform Type

- 17.3.2. Operational Mode

- 17.3.3. Payload Capacity

- 17.3.4. Operating Range

- 17.3.5. Endurance/Operating Duration

- 17.3.6. Propulsion System

- 17.3.7. Technology Integration

- 17.3.8. Deployment Environment

- 17.3.9. System Components

- 17.3.10. End-Use

- 17.3.11. Country

- 17.3.11.1. USA

- 17.3.11.2. Canada

- 17.3.11.3. Mexico

- 17.4. USA Military Robotics Market

- 17.4.1. Country Segmental Analysis

- 17.4.2. Platform Type

- 17.4.3. Operational Mode

- 17.4.4. Payload Capacity

- 17.4.5. Operating Range

- 17.4.6. Endurance/Operating Duration

- 17.4.7. Propulsion System

- 17.4.8. Technology Integration

- 17.4.9. Deployment Environment

- 17.4.10. System Components

- 17.4.11. End-Use

- 17.5. Canada Military Robotics Market

- 17.5.1. Country Segmental Analysis

- 17.5.2. Platform Type

- 17.5.3. Operational Mode

- 17.5.4. Payload Capacity

- 17.5.5. Operating Range

- 17.5.6. Endurance/Operating Duration

- 17.5.7. Propulsion System

- 17.5.8. Technology Integration

- 17.5.9. Deployment Environment

- 17.5.10. System Components

- 17.5.11. End-Use

- 17.6. Mexico Military Robotics Market

- 17.6.1. Country Segmental Analysis

- 17.6.2. Platform Type

- 17.6.3. Operational Mode

- 17.6.4. Payload Capacity

- 17.6.5. Operating Range

- 17.6.6. Endurance/Operating Duration

- 17.6.7. Propulsion System

- 17.6.8. Technology Integration

- 17.6.9. Deployment Environment

- 17.6.10. System Components

- 17.6.11. End-Use

- 18. Europe Military Robotics Market Analysis

- 18.1. Key Segment Analysis

- 18.2. Regional Snapshot

- 18.3. Europe Military Robotics Market Size Volume (Thousand Units) and Value (US$ Bn), Analysis, and Forecasts, 2021-2035

- 18.3.1. Platform Type

- 18.3.2. Operational Mode

- 18.3.3. Payload Capacity

- 18.3.4. Operating Range

- 18.3.5. Endurance/Operating Duration

- 18.3.6. Propulsion System

- 18.3.7. Technology Integration

- 18.3.8. Deployment Environment

- 18.3.9. System Components

- 18.3.10. End-Use

- 18.3.11. Country

- 18.3.11.1. Germany

- 18.3.11.2. United Kingdom

- 18.3.11.3. France

- 18.3.11.4. Italy

- 18.3.11.5. Spain

- 18.3.11.6. Netherlands

- 18.3.11.7. Nordic Countries

- 18.3.11.8. Poland

- 18.3.11.9. Russia & CIS

- 18.3.11.10. Rest of Europe

- 18.4. Germany Military Robotics Market

- 18.4.1. Country Segmental Analysis

- 18.4.2. Platform Type

- 18.4.3. Operational Mode

- 18.4.4. Payload Capacity

- 18.4.5. Operating Range

- 18.4.6. Endurance/Operating Duration

- 18.4.7. Propulsion System

- 18.4.8. Technology Integration

- 18.4.9. Deployment Environment

- 18.4.10. System Components

- 18.4.11. End-Use

- 18.5. United Kingdom Military Robotics Market

- 18.5.1. Country Segmental Analysis

- 18.5.2. Platform Type

- 18.5.3. Operational Mode

- 18.5.4. Payload Capacity

- 18.5.5. Operating Range

- 18.5.6. Endurance/Operating Duration

- 18.5.7. Propulsion System

- 18.5.8. Technology Integration

- 18.5.9. Deployment Environment

- 18.5.10. System Components

- 18.5.11. End-Use

- 18.6. France Military Robotics Market

- 18.6.1. Country Segmental Analysis

- 18.6.2. Platform Type

- 18.6.3. Operational Mode

- 18.6.4. Payload Capacity

- 18.6.5. Operating Range

- 18.6.6. Endurance/Operating Duration

- 18.6.7. Propulsion System

- 18.6.8. Technology Integration

- 18.6.9. Deployment Environment

- 18.6.10. System Components

- 18.6.11. End-Use

- 18.7. Italy Military Robotics Market

- 18.7.1. Country Segmental Analysis

- 18.7.2. Platform Type

- 18.7.3. Operational Mode

- 18.7.4. Payload Capacity

- 18.7.5. Operating Range

- 18.7.6. Endurance/Operating Duration

- 18.7.7. Propulsion System

- 18.7.8. Technology Integration

- 18.7.9. Deployment Environment

- 18.7.10. System Components

- 18.7.11. End-Use

- 18.8. Spain Military Robotics Market

- 18.8.1. Country Segmental Analysis

- 18.8.2. Platform Type

- 18.8.3. Operational Mode

- 18.8.4. Payload Capacity

- 18.8.5. Operating Range

- 18.8.6. Endurance/Operating Duration

- 18.8.7. Propulsion System

- 18.8.8. Technology Integration

- 18.8.9. Deployment Environment

- 18.8.10. System Components

- 18.8.11. End-Use

- 18.9. Netherlands Military Robotics Market

- 18.9.1. Country Segmental Analysis

- 18.9.2. Platform Type

- 18.9.3. Operational Mode

- 18.9.4. Payload Capacity

- 18.9.5. Operating Range

- 18.9.6. Endurance/Operating Duration

- 18.9.7. Propulsion System

- 18.9.8. Technology Integration

- 18.9.9. Deployment Environment

- 18.9.10. System Components

- 18.9.11. End-Use

- 18.10. Nordic Countries Military Robotics Market

- 18.10.1. Country Segmental Analysis

- 18.10.2. Platform Type

- 18.10.3. Operational Mode

- 18.10.4. Payload Capacity

- 18.10.5. Operating Range

- 18.10.6. Endurance/Operating Duration

- 18.10.7. Propulsion System

- 18.10.8. Technology Integration

- 18.10.9. Deployment Environment

- 18.10.10. System Components

- 18.10.11. End-Use

- 18.11. Poland Military Robotics Market

- 18.11.1. Country Segmental Analysis

- 18.11.2. Platform Type

- 18.11.3. Operational Mode

- 18.11.4. Payload Capacity

- 18.11.5. Operating Range

- 18.11.6. Endurance/Operating Duration

- 18.11.7. Propulsion System

- 18.11.8. Technology Integration

- 18.11.9. Deployment Environment

- 18.11.10. System Components

- 18.11.11. End-Use

- 18.12. Russia & CIS Military Robotics Market

- 18.12.1. Country Segmental Analysis

- 18.12.2. Platform Type

- 18.12.3. Operational Mode

- 18.12.4. Payload Capacity

- 18.12.5. Operating Range

- 18.12.6. Endurance/Operating Duration

- 18.12.7. Propulsion System

- 18.12.8. Technology Integration

- 18.12.9. Deployment Environment

- 18.12.10. System Components

- 18.12.11. End-Use

- 18.13. Rest of Europe Military Robotics Market

- 18.13.1. Country Segmental Analysis

- 18.13.2. Platform Type

- 18.13.3. Operational Mode

- 18.13.4. Payload Capacity

- 18.13.5. Operating Range

- 18.13.6. Endurance/Operating Duration

- 18.13.7. Propulsion System

- 18.13.8. Technology Integration

- 18.13.9. Deployment Environment

- 18.13.10. System Components

- 18.13.11. End-Use

- 19. Asia Pacific Military Robotics Market Analysis

- 19.1. Key Segment Analysis

- 19.2. Regional Snapshot

- 19.3. Asia Pacific Military Robotics Market Size Volume (Thousand Units) and Value (US$ Bn), Analysis, and Forecasts, 2021-2035

- 19.3.1. Platform Type

- 19.3.2. Operational Mode

- 19.3.3. Payload Capacity

- 19.3.4. Operating Range

- 19.3.5. Endurance/Operating Duration

- 19.3.6. Propulsion System

- 19.3.7. Technology Integration

- 19.3.8. Deployment Environment

- 19.3.9. System Components

- 19.3.10. End-Use

- 19.3.11. Country

- 19.3.11.1. China

- 19.3.11.2. India

- 19.3.11.3. Japan

- 19.3.11.4. South Korea

- 19.3.11.5. Australia and New Zealand

- 19.3.11.6. Indonesia

- 19.3.11.7. Malaysia

- 19.3.11.8. Thailand

- 19.3.11.9. Vietnam

- 19.3.11.10. Rest of Asia Pacific

- 19.4. China Military Robotics Market

- 19.4.1. Country Segmental Analysis

- 19.4.2. Platform Type

- 19.4.3. Operational Mode

- 19.4.4. Payload Capacity

- 19.4.5. Operating Range

- 19.4.6. Endurance/Operating Duration

- 19.4.7. Propulsion System

- 19.4.8. Technology Integration

- 19.4.9. Deployment Environment

- 19.4.10. System Components

- 19.4.11. End-Use

- 19.5. India Military Robotics Market

- 19.5.1. Country Segmental Analysis

- 19.5.2. Platform Type

- 19.5.3. Operational Mode

- 19.5.4. Payload Capacity

- 19.5.5. Operating Range

- 19.5.6. Endurance/Operating Duration

- 19.5.7. Propulsion System

- 19.5.8. Technology Integration

- 19.5.9. Deployment Environment

- 19.5.10. System Components

- 19.5.11. End-Use

- 19.6. Japan Military Robotics Market

- 19.6.1. Country Segmental Analysis

- 19.6.2. Platform Type

- 19.6.3. Operational Mode

- 19.6.4. Payload Capacity

- 19.6.5. Operating Range

- 19.6.6. Endurance/Operating Duration

- 19.6.7. Propulsion System

- 19.6.8. Technology Integration

- 19.6.9. Deployment Environment

- 19.6.10. System Components

- 19.6.11. End-Use

- 19.7. South Korea Military Robotics Market

- 19.7.1. Country Segmental Analysis

- 19.7.2. Platform Type

- 19.7.3. Operational Mode

- 19.7.4. Payload Capacity

- 19.7.5. Operating Range

- 19.7.6. Endurance/Operating Duration

- 19.7.7. Propulsion System

- 19.7.8. Technology Integration

- 19.7.9. Deployment Environment

- 19.7.10. System Components

- 19.7.11. End-Use

- 19.8. Australia and New Zealand Military Robotics Market

- 19.8.1. Country Segmental Analysis

- 19.8.2. Platform Type

- 19.8.3. Operational Mode

- 19.8.4. Payload Capacity

- 19.8.5. Operating Range

- 19.8.6. Endurance/Operating Duration

- 19.8.7. Propulsion System

- 19.8.8. Technology Integration

- 19.8.9. Deployment Environment

- 19.8.10. System Components

- 19.8.11. End-Use

- 19.9. Indonesia Military Robotics Market

- 19.9.1. Country Segmental Analysis

- 19.9.2. Platform Type

- 19.9.3. Operational Mode

- 19.9.4. Payload Capacity

- 19.9.5. Operating Range

- 19.9.6. Endurance/Operating Duration

- 19.9.7. Propulsion System

- 19.9.8. Technology Integration

- 19.9.9. Deployment Environment

- 19.9.10. System Components

- 19.9.11. End-Use

- 19.10. Malaysia Military Robotics Market

- 19.10.1. Country Segmental Analysis

- 19.10.2. Platform Type

- 19.10.3. Operational Mode

- 19.10.4. Payload Capacity

- 19.10.5. Operating Range

- 19.10.6. Endurance/Operating Duration

- 19.10.7. Propulsion System

- 19.10.8. Technology Integration

- 19.10.9. Deployment Environment

- 19.10.10. System Components

- 19.10.11. End-Use

- 19.11. Thailand Military Robotics Market

- 19.11.1. Country Segmental Analysis

- 19.11.2. Platform Type

- 19.11.3. Operational Mode

- 19.11.4. Payload Capacity

- 19.11.5. Operating Range

- 19.11.6. Endurance/Operating Duration

- 19.11.7. Propulsion System

- 19.11.8. Technology Integration

- 19.11.9. Deployment Environment

- 19.11.10. System Components

- 19.11.11. End-Use

- 19.12. Vietnam Military Robotics Market

- 19.12.1. Country Segmental Analysis

- 19.12.2. Platform Type

- 19.12.3. Operational Mode

- 19.12.4. Payload Capacity

- 19.12.5. Operating Range

- 19.12.6. Endurance/Operating Duration

- 19.12.7. Propulsion System

- 19.12.8. Technology Integration

- 19.12.9. Deployment Environment

- 19.12.10. System Components

- 19.12.11. End-Use

- 19.13. Rest of Asia Pacific Military Robotics Market

- 19.13.1. Country Segmental Analysis

- 19.13.2. Platform Type

- 19.13.3. Operational Mode

- 19.13.4. Payload Capacity

- 19.13.5. Operating Range

- 19.13.6. Endurance/Operating Duration

- 19.13.7. Propulsion System

- 19.13.8. Technology Integration

- 19.13.9. Deployment Environment

- 19.13.10. System Components

- 19.13.11. End-Use

- 20. Middle East Military Robotics Market Analysis

- 20.1. Key Segment Analysis

- 20.2. Regional Snapshot

- 20.3. Middle East Military Robotics Market Size Volume (Thousand Units) and Value (US$ Bn), Analysis, and Forecasts, 2021-2035

- 20.3.1. Platform Type

- 20.3.2. Operational Mode

- 20.3.3. Payload Capacity

- 20.3.4. Operating Range

- 20.3.5. Endurance/Operating Duration

- 20.3.6. Propulsion System

- 20.3.7. Technology Integration

- 20.3.8. Deployment Environment

- 20.3.9. System Components

- 20.3.10. End-Use

- 20.3.11. Country

- 20.3.11.1. Turkey

- 20.3.11.2. UAE

- 20.3.11.3. Saudi Arabia

- 20.3.11.4. Israel

- 20.3.11.5. Rest of Middle East

- 20.4. Turkey Military Robotics Market

- 20.4.1. Country Segmental Analysis

- 20.4.2. Platform Type

- 20.4.3. Operational Mode

- 20.4.4. Payload Capacity

- 20.4.5. Operating Range

- 20.4.6. Endurance/Operating Duration

- 20.4.7. Propulsion System

- 20.4.8. Technology Integration

- 20.4.9. Deployment Environment

- 20.4.10. System Components

- 20.4.11. End-Use

- 20.5. UAE Military Robotics Market

- 20.5.1. Country Segmental Analysis

- 20.5.2. Platform Type

- 20.5.3. Operational Mode

- 20.5.4. Payload Capacity

- 20.5.5. Operating Range

- 20.5.6. Endurance/Operating Duration

- 20.5.7. Propulsion System

- 20.5.8. Technology Integration

- 20.5.9. Deployment Environment

- 20.5.10. System Components

- 20.5.11. End-Use

- 20.6. Saudi Arabia Military Robotics Market

- 20.6.1. Country Segmental Analysis

- 20.6.2. Platform Type

- 20.6.3. Operational Mode

- 20.6.4. Payload Capacity

- 20.6.5. Operating Range

- 20.6.6. Endurance/Operating Duration

- 20.6.7. Propulsion System

- 20.6.8. Technology Integration

- 20.6.9. Deployment Environment

- 20.6.10. System Components

- 20.6.11. End-Use

- 20.7. Israel Military Robotics Market

- 20.7.1. Country Segmental Analysis

- 20.7.2. Platform Type

- 20.7.3. Operational Mode

- 20.7.4. Payload Capacity

- 20.7.5. Operating Range

- 20.7.6. Endurance/Operating Duration

- 20.7.7. Propulsion System

- 20.7.8. Technology Integration

- 20.7.9. Deployment Environment

- 20.7.10. System Components

- 20.7.11. End-Use

- 20.8. Rest of Middle East Military Robotics Market

- 20.8.1. Country Segmental Analysis

- 20.8.2. Platform Type

- 20.8.3. Operational Mode

- 20.8.4. Payload Capacity

- 20.8.5. Operating Range

- 20.8.6. Endurance/Operating Duration

- 20.8.7. Propulsion System

- 20.8.8. Technology Integration

- 20.8.9. Deployment Environment

- 20.8.10. System Components

- 20.8.11. End-Use

- 21. Africa Military Robotics Market Analysis

- 21.1. Key Segment Analysis

- 21.2. Regional Snapshot

- 21.3. Africa Military Robotics Market Size Volume (Thousand Units) and Value (US$ Bn), Analysis, and Forecasts, 2021-2035

- 21.3.1. Platform Type

- 21.3.2. Operational Mode

- 21.3.3. Payload Capacity

- 21.3.4. Operating Range

- 21.3.5. Endurance/Operating Duration

- 21.3.6. Propulsion System

- 21.3.7. Technology Integration

- 21.3.8. Deployment Environment

- 21.3.9. System Components

- 21.3.10. End-Use

- 21.3.11. country

- 21.3.11.1. South Africa

- 21.3.11.2. Egypt

- 21.3.11.3. Nigeria

- 21.3.11.4. Algeria

- 21.3.11.5. Rest of Africa

- 21.4. South Africa Military Robotics Market

- 21.4.1. Country Segmental Analysis

- 21.4.2. Platform Type

- 21.4.3. Operational Mode

- 21.4.4. Payload Capacity

- 21.4.5. Operating Range

- 21.4.6. Endurance/Operating Duration

- 21.4.7. Propulsion System

- 21.4.8. Technology Integration

- 21.4.9. Deployment Environment

- 21.4.10. System Components

- 21.4.11. End-Use

- 21.5. Egypt Military Robotics Market

- 21.5.1. Country Segmental Analysis

- 21.5.2. Platform Type

- 21.5.3. Operational Mode

- 21.5.4. Payload Capacity

- 21.5.5. Operating Range

- 21.5.6. Endurance/Operating Duration

- 21.5.7. Propulsion System

- 21.5.8. Technology Integration

- 21.5.9. Deployment Environment

- 21.5.10. System Components

- 21.5.11. End-Use

- 21.6. Nigeria Military Robotics Market

- 21.6.1. Country Segmental Analysis

- 21.6.2. Platform Type

- 21.6.3. Operational Mode

- 21.6.4. Payload Capacity

- 21.6.5. Operating Range

- 21.6.6. Endurance/Operating Duration

- 21.6.7. Propulsion System

- 21.6.8. Technology Integration

- 21.6.9. Deployment Environment

- 21.6.10. System Components

- 21.6.11. End-Use

- 21.7. Algeria Military Robotics Market

- 21.7.1. Country Segmental Analysis

- 21.7.2. Platform Type

- 21.7.3. Operational Mode

- 21.7.4. Payload Capacity

- 21.7.5. Operating Range

- 21.7.6. Endurance/Operating Duration

- 21.7.7. Propulsion System

- 21.7.8. Technology Integration

- 21.7.9. Deployment Environment

- 21.7.10. System Components

- 21.7.11. End-Use

- 21.8. Rest of Africa Military Robotics Market

- 21.8.1. Country Segmental Analysis

- 21.8.2. Platform Type

- 21.8.3. Operational Mode

- 21.8.4. Payload Capacity

- 21.8.5. Operating Range

- 21.8.6. Endurance/Operating Duration

- 21.8.7. Propulsion System

- 21.8.8. Technology Integration

- 21.8.9. Deployment Environment

- 21.8.10. System Components

- 21.8.11. End-Use

- 22. South America Military Robotics Market Analysis

- 22.1. Key Segment Analysis

- 22.2. Regional Snapshot

- 22.3. South America Military Robotics Market Size Volume (Thousand Units) and Value (US$ Bn), Analysis, and Forecasts, 2021-2035

- 22.3.1. Platform Type

- 22.3.2. Operational Mode

- 22.3.3. Payload Capacity

- 22.3.4. Operating Range

- 22.3.5. Endurance/Operating Duration

- 22.3.6. Propulsion System

- 22.3.7. Technology Integration

- 22.3.8. Deployment Environment

- 22.3.9. System Components

- 22.3.10. End-Use

- 22.3.11. Country

- 22.3.11.1. Brazil

- 22.3.11.2. Argentina

- 22.3.11.3. Rest of South America

- 22.4. Brazil Military Robotics Market

- 22.4.1. Country Segmental Analysis

- 22.4.2. Platform Type

- 22.4.3. Operational Mode

- 22.4.4. Payload Capacity

- 22.4.5. Operating Range

- 22.4.6. Endurance/Operating Duration

- 22.4.7. Propulsion System

- 22.4.8. Technology Integration

- 22.4.9. Deployment Environment

- 22.4.10. System Components

- 22.4.11. End-Use

- 22.5. Argentina Military Robotics Market

- 22.5.1. Country Segmental Analysis

- 22.5.2. Platform Type

- 22.5.3. Operational Mode

- 22.5.4. Payload Capacity

- 22.5.5. Operating Range

- 22.5.6. Endurance/Operating Duration

- 22.5.7. Propulsion System

- 22.5.8. Technology Integration

- 22.5.9. Deployment Environment

- 22.5.10. System Components

- 22.5.11. End-Use

- 22.6. Rest of South America Military Robotics Market

- 22.6.1. Country Segmental Analysis

- 22.6.2. Platform Type

- 22.6.3. Operational Mode

- 22.6.4. Payload Capacity

- 22.6.5. Operating Range

- 22.6.6. Endurance/Operating Duration

- 22.6.7. Propulsion System

- 22.6.8. Technology Integration

- 22.6.9. Deployment Environment

- 22.6.10. System Components

- 22.6.11. End-Use

- 23. Key Players/ Company Profile

- 23.1. AeroVironment Inc.

- 23.1.1. Company Details/ Overview

- 23.1.2. Company Financials

- 23.1.3. Key Customers and Competitors

- 23.1.4. Business/ Industry Portfolio

- 23.1.5. Product Portfolio/ Specification Details

- 23.1.6. Pricing Data

- 23.1.7. Strategic Overview

- 23.1.8. Recent Developments

- 23.2. BAE Systems plc

- 23.3. Boston Dynamics Inc.

- 23.4. Clearpath Robotics Inc.

- 23.5. Elbit Systems Ltd.

- 23.6. FLIR Systems Inc. (Teledyne FLIR)

- 23.7. General Dynamics Corporation

- 23.8. Israel Aerospace Industries Ltd.

- 23.9. Kratos Defense & Security Solutions Inc.

- 23.10. L3Harris Technologies Inc.

- 23.11. Leonardo S.p.A.

- 23.12. Lockheed Martin Corporation

- 23.13. Northrop Grumman Corporation

- 23.14. QinetiQ Group plc

- 23.15. Raytheon Technologies Corporation

- 23.16. Rheinmetall AG

- 23.17. Saab AB

- 23.18. Textron Inc.

- 23.19. Thales Group

- 23.20. The Boeing Company

- 23.21. Turkish Aerospace Industries Inc.

- 23.22. Other Key Players

- 23.1. AeroVironment Inc.

Note* - This is just tentative list of players. While providing the report, we will cover more number of players based on their revenue and share for each geography

Research Design

Our research design integrates both demand-side and supply-side analysis through a balanced combination of primary and secondary research methodologies. By utilizing both bottom-up and top-down approaches alongside rigorous data triangulation methods, we deliver robust market intelligence that supports strategic decision-making.

MarketGenics' comprehensive research design framework ensures the delivery of accurate, reliable, and actionable market intelligence. Through the integration of multiple research approaches, rigorous validation processes, and expert analysis, we provide our clients with the insights needed to make informed strategic decisions and capitalize on market opportunities.

MarketGenics leverages a dedicated industry panel of experts and a comprehensive suite of paid databases to effectively collect, consolidate, and analyze market intelligence.

Our approach has consistently proven to be reliable and effective in generating accurate market insights, identifying key industry trends, and uncovering emerging business opportunities.

Through both primary and secondary research, we capture and analyze critical company-level data such as manufacturing footprints, including technical centers, R&D facilities, sales offices, and headquarters.

Our expert panel further enhances our ability to estimate market size for specific brands based on validated field-level intelligence.

Our data mining techniques incorporate both parametric and non-parametric methods, allowing for structured data collection, sorting, processing, and cleaning.

Demand projections are derived from large-scale data sets analyzed through proprietary algorithms, culminating in robust and reliable market sizing.

Research Approach

The bottom-up approach builds market estimates by starting with the smallest addressable market units and systematically aggregating them to create comprehensive market size projections.

This method begins with specific, granular data points and builds upward to create the complete market landscape.

Customer Analysis → Segmental Analysis → Geographical Analysis

The top-down approach starts with the broadest possible market data and systematically narrows it down through a series of filters and assumptions to arrive at specific market segments or opportunities.

This method begins with the big picture and works downward to increasingly specific market slices.

TAM → SAM → SOM

Research Methods

Desk / Secondary Research

While analysing the market, we extensively study secondary sources, directories, and databases to identify and collect information useful for this technical, market-oriented, and commercial report. Secondary sources that we utilize are not only the public sources, but it is a combination of Open Source, Associations, Paid Databases, MG Repository & Knowledgebase, and others.

- Company websites, annual reports, financial reports, broker reports, and investor presentations

- National government documents, statistical databases and reports

- News articles, press releases and web-casts specific to the companies operating in the market, Magazines, reports, and others

- We gather information from commercial data sources for deriving company specific data such as segmental revenue, share for geography, product revenue, and others

- Internal and external proprietary databases (industry-specific), relevant patent, and regulatory databases

- Governing Bodies, Government Organizations

- Relevant Authorities, Country-specific Associations for Industries

We also employ the model mapping approach to estimate the product level market data through the players' product portfolio

Primary Research

Primary research/ interviews is vital in analyzing the market. Most of the cases involves paid primary interviews. Primary sources include primary interviews through e-mail interactions, telephonic interviews, surveys as well as face-to-face interviews with the different stakeholders across the value chain including several industry experts.

| Type of Respondents | Number of Primaries |

|---|---|

| Tier 2/3 Suppliers | ~20 |

| Tier 1 Suppliers | ~25 |

| End-users | ~25 |

| Industry Expert/ Panel/ Consultant | ~30 |

| Total | ~100 |

MG Knowledgebase

• Repository of industry blog, newsletter and case studies

• Online platform covering detailed market reports, and company profiles

Forecasting Factors and Models

Forecasting Factors

- Historical Trends – Past market patterns, cycles, and major events that shaped how markets behave over time. Understanding past trends helps predict future behavior.

- Industry Factors – Specific characteristics of the industry like structure, regulations, and innovation cycles that affect market dynamics.

- Macroeconomic Factors – Economic conditions like GDP growth, inflation, and employment rates that affect how much money people have to spend.

- Demographic Factors – Population characteristics like age, income, and location that determine who can buy your product.

- Technology Factors – How quickly people adopt new technology and how much technology infrastructure exists.

- Regulatory Factors – Government rules, laws, and policies that can help or restrict market growth.

- Competitive Factors – Analyzing competition structure such as degree of competition and bargaining power of buyers and suppliers.

Forecasting Models / Techniques

Multiple Regression Analysis

- Identify and quantify factors that drive market changes

- Statistical modeling to establish relationships between market drivers and outcomes

Time Series Analysis – Seasonal Patterns

- Understand regular cyclical patterns in market demand

- Advanced statistical techniques to separate trend, seasonal, and irregular components

Time Series Analysis – Trend Analysis

- Identify underlying market growth patterns and momentum

- Statistical analysis of historical data to project future trends

Expert Opinion – Expert Interviews

- Gather deep industry insights and contextual understanding

- In-depth interviews with key industry stakeholders

Multi-Scenario Development

- Prepare for uncertainty by modeling different possible futures

- Creating optimistic, pessimistic, and most likely scenarios

Time Series Analysis – Moving Averages

- Sophisticated forecasting for complex time series data

- Auto-regressive integrated moving average models with seasonal components

Econometric Models

- Apply economic theory to market forecasting

- Sophisticated economic models that account for market interactions

Expert Opinion – Delphi Method

- Harness collective wisdom of industry experts

- Structured, multi-round expert consultation process

Monte Carlo Simulation

- Quantify uncertainty and probability distributions

- Thousands of simulations with varying input parameters

Research Analysis

Our research framework is built upon the fundamental principle of validating market intelligence from both demand and supply perspectives. This dual-sided approach ensures comprehensive market understanding and reduces the risk of single-source bias.

Demand-Side Analysis: We understand end-user/application behavior, preferences, and market needs along with the penetration of the product for specific application.

Supply-Side Analysis: We estimate overall market revenue, analyze the segmental share along with industry capacity, competitive landscape, and market structure.

Validation & Evaluation

Data triangulation is a validation technique that uses multiple methods, sources, or perspectives to examine the same research question, thereby increasing the credibility and reliability of research findings. In market research, triangulation serves as a quality assurance mechanism that helps identify and minimize bias, validate assumptions, and ensure accuracy in market estimates.

- Data Source Triangulation – Using multiple data sources to examine the same phenomenon

- Methodological Triangulation – Using multiple research methods to study the same research question

- Investigator Triangulation – Using multiple researchers or analysts to examine the same data

- Theoretical Triangulation – Using multiple theoretical perspectives to interpret the same data

Custom Market Research Services

We will customise the research for you, in case the report listed above does not meet your requirements.

Get 10% Free Customisation