Quinoa Starch Market Size, Share & Trends Analysis Report by Product Type (Native Quinoa Starch, Modified Quinoa Starch, Organic Quinoa Starch, Conventional Quinoa Starch), Form, Source/Variety, Extraction Method, Functionality, Distribution Channel, Packaging Type, End-use Industry, and Geography (North America, Europe, Asia Pacific, Middle East, Africa, and South America) – Global Industry Data, Trends, and Forecasts, 2026–2035

|

|

|

Segmental Data Insights |

|

|

Demand Trends |

|

|

Competitive Landscape |

|

|

Strategic Development |

|

|

Future Outlook & Opportunities |

|

Quinoa Starch Market Size, Share, and Growth

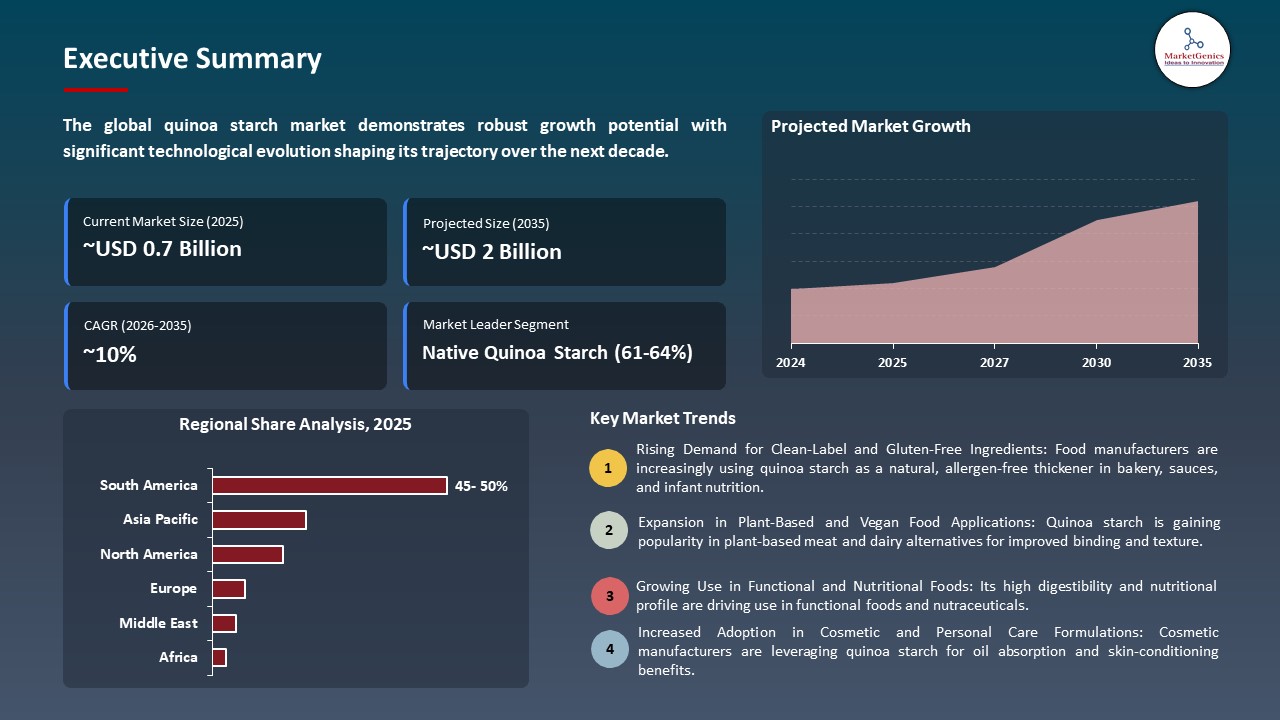

The global quinoa starch market is experiencing robust growth, with its estimated value of USD 0.7 billion in the year 2025 and USD 1.9 billion by the period 2035, registering a CAGR of 10.3%, during the forecast period. The global quinoa starch market is undergoing a surge in growth as producers, brand name, and food regulatory authorities identify the essence of the sustainable, traceable, and environmentally friendly sourcing of ingredients.

Isabelle Lacasse, Head Global Marketing, Product Line Management & Formulation at Lucas Meyer Cosmetics, states that Pickmulse offers a multifaceted and innovative approach to cosmetics. She explains that the product is designed to significantly accelerate new formula development while improving consumer satisfaction. According to her, this next-generation 2-in-1 solution strikes a balance between formulation requirements and enhancing skin health and feel.

The global quinoa starch market is moving past a niche functional ingredient and into a strategic ingredient in clean-label, plant-based, sustainable formulations in the food, beverage, nutraceutical, personal-care, and pharmaceutical industries. The growing popularity of natural, allergen free and gluten free products, plus the growing regulatory focus on transparency and ingredient traceability, is pushing manufacturers towards high purity and organic as well as sustainability sourced quinoa starch.

Its processing and use are becoming more diverse and is finding application in specialty grades, ultra-fine starches and in fractionated functional ingredients that deliver better texture, stability and nutritional value. The focus on sustainability through environmentally friendly sourcing, low impact extraction and little processing makes quinoa starch consistent with larger sustainability objectives without compromising its practical efficiency.

Adjacent opportunities to the quinoa starch market include gluten-free and clean-label bakery products, plant-based dairy alternatives, nutraceutical and functional food formulations, biodegradable films and edible coatings, and pharmaceutical excipients for tablets and capsules, leveraging quinoa starch’s thickening, gelling, and film-forming properties, thereby expanding application versatility, supporting health-focused product innovation, and reducing reliance on conventional starch sources.

Quinoa Starch Market Dynamics and Trends

Driver: Growing Demand for Clean-Label and Gluten-Free Products

-

The global quinoa starch market is being propelled by the trend of using clean-label, allergen-free, and plant-based ingredients in food, beverage, nutraceutical, and personal-care markets. The movement of customers towards more natural, least-processed, and artificial-additive-free products is directly promoting the usage of gluten-free and native quinoa starch.

- Manufacturers are redeveloping products with the use of quinoa starch to substitute modified or synthetic starches without reducing texture, stability, or shelf-life as a response both to health-conscious movement and to regulatory requirements regarding the transparency of labels. This change provides brands with gluten free, high protein, and functional food solutions that meet specialized dietary requirements.

- Growing health consciousness and favor towards gluten-free, clean-label, and plant-based foods are increasing the demand in quinoa starch in bakery, dairy substitutes, and beverage uses, which is driving the global market growth.

Restraint: High Raw Material Cost and Limited Large-Scale Cultivation

-

Limitations of the global quinoa starch market is the high price of raw quinoa grains in comparison to traditional sources of starch i.e. corn, wheat, or potato. Production costs are also increased as special extraction tools and controlled processing environment and quality assurance systems are costlier and restrict competitiveness of small and medium-sized producers.

- Supply chain limitations make the problem worse, since high-quality quinoa that can be extracted to produce starch is located in particular parts of Andes, making it susceptible to seasons, climate unpredictability’s, and geopolitics. Such geographic concentration limits the ability to supply on a large scale and scale, and procurement becomes expensive to international manufacturers.

- Additional challenges, such as the intricacy of the processing system, storage requirements, and adherence to food-grade standards, contribute to increased operational costs. These obstacles restrict the fast uptake and expansion of quinoa starch in the new markets.

Opportunity: Expansion in Organic and Sustainable Ingredients

-

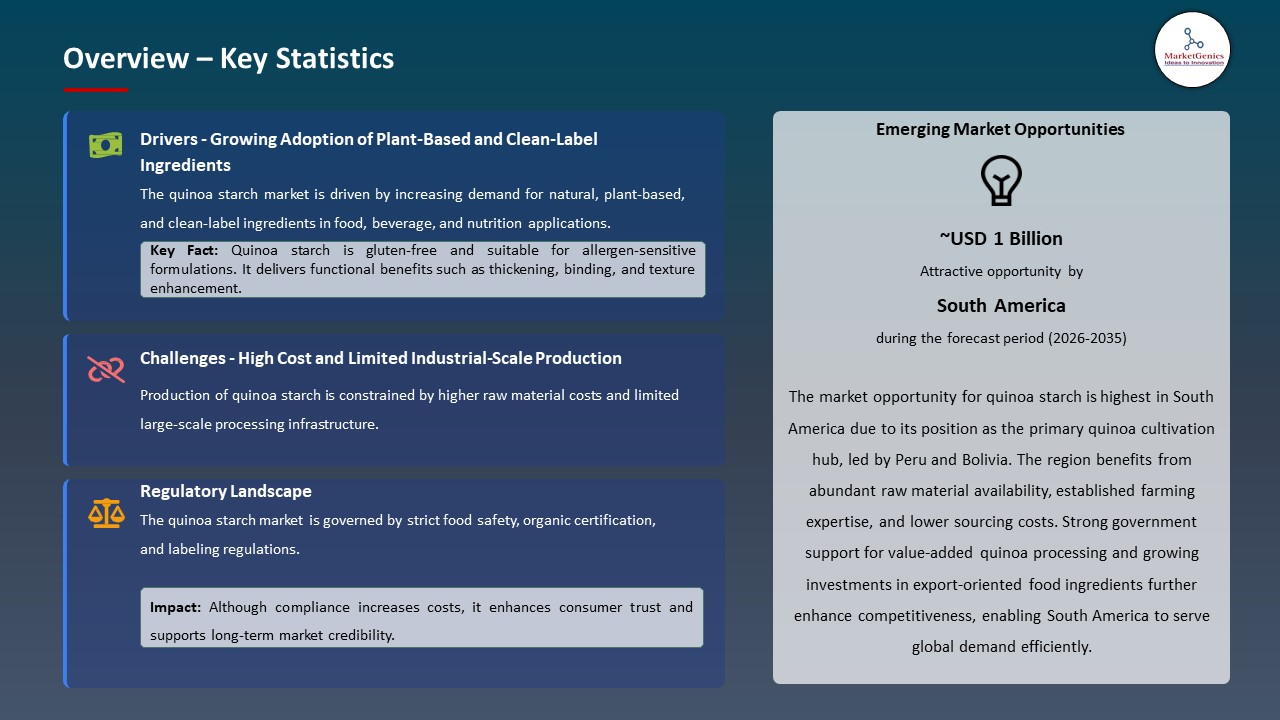

There is a rising opportunity in the global quinoa starch market due to the increase in the demand of organic, non-GMO, and sustainably sourced food, beverage, nutraceutical, and personal-care products. Consumers and brands are becoming more concerned with natural, eco-friendly ingredients and this has resulted in the need to have quinoa starch with organic certification and low-impact production.

- Manufacturers are also utilizing this trend by investing in more advanced more eco-friendly cultivation and extraction processes. For instance, businesses are launching organic-certified quinoa starch which is minimally processed and extracted without any solvents and is highly pure and functional in use with little water, energy usage and carbon footprint throughout the supply-chain.

- As brands gain popularity in the use of clean-label and sustainably sourced ingredients, quinoa starch manufacturers will have the ability to drive portfolios, create specialty functional grades, and tap into high-value markets in need of high-end and eco-friendly ingredients.

Key Trend: Integration into Functional and Specialty Applications

-

The quinoa starch market is undergoing a major trend of integration into high-value functionality and specialty uses because of the consumer demand of natural and plant-based ingredients with customized functionality in various end-use applications. The rheological and sensory properties that quinoa starch has are being used by manufacturers to reformulate products in gluten-free bakery, clean-label sauces, and protein-fortified beverages without affecting the quality of the product.

- Quinoa starch applications have gained more rapidity in terms of innovation whereby refined and fractionation technologies have made it possible to produce ultra-fine, clarity starch, and starch grades that can hydrate rapidly. For instance, next-generation quinoa starch derivatives are currently being used in speciality nutraceuticals and encapsulation system to enhance bioavailability of active compounds, expand functionality in freeze/thaw stable systems, and serve new texturization requirements in plant-based dairy analogs.

- Quinoa starch solutions that are functional are becoming popular because of their appeal as clean labels and as natural processed products. The trend is increasing the product differentiation and performance in the global food, beverage, pharmaceutical and cosmetic applications.

Quinoa-Starch-Market Analysis and Segmental Data

Native Quinoa Starch Dominate Global Quinoa Starch Market

-

Native quinoa starch leads the quinoa starch market because of inherent functionality such as excellent gel strength, neutral flavor profile, and clean-label use in food, beverage, pharmaceutical and cosmetic products. It has both favorable attributes of gluten-free and plant-based formulations, which makes it a good option to formulators who aim to provide natural texture and stability without having to change the formulation significantly.

- Native quinoa starch innovation is ongoing, where manufacturers are maximizing the extraction and purification to produce a starch of greater clarity and smaller particle size, and with better hydration behavior. This improvement facilitates greater expansion in high-growth markets in the dairy substitutes and specialty bakery, nutritional supplements and biodegradable film applications, which attests to its applicability and scalability.

- Native quinoa starch is a more sustainable choice and incurs a very low processing footprint compared to the modified or synthetic versions. Its flexibility in different formulations strengthens its leading position in ingredient portfolios in the world.

South America Leads Global Quinoa Starch Market Demand

-

South America leads the global quinoa starch market with its dominant influence in quinoa grain production which is the raw material in the extraction of starch. The combination of Peru and Bolivia accounts to most part of the global quinoa production, which makes the region a regional powerhouse in the volume and quality of varieties of quinoa in terms of upstreams both in starch processing and export supply chains. This established source base facilitates the sourcing throughout the year, scale economies, and reputation of functional feedstock of quinoa starch in overseas markets.

- The dynamics of the regional industry demonstrate that domestic consumption is rapidly increasing and that growth is based on exports. This combined requirement boosts investment in processing capacity to enable adding value to raw grain beyond food, nutraceutical, and industrial applications by producing high-purity starch. In an effort to satisfy the increasing demand of functional and clean-label ingredients in the world, manufacturers are also paying much attention to sustainability and quality standards.

- The organic and specialty quinoa varieties produced in South America command a premium and niche demand in the world and this makes it a major supplier of quinoa as well as innovation.

Quinoa-Starch-Market Ecosystem

The global quinoa starch market has a moderately consolidated structure which is characterized by a combination of multinationals conglomerates and regional suppliers. Tier-1 competitors, such as Archer Daniels Midland Company (ADM), Cargill Incorporated and Ingredion Incorporated, use their large-scale production networks, leading-edge research and development and sustainability-focused innovations to offer high-quality quinoa starch to food, beverage, pharmaceutical and personal-care products at a global scale.

Tier-2 participants are Roquette Freres, which target niche or geographic markets, with specialized solutions, which are clean-label, functional, and bio-based starch derivatives. Tier-3 players are generally smaller niche producers, having a local or niche demand and highly tailored formulations or organic quinoa starch variations.

These include manufacturing (quinoa grains), starch extraction and processing, contract manufacturing and distribution via retail, e-commerce and industrial. Players in the market are investing more in automation, quality assurance, life cycle assessment and compliance with regulatory measures to ensure increased sustainability, less environmental impact and consolidated competitive standing in the various end-use industries.

Recent Development and Strategic Overview

-

In October 2024, Lucas Meyer Cosmetics by Clariant launched a new quinoa-based, skin-friendly emulsifier suitable in the modern cosmetic formulations. The ingredient uses biopolymers of quinoa to enhance texture stability and sensory activity. It advises clean-label, biodegradable and natural sourced formulation policies, which enhances quinoa starch-based ingredients as ingredients in high-end personal-care items.

- In March 2024, Kiwi Quinoa signed a deal to enter the U.S. market launching unique quinoa products that are grown in New Zealand. Its launch strives to focus on good, nutritious quinoa and broaden the consumer options, and help the innovation in functional and natural food ingredients.

Report Scope

|

Detail |

|

|

Market Size in 2025 |

USD 0.7 Bn |

|

Market Forecast Value in 2035 |

USD 1.9 Bn |

|

Growth Rate (CAGR) |

10.3% |

|

Forecast Period |

2026 – 2035 |

|

Historical Data Available for |

2021 – 2024 |

|

Market Size Units |

US$ Billion for Value Tons for Volume |

|

Report Format |

Electronic (PDF) + Excel |

|

North America |

Europe |

Asia Pacific |

Middle East |

Africa |

South America |

|

|

|

|

|

|

|

Companies Covered |

|||||

|

|

|

|

|

|

Quinoa-Starch-Market Segmentation and Highlights

|

Segment |

Sub-segment |

|

Quinoa Starch Market, By Product Type |

|

|

Quinoa Starch Market, By Form |

|

|

Quinoa Starch Market, By Technology |

|

|

Quinoa Starch Market, By Source/Variety |

|

|

Quinoa Starch Market, By Extraction Method |

|

|

Quinoa Starch Market, By Functionality |

|

|

Quinoa Starch Market, By Distribution Channel |

|

|

Quinoa Starch Market, By Packaging Type |

|

|

Quinoa Starch Market, By End-use Industry |

|

Frequently Asked Questions

Table of Contents

- 1. Research Methodology and Assumptions

- 1.1. Definitions

- 1.2. Research Design and Approach

- 1.3. Data Collection Methods

- 1.4. Base Estimates and Calculations

- 1.5. Forecasting Models

- 1.5.1. Key Forecast Factors & Impact Analysis

- 1.6. Secondary Research

- 1.6.1. Open Sources

- 1.6.2. Paid Databases

- 1.6.3. Associations

- 1.7. Primary Research

- 1.7.1. Primary Sources

- 1.7.2. Primary Interviews with Stakeholders across Ecosystem

- 2. Executive Summary

- 2.1. Global Quinoa Starch Market Outlook

- 2.1.1. Quinoa Starch Market Size (Volume - Tons and Value - US$ Bn), and Forecasts, 2021-2035

- 2.1.2. Compounded Annual Growth Rate Analysis

- 2.1.3. Growth Opportunity Analysis

- 2.1.4. Segmental Share Analysis

- 2.1.5. Geographical Share Analysis

- 2.2. Market Analysis and Facts

- 2.3. Supply-Demand Analysis

- 2.4. Competitive Benchmarking

- 2.5. Go-to- Market Strategy

- 2.5.1. Customer/ End-use Industry Assessment

- 2.5.2. Growth Opportunity Data, 2026-2035

- 2.5.2.1. Regional Data

- 2.5.2.2. Country Data

- 2.5.2.3. Segmental Data

- 2.5.3. Identification of Potential Market Spaces

- 2.5.4. GAP Analysis

- 2.5.5. Potential Attractive Price Points

- 2.5.6. Prevailing Market Risks & Challenges

- 2.5.7. Preferred Sales & Marketing Strategies

- 2.5.8. Key Recommendations and Analysis

- 2.5.9. A Way Forward

- 2.1. Global Quinoa Starch Market Outlook

- 3. Industry Data and Premium Insights

- 3.1. Global Food & Beverages Industry Overview, 2025

- 3.1.1. Food & Beverages Industry Ecosystem Analysis

- 3.1.2. Key Trends for Food & Beverages Industry

- 3.1.3. Regional Distribution for Food & Beverages Industry

- 3.2. Supplier Customer Data

- 3.3. Technology Roadmap and Developments

- 3.4. Trade Analysis

- 3.4.1. Import & Export Analysis, 2025

- 3.4.2. Top Importing Countries

- 3.4.3. Top Exporting Countries

- 3.5. Trump Tariff Impact Analysis

- 3.5.1. Manufacturer

- 3.5.1.1. Based on the component & Raw material

- 3.5.2. Supply Chain

- 3.5.3. End Consumer

- 3.5.1. Manufacturer

- 3.6. Raw Material Analysis

- 3.1. Global Food & Beverages Industry Overview, 2025

- 4. Market Overview

- 4.1. Market Dynamics

- 4.1.1. Drivers

- 4.1.1.1. Growing demand for gluten-free and clean-label food ingredients.

- 4.1.1.2. Increasing use of quinoa starch in functional foods and beverages.

- 4.1.1.3. Rising application in cosmetics and biodegradable packaging formulations.

- 4.1.2. Restraints

- 4.1.2.1. High raw material and processing costs compared to conventional starches.

- 4.1.2.2. Limited large-scale availability and supply chain constraints.

- 4.1.1. Drivers

- 4.2. Key Trend Analysis

- 4.3. Regulatory Framework

- 4.3.1. Key Regulations, Norms, and Subsidies, by Key Countries

- 4.3.2. Tariffs and Standards

- 4.3.3. Impact Analysis of Regulations on the Market

- 4.4. Value Chain Analysis

- 4.4.1. Raw Material Suppliers

- 4.4.2. Manufacturers

- 4.4.3. Dealers/ Distributors

- 4.4.4. End-Users/ Customers

- 4.5. Porter’s Five Forces Analysis

- 4.6. PESTEL Analysis

- 4.7. Global Quinoa Starch Market Demand

- 4.7.1. Historical Market Size – Volume (Tons) and Value (US$ Bn), 2020-2024

- 4.7.2. Current and Future Market Size – Volume (Tons) and Value (US$ Bn), 2026–2035

- 4.7.2.1. Y-o-Y Growth Trends

- 4.7.2.2. Absolute $ Opportunity Assessment

- 4.1. Market Dynamics

- 5. Competition Landscape

- 5.1. Competition structure

- 5.1.1. Fragmented v/s consolidated

- 5.2. Company Share Analysis, 2025

- 5.2.1. Global Company Market Share

- 5.2.2. By Region

- 5.2.2.1. North America

- 5.2.2.2. Europe

- 5.2.2.3. Asia Pacific

- 5.2.2.4. Middle East

- 5.2.2.5. Africa

- 5.2.2.6. South America

- 5.3. Product Comparison Matrix

- 5.3.1. Specifications

- 5.3.2. Market Positioning

- 5.3.3. Pricing

- 5.1. Competition structure

- 6. Global Quinoa Starch Market Analysis, by Product Type

- 6.1. Key Segment Analysis

- 6.2. Quinoa Starch Market Size (Volume - Tons and Value - US$ Bn), Analysis, and Forecasts, by Product Type, 2021-2035

- 6.2.1. Native Quinoa Starch

- 6.2.2. Modified Quinoa Starch

- 6.2.2.1. Physically Modified

- 6.2.2.2. Chemically Modified

- 6.2.2.3. Enzymatically Modified

- 6.2.3. Organic Quinoa Starch

- 6.2.4. Conventional Quinoa Starch

- 7. Global Quinoa Starch Market Analysis, by Form

- 7.1. Key Segment Analysis

- 7.2. Quinoa Starch Market Size (Volume - Tons and Value - US$ Bn), Analysis, and Forecasts, by Form, 2021-2035

- 7.2.1. Powder

- 7.2.2. Granules

- 7.2.3. Liquid/Gel

- 7.2.4. Flakes

- 8. Global Quinoa Starch Market Analysis, by Source/Variety

- 8.1. Key Segment Analysis

- 8.2. Quinoa Starch Market Size (Volume - Tons and Value - US$ Bn), Analysis, and Forecasts, by Source/Variety, 2021-2035

- 8.2.1. White Quinoa Starch

- 8.2.2. Red Quinoa Starch

- 8.2.3. Black Quinoa Starch

- 8.2.4. Tri-color Quinoa Starch

- 8.2.5. Others

- 9. Global Quinoa Starch Market Analysis, by Extraction Method

- 9.1. Key Segment Analysis

- 9.2. Quinoa Starch Market Size (Volume - Tons and Value - US$ Bn), Analysis, and Forecasts, by Extraction Method, 2021-2035

- 9.2.1. Wet Milling

- 9.2.2. Dry Milling

- 9.2.3. Enzymatic Extraction

- 9.2.4. Alkaline Extraction

- 9.2.5. Others

- 10. Global Quinoa Starch Market Analysis, by Functionality

- 10.1. Key Segment Analysis

- 10.2. Quinoa Starch Market Size (Volume - Tons and Value - US$ Bn), Analysis, and Forecasts, by Functionality, 2021-2035

- 10.2.1. Thickening Agent

- 10.2.2. Stabilizing Agent

- 10.2.3. Binding Agent

- 10.2.4. Gelling Agent

- 10.2.5. Emulsifying Agent

- 10.2.6. Film-forming Agent

- 10.2.7. Others

- 11. Global Quinoa Starch Market Analysis, by Distribution Channel

- 11.1. Key Segment Analysis

- 11.2. Quinoa Starch Market Size (Volume - Tons and Value - US$ Bn), Analysis, and Forecasts, by Distribution Channel, 2021-2035

- 11.2.1. Direct Sales/B2B

- 11.2.2. Distributors & Wholesalers

- 11.2.3. Online Retail

- 11.2.4. Specialty Stores

- 11.2.5. Supermarkets & Hypermarkets

- 12. Global Quinoa Starch Market Analysis, by Packaging Type

- 12.1. Key Segment Analysis

- 12.2. Quinoa Starch Market Size (Volume - Tons and Value - US$ Bn), Analysis, and Forecasts, by Packaging Type, 2021-2035

- 12.2.1. Bulk Packaging

- 12.2.1.1. 25 kg bags

- 12.2.1.2. 50 kg bags

- 12.2.1.3. Jumbo bags

- 12.2.2. Retail Packaging

- 12.2.2.1. Small packs (below 5 kg)

- 12.2.2.2. Medium packs (5-10 kg)

- 12.2.1. Bulk Packaging

- 13. Global Quinoa Starch Market Analysis, by End-use Industry

- 13.1. Key Segment Analysis

- 13.2. Quinoa Starch Market Size (Volume - Tons and Value - US$ Bn), Analysis, and Forecasts, by End-use Industry, 2021-2035

- 13.2.1. Food & Beverage

- 13.2.1.1. Bakery Products

- 13.2.1.1.1. Bread

- 13.2.1.1.2. Cakes & Pastries

- 13.2.1.1.3. Cookies & Biscuits

- 13.2.1.1.4. Gluten-free baked goods

- 13.2.1.1.5. Others

- 13.2.1.2. Confectionery

- 13.2.1.2.1. Candies

- 13.2.1.2.2. Chocolates

- 13.2.1.2.3. Gummies

- 13.2.1.2.4. Others

- 13.2.1.3. Dairy & Frozen Desserts

- 13.2.1.3.1. Ice cream

- 13.2.1.3.2. Yogurt

- 13.2.1.3.3. Puddings

- 13.2.1.3.4. Others

- 13.2.1.4. Sauces & Dressings

- 13.2.1.4.1. Mayonnaise

- 13.2.1.4.2. Ketchup

- 13.2.1.4.3. Salad dressings

- 13.2.1.4.4. Others

- 13.2.1.5. Soups & Gravies

- 13.2.1.6. Snacks & Convenience Foods

- 13.2.1.7. Baby Food

- 13.2.1.8. Beverages

- 13.2.1.8.1. Smoothies

- 13.2.1.8.2. Nutritional drinks

- 13.2.1.8.3. Others

- 13.2.1.9. Meat & Poultry Products

- 13.2.1.10. Pasta & Noodles

- 13.2.1.11. Others

- 13.2.1.1. Bakery Products

- 13.2.2. Pharmaceutical

- 13.2.2.1. Tablet Binding

- 13.2.2.2. Capsule Coating

- 13.2.2.3. Excipient Formulations

- 13.2.2.4. Controlled Release Systems

- 13.2.2.5. Disintegrants

- 13.2.2.6. Nutraceuticals

- 13.2.2.7. Others

- 13.2.3. Cosmetics & Personal Care

- 13.2.3.1. Skincare Products

- 13.2.3.1.1. Creams & Lotions

- 13.2.3.1.2. Face masks

- 13.2.3.1.3. Anti-aging products

- 13.2.3.1.4. Others

- 13.2.3.2. Haircare Products

- 13.2.3.2.1. Shampoos

- 13.2.3.2.2. Conditioners

- 13.2.3.2.3. Hair styling products

- 13.2.3.2.4. Others

- 13.2.3.3. Makeup Products

- 13.2.3.3.1. Foundation

- 13.2.3.3.2. Powder compacts

- 13.2.3.3.3. Others

- 13.2.3.4. Personal Hygiene Products

- 13.2.3.5. Others

- 13.2.3.1. Skincare Products

- 13.2.4. Animal Feed

- 13.2.4.1. Pet Food

- 13.2.4.2. Livestock Feed

- 13.2.4.3. Aquaculture Feed

- 13.2.4.4. Others

- 13.2.5. Paper & Textile

- 13.2.5.1. Paper Coating

- 13.2.5.2. Textile Sizing

- 13.2.5.3. Fabric Finishing

- 13.2.5.4. Others

- 13.2.6. Adhesives & Packaging

- 13.2.6.1. Bio-based Adhesives

- 13.2.6.2. Biodegradable Packaging Films

- 13.2.6.3. Coating Materials

- 13.2.6.4. Others

- 13.2.7. Chemical

- 13.2.7.1. Bio-plastics

- 13.2.7.2. Industrial Binders

- 13.2.7.3. Detergents

- 13.2.7.4. Others

- 13.2.8. Other Industries

- 13.2.1. Food & Beverage

- 14. Global Quinoa Starch Market Analysis and Forecasts, by Region

- 14.1. Key Findings

- 14.2. Quinoa Starch Market Size (Volume - Tons and Value - US$ Bn), Analysis, and Forecasts, by Region, 2021-2035

- 14.2.1. North America

- 14.2.2. Europe

- 14.2.3. Asia Pacific

- 14.2.4. Middle East

- 14.2.5. Africa

- 14.2.6. South America

- 15. North America Quinoa Starch Market Analysis

- 15.1. Key Segment Analysis

- 15.2. Regional Snapshot

- 15.3. North America Quinoa Starch Market Size (Volume - Tons and Value - US$ Bn), Analysis, and Forecasts, 2021-2035

- 15.3.1. Product Type

- 15.3.2. Form

- 15.3.3. Source/Variety

- 15.3.4. Extraction Method

- 15.3.5. Functionality

- 15.3.6. Distribution Channel

- 15.3.7. Packaging Type

- 15.3.8. End-use Industry

- 15.3.9. Country

- 15.3.9.1. USA

- 15.3.9.2. Canada

- 15.3.9.3. Mexico

- 15.4. USA Quinoa Starch Market

- 15.4.1. Country Segmental Analysis

- 15.4.2. Product Type

- 15.4.3. Form

- 15.4.4. Source/Variety

- 15.4.5. Extraction Method

- 15.4.6. Functionality

- 15.4.7. Distribution Channel

- 15.4.8. Packaging Type

- 15.4.9. End-use Industry

- 15.5. Canada Quinoa Starch Market

- 15.5.1. Country Segmental Analysis

- 15.5.2. Product Type

- 15.5.3. Form

- 15.5.4. Source/Variety

- 15.5.5. Extraction Method

- 15.5.6. Functionality

- 15.5.7. Distribution Channel

- 15.5.8. Packaging Type

- 15.5.9. End-use Industry

- 15.6. Mexico Quinoa Starch Market

- 15.6.1. Country Segmental Analysis

- 15.6.2. Product Type

- 15.6.3. Form

- 15.6.4. Source/Variety

- 15.6.5. Extraction Method

- 15.6.6. Functionality

- 15.6.7. Distribution Channel

- 15.6.8. Packaging Type

- 15.6.9. End-use Industry

- 16. Europe Quinoa Starch Market Analysis

- 16.1. Key Segment Analysis

- 16.2. Regional Snapshot

- 16.3. Europe Quinoa Starch Market Size (Volume - Tons and Value - US$ Bn), Analysis, and Forecasts, 2021-2035

- 16.3.1. Product Type

- 16.3.2. Form

- 16.3.3. Source/Variety

- 16.3.4. Extraction Method

- 16.3.5. Functionality

- 16.3.6. Distribution Channel

- 16.3.7. Packaging Type

- 16.3.8. End-use Industry

- 16.3.9. Country

- 16.3.9.1. Germany

- 16.3.9.2. United Kingdom

- 16.3.9.3. France

- 16.3.9.4. Italy

- 16.3.9.5. Spain

- 16.3.9.6. Netherlands

- 16.3.9.7. Nordic Countries

- 16.3.9.8. Poland

- 16.3.9.9. Russia & CIS

- 16.3.9.10. Rest of Europe

- 16.4. Germany Quinoa Starch Market

- 16.4.1. Country Segmental Analysis

- 16.4.2. Product Type

- 16.4.3. Form

- 16.4.4. Source/Variety

- 16.4.5. Extraction Method

- 16.4.6. Functionality

- 16.4.7. Distribution Channel

- 16.4.8. Packaging Type

- 16.4.9. End-use Industry

- 16.5. United Kingdom Quinoa Starch Market

- 16.5.1. Country Segmental Analysis

- 16.5.2. Product Type

- 16.5.3. Form

- 16.5.4. Source/Variety

- 16.5.5. Extraction Method

- 16.5.6. Functionality

- 16.5.7. Distribution Channel

- 16.5.8. Packaging Type

- 16.5.9. End-use Industry

- 16.6. France Quinoa Starch Market

- 16.6.1. Country Segmental Analysis

- 16.6.2. Product Type

- 16.6.3. Form

- 16.6.4. Source/Variety

- 16.6.5. Extraction Method

- 16.6.6. Functionality

- 16.6.7. Distribution Channel

- 16.6.8. Packaging Type

- 16.6.9. End-use Industry

- 16.7. Italy Quinoa Starch Market

- 16.7.1. Country Segmental Analysis

- 16.7.2. Product Type

- 16.7.3. Form

- 16.7.4. Source/Variety

- 16.7.5. Extraction Method

- 16.7.6. Functionality

- 16.7.7. Distribution Channel

- 16.7.8. Packaging Type

- 16.7.9. End-use Industry

- 16.8. Spain Quinoa Starch Market

- 16.8.1. Country Segmental Analysis

- 16.8.2. Product Type

- 16.8.3. Form

- 16.8.4. Source/Variety

- 16.8.5. Extraction Method

- 16.8.6. Functionality

- 16.8.7. Distribution Channel

- 16.8.8. Packaging Type

- 16.8.9. End-use Industry

- 16.9. Netherlands Quinoa Starch Market

- 16.9.1. Country Segmental Analysis

- 16.9.2. Product Type

- 16.9.3. Form

- 16.9.4. Source/Variety

- 16.9.5. Extraction Method

- 16.9.6. Functionality

- 16.9.7. Distribution Channel

- 16.9.8. Packaging Type

- 16.9.9. End-use Industry

- 16.10. Nordic Countries Quinoa Starch Market

- 16.10.1. Country Segmental Analysis

- 16.10.2. Product Type

- 16.10.3. Form

- 16.10.4. Source/Variety

- 16.10.5. Extraction Method

- 16.10.6. Functionality

- 16.10.7. Distribution Channel

- 16.10.8. Packaging Type

- 16.10.9. End-use Industry

- 16.11. Poland Quinoa Starch Market

- 16.11.1. Country Segmental Analysis

- 16.11.2. Product Type

- 16.11.3. Form

- 16.11.4. Source/Variety

- 16.11.5. Extraction Method

- 16.11.6. Functionality

- 16.11.7. Distribution Channel

- 16.11.8. Packaging Type

- 16.11.9. End-use Industry

- 16.12. Russia & CIS Quinoa Starch Market

- 16.12.1. Country Segmental Analysis

- 16.12.2. Product Type

- 16.12.3. Form

- 16.12.4. Source/Variety

- 16.12.5. Extraction Method

- 16.12.6. Functionality

- 16.12.7. Distribution Channel

- 16.12.8. Packaging Type

- 16.12.9. End-use Industry

- 16.13. Rest of Europe Quinoa Starch Market

- 16.13.1. Country Segmental Analysis

- 16.13.2. Product Type

- 16.13.3. Form

- 16.13.4. Source/Variety

- 16.13.5. Extraction Method

- 16.13.6. Functionality

- 16.13.7. Distribution Channel

- 16.13.8. Packaging Type

- 16.13.9. End-use Industry

- 17. Asia Pacific Quinoa Starch Market Analysis

- 17.1. Key Segment Analysis

- 17.2. Regional Snapshot

- 17.3. Asia Pacific Quinoa Starch Market Size (Volume - Tons and Value - US$ Bn), Analysis, and Forecasts, 2021-2035

- 17.3.1. Product Type

- 17.3.2. Form

- 17.3.3. Source/Variety

- 17.3.4. Extraction Method

- 17.3.5. Functionality

- 17.3.6. Distribution Channel

- 17.3.7. Packaging Type

- 17.3.8. End-use Industry

- 17.3.9. Country

- 17.3.9.1. China

- 17.3.9.2. India

- 17.3.9.3. Japan

- 17.3.9.4. South Korea

- 17.3.9.5. Australia and New Zealand

- 17.3.9.6. Indonesia

- 17.3.9.7. Malaysia

- 17.3.9.8. Thailand

- 17.3.9.9. Vietnam

- 17.3.9.10. Rest of Asia Pacific

- 17.4. China Quinoa Starch Market

- 17.4.1. Country Segmental Analysis

- 17.4.2. Product Type

- 17.4.3. Form

- 17.4.4. Source/Variety

- 17.4.5. Extraction Method

- 17.4.6. Functionality

- 17.4.7. Distribution Channel

- 17.4.8. Packaging Type

- 17.4.9. End-use Industry

- 17.5. India Quinoa Starch Market

- 17.5.1. Country Segmental Analysis

- 17.5.2. Product Type

- 17.5.3. Form

- 17.5.4. Source/Variety

- 17.5.5. Extraction Method

- 17.5.6. Functionality

- 17.5.7. Distribution Channel

- 17.5.8. Packaging Type

- 17.5.9. End-use Industry

- 17.6. Japan Quinoa Starch Market

- 17.6.1. Country Segmental Analysis

- 17.6.2. Product Type

- 17.6.3. Form

- 17.6.4. Source/Variety

- 17.6.5. Extraction Method

- 17.6.6. Functionality

- 17.6.7. Distribution Channel

- 17.6.8. Packaging Type

- 17.6.9. End-use Industry

- 17.7. South Korea Quinoa Starch Market

- 17.7.1. Country Segmental Analysis

- 17.7.2. Product Type

- 17.7.3. Form

- 17.7.4. Source/Variety

- 17.7.5. Extraction Method

- 17.7.6. Functionality

- 17.7.7. Distribution Channel

- 17.7.8. Packaging Type

- 17.7.9. End-use Industry

- 17.8. Australia and New Zealand Quinoa Starch Market

- 17.8.1. Country Segmental Analysis

- 17.8.2. Product Type

- 17.8.3. Form

- 17.8.4. Source/Variety

- 17.8.5. Extraction Method

- 17.8.6. Functionality

- 17.8.7. Distribution Channel

- 17.8.8. Packaging Type

- 17.8.9. End-use Industry

- 17.9. Indonesia Quinoa Starch Market

- 17.9.1. Country Segmental Analysis

- 17.9.2. Product Type

- 17.9.3. Form

- 17.9.4. Source/Variety

- 17.9.5. Extraction Method

- 17.9.6. Functionality

- 17.9.7. Distribution Channel

- 17.9.8. Packaging Type

- 17.9.9. End-use Industry

- 17.10. Malaysia Quinoa Starch Market

- 17.10.1. Country Segmental Analysis

- 17.10.2. Product Type

- 17.10.3. Form

- 17.10.4. Source/Variety

- 17.10.5. Extraction Method

- 17.10.6. Functionality

- 17.10.7. Distribution Channel

- 17.10.8. Packaging Type

- 17.10.9. End-use Industry

- 17.11. Thailand Quinoa Starch Market

- 17.11.1. Country Segmental Analysis

- 17.11.2. Product Type

- 17.11.3. Form

- 17.11.4. Source/Variety

- 17.11.5. Extraction Method

- 17.11.6. Functionality

- 17.11.7. Distribution Channel

- 17.11.8. Packaging Type

- 17.11.9. End-use Industry

- 17.12. Vietnam Quinoa Starch Market

- 17.12.1. Country Segmental Analysis

- 17.12.2. Product Type

- 17.12.3. Form

- 17.12.4. Source/Variety

- 17.12.5. Extraction Method

- 17.12.6. Functionality

- 17.12.7. Distribution Channel

- 17.12.8. Packaging Type

- 17.12.9. End-use Industry

- 17.13. Rest of Asia Pacific Quinoa Starch Market

- 17.13.1. Country Segmental Analysis

- 17.13.2. Product Type

- 17.13.3. Form

- 17.13.4. Source/Variety

- 17.13.5. Extraction Method

- 17.13.6. Functionality

- 17.13.7. Distribution Channel

- 17.13.8. Packaging Type

- 17.13.9. End-use Industry

- 18. Middle East Quinoa Starch Market Analysis

- 18.1. Key Segment Analysis

- 18.2. Regional Snapshot

- 18.3. Middle East Quinoa Starch Market Size (Volume - Tons and Value - US$ Bn), Analysis, and Forecasts, 2021-2035

- 18.3.1. Product Type

- 18.3.2. Form

- 18.3.3. Source/Variety

- 18.3.4. Extraction Method

- 18.3.5. Functionality

- 18.3.6. Distribution Channel

- 18.3.7. Packaging Type

- 18.3.8. End-use Industry

- 18.3.9. Country

- 18.3.9.1. Turkey

- 18.3.9.2. UAE

- 18.3.9.3. Saudi Arabia

- 18.3.9.4. Israel

- 18.3.9.5. Rest of Middle East

- 18.4. Turkey Quinoa Starch Market

- 18.4.1. Country Segmental Analysis

- 18.4.2. Product Type

- 18.4.3. Form

- 18.4.4. Source/Variety

- 18.4.5. Extraction Method

- 18.4.6. Functionality

- 18.4.7. Distribution Channel

- 18.4.8. Packaging Type

- 18.4.9. End-use Industry

- 18.5. UAE Quinoa Starch Market

- 18.5.1. Country Segmental Analysis

- 18.5.2. Product Type

- 18.5.3. Form

- 18.5.4. Source/Variety

- 18.5.5. Extraction Method

- 18.5.6. Functionality

- 18.5.7. Distribution Channel

- 18.5.8. Packaging Type

- 18.5.9. End-use Industry

- 18.6. Saudi Arabia Quinoa Starch Market

- 18.6.1. Country Segmental Analysis

- 18.6.2. Product Type

- 18.6.3. Form

- 18.6.4. Source/Variety

- 18.6.5. Extraction Method

- 18.6.6. Functionality

- 18.6.7. Distribution Channel

- 18.6.8. Packaging Type

- 18.6.9. End-use Industry

- 18.7. Israel Quinoa Starch Market

- 18.7.1. Country Segmental Analysis

- 18.7.2. Product Type

- 18.7.3. Form

- 18.7.4. Source/Variety

- 18.7.5. Extraction Method

- 18.7.6. Functionality

- 18.7.7. Distribution Channel

- 18.7.8. Packaging Type

- 18.7.9. End-use Industry

- 18.8. Rest of Middle East Quinoa Starch Market

- 18.8.1. Country Segmental Analysis

- 18.8.2. Product Type

- 18.8.3. Form

- 18.8.4. Source/Variety

- 18.8.5. Extraction Method

- 18.8.6. Functionality

- 18.8.7. Distribution Channel

- 18.8.8. Packaging Type

- 18.8.9. End-use Industry

- 19. Africa Quinoa Starch Market Analysis

- 19.1. Key Segment Analysis

- 19.2. Regional Snapshot

- 19.3. Africa Quinoa Starch Market Size (Volume - Tons and Value - US$ Bn), Analysis, and Forecasts, 2021-2035

- 19.3.1. Product Type

- 19.3.2. Form

- 19.3.3. Source/Variety

- 19.3.4. Extraction Method

- 19.3.5. Functionality

- 19.3.6. Distribution Channel

- 19.3.7. Packaging Type

- 19.3.8. End-use Industry

- 19.3.9. Country

- 19.3.9.1. South Africa

- 19.3.9.2. Egypt

- 19.3.9.3. Nigeria

- 19.3.9.4. Algeria

- 19.3.9.5. Rest of Africa

- 19.4. South Africa Quinoa Starch Market

- 19.4.1. Country Segmental Analysis

- 19.4.2. Product Type

- 19.4.3. Form

- 19.4.4. Source/Variety

- 19.4.5. Extraction Method

- 19.4.6. Functionality

- 19.4.7. Distribution Channel

- 19.4.8. Packaging Type

- 19.4.9. End-use Industry

- 19.5. Egypt Quinoa Starch Market

- 19.5.1. Country Segmental Analysis

- 19.5.2. Product Type

- 19.5.3. Form

- 19.5.4. Source/Variety

- 19.5.5. Extraction Method

- 19.5.6. Functionality

- 19.5.7. Distribution Channel

- 19.5.8. Packaging Type

- 19.5.9. End-use Industry

- 19.6. Nigeria Quinoa Starch Market

- 19.6.1. Country Segmental Analysis

- 19.6.2. Product Type

- 19.6.3. Form

- 19.6.4. Source/Variety

- 19.6.5. Extraction Method

- 19.6.6. Functionality

- 19.6.7. Distribution Channel

- 19.6.8. Packaging Type

- 19.6.9. End-use Industry

- 19.7. Algeria Quinoa Starch Market

- 19.7.1. Country Segmental Analysis

- 19.7.2. Product Type

- 19.7.3. Form

- 19.7.4. Source/Variety

- 19.7.5. Extraction Method

- 19.7.6. Functionality

- 19.7.7. Distribution Channel

- 19.7.8. Packaging Type

- 19.7.9. End-use Industry

- 19.8. Rest of Africa Quinoa Starch Market

- 19.8.1. Country Segmental Analysis

- 19.8.2. Product Type

- 19.8.3. Form

- 19.8.4. Source/Variety

- 19.8.5. Extraction Method

- 19.8.6. Functionality

- 19.8.7. Distribution Channel

- 19.8.8. Packaging Type

- 19.8.9. End-use Industry

- 20. South America Quinoa Starch Market Analysis

- 20.1. Key Segment Analysis

- 20.2. Regional Snapshot

- 20.3. South America Quinoa Starch Market Size (Volume - Tons and Value - US$ Bn), Analysis, and Forecasts, 2021-2035

- 20.3.1. Product Type

- 20.3.2. Form

- 20.3.3. Source/Variety

- 20.3.4. Extraction Method

- 20.3.5. Functionality

- 20.3.6. Distribution Channel

- 20.3.7. Packaging Type

- 20.3.8. End-use Industry

- 20.3.9. Country

- 20.3.9.1. Brazil

- 20.3.9.2. Argentina

- 20.3.9.3. Rest of South America

- 20.4. Brazil Quinoa Starch Market

- 20.4.1. Country Segmental Analysis

- 20.4.2. Product Type

- 20.4.3. Form

- 20.4.4. Source/Variety

- 20.4.5. Extraction Method

- 20.4.6. Functionality

- 20.4.7. Distribution Channel

- 20.4.8. Packaging Type

- 20.4.9. End-use Industry

- 20.5. Argentina Quinoa Starch Market

- 20.5.1. Country Segmental Analysis

- 20.5.2. Product Type

- 20.5.3. Form

- 20.5.4. Source/Variety

- 20.5.5. Extraction Method

- 20.5.6. Functionality

- 20.5.7. Distribution Channel

- 20.5.8. Packaging Type

- 20.5.9. End-use Industry

- 20.6. Rest of South America Quinoa Starch Market

- 20.6.1. Country Segmental Analysis

- 20.6.2. Product Type

- 20.6.3. Form

- 20.6.4. Source/Variety

- 20.6.5. Extraction Method

- 20.6.6. Functionality

- 20.6.7. Distribution Channel

- 20.6.8. Packaging Type

- 20.6.9. End-use Industry

- 21. Key Players/ Company Profile

- 21.1. Alter Eco

- 21.1.1. Company Details/ Overview

- 21.1.2. Company Financials

- 21.1.3. Key Customers and Competitors

- 21.1.4. Business/ Industry Portfolio

- 21.1.5. Product Portfolio/ Specification Details

- 21.1.6. Pricing Data

- 21.1.7. Strategic Overview

- 21.1.8. Recent Developments

- 21.2. Ancient Harvest

- 21.3. Andean Naturals

- 21.4. Archer Daniels Midland Company (ADM)

- 21.5. Arrowhead Mills

- 21.6. Beneo GmbH

- 21.7. Bob's Red Mill Natural Foods

- 21.8. Cargill Incorporated

- 21.9. Ingredion Incorporated

- 21.10. Irupana Andean Organic Food

- 21.11. King Arthur Baking Company

- 21.12. Lundberg Family Farms

- 21.13. Nature's Path Foods

- 21.14. Hodmedod's British Pulses & Grains

- 21.15. Northern Quinoa Production Corporation

- 21.16. Quinoa Corporation

- 21.17. Roquette Frères

- 21.18. Shiloh Farms

- 21.19. Tate & Lyle PLC

- 21.20. The British Quinoa Company

- 21.21. Other Key Players

- 21.1. Alter Eco

Note* - This is just tentative list of players. While providing the report, we will cover more number of players based on their revenue and share for each geography

Research Design

Our research design integrates both demand-side and supply-side analysis through a balanced combination of primary and secondary research methodologies. By utilizing both bottom-up and top-down approaches alongside rigorous data triangulation methods, we deliver robust market intelligence that supports strategic decision-making.

MarketGenics' comprehensive research design framework ensures the delivery of accurate, reliable, and actionable market intelligence. Through the integration of multiple research approaches, rigorous validation processes, and expert analysis, we provide our clients with the insights needed to make informed strategic decisions and capitalize on market opportunities.

MarketGenics leverages a dedicated industry panel of experts and a comprehensive suite of paid databases to effectively collect, consolidate, and analyze market intelligence.

Our approach has consistently proven to be reliable and effective in generating accurate market insights, identifying key industry trends, and uncovering emerging business opportunities.

Through both primary and secondary research, we capture and analyze critical company-level data such as manufacturing footprints, including technical centers, R&D facilities, sales offices, and headquarters.

Our expert panel further enhances our ability to estimate market size for specific brands based on validated field-level intelligence.

Our data mining techniques incorporate both parametric and non-parametric methods, allowing for structured data collection, sorting, processing, and cleaning.

Demand projections are derived from large-scale data sets analyzed through proprietary algorithms, culminating in robust and reliable market sizing.

Research Approach

The bottom-up approach builds market estimates by starting with the smallest addressable market units and systematically aggregating them to create comprehensive market size projections.

This method begins with specific, granular data points and builds upward to create the complete market landscape.

Customer Analysis → Segmental Analysis → Geographical Analysis

The top-down approach starts with the broadest possible market data and systematically narrows it down through a series of filters and assumptions to arrive at specific market segments or opportunities.

This method begins with the big picture and works downward to increasingly specific market slices.

TAM → SAM → SOM

Research Methods

Desk / Secondary Research

While analysing the market, we extensively study secondary sources, directories, and databases to identify and collect information useful for this technical, market-oriented, and commercial report. Secondary sources that we utilize are not only the public sources, but it is a combination of Open Source, Associations, Paid Databases, MG Repository & Knowledgebase, and others.

- Company websites, annual reports, financial reports, broker reports, and investor presentations

- National government documents, statistical databases and reports

- News articles, press releases and web-casts specific to the companies operating in the market, Magazines, reports, and others

- We gather information from commercial data sources for deriving company specific data such as segmental revenue, share for geography, product revenue, and others

- Internal and external proprietary databases (industry-specific), relevant patent, and regulatory databases

- Governing Bodies, Government Organizations

- Relevant Authorities, Country-specific Associations for Industries

We also employ the model mapping approach to estimate the product level market data through the players' product portfolio

Primary Research

Primary research/ interviews is vital in analyzing the market. Most of the cases involves paid primary interviews. Primary sources include primary interviews through e-mail interactions, telephonic interviews, surveys as well as face-to-face interviews with the different stakeholders across the value chain including several industry experts.

| Type of Respondents | Number of Primaries |

|---|---|

| Tier 2/3 Suppliers | ~20 |

| Tier 1 Suppliers | ~25 |

| End-users | ~25 |

| Industry Expert/ Panel/ Consultant | ~30 |

| Total | ~100 |

MG Knowledgebase

• Repository of industry blog, newsletter and case studies

• Online platform covering detailed market reports, and company profiles

Forecasting Factors and Models

Forecasting Factors

- Historical Trends – Past market patterns, cycles, and major events that shaped how markets behave over time. Understanding past trends helps predict future behavior.

- Industry Factors – Specific characteristics of the industry like structure, regulations, and innovation cycles that affect market dynamics.

- Macroeconomic Factors – Economic conditions like GDP growth, inflation, and employment rates that affect how much money people have to spend.

- Demographic Factors – Population characteristics like age, income, and location that determine who can buy your product.

- Technology Factors – How quickly people adopt new technology and how much technology infrastructure exists.

- Regulatory Factors – Government rules, laws, and policies that can help or restrict market growth.

- Competitive Factors – Analyzing competition structure such as degree of competition and bargaining power of buyers and suppliers.

Forecasting Models / Techniques

Multiple Regression Analysis

- Identify and quantify factors that drive market changes

- Statistical modeling to establish relationships between market drivers and outcomes

Time Series Analysis – Seasonal Patterns

- Understand regular cyclical patterns in market demand

- Advanced statistical techniques to separate trend, seasonal, and irregular components

Time Series Analysis – Trend Analysis

- Identify underlying market growth patterns and momentum

- Statistical analysis of historical data to project future trends

Expert Opinion – Expert Interviews

- Gather deep industry insights and contextual understanding

- In-depth interviews with key industry stakeholders

Multi-Scenario Development

- Prepare for uncertainty by modeling different possible futures

- Creating optimistic, pessimistic, and most likely scenarios

Time Series Analysis – Moving Averages

- Sophisticated forecasting for complex time series data

- Auto-regressive integrated moving average models with seasonal components

Econometric Models

- Apply economic theory to market forecasting

- Sophisticated economic models that account for market interactions

Expert Opinion – Delphi Method

- Harness collective wisdom of industry experts

- Structured, multi-round expert consultation process

Monte Carlo Simulation

- Quantify uncertainty and probability distributions

- Thousands of simulations with varying input parameters

Research Analysis

Our research framework is built upon the fundamental principle of validating market intelligence from both demand and supply perspectives. This dual-sided approach ensures comprehensive market understanding and reduces the risk of single-source bias.

Demand-Side Analysis: We understand end-user/application behavior, preferences, and market needs along with the penetration of the product for specific application.

Supply-Side Analysis: We estimate overall market revenue, analyze the segmental share along with industry capacity, competitive landscape, and market structure.

Validation & Evaluation

Data triangulation is a validation technique that uses multiple methods, sources, or perspectives to examine the same research question, thereby increasing the credibility and reliability of research findings. In market research, triangulation serves as a quality assurance mechanism that helps identify and minimize bias, validate assumptions, and ensure accuracy in market estimates.

- Data Source Triangulation – Using multiple data sources to examine the same phenomenon

- Methodological Triangulation – Using multiple research methods to study the same research question

- Investigator Triangulation – Using multiple researchers or analysts to examine the same data

- Theoretical Triangulation – Using multiple theoretical perspectives to interpret the same data

Custom Market Research Services

We will customise the research for you, in case the report listed above does not meet your requirements.

Get 10% Free Customisation