Organic and Clean Label Baby Food Market Size, Share & Trends Analysis Report by Product Type (Organic Baby Food, Clean Label Baby Food), Food Category, Packaging Type, Age Group, Ingredient Base, Distribution Channel, Texture/Consistency, End-users, and Geography (North America, Europe, Asia Pacific, Middle East, Africa, and South America) – Global Industry Data, Trends, and Forecasts, 2026–2035

|

|

|

Segmental Data Insights |

|

|

Demand Trends |

|

|

Competitive Landscape |

|

|

Strategic Development |

|

|

Future Outlook & Opportunities |

|

Organic and Clean Label Baby Food Market Size, Share, and Growth

The global organic and clean label baby food market is experiencing robust growth, with its estimated value of USD 5.9 billion in the year 2025 and USD 12.2 billion by the period 2035, registering a CAGR of 7.5%, during the forecast period. The global organic and clean label baby food market is growing and improving with the rising knowledge on the nutritional values of infants, digestive systems, and long-term health. The parents prioritize clinical safety, naturalness, and nutritional efficacy of infant food items, and they are looking for formulations that promote healthy growth, immunological function, and microbiome balance.

Esther Hallam, Founder and CEO of Nara Organics, said: Just like so many, breastfeeding didn’t exactly go to plan. In a panic, I searched for an organic formula to feed my baby and couldn’t find a single option that I felt good feeding my daughter. Even the ‘organic’ choices had ingredients like sugar, corn syrup, palm oil, and soy—and I was shocked to learn that many of them were made by the same company, just sold under different brands. I created Nara because it’s the formula I wish existed for my daughter. We spent seven years developing this product with no compromises, so that parents who are still demanding better don’t have to settle.

The organic and clean label baby food market is experiencing rapid development due to the increasing consumer expectations to gain transparency, natural products and sustainable production technologies. Modern consumers are increasingly choosing products that are in line with their health, environmental and ethical lifestyles including clean formulations, traceable sourcing and improved nutritional efficacy. It is this changing attitude of consumers that is transforming the way people shop and it is affecting the product innovation in the industry.

Major players are reacting accordingly by repackaging products, making them more sustainable and using online interactions to develop a brand identity. For instance, in 2024, Happy Family Organics launched its new patented goat-milk-based infant formulas with non-European certification of the USDA and the EU as an answer to the nutritional and functional needs of parents, which have new probiotic and prebiotic blends. Programs such as this one backed by certifications and scientific validation build trust, promote brand loyalty and premium positioning in the competitive markets.

The opportunities adjacent comprise the delivery model on subscription, individualized formulations, the telehealth option of nutrition education, and the venturing into other complementary wellness lines. The strategies allow companies to spread their sources of revenue, increase the lifetime customer value and provide holistic solutions that can respond to the changed parental expectation.

Organic and Clean Label Baby Food Market Dynamics and Trends

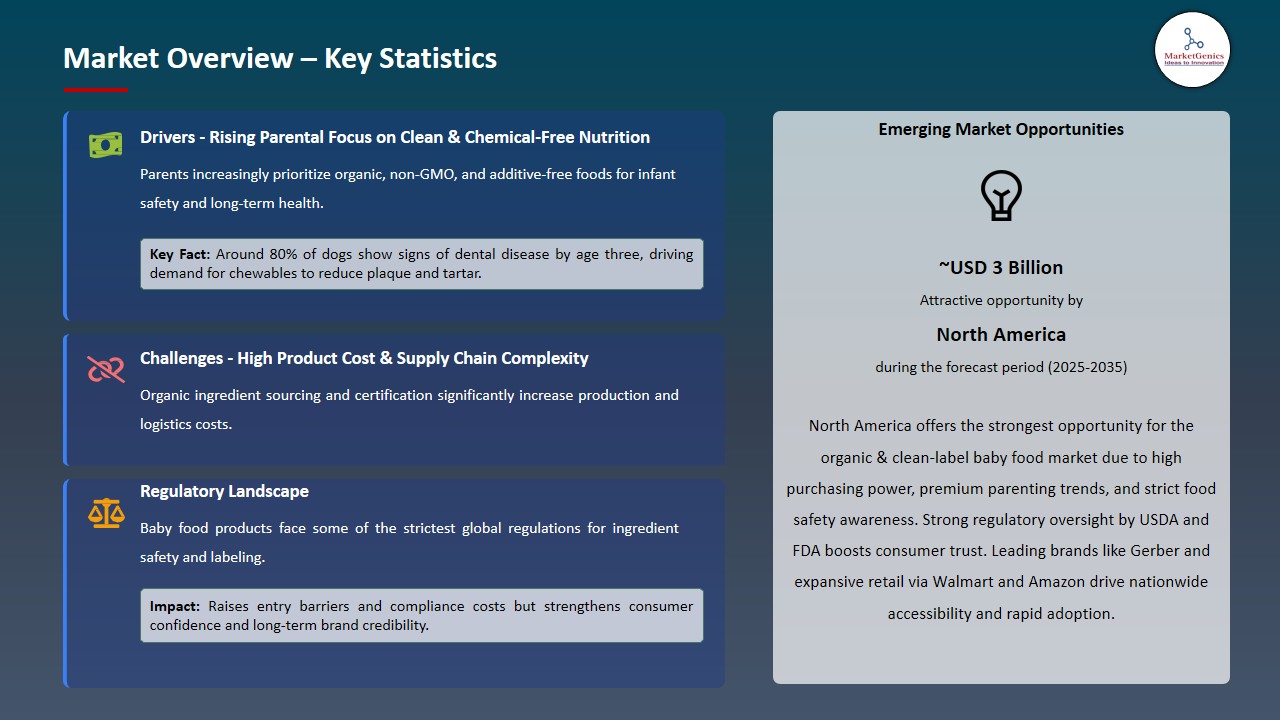

Driver: Millennial and Gen Z Parenting Preferences for Clean Ingredients

-

The demand of clean, transparent, and minimally processed food is transforming the organic and clean-label baby food market. Millennial and GenZ parents are concerned about health, sustainability, and product transparency and focus on them when choosing the products. These groups of people affect the decision to buy, loyalty to a certain brand, priorities in product development, forcing organizations to develop and reshape products in order to correspond to current requirements of parents.

- Brands are responding to this demand by making more and more innovative formulations. For instance, in April 2024, Else Nutrition released a soy-free and plant-based infant formula and toddler drink in Australia, with whole-food ingredients containing almond, buckwheat, and tapioca and no antibiotics, hormones, GMOs, and heavy metals.

- Firms are investing in third-party certifications, traceability systems, and value-based marketing to differentiate their brands. The trend is driving long-term market growth and providing new opportunities for innovation leaders to gain loyalty in high-level positions.

Restraint: High Product Costs and Reimbursement Limitations

-

Premium pricing in organic and clean label baby food markets is largely due to the structurally higher production cost and not brand positioning. The process of certified organic farming is lengthier and requires more strict measures in terms of input control, traceability, and high-quality testing to avoid pesticide, antibiotic, and heavy metal residues. These successive protective mechanisms add up to a large increment in the cost of raw materials and processing, which leads to intractable price additional charges in different lines of products, including infant formula, purees, and toddler snacks.

- Manufacturers have limited price cuts without jeopardizing profits due to cost inflation at the farm level, logistics, and certification. Weather instability, soil health, and variable organic feed all pose risks to clean-label sourcing, increasing cost unpredictability. As such, even large-scale producers face challenges in maintaining stable prices.

- Value-sensitive consumers face significant restraint, as their daily food budgets are tightly controlled. Although parents' awareness of clean nutrition is increasing, price continues to hinder the capacity to make repeat purchases and penetrate the mass market.

Opportunity: Expansion in Personalized and Allergy-Friendly Formulations

-

The increasing prevalence of food sensitivities and increasing parental demand to customized nutrition is moving the organic and clean-label baby food market to customized and allergy-free options. People are becoming more demanding about products that meet their particular dietary requirements with safety, quality, and transparency of clean labels. Firms who can provide such special solutions are highly suited to strike premium market segments and create loyalty in the long-run.

- Consumer desire for distinctive and health-oriented products has driven tangible innovation. For example, in September 2024, Happy Family Organics introduced its own line of newborn formula with USDA and EU certification, which was a proprietary blend of probiotics and prebiotics intended at improving gut health and immunity, with no significant allergies. This highlights how corporations are tailoring allergy-focused solutions to the changing needs of parents while increasing perceived value.

- As adoption grows, brands will likely employ subscription delivery, digital nutritional tracking, and personalized advice to boost personalization, consumer interaction, and competitive differentiation.

Key Trend: Development of Regenerative Agriculture Sourcing

-

Regenerative agriculture is transforming the organic and clean-label baby food market. Consumers are looking for products that not only have clean ingredients but also promote soil health and long-term sustainability. This is consistent with the growing parental emphasis on transparency, safety, and measurable nutritional outcomes in early childhood nutrition.

- Consumers expect traceable and responsibly sourced baby food, prompting brands to adopt regenerative practices. For example, in October 2024, Babylife Organics launched a brand of Regenerative-Organic Certified baby food that is supplied from regenerative farms and undergoes four phases of heavy-metal testing from soil to finished product, with validated results labeled on each packet via a QR code.

- Awareness and utilization of regenerative sourcing will increase among bigger market groups, including value-sensitive and mass-market customers. This will result in structural transformation, allowing for individualized products, subscription-based plans, and projects that will foster long-term consumer confidence and loyalty.

Organic-and-Clean-Label-Baby-Food-Market Analysis and Segmental Data

Dairy-Based Dominate Global Organic and Clean Label Baby Food Market

-

Dairy-based leads the global organic and clean-label baby food market, with a strong parental trust base, history of safety, and nutritional adequacy of the formula that many parents perceive to be closest to breast milk. Organic formulas made of cow-milk remain dominant in the market particularly regarding early-life nutrition where balanced macro- and micronutrients, digestibility and consistency are of utmost importance.

- There are new product innovations as a result of the consumer demand towards transparent, certified-organic dairy formulas. For instance, in June 2025, Nestle introduced NAN Sinergity, its so-called super-premium infant formula, which is a blend of six human-milk oligosaccharides (HMOs) and the probiotic Bifidobacterium infantis a blend that was developed to simulate the main features of breastmilk, support gut health and immunity and attract parents seeking premium, science-backed dairy-based infant nutrition.

- Dairy-formula maintains its dominance due to strong supply-chain infrastructure, regulatory transparency, and high certification standards. Despite global consumer desire in clean-label transparency and ingredient quality, these structural facilitators keep dairy-based organic infant meals at the forefront.

North America Leads Global Organic and Clean Label Baby Food Market Demand

-

North America leads the global organic and clean-label baby food market, which is supported by the high disposable incomes, rising parental awareness concerning the infant nutrition and high demand of high quality and transparent baby food solutions. These circumstances have provided a favorable reception of clean-label products, which are of stringent organic and safety standards.

- The willingness of the region to invest in the better infant nutrition is reflected by the increasing demand of parents to get high-quality and certified organic formulas and convenient forms of the products. For instance, in March 2025, Bobbie a U.S.-based organic infant-formula company introduced its Organic Whole Milk Infant Formula, the first and the only fully USDA-Organic whole-milk formula produced in the United States. Strong retail and e-commerce platform served to introduce the product into the market fast making it more accessible and adopted.

- North America's supply-chain capability, regulatory clarity, and existing distribution ecosystem enable rapid product innovation and large-scale rollouts. These advantages solidify its position as a global leader in organic and clean-label infant food, as customer preferences shift toward quality, safety, and transparency.

Organic-and-Clean-Label-Baby-Food-Market Ecosystem

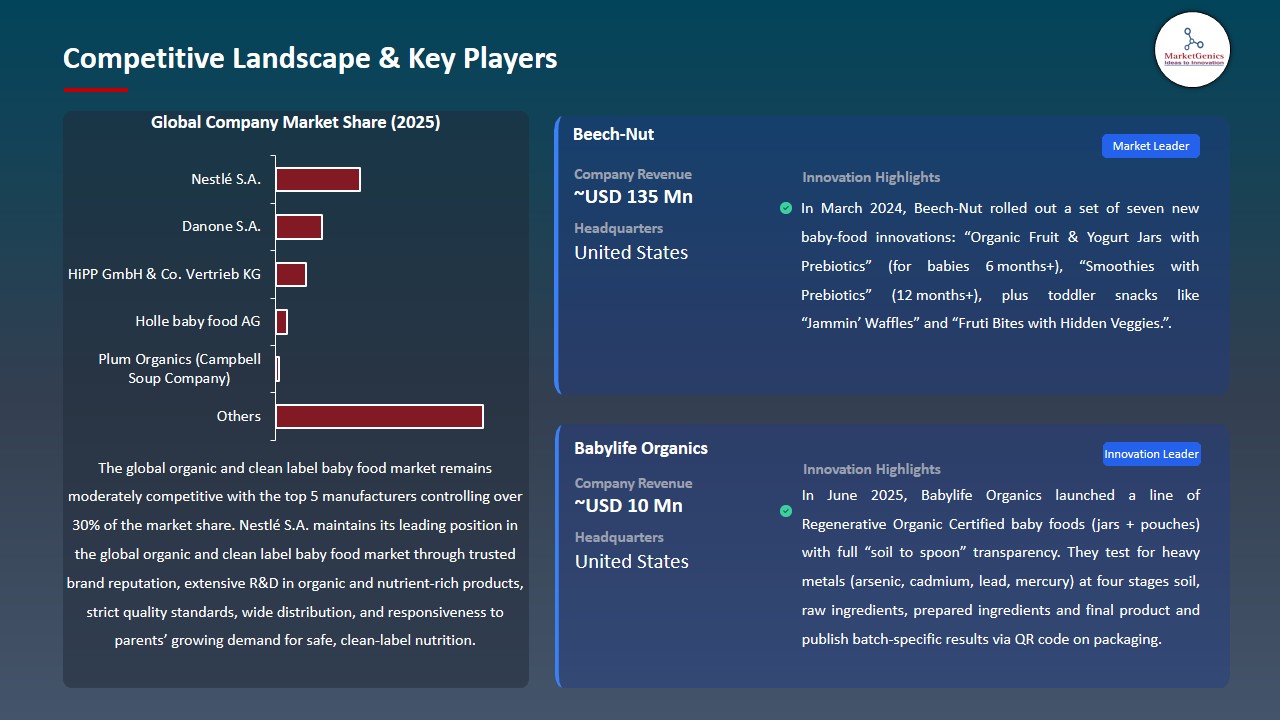

The global organic and clean label baby food market is slightly fragmented as it consists of multinational conglomerates, specialty brands, and direct-to-consumer start-ups competing over various segments and price ranges. The major competitors, such as Nestle S.A., Danone S.A., HiPP GmbH & Co., Holle Baby Food AG, and Plum Organics (Campbell Soup Company), use the ability to conduct research and development, the power of scale, and wide distribution channels to stay on the top of the mass-market markets.

The distinguishing factors used by the specialty brands include high-quality formulations, clean-label status, and specific consumer relationships to attract the niche markets of those consumers who are interested in safe, natural, and nutrient-dense solutions to baby food. The market value chain consists of suppliers of ingredients, formulation developers, contract manufacturers, packaging suppliers, distribution partners, retail channels, and marketing agencies.

Industry leaders are investing in vertical integration, direct to consumer, and digital marketing to improve their competitive positions, operational efficiency, and profits. These initiatives promote evidence-based product innovation, differentiation, and responsive solutions to meet increasing parental demands for high-quality, transparent, and trustworthy infant food products.

Recent Development and Strategic Overview

-

In June 2025, Nara Organics introduced its initial clean-label, whole-milk organic infant formula, USDA-Organic and registered by FDA. The formula contains no palm oil, no soy, no corn syrup, no maltodextrin, and no GMOs and gets fortified with MFGM, prebiotics, and DHA/ARA in order to promote gut health, immunity, and brain development.

- In June 2025, Petite Palates introduced a new high-protein savory product brand of baby food, which the company is expanding nationwide into independent retailers and natural-grocery stores in the U.S. This introduction is an indication of the increasing consumer need to find healthy, high protein products in organic and clean label baby foods.

Report Scope

|

Detail |

|

|

Market Size in 2025 |

USD 5.9 Bn |

|

Market Forecast Value in 2035 |

USD 12.2 Bn |

|

Growth Rate (CAGR) |

7.5% |

|

Forecast Period |

2026 – 2035 |

|

Historical Data Available for |

2021 – 2024 |

|

Market Size Units |

US$ Billion for Value |

|

Report Format |

Electronic (PDF) + Excel |

|

North America |

Europe |

Asia Pacific |

Middle East |

Africa |

South America |

|

|

|

|

|

|

|

Companies Covered |

|||||

|

|

|

|

|

|

Organic-and-Clean-Label-Baby-Food-Market Segmentation and Highlights

|

Segment |

Sub-segment |

|

Organic and Clean Label Baby Food Market, By Product Type |

|

|

Organic and Clean Label Baby Food Market, By Food Category |

|

|

Organic and Clean Label Baby Food Market, By Packaging Type |

|

|

Organic and Clean Label Baby Food Market, By Age Group |

|

|

Organic and Clean Label Baby Food Market, By Ingredient Base |

|

|

Organic and Clean Label Baby Food Market, By Distribution Channel |

|

|

Organic and Clean Label Baby Food Market, By Texture/Consistency |

|

|

Organic and Clean Label Baby Food Market, By End-users |

|

Frequently Asked Questions

Table of Contents

- 1. Research Methodology and Assumptions

- 1.1. Definitions

- 1.2. Research Design and Approach

- 1.3. Data Collection Methods

- 1.4. Base Estimates and Calculations

- 1.5. Forecasting Models

- 1.5.1. Key Forecast Factors & Impact Analysis

- 1.6. Secondary Research

- 1.6.1. Open Sources

- 1.6.2. Paid Databases

- 1.6.3. Associations

- 1.7. Primary Research

- 1.7.1. Primary Sources

- 1.7.2. Primary Interviews with Stakeholders across Ecosystem

- 2. Executive Summary

- 2.1. Global Organic and Clean Label Baby Food Market Outlook

- 2.1.1. Organic and Clean Label Baby Food Market Size (Value - US$ Bn), and Forecasts, 2021-2035

- 2.1.2. Compounded Annual Growth Rate Analysis

- 2.1.3. Growth Opportunity Analysis

- 2.1.4. Segmental Share Analysis

- 2.1.5. Geographical Share Analysis

- 2.2. Market Analysis and Facts

- 2.3. Supply-Demand Analysis

- 2.4. Competitive Benchmarking

- 2.5. Go-to- Market Strategy

- 2.5.1. Customer/ End-use Industry Assessment

- 2.5.2. Growth Opportunity Data, 2026-2035

- 2.5.2.1. Regional Data

- 2.5.2.2. Country Data

- 2.5.2.3. Segmental Data

- 2.5.3. Identification of Potential Market Spaces

- 2.5.4. GAP Analysis

- 2.5.5. Potential Attractive Price Points

- 2.5.6. Prevailing Market Risks & Challenges

- 2.5.7. Preferred Sales & Marketing Strategies

- 2.5.8. Key Recommendations and Analysis

- 2.5.9. A Way Forward

- 2.1. Global Organic and Clean Label Baby Food Market Outlook

- 3. Industry Data and Premium Insights

- 3.1. Global Consumer Goods & Services Industry Overview, 2025

- 3.1.1. Consumer Goods & Services Industry Ecosystem Analysis

- 3.1.2. Key Trends for Consumer Goods & Services Industry

- 3.1.3. Regional Distribution for Consumer Goods & Services Industry

- 3.2. Supplier Customer Data

- 3.3. Technology Roadmap and Developments

- 3.4. Trade Analysis

- 3.4.1. Import & Export Analysis, 2025

- 3.4.2. Top Importing Countries

- 3.4.3. Top Exporting Countries

- 3.5. Trump Tariff Impact Analysis

- 3.5.1. Manufacturer

- 3.5.1.1. Based on the component & Raw material

- 3.5.2. Supply Chain

- 3.5.3. End Consumer

- 3.5.1. Manufacturer

- 3.6. Raw Material Analysis

- 3.1. Global Consumer Goods & Services Industry Overview, 2025

- 4. Market Overview

- 4.1. Market Dynamics

- 4.1.1. Drivers

- 4.1.1.1. Rising parental awareness of infant nutrition and food safety

- 4.1.1.2. Increasing preference for organic, non-GMO, and additive-free products

- 4.1.1.3. Growth of premium baby care spending and e-commerce adoption.

- 4.1.2. Restraints

- 4.1.2.1. High cost of organic and clean-label baby food products

- 4.1.2.2. Limited shelf life and supply chain complexities for organic ingredients.

- 4.1.1. Drivers

- 4.2. Key Trend Analysis

- 4.3. Regulatory Framework

- 4.3.1. Key Regulations, Norms, and Subsidies, by Key Countries

- 4.3.2. Tariffs and Standards

- 4.3.3. Impact Analysis of Regulations on the Market

- 4.4. Value Chain Analysis

- 4.4.1. Raw Material Suppliers

- 4.4.2. Manufacturers

- 4.4.3. Dealers/ Distributors

- 4.4.4. End-Users/ Customers

- 4.5. Porter’s Five Forces Analysis

- 4.6. PESTEL Analysis

- 4.7. Global Organic and Clean Label Baby Food Market Demand

- 4.7.1. Historical Market Size – Value (US$ Bn), 2020-2024

- 4.7.2. Current and Future Market Size – Value (US$ Bn), 2026–2035

- 4.7.2.1. Y-o-Y Growth Trends

- 4.7.2.2. Absolute $ Opportunity Assessment

- 4.1. Market Dynamics

- 5. Competition Landscape

- 5.1. Competition structure

- 5.1.1. Fragmented v/s consolidated

- 5.2. Company Share Analysis, 2025

- 5.2.1. Global Company Market Share

- 5.2.2. By Region

- 5.2.2.1. North America

- 5.2.2.2. Europe

- 5.2.2.3. Asia Pacific

- 5.2.2.4. Middle East

- 5.2.2.5. Africa

- 5.2.2.6. South America

- 5.3. Product Comparison Matrix

- 5.3.1. Specifications

- 5.3.2. Market Positioning

- 5.3.3. Pricing

- 5.1. Competition structure

- 6. Global Organic and Clean Label Baby Food Market Analysis, by Product Type

- 6.1. Key Segment Analysis

- 6.2. Organic and Clean Label Baby Food Market Size (Value - US$ Bn), Analysis, and Forecasts, by Product Type, 2021-2035

- 6.2.1. Organic Baby Food

- 6.2.1.1. Certified Organic

- 6.2.1.2. 100% Organic Ingredients

- 6.2.1.3. Made with Organic Ingredients

- 6.2.2. Clean Label Baby Food

- 6.2.2.1. No Artificial Additives

- 6.2.2.2. Non-GMO

- 6.2.2.3. Free-From Products

- 6.2.1. Organic Baby Food

- 7. Global Organic and Clean Label Baby Food Market Analysis, by Food Category

- 7.1. Key Segment Analysis

- 7.2. Organic and Clean Label Baby Food Market Size (Value - US$ Bn), Analysis, and Forecasts, by Food Category, 2021-2035

- 7.2.1. Baby Cereals

- 7.2.1.1. Single Grain Cereals

- 7.2.1.2. Multi-Grain Cereals

- 7.2.1.3. Fortified Cereals

- 7.2.1.4. Others

- 7.2.2. Prepared Baby Food

- 7.2.2.1. Purees

- 7.2.2.2. Meals

- 7.2.2.3. Snacks

- 7.2.2.4. Others

- 7.2.3. Baby Drinks

- 7.2.3.1. Fruit Juices

- 7.2.3.2. Vegetable Juices

- 7.2.3.3. Formula Alternatives

- 7.2.3.4. Others

- 7.2.4. Baby Snacks

- 7.2.4.1. Puffs

- 7.2.4.2. Biscuits/Cookies

- 7.2.4.3. Freeze-Dried Snacks

- 7.2.4.4. Others

- 7.2.5. Baby Formula

- 7.2.5.1. Organic Infant Formula

- 7.2.5.2. Follow-On Formula

- 7.2.5.3. Toddler Formula

- 7.2.5.4. Others

- 7.2.1. Baby Cereals

- 8. Global Organic and Clean Label Baby Food Market Analysis, by Packaging Type

- 8.1. Key Segment Analysis

- 8.2. Organic and Clean Label Baby Food Market Size (Value - US$ Bn), Analysis, and Forecasts, by Packaging Type, 2021-2035

- 8.2.1. Jars

- 8.2.2. Pouches

- 8.2.2.1. Squeeze Pouches

- 8.2.2.2. Stand-Up Pouches

- 8.2.2.3. Spout Pouches

- 8.2.3. Boxes

- 8.2.4. Cans

- 8.2.4.1. Metal Cans

- 8.2.4.2. Composite Cans

- 8.2.5. Bottles

- 8.2.6. Others

- 9. Global Organic and Clean Label Baby Food Market Analysis, by Age Group

- 9.1. Key Segment Analysis

- 9.2. Organic and Clean Label Baby Food Market Size (Value - US$ Bn), Analysis, and Forecasts, by Age Group, 2021-2035

- 9.2.1. 0-6 Months

- 9.2.2. 6-12 Months

- 9.2.3. 12-24 Months

- 9.2.4. 24-36 Months

- 9.2.5. Above 36 Months

- 10. Global Organic and Clean Label Baby Food Market Analysis, by Ingredient Base

- 10.1. Key Segment Analysis

- 10.2. Organic and Clean Label Baby Food Market Size (Value - US$ Bn), Analysis, and Forecasts, by Ingredient Base, 2021-2035

- 10.2.1. Fruit-Based

- 10.2.2. Vegetable-Based

- 10.2.3. Grain-Based

- 10.2.4. Protein-Based

- 10.2.5. Dairy-Based

- 11. Global Organic and Clean Label Baby Food Market Analysis, by Distribution Channel

- 11.1. Key Segment Analysis

- 11.2. Organic and Clean Label Baby Food Market Size (Value - US$ Bn), Analysis, and Forecasts, by Distribution Channel, 2021-2035

- 11.2.1. Offline Channels

- 11.2.1.1. Supermarkets/Hypermarkets

- 11.2.1.2. Specialty Stores

- 11.2.1.3. Convenience Stores

- 11.2.1.4. Pharmacies/Drugstores

- 11.2.1.5. Baby Product Stores

- 11.2.1.6. Others

- 11.2.2. Online Channels

- 11.2.2.1. E-commerce Platforms

- 11.2.2.2. Company Websites

- 11.2.2.3. Others

- 11.2.1. Offline Channels

- 12. Global Organic and Clean Label Baby Food Market Analysis, by Texture/Consistency

- 12.1. Key Segment Analysis

- 12.2. Organic and Clean Label Baby Food Market Size (Value - US$ Bn), Analysis, and Forecasts, by Texture/Consistency, 2021-2035

- 12.2.1. Smooth Purees

- 12.2.2. Chunky Purees

- 12.2.3. Mashed

- 12.2.4. Finger Foods

- 12.2.5. Liquid

- 13. Global Organic and Clean Label Baby Food Market Analysis, by End-users

- 13.1. Key Segment Analysis

- 13.2. Organic and Clean Label Baby Food Market Size (Value - US$ Bn), Analysis, and Forecasts, by End-users, 2021-2035

- 13.2.1. Direct Consumer Purchase

- 13.2.2. Hospital Nurseries

- 13.2.3. Pediatric Clinics

- 13.2.4. Airline Catering

- 13.2.5. Daycare Centers

- 13.2.6. Orphanages

- 13.2.7. Preschools

- 13.2.8. Others

- 14. Global Organic and Clean Label Baby Food Market Analysis and Forecasts, by Region

- 14.1. Key Findings

- 14.2. Organic and Clean Label Baby Food Market Size (Value - US$ Bn), Analysis, and Forecasts, by Region, 2021-2035

- 14.2.1. North America

- 14.2.2. Europe

- 14.2.3. Asia Pacific

- 14.2.4. Middle East

- 14.2.5. Africa

- 14.2.6. South America

- 15. North America Organic and Clean Label Baby Food Market Analysis

- 15.1. Key Segment Analysis

- 15.2. Regional Snapshot

- 15.3. North America Organic and Clean Label Baby Food Market Size (Value - US$ Bn), Analysis, and Forecasts, 2021-2035

- 15.3.1. Product Type

- 15.3.2. Food Category

- 15.3.3. Packaging Type

- 15.3.4. Age Group

- 15.3.5. Ingredient Base

- 15.3.6. Distribution Channel

- 15.3.7. Texture/Consistency

- 15.3.8. End-users

- 15.3.9. Country

- 15.3.9.1. USA

- 15.3.9.2. Canada

- 15.3.9.3. Mexico

- 15.4. USA Organic and Clean Label Baby Food Market

- 15.4.1. Country Segmental Analysis

- 15.4.2. Product Type

- 15.4.3. Food Category

- 15.4.4. Packaging Type

- 15.4.5. Age Group

- 15.4.6. Ingredient Base

- 15.4.7. Distribution Channel

- 15.4.8. Texture/Consistency

- 15.4.9. End-users

- 15.5. Canada Organic and Clean Label Baby Food Market

- 15.5.1. Country Segmental Analysis

- 15.5.2. Product Type

- 15.5.3. Food Category

- 15.5.4. Packaging Type

- 15.5.5. Age Group

- 15.5.6. Ingredient Base

- 15.5.7. Distribution Channel

- 15.5.8. Texture/Consistency

- 15.5.9. End-users

- 15.6. Mexico Organic and Clean Label Baby Food Market

- 15.6.1. Country Segmental Analysis

- 15.6.2. Product Type

- 15.6.3. Food Category

- 15.6.4. Packaging Type

- 15.6.5. Age Group

- 15.6.6. Ingredient Base

- 15.6.7. Distribution Channel

- 15.6.8. Texture/Consistency

- 15.6.9. End-users

- 16. Europe Organic and Clean Label Baby Food Market Analysis

- 16.1. Key Segment Analysis

- 16.2. Regional Snapshot

- 16.3. Europe Organic and Clean Label Baby Food Market Size (Value - US$ Bn), Analysis, and Forecasts, 2021-2035

- 16.3.1. Product Type

- 16.3.2. Food Category

- 16.3.3. Packaging Type

- 16.3.4. Age Group

- 16.3.5. Ingredient Base

- 16.3.6. Distribution Channel

- 16.3.7. Texture/Consistency

- 16.3.8. End-users

- 16.3.9. Country

- 16.3.9.1. Germany

- 16.3.9.2. United Kingdom

- 16.3.9.3. France

- 16.3.9.4. Italy

- 16.3.9.5. Spain

- 16.3.9.6. Netherlands

- 16.3.9.7. Nordic Countries

- 16.3.9.8. Poland

- 16.3.9.9. Russia & CIS

- 16.3.9.10. Rest of Europe

- 16.4. Germany Organic and Clean Label Baby Food Market

- 16.4.1. Country Segmental Analysis

- 16.4.2. Product Type

- 16.4.3. Food Category

- 16.4.4. Packaging Type

- 16.4.5. Age Group

- 16.4.6. Ingredient Base

- 16.4.7. Distribution Channel

- 16.4.8. Texture/Consistency

- 16.4.9. End-users

- 16.5. United Kingdom Organic and Clean Label Baby Food Market

- 16.5.1. Country Segmental Analysis

- 16.5.2. Product Type

- 16.5.3. Food Category

- 16.5.4. Packaging Type

- 16.5.5. Age Group

- 16.5.6. Ingredient Base

- 16.5.7. Distribution Channel

- 16.5.8. Texture/Consistency

- 16.5.9. End-users

- 16.6. France Organic and Clean Label Baby Food Market

- 16.6.1. Country Segmental Analysis

- 16.6.2. Product Type

- 16.6.3. Food Category

- 16.6.4. Packaging Type

- 16.6.5. Age Group

- 16.6.6. Ingredient Base

- 16.6.7. Distribution Channel

- 16.6.8. Texture/Consistency

- 16.6.9. End-users

- 16.7. Italy Organic and Clean Label Baby Food Market

- 16.7.1. Country Segmental Analysis

- 16.7.2. Product Type

- 16.7.3. Food Category

- 16.7.4. Packaging Type

- 16.7.5. Age Group

- 16.7.6. Ingredient Base

- 16.7.7. Distribution Channel

- 16.7.8. Texture/Consistency

- 16.7.9. End-users

- 16.8. Spain Organic and Clean Label Baby Food Market

- 16.8.1. Country Segmental Analysis

- 16.8.2. Product Type

- 16.8.3. Food Category

- 16.8.4. Packaging Type

- 16.8.5. Age Group

- 16.8.6. Ingredient Base

- 16.8.7. Distribution Channel

- 16.8.8. Texture/Consistency

- 16.8.9. End-users

- 16.9. Netherlands Organic and Clean Label Baby Food Market

- 16.9.1. Country Segmental Analysis

- 16.9.2. Product Type

- 16.9.3. Food Category

- 16.9.4. Packaging Type

- 16.9.5. Age Group

- 16.9.6. Ingredient Base

- 16.9.7. Distribution Channel

- 16.9.8. Texture/Consistency

- 16.9.9. End-users

- 16.10. Nordic Countries Organic and Clean Label Baby Food Market

- 16.10.1. Country Segmental Analysis

- 16.10.2. Product Type

- 16.10.3. Food Category

- 16.10.4. Packaging Type

- 16.10.5. Age Group

- 16.10.6. Ingredient Base

- 16.10.7. Distribution Channel

- 16.10.8. Texture/Consistency

- 16.10.9. End-users

- 16.11. Poland Organic and Clean Label Baby Food Market

- 16.11.1. Country Segmental Analysis

- 16.11.2. Product Type

- 16.11.3. Food Category

- 16.11.4. Packaging Type

- 16.11.5. Age Group

- 16.11.6. Ingredient Base

- 16.11.7. Distribution Channel

- 16.11.8. Texture/Consistency

- 16.11.9. End-users

- 16.12. Russia & CIS Organic and Clean Label Baby Food Market

- 16.12.1. Country Segmental Analysis

- 16.12.2. Product Type

- 16.12.3. Food Category

- 16.12.4. Packaging Type

- 16.12.5. Age Group

- 16.12.6. Ingredient Base

- 16.12.7. Distribution Channel

- 16.12.8. Texture/Consistency

- 16.12.9. End-users

- 16.13. Rest of Europe Organic and Clean Label Baby Food Market

- 16.13.1. Country Segmental Analysis

- 16.13.2. Product Type

- 16.13.3. Food Category

- 16.13.4. Packaging Type

- 16.13.5. Age Group

- 16.13.6. Ingredient Base

- 16.13.7. Distribution Channel

- 16.13.8. Texture/Consistency

- 16.13.9. End-users

- 17. Asia Pacific Organic and Clean Label Baby Food Market Analysis

- 17.1. Key Segment Analysis

- 17.2. Regional Snapshot

- 17.3. Asia Pacific Organic and Clean Label Baby Food Market Size (Value - US$ Bn), Analysis, and Forecasts, 2021-2035

- 17.3.1. Product Type

- 17.3.2. Food Category

- 17.3.3. Packaging Type

- 17.3.4. Age Group

- 17.3.5. Ingredient Base

- 17.3.6. Distribution Channel

- 17.3.7. Texture/Consistency

- 17.3.8. End-users

- 17.3.9. Country

- 17.3.9.1. China

- 17.3.9.2. India

- 17.3.9.3. Japan

- 17.3.9.4. South Korea

- 17.3.9.5. Australia and New Zealand

- 17.3.9.6. Indonesia

- 17.3.9.7. Malaysia

- 17.3.9.8. Thailand

- 17.3.9.9. Vietnam

- 17.3.9.10. Rest of Asia Pacific

- 17.4. China Organic and Clean Label Baby Food Market

- 17.4.1. Country Segmental Analysis

- 17.4.2. Product Type

- 17.4.3. Food Category

- 17.4.4. Packaging Type

- 17.4.5. Age Group

- 17.4.6. Ingredient Base

- 17.4.7. Distribution Channel

- 17.4.8. Texture/Consistency

- 17.4.9. End-users

- 17.5. India Organic and Clean Label Baby Food Market

- 17.5.1. Country Segmental Analysis

- 17.5.2. Product Type

- 17.5.3. Food Category

- 17.5.4. Packaging Type

- 17.5.5. Age Group

- 17.5.6. Ingredient Base

- 17.5.7. Distribution Channel

- 17.5.8. Texture/Consistency

- 17.5.9. End-users

- 17.6. Japan Organic and Clean Label Baby Food Market

- 17.6.1. Country Segmental Analysis

- 17.6.2. Product Type

- 17.6.3. Food Category

- 17.6.4. Packaging Type

- 17.6.5. Age Group

- 17.6.6. Ingredient Base

- 17.6.7. Distribution Channel

- 17.6.8. Texture/Consistency

- 17.6.9. End-users

- 17.7. South Korea Organic and Clean Label Baby Food Market

- 17.7.1. Country Segmental Analysis

- 17.7.2. Product Type

- 17.7.3. Food Category

- 17.7.4. Packaging Type

- 17.7.5. Age Group

- 17.7.6. Ingredient Base

- 17.7.7. Distribution Channel

- 17.7.8. Texture/Consistency

- 17.7.9. End-users

- 17.8. Australia and New Zealand Organic and Clean Label Baby Food Market

- 17.8.1. Country Segmental Analysis

- 17.8.2. Product Type

- 17.8.3. Food Category

- 17.8.4. Packaging Type

- 17.8.5. Age Group

- 17.8.6. Ingredient Base

- 17.8.7. Distribution Channel

- 17.8.8. Texture/Consistency

- 17.8.9. End-users

- 17.9. Indonesia Organic and Clean Label Baby Food Market

- 17.9.1. Country Segmental Analysis

- 17.9.2. Product Type

- 17.9.3. Food Category

- 17.9.4. Packaging Type

- 17.9.5. Age Group

- 17.9.6. Ingredient Base

- 17.9.7. Distribution Channel

- 17.9.8. Texture/Consistency

- 17.9.9. End-users

- 17.10. Malaysia Organic and Clean Label Baby Food Market

- 17.10.1. Country Segmental Analysis

- 17.10.2. Product Type

- 17.10.3. Food Category

- 17.10.4. Packaging Type

- 17.10.5. Age Group

- 17.10.6. Ingredient Base

- 17.10.7. Distribution Channel

- 17.10.8. Texture/Consistency

- 17.10.9. End-users

- 17.11. Thailand Organic and Clean Label Baby Food Market

- 17.11.1. Country Segmental Analysis

- 17.11.2. Product Type

- 17.11.3. Food Category

- 17.11.4. Packaging Type

- 17.11.5. Age Group

- 17.11.6. Ingredient Base

- 17.11.7. Distribution Channel

- 17.11.8. Texture/Consistency

- 17.11.9. End-users

- 17.12. Vietnam Organic and Clean Label Baby Food Market

- 17.12.1. Country Segmental Analysis

- 17.12.2. Product Type

- 17.12.3. Food Category

- 17.12.4. Packaging Type

- 17.12.5. Age Group

- 17.12.6. Ingredient Base

- 17.12.7. Distribution Channel

- 17.12.8. Texture/Consistency

- 17.12.9. End-users

- 17.13. Rest of Asia Pacific Organic and Clean Label Baby Food Market

- 17.13.1. Country Segmental Analysis

- 17.13.2. Product Type

- 17.13.3. Food Category

- 17.13.4. Packaging Type

- 17.13.5. Age Group

- 17.13.6. Ingredient Base

- 17.13.7. Distribution Channel

- 17.13.8. Texture/Consistency

- 17.13.9. End-users

- 18. Middle East Organic and Clean Label Baby Food Market Analysis

- 18.1. Key Segment Analysis

- 18.2. Regional Snapshot

- 18.3. Middle East Organic and Clean Label Baby Food Market Size (Value - US$ Bn), Analysis, and Forecasts, 2021-2035

- 18.3.1. Product Type

- 18.3.2. Food Category

- 18.3.3. Packaging Type

- 18.3.4. Age Group

- 18.3.5. Ingredient Base

- 18.3.6. Distribution Channel

- 18.3.7. Texture/Consistency

- 18.3.8. End-users

- 18.3.9. Country

- 18.3.9.1. Turkey

- 18.3.9.2. UAE

- 18.3.9.3. Saudi Arabia

- 18.3.9.4. Israel

- 18.3.9.5. Rest of Middle East

- 18.4. Turkey Organic and Clean Label Baby Food Market

- 18.4.1. Country Segmental Analysis

- 18.4.2. Product Type

- 18.4.3. Food Category

- 18.4.4. Packaging Type

- 18.4.5. Age Group

- 18.4.6. Ingredient Base

- 18.4.7. Distribution Channel

- 18.4.8. Texture/Consistency

- 18.4.9. End-users

- 18.5. UAE Organic and Clean Label Baby Food Market

- 18.5.1. Country Segmental Analysis

- 18.5.2. Product Type

- 18.5.3. Food Category

- 18.5.4. Packaging Type

- 18.5.5. Age Group

- 18.5.6. Ingredient Base

- 18.5.7. Distribution Channel

- 18.5.8. Texture/Consistency

- 18.5.9. End-users

- 18.6. Saudi Arabia Organic and Clean Label Baby Food Market

- 18.6.1. Country Segmental Analysis

- 18.6.2. Product Type

- 18.6.3. Food Category

- 18.6.4. Packaging Type

- 18.6.5. Age Group

- 18.6.6. Ingredient Base

- 18.6.7. Distribution Channel

- 18.6.8. Texture/Consistency

- 18.6.9. End-users

- 18.7. Israel Organic and Clean Label Baby Food Market

- 18.7.1. Country Segmental Analysis

- 18.7.2. Product Type

- 18.7.3. Food Category

- 18.7.4. Packaging Type

- 18.7.5. Age Group

- 18.7.6. Ingredient Base

- 18.7.7. Distribution Channel

- 18.7.8. Texture/Consistency

- 18.7.9. End-users

- 18.8. Rest of Middle East Organic and Clean Label Baby Food Market

- 18.8.1. Country Segmental Analysis

- 18.8.2. Product Type

- 18.8.3. Food Category

- 18.8.4. Packaging Type

- 18.8.5. Age Group

- 18.8.6. Ingredient Base

- 18.8.7. Distribution Channel

- 18.8.8. Texture/Consistency

- 18.8.9. End-users

- 19. Africa Organic and Clean Label Baby Food Market Analysis

- 19.1. Key Segment Analysis

- 19.2. Regional Snapshot

- 19.3. Africa Organic and Clean Label Baby Food Market Size (Value - US$ Bn), Analysis, and Forecasts, 2021-2035

- 19.3.1. Product Type

- 19.3.2. Food Category

- 19.3.3. Packaging Type

- 19.3.4. Age Group

- 19.3.5. Ingredient Base

- 19.3.6. Distribution Channel

- 19.3.7. Texture/Consistency

- 19.3.8. End-users

- 19.3.9. Country

- 19.3.9.1. South Africa

- 19.3.9.2. Egypt

- 19.3.9.3. Nigeria

- 19.3.9.4. Algeria

- 19.3.9.5. Rest of Africa

- 19.4. South Africa Organic and Clean Label Baby Food Market

- 19.4.1. Country Segmental Analysis

- 19.4.2. Product Type

- 19.4.3. Food Category

- 19.4.4. Packaging Type

- 19.4.5. Age Group

- 19.4.6. Ingredient Base

- 19.4.7. Distribution Channel

- 19.4.8. Texture/Consistency

- 19.4.9. End-users

- 19.5. Egypt Organic and Clean Label Baby Food Market

- 19.5.1. Country Segmental Analysis

- 19.5.2. Product Type

- 19.5.3. Food Category

- 19.5.4. Packaging Type

- 19.5.5. Age Group

- 19.5.6. Ingredient Base

- 19.5.7. Distribution Channel

- 19.5.8. Texture/Consistency

- 19.5.9. End-users

- 19.6. Nigeria Organic and Clean Label Baby Food Market

- 19.6.1. Country Segmental Analysis

- 19.6.2. Product Type

- 19.6.3. Food Category

- 19.6.4. Packaging Type

- 19.6.5. Age Group

- 19.6.6. Ingredient Base

- 19.6.7. Distribution Channel

- 19.6.8. Texture/Consistency

- 19.6.9. End-users

- 19.7. Algeria Organic and Clean Label Baby Food Market

- 19.7.1. Country Segmental Analysis

- 19.7.2. Product Type

- 19.7.3. Food Category

- 19.7.4. Packaging Type

- 19.7.5. Age Group

- 19.7.6. Ingredient Base

- 19.7.7. Distribution Channel

- 19.7.8. Texture/Consistency

- 19.7.9. End-users

- 19.8. Rest of Africa Organic and Clean Label Baby Food Market

- 19.8.1. Country Segmental Analysis

- 19.8.2. Product Type

- 19.8.3. Food Category

- 19.8.4. Packaging Type

- 19.8.5. Age Group

- 19.8.6. Ingredient Base

- 19.8.7. Distribution Channel

- 19.8.8. Texture/Consistency

- 19.8.9. End-users

- 20. South America Organic and Clean Label Baby Food Market Analysis

- 20.1. Key Segment Analysis

- 20.2. Regional Snapshot

- 20.3. South America Organic and Clean Label Baby Food Market Size (Value - US$ Bn), Analysis, and Forecasts, 2021-2035

- 20.3.1. Product Type

- 20.3.2. Food Category

- 20.3.3. Packaging Type

- 20.3.4. Age Group

- 20.3.5. Ingredient Base

- 20.3.6. Distribution Channel

- 20.3.7. Texture/Consistency

- 20.3.8. End-users

- 20.3.9. Country

- 20.3.9.1. Brazil

- 20.3.9.2. Argentina

- 20.3.9.3. Rest of South America

- 20.4. Brazil Organic and Clean Label Baby Food Market

- 20.4.1. Country Segmental Analysis

- 20.4.2. Product Type

- 20.4.3. Food Category

- 20.4.4. Packaging Type

- 20.4.5. Age Group

- 20.4.6. Ingredient Base

- 20.4.7. Distribution Channel

- 20.4.8. Texture/Consistency

- 20.4.9. End-users

- 20.5. Argentina Organic and Clean Label Baby Food Market

- 20.5.1. Country Segmental Analysis

- 20.5.2. Product Type

- 20.5.3. Food Category

- 20.5.4. Packaging Type

- 20.5.5. Age Group

- 20.5.6. Ingredient Base

- 20.5.7. Distribution Channel

- 20.5.8. Texture/Consistency

- 20.5.9. End-users

- 20.6. Rest of South America Organic and Clean Label Baby Food Market

- 20.6.1. Country Segmental Analysis

- 20.6.2. Product Type

- 20.6.3. Food Category

- 20.6.4. Packaging Type

- 20.6.5. Age Group

- 20.6.6. Ingredient Base

- 20.6.7. Distribution Channel

- 20.6.8. Texture/Consistency

- 20.6.9. End-users

- 21. Key Players/ Company Profile

- 21.1. Amara Organic Foods

- 21.1.1. Company Details/ Overview

- 21.1.2. Company Financials

- 21.1.3. Key Customers and Competitors

- 21.1.4. Business/ Industry Portfolio

- 21.1.5. Product Portfolio/ Specification Details

- 21.1.6. Pricing Data

- 21.1.7. Strategic Overview

- 21.1.8. Recent Developments

- 21.2. Baby Gourmet Foods Inc.

- 21.3. Beech-Nut Nutrition Company

- 21.4. Cerebelly

- 21.5. Danone S.A.

- 21.6. Ella's Kitchen (Hain Celestial)

- 21.7. Happy Family Organics (Danone)

- 21.8. Hero Group

- 21.9. HiPP GmbH & Co. Vertrieb KG

- 21.10. Holle baby food AG

- 21.11. Little Freddie

- 21.12. Little Spoon

- 21.13. Nestlé S.A.

- 21.14. Once Upon a Farm

- 21.15. Perrigo Company plc

- 21.16. Piccolo

- 21.17. Plum Organics (Campbell Soup Company)

- 21.18. Serenity Kids

- 21.19. Sprout Organic Foods

- 21.20. The Hain Celestial Group

- 21.21. Other Key Players

- 21.1. Amara Organic Foods

Note* - This is just tentative list of players. While providing the report, we will cover more number of players based on their revenue and share for each geography

Research Design

Our research design integrates both demand-side and supply-side analysis through a balanced combination of primary and secondary research methodologies. By utilizing both bottom-up and top-down approaches alongside rigorous data triangulation methods, we deliver robust market intelligence that supports strategic decision-making.

MarketGenics' comprehensive research design framework ensures the delivery of accurate, reliable, and actionable market intelligence. Through the integration of multiple research approaches, rigorous validation processes, and expert analysis, we provide our clients with the insights needed to make informed strategic decisions and capitalize on market opportunities.

MarketGenics leverages a dedicated industry panel of experts and a comprehensive suite of paid databases to effectively collect, consolidate, and analyze market intelligence.

Our approach has consistently proven to be reliable and effective in generating accurate market insights, identifying key industry trends, and uncovering emerging business opportunities.

Through both primary and secondary research, we capture and analyze critical company-level data such as manufacturing footprints, including technical centers, R&D facilities, sales offices, and headquarters.

Our expert panel further enhances our ability to estimate market size for specific brands based on validated field-level intelligence.

Our data mining techniques incorporate both parametric and non-parametric methods, allowing for structured data collection, sorting, processing, and cleaning.

Demand projections are derived from large-scale data sets analyzed through proprietary algorithms, culminating in robust and reliable market sizing.

Research Approach

The bottom-up approach builds market estimates by starting with the smallest addressable market units and systematically aggregating them to create comprehensive market size projections.

This method begins with specific, granular data points and builds upward to create the complete market landscape.

Customer Analysis → Segmental Analysis → Geographical Analysis

The top-down approach starts with the broadest possible market data and systematically narrows it down through a series of filters and assumptions to arrive at specific market segments or opportunities.

This method begins with the big picture and works downward to increasingly specific market slices.

TAM → SAM → SOM

Research Methods

Desk / Secondary Research

While analysing the market, we extensively study secondary sources, directories, and databases to identify and collect information useful for this technical, market-oriented, and commercial report. Secondary sources that we utilize are not only the public sources, but it is a combination of Open Source, Associations, Paid Databases, MG Repository & Knowledgebase, and others.

- Company websites, annual reports, financial reports, broker reports, and investor presentations

- National government documents, statistical databases and reports

- News articles, press releases and web-casts specific to the companies operating in the market, Magazines, reports, and others

- We gather information from commercial data sources for deriving company specific data such as segmental revenue, share for geography, product revenue, and others

- Internal and external proprietary databases (industry-specific), relevant patent, and regulatory databases

- Governing Bodies, Government Organizations

- Relevant Authorities, Country-specific Associations for Industries

We also employ the model mapping approach to estimate the product level market data through the players' product portfolio

Primary Research

Primary research/ interviews is vital in analyzing the market. Most of the cases involves paid primary interviews. Primary sources include primary interviews through e-mail interactions, telephonic interviews, surveys as well as face-to-face interviews with the different stakeholders across the value chain including several industry experts.

| Type of Respondents | Number of Primaries |

|---|---|

| Tier 2/3 Suppliers | ~20 |

| Tier 1 Suppliers | ~25 |

| End-users | ~25 |

| Industry Expert/ Panel/ Consultant | ~30 |

| Total | ~100 |

MG Knowledgebase

• Repository of industry blog, newsletter and case studies

• Online platform covering detailed market reports, and company profiles

Forecasting Factors and Models

Forecasting Factors

- Historical Trends – Past market patterns, cycles, and major events that shaped how markets behave over time. Understanding past trends helps predict future behavior.

- Industry Factors – Specific characteristics of the industry like structure, regulations, and innovation cycles that affect market dynamics.

- Macroeconomic Factors – Economic conditions like GDP growth, inflation, and employment rates that affect how much money people have to spend.

- Demographic Factors – Population characteristics like age, income, and location that determine who can buy your product.

- Technology Factors – How quickly people adopt new technology and how much technology infrastructure exists.

- Regulatory Factors – Government rules, laws, and policies that can help or restrict market growth.

- Competitive Factors – Analyzing competition structure such as degree of competition and bargaining power of buyers and suppliers.

Forecasting Models / Techniques

Multiple Regression Analysis

- Identify and quantify factors that drive market changes

- Statistical modeling to establish relationships between market drivers and outcomes

Time Series Analysis – Seasonal Patterns

- Understand regular cyclical patterns in market demand

- Advanced statistical techniques to separate trend, seasonal, and irregular components

Time Series Analysis – Trend Analysis

- Identify underlying market growth patterns and momentum

- Statistical analysis of historical data to project future trends

Expert Opinion – Expert Interviews

- Gather deep industry insights and contextual understanding

- In-depth interviews with key industry stakeholders

Multi-Scenario Development

- Prepare for uncertainty by modeling different possible futures

- Creating optimistic, pessimistic, and most likely scenarios

Time Series Analysis – Moving Averages

- Sophisticated forecasting for complex time series data

- Auto-regressive integrated moving average models with seasonal components

Econometric Models

- Apply economic theory to market forecasting

- Sophisticated economic models that account for market interactions

Expert Opinion – Delphi Method

- Harness collective wisdom of industry experts

- Structured, multi-round expert consultation process

Monte Carlo Simulation

- Quantify uncertainty and probability distributions

- Thousands of simulations with varying input parameters

Research Analysis

Our research framework is built upon the fundamental principle of validating market intelligence from both demand and supply perspectives. This dual-sided approach ensures comprehensive market understanding and reduces the risk of single-source bias.

Demand-Side Analysis: We understand end-user/application behavior, preferences, and market needs along with the penetration of the product for specific application.

Supply-Side Analysis: We estimate overall market revenue, analyze the segmental share along with industry capacity, competitive landscape, and market structure.

Validation & Evaluation

Data triangulation is a validation technique that uses multiple methods, sources, or perspectives to examine the same research question, thereby increasing the credibility and reliability of research findings. In market research, triangulation serves as a quality assurance mechanism that helps identify and minimize bias, validate assumptions, and ensure accuracy in market estimates.

- Data Source Triangulation – Using multiple data sources to examine the same phenomenon

- Methodological Triangulation – Using multiple research methods to study the same research question

- Investigator Triangulation – Using multiple researchers or analysts to examine the same data

- Theoretical Triangulation – Using multiple theoretical perspectives to interpret the same data

Custom Market Research Services

We will customise the research for you, in case the report listed above does not meet your requirements.

Get 10% Free Customisation