Vertical Farming Market Size, Share & Trends Analysis Report by Component (Lighting Systems, Climate Control Systems, Irrigation & Fertigation Systems, Sensors & Monitoring Systems, Software & Control Platforms, Structural Components, Others), Growing Mechanism, Structure Type, Crop Type, Lighting Type, Growth Medium, Farm Size, End User, Distribution Channel, and Geography (North America, Europe, Asia Pacific, Middle East, Africa, and South America) – Global Industry Data, Trends, and Forecasts, 2026–2035

Market Overview:

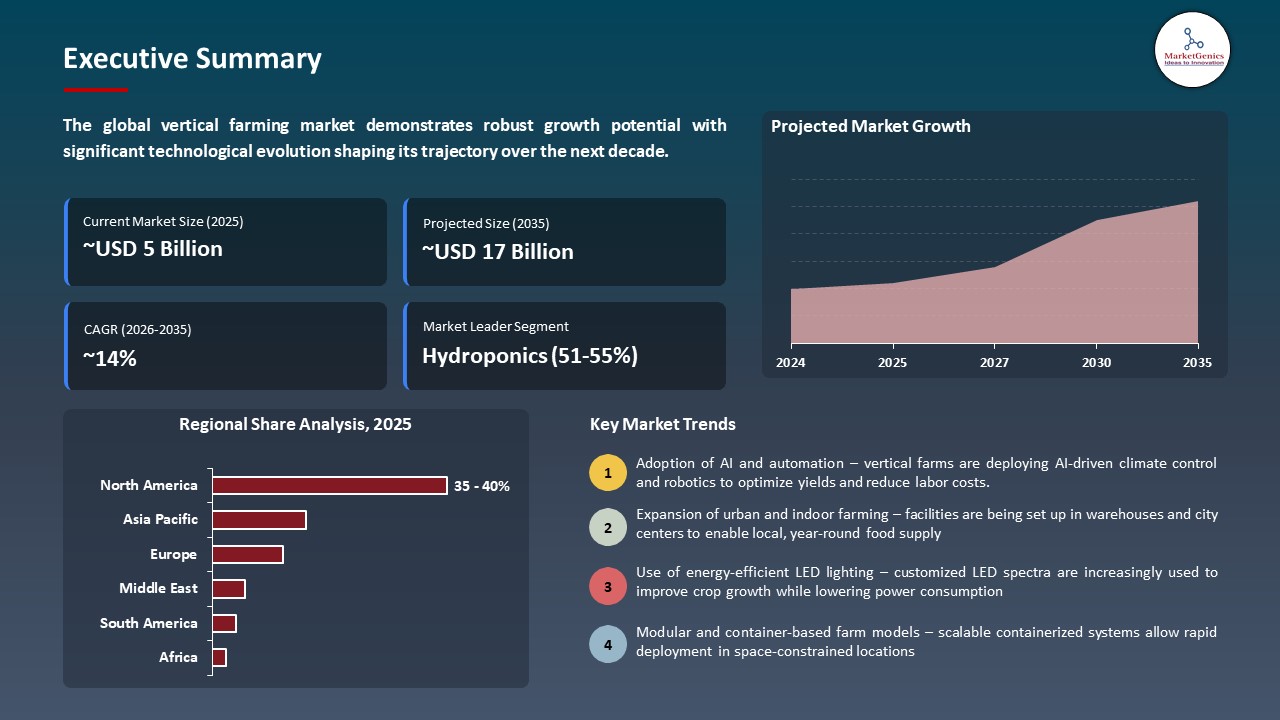

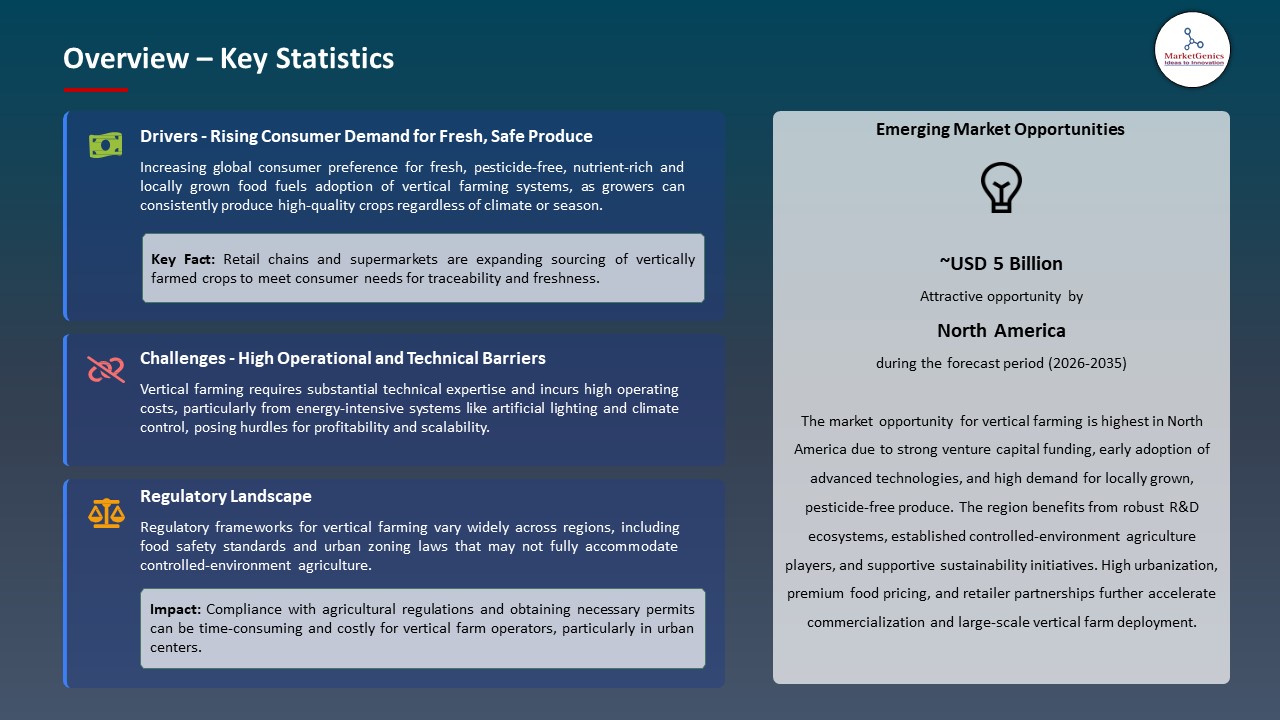

According to MarketGenics analysis only, the global vertical farming market is witnessing strong growth, with an estimated valuation of USD 4.5 billion in 2025 and projected to reach USD 17.2 billion by 2035, expanding at a CAGR of 14.3% during the forecast period.

|

|

|

Segmental Data Insights |

|

|

Demand Trends |

|

|

Competitive Landscape |

|

|

Strategic Development |

|

|

Future Outlook & Opportunities |

|

Vertical Farming market Size, Share, and Growth

AI-driven automation, adaptive sensor networks, and real-time data analytics are becoming major defining traits of the vertical-farming-market, allowing it to accurately monitor the development of plants, optimize the utilization of water, nutrients, and energy, and adapt to the modification of environmental conditions fast.

Rick Langille, CEO of Harvest Today, said, We are proud to bring the ‘Harvest Wall’ to Southeast Asia with Agroz. Our goal is to demonstrate that vertical farming can thrive in tropical markets when you apply practical thinking and solid designs.

The vertical-farming-market is currently undergoing a change with the increasing demand of urban food supplies, climatic uncertainty and land scarcity, turning the world more towards fully controlled, technology-oriented cultivation system. Vertical farms are becoming increasingly structured as data-driven production systems, in which artificial intelligence, automation, and sensor-mediated controls can allow them to maintain consistent crop yields, use fewer resources, and operate reliably without being influenced by the external climate.

State-of-the-art vertical farming systems combine AI-controlled LED light lamps, climate control, real-time nutrient dose, and IoT-based environmental monitoring to accurately control growth parameters on a plant level. Temperature, humidity, CO 2, and nutrient sensors continuously stream their data to be processed using cloud and edge analytics to optimize plant growth cycles, predict yields more accurately, and consume less energy and water. Machine learning models are also used to predict when a harvest will occur, early detection of plant stress and enhance crop consistency among stacked growing systems.

The adjacent opportunities in the vertical farming market are robotic seeding and harvesting, autonomous material handling, model of a digital twin farm, and direct connection to urban retail and foodservice supply chains. These inventions make it more scalable, reduce variability of operations and make it more sustainable. With the uptake of modular farm architecture and interoperable software platform, vertical farming is beginning to be a vital answer to resilient, high-efficiency and sustainable food production on global scale.

Vertical Farming market Dynamics and Trends

Vertical Farming market Dynamics and Trends

Driver: Rising Demand for Year-Round Crop Production

-

The fast urbanization of population, climatic changes, and land degradation are placing an increase on the need to produce food on a dependable basis throughout the year, which is prompting the use of vertical farm systems, which produce food all through the year and are not affected by seasonal and climatic shifts.

- Technologically advanced vertical farming processes allow uninterrupted crop growth via AI-controlled climate, controlled LED-based lighting, and automated nutrient delivery, so there is predictable harvesting and consistent supply to retailers. For instance, in 2025, Gotham Greens will grow its climate-controlled vertical farms in North America to supply continuous production of leafy greens throughout the year with automated growing systems.

- Vertical farming technologies will improve crop reliability, operational efficiency, and supply chain resilience enabling producers to supply year-round food demand at a limited land use and reducing production variability.

Restraint: High Initial Capital and Operational Costs

-

The aggressive aspect of the deployment of advanced Vertical Farming solutions is also on the list of the major constraints since the AI-driven farm equipment, IoT sensor networks, edge computers, and embedded software platforms are significantly more expensive to invest in capital than conventional farming equipment.

- The recurring costs are the subscription to data analytics, cloud storage, software updates, and operator training which add to the financial taxing burden. Indicatively, the cost of autonomous machinery and IoT sensors finished in a farm can run millions of dollars annually, thereby limiting the use of autonomous technology to large agribusinesses.

- Rural connectivity is poor, specialized technical services, and infrastructure are also deterrents to large scale implementation, especially in the developing markets.

Opportunity: Integration of IoT and Data Analytics

-

The growth of internet of things based sensors, cloud-based monitoring and AI based analytics platforms are fostering great prospects in international vertical farming market through the provision of real time monitoring of crops, predictive yield management and effective management of resources.

- Developed analytics enable decision-making at the field level that works with machine learning and predictive intelligence to enhance water, nutrient and energy efficiency and reduce crop losses.

- The integration of IoT and data analytics is another factor that is facilitating quicker decisions, scalable implementation across farms of any size, and greater profitability in the operational aspects of vertical farming, which is why it is a key growth opportunity in the industry worldwide.

Key Trend: Adoption of Modular and Automated Systems

-

Global vertical farming market is experiencing a great opportunity due to the emergence of robotic planting systems, automated nutrient delivery systems, and IoT-based climate control systems which provide opportunities to manage crop in real-time, use resources economically, and optimally and increase the efficiency of the work.

- Automation platforms are being adapted to enable predictive decisions, adjustment of lighting and irrigation dynamically and the health of crop to be monitored remotely. For instance, in August 2025, Plenty Unlimited deployed a modular robot growth rack system with AI sensors to allow modern urban farms to autonomously make nutrient and climate changes.

- Having automated and modular systems is increasing scalability, decreasing labor reliance, and increasing profitability, making it a major growth trend in the global vertical farming market.

Vertical Farming Market Analysis and Segmental Data

Vertical Farming Market Analysis and Segmental Data

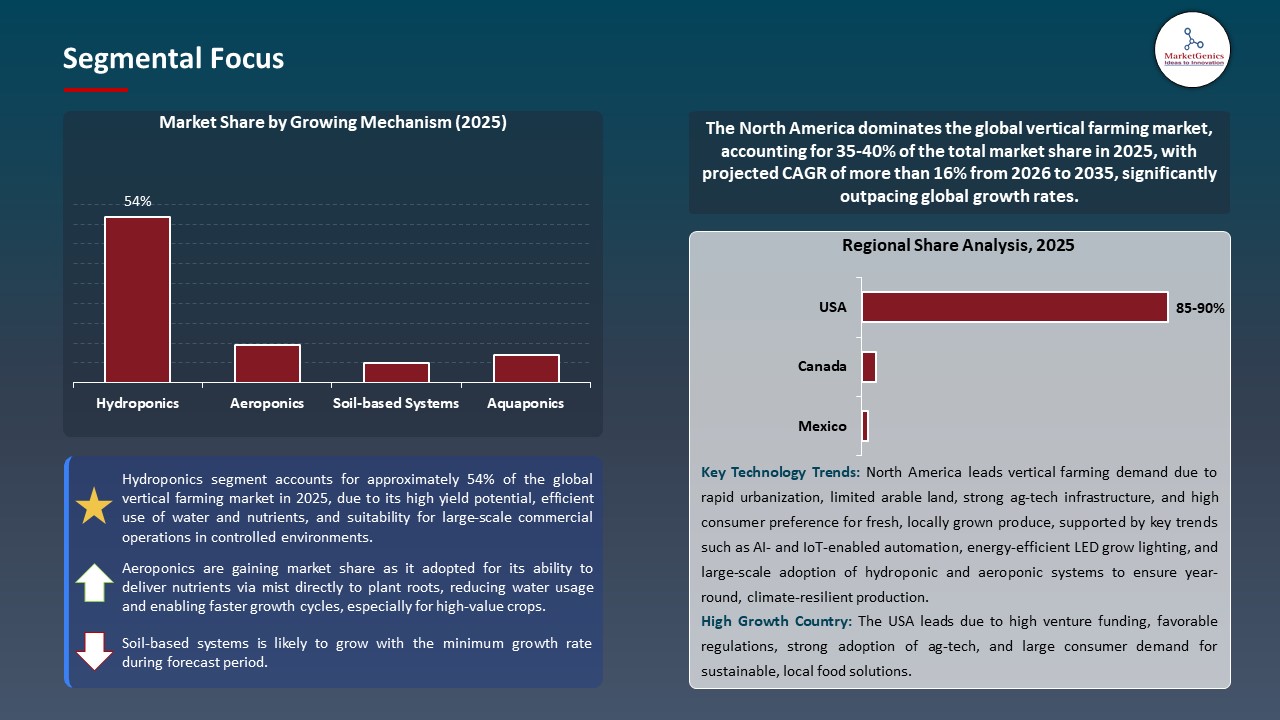

Hydroponics Dominate Global Vertical Farming Market

-

Agritech companies, lighting companies, and online applications are expanding the market of vertical farming by implementing AI-based integration of hydroponics, IoT-connected nutrient sensors, automated climate regulators, and cloud-based crop managers to increase the plant growth, efficiency, and resource utilization.

- Features like platform interoperability and modular systems help to improve performance by providing real-time data exchange, AI-controlled nutrient and water, and predictive analytics. For instance, in June 2025, AeroFarms installed a hydroponic growth facility using the IoT and AI climate control, cutting water use by 35 percent and able to predict the yield.

- The modular hydroponic systems allow more rapid upgrades, internationalisation, and robotics, LED lighting and precision irrigation, which makes hydroponics the optimal solution to vertical farms.

North America Leads Global Vertical Farming Market Demand

-

North America leads the global vertical farming market with U.S. and Canadian agritech innovators and city planners hastening the installation of modular indoor farms, IoT-enabled environmental management, and AI-guided growth optimization systems to increase production throughout the year, local food security, and sustainable supply chains.

- The market activity has been boosted with strategic alliances creating diffusion of technology. For instance, in February 2025, Just Vertical established strategic alliances with NuLeaf Farms to roll out full-scale indoor farming systems in both urban and rural communities in Canada and the United States, integrating advanced grow rack systems with IoT automation of climate, nutrient and lighting.

- Strong investments and supporting by the government and business have resulted in a large vertical farming market in North America, and hydroponic and building-based farms are quickly expanding.

Vertical Farming Market Ecosystem

The global vertical farming market is moderately consolidated, and the rivalry is directed at aeroponic and hydroponic systems, automation, AI-based crop data gathering, and network integration with retail and supply chains. The availability of AeroFarms, Bowery Farming, Plenty Unlimited, Crop One Holdings, and Kalera have a significant market share comprising of the provision of end-to-end vertical farming offers that imply climate-controlled farm structures, crop intelligence that is sensor-based, plant and harvesting automation, and predictive crop management.

These firms focus on high-value and specialized vertical farming solutions that ensure technological leadership. AeroFarms is working on advancing aeroponic farms, data-driven growth control, and sustainable resource management; Bowery Farming is working on robots, IoT sensors, and bespoke BoweryOS software to optimize crops precisely and urban-friendly hydroponic farms. Plenty Unlimited is working on scalable hydroponic farms with automated nutrient control, on-demand farm-to-fork delivery, and modular farm design; Crop One Holdings is working on urban architecturally friendly hydroponic farms; and Kalera is working on fully automated, scal

Government programs in the field of sustainable agriculture, urban food production and the introduction of smart farms, as well as cooperation with technology distributors and research institutions, have boosted the introduction of innovations of vertical farming systems, precision agriculture, and resource-saving methods. These ecosystem processes generate competitive differentiation, can be easily implemented with advanced solutions, and can help the global Vertical Farming market to pursue the escalating urban food need, resource-efficiency objectives, and sustainable agricultural output requirements.

Recent Development and Strategic Overview

Recent Development and Strategic Overview

- In October 2025, Agroz Inc., a Malaysia‑based AgTech company, announced a strategic collaboration with U.S.‑based Harvest Today to launch the Agroz Groz Wall, a scalable vertical farming system featuring Harvest Today’s patented Harvest Wall technology.

- In July 2025, Water Ways Technologies, a Canadian smart agriculture and irrigation solutions provider, entered a strategic partnership with Israeli crop developer BF AGRITECH to create a proprietary tomato hybrid specifically for vertical farming systems.

Report Scope

|

Detail |

|

|

Market Size in 2025 |

USD 4.5 Bn |

|

Market Forecast Value in 2035 |

USD 17.2 Bn |

|

Growth Rate (CAGR) |

14.3% |

|

Forecast Period |

2026 – 2035 |

|

Historical Data Available for |

2021 – 2024 |

|

Market Size Units |

US$ Billion for Value |

|

Report Format |

Electronic (PDF) + Excel |

|

North America |

Europe |

Asia Pacific |

Middle East |

Africa |

South America |

|

|

|

|

|

|

|

Companies Covered |

|||||

|

|

|

|

|

|

Vertical Farming Market Segmentation and Highlights

|

Segment |

Sub-segment |

|

Vertical Farming Market, By Component |

|

|

Vertical Farming Market, By Growing Mechanism |

|

|

Vertical Farming Market, By Structure Type |

|

|

Vertical Farming Market, By Crop Type |

|

|

Vertical Farming Market, By Lighting Type |

|

|

Vertical Farming Market, By Growth Medium |

|

|

Vertical Farming Market, By Farm Size |

|

|

Vertical Farming Market, By End User |

|

|

Vertical Farming Market, By Distribution Channel |

|

Frequently Asked Questions

Table of Contents

- 1. Research Methodology and Assumptions

- 1.1. Definitions

- 1.2. Research Design and Approach

- 1.3. Data Collection Methods

- 1.4. Base Estimates and Calculations

- 1.5. Forecasting Models

- 1.5.1. Key Forecast Factors & Impact Analysis

- 1.6. Secondary Research

- 1.6.1. Open Sources

- 1.6.2. Paid Databases

- 1.6.3. Associations

- 1.7. Primary Research

- 1.7.1. Primary Sources

- 1.7.2. Primary Interviews with Stakeholders across Ecosystem

- 2. Executive Summary

- 2.1. Global Vertical Farming Market Outlook

- 2.1.1. Vertical Farming Market Size (Value - US$ Bn), and Forecasts, 2021-2035

- 2.1.2. Compounded Annual Growth Rate Analysis

- 2.1.3. Growth Opportunity Analysis

- 2.1.4. Segmental Share Analysis

- 2.1.5. Geographical Share Analysis

- 2.2. Market Analysis and Facts

- 2.3. Supply-Demand Analysis

- 2.4. Competitive Benchmarking

- 2.5. Go-to- Market Strategy

- 2.5.1. Customer/ End-use Industry Assessment

- 2.5.2. Growth Opportunity Data, 2026-2035

- 2.5.2.1. Regional Data

- 2.5.2.2. Country Data

- 2.5.2.3. Segmental Data

- 2.5.3. Identification of Potential Market Spaces

- 2.5.4. GAP Analysis

- 2.5.5. Potential Attractive Price Points

- 2.5.6. Prevailing Market Risks & Challenges

- 2.5.7. Preferred Sales & Marketing Strategies

- 2.5.8. Key Recommendations and Analysis

- 2.5.9. A Way Forward

- 2.1. Global Vertical Farming Market Outlook

- 3. Industry Data and Premium Insights

- 3.1. Global Agriculture Industry Overview, 2025

- 3.1.1. Agriculture Industry Ecosystem Analysis

- 3.1.2. Key Trends for Agriculture Industry

- 3.1.3. Regional Distribution for Agriculture Industry

- 3.2. Supplier Customer Data

- 3.3. Technology Roadmap and Developments

- 3.4. Trade Analysis

- 3.4.1. Import & Export Analysis, 2025

- 3.4.2. Top Importing Countries

- 3.4.3. Top Exporting Countries

- 3.5. Trump Tariff Impact Analysis

- 3.5.1. Manufacturer

- 3.5.1.1. Based on the component & Raw material

- 3.5.2. Supply Chain

- 3.5.3. End Consumer

- 3.5.1. Manufacturer

- 3.6. Raw Material Analysis

- 3.1. Global Agriculture Industry Overview, 2025

- 4. Market Overview

- 4.1. Market Dynamics

- 4.1.1. Drivers

- 4.1.1.1. Rising demand for fresh, pesticide-free produce.

- 4.1.1.2. Rapid urbanization and shrinking arable land.

- 4.1.1.3. Advancements in controlled-environment and automation technologies.

- 4.1.2. Restraints

- 4.1.2.1. High initial capital and energy-intensive operating costs.

- 4.1.2.2. Limited crop variety and technical complexity.

- 4.1.1. Drivers

- 4.2. Key Trend Analysis

- 4.3. Regulatory Framework

- 4.3.1. Key Regulations, Norms, and Subsidies, by Key Countries

- 4.3.2. Tariffs and Standards

- 4.3.3. Impact Analysis of Regulations on the Market

- 4.4. Value Chain Analysis

- 4.4.1. Raw Material Suppliers

- 4.4.2. Manufacturers

- 4.4.3. Dealers/ Distributors

- 4.4.4. End-Users/ Customers

- 4.5. Porter’s Five Forces Analysis

- 4.6. PESTEL Analysis

- 4.7. Global Vertical Farming Market Demand

- 4.7.1. Historical Market Size – Value (US$ Bn), 2020-2024

- 4.7.2. Current and Future Market Size – Value (US$ Bn), 2026–2035

- 4.7.2.1. Y-o-Y Growth Trends

- 4.7.2.2. Absolute $ Opportunity Assessment

- 4.1. Market Dynamics

- 5. Competition Landscape

- 5.1. Competition structure

- 5.1.1. Fragmented v/s consolidated

- 5.2. Company Share Analysis, 2025

- 5.2.1. Global Company Market Share

- 5.2.2. By Region

- 5.2.2.1. North America

- 5.2.2.2. Europe

- 5.2.2.3. Asia Pacific

- 5.2.2.4. Middle East

- 5.2.2.5. Africa

- 5.2.2.6. South America

- 5.3. Product Comparison Matrix

- 5.3.1. Specifications

- 5.3.2. Market Positioning

- 5.3.3. Pricing

- 5.1. Competition structure

- 6. Global Vertical Farming Market Analysis, by Component

- 6.1. Key Segment Analysis

- 6.2. Vertical Farming Market Size (Value - US$ Bn), Analysis, and Forecasts, by Component, 2021-2035

- 6.2.1. Lighting Systems

- 6.2.2. Climate Control Systems

- 6.2.3. Irrigation & Fertigation Systems

- 6.2.4. Sensors & Monitoring Systems

- 6.2.5. Software & Control Platforms

- 6.2.6. Structural Components

- 6.2.7. Others

- 7. Global Vertical Farming Market Analysis, by Growing Mechanism

- 7.1. Key Segment Analysis

- 7.2. Vertical Farming Market Size (Value - US$ Bn), Analysis, and Forecasts, by Growing Mechanism, 2021-2035

- 7.2.1. Hydroponics

- 7.2.2. Aeroponics

- 7.2.3. Aquaponics

- 7.2.4. Soil-based Systems

- 7.2.5. Hybrid Systems

- 7.2.6. Others

- 8. Global Vertical Farming Market Analysis, by Structure Type

- 8.1. Key Segment Analysis

- 8.2. Vertical Farming Market Size (Value - US$ Bn), Analysis, and Forecasts, by Structure Type, 2021-2035

- 8.2.1. Building-based Vertical Farms

- 8.2.2. Shipping Container Vertical Farms

- 8.2.3. Warehouse-based Vertical Farms

- 8.2.4. Greenhouse-integrated Vertical Farms

- 8.2.5. Others

- 9. Global Vertical Farming Market Analysis, by Crop Type

- 9.1. Key Segment Analysis

- 9.2. Vertical Farming Market Size (Value - US$ Bn), Analysis, and Forecasts, by Crop Type, 2021-2035

- 9.2.1. Leafy Greens

- 9.2.2. Herbs

- 9.2.3. Microgreens

- 9.2.4. Fruits & Vegetables

- 9.2.5. Flowers & Ornamentals

- 9.2.6. Medicinal & Aromatic Plants

- 9.2.7. Others

- 10. Global Vertical Farming Market Analysis, by Lighting Type

- 10.1. Key Segment Analysis

- 10.2. Vertical Farming Market Size (Value - US$ Bn), Analysis, and Forecasts, by Lighting Type, 2021-2035

- 10.2.1. LED Grow Lights

- 10.2.2. Fluorescent Lighting

- 10.2.3. High-Intensity Discharge (HID) Lighting

- 10.2.4. Hybrid Lighting

- 10.2.5. Others

- 11. Global Vertical Farming Market Analysis, by Growth Medium

- 11.1. Key Segment Analysis

- 11.2. Vertical Farming Market Size (Value - US$ Bn), Analysis, and Forecasts, by Growth Medium, 2021-2035

- 11.2.1. Coco Peat

- 11.2.2. Rockwool

- 11.2.3. Perlite

- 11.2.4. Vermiculite

- 11.2.5. Clay Pellets

- 11.2.6. Liquid Nutrient Solutions

- 11.2.7. Others

- 12. Global Vertical Farming Market Analysis, by Farm Size

- 12.1. Key Segment Analysis

- 12.2. Vertical Farming Market Size (Value - US$ Bn), Analysis, and Forecasts, by Farm Size, 2021-2035

- 12.2.1. Small-scale Vertical Farms

- 12.2.2. Medium-scale Vertical Farms

- 12.2.3. Large-scale Commercial Vertical Farms

- 13. Global Vertical Farming Market Analysis, by End User

- 13.1. Key Segment Analysis

- 13.2. Vertical Farming Market Size (Value - US$ Bn), Analysis, and Forecasts, by End User, 2021-2035

- 13.2.1. Commercial Growers

- 13.2.2. Restaurants & Hotels

- 13.2.3. Retail Chains & Supermarkets

- 13.2.4. Research & Educational Institutes

- 13.2.5. Residential Users

- 13.2.6. Others

- 14. Global Vertical Farming Market Analysis, by Distribution Channel

- 14.1. Key Segment Analysis

- 14.2. Vertical Farming Market Size (Value - US$ Bn), Analysis, and Forecasts, by Distribution Channel, 2021-2035

- 14.2.1. Direct Sales

- 14.2.2. Online Channels

- 14.2.3. Retail Distribution

- 15. Global Vertical Farming Market Analysis and Forecasts, by Region

- 15.1. Key Findings

- 15.2. Vertical Farming Market Size (Value - US$ Bn), Analysis, and Forecasts, by Region, 2021-2035

- 15.2.1. North America

- 15.2.2. Europe

- 15.2.3. Asia Pacific

- 15.2.4. Middle East

- 15.2.5. Africa

- 15.2.6. South America

- 16. North America Vertical Farming Market Analysis

- 16.1. Key Segment Analysis

- 16.2. Regional Snapshot

- 16.3. North America Vertical Farming Market Size (Value - US$ Bn), Analysis, and Forecasts, 2021-2035

- 16.3.1. Component

- 16.3.2. Growing Mechanism

- 16.3.3. Structure Type

- 16.3.4. Crop Type

- 16.3.5. Lighting Type

- 16.3.6. Growth Medium

- 16.3.7. Farm Size

- 16.3.8. End User

- 16.3.9. Distribution Channel

- 16.3.10. Country

- 16.3.10.1. USA

- 16.3.10.2. Canada

- 16.3.10.3. Mexico

- 16.4. USA Vertical Farming Market

- 16.4.1. Country Segmental Analysis

- 16.4.2. Component

- 16.4.3. Growing Mechanism

- 16.4.4. Structure Type

- 16.4.5. Crop Type

- 16.4.6. Lighting Type

- 16.4.7. Growth Medium

- 16.4.8. Farm Size

- 16.4.9. End User

- 16.4.10. Distribution Channel

- 16.5. Canada Vertical Farming Market

- 16.5.1. Country Segmental Analysis

- 16.5.2. Component

- 16.5.3. Growing Mechanism

- 16.5.4. Structure Type

- 16.5.5. Crop Type

- 16.5.6. Lighting Type

- 16.5.7. Growth Medium

- 16.5.8. Farm Size

- 16.5.9. End User

- 16.5.10. Distribution Channel

- 16.6. Mexico Vertical Farming Market

- 16.6.1. Country Segmental Analysis

- 16.6.2. Component

- 16.6.3. Growing Mechanism

- 16.6.4. Structure Type

- 16.6.5. Crop Type

- 16.6.6. Lighting Type

- 16.6.7. Growth Medium

- 16.6.8. Farm Size

- 16.6.9. End User

- 16.6.10. Distribution Channel

- 17. Europe Vertical Farming Market Analysis

- 17.1. Key Segment Analysis

- 17.2. Regional Snapshot

- 17.3. Europe Vertical Farming Market Size (Value - US$ Bn), Analysis, and Forecasts, 2021-2035

- 17.3.1. Component

- 17.3.2. Growing Mechanism

- 17.3.3. Structure Type

- 17.3.4. Crop Type

- 17.3.5. Lighting Type

- 17.3.6. Growth Medium

- 17.3.7. Farm Size

- 17.3.8. End User

- 17.3.9. Distribution Channel

- 17.3.10. Country

- 17.3.10.1. Germany

- 17.3.10.2. United Kingdom

- 17.3.10.3. France

- 17.3.10.4. Italy

- 17.3.10.5. Spain

- 17.3.10.6. Netherlands

- 17.3.10.7. Nordic Countries

- 17.3.10.8. Poland

- 17.3.10.9. Russia & CIS

- 17.3.10.10. Rest of Europe

- 17.4. Germany Vertical Farming Market

- 17.4.1. Country Segmental Analysis

- 17.4.2. Component

- 17.4.3. Growing Mechanism

- 17.4.4. Structure Type

- 17.4.5. Crop Type

- 17.4.6. Lighting Type

- 17.4.7. Growth Medium

- 17.4.8. Farm Size

- 17.4.9. End User

- 17.4.10. Distribution Channel

- 17.5. United Kingdom Vertical Farming Market

- 17.5.1. Country Segmental Analysis

- 17.5.2. Component

- 17.5.3. Growing Mechanism

- 17.5.4. Structure Type

- 17.5.5. Crop Type

- 17.5.6. Lighting Type

- 17.5.7. Growth Medium

- 17.5.8. Farm Size

- 17.5.9. End User

- 17.5.10. Distribution Channel

- 17.6. France Vertical Farming Market

- 17.6.1. Country Segmental Analysis

- 17.6.2. Component

- 17.6.3. Growing Mechanism

- 17.6.4. Structure Type

- 17.6.5. Crop Type

- 17.6.6. Lighting Type

- 17.6.7. Growth Medium

- 17.6.8. Farm Size

- 17.6.9. End User

- 17.6.10. Distribution Channel

- 17.7. Italy Vertical Farming Market

- 17.7.1. Country Segmental Analysis

- 17.7.2. Component

- 17.7.3. Growing Mechanism

- 17.7.4. Structure Type

- 17.7.5. Crop Type

- 17.7.6. Lighting Type

- 17.7.7. Growth Medium

- 17.7.8. Farm Size

- 17.7.9. End User

- 17.7.10. Distribution Channel

- 17.8. Spain Vertical Farming Market

- 17.8.1. Country Segmental Analysis

- 17.8.2. Component

- 17.8.3. Growing Mechanism

- 17.8.4. Structure Type

- 17.8.5. Crop Type

- 17.8.6. Lighting Type

- 17.8.7. Growth Medium

- 17.8.8. Farm Size

- 17.8.9. End User

- 17.8.10. Distribution Channel

- 17.9. Netherlands Vertical Farming Market

- 17.9.1. Country Segmental Analysis

- 17.9.2. Component

- 17.9.3. Growing Mechanism

- 17.9.4. Structure Type

- 17.9.5. Crop Type

- 17.9.6. Lighting Type

- 17.9.7. Growth Medium

- 17.9.8. Farm Size

- 17.9.9. End User

- 17.9.10. Distribution Channel

- 17.10. Nordic Countries Vertical Farming Market

- 17.10.1. Country Segmental Analysis

- 17.10.2. Component

- 17.10.3. Growing Mechanism

- 17.10.4. Structure Type

- 17.10.5. Crop Type

- 17.10.6. Lighting Type

- 17.10.7. Growth Medium

- 17.10.8. Farm Size

- 17.10.9. End User

- 17.10.10. Distribution Channel

- 17.11. Poland Vertical Farming Market

- 17.11.1. Country Segmental Analysis

- 17.11.2. Component

- 17.11.3. Growing Mechanism

- 17.11.4. Structure Type

- 17.11.5. Crop Type

- 17.11.6. Lighting Type

- 17.11.7. Growth Medium

- 17.11.8. Farm Size

- 17.11.9. End User

- 17.11.10. Distribution Channel

- 17.12. Russia & CIS Vertical Farming Market

- 17.12.1. Country Segmental Analysis

- 17.12.2. Component

- 17.12.3. Growing Mechanism

- 17.12.4. Structure Type

- 17.12.5. Crop Type

- 17.12.6. Lighting Type

- 17.12.7. Growth Medium

- 17.12.8. Farm Size

- 17.12.9. End User

- 17.12.10. Distribution Channel

- 17.13. Rest of Europe Vertical Farming Market

- 17.13.1. Country Segmental Analysis

- 17.13.2. Component

- 17.13.3. Growing Mechanism

- 17.13.4. Structure Type

- 17.13.5. Crop Type

- 17.13.6. Lighting Type

- 17.13.7. Growth Medium

- 17.13.8. Farm Size

- 17.13.9. End User

- 17.13.10. Distribution Channel

- 18. Asia Pacific Vertical Farming Market Analysis

- 18.1. Key Segment Analysis

- 18.2. Regional Snapshot

- 18.3. Asia Pacific Vertical Farming Market Size (Value - US$ Bn), Analysis, and Forecasts, 2021-2035

- 18.3.1. Component

- 18.3.2. Growing Mechanism

- 18.3.3. Structure Type

- 18.3.4. Crop Type

- 18.3.5. Lighting Type

- 18.3.6. Growth Medium

- 18.3.7. Farm Size

- 18.3.8. End User

- 18.3.9. Distribution Channel

- 18.3.10. Country

- 18.3.10.1. China

- 18.3.10.2. India

- 18.3.10.3. Japan

- 18.3.10.4. South Korea

- 18.3.10.5. Australia and New Zealand

- 18.3.10.6. Indonesia

- 18.3.10.7. Malaysia

- 18.3.10.8. Thailand

- 18.3.10.9. Vietnam

- 18.3.10.10. Rest of Asia Pacific

- 18.4. China Vertical Farming Market

- 18.4.1. Country Segmental Analysis

- 18.4.2. Component

- 18.4.3. Growing Mechanism

- 18.4.4. Structure Type

- 18.4.5. Crop Type

- 18.4.6. Lighting Type

- 18.4.7. Growth Medium

- 18.4.8. Farm Size

- 18.4.9. End User

- 18.4.10. Distribution Channel

- 18.5. India Vertical Farming Market

- 18.5.1. Country Segmental Analysis

- 18.5.2. Component

- 18.5.3. Growing Mechanism

- 18.5.4. Structure Type

- 18.5.5. Crop Type

- 18.5.6. Lighting Type

- 18.5.7. Growth Medium

- 18.5.8. Farm Size

- 18.5.9. End User

- 18.5.10. Distribution Channel

- 18.5.11. End User

- 18.6. Japan Vertical Farming Market

- 18.6.1. Country Segmental Analysis

- 18.6.2. Component

- 18.6.3. Growing Mechanism

- 18.6.4. Structure Type

- 18.6.5. Crop Type

- 18.6.6. Lighting Type

- 18.6.7. Growth Medium

- 18.6.8. Farm Size

- 18.6.9. End User

- 18.6.10. Distribution Channel

- 18.7. South Korea Vertical Farming Market

- 18.7.1. Country Segmental Analysis

- 18.7.2. Component

- 18.7.3. Growing Mechanism

- 18.7.4. Structure Type

- 18.7.5. Crop Type

- 18.7.6. Lighting Type

- 18.7.7. Growth Medium

- 18.7.8. Farm Size

- 18.7.9. End User

- 18.7.10. Distribution Channel

- 18.8. Australia and New Zealand Vertical Farming Market

- 18.8.1. Country Segmental Analysis

- 18.8.2. Component

- 18.8.3. Growing Mechanism

- 18.8.4. Structure Type

- 18.8.5. Crop Type

- 18.8.6. Lighting Type

- 18.8.7. Growth Medium

- 18.8.8. Farm Size

- 18.8.9. End User

- 18.8.10. Distribution Channel

- 18.9. Indonesia Vertical Farming Market

- 18.9.1. Country Segmental Analysis

- 18.9.2. Component

- 18.9.3. Growing Mechanism

- 18.9.4. Structure Type

- 18.9.5. Crop Type

- 18.9.6. Lighting Type

- 18.9.7. Growth Medium

- 18.9.8. Farm Size

- 18.9.9. End User

- 18.9.10. Distribution Channel

- 18.10. Malaysia Vertical Farming Market

- 18.10.1. Country Segmental Analysis

- 18.10.2. Component

- 18.10.3. Growing Mechanism

- 18.10.4. Structure Type

- 18.10.5. Crop Type

- 18.10.6. Lighting Type

- 18.10.7. Growth Medium

- 18.10.8. Farm Size

- 18.10.9. End User

- 18.10.10. Distribution Channel

- 18.11. Thailand Vertical Farming Market

- 18.11.1. Country Segmental Analysis

- 18.11.2. Component

- 18.11.3. Growing Mechanism

- 18.11.4. Structure Type

- 18.11.5. Crop Type

- 18.11.6. Lighting Type

- 18.11.7. Growth Medium

- 18.11.8. Farm Size

- 18.11.9. End User

- 18.11.10. Distribution Channel

- 18.12. Vietnam Vertical Farming Market

- 18.12.1. Country Segmental Analysis

- 18.12.2. Component

- 18.12.3. Growing Mechanism

- 18.12.4. Structure Type

- 18.12.5. Crop Type

- 18.12.6. Lighting Type

- 18.12.7. Growth Medium

- 18.12.8. Farm Size

- 18.12.9. End User

- 18.12.10. Distribution Channel

- 18.13. Rest of Asia Pacific Vertical Farming Market

- 18.13.1. Country Segmental Analysis

- 18.13.2. Component

- 18.13.3. Growing Mechanism

- 18.13.4. Structure Type

- 18.13.5. Crop Type

- 18.13.6. Lighting Type

- 18.13.7. Growth Medium

- 18.13.8. Farm Size

- 18.13.9. End User

- 18.13.10. Distribution Channel

- 19. Middle East Vertical Farming Market Analysis

- 19.1. Key Segment Analysis

- 19.2. Regional Snapshot

- 19.3. Middle East Vertical Farming Market Size (Value - US$ Bn), Analysis, and Forecasts, 2021-2035

- 19.3.1. Component

- 19.3.2. Growing Mechanism

- 19.3.3. Structure Type

- 19.3.4. Crop Type

- 19.3.5. Lighting Type

- 19.3.6. Growth Medium

- 19.3.7. Farm Size

- 19.3.8. End User

- 19.3.9. Distribution Channel

- 19.3.10. Country

- 19.3.10.1. Turkey

- 19.3.10.2. UAE

- 19.3.10.3. Saudi Arabia

- 19.3.10.4. Israel

- 19.3.10.5. Rest of Middle East

- 19.4. Turkey Vertical Farming Market

- 19.4.1. Country Segmental Analysis

- 19.4.2. Component

- 19.4.3. Growing Mechanism

- 19.4.4. Structure Type

- 19.4.5. Crop Type

- 19.4.6. Lighting Type

- 19.4.7. Growth Medium

- 19.4.8. Farm Size

- 19.4.9. End User

- 19.4.10. Distribution Channel

- 19.5. UAE Vertical Farming Market

- 19.5.1. Country Segmental Analysis

- 19.5.2. Component

- 19.5.3. Growing Mechanism

- 19.5.4. Structure Type

- 19.5.5. Crop Type

- 19.5.6. Lighting Type

- 19.5.7. Growth Medium

- 19.5.8. Farm Size

- 19.5.9. End User

- 19.5.10. Distribution Channel

- 19.6. Saudi Arabia Vertical Farming Market

- 19.6.1. Country Segmental Analysis

- 19.6.2. Component

- 19.6.3. Growing Mechanism

- 19.6.4. Structure Type

- 19.6.5. Crop Type

- 19.6.6. Lighting Type

- 19.6.7. Growth Medium

- 19.6.8. Farm Size

- 19.6.9. End User

- 19.6.10. Distribution Channel

- 19.7. Israel Vertical Farming Market

- 19.7.1. Country Segmental Analysis

- 19.7.2. Component

- 19.7.3. Growing Mechanism

- 19.7.4. Structure Type

- 19.7.5. Crop Type

- 19.7.6. Lighting Type

- 19.7.7. Growth Medium

- 19.7.8. Farm Size

- 19.7.9. End User

- 19.7.10. Distribution Channel

- 19.8. Rest of Middle East Vertical Farming Market

- 19.8.1. Country Segmental Analysis

- 19.8.2. Component

- 19.8.3. Growing Mechanism

- 19.8.4. Structure Type

- 19.8.5. Crop Type

- 19.8.6. Lighting Type

- 19.8.7. Growth Medium

- 19.8.8. Farm Size

- 19.8.9. End User

- 19.8.10. Distribution Channel

- 20. Africa Vertical Farming Market Analysis

- 20.1. Key Segment Analysis

- 20.2. Regional Snapshot

- 20.3. Africa Vertical Farming Market Size (Value - US$ Bn), Analysis, and Forecasts, 2021-2035

- 20.3.1. Component

- 20.3.2. Growing Mechanism

- 20.3.3. Structure Type

- 20.3.4. Crop Type

- 20.3.5. Lighting Type

- 20.3.6. Growth Medium

- 20.3.7. Farm Size

- 20.3.8. End User

- 20.3.9. Distribution Channel

- 20.3.10. Country

- 20.3.10.1. South Africa

- 20.3.10.2. Egypt

- 20.3.10.3. Nigeria

- 20.3.10.4. Algeria

- 20.3.10.5. Rest of Africa

- 20.4. South Africa Vertical Farming Market

- 20.4.1. Country Segmental Analysis

- 20.4.2. Component

- 20.4.3. Growing Mechanism

- 20.4.4. Structure Type

- 20.4.5. Crop Type

- 20.4.6. Lighting Type

- 20.4.7. Growth Medium

- 20.4.8. Farm Size

- 20.4.9. End User

- 20.4.10. Distribution Channel

- 20.5. Egypt Vertical Farming Market

- 20.5.1. Country Segmental Analysis

- 20.5.2. Component

- 20.5.3. Growing Mechanism

- 20.5.4. Structure Type

- 20.5.5. Crop Type

- 20.5.6. Lighting Type

- 20.5.7. Growth Medium

- 20.5.8. Farm Size

- 20.5.9. End User

- 20.5.10. Distribution Channel

- 20.6. Nigeria Vertical Farming Market

- 20.6.1. Country Segmental Analysis

- 20.6.2. Component

- 20.6.3. Growing Mechanism

- 20.6.4. Structure Type

- 20.6.5. Crop Type

- 20.6.6. Lighting Type

- 20.6.7. Growth Medium

- 20.6.8. Farm Size

- 20.6.9. End User

- 20.6.10. Distribution Channel

- 20.7. Algeria Vertical Farming Market

- 20.7.1. Country Segmental Analysis

- 20.7.2. Component

- 20.7.3. Growing Mechanism

- 20.7.4. Structure Type

- 20.7.5. Crop Type

- 20.7.6. Lighting Type

- 20.7.7. Growth Medium

- 20.7.8. Farm Size

- 20.7.9. End User

- 20.7.10. Distribution Channel

- 20.8. Rest of Africa Vertical Farming Market

- 20.8.1. Country Segmental Analysis

- 20.8.2. Component

- 20.8.3. Growing Mechanism

- 20.8.4. Structure Type

- 20.8.5. Crop Type

- 20.8.6. Lighting Type

- 20.8.7. Growth Medium

- 20.8.8. Farm Size

- 20.8.9. End User

- 20.8.10. Distribution Channel

- 21. South America Vertical Farming Market Analysis

- 21.1. Key Segment Analysis

- 21.2. Regional Snapshot

- 21.3. South America Vertical Farming Market Size (Value - US$ Bn), Analysis, and Forecasts, 2021-2035

- 21.3.1. Component

- 21.3.2. Growing Mechanism

- 21.3.3. Structure Type

- 21.3.4. Crop Type

- 21.3.5. Lighting Type

- 21.3.6. Growth Medium

- 21.3.7. Farm Size

- 21.3.8. End User

- 21.3.9. Distribution Channel

- 21.3.10. Country

- 21.3.10.1. Brazil

- 21.3.10.2. Argentina

- 21.3.10.3. Rest of South America

- 21.4. Brazil Vertical Farming Market

- 21.4.1. Country Segmental Analysis

- 21.4.2. Component

- 21.4.3. Growing Mechanism

- 21.4.4. Structure Type

- 21.4.5. Crop Type

- 21.4.6. Lighting Type

- 21.4.7. Growth Medium

- 21.4.8. Farm Size

- 21.4.9. End User

- 21.4.10. Distribution Channel

- 21.5. Argentina Vertical Farming Market

- 21.5.1. Country Segmental Analysis

- 21.5.2. Component

- 21.5.3. Growing Mechanism

- 21.5.4. Structure Type

- 21.5.5. Crop Type

- 21.5.6. Lighting Type

- 21.5.7. Growth Medium

- 21.5.8. Farm Size

- 21.5.9. End User

- 21.5.10. Distribution Channel

- 21.6. Rest of South America Vertical Farming Market

- 21.6.1. Country Segmental Analysis

- 21.6.2. Component

- 21.6.3. Growing Mechanism

- 21.6.4. Structure Type

- 21.6.5. Crop Type

- 21.6.6. Lighting Type

- 21.6.7. Growth Medium

- 21.6.8. Farm Size

- 21.6.9. End User

- 21.6.10. Distribution Channel

- 22. Key Players/ Company Profile

- 22.1. AeroFarms.

- 22.1.1. Company Details/ Overview

- 22.1.2. Company Financials

- 22.1.3. Key Customers and Competitors

- 22.1.4. Business/ Industry Portfolio

- 22.1.5. Product Portfolio/ Specification Details

- 22.1.6. Pricing Data

- 22.1.7. Strategic Overview

- 22.1.8. Recent Developments

- 22.2. AppHarvest

- 22.3. Bowery Farming

- 22.4. Crop One Holdings

- 22.5. Eden Green Technology

- 22.6. Freight Farms

- 22.7. Gotham Greens

- 22.8. Green Sense Farms

- 22.9. Heliospectra AB

- 22.10. iFarm

- 22.11. Intelligent Growth Solutions (IGS)

- 22.12. Jones Food Company

- 22.13. Kalera

- 22.14. Oishii

- 22.15. Plenty Unlimited

- 22.16. Pure Harvest Smart Farms

- 22.17. Signify Holding

- 22.18. Stacked Farm

- 22.19. Urban Crop Solutions

- 22.20. Vertical Harvest

- 22.21. Other Key Players

- 22.1. AeroFarms.

Note* - This is just tentative list of players. While providing the report, we will cover more number of players based on their revenue and share for each geography

Research Design

Our research design integrates both demand-side and supply-side analysis through a balanced combination of primary and secondary research methodologies. By utilizing both bottom-up and top-down approaches alongside rigorous data triangulation methods, we deliver robust market intelligence that supports strategic decision-making.

MarketGenics' comprehensive research design framework ensures the delivery of accurate, reliable, and actionable market intelligence. Through the integration of multiple research approaches, rigorous validation processes, and expert analysis, we provide our clients with the insights needed to make informed strategic decisions and capitalize on market opportunities.

MarketGenics leverages a dedicated industry panel of experts and a comprehensive suite of paid databases to effectively collect, consolidate, and analyze market intelligence.

Our approach has consistently proven to be reliable and effective in generating accurate market insights, identifying key industry trends, and uncovering emerging business opportunities.

Through both primary and secondary research, we capture and analyze critical company-level data such as manufacturing footprints, including technical centers, R&D facilities, sales offices, and headquarters.

Our expert panel further enhances our ability to estimate market size for specific brands based on validated field-level intelligence.

Our data mining techniques incorporate both parametric and non-parametric methods, allowing for structured data collection, sorting, processing, and cleaning.

Demand projections are derived from large-scale data sets analyzed through proprietary algorithms, culminating in robust and reliable market sizing.

Research Approach

The bottom-up approach builds market estimates by starting with the smallest addressable market units and systematically aggregating them to create comprehensive market size projections.

This method begins with specific, granular data points and builds upward to create the complete market landscape.

Customer Analysis → Segmental Analysis → Geographical Analysis

The top-down approach starts with the broadest possible market data and systematically narrows it down through a series of filters and assumptions to arrive at specific market segments or opportunities.

This method begins with the big picture and works downward to increasingly specific market slices.

TAM → SAM → SOM

Research Methods

Desk / Secondary Research

While analysing the market, we extensively study secondary sources, directories, and databases to identify and collect information useful for this technical, market-oriented, and commercial report. Secondary sources that we utilize are not only the public sources, but it is a combination of Open Source, Associations, Paid Databases, MG Repository & Knowledgebase, and others.

- Company websites, annual reports, financial reports, broker reports, and investor presentations

- National government documents, statistical databases and reports

- News articles, press releases and web-casts specific to the companies operating in the market, Magazines, reports, and others

- We gather information from commercial data sources for deriving company specific data such as segmental revenue, share for geography, product revenue, and others

- Internal and external proprietary databases (industry-specific), relevant patent, and regulatory databases

- Governing Bodies, Government Organizations

- Relevant Authorities, Country-specific Associations for Industries

We also employ the model mapping approach to estimate the product level market data through the players' product portfolio

Primary Research

Primary research/ interviews is vital in analyzing the market. Most of the cases involves paid primary interviews. Primary sources include primary interviews through e-mail interactions, telephonic interviews, surveys as well as face-to-face interviews with the different stakeholders across the value chain including several industry experts.

| Type of Respondents | Number of Primaries |

|---|---|

| Tier 2/3 Suppliers | ~20 |

| Tier 1 Suppliers | ~25 |

| End-users | ~25 |

| Industry Expert/ Panel/ Consultant | ~30 |

| Total | ~100 |

MG Knowledgebase

• Repository of industry blog, newsletter and case studies

• Online platform covering detailed market reports, and company profiles

Forecasting Factors and Models

Forecasting Factors

- Historical Trends – Past market patterns, cycles, and major events that shaped how markets behave over time. Understanding past trends helps predict future behavior.

- Industry Factors – Specific characteristics of the industry like structure, regulations, and innovation cycles that affect market dynamics.

- Macroeconomic Factors – Economic conditions like GDP growth, inflation, and employment rates that affect how much money people have to spend.

- Demographic Factors – Population characteristics like age, income, and location that determine who can buy your product.

- Technology Factors – How quickly people adopt new technology and how much technology infrastructure exists.

- Regulatory Factors – Government rules, laws, and policies that can help or restrict market growth.

- Competitive Factors – Analyzing competition structure such as degree of competition and bargaining power of buyers and suppliers.

Forecasting Models / Techniques

Multiple Regression Analysis

- Identify and quantify factors that drive market changes

- Statistical modeling to establish relationships between market drivers and outcomes

Time Series Analysis – Seasonal Patterns

- Understand regular cyclical patterns in market demand

- Advanced statistical techniques to separate trend, seasonal, and irregular components

Time Series Analysis – Trend Analysis

- Identify underlying market growth patterns and momentum

- Statistical analysis of historical data to project future trends

Expert Opinion – Expert Interviews

- Gather deep industry insights and contextual understanding

- In-depth interviews with key industry stakeholders

Multi-Scenario Development

- Prepare for uncertainty by modeling different possible futures

- Creating optimistic, pessimistic, and most likely scenarios

Time Series Analysis – Moving Averages

- Sophisticated forecasting for complex time series data

- Auto-regressive integrated moving average models with seasonal components

Econometric Models

- Apply economic theory to market forecasting

- Sophisticated economic models that account for market interactions

Expert Opinion – Delphi Method

- Harness collective wisdom of industry experts

- Structured, multi-round expert consultation process

Monte Carlo Simulation

- Quantify uncertainty and probability distributions

- Thousands of simulations with varying input parameters

Research Analysis

Our research framework is built upon the fundamental principle of validating market intelligence from both demand and supply perspectives. This dual-sided approach ensures comprehensive market understanding and reduces the risk of single-source bias.

Demand-Side Analysis: We understand end-user/application behavior, preferences, and market needs along with the penetration of the product for specific application.

Supply-Side Analysis: We estimate overall market revenue, analyze the segmental share along with industry capacity, competitive landscape, and market structure.

Validation & Evaluation

Data triangulation is a validation technique that uses multiple methods, sources, or perspectives to examine the same research question, thereby increasing the credibility and reliability of research findings. In market research, triangulation serves as a quality assurance mechanism that helps identify and minimize bias, validate assumptions, and ensure accuracy in market estimates.

- Data Source Triangulation – Using multiple data sources to examine the same phenomenon

- Methodological Triangulation – Using multiple research methods to study the same research question

- Investigator Triangulation – Using multiple researchers or analysts to examine the same data

- Theoretical Triangulation – Using multiple theoretical perspectives to interpret the same data

Custom Market Research Services

We will customise the research for you, in case the report listed above does not meet your requirements.

Get 10% Free Customisation