Food Grade Alcohol (Ethanol) Market Size, Share & Trends Analysis Report by Purity Level (95% Ethanol, 96% Ethanol, 99% Ethanol, 99.5% Ethanol, 99.9% Ethanol (Ultra-pure)), Source/Feedstock, Production Process, Form, Rated Capacity (Production Volume), Packaging Type, Distribution Channel, Storage Temperature Requirements, End-Use, and Geography (North America, Europe, Asia Pacific, Middle East, Africa, and South America) – Global Industry Data, Trends, and Forecasts, 2026–2035

|

|

|

Segmental Data Insights |

|

|

Demand Trends |

|

|

Competitive Landscape |

|

|

Strategic Development |

|

|

Future Outlook & Opportunities |

|

Food Grade Alcohol (Ethanol) Market Size, Share, and Growth

The global food grade alcohol (ethanol) market is experiencing robust growth, with its estimated value of ~USD 3 billion in the year 2025 and USD 3.9 billion by the period 2035, registering a CAGR of 2.7%, during the forecast period. The global food grade alcohol (ethanol) market is expanding with the industries focusing on purity, safety and certification to be used in the beverage, flavor, extracts, pharmaceutical, and personal care sectors. The increase in the consumption of clean-label ingredients, sustainable production based on bio-products, and traceable supply chains is driving manufacturers to more sophisticated distillation and acceptable fermentation procedures. This change will provide stability of quality and reliability in a wide range of end-use applications.

Russ Zeeck, co-founder and COO, explains that, Precision fermentation is revolutionizing protein production with sustainable and efficient alternatives to traditional protein production.” He adds that global market adoption is driven by growing consumer awareness and demand for eco-friendly products, while untapped markets present strong opportunities for expansion across food, nutraceuticals, enzymes, fertilizers, and soil microbiome applications.

The food grade alcohol (ethanol) industry is moving beyond being a commodity input to a strategic facilitator of brand distinction, regulatory security and high-quality formulation across the pharmaceuticals, nutraceuticals, beverages, functional foods and personal care products. The growing attention to purity profiles, solvent safety, organoleptic stability, and free of contamination processing is pressuring producers to remodel their production, distillation and dehydration models. The excessive litigation risk associated with adulteration, residue limits and solvent traces is forcing manufacturers to switch to validated logic of purification as opposed to traditional single-stage distillation, and ethanol quality is now a fundamental factor of product credibility and export preparedness.

The conflict between high purity and sustainability goals is pushing to a deeper level of material and process innovation within the ethanol value chain. Manufacturers are moving to renewable feedstock, low-carbon fermentation, enzyme-enhanced conversion and solvent-free filtration systems that satisfy world food-pharma standards but also promote the goals of a circular-economy. The accelerated technological improvements including high-performance rectification columns, molecular-sieve dehydration and energy-efficient recovery are facilitating the consistency of high-purity performance, enhanced batch reproducibility, and smaller operational footprints of both high-volume and specialty manufacturers.

The purification systems are being automated and digital quality control, and standard regulatory systems are making production easier, enhancing the quality of supply worldwide, and promoting market growth in places with increasing pharmaceutical, beverage, and nutraceutical production. Collectively, these developments make food grade alcohol (ethanol) a strategic initiative of product integrity and competitive differentiation that is way beyond its traditional functions as a base solvent.

Food Grade Alcohol (Ethanol) Market Dynamics and Trends

Driver: Rising Demand in Pharmaceuticals and Beverages

-

Global food grade alcohol (ethanol) market is growing at a rapid pace as more pharmaceutical, nutraceutical and beverage companies have turned to high-purity ethanol in formulations, extraction procedures, sanitizing solutions, botanical extracts and high-quality beverage mixes. The increase in the manufacturing of OTC syrups, herbal tinctures, ready-to-drink drinks, and functional nutrition products has further served to increase the use of ethanol in the regulated markets.

- To accommodate this demand, manufacturers are improving purification, rectification and dehydration technologies to provide consistent high quality ethanol with low impurity levels, neutral sensory characteristics and consistent performance in a wide range of applications. Ethanol suppliers are also responding to the pressure of demanding the ethanol to be of the highest specifications with the help of investments in process optimization and quality-controlled manufacturing.

- The consumer inclination towards natural ingredients, clean-label formulations and quality of the beverage is enhancing the importance of ethanol as a necessary solvent and processing aid. Its wide application in extraction, preservation, flavor improvement and formulation stability is propelling its use in greater applications in pharmaceutical, nutraceutical and beverage industries around the globe.

Restraint: Regulatory Compliance and Safety Challenges

-

Food grade alcohol (ethanol) market is experiencing an increase in compliance requirements as regulatory bodies worldwide squeeze the screws on methanol, aldehydes, heavy metals and microbial contaminations. To attain a steady pharma- and food-grade purity, further distillation, dehydration and continuous monitoring systems are essential further incurring operation and capital expenses, particularly in the case of mid-scale manufacturers.

- The regulatory difference of countries that include varying FCC, USP, EU, and Codex requirements further complicate formulation, documentation and export processes. Routine validations, batch tests, preparation of audits, and certifications of the facilities raise indirect costs and time-to-market of beverage, pharmaceutical, and nutraceutical applications.

- All of these challenges contribute to the market's limited growth, particularly for manufacturers in emerging economies that confront poor infrastructure and significant compliance investment costs.

Opportunity: Growth in Clean-Label and Natural Products

-

The demand in global food grade alcohol (ethanol) is changing towards clean-label, minimally processed, and traceable origins inputs as food, beverage, nutraceutical and extraction companies formulates shift into transparency. In support of regulatory impetuses on disclosure of ingredients and retailer clean-label scorecards, manufacturers are urgently in need of low-impurity, allergen-free, non-synthetic ethanol that fits the free-from and natural positioning.

- The manufacturers too are creating to combine natural sourcing and functional purity. For instance, CropEnergies AG that has increased its range of specialty alcohol that is produced using certified sustainable grain, to help clean-label beverages and botanicals, with bio-origin verification and low levels of congeneres. These products not only increase the transparency of the brands, but also improve extraction performance, which indicates that the industry in general is shifting to differentiation based on ingredient authenticity and purity.

- Advancements in bio-fermentation, enzymatic purification, and impurity-reduction technologies enable manufacturers to make clean-label ethanol with lower residues and better assurance of its natural origin. Clean-label food grade alcohol (ethanol) is emerging as a key development opportunity globally, as brands and merchants want verified-pure ingredients.

Key Trend: Advanced Purification and Specialty Grades

-

The food grade alcohol (ethanol) market is moving to high purity speciality grade ethanol with specifications that are accurate in pharmaceutical, nutraceutical and functional beverage use. Strict distillation, filtration and molecular-sieving technologies guarantee the uniform quality, reduce impurities, and increase compatibility with sensitive formulations, which increases regulatory compliance and product performance.

- Manufacturers are implementing real-time quality control and analytics on production lines, which provides the opportunity to detect the level of contaminants instantly, its concentration differences, and storage environments. For instance, in 2025, one of the largest producers of ethanol installed continuous distillation sensors, which monitor the purity of the batch during the whole process, giving operators the opportunity to change the process on the fly, which would guarantee stable and high-grade production to higher-end uses.

- High-purity ethanol is being used to differentiate, serve specialty formulations, clean-label products, and sensitive pharmaceutical uses, and create new opportunities in innovative, environmental-friendly, and traceable production systems in global markets.

Food-Grade-Alcohol-(Ethanol)-Market Analysis and Segmental Data

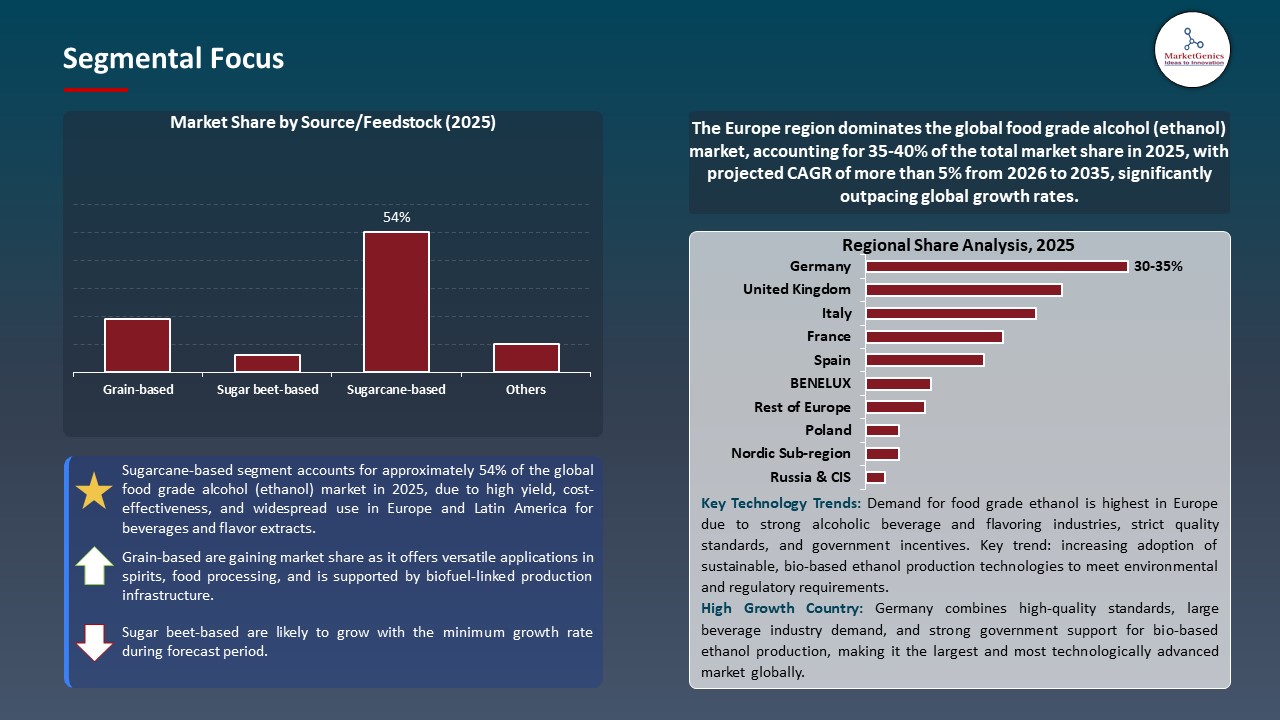

Sugarcane-based Dominate Global Food Grade Alcohol (Ethanol) Market

-

Sugarcane-based segment dominates the food grade alcohol (ethanol) market owing to its high purity, renewable and its applicability in the pharmaceuticals, nutraceuticals, household chemicals and beverage market. It is the best, as maintained, which makes it adhere to the international regulatory standards in promoting safe production, distribution, and consumption.

- The sugarcane ethanol is environmentally friendly and suit the increasing industry and customer expectation of sustainable and renewable sources and hence is a solution of choice among manufacturers that are in need of environmentally friendly alternatives. The production scalability and the integration in the contemporary processing systems improves operational efficiency and reliability in the supply-chain of various sectors.

- Sugarcane-ethanols have been found to ensure stability of products in use in the pharmaceutical, nutraceutical and functional beverage sector across the globe. Sugarcane ethanol is influencing the market of food-grade alcohol as a safe, consistent, and eco-friendly base ingredient in that manner.

Europe Leads Global Food Grade Alcohol (Ethanol) Market Demand

-

The Europe dominates the food grade alcohol (ethanol) market, with a high level of regulation like the REACH and CLP regulations, consumer awareness on product safety and strong demand in the pharmaceutical and OTC drugs, nutraceutical, household chemicals as well as cannabis-derived products. The presence of developed healthcare systems and developed retail chains contribute to the steady process of adopting high-purity ethanol in various implementation areas.

- The well-established pharmaceutical and nutraceutical industries in the region are highly dependent on food grade alcohol in terms of formulations, extractions, and preservative purposes. The high volume of prescription and non-prescription products guarantees the influence of the demand and the growth of market is supported by the increased attention to functional drinks, botanical extracts, and high-value nutraceuticals.

- Europe offers benefits such as local manufacture, research, and development, leading to high quality and regulatory compliance. These factors provide a steady supply of high purity ethanol, help Europe define global market trends, and influence the shift toward the use of food grade alcohol in sensitive and high-value applications.

Food-Grade-Alcohol-(Ethanol)-Market Ecosystem

Multinational ingredient suppliers, niche solution providers to the pharmaceutical, food and beverages, chemical and nutraceutical segments are some of the factors that make the global food grade alcohol (ethanol) market moderately fragmented. ADM, Cargill, Incorporated, BASF SE, The Andersons, Inc., and Chr. Hansen are the major suppliers, providing beverage and food processing grade as well as specialty ethanol. Their strong international manufacturing circuits, sustained research, and regulation skills allow them uniform quality, innovation and scale with various end-use sectors.

Food-grade alcohol (ethanol) value chain includes suppliers of raw material (corn, sugarcane, and grains), ethanol manufacturer, purification and formulation team, brand holder and food, beverage and pharmaceutical downstream processors. The market players are improving the ecosystem by investing in renewable feedstock, production of ultra-pure and denaturant-free ethanol, production automation, and high-tech digital quality control. Firms are also emphasizing on vertical integration, sustainability-based processing, and regulatory compliance and co-location strategies as a way of enhancing the efficiency of operations, product safety and environmental performance within the global markets.

Recent Development and Strategic Overview

-

In August 2025, Cargill’s Brazil unit announced a new corn‑ethanol plant in Goiás, adjacent to its existing sugarcane facility a strategic move to expand its food‑grade and industrial ethanol capacity. The plant was part of Cargill’s broader expansion of its bio‑fuels footprint in Brazil.

- In August 2025, AgVault developed a precision‑fermentation platform that converts ethanol plant byproducts into high‑grade yeast and yeast-derived products. This innovation allows ethanol facilities to produce value-added ingredients for food, feed, and biotech, enhancing profitability and sustainability.

Report Scope

|

Detail |

|

|

Market Size in 2025 |

~USD 3 Bn |

|

Market Forecast Value in 2035 |

USD 3.9 Bn |

|

Growth Rate (CAGR) |

2.7% |

|

Forecast Period |

2026 – 2035 |

|

Historical Data Available for |

2021 – 2024 |

|

Market Size Units |

US$ Billion for Value Volume Tons |

|

Report Format |

Electronic (PDF) + Excel |

|

North America |

Europe |

Asia Pacific |

Middle East |

Africa |

South America |

|

|

|

|

|

|

|

Companies Covered |

|||||

|

|

|

|

|

|

Food-Grade-Alcohol-(Ethanol)-Market Segmentation and Highlights

|

Segment |

Sub-segment |

|

Food Grade Alcohol (Ethanol) Market, By Purity Level |

|

|

Food Grade Alcohol (Ethanol) Market, By Source/Feedstock |

|

|

Food Grade Alcohol (Ethanol) Market, By Production Process |

|

|

Food Grade Alcohol (Ethanol) Market, By Form |

|

|

Food Grade Alcohol (Ethanol) Market, By Rated Capacity (Production Volume) |

|

|

Food Grade Alcohol (Ethanol) Market, By Packaging Type |

|

|

Food Grade Alcohol (Ethanol) Market, By Distribution Channel |

|

|

Food Grade Alcohol (Ethanol) Market, By Storage Temperature Requirements |

|

|

Food Grade Alcohol (Ethanol) Market, By End-Use |

|

Frequently Asked Questions

Table of Contents

- 1. Research Methodology and Assumptions

- 1.1. Definitions

- 1.2. Research Design and Approach

- 1.3. Data Collection Methods

- 1.4. Base Estimates and Calculations

- 1.5. Forecasting Models

- 1.5.1. Key Forecast Factors & Impact Analysis

- 1.6. Secondary Research

- 1.6.1. Open Sources

- 1.6.2. Paid Databases

- 1.6.3. Associations

- 1.7. Primary Research

- 1.7.1. Primary Sources

- 1.7.2. Primary Interviews with Stakeholders across Ecosystem

- 2. Executive Summary

- 2.1. Global Food Grade Alcohol (Ethanol) Market Outlook

- 2.1.1. Food Grade Alcohol (Ethanol) Market Size Volume (Tons) and Value (US$ Bn), and Forecasts, 2021-2035

- 2.1.2. Compounded Annual Growth Rate Analysis

- 2.1.3. Growth Opportunity Analysis

- 2.1.4. Segmental Share Analysis

- 2.1.5. Geographical Share Analysis

- 2.2. Market Analysis and Facts

- 2.3. Supply-Demand Analysis

- 2.4. Competitive Benchmarking

- 2.5. Go-to- Market Strategy

- 2.5.1. Customer/ End-use Industry Assessment

- 2.5.2. Growth Opportunity Data, 2026-2035

- 2.5.2.1. Regional Data

- 2.5.2.2. Country Data

- 2.5.2.3. Segmental Data

- 2.5.3. Identification of Potential Market Spaces

- 2.5.4. GAP Analysis

- 2.5.5. Potential Attractive Price Points

- 2.5.6. Prevailing Market Risks & Challenges

- 2.5.7. Preferred Sales & Marketing Strategies

- 2.5.8. Key Recommendations and Analysis

- 2.5.9. A Way Forward

- 2.1. Global Food Grade Alcohol (Ethanol) Market Outlook

- 3. Industry Data and Premium Insights

- 3.1. Global Food & Beverages Industry Overview, 2025

- 3.1.1. Industry Ecosystem Analysis

- 3.1.2. Key Trends for Food & Beverages Industry

- 3.1.3. Regional Distribution for Food & Beverages Industry

- 3.2. Supplier Customer Data

- 3.3. Technology Roadmap and Developments

- 3.4. Trade Analysis

- 3.4.1. Import & Export Analysis, 2025

- 3.4.2. Top Importing Countries

- 3.4.3. Top Exporting Countries

- 3.5. Trump Tariff Impact Analysis

- 3.5.1. Manufacturer

- 3.5.1.1. Based on the component & Raw material

- 3.5.2. Supply Chain

- 3.5.3. End Consumer

- 3.5.1. Manufacturer

- 3.6. Raw Material Analysis

- 3.1. Global Food & Beverages Industry Overview, 2025

- 4. Market Overview

- 4.1. Market Dynamics

- 4.1.1. Drivers

- 4.1.1.1. Rising demand in beverages and food applications (e.g., spirits, flavor extracts, preservatives).

- 4.1.1.2. Growing pharmaceutical and personal care industry usage (e.g., sanitizers, cosmetics, tinctures).

- 4.1.1.3. Increasing preference for sustainable and bio-based alcohol over synthetic chemicals.

- 4.1.2. Restraints

- 4.1.2.1. Price volatility of raw materials (corn, sugarcane, grains) affecting production cost.

- 4.1.2.2. Stringent government regulations and licensing requirements for food-grade ethanol production and distribution.

- 4.1.1. Drivers

- 4.2. Key Trend Analysis

- 4.3. Regulatory Framework

- 4.3.1. Key Regulations, Norms, and Subsidies, by Key Countries

- 4.3.2. Tariffs and Standards

- 4.3.3. Impact Analysis of Regulations on the Market

- 4.4. Value Chain Analysis

- 4.4.1. Raw Material Suppliers

- 4.4.2. Manufacturing

- 4.4.3. Distribution

- 4.4.4. End-Use

- 4.5. Cost Structure Analysis

- 4.5.1. Parameter’s Share for Cost Associated

- 4.5.2. COGP vs COGS

- 4.5.3. Profit Margin Analysis

- 4.6. Pricing Analysis

- 4.6.1. Regional Pricing Analysis

- 4.6.2. Segmental Pricing Trends

- 4.6.3. Factors Influencing Pricing

- 4.7. Porter’s Five Forces Analysis

- 4.8. PESTEL Analysis

- 4.9. Global Food Grade Alcohol (Ethanol) Market Demand

- 4.9.1. Historical Market Size – Volume (Tons) and Value (US$ Bn), 2020-2024

- 4.9.2. Current and Future Market Size - Volume(Tons) and Value (US$ Bn), 2026–2035

- 4.9.2.1. Y-o-Y Growth Trends

- 4.9.2.2. Absolute $ Opportunity Assessment

- 4.1. Market Dynamics

- 5. Competition Landscape

- 5.1. Competition structure

- 5.1.1. Fragmented v/s consolidated

- 5.2. Company Share Analysis, 2025

- 5.2.1. Global Company Market Share

- 5.2.2. By Region

- 5.2.2.1. North America

- 5.2.2.2. Europe

- 5.2.2.3. Asia Pacific

- 5.2.2.4. Middle East

- 5.2.2.5. Africa

- 5.2.2.6. South America

- 5.3. Product Comparison Matrix

- 5.3.1. Specifications

- 5.3.2. Market Positioning

- 5.3.3. Pricing

- 5.1. Competition structure

- 6. Global Food Grade Alcohol (Ethanol) Market Analysis, by Purity Level

- 6.1. Key Segment Analysis

- 6.2. Food Grade Alcohol (Ethanol) Market Size Volume(Tons) and Value (US$ Bn), Analysis, and Forecasts, by Purity Level, 2021-2035

- 6.2.1. 95% Ethanol

- 6.2.2. 96% Ethanol

- 6.2.3. 99% Ethanol

- 6.2.4. 5% Ethanol

- 6.2.5. 9% Ethanol (Ultra-pure)

- 7. Global Food Grade Alcohol (Ethanol) Market Analysis, by Source/Feedstock

- 7.1. Key Segment Analysis

- 7.2. Food Grade Alcohol (Ethanol) Market Size Volume(Tons) and Value (US$ Bn), Analysis, and Forecasts, by Source/Feedstock, 2021-2035

- 7.2.1. Grain-based

- 7.2.1.1. Corn

- 7.2.1.2. Wheat

- 7.2.1.3. Barley

- 7.2.1.4. Rye

- 7.2.1.5. Others

- 7.2.2. Sugarcane-based

- 7.2.3. Sugar beet-based

- 7.2.4. Molasses-based

- 7.2.5. Fruit-based

- 7.2.6. Synthetic ethanol

- 7.2.1. Grain-based

- 8. Global Food Grade Alcohol (Ethanol) Market Analysis, by Production Process

- 8.1. Key Segment Analysis

- 8.2. Food Grade Alcohol (Ethanol) Market Size Volume(Tons) and Value (US$ Bn), Analysis, and Forecasts, by Production Process, 2021-2035

- 8.2.1. Fermentation-based

- 8.2.2. Distillation-based

- 8.2.3. Molecular sieve dehydration

- 8.2.4. Azeotropic distillation

- 8.2.5. Membrane separation technology

- 8.2.6. Others

- 9. Global Food Grade Alcohol (Ethanol) Market Analysis, by Form

- 9.1. Key Segment Analysis

- 9.2. Food Grade Alcohol (Ethanol) Market Size Volume(Tons) and Value (US$ Bn), Analysis, and Forecasts, by Form, 2021-2035

- 9.2.1. Liquid

- 9.2.2. Spray-dried powder

- 9.2.3. Anhydrous ethanol

- 9.2.4. Hydrous ethanol

- 10. Global Food Grade Alcohol (Ethanol) Market Analysis, by Rated Capacity (Production Volume)

- 10.1. Key Segment Analysis

- 10.2. Food Grade Alcohol (Ethanol) Market Size Volume(Tons) and Value (US$ Bn), Analysis, and Forecasts, by Rated Capacity (Production Volume), 2021-2035

- 10.2.1. < 10,000 liters/day

- 10.2.2. 10,000 - 50,000 liters/day

- 10.2.3. 50,000 - 200,000 liters/day

- 10.2.4. > 200,000 liters/day

- 11. Global Food Grade Alcohol (Ethanol) Market Analysis, by Packaging Type

- 11.1. Key Segment Analysis

- 11.2. Food Grade Alcohol (Ethanol) Market Size Volume(Tons) and Value (US$ Bn), Analysis, and Forecasts, by Packaging Type, 2021-2035

- 11.2.1. Drums (200L-220L)

- 11.2.2. Intermediate Bulk Containers (IBC) (1000L)

- 11.2.3. ISO Tanks

- 11.2.4. Flexitanks

- 11.2.5. Bottles and Jerrycans (1L-25L)

- 11.2.6. Bulk tankers

- 11.2.7. Others

- 12. Global Food Grade Alcohol (Ethanol) Market Analysis, by Distribution Channel

- 12.1. Key Segment Analysis

- 12.2. Food Grade Alcohol (Ethanol) Market Size Volume(Tons) and Value (US$ Bn), Analysis, and Forecasts, by Distribution Channel, 2021-2035

- 12.2.1. Direct Sales

- 12.2.2. Distributors

- 12.2.3. Online Platforms

- 12.2.4. Specialty Chemical Suppliers

- 12.2.5. Contract Manufacturing

- 13. Global Food Grade Alcohol (Ethanol) Market Analysis, by Storage Temperature Requirements

- 13.1. Key Segment Analysis

- 13.2. Food Grade Alcohol (Ethanol) Market Size Volume(Tons) and Value (US$ Bn), Analysis, and Forecasts, by Storage Temperature Requirements, 2021-2035

- 13.2.1. Ambient Storage

- 13.2.2. Temperature-controlled Storage

- 13.2.3. Cold Storage

- 14. Global Food Grade Alcohol (Ethanol) Market Analysis, by End-Use

- 14.1. Key Segment Analysis

- 14.2. Food Grade Alcohol (Ethanol) Market Size Volume(Tons) and Value (US$ Bn), Analysis, and Forecasts, by End-Use, 2021-2035

- 14.2.1. Food & Beverage

- 14.2.1.1. Flavor extraction

- 14.2.1.2. Food preservation

- 14.2.1.3. Beverage production (spirits, liqueurs)

- 14.2.1.4. Food coloring extraction

- 14.2.1.5. Vinegar production

- 14.2.1.6. Food processing aid

- 14.2.1.7. Others

- 14.2.2. Nutraceutical

- 14.2.2.1. Herbal extracts

- 14.2.2.2. Dietary supplement manufacturing

- 14.2.2.3. Vitamin extraction

- 14.2.2.4. Essential oil production

- 14.2.2.5. Tincture preparation

- 14.2.2.6. Others

- 14.2.1. Food & Beverage

- 15. Global Food Grade Alcohol (Ethanol) Market Analysis and Forecasts, by Region

- 15.1. Key Findings

- 15.2. Food Grade Alcohol (Ethanol) Market Size Volume(Tons) and Value (US$ Bn), Analysis, and Forecasts, by Region, 2021-2035

- 15.2.1. North America

- 15.2.2. Europe

- 15.2.3. Asia Pacific

- 15.2.4. Middle East

- 15.2.5. Africa

- 15.2.6. South America

- 16. North America Food Grade Alcohol (Ethanol) Market Analysis

- 16.1. Key Segment Analysis

- 16.2. Regional Snapshot

- 16.3. North America Food Grade Alcohol (Ethanol) Market Size- Volume(Tons) and Value (US$ Bn), Analysis, and Forecasts, 2021-2035

- 16.3.1. Purity Level

- 16.3.2. Source/Feedstock

- 16.3.3. Production Process

- 16.3.4. Form

- 16.3.5. Rated Capacity (Production Volume)

- 16.3.6. Packaging Type

- 16.3.7. Distribution Channel

- 16.3.8. Storage Temperature Requirements

- 16.3.9. End-Use

- 16.3.10. Country

- 16.3.10.1. USA

- 16.3.10.2. Canada

- 16.3.10.3. Mexico

- 16.4. USA Food Grade Alcohol (Ethanol) Market

- 16.4.1. Country Segmental Analysis

- 16.4.2. Purity Level

- 16.4.3. Source/Feedstock

- 16.4.4. Production Process

- 16.4.5. Form

- 16.4.6. Rated Capacity (Production Volume)

- 16.4.7. Packaging Type

- 16.4.8. Distribution Channel

- 16.4.9. Storage Temperature Requirements

- 16.4.10. End-Use

- 16.5. Canada Food Grade Alcohol (Ethanol) Market

- 16.5.1. Country Segmental Analysis

- 16.5.2. Purity Level

- 16.5.3. Source/Feedstock

- 16.5.4. Production Process

- 16.5.5. Form

- 16.5.6. Rated Capacity (Production Volume)

- 16.5.7. Packaging Type

- 16.5.8. Distribution Channel

- 16.5.9. Storage Temperature Requirements

- 16.5.10. End-Use

- 16.6. Mexico Food Grade Alcohol (Ethanol) Market

- 16.6.1. Country Segmental Analysis

- 16.6.2. Purity Level

- 16.6.3. Source/Feedstock

- 16.6.4. Production Process

- 16.6.5. Form

- 16.6.6. Rated Capacity (Production Volume)

- 16.6.7. Packaging Type

- 16.6.8. Distribution Channel

- 16.6.9. Storage Temperature Requirements

- 16.6.10. End-Use

- 17. Europe Food Grade Alcohol (Ethanol) Market Analysis

- 17.1. Key Segment Analysis

- 17.2. Regional Snapshot

- 17.3. Europe Food Grade Alcohol (Ethanol) Market Size Volume(Tons) and Value (US$ Bn), Analysis, and Forecasts, 2021-2035

- 17.3.1. Purity Level

- 17.3.2. Source/Feedstock

- 17.3.3. Production Process

- 17.3.4. Form

- 17.3.5. Rated Capacity (Production Volume)

- 17.3.6. Packaging Type

- 17.3.7. Distribution Channel

- 17.3.8. Storage Temperature Requirements

- 17.3.9. End-Use

- 17.3.10. Country

- 17.3.10.1. Germany

- 17.3.10.2. United Kingdom

- 17.3.10.3. France

- 17.3.10.4. Italy

- 17.3.10.5. Spain

- 17.3.10.6. Netherlands

- 17.3.10.7. Nordic Countries

- 17.3.10.8. Poland

- 17.3.10.9. Russia & CIS

- 17.3.10.10. Rest of Europe

- 17.4. Germany Food Grade Alcohol (Ethanol) Market

- 17.4.1. Country Segmental Analysis

- 17.4.2. Purity Level

- 17.4.3. Source/Feedstock

- 17.4.4. Production Process

- 17.4.5. Form

- 17.4.6. Rated Capacity (Production Volume)

- 17.4.7. Packaging Type

- 17.4.8. Distribution Channel

- 17.4.9. Storage Temperature Requirements

- 17.4.10. End-Use

- 17.5. United Kingdom Food Grade Alcohol (Ethanol) Market

- 17.5.1. Country Segmental Analysis

- 17.5.2. Purity Level

- 17.5.3. Source/Feedstock

- 17.5.4. Production Process

- 17.5.5. Form

- 17.5.6. Rated Capacity (Production Volume)

- 17.5.7. Packaging Type

- 17.5.8. Distribution Channel

- 17.5.9. Storage Temperature Requirements

- 17.5.10. End-Use

- 17.6. France Food Grade Alcohol (Ethanol) Market

- 17.6.1. Country Segmental Analysis

- 17.6.2. Purity Level

- 17.6.3. Source/Feedstock

- 17.6.4. Production Process

- 17.6.5. Form

- 17.6.6. Rated Capacity (Production Volume)

- 17.6.7. Packaging Type

- 17.6.8. Distribution Channel

- 17.6.9. Storage Temperature Requirements

- 17.6.10. End-Use

- 17.7. Italy Food Grade Alcohol (Ethanol) Market

- 17.7.1. Country Segmental Analysis

- 17.7.2. Purity Level

- 17.7.3. Source/Feedstock

- 17.7.4. Production Process

- 17.7.5. Form

- 17.7.6. Rated Capacity (Production Volume)

- 17.7.7. Packaging Type

- 17.7.8. Distribution Channel

- 17.7.9. Storage Temperature Requirements

- 17.7.10. End-Use

- 17.8. Spain Food Grade Alcohol (Ethanol) Market

- 17.8.1. Country Segmental Analysis

- 17.8.2. Purity Level

- 17.8.3. Source/Feedstock

- 17.8.4. Production Process

- 17.8.5. Form

- 17.8.6. Rated Capacity (Production Volume)

- 17.8.7. Packaging Type

- 17.8.8. Distribution Channel

- 17.8.9. Storage Temperature Requirements

- 17.8.10. End-Use

- 17.9. Netherlands Food Grade Alcohol (Ethanol) Market

- 17.9.1. Country Segmental Analysis

- 17.9.2. Purity Level

- 17.9.3. Source/Feedstock

- 17.9.4. Production Process

- 17.9.5. Form

- 17.9.6. Rated Capacity (Production Volume)

- 17.9.7. Packaging Type

- 17.9.8. Distribution Channel

- 17.9.9. Storage Temperature Requirements

- 17.9.10. End-Use

- 17.10. Nordic Countries Food Grade Alcohol (Ethanol) Market

- 17.10.1. Country Segmental Analysis

- 17.10.2. Purity Level

- 17.10.3. Source/Feedstock

- 17.10.4. Production Process

- 17.10.5. Form

- 17.10.6. Rated Capacity (Production Volume)

- 17.10.7. Packaging Type

- 17.10.8. Distribution Channel

- 17.10.9. Storage Temperature Requirements

- 17.10.10. End-Use

- 17.11. Poland Food Grade Alcohol (Ethanol) Market

- 17.11.1. Country Segmental Analysis

- 17.11.2. Purity Level

- 17.11.3. Source/Feedstock

- 17.11.4. Production Process

- 17.11.5. Form

- 17.11.6. Rated Capacity (Production Volume)

- 17.11.7. Packaging Type

- 17.11.8. Distribution Channel

- 17.11.9. Storage Temperature Requirements

- 17.11.10. End-Use

- 17.12. Russia & CIS Food Grade Alcohol (Ethanol) Market

- 17.12.1. Country Segmental Analysis

- 17.12.2. Purity Level

- 17.12.3. Source/Feedstock

- 17.12.4. Production Process

- 17.12.5. Form

- 17.12.6. Rated Capacity (Production Volume)

- 17.12.7. Packaging Type

- 17.12.8. Distribution Channel

- 17.12.9. Storage Temperature Requirements

- 17.12.10. End-Use

- 17.13. Rest of Europe Food Grade Alcohol (Ethanol) Market

- 17.13.1. Country Segmental Analysis

- 17.13.2. Purity Level

- 17.13.3. Source/Feedstock

- 17.13.4. Production Process

- 17.13.5. Form

- 17.13.6. Rated Capacity (Production Volume)

- 17.13.7. Packaging Type

- 17.13.8. Distribution Channel

- 17.13.9. Storage Temperature Requirements

- 17.13.10. End-Use

- 18. Asia Pacific Food Grade Alcohol (Ethanol) Market Analysis

- 18.1. Key Segment Analysis

- 18.2. Regional Snapshot

- 18.3. Asia Pacific Food Grade Alcohol (Ethanol) Market Size Volume(Tons) and Value (US$ Bn), Analysis, and Forecasts, 2021-2035

- 18.3.1. Purity Level

- 18.3.2. Source/Feedstock

- 18.3.3. Production Process

- 18.3.4. Form

- 18.3.5. Rated Capacity (Production Volume)

- 18.3.6. Packaging Type

- 18.3.7. Distribution Channel

- 18.3.8. Storage Temperature Requirements

- 18.3.9. End-Use

- 18.3.10. Country

- 18.3.10.1. China

- 18.3.10.2. India

- 18.3.10.3. Japan

- 18.3.10.4. South Korea

- 18.3.10.5. Australia and New Zealand

- 18.3.10.6. Indonesia

- 18.3.10.7. Malaysia

- 18.3.10.8. Thailand

- 18.3.10.9. Vietnam

- 18.3.10.10. Rest of Asia Pacific

- 18.4. China Food Grade Alcohol (Ethanol) Market

- 18.4.1. Country Segmental Analysis

- 18.4.2. Purity Level

- 18.4.3. Source/Feedstock

- 18.4.4. Production Process

- 18.4.5. Form

- 18.4.6. Rated Capacity (Production Volume)

- 18.4.7. Packaging Type

- 18.4.8. Distribution Channel

- 18.4.9. Storage Temperature Requirements

- 18.4.10. End-Use

- 18.5. India Food Grade Alcohol (Ethanol) Market

- 18.5.1. Country Segmental Analysis

- 18.5.2. Purity Level

- 18.5.3. Source/Feedstock

- 18.5.4. Production Process

- 18.5.5. Form

- 18.5.6. Rated Capacity (Production Volume)

- 18.5.7. Packaging Type

- 18.5.8. Distribution Channel

- 18.5.9. Storage Temperature Requirements

- 18.5.10. End-Use

- 18.6. Japan Food Grade Alcohol (Ethanol) Market

- 18.6.1. Country Segmental Analysis

- 18.6.2. Purity Level

- 18.6.3. Source/Feedstock

- 18.6.4. Production Process

- 18.6.5. Form

- 18.6.6. Rated Capacity (Production Volume)

- 18.6.7. Packaging Type

- 18.6.8. Distribution Channel

- 18.6.9. Storage Temperature Requirements

- 18.6.10. End-Use

- 18.7. South Korea Food Grade Alcohol (Ethanol) Market

- 18.7.1. Country Segmental Analysis

- 18.7.2. Purity Level

- 18.7.3. Source/Feedstock

- 18.7.4. Production Process

- 18.7.5. Form

- 18.7.6. Rated Capacity (Production Volume)

- 18.7.7. Packaging Type

- 18.7.8. Distribution Channel

- 18.7.9. Storage Temperature Requirements

- 18.7.10. End-Use

- 18.8. Australia and New Zealand Food Grade Alcohol (Ethanol) Market

- 18.8.1. Country Segmental Analysis

- 18.8.2. Purity Level

- 18.8.3. Source/Feedstock

- 18.8.4. Production Process

- 18.8.5. Form

- 18.8.6. Rated Capacity (Production Volume)

- 18.8.7. Packaging Type

- 18.8.8. Distribution Channel

- 18.8.9. Storage Temperature Requirements

- 18.8.10. End-Use

- 18.9. Indonesia Food Grade Alcohol (Ethanol) Market

- 18.9.1. Country Segmental Analysis

- 18.9.2. Purity Level

- 18.9.3. Source/Feedstock

- 18.9.4. Production Process

- 18.9.5. Form

- 18.9.6. Rated Capacity (Production Volume)

- 18.9.7. Packaging Type

- 18.9.8. Distribution Channel

- 18.9.9. Storage Temperature Requirements

- 18.9.10. End-Use

- 18.10. Malaysia Food Grade Alcohol (Ethanol) Market

- 18.10.1. Country Segmental Analysis

- 18.10.2. Purity Level

- 18.10.3. Source/Feedstock

- 18.10.4. Production Process

- 18.10.5. Form

- 18.10.6. Rated Capacity (Production Volume)

- 18.10.7. Packaging Type

- 18.10.8. Distribution Channel

- 18.10.9. Storage Temperature Requirements

- 18.10.10. End-Use

- 18.11. Thailand Food Grade Alcohol (Ethanol) Market

- 18.11.1. Country Segmental Analysis

- 18.11.2. Purity Level

- 18.11.3. Source/Feedstock

- 18.11.4. Production Process

- 18.11.5. Form

- 18.11.6. Rated Capacity (Production Volume)

- 18.11.7. Packaging Type

- 18.11.8. Distribution Channel

- 18.11.9. Storage Temperature Requirements

- 18.11.10. End-Use

- 18.12. Vietnam Food Grade Alcohol (Ethanol) Market

- 18.12.1. Country Segmental Analysis

- 18.12.2. Purity Level

- 18.12.3. Source/Feedstock

- 18.12.4. Production Process

- 18.12.5. Form

- 18.12.6. Rated Capacity (Production Volume)

- 18.12.7. Packaging Type

- 18.12.8. Distribution Channel

- 18.12.9. Storage Temperature Requirements

- 18.12.10. End-Use

- 18.13. Rest of Asia Pacific Food Grade Alcohol (Ethanol) Market

- 18.13.1. Country Segmental Analysis

- 18.13.2. Purity Level

- 18.13.3. Source/Feedstock

- 18.13.4. Production Process

- 18.13.5. Form

- 18.13.6. Rated Capacity (Production Volume)

- 18.13.7. Packaging Type

- 18.13.8. Distribution Channel

- 18.13.9. Storage Temperature Requirements

- 18.13.10. End-Use

- 19. Middle East Food Grade Alcohol (Ethanol) Market Analysis

- 19.1. Key Segment Analysis

- 19.2. Regional Snapshot

- 19.3. Middle East Food Grade Alcohol (Ethanol) Market Size Volume(Tons) and Value (US$ Bn), Analysis, and Forecasts, 2021-2035

- 19.3.1. Purity Level

- 19.3.2. Source/Feedstock

- 19.3.3. Production Process

- 19.3.4. Form

- 19.3.5. Rated Capacity (Production Volume)

- 19.3.6. Packaging Type

- 19.3.7. Distribution Channel

- 19.3.8. Storage Temperature Requirements

- 19.3.9. End-Use

- 19.3.10. Country

- 19.3.10.1. Turkey

- 19.3.10.2. UAE

- 19.3.10.3. Saudi Arabia

- 19.3.10.4. Israel

- 19.3.10.5. Rest of Middle East

- 19.4. Turkey Food Grade Alcohol (Ethanol) Market

- 19.4.1. Country Segmental Analysis

- 19.4.2. Purity Level

- 19.4.3. Source/Feedstock

- 19.4.4. Production Process

- 19.4.5. Form

- 19.4.6. Rated Capacity (Production Volume)

- 19.4.7. Packaging Type

- 19.4.8. Distribution Channel

- 19.4.9. Storage Temperature Requirements

- 19.4.10. End-Use

- 19.5. UAE Food Grade Alcohol (Ethanol) Market

- 19.5.1. Country Segmental Analysis

- 19.5.2. Purity Level

- 19.5.3. Source/Feedstock

- 19.5.4. Production Process

- 19.5.5. Form

- 19.5.6. Rated Capacity (Production Volume)

- 19.5.7. Packaging Type

- 19.5.8. Distribution Channel

- 19.5.9. Storage Temperature Requirements

- 19.5.10. End-Use

- 19.6. Saudi Arabia Food Grade Alcohol (Ethanol) Market

- 19.6.1. Country Segmental Analysis

- 19.6.2. Purity Level

- 19.6.3. Source/Feedstock

- 19.6.4. Production Process

- 19.6.5. Form

- 19.6.6. Rated Capacity (Production Volume)

- 19.6.7. Packaging Type

- 19.6.8. Distribution Channel

- 19.6.9. Storage Temperature Requirements

- 19.6.10. End-Use

- 19.7. Israel Food Grade Alcohol (Ethanol) Market

- 19.7.1. Country Segmental Analysis

- 19.7.2. Purity Level

- 19.7.3. Source/Feedstock

- 19.7.4. Production Process

- 19.7.5. Form

- 19.7.6. Rated Capacity (Production Volume)

- 19.7.7. Packaging Type

- 19.7.8. Distribution Channel

- 19.7.9. Storage Temperature Requirements

- 19.7.10. End-Use

- 19.8. Rest of Middle East Food Grade Alcohol (Ethanol) Market

- 19.8.1. Country Segmental Analysis

- 19.8.2. Purity Level

- 19.8.3. Source/Feedstock

- 19.8.4. Production Process

- 19.8.5. Form

- 19.8.6. Rated Capacity (Production Volume)

- 19.8.7. Packaging Type

- 19.8.8. Distribution Channel

- 19.8.9. Storage Temperature Requirements

- 19.8.10. End-Use

- 20. Africa Food Grade Alcohol (Ethanol) Market Analysis

- 20.1. Key Segment Analysis

- 20.2. Regional Snapshot

- 20.3. Africa Food Grade Alcohol (Ethanol) Market Size Volume(Tons) and Value (US$ Bn), Analysis, and Forecasts, 2021-2035

- 20.3.1. Purity Level

- 20.3.2. Source/Feedstock

- 20.3.3. Production Process

- 20.3.4. Form

- 20.3.5. Rated Capacity (Production Volume)

- 20.3.6. Packaging Type

- 20.3.7. Distribution Channel

- 20.3.8. Storage Temperature Requirements

- 20.3.9. End-Use

- 20.3.10. country

- 20.3.10.1. South Africa

- 20.3.10.2. Egypt

- 20.3.10.3. Nigeria

- 20.3.10.4. Algeria

- 20.3.10.5. Rest of Africa

- 20.4. South Africa Food Grade Alcohol (Ethanol) Market

- 20.4.1. Country Segmental Analysis

- 20.4.2. Purity Level

- 20.4.3. Source/Feedstock

- 20.4.4. Production Process

- 20.4.5. Form

- 20.4.6. Rated Capacity (Production Volume)

- 20.4.7. Packaging Type

- 20.4.8. Distribution Channel

- 20.4.9. Storage Temperature Requirements

- 20.4.10. End-Use

- 20.5. Egypt Food Grade Alcohol (Ethanol) Market

- 20.5.1. Country Segmental Analysis

- 20.5.2. Purity Level

- 20.5.3. Source/Feedstock

- 20.5.4. Production Process

- 20.5.5. Form

- 20.5.6. Rated Capacity (Production Volume)

- 20.5.7. Packaging Type

- 20.5.8. Distribution Channel

- 20.5.9. Storage Temperature Requirements

- 20.5.10. End-Use

- 20.6. Nigeria Food Grade Alcohol (Ethanol) Market

- 20.6.1. Country Segmental Analysis

- 20.6.2. Purity Level

- 20.6.3. Source/Feedstock

- 20.6.4. Production Process

- 20.6.5. Form

- 20.6.6. Rated Capacity (Production Volume)

- 20.6.7. Packaging Type

- 20.6.8. Distribution Channel

- 20.6.9. Storage Temperature Requirements

- 20.6.10. End-Use

- 20.7. Algeria Food Grade Alcohol (Ethanol) Market

- 20.7.1. Country Segmental Analysis

- 20.7.2. Purity Level

- 20.7.3. Source/Feedstock

- 20.7.4. Production Process

- 20.7.5. Form

- 20.7.6. Rated Capacity (Production Volume)

- 20.7.7. Packaging Type

- 20.7.8. Distribution Channel

- 20.7.9. Storage Temperature Requirements

- 20.7.10. End-Use

- 20.8. Rest of Africa Food Grade Alcohol (Ethanol) Market

- 20.8.1. Country Segmental Analysis

- 20.8.2. Purity Level

- 20.8.3. Source/Feedstock

- 20.8.4. Production Process

- 20.8.5. Form

- 20.8.6. Rated Capacity (Production Volume)

- 20.8.7. Packaging Type

- 20.8.8. Distribution Channel

- 20.8.9. Storage Temperature Requirements

- 20.8.10. End-Use

- 21. South America Food Grade Alcohol (Ethanol) Market Analysis

- 21.1. Key Segment Analysis

- 21.2. Regional Snapshot

- 21.3. South America Food Grade Alcohol (Ethanol) Market Size Volume(Tons) and Value (US$ Bn), Analysis, and Forecasts, 2021-2035

- 21.3.1. Purity Level

- 21.3.2. Source/Feedstock

- 21.3.3. Production Process

- 21.3.4. Form

- 21.3.5. Rated Capacity (Production Volume)

- 21.3.6. Packaging Type

- 21.3.7. Distribution Channel

- 21.3.8. Storage Temperature Requirements

- 21.3.9. End-Use

- 21.3.10. Country

- 21.3.10.1. Brazil

- 21.3.10.2. Argentina

- 21.3.10.3. Rest of South America

- 21.4. Brazil Food Grade Alcohol (Ethanol) Market

- 21.4.1. Country Segmental Analysis

- 21.4.2. Purity Level

- 21.4.3. Source/Feedstock

- 21.4.4. Production Process

- 21.4.5. Form

- 21.4.6. Rated Capacity (Production Volume)

- 21.4.7. Packaging Type

- 21.4.8. Distribution Channel

- 21.4.9. Storage Temperature Requirements

- 21.4.10. End-Use

- 21.5. Argentina Food Grade Alcohol (Ethanol) Market

- 21.5.1. Country Segmental Analysis

- 21.5.2. Purity Level

- 21.5.3. Source/Feedstock

- 21.5.4. Production Process

- 21.5.5. Form

- 21.5.6. Rated Capacity (Production Volume)

- 21.5.7. Packaging Type

- 21.5.8. Distribution Channel

- 21.5.9. Storage Temperature Requirements

- 21.5.10. End-Use

- 21.6. Rest of South America Food Grade Alcohol (Ethanol) Market

- 21.6.1. Country Segmental Analysis

- 21.6.2. Purity Level

- 21.6.3. Source/Feedstock

- 21.6.4. Production Process

- 21.6.5. Form

- 21.6.6. Rated Capacity (Production Volume)

- 21.6.7. Packaging Type

- 21.6.8. Distribution Channel

- 21.6.9. Storage Temperature Requirements

- 21.6.10. End-Use

- 22. Key Players/ Company Profile

- 22.1. Alcofi

- 22.1.1. Company Details/ Overview

- 22.1.2. Company Financials

- 22.1.3. Key Customers and Competitors

- 22.1.4. Business/ Industry Portfolio

- 22.1.5. Product Portfolio/ Specification Details

- 22.1.6. Pricing Data

- 22.1.7. Strategic Overview

- 22.1.8. Recent Developments

- 22.2. Archer Daniels Midland Company (ADM)

- 22.3. Cargill, Incorporated

- 22.4. Cristalco

- 22.5. CropEnergies AG

- 22.6. Extractohol

- 22.7. Flint Hills Resources

- 22.8. Glacial Grain Spirits

- 22.9. Grain Processing Corporation (GPC)

- 22.10. Greenfield Global

- 22.11. Integrated BioEthanol Technologies

- 22.12. Manildra Group

- 22.13. Merck KGaA

- 22.14. MGP Ingredients, Inc.

- 22.15. Pacific Ethanol

- 22.16. Pharmco Products

- 22.17. Praj Industries

- 22.18. Roquette Frères

- 22.19. Sasol Limited

- 22.20. Spectrum Chemical Manufacturing Corp.

- 22.21. Südzucker AG

- 22.22. Tereos

- 22.23. The Andersons, Inc.

- 22.24. Valero Energy Corporation

- 22.25. Warner Graham Company

- 22.26. Wilmar International Limited

- 22.27. Other Key Players

- 22.1. Alcofi

Note* - This is just tentative list of players. While providing the report, we will cover more number of players based on their revenue and share for each geography

Research Design

Our research design integrates both demand-side and supply-side analysis through a balanced combination of primary and secondary research methodologies. By utilizing both bottom-up and top-down approaches alongside rigorous data triangulation methods, we deliver robust market intelligence that supports strategic decision-making.

MarketGenics' comprehensive research design framework ensures the delivery of accurate, reliable, and actionable market intelligence. Through the integration of multiple research approaches, rigorous validation processes, and expert analysis, we provide our clients with the insights needed to make informed strategic decisions and capitalize on market opportunities.

MarketGenics leverages a dedicated industry panel of experts and a comprehensive suite of paid databases to effectively collect, consolidate, and analyze market intelligence.

Our approach has consistently proven to be reliable and effective in generating accurate market insights, identifying key industry trends, and uncovering emerging business opportunities.

Through both primary and secondary research, we capture and analyze critical company-level data such as manufacturing footprints, including technical centers, R&D facilities, sales offices, and headquarters.

Our expert panel further enhances our ability to estimate market size for specific brands based on validated field-level intelligence.

Our data mining techniques incorporate both parametric and non-parametric methods, allowing for structured data collection, sorting, processing, and cleaning.

Demand projections are derived from large-scale data sets analyzed through proprietary algorithms, culminating in robust and reliable market sizing.

Research Approach

The bottom-up approach builds market estimates by starting with the smallest addressable market units and systematically aggregating them to create comprehensive market size projections.

This method begins with specific, granular data points and builds upward to create the complete market landscape.

Customer Analysis → Segmental Analysis → Geographical Analysis

The top-down approach starts with the broadest possible market data and systematically narrows it down through a series of filters and assumptions to arrive at specific market segments or opportunities.

This method begins with the big picture and works downward to increasingly specific market slices.

TAM → SAM → SOM

Research Methods

Desk / Secondary Research

While analysing the market, we extensively study secondary sources, directories, and databases to identify and collect information useful for this technical, market-oriented, and commercial report. Secondary sources that we utilize are not only the public sources, but it is a combination of Open Source, Associations, Paid Databases, MG Repository & Knowledgebase, and others.

- Company websites, annual reports, financial reports, broker reports, and investor presentations

- National government documents, statistical databases and reports

- News articles, press releases and web-casts specific to the companies operating in the market, Magazines, reports, and others

- We gather information from commercial data sources for deriving company specific data such as segmental revenue, share for geography, product revenue, and others

- Internal and external proprietary databases (industry-specific), relevant patent, and regulatory databases

- Governing Bodies, Government Organizations

- Relevant Authorities, Country-specific Associations for Industries

We also employ the model mapping approach to estimate the product level market data through the players' product portfolio

Primary Research

Primary research/ interviews is vital in analyzing the market. Most of the cases involves paid primary interviews. Primary sources include primary interviews through e-mail interactions, telephonic interviews, surveys as well as face-to-face interviews with the different stakeholders across the value chain including several industry experts.

| Type of Respondents | Number of Primaries |

|---|---|

| Tier 2/3 Suppliers | ~20 |

| Tier 1 Suppliers | ~25 |

| End-users | ~25 |

| Industry Expert/ Panel/ Consultant | ~30 |

| Total | ~100 |

MG Knowledgebase

• Repository of industry blog, newsletter and case studies

• Online platform covering detailed market reports, and company profiles

Forecasting Factors and Models

Forecasting Factors

- Historical Trends – Past market patterns, cycles, and major events that shaped how markets behave over time. Understanding past trends helps predict future behavior.

- Industry Factors – Specific characteristics of the industry like structure, regulations, and innovation cycles that affect market dynamics.

- Macroeconomic Factors – Economic conditions like GDP growth, inflation, and employment rates that affect how much money people have to spend.

- Demographic Factors – Population characteristics like age, income, and location that determine who can buy your product.

- Technology Factors – How quickly people adopt new technology and how much technology infrastructure exists.

- Regulatory Factors – Government rules, laws, and policies that can help or restrict market growth.

- Competitive Factors – Analyzing competition structure such as degree of competition and bargaining power of buyers and suppliers.

Forecasting Models / Techniques

Multiple Regression Analysis

- Identify and quantify factors that drive market changes

- Statistical modeling to establish relationships between market drivers and outcomes

Time Series Analysis – Seasonal Patterns

- Understand regular cyclical patterns in market demand

- Advanced statistical techniques to separate trend, seasonal, and irregular components

Time Series Analysis – Trend Analysis

- Identify underlying market growth patterns and momentum

- Statistical analysis of historical data to project future trends

Expert Opinion – Expert Interviews

- Gather deep industry insights and contextual understanding

- In-depth interviews with key industry stakeholders

Multi-Scenario Development

- Prepare for uncertainty by modeling different possible futures

- Creating optimistic, pessimistic, and most likely scenarios

Time Series Analysis – Moving Averages

- Sophisticated forecasting for complex time series data

- Auto-regressive integrated moving average models with seasonal components

Econometric Models

- Apply economic theory to market forecasting

- Sophisticated economic models that account for market interactions

Expert Opinion – Delphi Method

- Harness collective wisdom of industry experts

- Structured, multi-round expert consultation process

Monte Carlo Simulation

- Quantify uncertainty and probability distributions

- Thousands of simulations with varying input parameters

Research Analysis

Our research framework is built upon the fundamental principle of validating market intelligence from both demand and supply perspectives. This dual-sided approach ensures comprehensive market understanding and reduces the risk of single-source bias.

Demand-Side Analysis: We understand end-user/application behavior, preferences, and market needs along with the penetration of the product for specific application.

Supply-Side Analysis: We estimate overall market revenue, analyze the segmental share along with industry capacity, competitive landscape, and market structure.

Validation & Evaluation

Data triangulation is a validation technique that uses multiple methods, sources, or perspectives to examine the same research question, thereby increasing the credibility and reliability of research findings. In market research, triangulation serves as a quality assurance mechanism that helps identify and minimize bias, validate assumptions, and ensure accuracy in market estimates.

- Data Source Triangulation – Using multiple data sources to examine the same phenomenon

- Methodological Triangulation – Using multiple research methods to study the same research question

- Investigator Triangulation – Using multiple researchers or analysts to examine the same data

- Theoretical Triangulation – Using multiple theoretical perspectives to interpret the same data

Custom Market Research Services

We will customise the research for you, in case the report listed above does not meet your requirements.

Get 10% Free Customisation